enhancing international competitiveness and inclusive...

TRANSCRIPT

ENHANCING INTERNATIONAL COMPETITIVENESS AND INCLUSIVE ECONOMIC

DEVELOPMENT

Prof. Dr. Sri AdiningsihChairperson of Presidential Advisory Council

Republic of Indonesia

Indonesia Australia Business ConferenceYogyakarta, 16 November 2015

i

expanding to Eastern Europe

expanding to Latin America

GLOBAL ECONOMIC INTEGRATIONNAFTAPopulation: 469.9 millionGDP: US$20,345.4 billion

EUPopulation: 505,7 millionGDP PPP: US$ 17,578.4 billion

CHINA Population: 1,360.8 million GDP PPP : US$ 16,149.1 billion

JAPANPopulation: 127.3 million GDP PPP : US$ 4,667.6 billion

ASEANPopulation: 625 millionGDP PPP: US$ 3,852.3 billion

FTA Canada – Chile 1997FTA : Chile – Mexico 1999FTA : USA – Chile 2004FTA : USA – Singapore 2004FTA : USA – Australia 2005FTA : Mexico – Japan 2005FTA : Chile – Brunei – NZ –Singapore 2006

MERCOSURArgentina, Brazil,

Paraguay, Uruguay

FTAA(by 2005)

under negotiation

NAFTAU.S.A.,

Canada,Mexico

SAPTABangladesh, Bhutan,

India, Maldives,Nepal, Pakistan, Sri Lanka

China - ASEAN FTA

ASEAN-Japan Comprehensive Economic

Partnership (AJCEP)

Japan-Korea FTA(under negotiation)

Japan-Mexico EPA(signed agreement)

Japan’s Bilaterals:•Japan-Singapore EPA •Japan-Philippines EPA•Japan-Thailand EPA•Japan-Malaysia EPA•Japan-Indonesia EPA

AFTAIndonesia, Malaysia, Philippines,

Singapore, Thailand, Brunei, Vietnam, Laos, Myanmar, Cambodia

India - ASEAN FTA

EU-MEXICO FTA

EU25 countries

ACP-EUCountries in Africa and

the Caribbean (approx. 70 countries)

Japan-Mexico EPA

(signed agreement)

Japan-Korea-China FTA (under negotiation)

Australia-New Zealand-ASEAN FTA

Korea - ASEAN FTA2015: 612 RTAs,406 in force Source: WTO (2015)

• Slow economic recovery in Europe• Normalization of US Fed Funds Rate may

take years• Economic growth in Japan & China has

been declining• Rising global economic and financial

volatilities• Low commodity prices

External Condition

DOMESTIC ECONOMIC CONDITION

Inflation Rate, 2014 – 2015* (YoY, %)

*= October 2015

Source : BPS;CEIC (2015)

0

1000

2000

3000

4000

5000

6000

11000

11500

12000

12500

13000

13500

14000

14500

15000

IDR/USD (LHS) IDX (RHS)

Indonesia Exchange Rate and Indonesia Composite Index

2014 – 2015*

* = November 2015Source : BI; CEIC (2015)

International Reserve2013 – 2015 * (in USD Billion)

* = October 2015Source: BI; CEIC (2015)

12/2014, 112

2/2015, 116

10/2015, 101

90

95

100

105

110

115

120

Growth Rate of GDP by Expenditure, 2011 – 2015*Base Year 2010 (YoY, %)

* = Q3 2015Source : BPS; CEIC (2015)

Q3 2015 OVER Q3 2014 : Government Consumption = 6.56%; Non-Profit Institutions Servings Households Consumption =6.39%;Household Consumption = 4.96%; Gross Fixed Capital Formation = 4.62%; Export = -0.69%; Import = - 6.11%;

Growth Rate of GDP by Industrial Origin, 2013-2015*Base Year 2010 (YoY, %)

* = Q3 2015Source : BPS;CEIC (2015)

Q3 2015 OVER Q3 2014 : Information & Communication = 10.83%; Financial & Insurance Activity=10.35%; Education Services=8.25%; Other Services=8.15%; Mining & Quarrying= -5.64%;

Domestic ForeignUnit Rp trillion Unit USD billion

2011:Q1 250 14.1 902 4.42011:Q2 511 18.9 1456 4.82011:Q3 318 19.0 1236 5.22011:Q4 397 24.0 1300 5.12012:Q1 363 19.7 1454 5.72012:Q2 416 20.8 1499 6.22012:Q3 303 25.2 1233 6.32012:Q4 706 26.5 2286 6.32013:Q1 434 27.5 2013 7.02013:Q2 641 33.1 2834 7.22013:Q3 439 33.5 2175 7.02013:Q4 615 34.0 2590 7.42014:Q1 437 34,.6 2642 6.92014:Q2 477 38.2 3267 7.42014:Q3 507 41.6 2374 7.52014:Q4 971 41.7 4349 6.82015:Q1 876 42.5 3143 6.62015:Q2 1874 42.9 4460 7.4

* = q2 2015Source: BKPM;CEIC (2015)

Investment Realization , 2011 – 2015*Investment Realization , 2011 – 2015*

* = September 2015Source: BPS ;CEIC (2015)

