entry threat and entry delay: the timing of the u.s. … · 2018-05-31 · o ers the opportunity to...

TRANSCRIPT

Entry Threat and Entry Delay: The Timing of the U.S. Broadband

Rollout

Kyle Wilson1, Mo Xiao1, and Peter F. Orazem2

1University of Arizona

2Iowa State University

Abstract

In a rapidly growing industry, does a potential entrant speed up or delay its entry into a

local market when facing the threat of additional entrants? Do strategic entry decisions affect

market conditions in the long run? To study this, we investigate the evolution of the market

structure of high-speed Internet service providers from 1999 to 2007 using zip-code level data

on the reported number of providers. Furthermore, we assess the impact of the entry decisions

made during early rollout on modern-day broadband speeds using data on advertised internet

speeds. We identify a potential entrant into a local market as threatened when a neighboring

market houses at least one additional firm. We argue that the potential entrant believes the

threat of additional entry to be credible because scale economies allow firms to spill over into

adjacent markets. Allowing for spatial correlation across markets, we devise an instrumental

variable approach to deal with the problem of endogenous market structure in the neighboring

markets. We find that potential entrants into open markets are significantly less likely to enter

when facing the threat of additional entry, suggesting that firms are deterred by the negative

impact of a competitive marketplace on future profitability. Specifically, we find that on average,

it takes 3 years longer for threatened local markets to experience their first broadband entrant.

Moreover, this entry delay has long-run negative implications for the divergence of the U.S.

broadband infrastructure: one year of entry delay translates into an 11% decrease in average

present-day download speeds.

1

1 Introduction

A firm which enters a new market has projected that its future profits will be greater than the

cost of entry. In forming its expectation over future profits, the firm must anticipate the actions

of potential future rivals in the market. There is an established literature on how incumbent firms

respond to the threat of rivals’ future entry. It is then natural to back up one step to ask: before

entering a market, do potential entrants consider the possiblity of future entry of competitors and

adjust their entry strategies accordingly? If so, this may explain why firms at times appear to

delay entry into seemingly attractive markets. To our knowledge, this angle has not been explored

empirically, largely due to the difficulty of determining which markets face credible entry threats.

In this paper, we investigate this strategic entry behavior in the context of the initial rollout

of broadband internet in the United States during the early 2000s. We propose that this setting

offers the opportunity to identify markets which face a credible threat of entry. The Federal

Communications Commission (FCC) reports bi-annual data on the evolution of the market structure

of facilities-based broadband providers at the zip code level. In examining the data, we can identify a

potential entrant as threatened when a neighboring market houses additional providers of broadband

internet service. We then use the timing of entry into the market to understand how a firm’s entry

strategy is affected by the threat of future competition. Furthermore, we investigate whether

this early entry delay has long-run implications for the current state of the industry. Specifically,

we estimate the extent to which delayed initial entry into a market affects the download speeds

available there in 2013.

The empirical strategy we adopt is as follows: we construct a latent variable representation of a

market’s profitability, as a function of observable market characteristics which affect demand and

costs, and critically, whether or not a market is threatened by future entry. We then estimate the

effect of entry threat on the probability of entry into a market, and on the length of time elapsed

until a market is eventually entered. We then follow a similar approach to estimate the effect of

the number of years of entry delay on the download speeds available in a market in 2013.

Within this framework, we recognize that whether or not a market is threatened is determined

by previous entry into neighboring markets. Therefore, if characteristics of neighboring markets

which induced entry there are correlated with unobservable characteristics in the market at hand,

2

then entry threat is not exogenous. We address this by allowing markets close to one another to

have spatially correlated error terms. We then estimate the extent of this spatial correlation in a

generalized method of moments (GMM) framework developed by Pinkse and Slade (1998).

Additionally, if, as we claim, a prospective entrant into a market considers the market structure

of neighboring markets when making its entry decision, then it must be true that incumbents in

neighboring markets have engaged in a parallel exercise which incorporates their expectations about

entry into the market at hand. Therefore, the presence of incumbent firms in neighboring markets,

which serves as our indicator of entry threat, is an endogenous variable in a potential entrant’s

decision. To deal with this, we instrument for entry threat using the market attributes of nearby

markets. These attributes affect entry decisions into neighboring markets, and therefore the threat

of entry into the market of interest. At the same time, these attributes are exogenous to a potential

entrant’s decision to enter the market at hand, as they do not affect its profitability directly.

We find evidence that potential entrants place significant consideration on the possibility of

future competition when making their entry decision. First, we demonstrate that our measure

of entry threat is, in fact, credible; threatened markets are 4% more likely to be entered in the

long run. However, in the short run, a market which is threatened by the entry of competitors is

26% less likely to be entered than its un-threatened counterpart. This is a substantial effect, as it

represents the net of two countervailing effects: as we have described, a threatened market may be

less likely to be entered because firms are not likely to maintain market power; but at the same

time, a threatened market, by definition, has firms nearby which can spill over due to economies of

scale. Beyond this, we also show that an open threatened market will, on average, wait three years

longer before being entered.

Furthermore, this delayed entry turns out to have important implications for the long-run

development of broadband infrastructure. We find that for each additional year of delayed initial

entry, the download speeds available in 2013 fall by 11%. Initially, the expected sign of this effect

may appear to be ambiguous. One might imagine that markets which experience their initial entry

later would receive the latest technology, and therefore would have access to faster speeds today.

However, given the rapid pace of improvement in internet speeds, even the prevailing speeds of

2010 are slow and obsolete by current standards. Instead, we argue that markets which experience

delayed entry take longer to mature; they do not exhibit the competitive pressure necessary to spur

3

investment in quality improvements until later than their counterparts which experienced early

entry.

The broadband industry has been plagued by the so-called “digital divide.” Since the advent

of the industry, there has been persistent inequality in Americans’ access to broadband internet

service. Much of this inequality can be explained by socio-economic differences in populations

and by cost differences across regions, but we find that strategic concerns over future competition

further this divide. We provide evidence that even after controlling for factors which influence

demand and costs, firms delay entry into markets which are threatened by future entry of rivals,

and that these delays translate into meaningful differences in the quality of internet access available

today, more than a decade later.

1.1 Literature

This paper adds new evidence to the literature on the effect of entry threat on firms’ conduct. This

literature is largely theoretical, as it is often difficult to credibly measure the threat of future entry.

Spence (1979, 1981) shows that firms have incentives to enter early and invest to deter competition,

and that early entrant advantages are magnified by learning. Milgrom and Roberts (1982) stress

the importance of reputation and asymmetric information in deterring entry. Klemperer (1987)

shows that firms adopt pricing strategies which take advantage of consumers’ cost of switching to

new entrant.

In the empirical literature, Ellison and Ellison (2000) propose that investments should generally

increase monotonically in “market attractiveness”, but that strategic entry deterrence may alter

this; in markets of intermediate attractiveness, investment may deter entry, but is not likely to

have an effect on rivals’ entry decisions in very attractive or unattractive markets. Dafny (2005)

finds evidence of this behavior in the hospital industry. Goolsbee and Syverson (2008) find that

incumbent airlines cut prices dramatically in response to the potential entry of Southwest; in fact,

they find this effect to be larger than their response to the actual entry of Southwest. Seamans

(2012) finds that incumbent cable television providers were more likely to begin offering internet

service in areas where the local government already offered electric service, and therefore might

also provide internet service. We add to this literature by examining the effect of the potential

entry of rivals on a firm’s initial decision to enter a market. In addition, we investigate whether

4

these strategic interactions have long-lasting implications for the state of the industry.

