equity valuation project monday, december 6, 2004mmoore.ba.ttu.edu/valuationreports/coke.pdf ·...

TRANSCRIPT

Equity Valuation Project Monday, December 6, 2004

Finance 3321-002

Group 22

Katie Lewandowski Mike Phillips

Lee Hennington Jason Richardson Matthew Nasche

Table of Contents

I. Executive Summary 3

II. Business and Industry Overview 4

a. Business Overview 4

b. Industry Analysis 5

c. Strengths 6

d. Weaknesses 7

e. Opportunities 7

f. Threats 8

g. Rivalry Among Existing Firms 8

h. Threat of New Entrants 9

i. Threat of Substitute Products 9

j. Bargaining Power of Buyers 10

k. Bargaining Power of Suppliers 11

l. Key Success Factors 11

III. Accounting Analysis 13

a. Sales manipulation Diagnostics 13

b. Core Expense Manipulation Diagnostics 14

c. Key Accounting Policies 15

d. Accounting Flexibility 15

e. Accounting Strategy 16

f. Quality of Disclosure 17

g. Potential Red Flags 18

IV. Ratio Analysis and Forecasting 19

a. Forecast 19

b. Liquidity 22

c. Profitability 25

d. Capital Structure 27

e. Z-Score 29

V. Valuation 31

a. Cost of Equity 31

b. Cost of Debt 32

c. Weighted Average Cost of Capital 32

d. Method of Comparables 33

e. Abnormal Earnings Growth Valuation 33

f. Discounted Dividends Valuation 34

g. Free Cash Flows Valuation 35

h. Residual Income Valuation 36

i. Long Run Residual Income 37

VI. Appendices 38

a. Discounted Dividends Model Sensitivity Analysis 38

b. Free Cash Flows Model Sensitivity Analysis 38

c. Abnormal Earnings Growth Sensitivity Analysis 39

d. Residual Income Sensitivity Analysis 39

e. Long Run Residual Income Sensitivity Analysis 40

f. Discounted Dividends Valuation 41

g. Free Cash Flows Valuation 41

h. Residual Income Valuation 42

i. Method of Comparables Valuation 42

j. Abnormal Earnings Growth Valuation Model 43

k. Income Statement 44

l. Cash Flow Statement 45

m. Balance Sheet 46

n. Ratio Analysis List 47

VII. References 48

1

KO – NYSE (11/11/2004) $40.96 52 Week Range $38.30-$53.50 Revenue (FY 2004) $20,668,000,000 Market Capitalization $98.5 Billion Shares Outstanding 2.4 Billion Dividend Yield 2.47% Avg Daily Trading Volume 8.6 Million Book Value per Share $6.189 Return on Equity 31.65% Return on Assets 15.98%

EPS Forecast FYE 2002A 2003A 2004E 2005E 2006E EPS $7.83 $8.77 $8.61 $8.68 $8.74 Key Ratios Firm Industry Average Forward P/E $19.82 $21.18 Forward P/B $3.28 $5.01 Valuation Predictions Actual Current Price $40.96 (November 11, 2004) P/E Valuation $39.73 M/B Valuation $40.97 AEG Valuation $31.92 DCF Valuation $38.32

Investment Recommendation: BUY November 1, 2004

Analysis of

2

Executive Summary

Begun in an Atlanta residency, Coca-Cola has become one of the largest

manufacturers of soda in the world. They are currently a nationally recognized brand

name. Over the years, the company and their product have continually evolved to adapt

to the changing interests of the public. Coca-Cola’s competition includes PepsiCo and

Cadbury Schweppes. PepsiCo has proven to pose the greatest threat by picking up some

of Coca-Cola’s lagging market share this year.

In order for Coca-Cola to continue to thrive in the market there are three key

value drivers that must be addressed: profitable growth, cost management and efficient

capital structure. In order to remain profitable marketing and innovation are important

aspects for the company to focus on. Cost management focus is directed towards

lowering supply chain costs especially in foreign markets. Coca-Cola is already efficient

in that they have a strong competitive advantage but they hope to improve by decreasing

general and administrative costs in the future. Their largest weakness is their failure to

follow their competition’s lead in the non-beverage market where PepsiCo has gained

profit and market share.

Pepsi and Coke share much of the world market at 31.8% and 44% respectively.

Each brand tries to differentiate itself to gain and maintain loyal customers. Because

Coca-Cola only has two main competitors, price premiums are not a main focus of the

company. They instead focus on marketing, innovation and name brand image.

In order to analyze Coca-Cola, PepsiCo, and Cadbury Schweppes were used as

benchmarks for where the company stands in the industry. In looking at the firm’s past

performance in terms of liquidity, profitability and capital structure it was evident that

Coca-Cola is stronger than the industry. Coca-Cola’s liquidity was poor for the past five

years but held its own relative to the industry. The profitability of Coca-Cola outweighed

its competition while its measure of efficiency is currently far less than PepsiCo. Overall

the capital structure is well balanced. There have been many changes in the industry over

the past five years including the effects of September 11 and Coca-Cola appointing a new

CEO. After the initial adjustment period, the firm should be able to continue to improve

to more stable liquidity and increased stability.

3

Once the past reports were analyzed we were able to forecast the financial

statements for the next ten years. While sorting through financial statements it became

evident that the publicly available information was muddled and very condensed. The

difficulty ensued while trying to sort through the financial statements and raised

questions concerning the companies withholding of information. If they do not make

information easily accessible to the public we question whether they are trying to hide

certain valuable information. None the less, we were able to make assumptions and

derive the balance sheet from the forecasted income statement and the cash flows from

each of the aforementioned statements.

With the forecasted information, we were able to calculate a value for the firm

using the residual income method, the method of comparables, the abnormal earnings

growth method, the discounted dividends model and the free cash flow method. This was

done using the CAPM and the weighted average cost of capital each of which were

figured using a calculated beta and a published beta. After valuing the company using

each of the methods and comparing it to the price per share that Coca-Cola currently

trades for on the stock market, we felt that the price per share is currently understated

assuming that no more than 2% growth was attainable which we felt was fairly low

compared to past and potential growth. Coca-Cola’s stocks should be bought at this time.

4

Business and Industry Overview

Business Overview

Coca-cola has been around since 1886 when Dr. John Pemberton invented the

patented formula. In the beginning, the Atlanta pharmacist sold approximately nine

glasses of coca-cola a day for five cents per glass. Although he had a brilliant invention,

Pemberton lacked in marketing skills and soon sold the company for $2300 to Asa Griggs

Candler, who would become the company’s first president. Candler, whose vision was

much broader than Pemberton’s, had plants in Chicago, Dallas, and Los Angeles by

1895. Candler’s vision did not however run as far as bottling the popular drink and he

sold the bottling rights to two Chattanooga lawyers named Benjamin F. Thomas and

Joseph B. Whitehead for $1.

Early on, Coca-cola felt the pressure from their competition. In order to combat

the competition, they tried push their originality and produced their trademark contour

bottle (seen below) in 1915 which they pointed out could be recognized in the dark.

Their advertising ran towards slogans such as “Demand the genuine” and “accept no

substitute.” (2) Through it all, the Coca-Cola Company continued to grow. Between 1900

and 1920, they grew from two bottlers to 1,000, and in 1919, they came up with the

innovative 6-pack which made the product more mobile. In 1941 during WWII the

mobility increased when Woodruff, the president of their company, promised troops 5-

cent cokes wherever in the world they were which helped jump-start the foreign market.

In 1961, their growth continued when they introduced the new product Sprite.

Soon new flavors such as TAB and Fresca followed. Then in 1985 they released a new

Coca-Cola taste. This was the first change in formation in 99 years. While taste testers

loved it, the new Coca-Cola did not catch on with the public. The original formula was

returned under the name of Coca-Cola Classic. Today you can find over 20 flavors of

5

carbonated beverages as well as bottled water and juices all produced by the Coca-Cola

Company.

The Coca-Cola Company has been involved with the Olympic games almost from

the beginning. In the 90’s the market grew with endorsements in the FIFA World Cup

Football, Rugby World Cup and the National Basketball Association as well as becoming

the Official Soft Drink of NASCAR racing. In 1993 their advertising introduced

“Always Coca-Cola” and the adorable Coca-Cola polar bear as well as endorsing new

beverages including Powerade sports drink and Dasani bottled water. In 1997 $1 billion

servings of Coca-Cola beverages were sold daily, a big step from nine glasses per day.

