enhanced infrastructure financing districts - slo evc - a mechanism for eco-rapid transit... ·...

TRANSCRIPT

Enhanced Infrastructure Financing Districts A Mechanism to Finance Eco-Rapid Transit

University of Southern California, Sol Price School of Public Policy

Master of Planning Course: Planning Studio

December 2014

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

II | P a g e

ACKNOWLEDGEMENT The team is proud to present this report Enhanced Infrastructure Financing District: A Mechanism to Finance Eco-

Rapid Transit for our University of Southern California (USC) graduate planning studio project. This report is

based on the planning and analysis work of our core team comprising of:

• Rebecca Chung

• Qianyao Duan

• Adam Montgomery

• Kristine Rose

• Rui Tu

• Sasha Ussef

• Siyuan Yin

The study works were completed under the guidance and supervision of Mark Pisano, a professor of the

Practice of Public Administration at the USC Sol Price School of Public Policy. Serving as the executive director of

the Southern California Association of Governments (SGAG) for the past 31 years, his experience and

knowledge contributed greatly to the success of this project.

The team would also like to thank the contribution of those who ably prepared the necessary background

material and data required for the analysis of this report as well as providing our team with constructive

feedback regarding our work. These individuals are hereby gratefully acknowledged:

• Walter Beaumont

• Greg Devereaux

• Norman Emerson

• Gail Goldberg

• Michael Kodama

• Allyn Rifkin

• Fred Silva

• Lillian Burkenheim Silver

• Ping Wang

• Eco-Rapid Transit Staff

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

III | P a g e

Table of Contents

1 OVERVIEW: ECO-RAPID TODAY AND VISION FOR TOMORROW ................................................................... 1 1.1 The Corridor Today ....................................................................................................................................... 1 1.2 Eco-Rapid’s Vision ......................................................................................................................................... 2 1.3 Implementation of a Public Dialogue ......................................................................................................... 2

2 BACKGROUND: STATE OF ECO-RAPID TRANSIT ............................................................................................. 3 3 BRINGING THE VISION: LITERATURE REVIEW OF LONDON CASE STUDY ................................................... 4 4 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS (EIFD) ...................................................................... 6

4.1 Overview ........................................................................................................................................................ 7 4.2 Funding Strategies ........................................................................................................................................ 7 4.3 Facilities Financed by an EIFD ...................................................................................................................... 8 4.4 Differences between RDA, IFD, and EIFD ................................................................................................... 8 4.5 Benefits and Barriers of EIFD .................................................................................................................... 11 4.6 Multiple Funding Streams Available to use in EIFDs ............................................................................... 12

5 PROPOSED EIFD IMPLEMENTATION FOR ECO-RAPID ................................................................................. 13 5.1 Specific Steps for Eco-Rapid to Create and use EIFDs ............................................................................ 14

6 CASE STUDY: DOWNEY STATION ................................................................................................................... 15 6.1 Station Overview ......................................................................................................................................... 16 6.2 Opportunities for Value Capture ............................................................................................................... 19 6.3 Financial Strategy & Modeling Results ..................................................................................................... 21

6.3.1 Tax Increment Financing and Developer Fees ............................................................................... 21 6.3.2 Motor Vehicle-in-Lieu Fees (VLF) ...................................................................................................... 25 6.3.3 Parking Management Fees ............................................................................................................... 26

6.4 Summary of Value Capture ........................................................................................................................ 29 7 TOOLS FOR SUCCESSFUL ANALYSIS .............................................................................................................. 30 8 CONCLUSION ................................................................................................................................................... 31 REFERENCES ................................................................................................................................................................ 32 Appendix A: Key Terms and Explainer Overview

Appendix B: Visual Structure of EIFD JPA

Appendix C: Assumptions for Tax Increment Financing

Appendix D: Assumptions for VLF Backfill

Appendix E: Assumptions for Parking Management In-Lieu Fee

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

1 | P a g e

By embodying the vision of the public, the planning process reframes cities and has the ability to use many

mechanisms to create infrastructure, opportunities, and spaces for the people. Financial tools primarily

drive these changes and developments that ultimately create wealth for a region. Through a regional

collaborative and systematic effort, cities can create and capture more of this wealth. To erect this vision of

city advancement requires the engagement of all stakeholders to strategically invest and regenerate a

fiscally stressed city through competitive, attractive economic development.

1 OVERVIEW: ECO-RAPID TODAY AND VISION FOR TOMORROW Eco-Rapid Transit’s rail initiative will transform the Los Angeles and Orange County region if the

organization continues to collaborate. To expedite implementation of the rail corridor by providing access

to multiple funding streams, Eco-Rapid can use an Enhanced Infrastructure Financing District (EIFD), signed

into legislation under the purview of Senate Bill 628, to capture the inherent wealth created increased

socio-economic opportunities of the corridor. EIFD will not be a platform for negotiation, deliberation, or

even consensus, but rather a mode that promotes the process of thinking together in order to build

various forms of necessary infrastructure while using financial tools efficiently to address the pressing

needs of a place and a people. A common

understanding will provide the basis for a clear

analysis and deeper exploration of the varied

narratives and perspectives of multiple

constituents.

1.1 The Corridor Today The project’s focus area, a 34-mile corridor that

extends north and south of downtown Los Angeles,

has an elaborate history that has shaped the places’

current state of organization and infrastructure.

The needs of these cities vary, but the Eco-Rapid

project can positively influence each place if the

process remains flexible and open to the current

conditions of these places.

Figure 1: Project Location

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

2 | P a g e

The scope of the project requires the participation of many cities. The magnitude and significance of the

project will attract further engagement if the dialogue revolves around the specific public needs of each

jurisdiction. Therefore, understanding the initial point of public dialogue will occur through defining the

scale and underlying needs and urgencies for the project. Currently, the existing JPA (Joint Powers

Authority) has acquired some funding and produced studies and plans about the corridor. The jurisdictions

participating in the JPA have specific demands addressed in the plans, however, under the uniformly

prescribe to an overarching mission of increased opportunities.

