equity | india | it services cyient ltd. initiating...

TRANSCRIPT

Equity | India | IT Services

Cyient Ltd.

Growing with technology…… March 31, 2015

BUY

Analyst

Omkar Tanksale

+91-22- 6614 2692 [email protected] Institutional Research 1

Initiating Coverage

CMP (`) Target (`)

510 602

Potential Upside Absolute Rating

20% BUY

Market Info (as on March 30, 2015)

BSE Sensex 27,975.86

Nifty S&P 8,492.30

Stock Detail

BSE Group A

BSE Code 532175

NSE Code CYIENT

Bloomberg Code CYL IN

Market Cap (`bn) 57.29

Free Float (%) 65%

52wk Hi/Lo 592.80 / 265.00

Avg. Daily Volume (NSE) 36971

Face Value / Div. per share (`) 5.00 / 3.00

Shares Outstanding (mn) 112.2

Shareholding Pattern (in %)

Promoters FIIs DII Others

22.23 35.78 13.43 28.56

Financial Snapshot (`mn)

Y/E Mar FY13 FY14 FY15E FY16E

Net Sales 18,731 22,064 26,972 31,294

EBITDA 3,424 4,102 4,428 6,066

PAT 2,311 2,660 3,614 4,435

EPS 21 24 32 40

ROE (%) 17% 17% 19% 20%

ROCE (%) 23% 22% 25% 27%

P/E 8.3 13.4 15.7 12.7

EV/EBITDA 4.3 7.1 11.0 7.6

Share Price Performance

60

80

100

120

140

160

180

Mar-

14

Apr-

14

May-

14

Jun-1

4

Jul-

14

Aug-1

4

Sep-1

4

Oct

-14

Nov-

14

Dec-

14

Jan-1

5

Feb-1

5

Mar-

15

Cyient Ltd BSE SENSEX

Rel. Perf. 1Mth 3 Mths 6Mths 1Yr

Cyient (%) (8.3) (1.9) 12.8 57.6

Sensex (%) (4.7) 2.1 5.1 25.0

Source: Company data, Institutional Research

Company Snapshot

Cyient Ltd. (Cyient) formerly known as Infotech ltd. is an Indian IT services providing company.

Cyient is headquarters in Hyderabad (India) and majorly focus on the domains such as

Engineering, networking and operations. Cyient specializes in end to end solutions from co

creation and managing product life cycle which also helps Cyient to create long term

relationship with its clients. Cyient has also developed robust engineering ecosystem, functional

expertise, and streamlined processes. They deliver reliable and innovative products and

services, helping its clients to achieve and maintain competitive advantage.

Investment Rationale

Focus on moving up the value chain which will help to generate higher Realization

Cyient focus more on the product engineering and process engineering segment. More than 62%

of its revenue comes from the segment. Now company has also started to focus more on the non

linear business verticals like system integration, testing, embedded system etc. which help to

take value chain on the next level. This will also create Cyient better business opportunities not

only across verticals but also to give more robustness to the business structure.

Efficient use of the reserves to acquire companies will help to strengthen the business

Cyient has also history to use its reserves to strengthen the business among different verticals.

This helps Cyient to acquire new technology among different verticals and help to build brand.

Cyient has able to generate cash reserves on its balance sheet which help them to acquire the

business without raising the debt burden on their balance sheet. Company also finalizes the

strategic plan for growth for the verticals. Recently company has signed an agreement to

acquire the majority equity shares of Rangsons Electronics Private Limited. This acquisition will

help Cyient to strengthen design engineering, embedded Systems and aftermarket business and

will help to acquire some of the top clients among segment.

Long term contracts with global players will help Cyient to give more consistent

performance

Cyient specializes in providing end to end engineering solution to the companies across

verticals. The company has also become successful in delivering complete product engineering

solutions. Cyient has penetrated the business across geographies and make the company a

strong brand name in the field of product and process engineering. Strong clientele guarantees

the revenue over long term period. Timely delivery of the project will help the company to have

empanelment with the major businesses across the geographies. This strategy of the company

will help to create more stable business structure and also to perform consistently over the

longer period of time. The vertical wise list of clients given below gives an idea of

empanelment across the verticals and robustness of the business.

Valuation

At the CMP of `503, Cyient is trading at 15.8x, and 12.7x its FY15E, and FY16E EPS of `32.3 and

`39.60. Compared to its peers; Cyient is trading at a discount P/E multiple, although its margins

are better than or comparable to peers. We initiate coverage on Cyient Ltd with a BUY rating

and attach a multiple of 15.2 xs to Cyients’ FY16E earnings (EPS) to arrive at the target price of

`602, indicating a potential upside of 20%.