-444

843669

-1,963

53

-288

42

-312 -270

21

-425

187

633 663

1,026

477

1,077

528

1,384

328

1,017

-2,500

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500

1/2014 2/2014 3/2014 4/2014 5/2014 6/2014 7/2014 8/2014 9/2014 10/2014 11/2014 12/2014 1/2015 2/2015 3/2015 4/2015 5/2015 6/2015 7/2015 8/2015 9/2015

Balance of Trade, 2014 – 2015* (USD million)

Balance: Non-oil and Gas Balance: Oil and Gas Trade Balance

* = Q2 2015Source: BI ;CEIC (2015)

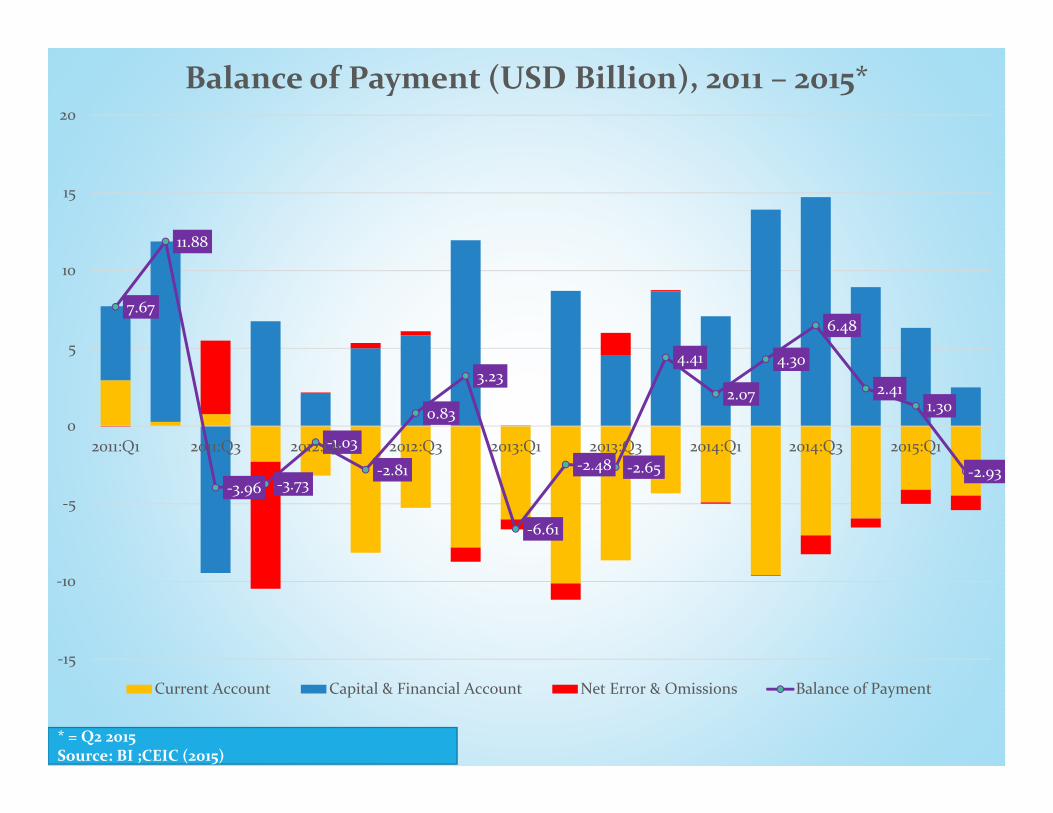

7.67

11.88

-3.96 -3.73

-1.03

-2.81

0.83

3.23

-6.61

-2.48 -2.65

4.41

2.07

4.30

6.48

2.411.30

-2.93

-15

-10

-5

0

5

10

15

20

2011:Q1 2011:Q3 2012:Q1 2012:Q3 2013:Q1 2013:Q3 2014:Q1 2014:Q3 2015:Q1

Balance of Payment (USD Billion), 2011 – 2015*

Current Account Capital & Financial Account Net Error & Omissions Balance of Payment

* = August 2015Source: Ministry of Finance; CEIC (2015)

External Debt, 2012 – 2015 *(USD Billion)External Debt, 2012 – 2015 *(USD Billion)

Poverty, 2009- March 2015

Source: BPS (2015)

32.5 31.0 30.1 30.0 29.3 28.7 28.2 28.6 28.3 27.7 28.6

14.2 13.3 12.5 12.5 12.0 11.7 11.4 11.5 11.3 11.0 11.2

2009 2010 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15

Number of Poor Percentage of Poor

Unemployment Rate, February 2010 – August 2015 (%)

Source: BPS (2015)

Note: * China including Taiwan,Source: United Nations Development Program; World Bank; World Economic Forum (2015)Note: * China including Taiwan,Source: United Nations Development Program; World Bank; World Economic Forum (2015)

HUMAN DEVELOPMENT INDEX, EASE OF DOING BUSINESS, AND GLOBAL COMPETITIVENESS INDEX: APEC ECONOMIES

ECONOMIES (Alphabetical Order)