By focusing on the rail project through an economic development plan that integrates mixed-use

infrastructure, the public can reconsider the potential socio-economic opportunities for the area. Through

the 3-D process - decentralized, diversified, and distributed- communities can create a platform to seek

further opportunities to thrive and develop long term (Pisano, 2013). Due to the current fiscal stress of the

state, financing projects has become more difficult because of the dependence on stressed public funds

and individual income levels (Pisano, 2013). Creating partnerships across sectors in order to improve

resource management and implement an outward procurement process will promote the decentralization

of networks and information and encourage user based systems (Pisano, 2013). The Eco-Rapid Transit rail

projects can inspire increased transparency amongst stakeholders, a platform for social and economic user

benefits, an occasion to preserve and progress the identity of residents in the jurisdictions, and will provide

fiscal, environmental, and innovation transformations for the community.

1.2 Eco-Rapid’s Vision In hopes of creating better communities adjacent to the project, the rail line will not only improve

accessibility and mobility, but will enhance the quality of quotidian life in these cities. The goals and

objectives of the project include economic stimulus, environmental justice, and creating public spaces

through the greening of the area. Each of these objectives will create wealth in the region that can and

should be captured. Enhanced Infrastructure Financing Districts serves as a mechanism to capture this

wealth by transforming land use and engineering plans into business plans.

1.3 Implementation of a Public Dialogue Prior to attempting to fulfill the need of a place, an extensive consideration of the current infrastructure is

necessary. How do we support a community plan for each of the participating members while keeping the

overarching ideas of the Eco-Rapid project in mind? How can we create a business plan that includes and

provides for the interests of all constituents? Transparency is key in order to understand the connections

between development and infrastructure.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

3 | P a g e

When reconsidering the built environment of a place, it is important to be cautious about meeting specific

demands of the public while understanding the changes that will occur in the long run. A flexible structure

that allows for site-specific growth defined through the applied financial tools will support strategic growth

of a city. This is further supported by a collaborative, corridor approach. The implementation of an EIFD

will catalyze significant public dialogue that will support not only the growth of infrastructure, but most

importantly the dialogue of the people and place. Interaction with stakeholders should be similar to the

process described in the London case below.

2 BACKGROUND: STATE OF ECO-RAPID TRANSIT Composed of 13 members and several supporting agencies, Eco-Rapid Transit, formerly known as the

Orangeline Development Authority (OLDA) is a joint powers authority (JPA) established for the purpose of

pursuing the development of a transit system. The system plans to be environmentally friendly and energy

efficient, while also providing improved transportation options to expand economic growth in the region.

The 13 members of the agency have proposed stations that will be located along a former Pacific Electric

Right-of-Way south of downtown Los Angeles (the West Santa Ana Branch) and a remaining rail corridor

north of downtown Los Angeles (the Antelope Valley Line). The current project scope proposes the

northernmost station be located at the Bob Hope Airport in the City of Burbank and the southernmost

station be located in the city of Artesia.

Formed in 2003, the Orangeline Development Authority was established to support mobility across the

Southern California region, with the specific objective of developing additional travel options in the

corridor. During its initial years, the agency strongly advocated for a transit line using Maglev technology to

connect the two counties; however, as alternatives have been analyzed, the agency has switched its focus

to a rail transit line. Over the course of its 11-year existence, city membership in the agency has fluctuated

resulting in changes in the scale of the project. As the years have progressed, the agency has generally

experienced a decreasing scale in the magnitude of the project. At its most extensive, the transit project’s

concept stretched from Palmdale in northern Los Angeles County to Santa Ana in Orange County. In the

last year alone, the agency has lost several city members including Palmdale, Cerritos, and Santa Ana.

Departures have placed constraints on the budget as membership dues have decreased to reflect the

fewer track miles of the future transit line. The project scope has contracted as city membership has

decreased, with the scope now extending from Bob Hope Airport to Artesia and focused on the following

13 members:

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

4 | P a g e

Table 1: Members of Eco-Rapid Transit

* City of Artesia * City of Huntington Park * City of Bell * City of Maywood * City of Bellflower * City of Paramount * City of Bell Gardens * City of South Gate * City of Cudahy * City of Vernon * City of Downey * Burbank/Glendale/Pasadena Airport Authority * City of Glendale

Total development costs for the Southern portion of the transit line extending from Downtown Los Angeles

to Artesia are estimated to be up to $3 billion (Ikhrata, 2013). Currently, the agency has secured $240

million in funding, which will be available in 2015, from the Los Angeles County voter approved Measure R

program. Further funding has been received for station, land use, and alternatives studies and analysis. In

2005, the agency was allocated $280,000 in Safe, Accountable, Flexible, Efficient Transportation Equity Act:

A Legacy for Users (SAFETEA-LU) federal funding to conduct preliminary station and land use analysis. In

2012, the Los Angeles County Metropolitan Transportation Authority (MTA), the Southern California

Association of Governments (SCAG), and the Orange County Transportation Act (OCTA) conducted a $1.8

million alternatives analysis, specifically for the Pacific Electric Right-of-Way stretching from Paramount to

Santa Ana (Ikhrata, 2013).

3 BRINGING THE VISION: LITERATURE REVIEW OF LONDON CASE STUDY The fundamental role of government is creating the formal and informal incentives for all the organizations

in society to operate in a way, through systematic innovation, that achieves desired goals (Pisano, n.d.).

The vision to implement infrastructure at the scale presented by Eco-Rapid Transit, begins at the

framework of the 3-D approach: decentralized, diversified, and distributed (Pisano, n.d.). Ken Livingstone,

the first Mayor of the Greater London Authority, initiated the regeneration of the city during a moment of

fiscal stress by focusing on two features of the city: transportation and land use planning. The former

mayor used his authority to exercise effective socio-economic change through focusing solely on land use

and transportation issues. Livingstone creatively took advantage of a systematic approach to collaborative

thinking in order to allow the public to have oversight over the process of developing the built

environment. He did not issue concessions, and instead reconfigured the system through evaluating

performance and providing opportunities for public oversight.