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 2

Index & Content

Sr. No. Topic Page No.

1 Company Background......................................... 3

2 Business Model................................................. 4

3 Key Management Personnel.................................. 5

4 Investment Rationale......................................... 6

5 Financial Overview........................................... 10

6 Key Risks........................................................ 14

7 SWOT Analysis.................................................. 15

8 Michael Porter’s Five Force Analysis........................ 16

9 Valuation & Outlook........................................... 17

10 Financials........................................................ 18

11 Disclaimer....................................................... 19

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 3

Company Background

Cyient Ltd. (Cyient) formerly known as Infotech Enterprises Ltd. is the Hyderabad based

midsized IT services company. The company is majorly involved in providing solutions and

engineering services to companies across verticals. Majority of verticals include Aerospace,

Transportation, Semiconductor, Medical and electronics etc. The company has developed the

expertise in the field of design engineering. Cyient also has strong presence in the field of data

transformation, network & operations and Utilities. They help their clients in communication

service providers (CSPs) plan, design and manage their next-generation networks.

Historical Journey of Cyient Ltd

1991 Infotech Incorporated as private limited company.

1995 The company receives its first ISO 1992 certification

1997 Become Public Ltd. company, Partner with the IBM for ERP system.

1999 Infotech acquires Cartographic Sciences Pvt. Ltd. Mumbai, India, from analytical surveys Inc USA

2000 Infotech announces Acquisition of the German company, Advanced graphic software GmBH specializing in 3D CAD/ CAM.

2000 Infotech Wins Multimillion dollar GIS project from Dutch multinational group FUGRO.

2002Pratt & Whitney to participate with up to ~18% equity stake in Infotech, demonstrating long-term partnering intent and

endorsing Infotech's business competence.

2003 Infotech signs long-term outsourcing contract with Bombardier Transportation to provide engineering services in India.

2004 Infotech acquires VARGIS, a GIS company in the US.

2004Infotech divests 51% of its stake in Infotech Aerospace Services Inc. in favor of United Technologies International

Corporation.

2007 Infotech sets up a development center at Kakinada at the newly developed STPI facility.

2007 Joint venture between Infotech and HAL is announced. Joint venture between Infotech and Geospace Integra is announced.

2010 Signed a long-term engineering services contract with Hamilton Sundstrand.

2010 Acquired Daxcon Engineering Inc., USA. Acquired Wellsco Inc., USA.

2011 IGIL (Infotech Geospatial (India) Limited) becomes a wholly-owned subsidiary.

2011 Awarded Supplier of the Year award by Boeing.

2014 Revealed the new brand and changed the name to Cyient

2014 Ranked among top 30 outsourcing companies in the world by IAOP

2015 Cyient awrded for excellance in Aerospace exports at Aero India 2015

Source: Company, Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 4

Business Model

Cyient has unique business model and different area of practice as compared to other IT

services companies. It is basically an engineering service and solution providing company. Cyient

operates under three vertical Viz. Data transformation & Analytics, Network Operations Product

Engineering and Process Engineering. Majority of the revenue comes from Design Engineering,

about 65% of the total revenue. Cyient has developed an expertise in the field of design

engineering across different segments like Aerospace, Heavy machinery, Semiconductor,

Transportation, Utilities & communication, Energy & Natural Resources. Other major contributor

of the top line is Data transformation, network and operations (DNO). Cyient help in efficiently

manage their network infrastructure and assets. They also support the implementation and

integration of distribution management and outage management systems. About 34% of the

revenue comes from DNO segment. Remaining revenue comes from Process Engineering.

Business Model

Domain

Transport & NavigationProduct

Engineering

Product Health Monitoring

Engineering Data Transformation &

AnalyticsNetwork & Operations

Process Engineering

Reliability Engineering

Technical Publication

Obsolescence Management

Sustenance Engineering

Feeds Support

Procurement Support

Operation & Maintenance

Support

Energy Natural Resources

Content & Geospatial

Communication

Utilities

Source: Company, Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 5

Key Management Personnel

Cyient Ltd. is blessed with credible management that takes Cyient on the path of the growth.

B.V.R Mohan Reddy (Executive Chairman):

Mohan focuses on the medium- to long-term future of the company. He is also involved in

leadership development, innovation, information systems and corporate social responsibility.