2 The Broadband Internet Market and the Digital Divide

In the United States, internet service is provided predominantly by two types of firms, cable tele-

vision and telephone companies. Cable firms provide broadband service using hybrid fiber-coaxial

cable networks, and telephone companies over digital subscriber lines (DSL). Both types of firms

provide internet service primarily using the lines put in place for their preexisting cable television

and telephone services, respectively, though recent years have seen greater use of fiber-optic cables

by both cable and telephone firms.

The 1996 Telecommunications Act was passed with the goal of encouraging competition in local

telecommunications markets, largely by removing barriers to entry and by requiring incumbent firms

to lease their lines to competitors. The act has been at least partially successful in achieving this

goal, as several papers have investigated strategic interaction among competitors and the welfare

effects of new entry into local telecommunications markets. Greenstein and Mazzeo (2006) found

that telephone firms differentiate themselves strategically when entering markets; Economides,

Seim, and Viard (2006) show that households in the state of New York benefit significantly from

this resulting product differentiation.

As shown in figure 1, the fraction of zip codes with access to at least one broadband provider rose

from 58% to 93% between 1999 and 2007, with most of this growth occurring by 2003. By the end

of 2007, less than half of one percent of the U.S. population did not have broadband service in their

zip code. However, this deployment did not occur evenly across the country. By 2003, zip codes

which did not yet have access to broadband internet, on average, had household incomes which were

about $8,000 less than those with broadband internet; they also had a 9 percentage point lower

rate of college graduation and were far more rural. The U.S. census records the percentage of each

zip code which is considered rural, and markets without broadband in 2003 were, on average, 87%

rural, while those with broadband were only 57% rural.1 While demographic differences explain a

great deal of the disparity in internet availability, the strategic entry decisions of firms may serve

to exacerbate this issue.

1Comparable statements can be made about the set of markets without access to broadband in any particularyear. 2003 is in no way unique is this regard.

5

Figure 1: Fraction of Zip Codes with Broadband Internet

Source: FCC Form 477 Data

2.1 Recent Broadband Quality Improvements: 2010 to 2014

Since its inception, the speeds of household broadband internet connections have continually im-

proved. Cable firms have improved speeds by adopting common standards for data transmission,

known as DOCSIS, the current version of which allows for many channels to be bonded together

and used by a single subscriber. At the same time, cable firms have expanded their use of fiber-optic

cables, which increase the available bandwidth and reduce congestion. Telephone firms have also

deployed fiber-optic cables throughout their networks. This strategy is particular important for

them, as transmitting data at high speeds over long distances using their existing telephone wires

is physically impossible. In some areas, cable and/or telephone firms have constructed networks

which consist exclusively of fiber-optic cables, in what is known as fiber-to-the-premises.

As shown in figure 2, the fraction of zip codes with download speeds of at least 10 megabits

per second (Mbps) increased from 49% to 69% from 2010 to 2014. Over the same period of time,

the fraction of zip codes with download speeds of at least 25 Mbps, the FCC’s current definition of

broadband speeds, rose from 16% to 44%. Finally, the share of zip codes with download speeds of

at least 100 Mbps grew from just 5% to 31%. Similarly to the initial deployment of internet access,

there are significant differences today between markets with and without access to broadband

speeds. Zip codes without access to download speeds of at least 25 Mbps, on average, have $10,000

6

Figure 2: Fraction of Zip Codes with Broadband Speeds

Source: National Broadband Map

lower household incomes, have college graduation rates which are 8 percentage points lower, and

are 34 percentage points more rural. We believe it is important to understand how the early

interactions of firms and the resulting variation in entry delay have helped to shape this behavior.

3 Data and Definitions

Our analysis is based primarily on information from two sources of data compiled by the FCC

and in partnership with the National Telecommunication and Information Administration (NTIA).

The first data set is the Survey of High Speed Internet Providers, collected bi-annually by the FCC

beginning in 1999, and made available from 1999 to 2007. The FCC requires every facilities-based

provider with at least 250 high-speed lines2 to report its presence in a given zip code as long as it

serves at least one customer there. The FCC releases summary statistics to the public aggregated

to the zip code level. From these snapshots of market structure, we can observe the timing of net

entry and exit of broadband providers over six month intervals. In our study, we only use the

2High-speed lines are defined as those that provide speeds exceeding 200 kilobits per second (kbps) in at least onedirection.

7

December data, to allow sufficient time for changes in market structure to occur, and so our net

entry and exit is measured over one year intervals.

This data set, covering the entire United States and spanning multiple time periods, is a rare

opportunity for researchers to study market evolution in the early stages of a rapidly-growing service

industry. However, we must acknowledge that the data has some drawbacks, mainly that it lacks

firm identities. As a result, we can only observe net entry, rather than actual entry and exit of

firms. It also means that our inference of entry threat is derived from observations of the number,

but not the identities, of incumbent providers across markets. We also cannot distinguish between

different types of broadband services such as cable and DSL, and so we cannot measure the different

impacts that entry threat may generate by type of broadband provider. Furthermore, very small

providers (with less than 250 high-speed lines), many of which serve sparsely-populated areas, are

not required to report to the FCC, generating measurement errors in our econometric analysis.3

Lastly, the data combine 1, 2, and 3 providers into a single category, due to confidentiality concerns.

As a result, we focus our analysis on the decision of the first entrant, rather than subsequent entries.

Despite these limitations, the breadth and depth of the data generate interesting inferences about

local firm entry decisions that are not possible from other data sets.

The second data set we use is the source data of the National Broadband Map, collected through

the State Broadband Initiative, a program overseen by the NTIA. This data again covers the entire

United States, and provides information at the census block level every six months from 2010 to

2014. We restrict our attention to the 2013 data, as the outcome of interest is the current state

of the broadband infrastructure.4 The data indicate the identities of each firm in each census

block, along with their technology used and their local maximum advertised download and upload

speeds. Maximum advertised speeds are reported as a discrete variable, whose values represent

ranges of speeds; we replace these values with the median value of the relevant range. In order to

pair this data with the early FCC data, we aggregate observations to the zip code level by taking

a population-weighted average across the blocks within a zip code.

Finally, we use three auxiliary data sets: we use demographic characteristics from the 2000

3Fortunately, few providers fall into this category. Research shows that entry will not pay off unless there are atleast 200 lines in a DSL service area (Paradyne, 2000).

4At the time of the analysis, 2013 was the most current set of data. The results will be updated using the nowavailable 2014 data.

8

Census and the 2010 American Community Survey (ACS), based upon zip code tabulation areas

(ZCTAs).5 The variables selected include population, average income, education, age, ethnicity,

commuting distance, and population density, all of which affect local demand for and/or the cost

of providing internet service. Finally, we use the number of business establishments for each zip

code from the 2000 Zip Code Business Patterns data, which serves as our measure of local business

activity. The descriptions and summary statistics for these variables can be found in section 3.4.

3.1 Market Definition: Zip Code

In any service industry, consumer mobility determines the boundaries of a local market. This

can be quite challenging, as researchers typically do not have good data on consumers’ willingness

to travel for desirable services. The broadband market, however, is unique; consumers have no

mobility at all, as they can only purchase a subscription from providers offering service at their

residence. Therefore, we avoid the problem of blurred market boundaries which has plagued many

studies of market structure.6

Fortunately, the FCC data offer a natural definition for markets, by indicating the number

of firms offering service within each zip code. Since households cannot subscribe to a broadband

provider who does not serve their zip code, this provides us with a very clean local market boundary.