London’s rail network includes a high speed international rail, central underground tube system, and an

extensive bus system. The tube and bus systems have been governed by the national government and

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

5 | P a g e

depended on the private sector for development (Pisano, n.d.). Along with these systems the radial city was

experiencing increased congestion from the highway and road network (Pisano, n.d.). Livingstone

appointed Bob Kiley as the transportation commissioner of the Transportation for London (TFL), and

together worked to shift the framework. Conventionally, the P3 approach allowed for the public sector to

contract with the private. This procurement instrument privatized operation and left the fiscal

responsibility and risk with the public sector (Pisano, n.d.).

Both opposed this system, Livingstone and Kiley gained public support by making the consumer appreciate

the value of transit and emphasize the consumer’s role as primary decision maker (Pisano, n.d.). The

development strategy shifted the procurement process and enabled the ties to be formed between the TFL

and other entities in order to create more funding streams to support the transit improvements in the

system and the adjacent areas. He pushed cars out of the central portion of the city by implementing a

congestion pricing fee. This not only decreased CO2 emissions, but also reduced the amount of vehicles

coming into the city and encouraged public transit (Pisano, n.d.). The tube was refurbished and upgraded,

to support sustainable systems, increased ridership, and improved information systems. The introduction

of the information chip, the Oyster Card, improved the collection of revenues and operational facilities

(Pisano, n.d.). These changes affected the travel behavior of individuals in the city, and were able to

complement these social changes with economic decisions. He also increased the pricing of the

underground system, assuming that the better designed, more flexible and accessible system increased

customer satisfaction and the demand for service (Pisano, n.d.).

Further, the public sector and the private sector used their capacity as partners to work on a transparent

level and within a specific legal framework in order to fund the acquisition of land, the development of

infrastructure, and the production of long-term investment strategies (Pisano, n.d.). The highly organized

TFL examined and understood the linkages of the national and international rails lines to the underground

system. With this, two upgrades to the system were introduced - the Crossrail and the London Overground.

These lines created more connectivity, increased the rail capacity, reduced travel time, increased ridership,

and affected the adjacent land uses especially in high-growth areas. Due to these changes the income

stream also increased (Pisano, n.d.). The $21 billion Crossrail project, which included 42 stations over 25

miles, was the largest capital structure project made in western countries. The funding strategy pulled from

three different sources - national funds, a beneficial use stream, and the increased productivity of

investments affected by the farebox recovery. Businesses were encouraged to support the underground

and overground systems. This allowed the for local authorities to implement community impact levies

(CILs) over the 50-year time period of the program, which are fees that are placed on business properties

that are put towards the cost of funding infrastructure (Pisano, n.d.).

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

6 | P a g e

The success factors in the case of London can be applied to elements of the US system. It is important to

keep in mind the following key elements of integrated problem solving and funding strategies (Pisano, n.d.):

Policy and staff leadership must transcend political cycles and parties long-term. They must

identify the scale of the project, the correct spatial linkages, and a structure to capture benefits.

Any strategic plan that includes a series of programming, projects, or investments tended toward a

specific outcome must have quantified benefits that can be used as a mechanism to motivate

users, consumers, and voters to pay the necessary fees.

Collaboration on levels - public, private, and community - in order to identify which tradeoffs will

lead to a desirable outcome is necessary.

Create accountability for the service through a marketing approach led by an executive that

brands the service with a great level of transparency and communication in order to build trust

with the existing and potential consumers and users.

Mega-regional decision making framework that provides a nexus between decisions and actions

through the lens of finance. During fiscal stress, this will create more beneficial use funding

strategies to accompany the conventional tools. Create a team of staff that works together and

understands the significance of enterprise funding that accompanies the development of the

system.

Overall, these strategies changed the demographic composition, therefore, increasing the economic

competitiveness of London. With a clear organization structure and a focus on financing specific

infrastructure projects, it is possible to create beneficial change in your city.

4 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS (EIFD) Similar to London, Eco-Rapid Transit has taken a revolutionary approach to transit finance by taking a

transportation project and transforming it into one focused on economic development. Eco-Rapid member

cities have realized that collaboration is the key. In order to capture the most wealth for the region, this

cannot just be a project that uses Right-of-Way (ROW) and bids for the most attractive Transit Oriented

Development, but must in fact be a system wide regeneration effort. As Eco-Rapid Transit already foresees

the rail projects as economic and environmental justice projects, the project was inherently designed to

create wealth around newly developed transit stations, providing access to employment centers, and

improving the quality of life through new, affordable housing. With access to Enhanced Infrastructure

Financing Districts (EIFDs), Eco-Rapid is poised to develop a business plan that captures the wealth created

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

7 | P a g e

by the transit line to fund environmentally efficient rail that creates competitive, attractive economic

development and improved quality of life for area residents.

4.1 Overview Introduced first in February of 2013 by Senators Beall and Wolk, EIFD Senate Bill No. 628 was signed into

law by Governor Jerry Brown on September 26, 2014 as a mechanism to fund construction and

rehabilitation of public infrastructure projects in California. EIFDs are independent government entities that

“drive sustainable growth by connecting a vast number of infrastructure projects with a new array of

funding streams” and by placing financing decisions at the front of the planning stage, rather than after

(California Economic Summit, 2014). While dramatically and influentially different, EIFDs will likely have the

impacts on local agency planning and development similar to the Redevelopment Agencies of past. A brief

set of key terms and an explainer document can be found in Appendix A.

4.2 Funding Strategies EIFD’s may fund infrastructure using the following mechanisms (Enhanced Infrastructure Financing

Districts, 2014):

1. Property tax increment of consenting taxing agencies (cities, counties, special districts but not

schools).

2. Revenues from property tax corresponding to the increase in assessed valuation of taxable

property attributed to those property shares received by a city or county pursuant to in lieu of VLF

and dedicated to a city or county to the EIFD.

3. Property tax revenue distributed to a city, county or special district after payment of a successor

agency debts.

4. Fees or assessment revenues derived from one of 10 specified existing sources, including

assessments for benefits and developer fees.

5. Loans from a city, county or special district, that must be repaid at no more than the Local Agency

Investment Fund (LAIF) interest rate that is in effect on the date the loan is approved by the

governing board of the city, county or special district making the loan.

