equity & debt strategy - kotak.com · us imposes tariff us hikes fed rate by 25 bps ... 12%...

TRANSCRIPT

Equity & Debt Strategy

Mid Apr – May’ 2018

Equity Market Update &

Equity MF Strategy

Confidential | 3

Equity markets corrected in Mar on global cues and selling pressure in Mutual Funds due to Dividend payouts

18,000

18,500

19,000

19,500

20,000

20,500

21,000

21,500

22,000

9,800

9,900

10,000

10,100

10,200

10,300

10,400

10,500

02-Mar-18 08-Mar-18 14-Mar-18 20-Mar-18 26-Mar-18 01-Apr-18

NIFTY Index Nsemcap index

US imposes tariff

US hikes Fed

rate by 25 bps

-6,663

13,254

-12,552

12,272

1,586

-7,131

1,651

-228

6,1827,540

16,257

4,973

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

Dec 17 Jan 18 Feb 18 Mar 18

FII DII excl MF MF

Nifty 50 and Midcap 100 corrected by 3.6% and 4.6% in

March on global cues

FII selling was concentrated in Derivatives market, MF flow

was subdued

March net inflow was lower due to higher redemptions in

both Pure Equity and Balanced funds possibly due to

Dividend payouts

Source: Bloomberg, Kotak Institutional Equities (KIE)As of 5th Apr 2018

cr

Flows to Equity Mutual Funds fell significantly in Mar 2018

cr

22,52820,372 19,535

11,047

0

5,000

10,000

15,000

20,000

25,000

Dec 17 Jan 18 Feb 18 Mar 18

Net investment in Cash market

0

10,000

20,000

30,000

40,000

50,000

Dec 17 Jan 18 Feb 18 Mar 18

Pure Equity Inflow Balanced Inflow

Pure Equity Redemption Balanced Redemption

Confidential | 4

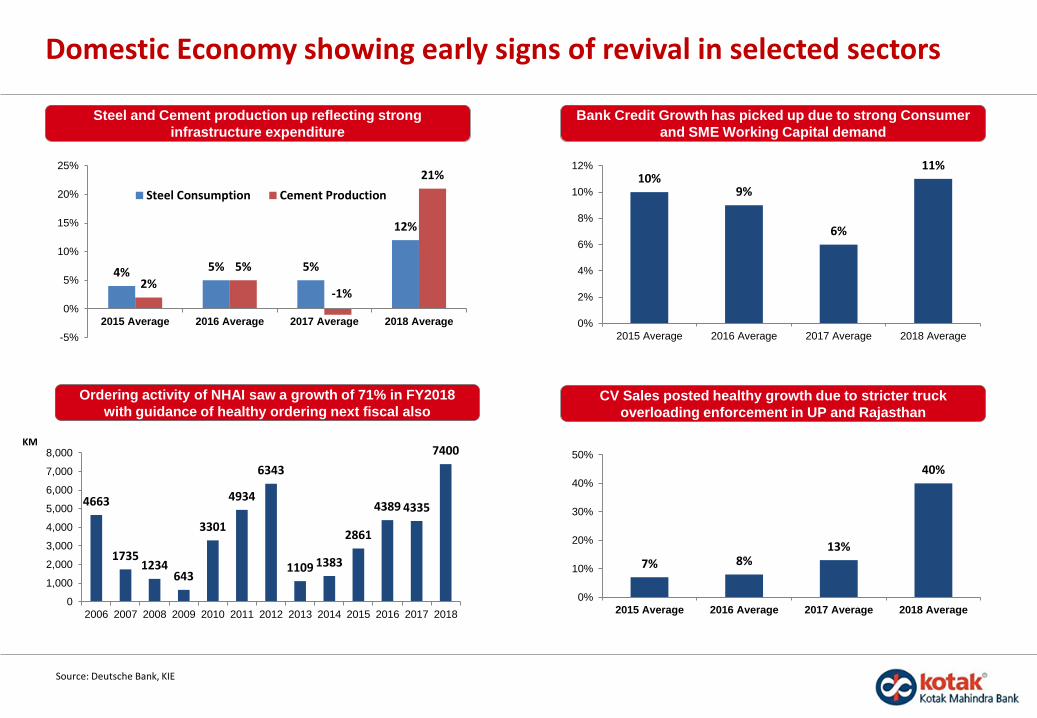

4% 5% 5%

12%

2%

5%

-1%

21%

-5%

0%

5%

10%

15%

20%

25%

2015 Average 2016 Average 2017 Average 2018 Average

Steel Consumption Cement Production

10%9%

6%

11%

0%

2%

4%

6%

8%

10%

12%

2015 Average 2016 Average 2017 Average 2018 Average

Steel and Cement production up reflecting strong

infrastructure expenditure

Bank Credit Growth has picked up due to strong Consumer

and SME Working Capital demand

Ordering activity of NHAI saw a growth of 71% in FY2018

with guidance of healthy ordering next fiscal alsoCV Sales posted healthy growth due to stricter truck

overloading enforcement in UP and Rajasthan

Source: Deutsche Bank, KIE

Domestic Economy showing early signs of revival in selected sectors