Today, “The Coca-Cola Company is the largest manufacturer, distributor and marketer of

nonalcoholic beverage concentrates and syrups in the world.” Coca-Cola products are

now among the leading products in most of the more than 200 countries where they are

sold. (2)

Industry Analysis

The carbonated soft drink industry has been expanding steadily for many years,

but has begun to slow recently. As a result of this slow market growth, competition to

create new products and expand in to new markets has become fierce. Various

acquisitions and mergers have led to the industry being dominated by three giants who

together hold over 90% of the market (3), Coca-Cola, Pepsi, and Cadbury Schweppes.

Pepsi is by far Coca-

Cola’s largest competitor.

They have found great

success by expanding in to

the snack market, selling all

kinds of sweet and salty

snacks under its Frito Lay

brand. Coca-Cola has

Carbonated Soft Drink Sales VolumeAccording to Beverage-Digest.com

880090009200940096009800

100001020010400

1996

1997

1998

1999

2000

2001

2002

2003

In Millions ofCases

6

neglected this market, which could be one of the reasons that while Coke’s sales have

been slumping lately, Pepsi has shown net sales increases and has been picking up

valuable market share dropped by Coke this year.

Cadbury Schweppes boasts such brands as Dr. Pepper, 7up, A&W, Country Time,

and Hawaiian Punch. While this smaller company is not a great force in the industry as of

yet, it seems to have done well in recent years, showing revenues just under 12 billion

last year (3). If Cadbury Schweppes continues to grow in to new international markets, it

could pose a threat to Coca-Cola.

Strengths

Coca-Cola believes that in order to achieve effective execution within their

company, focus needs to be aimed towards three key value drivers: profitable growth;

cost management; and efficient capital structure. In attaining profitable growth, Coca-

Cola continues to broaden its family of brands across markets, with support from

marketing and innovation. One thing that the company is trying to do to manage

expansion and growth is to shift their attention from a “volume only” focus to a “volume

and value” focus. This strategy helps to put more of an emphasis on gross profit and

profit before taxes instead of emphasis only on volume.

In order to satisfy cost management, Coca-Cola continues to emphasize supply

chain initiatives. System economics can be improved by lowering supply chain costs.

Over the past year, Coca-Cola has established supply chain management companies in

North America, Japan, and China to increase procurement efficiencies and to centralize

production and logistics operations.

Coca-Cola maintains an efficient capital structure intended to optimize their cost

of capital. The company believes that they are provided a competitive advantage through

access to key financial markets, ability to raise funds at a low cost, and low cost of

borrowing. Over time, Coca-Cola wishes to reduce cost by decreasing general and

administrative costs as a percentage of net operating revenues. (5)

7

Weaknesses

One particular weakness for Coca-Cola Company includes the lack of non-

beverage products. Many of their competitors compete in both the food and beverage

industry. Coca-Cola, accordingly, suffers a miss on potential earnings in this area. Other

weaknesses of this company include the high level of competition and power of

consumers. Coca-Cola is constantly competing with PepsiCo for the number one

beverage in the nation. They must always keep the demand of consumers in mind since

consumers ultimately determine the company’s prosperity. Also, it is important to notice

that while Coca-Cola has suppliers and bottlers in many countries, they only own a

majority of them. By not owning all of these companies, they lose a small portion of

profit that they must give to the owners of the companies. (1)

Opportunities

The Coca-Cola Company is very active in developing new and innovative

products to satisfy the ever changing desires of its customers. In fulfilling these needs,

there are always new ways to improve current product lines and make use of new

technologies. Recently, The Coca-Cola Company has come out with several new

products which follow the current trend of Americans being very carbohydrate

conscience in what they consume. Products such as the new Coke C2, (released July

2004) (2) are becoming very popular here in the United States. This product is unique in

that it filled a consumer need that was previously unsatisfied. There seems to be no

reason why this same type of product could not be carried over into the company’s other

product lines such as the Vanilla and Cherry Coke flavors. The Coca-Cola Company also

recently released PowerAde Flava23, which became the first sports drink flavor created

by a superstar athlete (2). This can possibly open the door to an entire line of superstar

affiliated flavors. The Coca-Cola Company has also embraced the epidemic of obesity in

America by helping get the message out to exercise more through their website, which

provides useful information on health issues and leading an active lifestyle. Coca-Cola,

like its competitor PepsiCo, has aligned itself with certain fast food chains such as

8

McDonalds and Wendy’s as their supplier of fountain beverages. This sector of the soft

drink industry appears to be the one with the most potential for new growth, as

companies can be convinced to switch suppliers through incentive-filled contracts.

Threats

The main threat in the industry is that of new substitute products and mergers.

The one company that has the capacity to do this is their main competitor in PepsiCo,

which rivals Coca-Cola in many aspects of the industry. PepsiCo is trying to become

known as the product that is more in touch with the different groups that consume its

products. This can be seen with the recent release of products such as Pepsi Edge, which

is in direct competition to Coke C2, and the already established Mountain Dew and

Mountain Dew Code Red, which are targeted at the extreme sports trend sweeping

America. There is also not too much of a threat of competition in the marketplace, since

both companies know that an all out price war would likely be disastrous to everyone

involved. New regulations are also not very likely, as this is a stable industry and has

been for many years. (1)

Rivalry Among Existing Firms

Coca-Cola, the

current worldwide market

leader, holds 44% of the total

market share. In close second

is Pepsi with 31.8% and in

third is Cadbury Schweppes

(Dr. Pepper, 7up) at 14.3%.

Since so few firms control

the market, they have successfully been able to work together and avoid harmful price

competition. However, because there is little or no switching cost to consumers, soft

drink companies have worked very hard to differentiate their products and create brand

Carbonated Soft Drink Market Share 2003According to Beverage-Digest.com

Coca-Cola Co.Pepsi-Cola Co.Cadbury SchweppesCott Corp.Private Label \ Other

9

awareness with consumers. They have also expanded into non-carbonated drinks and

experimented with new flavors.

Each company has had success with their diet brands, varied success with

flavored sodas (Cherry Coke, Vanilla Coke, Pepsi Twist), and most recently

disappointing results from their low carb brands (C2, Pepsi Edge). Pepsi has had great

success with its Gatorade brand which accounts for 73% of the sports drink market.

When combined with their Lipton and Tropicana brands, they are number one in the non-

carbonated beverage area and cokes biggest threat. Coke is also competing in these areas

with its Powerade, Minute Maid, and Nestea brands while Cadbury Schweppes has

recently purchased Snapple. The fastest growing segment right now is the 10 billion

dollar a year bottled water market, which Coca-Cola has moved in to with its Dasani

brand. (3)

Threat of New Entrants

There is little threat to Coca-Cola from new entrants. Any start up company

would require an enormous amount of capital to try and match the large beverage

companies’ advertising expenditures and efficient distribution. Even if a company could

raise enough capital they would find themselves at a serious cost disadvantage to the big

three. In the past, Coca-Cola and Pepsi have purchased most soft drink companies that

have shown potential for growth, effectively eliminating potential threats.

Threat of Substitute Products

In any industry, one of the big competitive threats is that of new products being

introduced into the market that could substitute for the original product that the company

offers. Some of the key factors with substitute products include relative price and

performance and a buyer’s willingness to switch products. One new phenomenon that

has recently caused a challenge in the substitution category is the Atkins diet craze. The

diet promotes losing weight by cutting carbohydrates among other things. This poses a

10

dilemma for the Coca-Cola team in that their predominate beverages are high in fructose

and contain many “bad carbs”. To combat this threat, Coca-Cola has begun producing

and selling a new substitute of their own. The new product, C2, has lower sugar content

and lower carbohydrate count then the original Coca-Cola. It is interesting to consider

that the Coca-Cola Company actually competes with itself by providing substitutions for

many of its original beverages.

There are many other substitute products currently on the market. The

nonalcoholic beverage industry is highly competitive with competitive products including

carbonates, packaged water, juices and nectars, fruit drinks, sports and energy drinks,

coffee and tea. Each of these substitute products are produced to perform the same

function of giving the customer an enjoyable tasting beverage while satisfying the

customer’s thirst. Their largest competitor, PepsiCo, sells a similar product for a

comparable price. These two companies together are able to offer a price premium when

compared to generic brands of similar beverage products because of their name brand

power. Coca-Cola is recognized worldwide thanks to their marketing and advertising

efforts. However, when you compare Coca-Cola to PepsiCo, the products, competition,

and name power are very similar. While most customers of Coca-Cola have a preference

due to the different tastes, these customers may be willing to switch products if there was

a sizable price difference between Coca-Cola and PepsiCo. So although Coca-Cola is the

largest selling non-alcoholic beverage, it has fierce enough competition from substitute

products to be a factor in pricing and continued effort to be innovative and provide the

quality that customers have come to expect.