Krishna Bodanapu (Managing Director and CEO):

Krishna Bodanapu joined Cyient in 2001. In his current role, he provides the strategic direction

for growth and is responsible for all operations.

B. ASHOK REDDY (President, Corporate Affairs & Infrastructure):

Ashok has fiduciary responsibility for all of Cyient’s subsidiaries. As the chairman of the

subsidiaries, he maintains all government and industry body relationships

AJAY AGGARWAL (Sr. VP & CFO):

Ajay has extensive international experience spanning 27 years in financial management and

commercial management at large multi location, multiproduct organizations. He is skilled in

setting up startups with expertise in funding, banking and strategic planning, business modeling,

MIS, ERP implementations, capital budgeting, corporate finance, M&A and restructuring.

DR. DEVENDRA RAO GUNTUPALLI (Sr. VP & CIO)

Dr. Rao is currently responsible for information technology and systems to generate business

value to the organization.

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 6

Investment Rationale

Strategic vertical split to drive the desire growth

Cyient is operating under different verticals to provide design and engineering services to its

clients. The company has managed successfully its product mix across different verticals to

attain desire growth momentum. Engineering Services Outsourcing (ESO) is one of the most

highly growing sectors in IT service industry. India will be leading offshore destination which

provide high end ESO.

Revenue Split (vertical wise)

0%

10%

20%

30%

40%

50%

60%

70%

1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 2QFY15 3QFY15

Engineering Data Transfrmation network Others

Source: Company data, Institutional Research

From the above chart we can see that in the Cyient operates fewer than three main verticals

viz. Engineering, Data transformation and analytics, Network and operations. More than 62% of

the revenue comes from engineering vertical. Cyient has multiyear contracts with the fortune

500 companies which give more robust business structure. Cyient is one of the old companies

which provides engineering outsource service (ESO) and has good market share. Cyient has also

created renowned brand in the field which help to increase and retain the client base across

vertical. In the last quarter 3QFY15, Cyient added 8 client on the on ESO vertical. Data

networking and operations (DNO) is other vertical which constitutes more than 37% of the

revenue. In the last quarter Cyient has become successful in acquiring 15 new clients in its

client list which again responsible for future robust top line growth.

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 7

Robust top line growth is expected in the upcoming period with high

growth in the segment revenue.

Cyient is the market leader in the field of Product engineering and Design Engineering. More

than 65% of the top line contribution comes from this segment. The Engineering services

outsourcing (ESO) is outpaced the IT service industry over the last five years. The engineering

services outsourcing has been growing across the geographies and among different sub segments

like new product development, Engineering consulting, value Engineering etc.

India's Product Engineering Growth Rate ($ bn)

1314.7

42

0

5

10

15

20

25

30

35

40

45

FY11 FY12 FY2020E

13% YoY Growth

Source: Zinnov, Institutional Research

From the above diagram we can say that, ESO has shown strong growth momentum in the past

few quarters and also have higher growth prospects. Cyient has larger client distribution from

the same industry.

India is one of the largest contributors to the industry with more than 20% market share. India is

considered to be better option for ESO as easy availability of the highly skilled labor,

infrastructure and technology. The total product engineering outsourcing sector is likely to grow

with 13-15% in the upcoming years. By the year 2020 the sector has the outlook of growing with

14% CAGR. The total market size of the Indian Engineering outsourcing will be $42 bn , this

potential of the market will definitely give Cyient an edge to grow with higher momentum. We

believe that as a market leader in India Cyient will outperform the market growth rate.

Specialize technology in the field will help the company to grow in the upcoming future.

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 8

Long term contracts with global players will help Cyient to give more

consistent performance

The product engineering and the design engineering outsourcing is very volatile in nature. Cut

throat competition among peers, competition among pricing and higher man hour supply put

pressure on the company from overseas. However strong clientele guarantees the revenue over

long term period. Timely delivery of the project will help the company to have empanelment

with the major businesses across the geographies. This strategy of the company will help to

create more stable business structure and also to perform consistently over the longer period of

time. The vertical wise list of clients given below gives an idea of empanelment across the

verticals and robustness of the business. We believe that, strong client list; robust business

structure will help company to improve its top line with higher momentum.