6. User Fees and Partnerships derived from the use of the Infrastructure Finance and Investment

Act, which the EIFD can use as it is established as an separate government entity.

7. Availability Payments, annual payments to a third party, which sit as line item entries city or

county budgets and are amortized over a specified period.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

8 | P a g e

4.3 Facilities Financed by an EIFD A multitude of public and private infrastructure and facilities can be financed by EIFDs, including

infrastructure construction and rehabilitation. Jurisdictions may create an EIFD to finance the following

types of facilities, but they are not limited to only these infrastructure projects (League of California Cities,

n.d.):

Highways, interchanges, ramps and bridges, arterial streets, parking and transit facilities.

Parks, recreational facilities, open space and libraries.

Brownfield restoration and other environmental mitigation. A district may use any powers of the

Polanco Redevelopment Act to remediate property.

Acquisition, construction and repair of industrial structures for private use.

Transit priority projects as defined under Section 21155 of the Public Resources Code.

Projects which implement a sustainable community’s strategy.

Mixed-income housing developments (An EIFD may fund only those units dedicated to low or

moderate income housing, and child care, after-school care and social services integrally linked to

the tenant of the restricted.

Reimbursement of a developer located within the boundaries of a district for permit and other

expenses incurred when constructing affordable housing pursuant to the Transit Priority Project

Program under Section 65470 of the Government Code.

Facilities constructed to house providers of consumer goods and services.

Authority to make investments to renovate and develop industrial properties.

4.4 Differences between RDA, IFD, and EIFD While sharing many similar components, Enhanced Infrastructure Financing Districts differ significantly

from related Redevelopment Agencies and traditional Infrastructure Financing Districts.

Redevelopment Agencies: The dissolution of Redevelopment Agencies (RDAs) at the end of 2011 ended the

ability of local governments to capture a share of property taxes to combat blight. In existence for 60 years,

cities and counties in California had formed over 400 redevelopment agencies to areas determined as

blighted. RDAs were accountable to the public as they were overseen by a local city council, county board

of supervisors, or a distinct appointed board. The formation of a RDA did not require an election; instead,

any governing body within a county or city could initiate the formation (Blount, 2014).

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

9 | P a g e

Through public investment and the use of eminent domain, RDAs would stimulate private sector

investment on a variety of projects. Common project types include (California redevelopment agencies, the

sequel, 2013):

Public and private capital improvements

Public works projects

Housing

The agencies were funded by the use of tax increment financing, which allowed for the entities to receive a

share of the increased property values generated by new investment and development. RDAs pledged the

tax increment to repay bonds and other debt initially used to finance the development. No voter approval

was required to issue bonds and 20 percent of the tax increment revenues were deposited into a “Low-and

Moderate-Income Housing Fund,” used to increase, improve, and preserve affordable housing in the

community (Greenhut, 2011).

Infrastructure Financing Districts: With RDAs dissolved, communities were forced to explore other financing

mechanism to stimulate economic development. One such mechanism is an Infrastructure Financing

District (IFD), which can help fund regional scale public works. The IFD, created by the 1990 California

statute, “The Infrastructure Financing District Act”, allows cities and counties to use a portion of the

property tax increment to finance defined public improvements for a period up to 30 years. The property

tax increment includes all collected property tax within the district, except for taxes allocated to school

districts, community college districts, county boards of education, and other taxing entities that did not

consent to the IFD formation (Reynolds & Thimmig, 2011). The tax increment is typically used for the

payment of IFD Revenue Bonds.

Unlike a RDA, an IFD must receive two-thirds voter approval by qualified electors in the district for both

bond issuance and for the initial formation. Further, the formation of an IFD also requires that an

infrastructure plan is developed, sent to every landowner within the district, and a public hearing be held.

The plan must be approved by all taxing entity within the district that will be contributing its property tax

increment.

Provisions within the Act detail the types of projects that IFDs can pursue. An IFD can finance the purchase,

construction, expansion, rehabilitation, and retrofit of public capital facilities, such as highways, water

systems, flood control, parks, solid waste facilities, ramps and bridges, transit, sewer projects, child care

facilities, libraries, parking facilities, and residential units (Infrastructure Financing Districts, n.d.).

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

10 | P a g e

Other provisions state that the IFD is unable to pay for maintenance, repairs, services, and operating costs

related to the project and the useful life of projects must be at least 15 years. While the projects do not

have to in areas determined as blighted, the must provide benefits to an area larger than the district.

Additionally, the district must not overlap an existing RDA.

Enhanced Infrastructure Financing Districts: The newest tool, an Enhanced Infrastructure Financing District

(EIFD), looks to fill the void left by RDAs by loosening the provisions of an IFD. An EIFD can be formed by a

city, county, or special district through the development of an infrastructure financing plan, instead of a

two-third voter approval. The district may also be governed by multiple taxing entities, including

municipalities, counties, and special districts, but the entities must consent to the allocation of their portion

of property tax increment to the district. Moreover, bonds supported by tax increment financing can be

issued with 55 percent of the electorate, not the two-thirds required by the IFD. The bond period has also

been extended to 45 years from the date of bond approval.

Further advancements include a broader range of projects that could be served by an EIFD. The EIFD can

also serve projects such as transit priority projects, low- and moderate-income housing, projects under

sustainable communities strategies, and environmental remediation. EIFDs also allow for tax increment

financing to be combined with other revenue streams, such as assessment and fee revenues, parking

districts, availability payments, and private investment.

To summarize, the EIFD allows for greater flexibility by offering a wider array of funding sources and

investment projects than the IFD. Furthermore, the 55 percent voter approval provides the district with a

more streamlined procedure for investment.

Table 2: Comparison of RDA, IFD and EIFD

RDA IFD EIFD

Forming Process No election required ⅔ Voter Approval No election required

Project Types Blighted Areas Public Capital Facilities Public Capital Facilities (+)

Community Significance

Financing Tools/Resources

Tax Increment Financing Tax Increment Financing Multiple Funding Streams: Tax Increment Financing, Development Impact fee, Special Assessment District, Developer Agreement, User Fees

Issues Bonds No voter approval required

⅔ Voter Approval 55% voter approval

Longevity ~ 40 years 30 years 45 years

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

11 | P a g e

4.5 Benefits and Barriers of EIFD Benefits: The EIFD provides cities and counties with several major benefits, including:

1. Greater financing authority: More revenue streams can be dedicated to funding a project under

an EIFD structure. Operating as a separate governmental entity, the district has the authority to

earn a portion of revenue from property tax increment, user, benefit fees and assessments,

among other revenue sources.