Bargaining Power of Buyers

Coca-Cola is the industry leader in the nonalcoholic beverage market. Due to the

large size of orders and the ease in which coke can switch to another supplier for its raw

materials, Coca-Cola has a considerable amount of buying power. Buyers are more cost

conscious when the products they buy are undifferentiated. This would be the case with

Coca-Cola when buying raw materials. They will buy from the supplier with the lowest

11

price. If the company wants a lower price than they are offered, they can bargain for a

better price. The supplier may give them a better deal than they would for a smaller

company. The supplier will have to consider its opportunity cost, the cost of not doing

business with Coca-Cola.

Bargaining Power of Suppliers

Because of the large number of bottlers relative to soft drink companies, Coca-

Cola as a supplier has significant power over the bottlers. Three major competitors, Coca-

Cola, Pepsi, and Cadbury Schweppes, control the nonalcoholic beverage market. Since

there are only a few companies the bottlers can buy from, the soft drink companies have

the power. Coca-Cola supplies directly to some restaurants and other businesses. They

have some power over these customers because they generally have contracts they would

have to break to switch products.

Key Success Factors

Overall the soft drink industry strategy is one of differentiation instead of cost

leadership. This means soft drink companies must spend millions of dollars a year to

build brand awareness through advertising. The ability to successfully market a soft drink

is the main key success factors in the industry

The ability to generate a recognizable brand is something Coke has been able to

do very effectively. Theirs is one of the most widely recognized brands, worldwide in any

industry. This is why they are the number one soft drink company in the world. Another

key success factor in the soft drink is the ability to produce new brands and flavors that

taste good and are accepted by the public. This is one area where Coke has occasionally

stumbled. “New Coke” and C2 were rejected by consumers and resulted in a loss for the

company.

12

In conclusion, the Coca-Cola Company exists to benefit and satisfy everyone that

its products come into contact with. The company makes large marketing expenditures in

areas such as advertising, sponsorship, and promotion in support of its brands. These

costs are extended to increase brand awareness and consumer preference to promote

long-term growth and obtain a healthy share of worldwide nonalcoholic beverage shares.

Coca-Cola continues to keep its focus on quality in the marketplace, a strong working

environment, and most importantly value to its consumers. It is upon this focus and

foundation that Coca-Cola has retained its position as one of the most recognized and

successful companies around the world.

13

Accounting Analysis

Sales Manipulation Diagnostics

To assess the quality of Coca-Cola’s financial disclosures with respect to sales,

we have figured three diagnostic ratios. The first is the Net Sales / Cash From Sales. This

ratio shows how much cash was recorded in relation to total sales. Ideally a company

would want this number to equal one. This would mean that all sales were paid for

entirely in cash, and no need to account for bad debt. Coca-Cola’s Net Sales / Cash From

Sales ratio has gone down steadily from 5.706 in 2000 to 3.857 in 2003. This is a positive

trend for Coca-Cola.

The second diagnostic ration we did for Coca-Cola was Net Sales / Net Accounts

Receivable. This ratio shows how much of Coca-Cola’s sales where on account. A high

number here means fewer bad debts and more money in our pockets now. Logic would

suggest that the higher the percentage of sales paid for in cash, the less the percentage of

sales would go in to accounts receivable. It is for this reason that we found it strange that

according to the results of our diagnostic ratios, Coke is showing an increase in cash from

sales and sales on account in relation to net sales. We see this as a potential red flag

marking possible manipulations in accounts receivable.

The third ratio we performed was the Net Sales / Inventory Ratio. This ratio

shows how much inventory a company is holding in relation to net sales. The higher the

number the less inventory a company is holding which indicates efficiency. This number

seems to be decreasing for Coca-Cola which could indicate problems. Growing

inventories can be a sign of over anticipated sales.

14

Sales Manipulation Diagnostics

0.000

5.000

10.000

15.000

20.000

25.000

1999 2000 2001 2002 2003

Net Sales / Cash FromSalesNet Sales / NetAccounts RecievableNet Sales / Inventory

Core Expense Manipulation Diagnostics

To look for possible manipulations to Coca-Cola’s reported expenses, we have

performed three diagnostic ratios. They are Declining Asset Turnover ratio

(Sales/Assets), Cash Flow From

Operating Activities/Operating

Income, and Pension Expense over

SG&A. The Declining Asset

Turnover shows how assets are

growing in relation to sales. Over

the last five years, Coca-Cola’s Declining Asset Turnover has decreased steadily meaning

that their assets are growing more rapidly than their sales are increasing. This could

represent slowing sales or large asset acquisitions, but doesn’t seem to be indicative of

any accounting manipulations.

The second diagnostic test we performed was CFFO/OI. The numbers from this

calculation show that each year,

CFFO/OI is about one. This is

generally where a company would

want this ratio since these numbers

indicate that its operating income

is mostly cash and not credit.

The third diagnostic we

performed was Pension Expense / SG&A. This ratio shows what percentage of SG&A is

pension expense. Coca-Cola’s

pension expense was .7% in 2001

and rose steadily to 1.5% in 2003.

According to the Coca-Cola web

site, pension expense is on the rise

due to unforeseen lay-offs as a

15

result of company wide streamlining and restructuring. They estimate that this trend will

continue through 2004. Over all we don’t see any reasons to suspect expense

manipulations in the results of our diagnostics.

Key Accounting Policies

The Coca-Company is a manufacturing company that relies heavily upon

trademarks, goodwill, and research and development which helps to keep the company

innovative and above the competition in terms of sales. Therefore their key accounting

policies will be most readily descriptive in these key areas. By examining how the

company accounts for these things, we are able to best analyze their accounting strategy

and find where distortions and problems may occur. “[Their] financial statements are

prepared in accordance with accounting principles generally accepted in the United

States,” as reported in their annual 10-K reports. They amortize trademarks over their

useful lives. Those trademarks or goodwill without definite lives are not amortized and

are reevaluated annually for impairment. Another area of importance to the finances of

the Coca-Cola Company includes investments in other companies, many of which are

bottling companies. In the companies that they have considerable control over, they use

the equity method. In those companies that Coca-Cola does not control, they use the cost

method. Some of the policies which Coca-Cola reports includes, “advancing payments to

fund future marketing activities.”

Accounting Flexibility

There are areas in which the Coca-Cola Company has flexibility and control over

reporting. Some of these areas of flexibility are inherent based on their tendency to

change with the market such as fair market value. Coca-Cola must decide whether to

“write-down” an asset when it’s fair value drops below its carrying value. Estimates are

required in many areas including company holdings which are not traded publicly. For

these assets, they are required to determine fair value “based on valuation methodologies

including discounted cash flows, estimates of sales proceeds and external appraisals, as

16

appropriate.” Pension funds are another area of reporting flexibility. Pension liabilities

are estimated and reported as long term liabilities. They are expensed over each year. The

amount that is expensed is based on estimates. These estimates include how long a person

will live after they retire, when an employee will retire and how much they get paid when

they retire. If these estimates are not correct they can cause problems. Low estimates will

overstate net income because the pension expense will be lower than it should be. A low

pension expense will reduce the over all expenses and cause net income to appear higher

than it should be. Over stating the pension expense will result in a lower net income. If

the pension expense is over stated it will increase the total expenses this will make net

income lower than it should be. If net income is understated the taxable income is less

than it should be.

Accounting Strategy

The accounting policies used by Coca-Cola are very comparable to Pepsico, a

similar firm. Their amortization of goodwill and trademarks are based on estimates. One

key in comparing the companies is that they each estimate pension funds in the same

manner. In considering the two companies and their accounting policies, it is important

to note that there is little room for distortions due to the fact that they are so similarly

reported. Therefore, we can conclude that unless both companies are distorting

information unilaterally, Coca-Cola is not manipulating their numbers in these areas of

estimation.

