entertainment one interim results - amazon s3 · movies in development: ... the mark gordon company...

TRANSCRIPT

entertainmentone.com

entertainmentone.com

Interim results 21 November 2017

entertainmentone.com

Business review

2 entertainmentone.com

entertainmentone.com

Highlights Robust first half performance across the Group

• Revenue consistent at £396m

• Underlying EBITDA up 36% to £51m

• EBITDA margin up 360 basis points reflecting the growth in Family and realisation of cost savings

Family ahead of expectations, driven by Peppa Pig in China and PJ Masks

• Retail revenue from brands up from US$0.7bn to US$1.2bn

Strong performance across Television • eOne Television delivers higher international sales revenue

• MGC experiences high levels of activity across television and film

Film starting to migrate from acquisition to production

Transition from physical to digital delivers ongoing cost savings

Integration of Film and Television proceeding as planned – expected annual cost savings of £8m by FY20

Library valuation increased by 13% to US$1.7 billion

Full year in line with management expectations

3

entertainmentone.com

Strategy: Connect, Create, Deliver

4

entertainmentone.com

Family Ahead of expectations: Revenues up 64% and underlying EBITDA up 54%

5

Brand H1 Progress Outlook

China a key driver to growth: licensing revenues up over 700% as consumer product ranges expanded. Audience traction on broadcast and VOD remains strong

US licensing programme continues to build, supported by infrastructure investment

Recently introduced to Japanese audiences in partnership with Tokyo TV

Chinese licence agreements anticipated to grow from 20 at the end of FY17 to 60 by the end of FY18

Peppa Pig S5 now in production, with new episodes to be delivered from March 2018 onwards

‘Evergreen’ status underlined with recent multi-territory Merlin deal for location based entertainment formats

Successful licensing roll-out from September 2016 continues, driving 600% revenue growth

PJ Masks now around 36% of total Family licensing revenues

PJ Masks S2 production progressing well, with broadcast anticipated in early 2018

Further licensing programmes due to be rolled out in FY18 across Europe and the Far East. Preparations are currently under way for a full consumer launch in China, expected in FY19

Strong audience response to PJ Masks Live! US stage show, opened October 2017

PJ Masks S3 greenlight anticipated in H2

Cupcake & Dino: General Services in production, with Netflix, Teletoon Canada and Disney Channel Latin America attached

Ricky Zoom now in production with broadcast partners from France, Italy and Latin America attached. Master toy licence currently in final stages of negotiation

Ricky Zoom and Cupcake & Dino: General Services expected to be delivered to broadcast partners in FY19

Family currently working on 10 development projects

entertainmentone.com

Key titles Revenue growth due to strong international sales of Designated Survivor and AMC series

Private Eyes renewed for third series after international audience success

The Other Guy, eOne’s first Australian production, positively received by audiences

US unscripted growth balanced by weaker performance from the Canadian unscripted slate

H1 Progress

Television 82% of FY18 forecast margin committed or greenlit

6

301

Key titles Key renewals for H2: • ICE – S2 • Mary Kills People – S2 • Ransom – S2 • Cardinal – S2 and S3 • You Me Her – S3 • Private Eyes – S3

New drama deliveries: • The Detail: November 2017 • Let’s Get Physical: December 2017 • Burden of Truth: December 2017 • Sharp Objects: May 2018

US unscripted set for a strong H2

International sales of key shows anticipated to be robust

Outlook

Half hours of produced/ acquired content delivered (2016: 360)

£96m Investment in produced and acquired content (2016: £75m)

900 Half hours of produced/ acquired content expected

£200m Investment in produced and acquired content

entertainmentone.com

Designated Survivor S2 deliveries continue into H2

50 projects in active development

New TV projects delivered: • Youth & Consequences: for YouTube Red

Molly’s Game slated for release on 25 December

New series The Rookie for ABC

Movies in development: • The Chronicles of Narnia: The Silver Chair • The Killer • All the Old Knives

Substantial revenue and EBITDA increases due to global success of Designated Survivor S1 and S2

Key shows recommissioned: • Grey’s Anatomy – S14 • Criminal Minds – S13 • Ray Donovan – S6 • Quantico – S3

Key movies: • Molly’s Game • Murder on The Orient Express:

currently in cinemas • The Nutcracker and the Four Realms:

in post-production

Key titles H1 Progress

The Mark Gordon Company 91% of FY18 forecast margin committed or greenlit

7

Outlook

21 Half hours of produced content (2016: 10)

£34m Investment in produced content (2016: £25m)