Human Development Index, 2014 Ease of Doing Business, 2016 Global Competitiveness Index, 2015-2016

from 187 countries from 189 countries from 140 countries

Value Categorize Rank Categorize Rank ValueGDP (PPP)

share as (%) world total

Rank

Australia 0.933 Very High HDI 2 High Income 13 5.15 1.02 21Brunei Darussalam 0.852 Very High HDI 30 High Income 84 n/a n/a n/aCanada 0.902 Very High HDI 8 High Income 14 5.31 1.48 13Chile 0.822 Very High HDI 41 High Income 48 4.58 0.38 35China* 0.719 High HDI 91 Upper Middle Income 84 4.89 16.32 28Hong Kong, China (SAR) 0.891 Very High HDI 15 High Income 5 5.46 0.37 7Indonesia 0.684 Medium HDI 108 Lower Middle Income 109 4.52 2.48 37Japan 0.890 Very High HDI 17 High Income 34 5.47 4.40 6Korea (Republic of) 0.891 Very High HDI 16 High Income 4 4.99 1.65 26Malaysia 0.773 High HDI 62 Upper Middle Income 18 5.23 0.69 18Mexico 0.756 High HDI 71 Upper Middle Income 38 4.29 1.98 57New Zealand 0.910 Very High HDI 7 High Income 2 5.25 0.15 16Papua New Guinea 0.491 Low HDI 157 Lower Middle Income 145 n/a n/a n/aPeru 0.737 High HDI 82 Upper Middle Income 50 4.21 0.34 69The Philippines 0.660 Medium HDI 117 Lower Middle Income 103 4.39 0.64 47Russian Federation 0.778 High HDI 57 High Income 51 4.44 3.30 45Singapore 0.901 Very High HDI 9 High Income 1 5.68 0.42 2Thailand 0.722 High HDI 89 Upper Middle Income 49 4.64 0.91 32United States 0.914 Very High HDI 5 High Income 7 5.61 16.14 3Viet Nam 0.638 Medium HDI 121 Lower Middle Income 90 4.30 0.47 56

THE POTENCIES

4.1

2.82.2 2.3 2.5

8.1

4.8

5.75.0

4.3

7.4

4.7 4.1 4.33.9

6.2 6.5 6.35.8

5.1

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2010 2011 2012 2013 2014

World ASEAN Asia Indonesia

Economic Growth, 2010 - 2014 (YoY, %)

Source: World Bank (2015)

Indonesia Nominal GDP Per Capita2001 - 2014

Indonesia Nominal GDP Per Capita2001 - 2014

19.9 20.5 21.2 22.022.9

23.925.1

26.227.1

28.429.8

31.232.5

33.7

4,812 5,037 5,311 5,656 6,089

6,534 7,041

7,511 7,816 8,294

8,870 9,449

9,995 10,517

-

2,000

4,000

6,000

8,000

10,000

12,000

10.0

15.0

20.0

25.0

30.0

35.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Million Rupiah PPP Current USD (RHS)

Source: World Bank (2015)

Demographic Bonus

Source: MP3EI

Middle Income Class Estimation: ADB

Source: McKinsey (2012)

Indonesian Middle Income Class Estimation: McKinsey Global Institute

National Medium-Term Development Plan (RPJMN)

2015 - 2019

National Development Agenda in RPJMN 2015 - 2019

I. Human DevelopmentII. Improving International

Competitiveness and National Productivity

III. Developing Local Economy

I. HUMAN DEVELOPMENT

Primary students receiving benefits through IndonesiaSmart Card = 15,380,582 (2015)Secondary students receiving benefits throughIndonesia Smart Card = 3,856,476 (2015)College students receiving BIDIK-MISI scholarship =269,905 (2015)Percentage of social security health membership =minimum 95% (2019)Improvement of public health services = “KartuIndonesia Sehat”Improvement of public welfares = “Kartu KeluargaSejaterah”

Source : RPJMN 2015 - 2019

Some Important Programs

II. IMPROVING INTERNATIONAL COMPETITIVENESS AND

NATIONAL PRODUCTIVITY

Some Important PoliciesBuilding toll roads: Trans-Sumatera, Samarinda-Balikpapan, Trans – Java, Manado-Bitung (2015-2019)Construction of dry port facility in a high economicgrowth area (Kendal and Paciran) (2015-2019)Railway construction:Trans Kalimantan, Sulawesi, and Papua, Trans Sumatrarailway (2015-2019)Development of fixed / wire line broadband, includingin the area of the state border (2015-2019)