KM

7% 8%13%

40%

0%

10%

20%

30%

40%

50%

2015 Average 2016 Average 2017 Average 2018 Average

4663

17351234

643

3301

4934

6343

1109 1383

2861

4389 4335

7400

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Confidential | 5

However favorable Liquidity scenario could reverse in 2018

India has been receiving major inflows from passive GEM ETFs

which could reverse on negative sentiment over EM in trade

war environment

Libor – OIS spread, a measure of credit risk, is at highest level

in last decade due to US Tax reforms

QE Unwind program has resulted in asset drop of $74 billion

resulting in lowest level of “Fed Balance Sheet” since 2014

Source: DB,Bloomberg, CLSA

0%

10%

20%

30%

40%

50%

60%

70%

Jan14

Apr14

Jul14

Oct14

Jan15

Apr15

Jul15

Oct15

Jan16

Apr16

Jul16

Oct16

Jan17

Apr17

Jul17

Oct17

Jan18

FII will continue to play an important role as domestic liquidity

will be sucked by IPOs and disinvestments by Govt

2

9.25

4.756.5

8.5

1.52.5

2.527.5

Ne

t D

om

estic

Institu

iton

al

Flo

w

Oth

er

QIP

PS

U B

ank

QIPIP

Os

Dis

investm

ent

by G

ovt

Div

iden

ds

Paid

by M

F

Insura

nce N

et

Flo

w

EP

FO

, N

PS

an

d o

ther

ET

Fs

Do

me

stic M

FIn

flow

4,250,000

4,300,000

4,350,000

4,400,000

4,450,000

4,500,000

4,550,000

Jun

14

Au

g 1

4

Oct 14

Dec 1

4

Fe

b 1

5

Ap

r 15

Jun

15

Au

g 1

5

Oct 15

Dec 1

5

Fe

b 1

6

Ap

r 16

Jun

16

Au

g 1

6

Oct 16

Dec 1

6

Fe

b 1

7

Ap

r 17

Jun

17

Au

g 1

7

Oct 17

Dec 1

7

Fe

b 1

8

USD bn

11%

2% 2%

-1%

2%

-2%

0%

2%

4%

6%

8%

10%

12%

GEM ETFs Others GEM Non ETF India ETF India Non ETF

Inflow in last 6 Months/ AUM

$ Mn

Confidential | 6

Market still remain overvalued compared to historic valuations, EPS growth coming from Auto, Metals and Banking

Mid Cap Index premium over large cap has been maintained in the correction so far

Q4 2018 Sensex PAT (KIE) is expected to increase by 10% yoy backed by Auto, Consumer, Infra, Metals and NBFCs

Consensus Earnings expectation of FY 2019 has been relatively stable compared to previous Fiscals

Infra looks attractive in terms of valuation, >40% of incremental profit expected from Banks due to lower provisions