With that said, one might wonder whether broadband providers actually make entry decisions at

such a fine geographic level. They may instead make decisions at the city, county, or even state

level, though it would take years to roll out full coverage to these larger areas. This type of long-run

strategy would not only compromise our market definition, but would also threaten the validity

of our instruments (proposed in section 4.3). Furthermore, the relevant market definition in the

long-run likely varies considerably across firms, and some broadband providers have a national

presence, while others serve only one city.

For these reasons, we focus on the short-run entry decision of firms, the gradual “rolling out”

process of broadband providers. Specifically, we consider a broadband provider’s marginal decision

to expand service to one more local market. Since expanding service to a local market involves sunk

5ZCTAs, defined by the Census Bureau, are not identical to zip codes, which are defined by the U.S. Postal Service.However, all zip codes in the FCC data do have a match in the 2000 Census data.

6Complete consumer immobility does have the potential to create a problem of its own. If we define a local marketto be too large, a provider within the market may not actually offer service to all households.

9

costs, we can define the boundaries of the market by the nature of those costs. In the broadband

industry, these sunk costs are the costs of deploying the so-called “last mile” of infrastructure. Firms

must lay or renovate coaxial cables and telephone wires, as well as build or modify switching and

distribution centers, cable television head ends, and DSL access multiplexers. The distance between

an end-user and a broadband provider is a primary factor in determining which neighborhoods can

be served, particularly for telephone providers. This physical constraint limits the radius of a local

market, as DSL can be provided reliably within a radius of about 3.4 miles from the firm’s central

office. This again suggests that zip codes are the appropriate geographic approximation of a local

broadband market, as the typical zip code has a radius of between 3 and 4 miles, according to the

2000 U.S. Census.

The National Broadband Map data is made available at the firm-census block level, which is

much finer than our market definition. Therefore, in order to match the two data sets together,

we must aggregate the National Broadband Map data to the zip code level. We do this by taking

the population-weighted average number of firms in each block within a zip code. To construct a

zip code-level measure of download speeds, for each census block, we take the maximum download

speed among all firms present, and we average these speeds over all blocks within a zip code.

3.2 Neighboring Market Definition

Our data indicates the latitude and longitude of the centroid of each zip code in the United States.

The distance between the centroids of two zip codes forms the basis of our definition of neighboring

markets. However, this distance alone ignores the geographic sizes of the zip codes; in fact, two

large zip codes could border one another but have centroids which are far apart. In order to address

this issue, we assume that all zip codes are circular and calculate their radius as follows:

rm =

√aream3.14

(1)

10

where rm is the radius of market m and aream is the geographic area of market m. We then define

market m and market m′ to be neighbors according to the following definition:

neighborsm,m′ =

1 if distancem,m′ ≤ 3 + maxrm, rm′

0 otherwise

(2)

where distancem,m′ is the distance between the centroids of markets m and m′. Put more simply, we

define two markets to be neighbors if the distance from the centroid of one market to the boundary

of the other is less than 3 miles. The choice of 3 miles is somewhat arbitrary, but supported by

the physical limitations of DSL technology. A telephone provider with a central office located at

the centroid of market m could feasibly serve market m′ if the boundary of market m′ was within

about 3 miles of the centroid of market m, as noted in the previous section.7

3.3 Sample Selection

The FCC’s Survey of High Speed Internet Service Providers contains deployment data on the

universe of the 31,862 zip codes in the United States. From this set, we drop 1,784 markets because

they do not have a neighboring market, and therefore our measure of entry threat is not defined. In

addition, we drop 64 markets which have more than 30 neighbors. These markets cover very little

geographic area, and therefore do not fit our market definition. Finally, there are 1,799 markets

which are missing demographic data, and so we drop these observations from our sample as well,

leaving us with a total of 28,207 markets.

Due to limitations of the data discussed earlier in this section, we focus our analysis on the

decision of the first entrant into an open market. Furthermore, because our goal is to understand the

effect of the threat of future competition on firms’ entry decisions in the early rollout of broadband

infrastructure, we focus on markets which were unserved in the year 2000.8 This restriction leaves

us with 8,476 markets.

Finally, there are some zip codes which we do not observe in the 2013 National Broadband

7To test the robustness of this definition, we replace the value of 3 in equation (2) with 1, 2, 4, and 5, and obtainqualitatively similar results.

8Our data begins in 1999, and would therefore permit us to study one year earlier, but only a tiny fraction ofopen markets were threatened at that time, which affords our estimates very little power. For robustness, we carryout our full analysis for 1999, 2000, and 2001, and find remarkably similar results.

11

Table 1: Neighbors Summary Statistics

Variable Mean Standard Deviation Min Median Max

# of neighbors 2.61 1.53 1 2 28

# of Markets = 7,642

Table 2: Demographic Summary Statistics

Variable Mean | Threat = 0 Mean | Threat = 1

Population 1,159.10 1,784.64% Black 0.05 0.04% Hispanic 0.04 0.06% Am. Indian 0.02 0.01% Asian 0.00 0.01ln(Median income) 10.36 10.63% College 0.36 0.43Household size 2.57 2.60% Female 0.50 0.50% Senior 0.33 0.31% Work from home 0.06 0.04% Long commute 0.20 0.19% Rent 0.20 0.23% Phone 0.95 0.98% Rural 0.95 0.60ln(Population density) 3.26 5.86ln(Business density) 2.80 3.22

# of Markets 7,115 527

Map data. In the interest of maintaining a consistent set of observations, we drop these from our

sample, leaving us with 7,642 markets.9

3.4 Summary Statistics

Summary statistics for the number of neighbors a market has are shown in table 1. On average, a

market has 2.61 neighbors, though this varies between 1 and 28 for all markets in our sample. Of

the 7,642 markets in our sample, about 7% or 535 markets are threatened.

Table 2 presents summary statistics for each of the market characteristics which will be included

in our specifications, broken down by entry threat status. Threatened and unthreatened markets are

quite similar across most dimensions, though threatened markets typically have larger populations,

are less rural, more densely populated, and have more businesses.

9For robustness, we estimate all models which do not require 2013 data without dropping these markets, and findqualitatively similar results.

12

Table 3: Outcome Summary Statistics

Variable Mean | Threat = 0 Mean | Threat = 1

Short-run Entry 0.34 0.18Long-run Entry 0.91 0.98Entry Delay 2.97 3.39Mean Current Download Speed 72.68 140.99

# of Markets 7,115 527

Despite these seemingly attractive features, in the short-run, threatened markets are entered

much less often than their unthreatened counterparts. Table 3 shows that threatened markets were

entered about half as often between 2000 and 2001. In addition, markets which were unserved in

2000 waited 0.44 years longer to be entered if they were threatened. In the long run, however,

threatened markets were more likely to be entered, as 98% had access to at least 1 provider in

2013.

4 Empirical Framework

4.1 Entry in the Short Run

When modeling the decision of a firm to enter an open market, we consider a static entry game in

the spirit of Bresnahan and Reiss (1991). In this setting, firms make their entry decisions and then

receive continuation values which depend on the actions of other firms. We choose this simpler

model over a full-fledged dynamic one because firms faced enormous uncertainty about their rivals’

behavior. The industry was still in its infancy, which meant that industry norms had not yet

formed, and that the turnover rate what quite high. Therefore, we do not believe that writing

down an explicit value function, which would require firms to make predictions about the entire

future evolution of the market, is appropriate for this setting.