Source : RPJMN 2015 - 2019

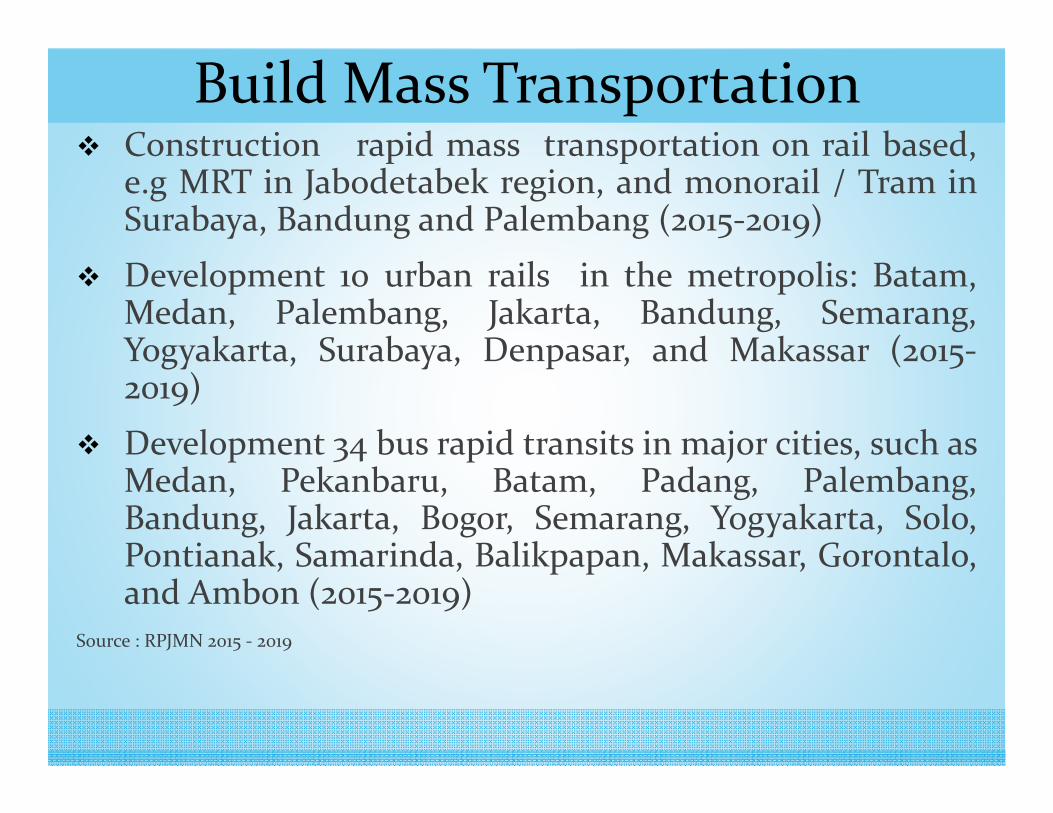

Build Mass Transportation Construction rapid mass transportation on rail based,e.g MRT in Jabodetabek region, and monorail / Tram inSurabaya, Bandung and Palembang (2015-2019)

Development 10 urban rails in the metropolis: Batam,Medan, Palembang, Jakarta, Bandung, Semarang,Yogyakarta, Surabaya, Denpasar, and Makassar (2015-2019)

Development 34 bus rapid transits in major cities, such asMedan, Pekanbaru, Batam, Padang, Palembang,Bandung, Jakarta, Bogor, Semarang, Yogyakarta, Solo,Pontianak, Samarinda, Balikpapan, Makassar, Gorontalo,and Ambon (2015-2019)

Source : RPJMN 2015 - 2019

Strengthening InvestmentIndonesia Investment Coordinating Board (BKPM) officiallylaunched the One Stop Service (OSS) Center, buildingonline monitoring service (2015)Investment licenses process = 15 days (2019)Starting a business procedure = 7 days and 5 procedures(2019)Increase investment growth/gross fixed capital formation =12.1% (2019)Increase domestic and foreign investment to IDR 933trillion in 2019 with the contribution of domesticinvestment, which increased to 38.9%

Source : RPJMN 2015 - 2019

Improve the Competitiveness of Labor

Build 100 Techno Park in the district / city andthe Science Park in every provinceImproving the quality and skills of workers byincreasing the proportion of the workforcethat is competent and recognized nationallyand internationallyIncrease competitiveness of labor marketefficiency at the international level;Increase number of formal workers from40.5% in 2014 to 51% in 2019

Developing National Trade Capacity

Reduce logistics costs to GDP ratio by5.0% per yearDwelling time = 3 – 4 days (2019)Build / revitalize 5.000 local marketsIncrease the share of manufacturingexports amounted to 65% (2019)

Source : RPJMN 2015 - 2019

III. Developing Local Economy

Building irrigation network services 1 million hectares (2015 - 2019)Rehabilitation 3 million ha of irrigation (2015 - 2019)Building 49 dams (2015 - 2019)

Source : RPJMN 2015 - 2019

Increasing Food Production

Electricfication ratio 96.6% by buildingpower plant with capacity of 35.000megawatt (2019)Construction of oil refineries with atotal capacity of 300 thousand barrelsper day (2015 – 2019)Build floating storage regasification unit= 7 units (2015 – 2019)

Source: RPJMN 2015 - 2019

Increasing Energy Production

Developing Maritime and Marine Economic:

Developing 24 deep sea ports (2015 – 2019)

Strengthening the Financial Sector:Development and implementation of the Agricultural Insurance ProgramEstablishment of Agriculture and Maritime Bank, also Bank Infrastructure

Reducing energy subsidies so that ratio ofenergy subsidies decrease from 1.3% of GDP in2015 to 0.6% of GDP in 2019Capital expenditure raise from 2.4 % of GDP in2015 to 3.9% in 2019Ratio of government debt below 30% of GDPand are expected to continue to decline to 20%of GDP in 2019Budget deficit below 3% of GDP and in 2019 thebudget deficit could be achieved 1% of GDP

Source: RPJMN 2015 - 2019

Strengthening the State’s Fiscal Capacity

GROUNDBREAKING PROJECTS (1 of 3)COMMENCED ON PROJECTS LOCATION

20 December 2015 Raknamo Dam Kupang, NTT

20 January 2015 Tertiary Irrigation Development Pontianak

26 January 2015 Inaugurated One Stop Services Center Jakarta

27 January 2015Development of Port and Industrial Area Kuala Tanjung - Sei Mangkei, Toll Road Terrain - Binjai and Diversification Project Aluminium.