Client Distribution

Aerospace

• Pratt & Whitney

• UTC Aerospace Systems

• Boeing

• Airbus

• Honeywell

Transportation

• Bombardier

• Siemens Rail

• Automation

• Alstom

• Thales

• Hitachi Rail

Off-highway Products

• Caterpillar

• Terex

• John Deere

• Joy Global

• Komatsu

• Rio Tinto

Semiconductor

• IBM

• Qualcomm

• Texas Instruments

• Broadcom

• Maxim

Utilities

• Southern California

Edison

• PG&E

• SP AusNet

• Ausgrid

• Powercor

Communications

• AT&T

• Verizon

• Cox

• Airtel

• Telstra

Energy & Natural Resources

• Westinghouse

• Siemens

• Transocean

• Fabricom

• Rio Tinto

• Mitsubishi

Commercial & Geospatial

• Tom Tom

• RPA

• Ordnance Survey

Medical & Electronics

• Philips Healthcare

• Thermofisher

• Medivators

Source: Company data, Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 9

Efficient use of the reserves to acquire companies will help to strengthen

the business

Cyient has also history to use its reserves to strengthen the business among different verticals.

This helps Cyient to acquire new technology among different verticals and help to build brand.

Cyient also able to generate cash reserves on its balance sheet which help them to acquire the

business without raising the debt burden on their balance sheet. Company also finalizes the

strategic plan for growth for the verticals. Recently company has signed an agreement to

acquire the majority equity shares of Rangsons Electronics Private Limited. This acquisition will

help Cyient to strengthen design engineering, embedded Systems and aftermarket business and

will help to acquire some of the top clients among segment.

Consistent employee addition help company to maintain higher efficiency

Strong employee support makes IT service company stronger. Higher the employees higher the

projects can IT company can take. Employee addition increases the efficiency of the company.

This will ultimately help to attain higher top line growth and also help company to grow.

Employee distribution

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1Q

FY11

2Q

FY11

3Q

FY11

4Q

FY11

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

Engineering DNO IT Services Support Functions Utilization

Source: Company data, Institutional Research

As shown in the above chart, Cyient has consistent employee addition which ensures timely

completion of the project. Higher efficiency ensures lower operating cost which will help Cyient

to produce better operating margins. Moderate addition in the employees also helps to add

active clients. This will also help to attain desire top line growth. From the above chart we can

see that, Cyient has maximum dedicated employees to engineering and DNO services. Stable

utilization levels also show the efficient use of its manpower to generate revenue. This enables

company to acquire new projects easily as compared to its peers, and also ensures the timeline

based delivery of the project.

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 10

Financial Overview

Pretax Margin

EBITDA Margins

As shown in the graph below, Cyient has shown consistent EBITDA growth over the past few

quarters. This shows that Cyient has been successful in managing the operating expenses

efficiently with the rise in the top line. After the slight decline in the EBITDA margins in 1QFY15

company has started regaining the desire operating efficiency over last two quarters and will

also likely to continue in the upcoming period.

EBITDA Margins

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1000

1200

1400

1Q

FY11

2Q

FY11

3Q

FY11

4Q

FY11

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

EBITDA Margin

Source: Company data, Institutional Research

Operating Margins

As shown in the graph below, Cyient has become successful in increasing the operating margins

over past few years. Consistent rise in the operating profit indicates that, Cyient has become

successful in transferring the operating cost to its customers. This also indicates rising efficiency

in the business. We believe that Cyient will deliver better operating margins as they focus more

on the segments where they have higher realizations.

Operating Margins

0%

5%

10%

15%

20%

25%

30%

0

200

400

600

800

1000

1200

1400

1600

1Q

FY11

2Q

FY11

3Q

FY11

4Q

FY11

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

EBIT after other Income Margin

Source: Company data, Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 11

Net Profit Margin

Cyient has become successful in delivering consistent and high growth in the net profit and also

margins are showing consistent growth. This shows that the business of the company has

become more robust over the period of time. Large multiyear contracts, strong client addition

makes company more lucrative. We believe that Cyient will likely to report higher bottom line

growth in the upcoming future. This also makes Cyient a safer bet.

NPAT Margin

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-

200

400

600

800

1,000

1,200

1Q

FY11

2Q

FY11

3Q

FY11

4Q

FY11

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

PAT Margin

Source: Company data, Institutional Research

Return Margin

ROE performance

As shown in the diagram below, we can see that ROE of the company has increasing consistently

over last four years. This shows that Cyient has produced better results on the invested equity.

This shows that, Cyient is a better investment opportunity and can produce better return in the

future.