Consider the decision of the first firm to enter a market, m, which contains no firms at time

t−1. Firms are ranked from 1 to N , where N is the total number of potential entrants, on the basis

of their efficiency. We assume that firms are sequentially given the opportunity to enter the market,

and that a more efficient firm will always enter earlier than a less efficient one. This assumption

ensures that at any point in time, there will be at most one potential entrant, which we label firm

n.

13

At the start of time period t, firm n observes the state of the market, and decides whether the

expected discounted value of the future profit stream is sufficiently high to support entry. Expected

profitability is calculated based upon market demand, cost of providing service, and anticipated

future market structure.

Critically, potential entrant n forms its expectation about market m’s future structure based

upon the market structures of neighboring markets. If at least one rival firm operates in a neighbor-

ing market but not in market m, then firm n believes that market m is likely to become competitive

in the future, and therefore considers it to be threatened. In the broadband industry, this thought

process is quite logical; there are enormous economies of scale in building out a network, and there-

fore an incumbent provider will find it much easier to spill over into an adjacent market than to

enter a more distant market. Formally, for each market, m, we define a variable

EntryThreatmt =

1 if for some market, m′, neighborsm,m′ = 1 and NFm′t > 1

0 otherwise

(3)

where neighborsm,m′ is as defined in equation (2) and NFm′t is the number of firms serving market

m′ at time t.10

Then, the expected discounted value of future profits of potential entrant n from entering market

m at time t is

E(Πnmt) = α0t +Xmα1t + α2tEntryThreatmt + unmt (4)

This reduced form representation of expected profits states that profits depend on a vector of

market attributes (Xm), the threat of future competition, and a stochastic error term (unmt) which

reflects factors influencing profits that are observed by firm n but not by the econometrician.

For a given market, m, potential entrant n’s entry decision can be represented by a binary

variable, Dnmt ∈ 0, 1, where Dn

mt = 1 if firm n enters market m at time t. This firm will choose

to enter the market if and only if expected discounted profits are positive; in other words, Dnmt = 1

10Because our data is censored such that all markets with 1, 2, or 3 firms are recorded as a 1, we can only detectthat a market has more than 1 firm if that market has at least 4 firms. EntryThreatmt is defined subject to thislimitation.

14

if and only if E(Πnmt) ≥ 0.

Xm contains market-specific variables which we expect to influence variable profits and fixed

operating costs. Market size, as measured by population, is a key element, as shown by Bresna-

han and Reiss (1990, 1991). Additionally, local characteristics such as gender, race, age, income,

commuting patterns, and business activities are all likely to shift demand for broadband internet,

while population density is an important factor in determining fixed costs, as rolling out wires in

rural areas is very expensive.

α2t is intended to capture firm n’s concern over a competitive future market structure. However,

because we do not observe firm identities, when EntryThreatmt = 1, it is possible that firm n is

itself one of the firms present in a neighboring market. In such a case, firm n can more easily enter

market m, and EntryThreatmt will pick up this positive spillover effect. Therefore, α2t represents

the net of two countervailing effects: the (positive) spillover effect and the (negative) entry threat

effect. We cannot separately identify these two effects, but if we estimate a negative α2t, then we

can conclude that the presence of rivals in neighboring markets makes potential entrants less likely

to enter the market.

4.2 Modelling Spatial Correlation in the Errors

unmt, is a random shock affecting firm n’s expected discounted flow of profits in market n at time

t, and is observed by the firm but not by the econometrician. These shocks may capture regional

spikes in demand, local economic downturns, regulatory hurdles, and any other factors which are

not controlled for through observable market characteristics. As such, it is likely that these shocks

are not isolated to a single zip code, but rather are correlated with the shocks experienced by other

nearby markets. To allow for this possibility, we impose the following structure on the error terms:

u = ψWu+ ε (5)

u is an M × 1 vector of error terms, where M is the total number of markets; ψ is a scalar; W

is an M ×M symmetric matrix with elements wij such that wij is a binary variable equal to 1

if and only if i 6= j and neighborsij = 1;11 ε is an M × 1 vector of identically and independently

11Note that since the diagonal elements of W are 0 by definition, no um will ever be defined recursively.

15

distributed random variables with

ε ∼ N(0, IM ) (6)

where IM is the identity matrix with dimension M . Note that the n and t subscripts have been

suppressed in equations (5) and (6) for ease of notation.

The ψ term captures spatial correlation in the errors, u. If ψ = 0, then there is no spatial

correlation and each ui is simply drawn from the normal distribution in equation (6). If ψ 6= 0,

then spatial correlation exists, and there are factors which influence profitability and are correlated

across neighboring markets.

Given equation (5), the variance-covariance matrix of u is

V (u) = [(IM − ψW )′(IM − ψW )]−1 (7)

and is heteroskedastic if ψ 6= 0. Therefore, if there is spatial correlation in the errors, the maxi-

mum likelihood estimates of the probit model will be inconsistent. To deal with this, we use the

generalized method of moments (GMM) approach developed by Pinkse and Slade (1998), which

yields consistent estimates of the parameters under spatial correlation.

First, in order to establish the existence of this spatial correlation, we need to test the null

hypothesis that ψ = 0. To do this, we implement the test designed by Pinkse and Slade (1998).12

To conduct the test, we begin by estimating the parameter vector, α, of equation (4) using GMM.

Under the null hypothesis, α is consistent and the residual, u(α|ψ = 0), is a vector of uncorrelated

elements. Under the alternative hypothesis, however, the elements of u(α|ψ = 0) are correlated.

Therefore, u(α|ψ = 0)′Wu(α|ψ = 0) tends to be larger than its counterpart constructed using data

simulated under the restrictions that ψ = 0 and that α = α. The fraction of occurrences where

this holds forms the basis for the test.

Given the latent variable representation of profits in equation (4), we do not actually observe

profits and therefore the ordinary residuals are not observed. Instead, the generalized error term

12The test is described in detail in Pinkse and Slade (1998), pages 130-131.

16

is defined as

um(α) = [Dm − Φ(Gm(α))]φ(Gm(α))

Φ(Gm(α))[1− Φ(Gm(α))](8)

where Gm(α) = α0+Xmα1+α2EntryThreatmνm(ψ) , νm(ψ) is the square root of the mth diagonal element of

V (u), and φ(·) and Φ(·) are the density and cumulative functions of a standard normal distribution.

The generalized residuals can be defined analogously, and we note that under the null hypothesis

of ψ = 0, the generalized residual simplifies to

um(α|ψ = 0) =Dm − Φ(Gm(α))

Φ(Gm(α))[1− Φ(Gm(α))](9)

4.3 Endogeneity of Entry Threat

In order to give our estimates a causal interpretation, we must deal with two sources of potential

endogeneity in our entry threat variable. First, entry threat is not exogenous if the error terms are

correlated across neighboring markets . To see why, consider two isolated neighboring markets, m

and m′. EntryThreatmt = 1 if and only if Dm′t′ = 1 for some period t′ < t. By equation (4) Dm′t′

is a function of um′t′ , and therefore, EntryThreatmt is a function of um′t′ . Then, in the presence of

spatial correlation, EntryThreatmt is correlated with umt, as long as there is some component of

the error term which is persistent over time. We test for, and correct for this source of endogeneity

using the framework of Pinkse and Slade (1998), as discussed in the previous section.