Kuala Tanjung - North Sumatera

23 February 2015 Special Economic Zone Tanjung Lesung Tanjung Lesung

29 April 2015

Desa Kuala Tanjung, Kecamatan Sei Suka, Kab. Batubara, Provinsi Sumatera Utara

Ungaran, Semarang –Central Java

Project: 1 Million Homes Ungaran, Semarang –Central Java

30 April 2015 –4 May 2015

1. Inaugurated the groundbreaking of Bakauheni-Terbanggi Besar Trans-Sumatera toll road

2. Inaugurated the groundbreaking of Palembang-Simpang Indralaya Trans-Sumatera toll road

3. Inaugurated the acceleration of Solo-Ngawi tollroad construction and Ngawi-Kertosono tollroad groundbreaking

Lampung

Palembang

Ngawi

Source : Ministry of State Secretary (2015)

GROUNDBREAKING PROJECTS (2 of 3)COMMENCED ON PROJECTS LOCATION

4 May 2015

Hydroelectric power plant Jatigede (2x55 Megawatt) Sumedang, West Java

Electric steam power plant Pangkalan Susu Unit III & IV (2x200 Megawatt)

Langkat, NorthSumatera

Electric steam power plant Takalar (2x100 Megawatt) South Sulawesi

7 May 2015Distributed “Magic Card”: Indonesian Health Card(KIS), Indonesian Smart Card (KIP), ProsperousFamily Card (KKS)

Buru Regency

9 May 2015 Flyover Hadami - Holtekam Jayapura, Papua

10 May 2015 Construction and inaugaration of the Sulawesi –Maluku – Papua Cable System (SMPCS) Manokwari, Papua

10 May 2015Named Merauke as the rice granary of Indonesia andset a target of 1.2 million hectares that must becompleted within three years

Merauke, Papua

21 May 2015 Terminal Teluk Lamong Surabaya, East Java

22 May 2015 Makassar New Port Makassar

27 May 2015 Pabrik Nikel Smelter PT Sulawesi Mining Investment. Morowali, Sulawesi

Source : Ministry of State Secretary (2015)

GROUNDBREAKING PROJECTS (3 of 3)COMMENCED ON PROJECTS LOCATION

25 June 2015 Bridge of Kotabaru – Pulau Laut Kotabaru – Southe Borneo

9 July 2015 Construction of Semarang-Solo toll road Section III Bawen - Salatiga

Central Java

9 September 2015

Light Rail Transit (LRT)

The 1st phase of RT construction began at the final quarter of 2015 and will be completed in the late of 2018, while the second phase will begin the final quarter of 2016 and expected to be completed in 2018.

LRT project development is done in two stages with a total length of 83.6 km each and comprises three cross- ministry , namely:

1. Phase I cross Cibubur services - Cawang - East Bekasi -Cawang, Cawang - Dukuh Atas with 18 stations and 42 inches long, 1 km;

2. Phase II cross Cibubur services - Bogor , Dukuh Atas -Palmerah - Senayan , and Palmerah - Grogol with a length of 41.5 km.

Jakarta

Source : Ministry of State Secretary (2015)

Investment Coordinating Board (BKPM)One Stop Service (OSS) Centre

• OSS combines the investment permission process of 21 ministries/institutions which delegate their authority to issue business permits and assign their officer to serve the licensing processes for investors

• In total, there are 134 licenses of 1.249 fields to be processed in OSS-BKPM, covering 5 business sectors (electricity, industry, industrial zones, tourism and agricultural sectors), but excluding the upstream oil and gas and financial sectors.

• Investors can also carry out the licensing application process and monitor the progress of applications by online (https://spmdashboard.bkpm.go.id/Tracking/tracking_en.zul)

• The establishment of OSS has cut the time of investment licensing process from about 930 days to less than 6 months