2. More infrastructure investments: EIFDs may fund other projects beyond “public capital

facilities”, including projects of “community wide significance”. Examples of such projects include

brownfield restoration, transit priority projects, projects relating to a sustainable communities

strategy, and the acquisition, construction, or rehabilitation of industrial facilities and low- and

moderate-income housing.

3. Longevity: From the date bonds have been issued or loans approved, the EIFD has 45 years to

receive funding support for their projects. This is 15 years longer than the 30 years allotted for

IFDs.

4. Increased collaboration among agencies: Different taxing entities that provide tax increment to

the EIFD and members of the public may / are required to sit on the district’s governing board.

Barriers: Despite its increased flexibility and streamlined approach, SB 628 does place some limits on the

formation and authority of EIFDs. Those limits include:

1. RDA Dissolution: If a local government previously created a RDA, the agency must have fully

completed the process of concluding its actions before the local government may proceed with

EIFD formation.

2. Tax-Increment Consent and Limits: A taxing entity within the district must approve and opt into

contributing its tax increment to an EIFD. Schools and other non-consenting tax entities cannot

divert their increment to the district.

3. Voter approval still required: An EIFD does not require voter approval in order to be formed;

local governments can form an EIFD without holding an election. However, issuing tax-increment

bonds does require a 55 percent vote, decreased from two-thirds vote required by an IFD.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

12 | P a g e

4.6 Multiple Funding Streams Available to use in EIFDs A leading benefit of the EIFD is multiple funding streams can be used in the same district. The following is

an overview of some types of funding streams but it does not represent the only options available:

1. Tax Increment Financing: Public taxing entities use the tax increment financing to capture

incremental property tax revenues from designated areas as compared to the base year. Prior to

dissolution in 2012, tax increments used to be a common financing tool for Community

Redevelopment Agencies in California. Now, SB 628 entitles cities to use tax increment financing to

finance infrastructure by creating EIFDs. Under the new law, only 55% vote is needed to issue debt

backed by AB8 Tax Increment as compared to previous legislations requiring a threshold of two

thirds vote. The tax revenue is divided into different pools, which go to cities, counties, school

districts and other taxing entities. Under SB 628, cities are able to divert property tax revenues

from school or community college districts. In the case of Eco-Rapid Transit line, cities in the OLDA

can capture the wealth by AB8 Tax Increment and VLF Backfill to finance the capital improvement.

2. Development Impact Fee: Under the Mitigation Fee Act, cities are allowed to charge developers

one-time development impact fees to mitigate the negative impacts associated with new

developments. The development impact fee should be charged based on reasonable findings of a

relation between new development and paying the fees. As it does not require voter approval, it

has been widely used to financing transportation and other infrastructure. The fees cannot be

used to fund existing deficiencies and cities must fund other sources to cover the cost of existing

uses. However, new infrastructure financed by the development impacts fee as a result of new

development, can benefit existing communities and future infrastructure users as well. In the case

of Eco-Rapid Transit Line, it will benefit the current communities by improving mobility and

enticing economic development opportunities.

3. Special Assessment District: Under a special assessment district, property owners agree to pay

additional assessment annually to fund special improvements within that district. The special

assessment should be directly proportional to the benefits the property owners will get prior to

payment. A simple majority is required to create a special assessments district. California Law

allows cities to create different type of special assessment districts to finance different types of

infrastructures. In the case of Eco-Rapid Transit line, special assessments can be charged, due to

improving mobility and economic development, as a result of the transit line.

4. Development Agreement: California law authorizes cities to negotiate with developer in order to

get desired development and new infrastructure in exchange of development rights. The public

improvement is based on project size, parking ratios and construction cost and other factors,

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

13 | P a g e

affecting anticipated cost and revenues. No voter approval is required. In the case of Eco-Rapid

Transit Corridor, new developers are attracted and the development agreement can be made by

negotiation to put new infrastructure.

5. Parking Management (or Other User Fees): A parking management district, which combines

several tools, can be created to finance the infrastructure and ensure efficient utilization of the

infrastructure. No vote approval is needed. In the case of Eco-Rapid Corridor, parking fees can be

charged for retail and residential uses and incentives can be provided to park-and-ride users to

utilize the transit line.

5 PROPOSED EIFD IMPLEMENTATION FOR ECO-RAPID Establishing the structure for the Eco-Rapid EIFD is critical to financing success yet there are several

ways to use an EIFD. In the instance of Eco-Rapid, member cities should take full advantage of the already

established Joint Powers Authority (JPA) and use a three phased set up approach (see Appendix B). This

structure will allow each jurisdiction to manage their own land-use plans while working in concert with the

line to streamline planning and administration. As Eco-Rapid staff recognize, the line will be most

successful if the stations are planned through a collaborative effort. Therefore, it is recommended that the

existing Eco-Rapid JPA enter into a cooperative agreement with each member city to participate in an EIFD

as the primary mechanism of funding for the line. Once cities have finalized their land use plans and

established an EIFD, the JPA can then serve as the management and administration for the cities’ EIFDs

through capacities established under California’s Joint Powers Authority statute.

Phase 1 - Mobilize JPA: Use current JPA to research, discuss, and propose EIFDs as the mechanism to fund

Eco-Rapid Transit.

Phase 2 - Individual Jurisdictions Create EIFD: It is imperative jurisdictions develop and adopt a strong

General Plan or Specific Plan around the planned stations that support the business plan appropriate for

an EIFD. The need to fund plan development is being communicated to State’s Strategic Growth Council

discussions on Cap and Trade monies, (Bridegam, 2014). For stations that touch multiple jurisdictions, city

staff should coordinate Planning efforts. In order to capture future value of development, the land will be

entitled through a planning process streamlined through collaboration with the JPA.