RoE

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

500

1,000

1,500

2,000

2,500

3,000

FY10 FY11 FY12 FY13 FY14

Net Profit ROE

Source: Company data, Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 12

Return on the capital Employed (ROCE)

Return on the capital employed (ROCE) is also one of the major important aspect while

investing. Cyient has zero or marginal debt on their balances sheet. So that the company has

produce the strong growth in terms of ROCE as net profit is growing. We believe that Cyient will

show a strong growth for the upcoming period.

RoCE

0%

5%

10%

15%

20%

25%

-

500

1,000

1,500

2,000

2,500

3,000

FY10 FY11 FY12 FY13 FY14

Net Profit RoCE

Source: Company data, Institutional Research

Payout Ratio

Dividend Payout Ratio

Cyient is one of the highly dividend paying company. As shown in the graph below Cyient has

strong payout ratio. This also makes stock very lucrative. We believe that in the upcoming

period Cyient will likely to maintain the payout ratio of 20% in the upcoming period.

Dividend Payout Ratio

0%

5%

10%

15%

20%

25%

-

100

200

300

400

500

600

700

800

FY10 FY11 FY12 FY13 FY14

Dividend Paid Dividend payout ratio

Source: Company data, Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 13

Net Profit to Payout Ratio

Cyient has history of paying dividend to its share holder. As shown in the diagram below we can

see that company had given dividends as proportion to the net profit. We believe that payout

ratio to net profit ratio will likely to remain same. This also makes stock more lucrative.

Investor can also take privilege of higher payout ratio.

Net Profit to Payout Ratio

0%

5%

10%

15%

20%

25%

-

500

1,000

1,500

2,000

2,500

3,000

FY10 FY11 FY12 FY13 FY14

Net Profit Dividend payout ratio

Source: Company data, Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 14

Key Risks

Investment Risk :

Fluctuations in the US$-INR and GBP-INR and GBP-US$. As majority of the revenue

comes from international territories. Fluctuation in the currencies will impact the

revenue of the company

Change in the economic climate / legislation against Indian offshore development in

the countries where the company provides its services. Fluctuation in world’s largest

economy will affect the IT services business on substantial front.

Increase in Visa fees will increase the cost. Rise in the visa fees will lead to rise in the

operating cost (Employee expenses) to IT industry. So it plays a major role in the IT

industry.

Salary hikes i.e. wage inflation may cause a spoil sport. Rising economic growth will

create more jobs in the country. This will ultimately give rise to wages hikes. Wage

hikes will affect the operating margins of the company. So fluctuation in the wages is

considered to be significant risk in IT service Industry.

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 15

SWOT Analysis

Cyient

Limited

Strengths

• Strong domain focus

• Diversification of business.

• North America is the main area

of operations

• Strong management and

Employee workforce

Opportunities

• Further penetration in US

• Mining the existing and the new

clients

Weaknesses

• High client concentration

• High geography concentration

• Single domain dependence

Threats• Slowdown in the European

economy

• Slowdown in the IT spending

• Loss of top client

• INR appreciates vis-a-vis

Source: Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 16

Michael Porter’s Five Force Analysis

Inter-firm Rivalry–High

Lower Entry barriers in

the industry have led to

high concentration in

the industry.

Threat of new entrants –

Increasing

• MNCs are entering the ‘offshore’

business heavily.

Bargaining Power of

Suppliers – High

• Intense competition in the

recruitment market puts higher

wage pressure and increasing

trend of attrition is witnessed.

Bargaining Power of Buyers –

Increasing

• With availability of multiple

vendors, Buyers have a lot of

choice and this has led to

pressures on the billing rates.

Threat from Substitutes -

Increasing

• Emerging economies like China,

Brazil and Russia can be the

substitute places for ‘offshoring’

taking away the India advantage

to certain extent.

Source: Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 17

Valuation & Outlook

At the CMP of `503, Cyient is trading at 15.8x, and 12.7x its FY15E, and FY16E EPS of `32.3 and

`39.60. Compared to its peers; Cyient is trading at a discount P/E multiple, although its margins

are better than or comparable to peers. We initiate coverage on Cyient Ltd with a BUY rating

and attach a multiple of 15.2 xs to Cyients’ FY16E earnings (EPS) to arrive at the target price of

`602, indicating a potential upside of 20%.