Source: BKPM, Cabinet Secretariat, Jakarta Post

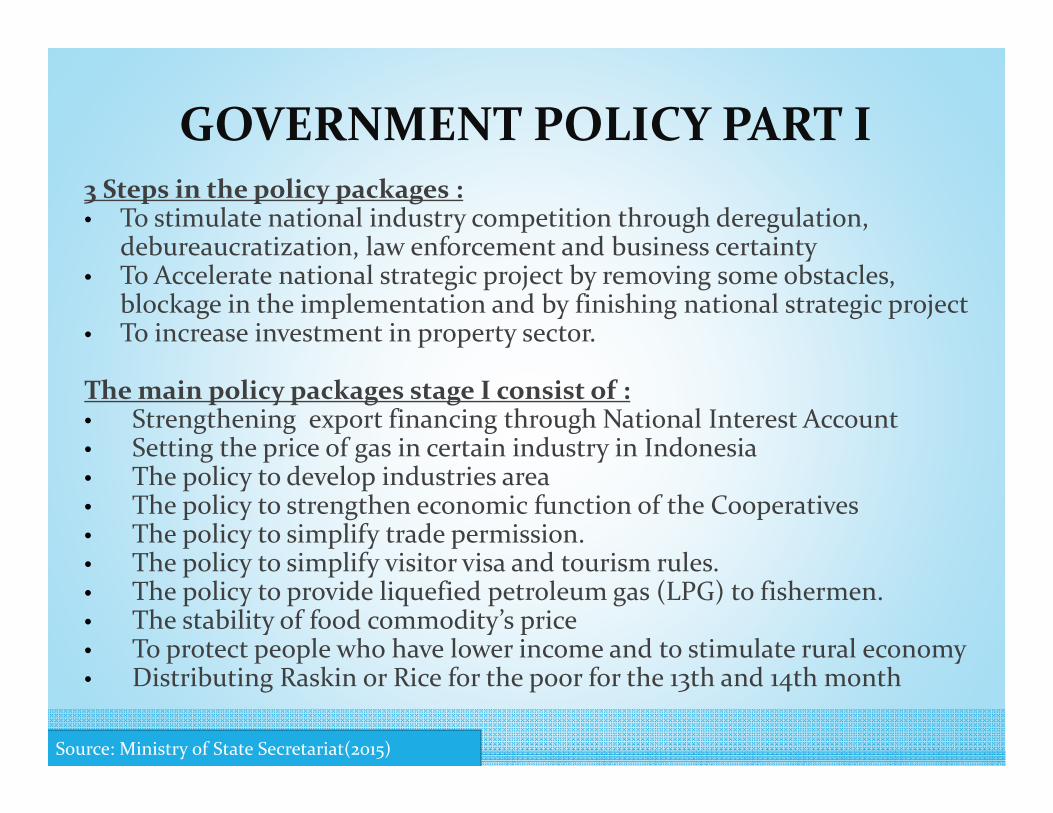

GOVERNMENT POLICY PACKAGES

GOVERNMENT POLICY PART I3 Steps in the policy packages :• To stimulate national industry competition through deregulation,

debureaucratization, law enforcement and business certainty• To Accelerate national strategic project by removing some obstacles,

blockage in the implementation and by finishing national strategic project• To increase investment in property sector.

The main policy packages stage I consist of :• Strengthening export financing through National Interest Account• Setting the price of gas in certain industry in Indonesia• The policy to develop industries area• The policy to strengthen economic function of the Cooperatives• The policy to simplify trade permission.• The policy to simplify visitor visa and tourism rules.• The policy to provide liquefied petroleum gas (LPG) to fishermen.• The stability of food commodity’s price• To protect people who have lower income and to stimulate rural economy• Distributing Raskin or Rice for the poor for the 13th and 14th month

Source: Ministry of State Secretariat(2015)

GOVERNMENT POLICY PART IIMinistry of Finance:• Maximum day of resolutin process of tax holiday = 45 days• Maximum day of tax allowance settlement = 25 days• Cut income tax on the interest that exporters earn when they deposit their export

proceeds in local banks10 percent income tax will apply to one-month US dollar-denominated

deposit accounts at local banks; 2.5 percent income tax for six-month deposits; and zero income tax for deposit accounts over six months.one-month rupiah-denominated deposit accounts, a 7.5 percent income tax will apply; 5 percent income tax for three-month deposits; and zero income tax for six-month (or longer) deposits.

Indonesia Investment Coordinating Board: Regulation of quick service for new investment • The time required to process investment permits (for industrial estates only) will be cut

from eight days to just three hours Requirement :• However, this fast service will only be available to those companies that invest at least

IDR 100 billion (approx. USD 7 million) and plan to employ at least 1,000 people.

Ministry of Environment and Forestry:• Shorten the permit issuance period to three to five days for forest area exploration and to

12 days for production• The issuance of a permit for forest area use must now be completed within 12 to 15 days

(previously between 2 to 4 years)• Trimming the total number of licenses for the forestry sector from 14 to 6

Source: Press Release of Ministry of Finance & Statement of Minister of Finance ; Press Release Coordinating Minister for the Economy; Statement of Minister of Environment and Forestry - 30 September 2015

GOVERNMENT POLICY PART III1. Lower price of fuel oils, electricity tariff, and gas• The price of diesel fuel is down by Rp200/liter retail price = Rp6,700/liter.• Premium fuel prices is unchanged• Electricity prices for customers category I3 and I4 (medium & large industries) will be decreased by IDR 12-IDR 13 per kWh• There will be a tariff discount up to 30% for electricity usage from 11:00 PMuntil 8:00 AM• Gas prices from new gas fields for factories in fertilizer industry will be set according to their purchasing power, which is equal to USD 7 MMBtu. • Gas prices for other industries (such as petrochemical, ceramics, etc.) will be reduced in line with capability of respective industries. 2. Expansion of the Business Credit for People (Kredit Usaha Rakyat or KUR)• Government has lowered the KUR rate from 22% to 12%.• Families with fixed income are able to receive KUR for productive businesssectors3. Simplification of Land Licenses for Investment Activities• Revised the Government Regulation No. 2/2015 on Standard of Service andRules of the Agrarian and Land Planning in the investment activities.• Information on the land availability can be obtained by applicants in 3 hours (from previously 7 hours)• All applications will be registered to provide certainty in regard to availability of land and land use planning. The letter will be issued in 3 hours.