Another key issue to report is that Coca-Cola has changed many of its policies

over the last few years. According to the auditing letter from Ernst & Young, Coca-Cola

changed it’s method of accounting and goodwill along with other intangible assets and

stock-based compensation in 2002. In 2001, there were changes made in their derivative

instruments and hedging activities. Ernst & Young went on to say that these changes

were acceptable in keeping Coca-Cola within industry standards.

In the past, Coca-Cola has been realistic in their estimates and policies in most

areas. They have recently had to increase their pension expenses by $48 million due to

underestimations. We do not feel that this was to overstate assets at any time it is just a

17

result of streamlining and restructuring which resulted in early pension payments to many

employees that they had to let go. This incurs longer pension payments and therefore

greater amounts of money.

One accounting strategy that Coca-Cola uses is hedging and derivatives. These

strategies are not used to distort information and are checked at least quarterly. As stated

on the Coca-Cola web-site, “virtually all of our derivatives are straightforward over-the-

counter instruments with liquid markets.” When the derivative instruments and hedging

activities were changed in 2001 to adhere to SFAS No. 133, there was a reduction in net

income of $10 million after taxes. When they enter into the money markets, they

consider the risk of default to be minimal due to the fact that they enter into investment

grade institutions only.

Overall, Coca-Cola’s accounting strategies are within the industry norms and

raise no questions as to why they use the policies they use. Their strategies make sense

for the type of company that they are and can be justified when changes occur.

Quality of Disclosure

With such a large emphasis on quality and brand-name, Coca-Cola is restricted

from disclosing one of their main strengths in marketing. Disclosure controls and

regulations guard the company, preventing them from including the value of marketing

performance as an asset to the business.

Coca-Cola Company does a good job of disclosing economic consequences by

providing a breakdown of financial statements separating countries with changing

political and economic environments and listing the carrying value of non-current assets.

This allows the investor to observe what percentage of the company could virtually be

affected by political or civil unrest and remove any uncertainty about solidity or stability

of their investment.

Reports have indicated that Coca-Cola has been on an apparent decline in the past

five years, but the company does not indicate to its investors the reason why it has not

been as efficient as in previous years. Instead, the company gives a sugar-coated version

of their recent and expected performance in the letter to its shareholders. The company

18

explains that they are optimistic about the future with focus on certain aspects needing

improvement, but they do not relay to the investor where they are at risk.

Coca-Cola is a firm of many segment and products in many different countries.

The company gives a limited explanation of the carrying value of some of the different

segments. They do not give an accurate breakdown of the individual countries’

performance or the breakdown of the different product lines. This breakdown is

significant in recognizing developing and potentially unstable markets and indicating just

how well each product line is doing.

Potential Red Flags

In performing our accounting analysis we were unable to find any accounting

distortions that we would want to correct for. We did have some problems finding some

of the accounts we would have liked to have used to do further diagnostic testing for sales

and expense manipulations, because of the overly consolidated financial statements

provided in their 10K. This in its self is a potential red flag, but because it is not

quantitative we don’t feel that corrections to the financial statements could be done

accurately. It is our opinion that the accounting decisions made are well within the

bounds of industry standards and the numbers reported are, as far as we could tell, true

and fair.

19

Ratio Analysis And Forecasting

In analyzing Coca-Cola’s financial reports it is important to gather past

information in order to predict what the future of the firm may be. First, we assessed the

firm by using financial ratio analysis. We used ratios to perform a liquidity analysis, a

profitability analysis, and a capital structure analysis. The liquidity ratios are used in

order to determine how liquid a company’s assets are. Liquidity is important in

“evaluating the risk related to a firm’s current liabilities” according to chapter 5 of

Business Analysis and Valuation. If a firm does not possess the assets required to repay

their liabilities, they may be considered an investment risk but, on the other hand if the

ratios are too high, then the company may not be imploring enough debt to reach it’s full

growth potential. The profitability ratios indicate how profitable a company is using its

current business methods. The ROE measures Net Income to Shareholders equity which

is very important to let a shareholder know how efficiently their investment is being

utilized. The ROA can tell “how much profit a company is able to generate for each

dollar of assets invested,” (BA&V). The capital structure ratios are useful in analyzing

investment strategy because it employs the use of debt and interest in computing the

ratios.

In performing an analysis it is important to come up with a benchmark to measure

Coca-Cola by. We therefore, measured Coca-Cola’s two main competitors, Pepsi and

Cadbury Schweppes, for liquidity, profitability, and capital structure using the same

ratios and plotted the results to come up with a comparison. After analyzing the recent

history of Coca-Cola in relation to Pepsi and Cadbury Schweppes, we forecasted Coca-

Cola’s financial statements.

Forecasting

To begin with, we first forecasted sales for the next 10 years. We have some

quarterly data for the year 2004. We used the data from the first two quarters to help

forecast the total for the year. The third quarter data was not available as of December 5,

20

2004. To forecast the next ten years we created a straight line representing Coke’s

upward trend through our existing data set using the following equation:

y = a + bx

Where

y = sales

x = number of years

xbya −=

( )∑∑

−

−= 22 xnx

yxnxyb

Linear Trend Line Sales Forecast Years(X) Sales(Y) X^2 XY X avrg= 3 1 $ 19,805 1 $ 19,805 Yavrg= 20,192.60 2 $ 20,458 4 $ 40,916 3 $ 20,092 9 $ 60,276 4 $ 19,564 16 $ 78,256 5 $ 21,044 25 $ 105,220 Totals 15 $ 100,963 55 $ 304,473 b= 158.40 a= 19,717.40

Sales (in millions)

$18,000$19,000$20,000$21,000$22,000$23,000

1999

2002

2005

2008

2011

Linear Trend(PredictedSales)Actual Sales

21

This formula predicted sales to increase by almost exactly one percent. To test

this formula we found the mean absolute deviation using the following formula:

nforecastactual

MAD ∑ −=

36.3835

80.916,1=

The mean absolute deviation equaled 383.36 which we found acceptable in relation to our

sales which were in the tens of thousands.

Once we had predicted sales we figured each account on the income statement as

a percentage of sales for the past five years and averaged them. (See page 44) We used

the resulting averages to predict the respective accounts for the next ten years. We used

the same method to predict accounts on the balance sheet figuring that a company would

have to maintain similar relationships in assets, liabilities, and owner’s equity in respect

to sales to sustain the growth of the company (See page 46).

To forecast the cash flow statements (See page 45), we looked at the rate in which

cash flow was increasing each year. We applied the information that was previously

forecasted on the balance sheet and income statement such as net income and

depreciation and amortization onto the statement of cash flows. We calculated the cash

flow from operations by using the net income and adding non-cash items such as

amortization and depreciation and change in current liabilities and subtracting change in

Actual Forecasted Difference 1999 $ 19,805.00 $ 19,875.80 $ 70.80 2000 $ 20,458.00 $ 20,034.20 $ 423.80 2001 $ 20,092.00 $ 20,192.60 $ 100.60 2002 $ 19,564.00 $ 20,351.00 $ 787.00 2003 $ 21,044.00 $ 20,509.40 $ 534.60 $ 1,916.80

22

non-cash current assets. Cash flow from investing activities has been steadily increasing

but remains negative throughout the past five years. Cash flow from financing activities

has been steadily decreasing and we therefore continued to decrease the cash flows for

future years making sure that the change in cash and cash equivalent from the previous

year equaled the sum of all cash flows.