Second, if firms do indeed consider the threat of future competition when making entry decisions,

then our entry threat variable cannot possibly be exogenous, as firms in neighboring markets each

make entry decisions while considering the threat of spillover from the other. To illustrate this,

again consider two isolated neighboring markets, m and m′. EntryThreatmt = 1 if and only if

Dm′t′ = 1 for some period t′ < t. By equation (4), Dm′t′ is a function of EntryThreatm′t′ , which

is equal to 1 if and only if Dmt′′ = 1 for some t′′ < t′. Therefore, since Dmt′′ is a function of umt′′ ,

EntryThreatm′t′ is a function of umt′′ . It then follows that Dm′t′ , and therefore EntryThreatmt,

are functions of umt′′ , which is the source of endogeneity.

This second source of endoegeneity exists regardless of the presence of spatial correlation. In

principle, we could embed all entry decisions into a simultaneous structural model, but identifica-

17

tion and estimation would quickly become intractable. Instead, we propose a set of instrumental

variables for the entry threat variable into equation (4).

In the spirit of Pinkse and Slade (1998), we use the average market attributes of all of a

market’s neighbors’ neighbors as instruments. These characteristics will affect entry into a market’s

neighbors, but should have no direct effect on the decision to enter the market itself. To be concrete,

suppose that market m′ has a neighbor, m′′, but that market m and market m′′ are not themselves

neighbors. As before, the attributes of market m′′ clearly affect whether market m′′ contains any

firms. Additionally, a firm’s presence in market m′′ increases its likelihood of spilling over into

market m′, which then creates an entry threat for market m. In order for these instruments to

be exogenous, firms may consider the attributes of neighboring markets when making their entry

decision, but they must not consider the attributes of other, further away markets. In other words,

firms can be forward-looking but must be sufficiently myopic. In principle, we could allow firms to

consider 3, 4, ..., T steps ahead, and construct the appropriate set of instruments.

4.4 Estimation

Given the generalized error defined in equation (8), we form the moment conditions using a set of

L instruments, Z, such that E[Z ′u(α)] = 0. Z is therefore and M × L matrix with L greater than

or equal to the length of the parameter vector, α.13 The sample analogue of the moment is

S(α) =1

MZ ′u(α) (10)

When the model is just-identified, we solve for the α such that S(α) = 0. When the model is

over-identified,

α = arg minαS′(α)ΩS(α) (11)

where Ω is an L× L positive definite weighting matrix.14

Even when ψ 6= 0, α is consistent and asymptotically normal. We then estimate the variance-

13Note that even when all right hand size variables are exogenous, we still need one extra instrument in order toidentify ψ.

14We use the optimal weighting matrix for Ω, which we construct by according to the following steps: first, we geta consistent GMM estimate, θ1 by using Ω = IM in equation (11); second, we construct Ω = ME[S(α1)S′(α1)].

18

covariance matrix of α by using the following property of α:

√M(α− α) ∼ N(0, [B2(α)]−1

∂S′(α)

∂αΩB1(α)Ω

∂S(α)

∂α′[B2(α)]−1) (12)

where B1(α) = ME[S(α)S′(α)] and B2(α) = ∂S′(α)∂α Ω ∂S(α)

partialα′ .

4.5 Other Outcomes of Interest

4.5.1 Entry Delay

If the threat of future competition makes firms less likely to enter a market in the short run, the

natural follow up question becomes: how long do firms delay entry into a market as a result of this

entry threat? To answer this question, we estimate the following model:

EntryDelaymt = β0t +Xmβ1t + β2tEntryThreatmt + umt (13)

where EntryDelaymt is equal to the number of years elapsed from time t until market m receives

its next entrant. Xm is again the set of observed market characteristics affecting market m’s

profitability, and umt are unobservable shocks affecting entry into market m. β2t represents the

degree to which firms delay entry into market m in response to the threat of future competition. We

estimate this model using the GMM approach described in section (4.4); the only modification is

that since EntryDelaymt is observed, the usual error term can be constructed and the generalized

error term of equation (8) is not necessary.

4.5.2 Entry in the Long Run

We intend for our measure of entry threat to capture the likelihood of future entry into market m.

Therefore, despite our hypothesis that entry threat will deter entry in the short run, it should be

the case that markets which are threatened in the short run are more likely to be entered in the

long run. To test this, we estimate the following model:

LongRunEntrymt = γ0t +Xmγ1t + γ2tEntryThreatmt + umt (14)

19

where LongRunEntrym is a binary variable equal to 1 if and only if market m is entered be-

tween time t and 2013,15 and Xm EntryThreatmt, and umt are as defined in the short-run entry

specification.

4.5.3 Broadband Speeds in the Long Run

Finally, we aim to understand how the early evolution of the broadband industry has shaped the

quality of internet service experienced in the long run. To this end, we estimate the effect of the

delay a market experiences in receiving its first entrant on the maximal download speeds currently

available in that market. Specifically, we estimate the following model:

Speedm,2013 = η0 +Xm,2013η1 + η2tEntryDelaymt+

+η3tln(#ISPs)m,2013 + umt (15)

where Speedm,2013 is the maximum advertised download speed available in market m in 2013,

Xm,2013 are the 2013 values of the same attributes of the previous specifications, EntryDelaymt is

the number of years elapsed from time t until market m is entered, and ln(#ISPs)m,2013 is the log

of the number of ISPs present in market in 2013. Since Speedm,2013 is observed, umt is constructed

as in section (4.5.1).

5 Results

The overarching goal of this paper is twofold: 1) to determine whether the threat of future compe-

tition led firms to delay entry into open markets, early in the deployment of the U.S. broadband

infrastructure; and 2) to estimate the impact of this delayed entry (if any), on the quality of the

U.S. broadband infrastructure in the long run.

5.1 Is Entry Threat Credible?

In order to address the first goal, we have argued that the broadband industry has a natural

indicator for the threat of future entry into a market, the presence of other firms in a neighboring

15We also estimate a specification where the outcome is a binary variable equal to 1 if and only if market m containsat least 4 firms by 2013, and obtain nearly identical results.

20

market. The enormous localized fixed costs of broadband infrastructure ensure that entering nearby

markets is far more efficient than entering more distant markets. Therefore, we should see that

markets which are threatened in the early stages of the rollout are more likely to be entered in

the long run. In support of this claim, we present the results of estimating equation (14) in table

(4). The first three columns report the results of estimating a linear probability model; the first

column was estimated with ordinary least squares, while the second and third are estimated using

neighbors’ attributes and neighbors’ neighbors’ attributes as instruments, respectively. The fourth

column reports the results of the GMM estimation procedure described in section 4.4, which controls

for spatial correlation in the error terms.

We show that after accounting for the endogeneity of entry threat, markets which are threat-

ened in the year 2000 are more likely to be entered by 2013. This finding is consistent with the idea

that firms can more easily spill over into areas where the firm already has a foothold, and critically,

demonstrates that this threat of entry is “real” in a very material way. Our results also show the

importance of addressing endogeneity, though the results are not sensitive to our choice of instru-

ments. Furthermore, in the GMM estimation, we find evidence of substantial spatial correlation.

It is important to note that unlike the GMM estimates, the estimates of linear probability models

represent the marginal effect of each variable on the probability of entry. In order to compare our

estimates, we use the GMM estimates to calculate that the average marginal effect of entry threat

on entry probability is 0.04.