17.0 19.5

36.9

11.316.0

22.517.3 17.0

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Au

to

Ban

kin

g

Co

nsu

mer

s

Ene

rgy

Infr

a

Ph

arm

a

Tech

Nif

ty 5

0

PE 2019E Average Earnings Growth FY19E

17.2

21.0

15.616.9

0.0

5.0

10.0

15.0

20.0

25.0

Large Cap Mid Cap

Current 12M Forward PE 5 Year Median

22% Premium vs 8% AverageBloomberg Estimate

400.00

450.00

500.00

550.00

600.00

650.00

700.00

Apr 15Jul 15Oct 15Jan 16Apr 16Jul 16Oct 16Jan 17Apr 17Jul 17Oct 17Jan 18

FY 2019 FY2018 FY2017

14.010.9

14.3 18.8

3.1

37.0

-22.5

-0.2 2.3

9.7

(30.0)

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

Au

to

Ban

ks

Co

nsu

me

r

Ene

rgy

Ind

ust

rial

s

Me

tals

Ph

arm

a

Tech

Uti

litie

s

Sen

sex

Source: Bloomberg, KIE

Confidential | 7

Key Triggers – Resolution of NPA & Earnings

• Global Economic data : World economy improving

• Commodity Prices: Sustained high prices is expected to lead to high earnings growth in Steel/Oil sector

• Resolution of NPA: Effective addressal by government of NPA issue in Indian Banks, initial bids for NCLT List 1 has been promising

• Weaker Rupee: Benefit IT and Pharma

• Rural recovery: Government focus on rural economy including increase of MSP could benefit rural consumption

Positive Triggers

• Outflow from EM: US tax reforms and rising global rates could trigger capital flight from Emerging markets like India

• Earnings: Consensus expected earnings growth for domestic equities is high at around 25% for FY19, any downgrade would make the valuations more expensive

• Geo-Political Risk: Further tariffs imposed by US/China

• Monetary Policy: Faster than expected monetary tightening in Europe and US

• Weaker Macro: Higher crude prices and low GST collection could lead to lower re-rating of Equity valuations

• Tight Credit and Higher NPA: Recent PNB event could lead to cascading effect in the whole banking system

• Slowdown in Retail Flows: Redemption pressure in retail possible post 10% LTCG and 10-15% correction in markets

• State Elections: Elections in Rajasthan and Karnataka are expected to be tight for NDA

Risks

Confidential | 8

India Equities: Valuations & Strategy – Maintain Neutral Stance

Indian markets lost ~4% for the month of March on account of weakness in markets worldwide. The financial year FY17-18 endedwith a gain of 10.2% as against 18.5% for the previous FY. FII flows into equity markets turned positive with a net investment ofINR 12,272 cr from negative last month.

At current levels of approx. 10,481 (13th April, 2018), Nifty is trading at a 1 year forward PE of 18.5X. In the current scenario, wecontinue to maintain a Neutral stance on the back of healthy earnings growth expectations..

Mutual Funds: As domestic liquidity continues to drive markets, we advise new investments in Mutual Funds to be deployed 25%in lumpsum and subsequent in tranches via SIPs/STPs.

Recommended allocation within equity mutual funds is as under:

• 50% Large Cap allocation (Prefer Large Caps due to relatively Favorable Valuations)

• 50% Multi Cap allocation (such funds currently have a bias toward large cap)

• For investors who want equity exposure but have low appetite for volatility, they can take equity exposure through

Balanced Funds. Balanced funds have around 25% to 30% of their portfolio into Debt instruments which provides cushion

to the portfolio return during market volatility.