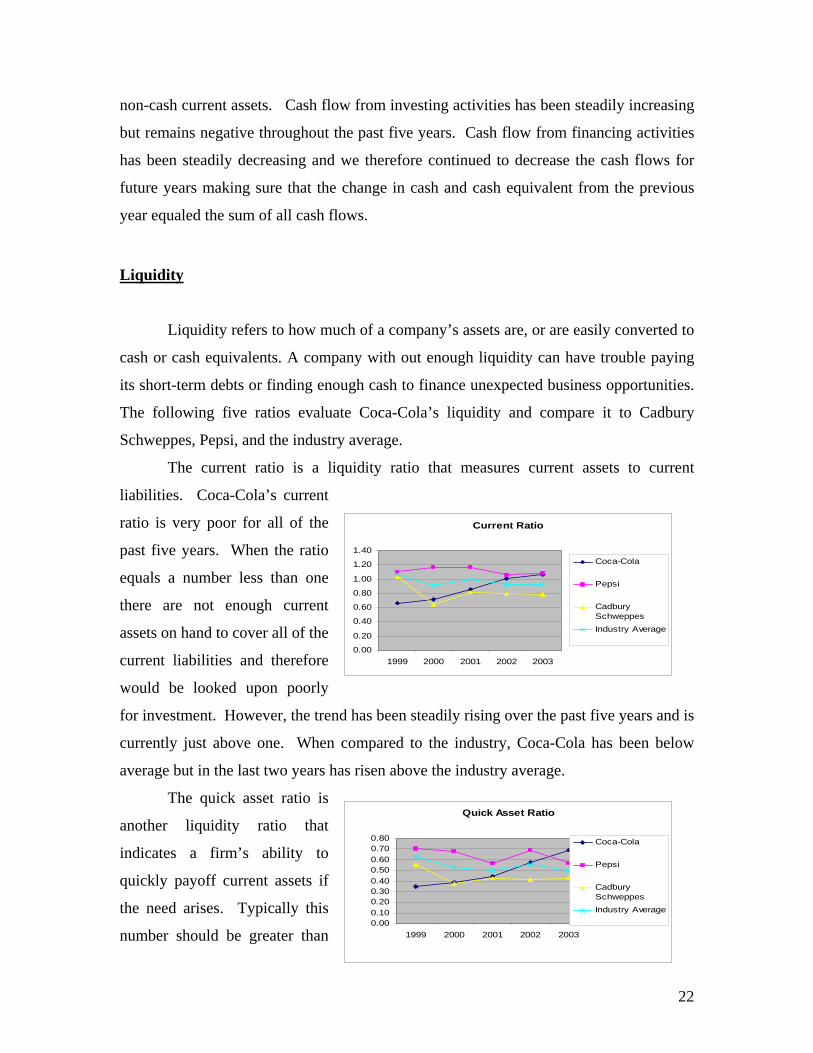

Liquidity

Liquidity refers to how much of a company’s assets are, or are easily converted to

cash or cash equivalents. A company with out enough liquidity can have trouble paying

its short-term debts or finding enough cash to finance unexpected business opportunities.

The following five ratios evaluate Coca-Cola’s liquidity and compare it to Cadbury

Schweppes, Pepsi, and the industry average.

The current ratio is a liquidity ratio that measures current assets to current

liabilities. Coca-Cola’s current

ratio is very poor for all of the

past five years. When the ratio

equals a number less than one

there are not enough current

assets on hand to cover all of the

current liabilities and therefore

would be looked upon poorly

for investment. However, the trend has been steadily rising over the past five years and is

currently just above one. When compared to the industry, Coca-Cola has been below

average but in the last two years has risen above the industry average.

The quick asset ratio is

another liquidity ratio that

indicates a firm’s ability to

quickly payoff current assets if

the need arises. Typically this

number should be greater than

Current Ratio

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1999 2000 2001 2002 2003

Coca-Cola

Pepsi

CadburySchweppesIndustry Average

Quick Asset Ratio

0.000.100.200.300.400.500.600.700.80

1999 2000 2001 2002 2003

Coca-Cola

Pepsi

CadburySchweppesIndustry Average

23

Inventory Turnover

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

1999 2000 2001 2002 2003

Coca-Cola

Pepsi

CadburySchw eppes

Industry Average

one, but as you can see from the table and chart, neither Pepsi, Cadbury Schweppes, nor

Coca-Cola maintain a quick asset ratio above one. The good news for Coca-Cola is that

their quick asset ratio is consistently rising while Pepsi’s has fallen over the past year.

This correlates to the previously mentioned Asset Ratio. It is our belief that Coca-Cola is

trying to raise each of these ratios to become an industry leader and become more

desirable to investors.

The accounts receivable turnover ratio and the days supply of receivables are

related. As the accounts

receivable turnover ratio rises

the days supply of receivables

goes down. The days supply of

receivables indicates the

duration in days that it requires

a company to collect

receivables; therefore it is best

to have a greater accounts receivable turnover ratio. As you can see from the graph,

Coca-Cola’s days supply of receivables is rising which would indicate trouble. The

market trend is rising and Coca-

Cola is well below the industry

average. In this case, Cadbury

Schweppes seems to be an

outlier dragging the industry

average with it. Because Pepsi

and Coca-Cola are so similar in

days supply of receivables there is no indicate of trouble from this analysis. Coca-Cola’s

days supply of receivables seems very reasonable especially considering most of their

sales are on account. Therefore,

we can conclude that Coca-Cola

has a good handle on accounts

receivables and will have a low

rate of bad debt.

Accounts Receivable Turnover

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1999 2000 2001 2002 2003

Coca-Cola

Pepsi

CadburySchweppes

Industry Average

Days Supply of Receivables

0.0010.0020.0030.0040.0050.0060.0070.0080.00

1999 2000 2001 2002 2003

Year

Day

s

Coca-Cola

Pepsi

CadburySchweppes

Industry Average

24

Days Supply

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

1999 2000 2001 2002 2003

Coca-Cola

Pepsi

Cadbury

Industry average

Working Capital Turnover

-200.000.00

200.00400.00600.00800.00

1000.001200.001400.001600.001800.002000.00

1999 2000 2001 2002 2003

Coca-Cola

Pepsi

CadburySchw eppes

Industry Average

Inventory turnover is cost of goods sold divided by inventory. This ratio shows

how many times a company turns over inventory. Coca-Cola turns its inventory over

about five times a year. In the year 2003 the inventory turnover was a little higher than

the previous years. This shows that the Coca-Cola company has increased its ability to

move product thus increasing its liquidity. Coca-Cola is below the industry average for

inventory turnover. Pepsi has by far more turnover than Coke while Cadbury trails the

industry.

Day’s supply is the

number of days in a year (365)

divided by inventory turnover.

This ratio shows how much

inventory the company is

holding in terms of days. Coke

is above the industry average for

days supply of inventory. This shows that coke is holding a large amount of inventory

and is not very efficient in managing its inventory. An efficient company would want to

keep inventory down as low as possible by making its products when they are ordered or

just in time. Coke and Cadbury have nearly twice as much days supply of inventory as

Pepsi thus showing that Pepsi is more efficient in managing inventory.

Working capital turnover is sales divided by working capital or current assets

subtracted by current liabilities. Coca-Cola has a large spike in working capital turnover.

In the first few years current

liabilities was larger than current

assets resulting in a negative

working capital turnover ratio.

This could be a very bad thing if

all the debt the company had

was called in Coke would not be able to pay off its debt. In the year 2002 Coke had

current assets nearly equal to current liabilities this caused a huge spike in the working

capital turnover. This also indicates a problem with liquidity the industry average without

Coke is between nine and seventy-one for Coke to improve its liquidity it would need to

25

Operating Expense Ratio

0.00

0.10

0.20

0.30

0.40

0.50

0.60

1999 2000 2001 2002 2003

CokePepsiCadbury SchweppesIndustry Average

Gross Profit Margin

0%

10%

20%

30%

40%

50%

60%

70%

80%

1999 2000 2001 2002 2003

Coca-ColaPepsiCadburry SchweppesIndustry Average

lower its working capital turnover ratio by increasing current assets or by decreasing

current liabilities.

We found Coca-Cola’s liquidity to be below industry standards. The current ratio

and quick asset ratio have shown improvements over the past few years because current

assets have been increasing in relation to current liabilities, however inventory turnover

and days supply remain unsatisfactory in relation to the industry. This could be due to

bad inventory management or over estimated sales. Overall Coke’s lack of liquidity could

result in problems for coke in the future. (See page 47)

Profitability

Gross profit margin is

gross profit divided by sales.

Coca-Cola has the highest gross

profit margin with a high of 74%

and a recent drop to 67%. The

industry average also had a drop

in the last few years probably due to a recession in the economy. Coke has a high profit

margin and is doing better than the industry average by more than ten percentage points.

This shows that Coca-Cola’s profitability is good.

The operating expense

ratio is a ratio that tells what

percentage selling and general

administrative expenses are to

sales. The higher the percentage,

the less efficient a company is

running. Coca- Cola’s operating

expense ratio has shown steady decline over the last five years, however it has always

been higher than any of its competitors. This indicates that Coca-Cola’s competitors are

able to turn a higher profit than coke for each dollar of sales.