60 Half hours of produced content

£80m Investment in produced content

Key partners

entertainmentone.com

Key titles Outlook H1 Progress

Film Migration from acquisition to production under way

8

Lower profile films and fewer releases in H1 reduce revenue

Business reshaping efficiencies started in FY16 deliver £10m annualised savings by FY18

Investment in productions net of tax credits increased to £22m (2016: inflow of £4m)

Key releases during the period: • Detroit • Valerian and the City of a Thousand

Planets • Hampstead • Logan Lucky

Key titles

76 Theatrical releases in H1 (2016: 88)

£71m

£22m

Investment in acquired content (2016: £98m)

Investment in productions (2016: £4m inflow)

Release slate for H2 includes: • The Post • A Bad Moms Christmas • Molly’s Game

New producer relationships: • Brad Weston/MAKEREADY • Neal Moritz (Fast and Furious) • Andy and Barbara Muschetti (It)

Ongoing streamlining anticipated to deliver around £8m in annualised savings by FY20 across Film and Television

48 Unique titles released in H1 (2016: 49)

180 Theatrical releases expected in FY18

£130m

£50m

Investment in acquired content

Investment in productions

100 Unique titles expected in FY18

entertainmentone.com

Lower revenue for the period due to prior year release of The Lumineers’ hit album, Cleopatra

Increase in digital revenue offsets continued decline in physical

EBITDA up 16% with improved margins, despite 9% lower revenue

110 digital single releases (2016: 98)

Artist management activities continue to perform strongly: • Arkells: Knocking At The Door • Jax Jones: You Don’t Know Me now

Platinum status in 20 countries • Lights: successful new album release,

Skin & Earth

Music continues to transition to higher margin digital sales

Recent music label album releases will drive revenues in H2 and beyond from acts including: • Death From Above • Emily Haynes & The Soft Skeleton • The Bloody Beetroots • Stars • Wu-Tang

Music supervision across a number of eOne projects: • Ice S2 • Let’s Get Physical • Molly’s Game • Ricky Zoom • PJ Masks Live! Tour

Key artists H1 Progress

Music Digital transition drives improved margins

9

Key artists Outlook

entertainmentone.com

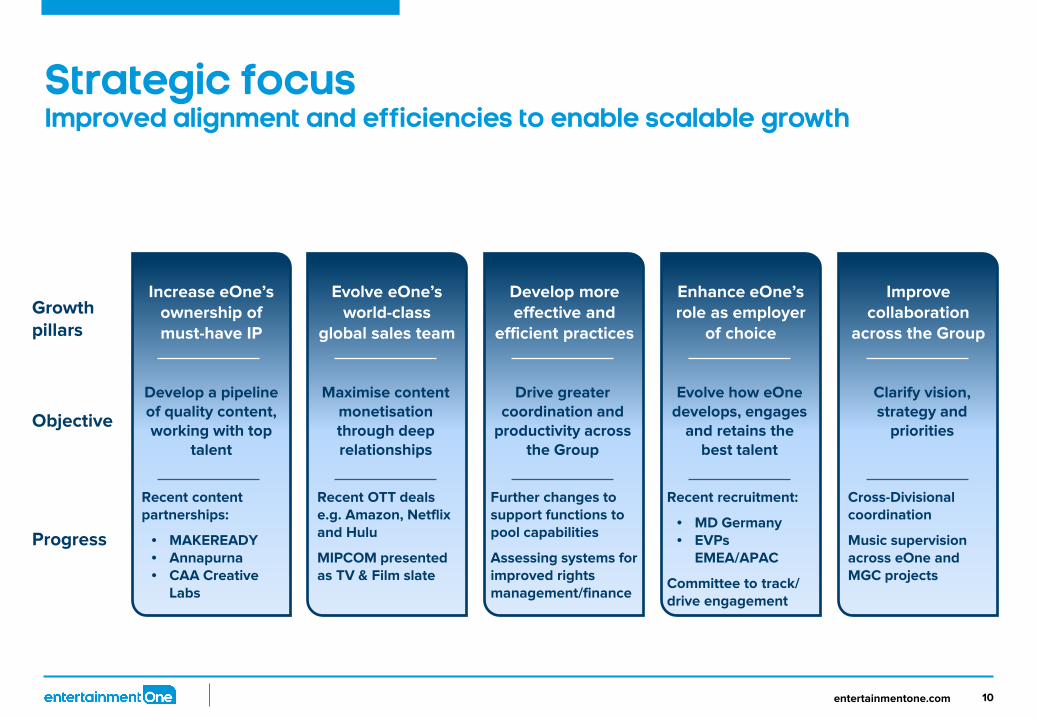

Strategic focus Improved alignment and efficiencies to enable scalable growth

10

Growth pillars

Objective

Progress

Recent content partnerships:

• MAKEREADY • Annapurna • CAA Creative

Labs

Increase eOne’s ownership of must-have IP

Develop a pipeline of quality content, working with top

talent

Recent OTT deals e.g. Amazon, Netflix and Hulu

MIPCOM presented as TV & Film slate

Evolve eOne’s world-class

global sales team

Maximise content monetisation through deep relationships

Further changes to support functions to pool capabilities

Assessing systems for improved rights management/finance

Develop more effective and

efficient practices

Drive greater coordination and

productivity across the Group

Recent recruitment:

• MD Germany • EVPs

EMEA/APAC

Committee to track/ drive engagement

Enhance eOne’s role as employer

of choice

Evolve how eOne develops, engages

and retains the best talent

Cross-Divisional coordination

Music supervision across eOne and MGC projects

Improve collaboration

across the Group

Clarify vision, strategy and

priorities

entertainmentone.com

Library valuation process and methodology Annual independent valuation of eOne’s content

11

eOne provides historic performance of each segment and projections for new titles to Salem Partners

Salem evaluates projections using historical performance for similar content and its own models

• Los Angeles-based financial services group, founded in 1997

• Widely-respected industry experts in the valuation of intellectual property

• Independent financial and valuation opinions recognised and approved by major regional and national accounting and law firms, major commercial banks and institutional investors

Management fee and tax deducted from cash flows

Post-tax cash flows discounted using eOne WACC over 10 years with terminal value

Deduct NPV of future advance obligations to arrive at final library valuation

entertainmentone.com

55%

45%

2017

Family

Film andTelevision

Library valuation up 13%

12

As at 31 March 2017, the overall value of the Group’s independent content library valuation increased to US$1.7 billion - The annual independent library valuation includes

eOne’s share of all of the Group’s television, family, film and music assets as at 31 March 2017

- Key valuation assumptions consistent year-on-year

- No significant change in Divisional split

Key assumptions FY16 FY17

Discount rate 8.2% 7.9%

Admin & OH rate 6.0% 6.0%

FX rates:

CAD 0.77 0.81

GBP 1.44 1.40

EUR 1.13 1.20

AUD 0.76 0.80

US$1,700m

entertainmentone.com

13 entertainmentone.com

Financial review

entertainmentone.com 14

Half Year Financial Highlights

entertainmentone.com

Revenue £395.7m Stable Growth across Family and Television offset by decline in Film

EBITDA1 £51.4m 36.3% Growth in Family and Television

EBITDA margin 13.0% 3.6pts Growth of Family and lower costs in Film

EPS2 4.8p 2.2p

Free cash outflow3 £66.6m £1.3m Broadly stable

Net debt £312.8m £49.5m Includes cash outflows due to prior years’ restructuring

entertainmentone.com 15

Revenue consistent period-on-period Revenue growth in Television and Family offset by Film

Period-on-Period Divisional Revenue Bridge

Group revenue 1.3% – Strong Television growth from higher international

distribution sales for third party content in eOne Television and strong revenues from Designated Survivor seasons 1 and 2

– Family growth driven by significant growth of PJ Masks and continued strong performance from Peppa Pig

– Film decline reflecting lower box office and lower profile of films compared to the prior period

Foreign exchange – Translation impact of weaker pound against the US,

Canadian and Australian dollar and the euro – underlying revenue decline on a constant currency basis was 5.0%

£m 2017 2016. Change

Television 168.5 144.5. 16.6%

eOne Television 118.9 ‘98.0. 21.3%

The Mark Gordon Company 51.6 28.3. 82.3%

Music 23.4 25.8. (9.3%)

Television eliminations (25.4) (7.6). (234.2%)

Family 62.1 37.9. 63.9%

Film 171.8 242.0. (29.0%)

Total Divisional Revenue 402.4 424.4. (5.2%)