Source: Coordinating Minister for the Economy (2015)

GOVERNMENT POLICY PART IV1. Minimun Wage• Introduction of a formula for the minimum wage annual increase toprovide certainty for workers and business• The formula not applicable to 8 provinces whose minimum wage is stillbelow the government determined basic cost of living, which will insteadbe grante an extra 5% every year for the next four years.2. Micro Loans• Expansion of sector and borrowers eligible for government micro loans(KUR)• KUR recipients include individuals or legal entiries, migrant workers• Sectors include productive businesses namely : agriculture, fisheries,manufacturing, services• KUR interest rate slashed to 12% from 22% previously3. Export financing• Widening the capability of the Indonesian Export Financing Agency(LPEI) to lend and subsidize the agency to provide cheaper loans forexport oriented companies to expand

Source: Coordinating Minister for the Economy (2015)

GOVERNMENT POLICY PART V

1.Asset RevaluationThose that apply for the asset revaluation before 31December 2015 will be eligible for a 3% tax rate, downfrom the current 10%The tax rate will be set at 4% for those that apply for therevaluation between 1 January 2016 and 30 June 2016And at 6% for periode of 1 July 2016 to 31 December 20162.Removed Double Taxation on Portfolio Investors who invest inReal Estate, Property and InfrastructureScrap double tax and developing products such CollectiveInvestment Contract (CIC), Real Estate Investment Trust(REIT), Collective Investment Contract on Asset BackedSecurities, etc3.Syariah Banking DeregulationLeniency regarding regulation and licensing for syariahbanking’s productsSource: Press Release Coordinating Minister for the Economy (2015)

GOVERNMENT POLICY PART VI1. Developing economy from remote areas by special economic region (KEK) development. Incentives given to develop including:a) Cutting income taxb) Value added tax and luxurious goods tax are not collectedc) Customs: foreigners or foreign entities can own residents in the regiond) Property ownership for foreigners: can be excluded from luxurious goods sale tax and value added tax on luxurious goodse) Tourism: can be included in tax cut for building tax I around 50%-100%f) Labor: creating a remuneration board and special tripartite cooperating body in the special economic regiong) Immigration: 1 year multiple visah) Land: special economic region proposed by private sectors is granted a building using permit and its extension is directly given at the same time the right is given.i) Permits: acceleration of issuance: maximum of 3hours2. Sustainable and fair provision of water 3. Paperless process in import permits for the raw material of medicinesSource: Press Release Coordinating Minister for the Economy (2015)

POLICY PACKAGES OF BANK INDONESIA AND FINANCIAL SERVICE AUTHORITY (OJK)

Bank Indonesia (Release: 9 September 2015 & 30 September 2015)

OJK (Release: 24 July 2015 & 8 October 2015)

Bank Indonesia’s Policies 9 September 2015

1. Strengthening inflation control and stimulating the real sector from the supply side.

2. Maintaining rupiah exchange rate 3. Strengthening rupiah liquidity management

• changing the auction mechanism for Reverse Repo (RR) SBN from a variable rate to a fixed rate tender

• reissuing 9 and 12-month Bank Indonesia Certificates (SBI) using a fixed rate tender auction mechanism and adjusting the pricing.

4. Strengthening foreign exchange supply and demand management.

• reducing the frequency of Foreign Exchange (FX) Swap auctions from twice to once per week.

• lowering the limit on foreign currency purchases backed by an underlying document from US$100 thousand to US$25 thousand per customer per month

5. Deepening the money market• providing swap hedging facilities• refining money market regulations

Source: Bank Indonesia (2015)

Bank Indonesia’s Policies 30 September 2015

1. Maintaining Rupiah Exchange Rate Stability• The presence of Bank Indonesia on the domestic foreign exchange market to

stabilize the rupiah exchange rate was strengthened through intervention on the forward market.

2. Strengthening Rupiah Liquidity Management • by releasing three-month Bank Indonesia Certificates of Deposit (SDBI) along

with two-week reverse repo tradable government securities (SBN). 3. Strengthening Foreign Exchange Supply and Demand

Management• foreign currency Bank Indonesia securities (SBBI) were also issued • the holding period of Bank Indonesia Certificates (SBI) was reduced from one

month to one week on order to attract foreign capital inflows. • incentive was provided in the form of a reduction in the interest tax paid on

term deposits for exporters depositing their foreign exchange earnings at banks in Indonesia or converting the proceeds into rupiah as requested by the government.

• strengthening the foreign exchange flow report

Source: Bank Indonesia (2015)

OJK’s Policies: Banking • Debts or loans guaranteed by the central government are to be charged at a zero-

percent risk weight when calculated as risk weighed assets (ATMR) for loan risks• The risk weight of motor-vehicle loans (KKB) is to be set at 75% in ATMR loan-

risk calculations• The implementation of business-prospect assessments• Loan restructuring must be conducted prior to a loan-quality reduction• The reduction of risk weight for house-backed loans not under a government

program is set at 35% without consideration of Loan to Value (LTV) in ATMRloan-risks calculations

• The reduction of risk weight for health-and-welfare (RSS) house mortgages underthe governmental program is set at 20%, without any consideration of Loan toValue (LTV) in ATMR loan-risks calculations

• The reduction of risk weight for the People’s Business Credit Program (KUR) isguaranteed by a Regional Credit Guarantee (Penjaminan Kredit Daerah -Jamkrida)

• Loan-quality assessment of a single debtor or project based on prompt paymentof a principal loan and/or interest has been raised from IDR 1 billion (max) to IDR5 billion

• Loan quality assessment of micro-small-medium enterprises loans (UMKM) with over IDR 5 billion value relating to risk management implementation quality (KPMR) assessment rank and bank health level composite rank are to be undertaken