26

N e t P r o f i t M a r g i n

0 . 0 0

0 . 0 5

0 . 1 0

0 . 1 5

0 . 2 0

0 . 2 5

1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3

C o c a - C o l a

P e p s i

C a d b u r y S c h w e p p e s

I n d u s t r y A v e r a g e

A s s e t T u rn o v e r

0 .0 0

0 .2 0

0 .4 0

0 .6 0

0 .8 0

1 .0 0

1 .2 0

1 .4 0

1 9 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3

C o c a -C o laP e p s iC a d b u ry S c h w e p p e sIn d u s try A v e ra g e

The net profit margin ratio is equal to net income divided by sales. This ratio tells

what percentage of sales was

retained by the company as net

income. Obviously stated the

higher the number the more

money the company is able to

keep. Coca-Colas net profit

margin has been somewhat erratic over the past five years, deviating from the industry in

2001 and showing an upward trend since. This suggests that Coca-Cola has become more

profitable than the industry.

The asset turnover ratio is computed as sales divided by total assets. The purpose

of this ratio is to determine how profitable a company’s assets are. A higher number

suggests that the company is

producing large sales volume in

relation to its assets. Coca-Cola’s

asset turn over has wavered

around or below the industry

average for the last five years and

has shown an overall downward

trend. We have also noted that Coke has stayed well below Pepsi, suggesting that Coca-

Cola is not using its assets as efficiently as its largest rival is.

In examining the rate of

return on assets, it is noticeable

that Coca-Cola Company has

shown a steady increase despite

a considerable decrease in 2001.

This increase is most likely due

to an increase in the profit margin or asset turnover. This serves as a positive for Coca-

Cola because it shows that the company employs a larger amount of profits and resources

to earn profits. Also, when comparing this company to its competitors and to the industry

Return On Assets

0.00%

5.00%

10.00%

15.00%

20.00%

1999 2000 2001 2002 2003

Coca-ColaCompanyPepsiCompanyCadburySchweppesIndustryAverage

27

Return On Equity

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

1999 2000 2001 2002 2003

Coca-Cola

Pepsi

Cadbury Shweppes

Industry Average (w/oCoke)

average, one can observe that Coca-Cola has managed to stay completely above the

industry line and has shown consistently higher numbers than both its competitors.

The rate of return on equity figures show that Coca-Cola has about the same

fluctuations as their return on asset

for the past five periods. They

still, for the most part, seem to be

steadily increasing within an up

and down trend line. This also

serves as a positive for the

company because it means that profits have shown an overall increase. It also means that

Coca-Cola is not using as much debt financing in order to increase its assets and, as a

result, owner’s equity represents a larger percentage of total resources. This ratio, along

with return on assets, also proves that Coca-Cola has stayed above that industry average.

Overall we have found Coke to have profitability above industry standards. One

problem we found in our ratio analysis is a high percentage of SG&A compared to sales

suggesting Coke is not selling as efficiently as its competitors. Coke has also not been

making as much money as others in the industry off of it’s assets as seen by its

decreasing asset turnover. Other than these two areas, Coke seems to be doing well. (See

page 47)

Capital Structure

The debt to equity evaluation proves positive for Coca-Cola because it has been

rather steady around one. This

decreases credit risk and the

possibility that interest and debt

repayment cannot be satisfied

with available cash flows. There

has been a slight decrease in this

ratio over the past five years,

which proves that debt has become a smaller portion of total financing. Compared to its

Debt To Equity

0

1

2

3

1999 2000 2001 2002 2003

Coca-ColaCompany Pepsi Company

CadburySchweppesIndustryAverage

28

competitors and the industry average, Coca-Cola has maintained a position along the

same pattern, but has stayed considerably closer to one.

The figures for Coca Cola and Pepsi Co follow a similar increasing trend, while

those for Cadbury Schweppes

stay relatively low, without

much change form year to year.

These figures indicate that Coca

Cola and Pepsi Co have

sufficient funds to cover the

interest payments on their long term debts. Cadbury’s numbers suggest that they need to

be much more careful in how much interest bearing debt they take on, or they will not be

able to make the interest payments.

The debt service margin ratio illustrates how well a company is able to cover the

yearly payments on their long

term debt. Coca Cola’s numbers

show that every year their ability

to meet these payments is

increasing at a fairly rapid rate.

PepsiCo’s numbers however,

indicate that their ability to make

the payment increased until 2000 then began dropping off in more recent years to levels

that may start to raise concerns from creditors about their ability to make the payments.

Cadbury Schweppes numbers have once again remained very low compared to the rest of

the industry, but constant from year to year.

The sustainable growth

rate is the rate at which the firm

can grow while without

decreasing its profits. This ratio

is an excellent benchmark to

show how the company is doing

in relation to the industry. Coca Cola has been the most unpredictable in recent years,

Times Interest Earned

0

5

10

15

20

25

30

35

1999 2000 2001 2002 2003

Coca Cola

PepsiCo

CadburySchw eppes

Industry

Debt Service Margin

0

5

10

15

20

25

30

35

40

1999 2000 2001 2002 2003

Coca ColaPepsiCoCadbury SchweppesIndustry

Sustainable Growth Rate

0

0.05

0.1

0.15

0.2

0.25

0.3

1999 2000 2001 2002 2003

Coca Cola

PepsiCo

Cadbury Schweppes

Indust ry

29

going from reasonable levels to very low levels on a yearly basis. Each time they fall,

they do not seem to fall as far as in the previous year, which indicates that things are

getting better. PepsiCo was stable for 1999 to 2001, and then grew in 2002 before falling

back to the previous levels in 2003. Cadbury Schweppes has dropped every year since

1999, with the greatest changes coming in 2000, since then they have continued to fall,

but not at the levels seen before. (See page 47)

Coke’s capital structure ratios are moving in a positive trend in relation to the

industry. Overall they should not expect many problems in the future related to their

capital structure. Relative to their competitors, Coca Cola overall has a well-balanced

capital structure.

Z-Score

Altman’s Z – score = 1.2(Working Capital/Total Assets) + 1.4(Retained

Earnings/Total Assets) + 3.3(EBIT/Total Assets) + 0.6(Market Value Equity/Book Value

Liabilities) + 1.0(Sales/Total Assets)

= 1.2(510/27,342) + 1.4(26,687/27,342) + 3.3(5,673/27,342) + 0.6(40.71/5.39) +

1.0(21,044/27,342)

= 7.375 This observation of Cola-Cola Company’s Z-score predicts a very healthy

company with, not surprisingly, a low likelihood of failure. The reason for Coca-Cola’s

apparent strong financial performance and high market valuation is due to the positive

numbers in all variables of the equation. In the first component, one can see that there is

no deepening trouble with regard to repeated operating losses which would show a

reduction in working capital relative to total assets. The second component shows the

company’s history in its ability to reinvest earnings in itself. This is most likely due to

the fact that Coca-Cola has survived many years and has created an advantage to younger

companies through accumulated earnings. Ratio three, which makes adjustments for

variable tax rates and leverage due to borrowings, gives a plus to Coca-Cola in its

utilization of assets. The fourth component is a good indicator of the extent to which the

company’s assets can decline before debts may exceed assets. The final component

30

points out the profitability of Coca-Cola’s assets relative to the amount of sales generated

per asset. Coca-Cola’s cost of debt is estimated to be 5.19% which is a fairly low rate.

Comparatively, the z-score matches up with the low cost of debt. Because Coca-Cola has

such a high z-score, they should have the ability to borrow money at very low cost which

is shown to be the case.

31

Valuation

In valuing Coca Cola a combination of historical and forecasted data are used to

predict the firm’s overall value. First we used the non-intrinsic Method of Comparables

model, and then moved onto the more intrinsic methods including the Discounted

Dividends, Free Cash Flow, Residual Income and Abnormal Earnings Growth models.

Each different model analyzes different information about Coca Cola, and work to give

those valuing the firm an idea about how its current market price relates to its estimated

price derived from each of the different models. While analyzing each of the different

models, it can be concluded that Coca Cola would be an undervalued company in the

eyes of analysts based on the differences in estimated and actual share prices and the

relatively small growth rates that are needed to make the two equal.

In the valuation section we will be using the method of comparables as well as

four intrinsic valuation models, the discounted dividends, the discounted free cash flows,

the discounted residual income, and the abnormal earnings growth model, to estimate the

value of the Coca-Cola Company. Valuing the price of the firm is important to

shareholders as well as potential shareholder so they are able to determine if the company

is worth what they are paying for it. If a company is overvalued then it is a good time to

sell shares as well as vice versa, when it is undervalued it is a good time to buy shares.