Group eliminations (6.7) (23.4). 71.4%

Total Group Revenue 395.7 401.0. (1.3%)

£424.4m £402.4m

£24.0m £24.2m (£70.2m)

2016 Television Family Film 2017

entertainmentone.com 16

£m 2017 2016 Change

Television 20.6 18.5. 11.4%

eOne Television 7.8 7.1. 9.9%

The Mark Gordon Company 9.9 9.0. 10.0%

Music 2.9 2.5. 16.0%

Family 38.1 24.7. 54.3%

Film (2.6) (2.3). (13.0%)

Total Divisional EBITDA 56.1 40.9. 37.2%

Group eliminations (0.1) -.. -

Group costs (4.6) (3.2). (43.8%)

Total Group EBITDA 51.4 37.7. 36.3%

EBITDA Margin % 13.0% 9.4% 360bps

EBITDA up 36.3% Growth driven by Television and Family with lower costs in Film

Period-on-Period EBITDA Bridge

£37.7m

£51.4m £2.1m

£13.4m (£0.3m) (£0.1m) (£1.4m)

2016 Television Family Film Group elims Centre 2017

Group EBITDA 36.3% – Strong performance by increased revenue across eOne

Television and MGC and improved margins in Music due to continued shift from physical to digital

– Family EBITDA growth from strong performance of PJ Masks and Peppa Pig

– Film EBITDA benefitted from gross margin improvements due to lower P&A spend and amortisation of acquired content and costs savings from prior years’ restructuring

Foreign exchange – Translation impact of weaker pound against the US,

Canadian and Australian dollar and the euro – underlying EBITDA growth on a constant currency basis was 33.5%

entertainmentone.com 17

Adjusted cash outflow lower by £12.5 million Reflecting strong cash generation in Family

Adjusted cash outflow lower than prior period by £12.5 million – Strong cash generation in Family driven by revenue growth

– Reduced investment in acquired content rights in Film due to limited higher profile films partly offset by lower amortisation driven by lower revenue

Negative free cash flow of £66.6 million, after interest, tax and capex – Driven by timing of tax payments

2017 2016

£m Television Family Film Centre &

Elims Total Television Family Film Centre &

Elims Total

Underlying EBITDA (exc. Production) 18.5 38.4 (2.7) (4.7) 49.5 21.2 24.8 (3.2) (3.2) 39.6

Amortisation of investment in acquired content rights 18.8 0.4 35.1 - 54.3 15.6 0.4 54.4 - 70.4

Investment in acquired content rights (15.7) (1.2) (71.2) - (88.1) (13.2) (0.7) (97.7) - (111.6)

Amortisation of investment in productions 19.3 1.2 2.3 - 22.8 20.1 (0.2) 0.8 - 20.7

Investment in productions, net of grants (31.6) (2.0) (1.3) 0.3 (34.6) (18.6) (1.1) 0.6 - (19.1)

Working capital - (10.4) (25.4) - (35.8) (13.8) (6.6) (24.4) - (44.8)

Joint venture movements - - - - - 0.4 - - - 0.4

Adjusted cash flow 9.3 26.4 (63.2) (4.4) (31.9) 11.7 16.6 (69.5) (3.2) (44.4)

Capital expenditure (1.5) (0.9)

Tax paid (21.7) (7.1)

Net interest paid (11.5) (12.9)

Free cash flow (66.6) (65.3)

entertainmentone.com 18

Net debt higher including cash outflows due to prior years’ restructuring costs

£m 2017 2016

Net debt (312.8) (263.3)

Net debt higher than prior period driven by: – Higher one-off items including financing (2017: £41.2m,