Source: EPS Estimates by KIE

Debt Market Update &

Debt MF Strategy

Confidential | 10

Indicators

Policy Action

• No rate action as expected in Apr policy

• We expect repo rate to be unchanged for extended

period of time

• Tone was softer and carried focus on upward risks to

inflation

Inflation

• CPI was lower than expectation at 4.28% in March 2018

• RBI lowered expectation of 4QFY18 to 4.5% and

1HFY19 to 4.7-5.1%

• We expect CPI averaging around 4.3% for FY2019

10 Year G-Sec Benchmark Yield

• Short term triggers like favorable Gsec supply,

favorable inflation Prints and expectation of hike in FII

could sustain rally

Liquidity

• Liquidity has gone to deficit from surplus due to tax payments

• RBI has reaffirmed their objective of maintaining a neutral

level

INR

• Concerns over LOU limits and CAD put pressure

on INR

• Expect mild depreciation towards 65.5 over 1 Year

• Broad range of 63-66 to hold

Key Risks

• Global monetary tightening

• Crude Prices

• Impact of GST revenues and spending on Fiscal Deficit

• Growth Recovery

G-Sec Supply

• Government announced to borrow INR 2.88 trn of

bonds in H1FY19, lower by 50k cr compensated by

lower buybacks and higher small savings

• Issuance in medium term segment of 10-14 years was

reduced to 29% against 50% in previous years

• A hike in FII limit and/or support from RBI in form of

OMO purchase could further improve the Supply-

Demand dynamics

Debt Market: Key Variables

Confidential | 11

Yields relaxed by 30-60 bps over positive news from inflation print, Borrowing announcement and RBI policy meet

-575

-2,000

-1,000

0

1,000

1-Mar 6-Mar 11-Mar 16-Mar 21-Mar 26-Mar 31-Mar

Am

ou

nt

in R

s. B

n 113

7.13

6.00

020406080100120140160180200

5.75

6.25

6.75

7.25

7.75

Spre

ad (

bp

s)

% Y

ield

Spread 10 Year G Sec Repo Rate

G Sec Spread over Repo has fallen from peak of 170 bps

to 113 bps

-30-23

-29-33

-36-43

-55

7.13

7.68

-70

-60

-50

-40

-30

-20

-10

0

6.00

6.40

6.80

7.20

7.60

8.00

8.40

1Y 2Y 3Y 4Y 5Y 8Y 10Y

Sp

read

(b

ps

)

% Y

ield

Change Current G-Sec Yield 1M earlier G-Sec Yield

10 Year papers rallied the most due to lower gross supply

announcement

Liquidity gone to deficit level before Fiscal end

Inflation for March 2018 was lower than expected

however Core inflation of 5% warrants caution

Note: As of 5th Apr 2018, Source Bloomberg

4.28%

5.20%

May17

Jun17

Jul17

Aug17

Sep17

Oct17

Nov17

Dec17

Jan18

Feb18

Mar18

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

CPI Core Inflation

Confidential | 12

Decision to increase FII limit could lend support to Bond market and INR

Jul 17 Aug 17 Sep 17 Oct 17 Nov 17 Dec 17 Jan 18 Feb 18 Mar 18

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

US

D M

illi

on

FIIs buying slowing down due to rising global rates

and high utilization levels

64.84

May17

Jun17

Jul17

Aug17

Sep17

Oct17

Nov17

Dec17

Jan18

Feb18

Mar18

Apr18

63.00

63.50

64.00

64.50

65.00

65.50

66.00

Indian currency has depreciated on sustained dollar

demand due to demand from importers and FII

outflow from Equity

Fed expects 5 rate hikes in 2018, ~3.5% rate till 2020

Jul 17 Aug 17 Sep 17 Oct 17 Nov 17 Dec 17 Jan 18 Feb 18

740

760

780

800

820

840

860

880

900

920

940

GST collections running below target rate of 1.1

Trillion Rs/month

Note: As of 5th Apr 2018, Source Bloomberg

o

4

o

3.75

oo

3.5 o o

ooo ooooo

3.25 o o

oo o

3 ooooo

ooooo

2.75 o oooo

o o oo o

2.5 o

oooooo

2.25 o

oooooo o

2

1.75

oo O o

1.5

2018 2019 2020 Long Term

The Fed’s Dot Plot chart: Dots represents number of members voting. The chart represents where each participant thinks the Fed rate should be in the next few years.