5.2 Does the Threat of Future Competition Deter and Delay Entry?

Equipped with evidence that the threat of entry does indeed lead to entry in the long run, we turn to

the question of whether potential entrants respond to this threat by discounting a market’s expected

future profitability and reducing their probability of entry in the short run. A firm which believes

that it can expect monopoly profits should be more likely to enter a market than one which expects

its market power to be eroded by the entry of rivals - the question is, did such forecasting make

cable and telephone companies reluctant to enter these threatened markets during the formative

years of the industry’s development? The results of estimating equation (4), as shown in table (5),

demonstrate that indeed firms were less likely to enter a threatened market, other things equal.

This finding is robust across all specifications. As before, we report results of estimating a linear

21

Table 4: Probability of Long-run Entry

OLS IV GMM

Entry Threat -0.002 0.12*** 5.98(0.01) (0.04) (3.85)

Population (10,000) 0.09*** 0.09*** 0.25***(0.02) (0.02) (0.05)

Percent Black -0.09*** -0.09*** -1.29***(0.02) (0.02) (0.28)

Percent Hispanic -0.16*** -0.17*** -1.78***(0.03) (0.03) (0.37)

Percent American Indian -0.34*** -0.35*** -2.31***(0.04) (0.04) (0.44)

Percent Asian 0.09 0.11 28.03**(0.15) (0.15) (12.79)

log(Median Houshold Income) 0.07*** 0.06*** 0.34***(0.01) (0.01) (0.13)

Percent Graduated College -0.05* -0.07** -0.43(0.03) (0.03) (0.35)

Average Household Size 0.02 0.01 0.08(0.02) (0.02) (0.20)

Percent Female 0.24** 0.26** 2.87***(0.10) (0.10) (0.93)

Percent Senior 0.025 0.01 0.08(0.06) (0.06) (0.64)

Percent Work from Home 0.15*** 0.14** 1.44**(0.06) (0.06) (0.60)

Percent Long Commute -0.32*** -0.33*** -1.97***(0.03) (0.03) (0.25)

Percent Rent 0.07* 0.06 0.18(0.04) (0.04) (0.40)

Percent with Phone 0.19*** 0.18*** 0.18(0.07) (0.07) (0.54)

Percent Rural -0.02 0.01 -2.36(0.02) (0.02) (1.70)

log(Population Density) 0.02*** 0.01*** 0.15***(0.002) (0.003) (0.03)

log(Business Density) -0.004 -0.005 -0.04(0.004) (0.004) (0.04)

ψ - - 1.32- - (0.22)***

Instruments: Neighbors’ Neighbors’ Attributes N Y YAllow for Spatial Correlation N N Y

# of Markets 7,642 7,642 7,642

22

probability model in columns 1-3, and the GMM estimation controlled for spatial correlation in

column 4. As in the previous section, we use the GMM point estimates to calculate that the average

marginal effect of entry threat on entry probability is -0.26, which is comparable to what we find

under the linear probability model with instruments.

Since firms appear reluctant to enter threatened markets, we next investigate the persistence

of this effect. Rather than looking solely at the entry decisions of a single time period, we estimate

the effect of entry threat on the length of time elapsed until a market is entered, in order to better

make use of our panel of data. We report the results of estimating equation (13) in table (6).

We find that an open market which is threatened in the year 2000 is entered, on average, about

3 years longer that its un-threatened counterpart. For perspective, the average un-threatened

market which was open in 2000 waited about 3.5 years until being entered, so this estimated effect

represents a significant delay. In this specification, since the outcome is a continuous variable, the

GMM estimates are directly comparable to the linear probability model estimates.

5.3 Does Delayed Entry Affect Broadband Speeds in the Long Run?

Despite the delay created by internet service providers’ reluctance to compete against their rivals,

over 95% of zip codes had at least one internet service provider as of 2013. It is then natural

to ask whether this delay really mattered, or whether “time heals all wounds.” Access to the

internet has never been more critical than it is today, and the speeds at which one can do so are

every bit as important. We therefore estimate the impact of delayed initial entry on the download

speeds available in 2013, more than 10 years after the start of our sample. We report the results of

estimating equation (15) in table 7.

We find evidence that delayed entry early in the rollout of the U.S. broadband infrastructure has

a significant impact on download speeds available today, specifically that each additional year that a

market remains open translates into an 11% decrease in present-day download speeds. Remarkably,

this result is true even when controlling for the current number of firms serving a market. This

means that the mechanism for this effect is not simply that markets which are entered later are

still less competitive today and therefore have faster available speeds today. Instead, our findings

suggest that if two identical markets have the same number of service providers today, the one

which was initially entered first will have access to faster speeds. We believe that this is because

23

Table 5: Probability of Short-run Entry

OLS IV GMM

Entry Threat -0.11*** -0.17*** -1.20***(0.02) (0.07) (0.46)

Population (10,000) 0.67*** 0.67*** 0.24***(0.03) (0.03) (0.05)

Percent Black -0.03 -0.03 0.08(0.04) (0.04) (0.15)

Percent Hispanic -0.12** -0.12** -0.10(0.05) (0.05) (0.21)

Percent American Indian -0.19*** -0.19*** -0.67***(0.07) (0.07) (0.25)

Percent Asian -0.83*** -0.84*** -5.94(0.24) (0.24) (6.68)

log(Median Houshold Income) 0.13*** 0.14*** 0.73***(0.02) (0.02) (0.17)

Percent Graduated College -0.03 -0.02 -0.10(0.05) (0.05) (0.19)

Average Household Size -0.01 -0.01 -0.12(0.03) (0.03) (0.13)

Percent Female 0.20 0.19 0.52(0.17) (0.17) (0.76)

Percent Senior -0.03 -0.02 -0.21(0.10) (0.10) (0.44)

Percent Work from Home -0.31*** -0.31*** -1.05**(0.09) (0.09) (0.33)

Percent Long Commute -0.01 -0.01 -0.11(0.04) (0.04) (0.19)

Percent Rent 0.06 0.07 0.23(0.06) (0.06) (0.29)

Percent with Phone -0.10 -0.10 -0.07(0.11) (0.11) (0.44)

Percent Rural 0.10*** 0.08*** 0.35**(0.03) (0.03) (0.17)

log(Population Density) -0.03*** -0.03*** -0.12***(0.004) (0.004) (0.02)

log(Business Density) -0.02*** -0.02*** -0.08***(0.01) (0.01) (0.03)

ψ - - 1.32- - (0.53)**

Instruments: Neighbors’ Neighbors’ Attributes N Y YAllow for Spatial Correlation N N Y

# of Markets 7,642 7,642 7,642

24

Table 6: Elapsed Time Until the Entry

OLS IV GMM

Entry Threat 1.13*** 2.67*** 3.01***(0.126) (0.367) (0.27)

Population (10,000) -5.26*** -5.21*** 0.05***(0.16) (0.16) (0.01)

Percent Black 0.37* 0.34 -0.75***(0.22) (0.22) (0.17)

Percent Hispanic 2.99*** 2.87*** -1.63***(0.28) (0.29) (0.23)

Percent American Indian 2.57*** 2.48*** -2.56***(0.36) (0.36) (0.39)

Percent Asian -0.59 -0.40 1.16**(1.35) (1.36) (0.49)

log(Median Houshold Income) -1.01*** -1.17*** -0.96***(0.12) (0.13) (0.12)

Percent Graduated College 1.32*** 1.08*** 1.45***(0.26) (0.26) (0.23)

Average Household Size 0.21 0.19 0.65***(0.15) (0.15) (0.16)