After this is complete, each city will create an EIFD in the surrounding station area within their jurisdiction.

To establish an EIFD, no vote is required. In order to pursue financing activity, the establishing city council

of the EIFD will need to ensure the EIFD also serves as a Public Financing Authority (PFA) with a governing

board. The board will include three members of the legislative body of participating entity (the City) plus

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

14 | P a g e

two members appointed from the public. With the powers provided to EIFD acting as a PFA, the EIFD will

create a financing strategy based on the cities’ General and Specific Plans and manage any voting for bond

issuance.

Phase 3 - JPA Manages and Administers EIFDs: After all JPA members establish individual EIFDs, the JPA can

amend their agreement to be responsible for Eco-Rapid member’s EIFD’s financing management and

administration. Through this mechanism, multiple EIFDs may collaborate on strategy, share the burden of

administrative costs, and share revenues to cover these administrative costs - all while maintaining the

jurisdictional land use decisions (California State Legislature Senate Local Government Committee, 2007,

pg. 27). The JPA should continue to consulate parties such as the Metropolitan Transit Authority (MTA), Los

Angeles County, Southern California Association of Government (SCAG), and Gateway Cities Council of

Governments - all with vested interested in the successful execution of the EIFD.

5.1 Specific Steps for Eco-Rapid to Create and use EIFDs The following steps are the proposed plan of action for Eco-Rapid to take as they look to implement EIFDs.

Note: some steps may run in parallel while others must be sequential.

1. Prior to establishing an EIFD, jurisdiction must dissolve remnants of redevelopment agency and

adhere to these guidelines (Enhanced Infrastructure Financing Districts, Provision 53398.54):

a. Within 10 days of a city or county’s legislative body’s action to participate in an IFD, the city

or county certifies to the Department of Finance and to the public financing authority that

no former redevelopment agency assets are the subject of litigation involving the state.

b. An EIFD may finance only the facilities authorized to the extent that the facilities are in

addition to those provided in the territory of the district before the district was created.

c. EIFD debt is subordinate to obligations of former Redevelopment Agency.

d. Available Tax Revenue does not include any pre-existing commitments to the

Redevelopment Property Tax Trust Fund.

2. Create funding mechanism to invest in General Plan Update. This need is being communicated to

the Cap and Trade monies of the State’s Strategic Growth Council (M. Pisano, Personal

Communication, November 2014).

3. Complete Station Area Land Use Plans, Specific Plan or General Plan updates for highest and best

uses (ex: adopt AECOM study). Planning for highest and best can be done through changes to

zoning and real estate improvements. Zoning changes involve changing land uses from residential

to commercial or light industrial. Real estate improvements include implementing Floor-to-Air ratio

(FAR) minimums and/or density requirements.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

15 | P a g e

4. The existing EPA coordinates individual jurisdictions to establish an EIFD around the proposed

station. Each jurisdiction will take the following steps:

a. Define the EIFD project scope. Recommend a 2-3 mile radius from Eco-Rapid Station to

capture the full breadth of investments and regeneration related to the station.

b. Create EIFD financing capacities by developing a Public Financing Authority with three

members of the jurisdiction’s legislative body plus two publicly appointed members.

Recommend including additional board members from MTA and County.

c. Board members will not receive compensation but are eligible for reimbursement of

expenses incurred during official duties.

5. Amend existing Joint Powers Authority (JPA) to coordinate financing activities, administration and

management of affiliated resources.

6. Through the JPA and using revenues contributed from jurisdictions EIFDs, hire staff specifically

dedicated to EIFDs for management of financial reporting required by EIFDs as well as

coordination with different agencies.

7. EIFDs develop and execute a package of financing tools. Based on the planning and entitlements in

each jurisdiction, the financing tools do not have to be the same across the line. However,

consistency will benefit the administrative duties of the JPA and encourage development by

mitigating the uncertainties and risk for the private sector. The package may, but is not limited to,

a combination of Tax Increment Financing, Development Impact Fee, Special Assessment Districts,

Development Agreement, and Parking Management (or Other User Fees).

8. If required, Issue Public Debt once funding sources has been decided.

a. The district requires only a 55% vote by constituents to approve public debt issuance for

AB8. The annual revenue stream of an EIFD that is used as an availability payment to

retire the obligation of a private investor does not need a vote.

b. An EIFD can be in place for up to 45 years.

9. Transition into day-to-day management and operations.

6 CASE STUDY: DOWNEY STATION In order to understand the financial opportunities of an EIFD, our team evaluated a singular station to

demonstrate how the individual jurisdictions may individually and collaboratively use EIFDs for Eco-Rapid

Funding. The proposed Downey Station serves as a strong example of the value capture possible using the

combined revenue streams provisioned for in an EIFD due to its complexity with three jurisdictions in the

regeneration catchment area (Downey, South Gate, and Cudahy), large swatch of County land in the station

area, and data available for analysis.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

16 | P a g e

Figure 2: Intersection of Gardendale Street and Garfield Avenue

6.1 Station Overview Known as the Downey-Gardendale Station, the station is located in a dynamic area of the City of Downey

where redevelopment and revitalization plans are creating a visionary mixed-use regional employment and

destination center. The predominant land uses surrounding the station area are single institutional to the

north and northeast and single-family residential south and southwest. Industrial uses dominate the main

north-south corridor. Two Specific Plans currently are in place:

1. Rancho Los Amigos Specific Plan: The business center, located in the southwest corner of the

city, is a public/private joint venture between the County and Fremont Properties on County-

owned Rancho Los Amigos Medical Center land. The concept involves phasing out the existing

medical center and replacing it with commercial manufacturing, including professional offices,

research and development activities, light manufacturing, financial institutions, and restaurants.

Retail uses would also be of convenience to employees and visitors of the other uses in the area

(AECOM, 2013).