Fed

Rat

e

Confidential | 13

Debt Market Trends

165.00

170.00

175.00

180.00

185.00

190.00

195.00

200.00

205.00

210.00

215.00

220.00

Sep 17 Oct 17 Nov 17 Dec 17 Jan 18 Feb 18 Mar 18 Apr 18

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

3 Year AAA 5 Year AAA SDL Credit RHS

Government Yields rallied more than Corporate papers

last monthFY19 Central Government Borrowing has been reduced by 50,000

cr, duration mix and H1 supply favorable for 10 Year paper

6.24

0.25

0.25

0.5

6.24

FY19 FiscalDeficit

Higher SmallSavings

Borrowing

Lower BondBuy Back

Lower GrossBorrowing

FY19 FiscalDeficit

6

6.25

6.5

6.75

7

1.9

2.5 2.62.8

3.12.9

2.6

FY13 FY14 FY15 FY16 FY17 FY18RE FY19BE

0

0.5

1

1.5

2

2.5

3

3.5

Due to better than expected Cess & stamp duty collection

and low expenditure growth, State FD is expected to

reduce this year

Spread over 10 Year GSec

Note: As of 3rd Apr 2018, Source Bloomberg, MFI

% of GDP

Rs lk cr

6.20

6.40

6.60

6.80

7.00

7.20

7.40

7.60

7.80

8.00

8.20

8.40

Jul 17 Aug 17 Sep 17 Oct 17 Nov 17 Dec 17 Jan 18 Feb 18 Mar 18

0.00

50.00

100.00

150.00

200.00

250.001 Year CP RHS

Spread of 1 Year CP over 1 Month CD has reduced but

still at attractive levels

Confidential | 14

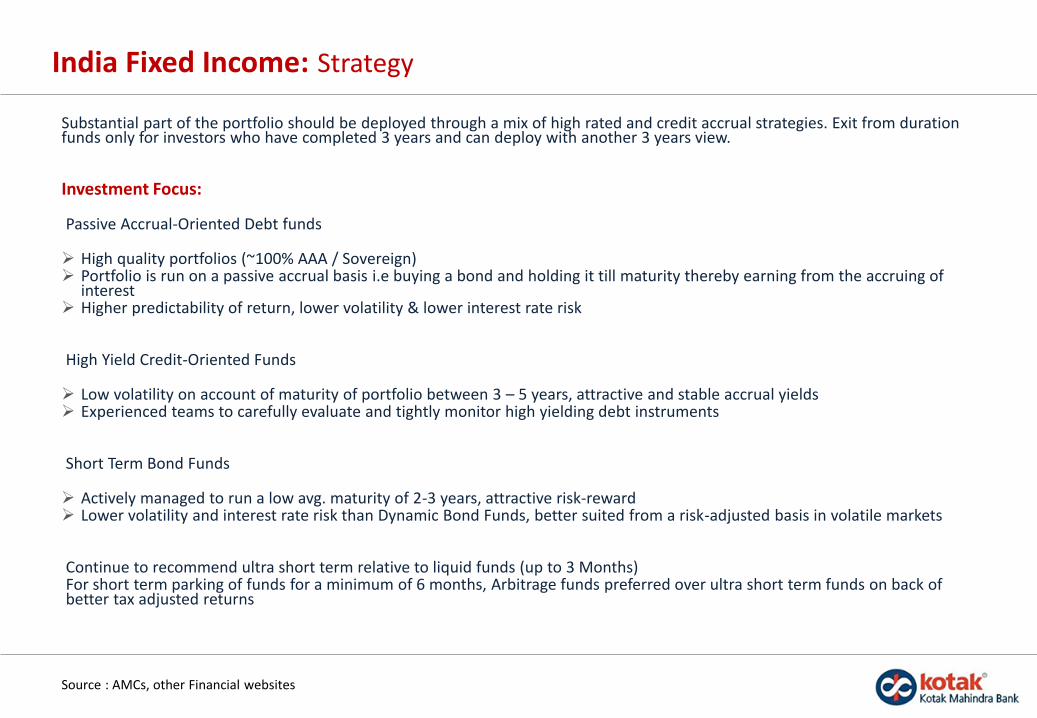

India Fixed Income: Strategy

Substantial part of the portfolio should be deployed through a mix of high rated and credit accrual strategies. Exit from duration funds only for investors who have completed 3 years and can deploy with another 3 years view.