Percent Female -2.53*** -2.30** -3.67***(0.91) (0.92) (0.91)

Percent Senior 1.76*** 1.60*** 0.31(0.55) (0.56) (0.50)

Percent Work from Home 0.55 0.44 0.68*(0.51) (0.51) (0.39)

Percent Long Commute 0.36 0.27 -0.74***(0.23) (0.23) (0.18)

Percent Rent 0.84** 0.73** -1.21***(0.34) (0.35) (0.30)

Percent with Phone -1.39** -1.49** -2.25***(0.60) (0.60) (0.72)

Percent Rural -0.54*** -0.18 0.24**(0.14) (0.17) (0.12)

log(Population Density) 0.80*** 0.74*** 0.10***(0.02) (0.03) (0.02)

log(Business Density) 0.44*** 0.43*** 0.07***(0.03) (0.03) (0.03)

ψ - - 4.40- - (0.01)***

Instruments: Neighbors’ Neighbors’ Attributes N Y YAllow for Spatial Correlation N N Y# of Markets 7,642 7,642 7,642

25

Table 7: 2013 Maximum Available Download Speed

Variable OLS IV GMM

Elapsed Time Until Entry 0.01 -0.05* -0.11***(0.01) (0.03) (0.03)

log(Number of ISPs) 0.86*** 2.06*** 1.05***(0.03) (0.12) (0.06)

Population (10,000) 0.11 -0.21* -0.03***(0.06) (0.12) (0.01)

Percent Black 0.08 0.19 0.15(0.10) (0.12) (0.11)

Percent Hispanic -0.28** 0.36** -0.01(0.12) (0.16) (0.15)

Percent American Indian -0.50*** 0.57*** -0.36(0.16) (0.21) (0.25)

Percent Asian 0.05 -0.02 -0.07(0.59) (0.67) (0.41)

log(Median Houshold Income) 0.40*** 0.14** 0.40***(0.05) (0.06) (0.06)

Percent Graduated College 0.31*** 0.33** 0.27**(0.11) (0.13) (0.13)

Average Household Size -0.08* 0.05 -0.07(0.04) (0.05) (0.05)

Percent Female -0.04 -0.41 -0.34(0.23) (0.26) (0.27)

Percent Senior -0.19 0.25 0.21(0.15) (0.19) (0.21)

Percent Work from Home 0.44** 0.03 0.65***(0.20) (0.24) (0.24)

Percent Long Commute 0.10 0.54*** 0.12(0.09) (0.12) (0.12)

Percent Rent -0.07 -0.05 0.10(0.12) (0.14) (0.15)

Percent with Phone 0.42 -0.04 0.70*(0.30) (0.34) (0.41)

Percent Rural -0.22*** 0.15 -0.23***(0.07) (0.09) (0.09)

log(Population Density) 0.07*** -0.01 0.17***(0.01) (0.03) (0.03)

log(Business Density) 0.01 -0.01 -0.01(0.01) (0.01) (0.01)

ψ - - 2.74***- - (0.01)

Instruments: Neighbors’ Neighbors’ Attributes N Y YAllow for Spatial Correlation N N Y# of Markets 7,642 7,642 7,642

26

when facing rivals, firms are under constant pressure to upgrade the quality of their service; absent

this pressure, firms are more likely to remain stagnant. Therefore, download speeds in markets

which did not exhibit this competitive pressure until recently lag behind speeds in those which

developed early. 16 In support of this hypothesis, we replace EntryDelaymt in equation 15 with

CompetitiveDelaymt, a variable which represents the number of years from 2000 it takes for the

market to become competitive.17 We present the results of this estimation in table 8. Indeed, we

find that the longer a market takes to become competitive, the slower its present-day download

speed. In fact, the effect of delayed competition is stronger than the effect of delayed entry.

6 Conclusion

In this paper, we trace out the evolution of the broadband internet market, from its inception

through the present. We find evidence that firms are reluctant to enter markets which are threatened

by future entry of rivals. This suggests that a firm’s perception of its ability to maintain market

power in the future is an important factor in its entry decision. We find that, on average, this

strategic consideration causes firms to delay entry into open markets by three years. Although this

early deployment stage is long past, this delayed entry appears to have had effects which persist

even today, as markets which experienced their initial entry later have access to considerably slower

download speeds.

16In contrast, one might be tempted to predict the opposite result, that markets which are initially entered later areequipped with better technology and therefore would have faster download speeds today. However, 93% of zip codeshad been entered by 2007, presumably with the cutting edge technology of the time. But, the prevailing downloadspeeds of 2007 are wholly obsolete by today’s standards; in fact, the average download speeds of 2007 do not evenmeet the FCC’s current definition of broadband. Therefore, regardless of the initial technology installed, it is onlythrough drastic innovations that firms can provide the download speeds we enjoy today.

17Given the limitations of the data, we define a market to be competitive when it has at least 4 firms.

27

Table 8: 2013 Maximum Available Download Speed

Variable OLS IV GMM

Elapsed Time Until Competition -0.01 -0.21*** -0.14***(0.01) (0.05) (0.05)

log(Number of ISPs) 0.86*** 1.98*** 1.01***(0.03) (0.12) (0.06)

Population (10,000) 0.06 -0.70* -0.04**(0.06) (0.16) (0.02)

Percent Black 0.07 0.01 0.11(0.11) (0.13) (0.12)

Percent Hispanic -0.26** 0.32** -0.09(0.12) (0.15) (0.14)

Percent American Indian -0.48*** 0.63*** -0.03(0.16) (0.21) (0.26)

Percent Asian 0.07 0.49 -0.14(0.59) (0.69) (0.36)

log(Median Houshold Income) 0.40*** 0.08 0.43***(0.05) (0.07) (0.06)

Percent Graduated College 0.31*** 0.25* 0.23*(0.11) (0.13) (0.13)

Average Household Size -0.08* 0.04 -0.06(0.04) (0.05) (0.06)

Percent Female -0.05 -0.56 -0.18(0.23) (0.27) (0.28)

Percent Senior -0.16 0.42** 0.12(0.15) (0.18) (0.20)

Percent Work from Home 0.46** 0.26 0.66**(0.20) (0.25) (0.26)

Percent Long Commute 0.10 0.53*** 0.22*(0.09) (0.12) (0.12)

Percent Rent -0.07 -0.04 0.10(0.12) (0.14) (0.15)

Percent with Phone 0.42 -0.06 0.75*(0.30) (0.35) (0.41)

Percent Rural -0.23*** 0.08 -0.17**(0.07) (0.10) (0.09)

log(Population Density) 0.08*** 0.02 0.13***(0.01) (0.02) (0.02)

log(Business Density) 0.01 -0.02** 0.01(0.01) (0.01) (0.01)

ψ - - 3.46***- - (0.03)

Instruments: Neighbors’ Neighbors’ Attributes N Y YAllow for Spatial Correlation N N Y# of Markets 7,642 7,642 7,642

28

References

Anselin, L. (1988), Spatial Econometrics: Methods and Models, Kluwer Academic Publishers,

Dordrecht.

Bresnahan, T. F. & P. C. Reiss (1990), Entry in Monopoly Markets, The Review of Economic

Studies, 57(4), 531-551.

—- (1991), ”Entry and Competition in Concentrated Markets,” Journal of Political Economy,

99(5), 977- 1009.

Dafny, L. (2005), Games Hospitals Play: Entry Deterrence in Hospital Procedure Markets,

Journal of Economics and Management Strategy, 14(3): 513-542.