1 year forward P/E Chart

0

100

200

300

400

500

600

Ap

r-04

Aug

-04

Dec-0

4

Ap

r-05

Aug

-05

Dec-0

5

Ap

r-06

Aug

-06

Dec-0

6

Ap

r-07

Aug

-07

Dec-0

7

Ap

r-08

Aug

-08

Dec-0

8

Ap

r-09

Aug

-09

Dec-0

9

Ap

r-10

Aug

-10

Dec-1

0

Ap

r-11

Aug

-11

Dec-1

1

Ap

r-12

Aug

-12

Dec-1

2

Ap

r-13

Aug

-13

Dec-1

3

Ap

r-14

Close -Unit Curr 10.0 X 12.0 X 15.0 X 18.0 X 20.0 X

Source: Capitaline, Institutional Research

1 year forward P/ BV Chart

0

100

200

300

400

500

600

Apr-

04

Sep-0

4

Feb-0

5

Jul-

05

Dec-

05

May-

06

Oct

-06

Mar-

07

Aug-0

7

Jan-0

8

Jun-0

8

Nov-

08

Apr-

09

Sep-0

9

Feb-1

0

Jul-

10

Dec-

10

May-

11

Oct

-11

Mar-

12

Aug-1

2

Jan-1

3

Jun-1

3

Nov-

13

Apr-

14

Close -Unit Curr 1.5 X 2.0 X 2.5 X 3.0 X 3.5 X

Source: Capitaline, Institutional Research

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 18

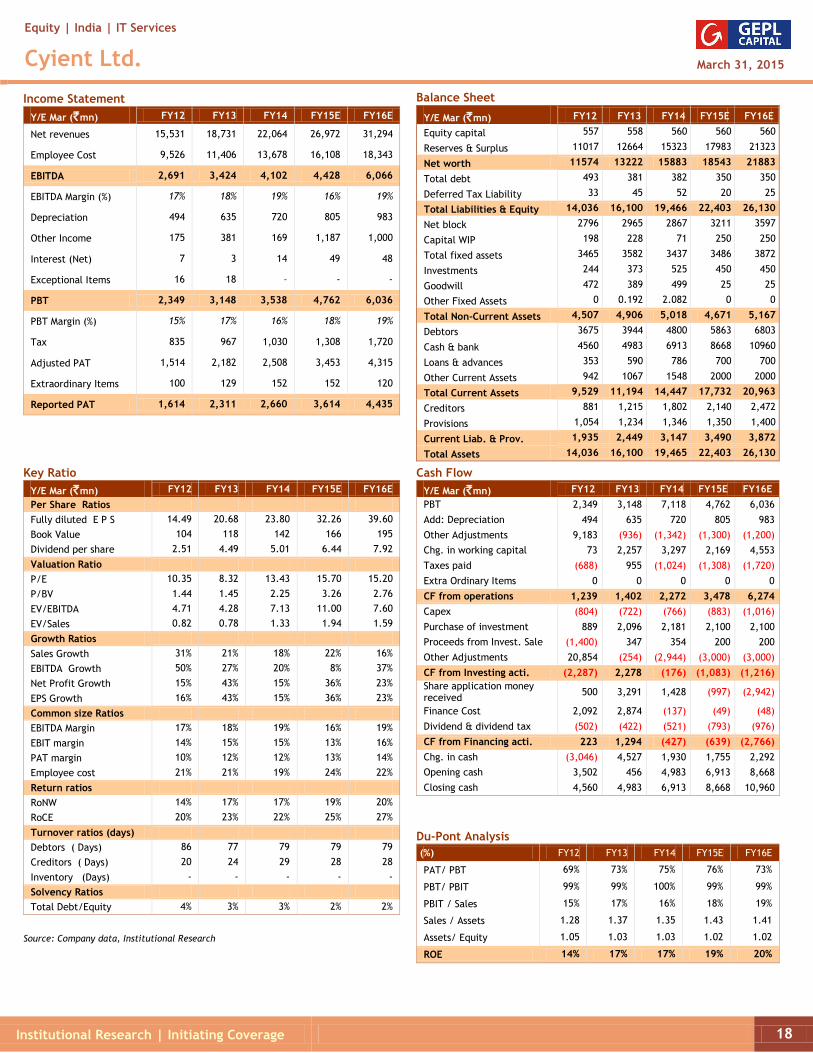

Income Statement

Y/E Mar (`mn) FY12 FY13 FY14 FY15E FY16E

Net revenues 15,531 18,731 22,064 26,972 31,294

Employee Cost 9,526 11,406 13,678 16,108 18,343

EBITDA 2,691 3,424 4,102 4,428 6,066

EBITDA Margin (%) 17% 18% 19% 16% 19%

Depreciation 494 635 720 805 983

Other Income 175 381 169 1,187 1,000

Interest (Net) 7 3 14 49 48

Exceptional Items 16 18 - - -

PBT 2,349 3,148 3,538 4,762 6,036

PBT Margin (%) 15% 17% 16% 18% 19%

Tax 835 967 1,030 1,308 1,720

Adjusted PAT 1,514 2,182 2,508 3,453 4,315

Extraordinary Items 100 129 152 152 120

Reported PAT 1,614 2,311 2,660 3,614 4,435

Balance Sheet

Y/E Mar (`mn) FY12 FY13 FY14 FY15E FY16E

Equity capital 557 558 560 560 560

Reserves & Surplus 11017 12664 15323 17983 21323

Net worth 11574 13222 15883 18543 21883

Total debt 493 381 382 350 350

Deferred Tax Liability 33 45 52 20 25

Total Liabilities & Equity 14,036 16,100 19,466 22,403 26,130

Net block 2796 2965 2867 3211 3597

Capital WIP 198 228 71 250 250

Total fixed assets 3465 3582 3437 3486 3872

Investments 244 373 525 450 450

Goodwill 472 389 499 25 25

Other Fixed Assets 0 0.192 2.082 0 0

Total Non-Current Assets 4,507 4,906 5,018 4,671 5,167