2. Redevelopment Plan for the Downey Redevelopment Project: The proposed station is located

within Gardendale/Downey Area (see Figure 3). The Plan includes the City’s desire to improve,

upgrade, and revitalize all areas of the city, which have become blighted because of deterioration,

disuse and unproductive conditions. Objectives include providing construction and employment

opportunities in the new industrial/commercial establishments as well as encouraging existing,

surrounding owners, businesses, and tenants to participate in the redevelopment activities, thus

sustaining the existing economic base of the community (AECOM, 2013)

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

17 | P a g e

In addition, there are several General Plan Policies consistent with the station development project which

includes: Land Use Policy 1.2.1-Program 1.2.1.2, Economic Development Policy 9.1.2-Program 9.1.2.2, and

Circulation Element Policy 2.4.1-Program 2.4.1.1(AECOM, 2013).

Data Source: U.S Census Bureau, Southern California Association of Governments, Los Angeles County GIS Data Portal

Figure 4: Percentage of Non-white Population

Figure 3: Median Household Income

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

18 | P a g e

Figure 5: Existing Land Use Map

Data Source: Southern California Association of Governments

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

19 | P a g e

In the Gardendale station study area, the biggest parcel within the opportunity area is the Rancho Los

Amigos campus, owned by Los Angeles County. According to the Rancho Los Angeles Campus Specific Plan,

the future building program on the South Campus will accommodate a daycare center, restaurant, retail,

community facilities, office and other uses (AECOM, 2013). It shows a motive for Los Angeles County to

lease out the property and a huge opportunity to generate revenue with EIFD. If the county is willing to

engage in the TOD project, more tax revenue can be captured. When a person or entity leases, rents or

uses real estate owned by a government agency for its exclusive use, a taxable possessory interest occurs.

The taxation of this type of interest is similar to the taxation of owners of privately owned property.

6.2 Opportunities for Value Capture The EIFD offers an opportunity to finance existing and future infrastructure, as cites are able to use tax

increment financing to capture wealth. Value is created (and should be captured) by zoning change, real

estate improvements, and investment in a transformative infrastructure of the transit line that can

regenerate the area around the stations. Further, these investments are long-term and effects are

compounded over the duration.

Change in Zoning: Development of a rail station and change in land use can facilitate new development

and ensure better utilization of the infrastructure. Cities can capture value by changing land use, including

density and land use types. Together, this can increase land value. These projects are intentionally

designed attract economic development.

Specifically with this rail project, Transit-Oriented-Developments (TOD) will feature a mix of land uses,

moderate to high density, pedestrian mobility and connectivity, and better landscape design. According to

Garfield Corridor Specific Plan, the zoning along the Garfield Corridor will be converted from residential use

to retail use (City of South Gate, 2009).

Real Estate Improvement: As property value is assessed by the land value and improvement on land, real

estate improvement can be another strategy to capture wealth. This type of value increase is usually

associated with zoning changes but is above and beyond. The change in land use will inevitably lead to new

real estate improvements, for example to build a new retail store. And the change in density will directly

encourage higher FAR or more building units based on existing land use, for example to build a new

apartment on existing residential use land. Noticeably, land value won’t change until transaction of land

occurs. So density increase won’t necessarily lead to increase in land value while real estate improvements

on use-changed land could capture both increases in land value as well as improvement value.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

20 | P a g e

In the Gardendale / Downey station case; there are two types of real estate improvement generating

revenues. First, retail and commercial improvement will occur after a zoning change along Garfield

Corridor. For instance, the retail office and industrial development along with zoning change of the Rancho

Los Amigos Plan will generate nearly one million tax increment revenues (AECOM, 2013). Second, value will

increase as a result of residential or commercial improvements encouraged by density increase from the

new transit village near the Firestone & Atlantic Intersection as detailed in the Redevelopment Specific Plan

for Downey Redevelopment Project. A second transit village on Garfield Avenue with plans for high density

housing, retail and office use, as detailed in the City of Southgate General Plan 2035, will further perpetuate

real estate improvement in the area (Community Design + Architecture). As the rail project will improve

mobility and accessibility, new construction will be likely take place within the opportunity areas around the

stations. The introduction of Eco-Rapid Transit will create a huge opportunity to capture real estate

improvement wealth.

Investment and Regeneration around the Station: Studies demonstrate transit lines have a positive

effect on property value in the station vicinities 11. However, the “transit premium”, or the value added to

property by locating proximity to public transit, may vary depending on distance and property type. This

impact of transit on property value is scaled, as seen in Table 1. Even with no change in zoning or real

estate improvements, cities recognize value by investing in transit development project.

In terms of Gardendale Station, by creating an EIFD the City of Downey and the City of Southgate can use

tax increment financing along with other financing tool to fund the eco-rapid transit project and in turns

capture a long term “transit premium” (Nelson-Nygaard Consulting Associates Inc., 2012).

Table 3: Summary of Estimated Property Value Premium (Nelson-Nygaard Consulting Associates Inc, 2012)

Long-Term Impacts of These Investments: Public transit investment can have significantly positive

impact on economy both in short-term and long-term. well-known long-term impacts like cost saving, social

justice benefits, and environmental benefits, cities also recognize compounding values of the revenues

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

21 | P a g e

streams created by transit projects. Gains captured by zoning change, real estate improvement, transit

premium and possessory interests can be compounded over a 45-year time frame in an EIFD.

6.3 Financial Strategy & Modeling Results Analysis demonstrates that the best opportunities to capture the wealth created by the proposed

Gardendale/Downey Station will be through (A) property tax increment and developer fees, (B) revenues

from property tax corresponding to the increase in assessed valuation of taxable property attributed to

those property shares received by a city or county pursuant to in lieu of Vehicle License Fees, and ‘(C)

parking management user fees. The revenue streams recognized here are based on a best estimate for

future land use plans. (Note: it is strongly advised that prior to establishing an EIFD, the jurisdictions

surrounding the station make a coordinated approach to develop land use plans that yield the highest and

best land uses for value capture).

6.3.1 Tax Increment Financing and Developer Fees

Tax Increment Financing (TIF) is a funding tool available for use by the EIFD, which allows the district to

capture a portion of the increased property tax values resulting from a development project. To determine

the growth, the current-assessed value of all parcels within a boundary (the base value) and the resulting

property tax value must first be determined. Once the base value has been established, the increased

property assessed value, resulting from the new development, will be calculated in order to determine the

incremental property tax value that can be allocated to the district.