Investment Focus:

Passive Accrual-Oriented Debt funds

High quality portfolios (~100% AAA / Sovereign) Portfolio is run on a passive accrual basis i.e buying a bond and holding it till maturity thereby earning from the accruing of

interest Higher predictability of return, lower volatility & lower interest rate risk

High Yield Credit-Oriented Funds

Low volatility on account of maturity of portfolio between 3 – 5 years, attractive and stable accrual yields Experienced teams to carefully evaluate and tightly monitor high yielding debt instruments

Short Term Bond Funds

Actively managed to run a low avg. maturity of 2-3 years, attractive risk-reward Lower volatility and interest rate risk than Dynamic Bond Funds, better suited from a risk-adjusted basis in volatile markets

Continue to recommend ultra short term relative to liquid funds (up to 3 Months)For short term parking of funds for a minimum of 6 months, Arbitrage funds preferred over ultra short term funds on back of better tax adjusted returns

Source : AMCs, other Financial websites

Confidential | 15

DisclaimerThe aforesaid is for information purposes only and should not be construed to be investment advice under SEBI (Investment Advisory) Regulations.

In the preparation of the material contained in this document, Kotak Mahindra Bank has used information that is publicly available, including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the Kotak Mahindra Bank and/or its affiliates and which mayhave been made available to Kotak Mahindra Bank and/or its affiliates. Information gathered & material used in this document is believed to be from reliable sources. KotakMahindra Bank however does not warrant the accuracy, reasonableness and/or completeness of any information. For data reference to any third party in this material nosuch party will assume any liability for the same. Kotak Mahindra Bank and/or any affiliate of Kotak Mahindra Bank does not in any way through this material solicit any offerfor purchase, sale or any financial transaction/commodities/products of any financial instrument dealt in this material. All recipients of this material should before dealingand or transacting in any of the products referred to in this material make their own investigation, seek appropriate professional advice

We have included statements/opinions/recommendations in this document which contain words or phrases such as "will", "expect" "should" and similar expressions orvariations of such expressions, that are "forward looking statements". Actual results may differ materially from those suggested by the forward looking statements due torisks or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India andother countries globally, which have an impact on our services and / or investments, the monetary and interest policies of India, inflation, deflation, unanticipatedturbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes indomestic and foreign laws, regulations and taxes and changes in competition in the industry. By their nature, certain market risk disclosures are only estimates and could bematerially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated

Kotak Mahindra Bank (including its affiliates) and any of its officers directors, personnel and employees, shall not liable for any loss, damage of any nature, including but notlimited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. The recipientalone shall be fully responsible/ are liable for any decision taken on the basis of this material. The investments discussed in this material may not be suitable for all investors.Any person subscribing to or investing in any product/financial instruments should do so on the basis of and after verifying the terms attached to such product/financialinstrument. Financial products and instruments are subject to market risks and yields may fluctuate depending on various factors affecting capital/debt markets. Please notethat past performance of the financial products and instruments does not necessarily indicate the future prospects and performance thereof. Such past performance mayormay not be sustained in future. Kotak Mahindra Bank (including its affiliates) or its officers, directors, personnel and employees, including persons involved in thepreparation or issuance of this material may; (a) from time to time, have long or short positions in, and buy or sell the securities mentioned herein or (b) be engaged in anyother transaction involving such securities and earn brokerage or other compensation in the financial instruments/products/commodities discussed herein or act as advisoror lender / borrower in respect of such securities/financial instruments/products/commodities or have other potential conflict of interest with respect to anyrecommendation and related information and opinions. The said persons may have acted upon and/or in a manner contradictory with the information contained here. Nopart of this material may be duplicated in whole or in part in any form and or redistributed without the prior written consent of Kotak Mahindra Bank. This material is strictlyconfidential to the recipient and should not be reproduced or disseminated to anyone else

This material is not a research report as per the SEBI (Research Analyst) Regulations, 2014.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.