Economides, N., K. Seim, & B. Viard (2004), Quantifying the Benefits of Entry into Local

Telephone Service, forthcoming, RAND Journal of Economics.

Ellison, G. & S. F. Ellison (2011), Strategic Entry Deterrence and the Behavior of Pharmaceu-

tical Incumbents Prior to Patent Expiration, American Economic Journal: Microeconomics, 3(1),

1-36.

Goolsbee, A. & C. Syverson (2004), How Do Incumbents Respond to the Threat of Entry?

Evidence from the Major Airlines, forthcoming, Quarterly Journal of Economics.

Greenstein, S. & M. Mazzeo (2006), ”The Role of Differentiation Strategy in Local Telecom-

munication Entry and Market Evolution: 1999-2002”, Journal of Industrial Economics, Vol. 54(3),

323-349.

Jackson, C. L. (2002), Wired High-Speed Access, Broadband —- Should We Regulate High-

Speed Internet Access, edited by R.W. Crandall & J. H. Alleman, published by Brookings Institu-

tion Press, Washington D.C.

Klemperer, P. (1987), Entry Deterrence in Markets with Consumer Switching Costs, The Eco-

nomic Journal, 97(Supplement: Conference Papers), 99-117.

Milgrom, P. & J. Roberts (1982), Limit Pricing and Entry Under Incomplete Information: An

Equilibrium Analysis, Econometrica, 50(2), 443-460.

Paradyne Corp. (2000), The DSL Sourcebook, on-line document, http:www.paradyne.comsourcebook offersb 1file.pdf.

Pinkse, J., M. Slade (1998), ”Contracting in Space: an Application of Spatial Statistics to the

Discrete Choice Model,” Journal of Econometrics, 85, 125-154.

29

Pinkse, J., M. Slade, & C. Brett (2002), Spatial Price Competition: a Semiparametric Approach,

Econometrica, 70-3, 1111-1153.

Seamans, R. (2012), Fighting City Hall: Entry Deterrence and New Technology Deployment in

Cable TV Markets, Management Science, 58(3), 461-475.

Spence, M. (1981), The Learning Curve and Competition, Bell Journal of Economics, 12(1),

1981, 49- 70.

30

Appendix

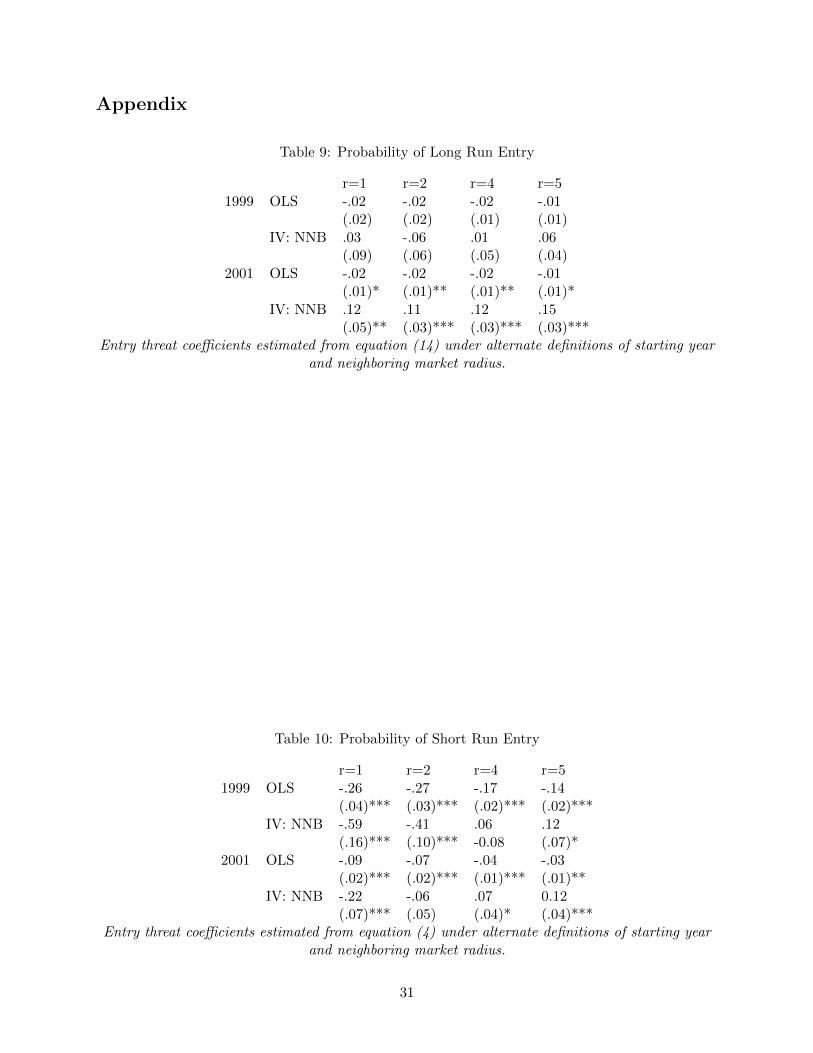

Table 9: Probability of Long Run Entry

r=1 r=2 r=4 r=51999 OLS -.02 -.02 -.02 -.01

(.02) (.02) (.01) (.01)IV: NNB .03 -.06 .01 .06

(.09) (.06) (.05) (.04)2001 OLS -.02 -.02 -.02 -.01

(.01)* (.01)** (.01)** (.01)*IV: NNB .12 .11 .12 .15

(.05)** (.03)*** (.03)*** (.03)***Entry threat coefficients estimated from equation (14) under alternate definitions of starting year

and neighboring market radius.

Table 10: Probability of Short Run Entry

r=1 r=2 r=4 r=51999 OLS -.26 -.27 -.17 -.14

(.04)*** (.03)*** (.02)*** (.02)***IV: NNB -.59 -.41 .06 .12

(.16)*** (.10)*** -0.08 (.07)*2001 OLS -.09 -.07 -.04 -.03

(.02)*** (.02)*** (.01)*** (.01)**IV: NNB -.22 -.06 .07 0.12

(.07)*** (.05) (.04)* (.04)***Entry threat coefficients estimated from equation (4) under alternate definitions of starting year

and neighboring market radius.

31

Table 11: Elapsed Time Until Entry

r=1 r=2 r=4 r=51999 OLS 1.66 1.68 1.34 1.18

(.24)*** (.19)*** (.14)*** (.13)***IV: NNB 6.31 4.45 1.91 1.37

(1.06)*** (.62)*** (.45)*** (.38)***2001 OLS .97 .86 .65 .54

(.13)*** (.10)*** (.08)*** (.08)***IV: NNB 2.69 1.89 .44 .02

(.48)*** (.34)*** (.25)* (.25)Entry threat coefficients estimated from equation (13) under alternate definitions of starting year

and neighboring market radius.

Table 12: Elapsed Time Until Entry

r=1 r=2 r=4 r=5P=1 OLS -.004 -.01 -.01 -.01

(.01) (.005)** (.004)** (.004)**IV: NNB -.16 -.22 -.13 -.12

(.03)*** (.03)*** (.02)*** (.02)***P=3 OLS .01 .01 .001 .002

(.01) (.01) (.01) (.01)IV: NNB -.02 -.03 .03 .04

(.04) (.03) (.02) (.02)Entry threat coefficients estimated from equation (15) under alternate definitions of starting year

and neighboring market radius.

32