Debtors 3675 3944 4800 5863 6803

Cash & bank 4560 4983 6913 8668 10960

Loans & advances 353 590 786 700 700

Other Current Assets 942 1067 1548 2000 2000

Total Current Assets 9,529 11,194 14,447 17,732 20,963

Creditors 881 1,215 1,802 2,140 2,472

Provisions 1,054 1,234 1,346 1,350 1,400

Current Liab. & Prov. 1,935 2,449 3,147 3,490 3,872

Total Assets 14,036 16,100 19,465 22,403 26,130

Key Ratio

Y/E Mar (`mn) FY12 FY13 FY14 FY15E FY16E

Per Share Ratios

Fully diluted E P S 14.49 20.68 23.80 32.26 39.60

Book Value 104 118 142 166 195

Dividend per share 2.51 4.49 5.01 6.44 7.92

Valuation Ratio

P/E 10.35 8.32 13.43 15.70 15.20

P/BV 1.44 1.45 2.25 3.26 2.76

EV/EBITDA 4.71 4.28 7.13 11.00 7.60

EV/Sales 0.82 0.78 1.33 1.94 1.59

Growth Ratios

Sales Growth 31% 21% 18% 22% 16%

EBITDA Growth 50% 27% 20% 8% 37%

Net Profit Growth 15% 43% 15% 36% 23%

EPS Growth 16% 43% 15% 36% 23%

Common size Ratios

EBITDA Margin 17% 18% 19% 16% 19%

EBIT margin 14% 15% 15% 13% 16%

PAT margin 10% 12% 12% 13% 14%

Employee cost 21% 21% 19% 24% 22%

Return ratios

RoNW 14% 17% 17% 19% 20%

RoCE 20% 23% 22% 25% 27%

Turnover ratios (days)

Debtors ( Days) 86 77 79 79 79

Creditors ( Days) 20 24 29 28 28

Inventory (Days) - - - - -

Solvency Ratios

Total Debt/Equity 4% 3% 3% 2% 2%

Source: Company data, Institutional Research

Cash Flow

Y/E Mar (`mn) FY12 FY13 FY14 FY15E FY16E

PBT 2,349 3,148 7,118 4,762 6,036

Add: Depreciation 494 635 720 805 983

Other Adjustments 9,183 (936) (1,342) (1,300) (1,200)

Chg. in working capital 73 2,257 3,297 2,169 4,553

Taxes paid (688) 955 (1,024) (1,308) (1,720)

Extra Ordinary Items 0 0 0 0 0

CF from operations 1,239 1,402 2,272 3,478 6,274

Capex (804) (722) (766) (883) (1,016)

Purchase of investment 889 2,096 2,181 2,100 2,100

Proceeds from Invest. Sale (1,400) 347 354 200 200

Other Adjustments 20,854 (254) (2,944) (3,000) (3,000)

CF from Investing acti. (2,287) 2,278 (176) (1,083) (1,216)

Share application money received

500 3,291 1,428 (997) (2,942)

Finance Cost 2,092 2,874 (137) (49) (48)

Dividend & dividend tax (502) (422) (521) (793) (976)

CF from Financing acti. 223 1,294 (427) (639) (2,766)