2016: £7.7m) including prior years’ restructuring as anticipated

Full year leverage expected to be 1.3x

entertainmentone.com 19

Full Year Outlook: Update 2018 Guidance Television May 2017 guidance Latest FY18

Investment in productions, eOne Television £170.0 million £160.0 million

Investment in acquired content, eOne Television £40.0 million £40.0 million

Investment in productions, The Mark Gordon Company £80.0 million £80.0 million

Half hours produced/acquired, eOne Television 1,000 900

Half hours produced, The Mark Gordon Company 75 60

Family May 2017 guidance Latest FY18

Investment in productions £5.0 million £5.0 million

Investment in acquired content £4.0 million £4.0 million

Film May 2017 guidance Latest FY18

Investment in acquired content £150.0 million £130.0 million

Investment in productions £50.0 million £50.0 million

No. of theatrical releases 200 180

No. of unique theatrical releases 100 100

May 2017 guidance Latest FY18

Amortisation of acquired intangibles £40.0 million £40.0 million

Operating one-off items £5.0 million £7.0 million

Net debt to Group EBITDA leverage 1.2x 1.3x

entertainmentone.com

Summary

Strong performance for the first half across the Group

Family ahead of expectations, driven by Peppa Pig in China and PJ Masks

Television pipeline robust, with a slate of new shows and recommissions

Film migrating from acquisition to production

Further reshaping will generate additional operational and financial benefits

Library valuation increased by 13% to US$1.7 billion

Full year in line with management expectations

20

entertainmentone.com

Q&A

21 entertainmentone.com

entertainmentone.com

Appendix

22 entertainmentone.com

entertainmentone.com 23

Reconciliation between H1 18 and H1 17 reported and adjusted earnings

2017 Restated 2016

£m Reported Adjustments Adjusted Reported Adjustments Adjusted

Underlying EBITDA 51.4 - 51.4 37.7 - 37.7

Amortisation of acquired intangibles (20.0) 20.0 - (20.7) 20.7 -

Depreciation/amortisation of software (1.9) - (1.9) (2.4) - (2.4)

Share-based payment charge (5.8) 5.8 - (2.8) 2.8 -

One-off items (3.3) 3.3 - 1.4 (1.4) -

Net finance charges (19.6) 6.5 (13.1) (15.7) 4.2 (11.5)

Profit/(loss) before tax 0.8 35.6 36.4 (2.5) 26.3 23.8

Tax 0.5 (9.5) (9.0) 1.3 (6.5) (5.2)

Profit/(loss) after tax 1.3 26.1 27.4 (1.2) 19.8 18.6

Less: Non-controlling interest (3.5) (2.8) (6.3) (4.7) (2.5) (7.2)

(Losses)/earnings (2.2) 23.3 21.1 (5.9) 17.3 11.4

Diluted (losses)/earnings per share (p) (0.5) 5.3 4.8 (1.4) 4.0 2.6

23

entertainmentone.com 24

One-off items

£m 2017 2016

Restructuring costs

Strategy-related 0.8 5.7

Total restructuring costs 0.8 5.7

Other items

Acquisition costs/(gains) 2.2 (9.0)

Other items 0.3 1.9

Total other items 2.5 (7.1)

Total one-off costs/(gains) 3.3 (1.4)

entertainmentone.com 25

Production financing cash flow 2017 2016

£m Television Family Film Total Television Family Film Total

Production underlying EBITDA 2.1 (0.3) 0.1 1.9 (2.7) (0.1) 0.9 (1.9)

Amortisation of investment in productions 23.5 0.1 4.0 27.6 21.9 1.3 21.8 45.0

Investment in productions, net of grants (84.2) (2.0) (20.9) (107.1) (70.3) (0.5) 3.1 (67.7)

Working capital 58.7 (0.1) 28.9 87.5 33.2 (0.5) (13.2) 19.5

Adjusted cash flow 0.1 (2.3) 12.1 9.9 (17.9) 0.2 12.6 (5.1)

Capital expenditure - (0.1)

Tax paid (1.0) (1.6)

Net interest paid (0.7) -

Production free cash flow 8.2 (6.8)