This is important to the company as well because they may be willing to buy back shares

when the price is low. However, as you will see, valuing the firm is a complex process

that has many variables affecting its outcome. The market may reflect many variables

that are unable to be accurately predicted and it is therefore unlikely that you will beat the

market on a short-term basis.

Cost of Equity

Coca Cola has an estimated cost of equity of 5.44%. This figure was generated by

using a risk free rate of 3.26%, which is the rate on the seven year treasury bonds. The

beta used was calculated using a data regression for the previous sixty months, which is

32

approximately 0.544. The market risk premium was estimated to be 4%. Coca Cola’s

numbers show that they are a low credit risk, with little default risk.

Cost of Debt

Coca Cola’s cost of debt is estimated to be 5.19%; this figure was calculated

using a weighted average of short and long term debt and their pension obligations. The

short term debt represents 59% of the total debt at a cost of 1.97% interest. Long term

debt is 19% of total debt at an estimated cost of 5.28%, while the pension fund obligation

for the year represents 22% of the total at 14.35%. Coca Cola’s long term debt is

represented by a weighted average of their bond maturities. The bonds were divided into

three different categories, with the earliest maturity being in 1-3 years, the next being

those with maturities of 3-7 years, and the longest term bonds were those with maturities

of 10 or more years. The pension fund obligation cost was calculated by dividing the

interest, service, and the actuarial costs by the beginning balance of the ending pension

balance for the year.

Weighted Average Cost of Capital

Coca Cola’s Weighted Average Cost of Capital (WACC) is estimated to be

5.278%, in making these calculations it was determined that Coke is comprised of

11.88% debt and 88.12 % equity. Coca Cola has a very low debt to equity ratio, which

frees it from having to worry much about debt covenants and interest payments. The

downside to having such a small amount of is that Coke loses the tax benefit of the

interest paid on it debt. WACC was calculated by taking a weighted average of Coke’s

total equity and after tax debt, and dividing each by the total value of the company.

Equity was estimated at $98.304 billion, this figure was reached by multiplying the

current share price of $40.96 by the 2.4 billion outstanding shares. Debt was the total

book value of debt from the balance sheet, or $13252 billion. Coke’s weighted average

tax rate is 21%, which was calculated on previous 10K annual reports.

33

Method of Comparables Valuation

The method of comparables is a non-intrinsic model that is the least reliable

because it takes only the competitions information and neglects all firm specific data. It

may also be unreliable due to outliers. In the case of Coca-Cola we are unable to identify

any industry outliers because the industry consists of only three companies. However,

we feel that PepsiCo is comparable to Coca-Cola with name brand recognition and

market shares while Cadbury Schweppes is fairly obscure in comparison; therefore, we

created a method of comparables model removing Cadbury Schweppes and treating it as

an outlier. When doing this, the valuations of Coca-Cola were generally nearer the actual

value of the firm. The price to earnings ratio rose above Coca-Cola’s actual market value

and the price to book value became the more accurate measure of value. Price to sales

decreased dramatically making it comparable to Coca-Cola’s price and debt to price

actually increased the gap between estimated price and actual price.

When using the entire industry, the price to earnings method most accurately

reflected Coca-Cola’s price per share. The other methods were fairly inaccurate. Due to

the fluctuations in valuation price we felt that it may be worth averaging the range of

estimated prices. In doing so, the valuation of Coca-Cola was relatively more accurate

than choosing any method. We have concluded from our valuation using method of

comparables that the price to earnings valuation is the most accurate value when using

the entire firm but there is little faith that any one method may be accurate in the future

and we therefore believe that averaging the industry price when using the method of

comparables would allow for the most consistent valuation. Otherwise we should

eliminate Cadbury Schweppes from the market and value Coca-Cola using only PepsiCo

because there values were comparable. (see page 42)

Abnormal Earnings Growth Valuation

The Abnormal Earnings Growth Model calculates the book value of equity plus

the present value of expected future abnormal earnings. Abnormal earnings consist of

expected net income less the normalized income multiplied by the discount rate. This

34

method implies that if a company has no difference between its expected net income and

the normalized earnings, then the amount invested in the stock should be no more than

the book value. Depending on whether a company’s expected earnings is more or less

than the normal income, investors should pay more or less for the stock. A high value for

abnormal earnings indicates that a firm shows positive abnormal future stock returns and

the contrary. (See page 43)

Our estimation for abnormal earnings was very low due to the minimal difference

between our cumulative dividend earnings and our normal earnings which suggest that

we have negative abnormal stock performance. Since we had a slightly lower estimated

value per share compared to the actual value per share, we added a reasonable growth

rate of 3.171%, implying that our estimations are not extremely sensitive to growth.

Using the given value of beta to calculate our cost of equity, we estimated that our value

per share was $46 compared to the actual value per share of 40$. Using our own cost of

equity and no growth , the model gives a stock price of 34.63 for November 1, 2004. This

would mean that our company would comprise a negative growth rate in order to meet

actual value. As a result, it can only be concluded that our company, in essence, is

undervalued using abnormal earnings and reveals an apparent limitation to this method.

(See page 39)

Discounted Dividends Valuation

The discounted dividends valuation model is used to relate Coca Cola’s future

equity to present values. The model is constructed by using the dividend growth rate to

project the future dividends, and then finding the present value of each individual

payment. The present value is calculated by dividing the dividend by 1 plus the cost of

equity minus the growth rate, and then multiplied to the power of the year the dividend

was issued. The terminal value is calculated by dividing the final forecasted dividend by

only the cost of equity minus the growth rate, and then finding the present value of it.

The estimated share price is calculated by adding the total of all the present values and

the present value of the terminal value. Coca Cola’s estimated share price, when using

the calculated Beta equaled its actual share price of $40.96 when a growth rate of 0.985%

35

was used in the calculations. This represents a very attainable figure that Coca Cola

should have no trouble achieving. According to this model Coca Cola is somewhat

undervalued, in that growth of not even 1% is required for the estimated price to equal

the actual share price. When calculated using the published Beta from Yahoo Finance,

even with a 0% growth rate the estimated share price was below the actual share price.

The model, with no growth values the stock at 34.63 at November 1, 2004. This

reinforces even more that Coca Cola is an unvalued stock when calculated using the

discounted dividends model. (See pages 41, 38)

Free Cash Flow Valuation

The free cash flow valuation utilizes the forecasts off the cash flow statements.

The predicted cash flow from operations and cash provided by the investing activities add

up to total the free cash flow which indicates the profitability of the firm. We then

determine the value in terms of today’s dollar amount. The book value of debt taken

from the value of the firm totals the book value of equity. The value of equity divided by

the number of shares should give you the firm value per share. (See page 45)

In our original valuation we assumed there was no growth and that our weighted

average cost of capital (WACC) is 5.278%. The estimated value per share resulted in

$26.94, a lower price than Coca-Cola is actually traded at by almost $15. We then

performed a sensitivity analysis by lowering the assumed weighted average cost of

capital to 3.75%. Leaving the growth rate at zero, the value of the firm using the adjusted

WACC came to $40.78, much closer to the market price per share of $40.96. We then

returned the WACC to our original estimate and adjusted the growth rate because we

assume that Coca-Cola will continue to grow in the future. With a growth rate of 2.15%,

the estimated value per share totaled $41. We then recalculated the WACC using the

published beta from yahoo finance and came up with 4.048% which increases the

estimated value of the firm to $37.26 with zero growth. The growth necessary to increase

the firms estimated value to $40.78, comparable to the actual value, was only 0.425%.

(See page 38)

36

After performing the free cash flow valuation we found that based on this model

the firm may be undervalued considering our growth rate is relatively small. There are

inherent limitations associated with this valuation process including how well the cash

flow statements are forecasted, if the cash flows are inaccurately predicted then the model

is less applicable. With no growth using our WACC, the model predicted a stock price of

37.33 for November 1, 2004.