Source: OJK (2015)

Some of OJK’s Policies: Capital Market • The development of infrastructure for the repurchase agreement market(Repo)• Development of small and medium enterprises with the aim of going public• Determination of an electronic trading platform (ETP)• Utilization of the central bank for transaction settlements• Plans to issue Indonesia Government Bond Futures (IGBF) derivative products• The issuance of a derivative product based on Indonesian Government BondFutures (IGBF) pertaining to the development of the government securities(SBN)• Utilization of the debt securities bond index• Issuance of an asset backed securities-participation letter (EBA-SP) in order toincrease the growth of house financing in Indonesia• The regulation of segmented licensing for securities intermediaryrepresentatives (WPPE) into three levels: WPPE, WPPE specializing inmarketing, and WPPE specializing in marketing agents;• Regulations on integrated investment management system• Encouraging state-owned enterprises and subsidiaries to go public• Provide regulatory leniency and legal certainty for sharia securitiesSource: OJK (2015)

OJK’s Policies: Non Bank Financial Institution • Leniency regarding non-performing financing (NPF) policy as

applied to finance companies in order to boost the growth of finance debt by finance companies;

• Development of agricultural insurance in order to improve farmers’ access to the finance system and develop the national agrarian sector;

• The establishment of a ratings agency for UMKM in order to minimize the asymmetric information issues pertaining to UMKM financing and to prepare for the ASEAN Economic Community (AEC) era;

• The development of micro-financing institutions (MFI) that will focus their efforts on inviting MFIs that are not formally registered to apply immediately to become legitimate MFIs in accordance with the MFI law.

Source: OJK (2015)

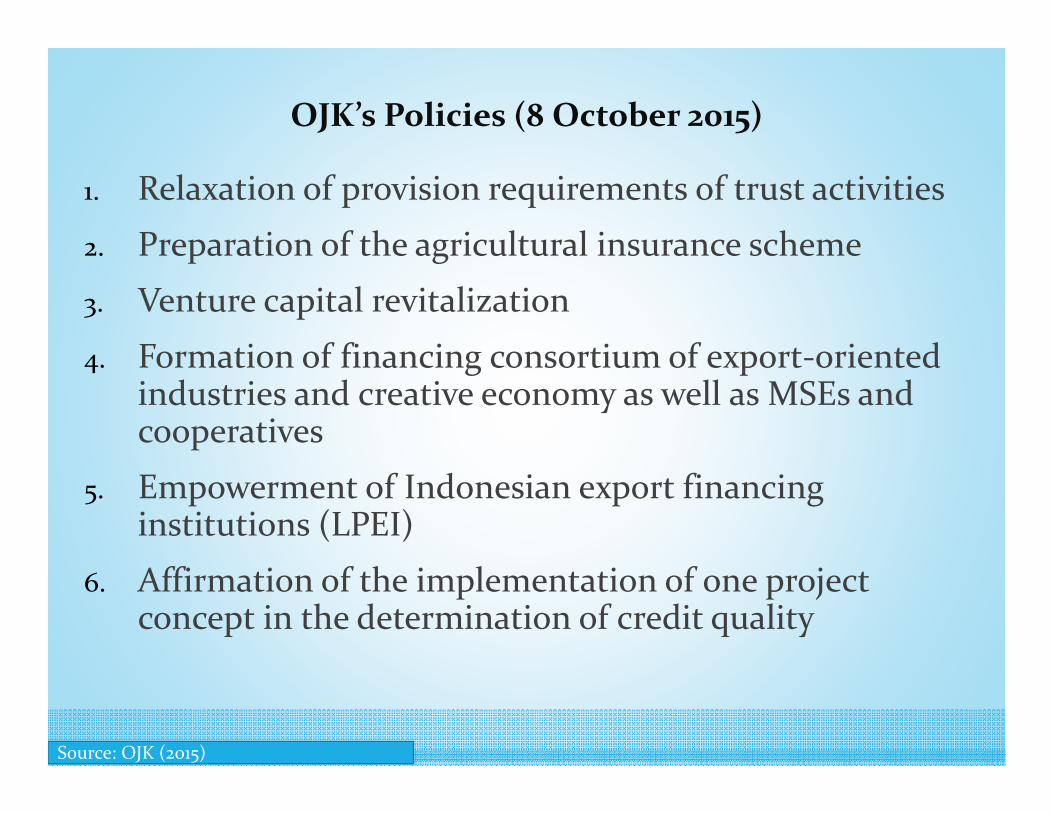

OJK’s Policies (8 October 2015)

1. Relaxation of provision requirements of trust activities

2. Preparation of the agricultural insurance scheme

3. Venture capital revitalization

4. Formation of financing consortium of export-orientedindustries and creative economy as well as MSEs and cooperatives

5. Empowerment of Indonesian export financing institutions (LPEI)

6. Affirmation of the implementation of one project concept in the determination of credit quality

Source: OJK (2015)

CONCLUSIONCONCLUSION• Indonesia is undergoing a transformation in

improving its global competitiveness.

• Government’s policy packages is leading to a better business and investment climate.

• Indonesia’s domestic market still has an ample potencies.

• Indonesia economic development’s quality will be better, stable, more competitive, and more equal.

THANK YOUTHANK YOU