entertainmentone.com 26

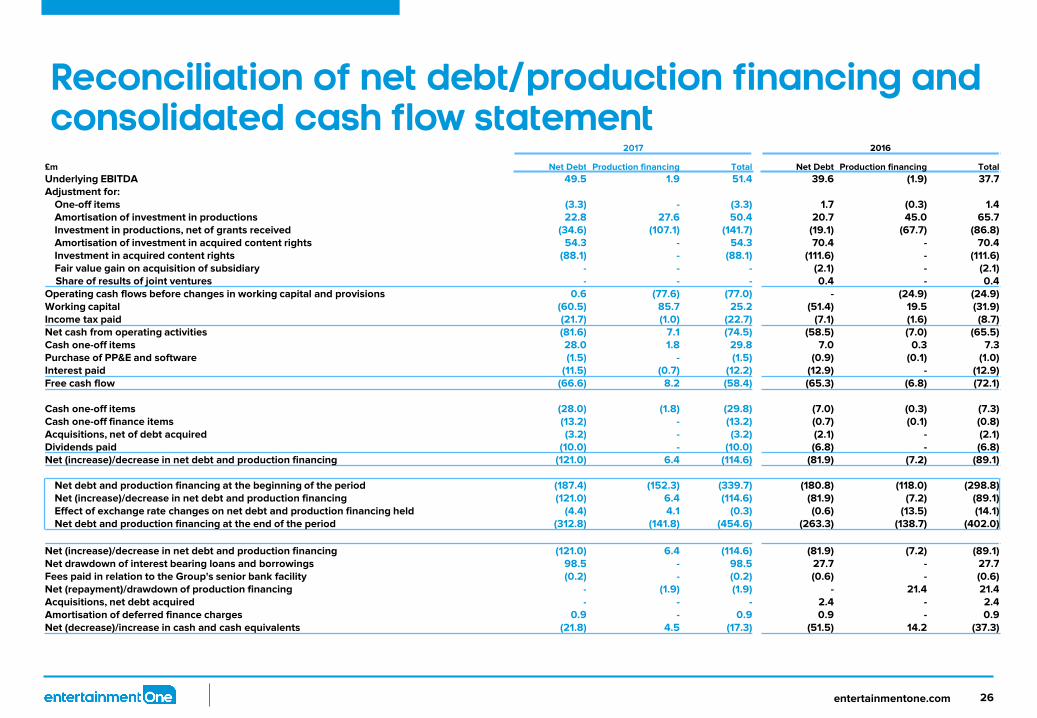

Reconciliation of net debt/production financing and consolidated cash flow statement

2017 2016

£m Net Debt Production financing Total Net Debt Production financing Total

Underlying EBITDA 49.5 1.9 51.4 39.6 (1.9) 37.7 Adjustment for:

One-off items (3.3) - (3.3) 1.7 (0.3) 1.4 Amortisation of investment in productions 22.8 27.6 50.4 20.7 45.0 65.7 Investment in productions, net of grants received (34.6) (107.1) (141.7) (19.1) (67.7) (86.8) Amortisation of investment in acquired content rights 54.3 - 54.3 70.4 - 70.4 Investment in acquired content rights (88.1) - (88.1) (111.6) - (111.6) Fair value gain on acquisition of subsidiary - - - (2.1) - (2.1)

Share of results of joint ventures - - - 0.4 - 0.4 Operating cash flows before changes in working capital and provisions 0.6 (77.6) (77.0) - (24.9) (24.9) Working capital (60.5) 85.7 25.2 (51.4) 19.5 (31.9) Income tax paid (21.7) (1.0) (22.7) (7.1) (1.6) (8.7) Net cash from operating activities (81.6) 7.1 (74.5) (58.5) (7.0) (65.5) Cash one-off items 28.0 1.8 29.8 7.0 0.3 7.3 Purchase of PP&E and software (1.5) - (1.5) (0.9) (0.1) (1.0) Interest paid (11.5) (0.7) (12.2) (12.9) - (12.9) Free cash flow (66.6) 8.2 (58.4) (65.3) (6.8) (72.1)

Cash one-off items (28.0) (1.8) (29.8) (7.0) (0.3) (7.3) Cash one-off finance items (13.2) - (13.2) (0.7) (0.1) (0.8) Acquisitions, net of debt acquired (3.2) - (3.2) (2.1) - (2.1) Dividends paid (10.0) - (10.0) (6.8) - (6.8) Net (increase)/decrease in net debt and production financing (121.0) 6.4 (114.6) (81.9) (7.2) (89.1)

Net debt and production financing at the beginning of the period (187.4) (152.3) (339.7) (180.8) (118.0) (298.8) Net (increase)/decrease in net debt and production financing (121.0) 6.4 (114.6) (81.9) (7.2) (89.1) Effect of exchange rate changes on net debt and production financing held (4.4) 4.1 (0.3) (0.6) (13.5) (14.1) Net debt and production financing at the end of the period (312.8) (141.8) (454.6) (263.3) (138.7) (402.0)