Residual Income Valuation

The Residual Income Model is an accounting based model. In the RI model we

use data from the past to help determine the value of the firm to see if the firm is over

valued or under valued. The Residual Income model uses the relationships between

earnings per share dividends paid and the cost of equity to find the residual income. The

Residual Income is the amount of earnings left over after stock holders cost of equity is

met. After finding the forecasted Residual Income we then take the present value of the

future cash flows and add them together this gives us the total present value of Residual

Income for the ten year forecast. Next we will compute a terminal value for the Residual

Income model to do this we calculate a perpetuity which will also need discounted back

to the present. (See page 42)

In our Residual Income Valuation Model we found the cost of equity to be

5.4364% and with a growth of almost three percent we calculated a present value that is

almost the same as the current price. A three percent growth may be too low for Coco-

Cola; in other words, the firm may be undervalued. When we use the beta from yahoo to

calculate the cost of equity we get 4.04% which is lower than the cost of equity we

calculated. With the cost of equity from yahoo we would need an even lower growth rate

to get today’s price, this may further indicate the firm is undervalued. The current book

value makes up 14% of the firms estimated share value while the predicted Residual

Income for the next ten years makes up 20% of the firms estimated share value, 66% of

the firms estimated share value comes from the terminal value estimation. The yahoo

numbers are close to our numbers current book value is 14% of total value the predicted

RI over ten years is 23%, and the terminal value makes up 63% of the total value. The

37

firm gets most of its value from the terminal prediction which has the greatest chance for

error this could mean the firm is under valued or possibly overvalued. With non growth

rate the model values the firm at 25.83 for November 1, 2004. (See page 39)

Long Run Residual Income

The long run residual income model estimates the value of the company’s stock

using the price over book ratio. Using 2003’s ROE of 35.98% and no growth the model

values the stock at 39.87 for November which is very close to Coke’s actual share price.

Because Coke will most likely have growth in the coming years, we feel that this model

shows that Coke is currently undervalued. (See page 40)

38

Appendices

Discounted Dividends Model Sensitivity Analysis

Ke Growth 4.040% 4.500% 5.000% 5.436% 6.000%

0.00% $ 49.57 $ 43.98 $ 39.10 $ 35.58 $ 31.81 0.25% $ 52.03 $ 45.87 $ 40.55 $ 36.75 $ 32.72 0.50% $ 54.85 $ 48.00 $ 42.16 $ 38.05 $ 33.71 0.75% $ 58.09 $ 50.41 $ 43.96 $ 39.47 $ 34.79 1.00% $ 61.87 $ 53.16 $ 45.99 $ 41.07 $ 35.99 1.25% $ 66.32 $ 56.34 $ 48.28 $ 42.85 $ 37.31 1.50% $ 71.65 $ 60.04 $ 50.91 $ 44.85 $ 38.77 1.75% $ 78.14 $ 64.42 $ 53.94 $ 47.13 $ 40.41 2.00% $ 86.23 $ 69.68 $ 57.47 $ 49.74 $ 42.25

Free Cash Flows Sensitivity Analysis

WACC Growth 3.500% 4.048% 4.500% 5.000% 5.278% 5.500%

0.00% $ 44.20 $ 37.26 $ 32.80 $ 28.82 $ 26.94 $ 25.57 0.25% $ 47.01 $ 39.23 $ 34.32 $ 29.99 $ 27.95 $ 26.48 0.50% $ 50.30 $ 41.49 $ 36.03 $ 31.29 $ 29.08 $ 27.49 0.75% $ 54.18 $ 44.08 $ 37.97 $ 32.73 $ 30.33 $ 28.60 1.00% $ 58.83 $ 47.10 $ 40.19 $ 34.36 $ 31.72 $ 29.84 1.25% $ 64.52 $ 50.66 $ 42.74 $ 36.21 $ 33.29 $ 31.22 1.50% $ 71.63 $ 54.92 $ 45.72 $ 38.32 $ 35.06 $ 32.78 1.75% $ 80.78 $ 60.11 $ 49.25 $ 40.76 $ 37.08 $ 34.54 2.00% $ 92.97 $ 66.56 $ 53.47 $ 43.60 $ 39.42 $ 36.55 2.25% $ 110.04 $ 74.79 $ 58.64 $ 46.96 $ 42.14 $ 38.88 2.50% $ 135.64 $ 85.70 $ 65.10 $ 50.99 $ 45.35 $ 41.59

39

Abnormal Earnings Growth Sensitivity Analysis

Ke Growth 4.048% 4.500% 5.000% 5.436% 6.000%0.00% $ 46.19 $ 40.45 $ 35.45 $ 40.96 $ 28.21 0.25% $ 46.95 $ 41.01 $ 35.85 $ 32.23 $ 28.43 0.50% $ 47.82 $ 41.63 $ 36.30 $ 32.58 $ 28.68 0.75% $ 48.82 $ 42.34 $ 36.80 $ 32.96 $ 28.96 1.00% $ 49.99 $ 43.15 $ 37.36 $ 33.38 $ 29.26 1.25% $ 51.36 $ 44.08 $ 38.00 $ 33.85 $ 29.59 1.50% $ 53.00 $ 45.17 $ 38.73 $ 34.38 $ 29.96 1.75% $ 55.00 $ 46.45 $ 39.57 $ 34.99 $ 30.37 2.00% $ 57.49 $ 48.00 $ 40.55 $ 35.68 $ 30.83 2.25% $ 60.67 $ 49.88 $ 41.71 $ 36.48 $ 31.36 2.50% $ 64.88 $ 52.24 $ 43.10 $ 37.42 $ 31.96 3.00% $ 79.32 $ 59.31 $ 46.93 $ 39.88 $ 33.46 3.50% $ 120.10 $ 73.46 $ 53.31 $ 43.60 $ 35.56

Residual Income Sensitivity Analysis

Ke Growth 3.500% 4.040% 5.000% 5.436% 6.000%

0.00% $ 41.43 $ 35.85 $ 28.89 $ 26.54 $ 24.00 0.25% $ 43.40 $ 37.21 $ 29.66 $ 27.15 $ 24.46 0.50% $ 45.71 $ 38.77 $ 30.51 $ 27.82 $ 24.96 0.75% $ 48.44 $ 40.56 $ 31.47 $ 28.56 $ 25.51 1.00% $ 51.71 $ 42.65 $ 32.55 $ 29.39 $ 26.12 1.25% $ 55.71 $ 45.11 $ 33.76 $ 30.31 $ 26.79 1.50% $ 60.71 $ 48.06 $ 35.16 $ 31.36 $ 27.53 1.75% $ 67.14 $ 51.65 $ 36.76 $ 32.54 $ 28.36 2.00% $ 75.71 $ 56.12 $ 38.64 $ 33.90 $ 29.30 2.25% $ 87.27 $ 61.84 $ 40.86 $ 35.47 $ 30.36 2.50% $ 105.72 $ 69.42 $ 43.51 $ 37.31 $ 31.57 2.75% $ 135.72 $ 79.93 $ 46.73 $ 39.49 $ 32.97 3.00% $ 195.73 $ 95.50 $ 50.83 $ 42.12 $ 34.60

40

Long Run Residual Income Sensitivity Analysis

Ke Growth 3.50% 4.04% 5.00% 5.44% 6.00%0.00% $ 63.63 $ 55.13 $ 44.54 $ 40.97 $37.12 0.25% $ 68.05 $ 58.36 $ 46.56 $ 42.65 $38.46 0.50% $ 73.21 $ 62.04 $ 48.80 $ 44.49 $39.93 0.75% $ 79.30 $ 66.28 $ 51.31 $ 46.54 $41.54 1.00% $ 86.61 $ 71.23 $ 54.13 $ 48.81 $43.31 1.25% $ 95.55 $ 77.05 $ 57.33 $ 51.36 $45.26 1.50% $ 106.72 $ 84.03 $ 60.98 $ 54.23 $47.43 1.75% $ 121.08 $ 92.53 $ 65.19 $ 57.48 $49.85 2.00% $ 140.22 $ 103.11 $ 70.11 $ 61.22 $52.58 2.25% $ 167.03 $ 116.64 $ 75.92 $ 65.53 $55.68 2.50% $ 207.24 $ 134.57 $ 82.90 $ 70.59 $59.21 2.75% $ 274.26 $ 159.45 $ 91.42 $ 76.58 $63.29 3.00% $ 408.29 $ 196.29 $ 102.07 $ 83.80 $68.05

41

42

43

44

45

46

47

48

References

1. http://finance.yahoo.com/

2. http://www2.coca-cola.com/

3. http://beverage-digest.com/editorial/datastats.html

4. http://moneycentral.msn.com/investor/invsub/results/hilite.asp?Symbol=KO

5. http://moneycentral.msn.com/investor/sec/filing.asp?Symbol=KO

(Coca-Cola 10k)

*All accounting numbers come from MSN Money and Edgarscan