Chg. in cash (3,046) 4,527 1,930 1,755 2,292

Opening cash 3,502 456 4,983 6,913 8,668

Closing cash 4,560 4,983 6,913 8,668 10,960

Du-Pont Analysis

(%) FY12 FY13 FY14 FY15E FY16E

PAT/ PBT 69% 73% 75% 76% 73%

PBT/ PBIT 99% 99% 100% 99% 99%

PBIT / Sales 15% 17% 16% 18% 19%

Sales / Assets 1.28 1.37 1.35 1.43 1.41

Assets/ Equity 1.05 1.03 1.03 1.02 1.02

ROE 14% 17% 17% 19% 20%

Equity | India | IT Services

Cyient Ltd. March 31, 2015

BUY

Institutional Research | Initiating Coverage 19

NOTES

Recommendation Rationale

Recommendation Expected Absolute Return (%) over 12 months

BUY >15%

ACCUMULATE <10% and >15%

NEUTRAL <-10% and <10%

REDUCE >-10% and <-20%

SELL >-10

Expected absolute returns are based on share price at market close unless otherwise stated. Stock recommendations are based on absolute upside (downside) and have a 12-month

horizon. Our target price represents the fair value of the stock based upon the analyst’s discretion. We note that future price fluctuations could lead to a temporary mismatch

between upside/downside for stock and our recommendation.

GEPL CAPITAL Pvt Ltd

Reg Office: D-21 Dhanraj mahal, CSM Marg, Colaba, Mumbai 400001

Analyst Certification

The following analysts hereby certify that their views about the companies and their securities discussed in this report are accurately expressed and that they have not received and will not receive direct or

indirect compensation in exchange for expressing specific recommendations or views in this report:

Name : Omkar Tanksale

Sector : IT Services

Disclaimer:

This report has been prepared by GEPL Capital Private Limited ("GEPL Capital "). GEPL Capital is regulated by the Securities and Exchange Board of India. This report does not constitute a prospectus, offering

circular or offering memorandum and is not an offer or invitation to buy or sell any securities, nor shall part, or all, of this presentation form the basis of, or be relied on in connection with, any contract or

investment decision in relation to any securities. This report is for distribution only under such circumstances as may be permitted by applicable law. Nothing in this report constitutes a representation that any

investment strategy, recommendation or any other content contained herein is suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation. All

investments involve risks and investors should exercise prudence in making their investment decisions. The report should not be regarded by the recipients as a substitute for the exercise of their own judgment.

Any opinions expressed in this report are subject to change without notice and may differ or be contrary to opinions expressed by other business areas or groups of GEPL Capital as a result of using different

assumptions and criteria. GEPL Capital is under no obligation to update or keep current the information contained herein. The securities described herein may not be eligible for sale in all jurisdictions or to

certain categories of investors. Options, derivative products and futures are not suitable for all investors, and trading in these instruments is considered risky. Past performance is not necessarily indicative of

future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related instrument mentioned in this report.

Any prices stated in this report are for information purposes only and do not represent valuations for individual securities or other instruments. There is no representation that any transaction can or could have

been effected at those prices and any prices do not necessarily reflect GEPL Capital’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different

assumptions, by GEPL Capital or any other source may yield substantially different results. GEPL Capital makes no representation or warranty, express or implied, as to, and does not accept any responsibility or

liability with respect to, the fairness, accuracy, completeness or correctness of any information or opinions contained herein. Further, GEPL Capital assumes no responsibility to publicly amend, modify or revise

any forward-looking statements, on the basis of any subsequent development, information or events, or otherwise. Neither GEPL Capital nor any of its affiliates, directors, employees or agents accepts any

liability for any loss or damage arising out of the use of all or any part of this report. In no event shall GEPL capital be liable for any direct, special indirect or consequential damages, or any other damages of

any kind, including but not limited to loss of use, loss of profits, or loss of data, whether in an action in contract, tort (including but not limited to negligence), or otherwise, arising out of or in any way

connected with the use of this report or the materials contained in, or accessed through, this report.

GEPL Capital and its affiliates and/or their officers, directors and employees may have similar or an opposite positions in any securities mentioned in this document (or in any related investment) and may from

time to time add to or dispose of any such securities (or investment). The disclosures contained in the reports produced by GEPL Capital shall be strictly governed by and construed in accordance with Indian

law. GEPL Capital specifically prohibits the redistribution of this material in whole or in part without the written permission of GEPL Capital and GEPL Capital accepts no liability whatsoever for the actions of

third parties in this regard.