Net (increase)/decrease in net debt and production financing (121.0) 6.4 (114.6) (81.9) (7.2) (89.1) Net drawdown of interest bearing loans and borrowings 98.5 - 98.5 27.7 - 27.7 Fees paid in relation to the Group's senior bank facility (0.2) - (0.2) (0.6) - (0.6) Net (repayment)/drawdown of production financing - (1.9) (1.9) - 21.4 21.4 Acquisitions, net debt acquired - - - 2.4 - 2.4 Amortisation of deferred finance charges 0.9 - 0.9 0.9 - 0.9 Net (decrease)/increase in cash and cash equivalents (21.8) 4.5 (17.3) (51.5) 14.2 (37.3)

entertainmentone.com 27

Analysis of net debt and cash

£m 2017 2016

£285m Senior secured notes at 6.875% (285.0) (285.0)

Bank borrowings (94.4) (32.5)

Cash (net of overdrafts) 59.4 45.7

Deferred finance charges 7.7 9.1

Other (0.5) (0.6)

Net debt (312.8) (263.3)

entertainmentone.com 28

Notes 1. Underlying EBITDA is operating profit or loss excluding amortisation of acquired intangibles; depreciation; amortisation of software; share-based payment

charge; tax, finance costs and depreciation related to joint ventures; and operating one-off items. Underlying EBITDA is reconciled to operating profit in the Other Financial Information section of the Interim Announcement.

2. Adjusted profit before tax and adjusted diluted earnings per share are the reported measures excluding amortisation of acquired intangibles; share-based payment charge; tax, finance costs and depreciation related to joint ventures; operating one-off items; finance one-off items; and, in the case of adjusted diluted earnings per share, one-off tax items. Refer to the Other Financial Information section of the Interim Announcement for a reconciliation of adjusted profit before tax and Note 6 in the condensed consolidated financial statements for the adjusted diluted earnings per share reconciliation.

3. Free cash flow is calculated from cash flows associated with the net debt of the Group. It excludes cash flows associated with production activities. Free cash flow is adjusted cash flow less capital expenditure, net interest paid and tax paid. It is measured excluding one-off items. Adjusted cash flow is underlying EBITDA (excluding EBITDA related to Production Financing), amortisation of investment in acquired content rights, investment in acquired content rights, amortisation of investment in productions, investment in productions (net of grants), working capital and joint venture movements.

entertainmentone.com 29

Important information

This confidential presentation (including any oral information, question and answer session and any other document or materials distributed at or in connection with this presentation) (the “Presentation”) has been prepared by Entertainment One Ltd. (the “Company”), and contains confidential information regarding the Company, its business and operations and members of its group (“Group”). It is provided for the exclusive use of the persons provided with the Presentation, and the Presentation and any further confidential information made available to any recipient, either verbally or in writing, must be held in complete confidence and without prejudice to the aforesaid, such information and documents containing such information may not be reproduced, used or in any way disclosed without the prior written consent of the Company.

This Presentation is not intended to form the basis of any investment activity or decision, and should not be considered as a recommendation by the Company that any recipient should acquire any interest in the share capital or in any other interest in the Company. It does not constitute or form part of and should not be relied upon in connection with any offer or invitation to sell or issue, or a solicitation of an offer or invitation to purchase or subscribe for, any securities or other interests in the Company or any related entity and no legal relations shall be created by its issue.

The contents of this Presentation have not been approved for distribution in the UK by an authorised person for the purposes of Section 21 of the Financial Services and Markets Act 2000 (“FSMA”). This Document may only be communicated or caused to be communicated in the UK to: (1) persons authorised to carry on a regulated activity (“Authorised Persons”) under FSMA; (2) persons otherwise having professional experience in matters relating to investments and qualifying as investment professionals under Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”); (3) persons qualifying as high net worth individuals under Article 48 of the Order; (4) persons qualifying as high net worth companies or unincorporated associations under Article 49 of the Order; or (5) to any other person to whom this Document may otherwise lawfully be communicated or caused to be communicated, including the recipients (“Relevant Persons” ).

The distribution of the Presentation in certain jurisdictions may be restricted by law and therefore persons into whose possession this document comes should inform themselves about and observe such restrictions. Any person who receives this Presentation in violation of such restrictions should not act upon it and should return it to the Company immediately. The Presentation is not directed to, or intended for distribution or use by any persons or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction. In particular, this Presentation (and the information contained in it) is not for release, publication or distribution, directly or indirectly, in the United States (or for the account of any "U.S. Person" as defined in Regulation S under the US Securities Act 1933), Australia, New Zealand, Canada, Japan or South Africa. Persons into whose possession this Presentation comes should inform themselves about and observe such restrictions.