For the Gardendale/ Downey Station Case, we propose a time two-phase business plan in order to capture

potential value. The first phase captures increases in value from 2014-2019, while the second phases

focuses on increases expected from 2020-2025. This two-phase business plan will incorporate gains

recognized from rezoning, real estate improvement, transit premium generated from the station, taxable

possessory interest as well as integrate all four financing tools identified above. Figure 6 illustrates the

proposed future land uses within the ½ mile catchment basin. Detailed of assumptions and analysis can be

found in the Appendix C.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

22 | P a g e

Figure 6: Future Land Use of Gardendale/Downey Station Based on Highest and Best Use

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

23 | P a g e

Phase 1: A high density, mix-used Garfield corridor with commercial vitality and a more attractive

employment center in Hollydale Industrial District.

According to Garfield Corridor Specific Plan, Garfield Corridor is designed to evolve into a corridor

resembling a revitalized main street with a variety of residential uses, high-end retail, improved landscaping

and building improvement that promote a pedestrian-oriented corridor. In the General Plan 2035, it

designates to improve density along the Garfield Corridor on FAR and units/acre (City of South Gate, 2009).

Following the Specific Plan and General Plan, the team identified the following value capture opportunities:

1) Rezoning along Garfield Corridor by converting 50% of the residential use land to commercial and retail

use; 2) Increasing commercial and retail land use density up to FAR 3.0 as shown in other LA Metro TOD

projects and the residential land use density to 30 units/ acre; 3) Facilitate real estate improvement on both

re-zoned parcels and existing residential and commercial uses by allowing three-story commercial building

residential buildings corresponding to the density increase (improvement costs are $211/SF for commercial

and $191,000/ D.U for residential uses respectively); 4) Instituting a developer Fee in both Garfield Corridor.

Developer fee is charged at $28/SF on commercial and retail development while a $26,000/D.U. fee for

residential projects (Economic & Planning Systems Inc., 2014).

In addition to the Garfield Corridor, rezoning in the Hollydale Industrial District constitutes value capture

opportunities, where the Specific Plan encourages transition from manufacturing/distribution to highly

desired light industrial/flex to make this district more attractive. This includes converting heavy

manufacturing parcels into retail and light industrial uses and increase the density in the whole district up

to FAR 2.0 (City of South Gate, 2009). Consistent with the Garfield Corridor, real estate improvement and

developer fee were also identified as value capture opportunities (Economic & Planning Systems Inc., 2014).

Improvement costs are $104/SF for light industrial development and 10% of the construction cost can be

attributed to developer fee.

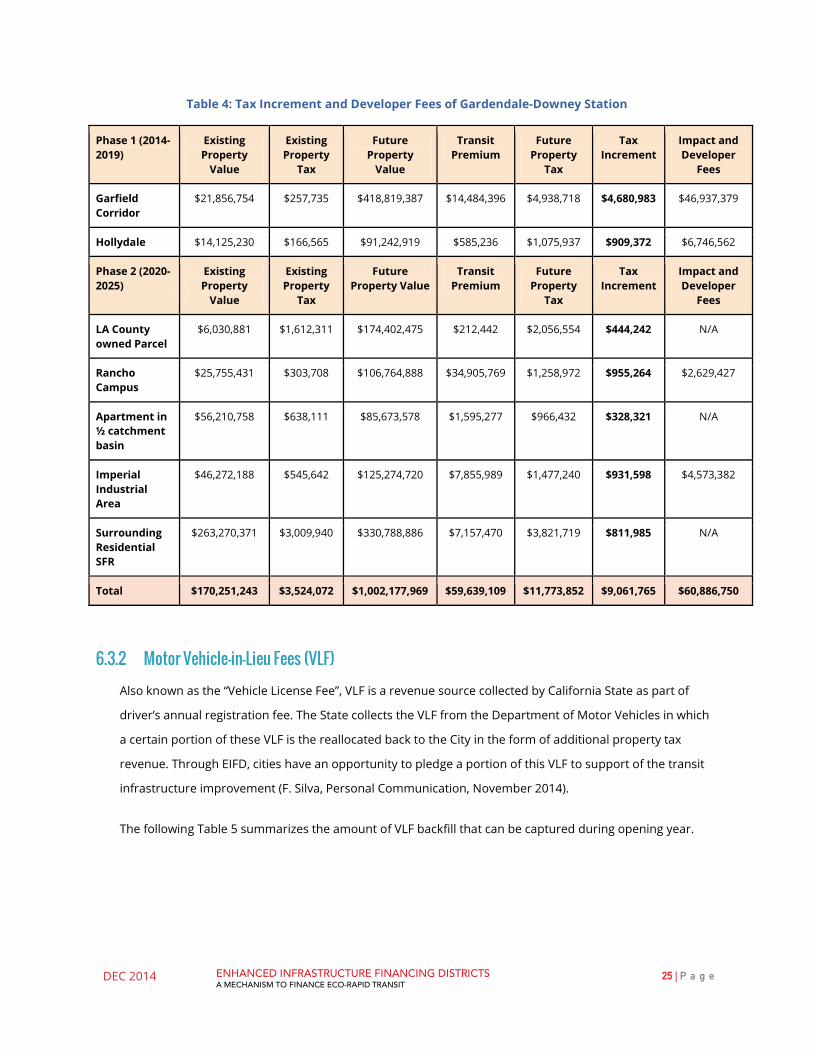

Using these assumptions and recommendations, future property values along Garfield Corridor increased

from $21,856,754 to $418,819,387 yielding, $4,680,983 in available tax increment per annum and

$46,937,379 developer fees available in 2025. The Hollydale Industrial District yields a tax increment of

$909,372 per annum and $6,746,562 in developer fees available in 2025.

Phase Two: An economically robust transit-oriented district within a ½ catchment basin from the

Gardendale/Downey Station.

Introducing public transit station will create a positive transit premium on nearby property values,

commercial activities and urban growth (Nelson-Nygaard Consulting Associates Inc., 2012). With the

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

24 | P a g e

opening of Gardendale/Downey Station, possessory interest, VLF backfill money, transit premium, real

estate improvement, developer fees and parking management fees

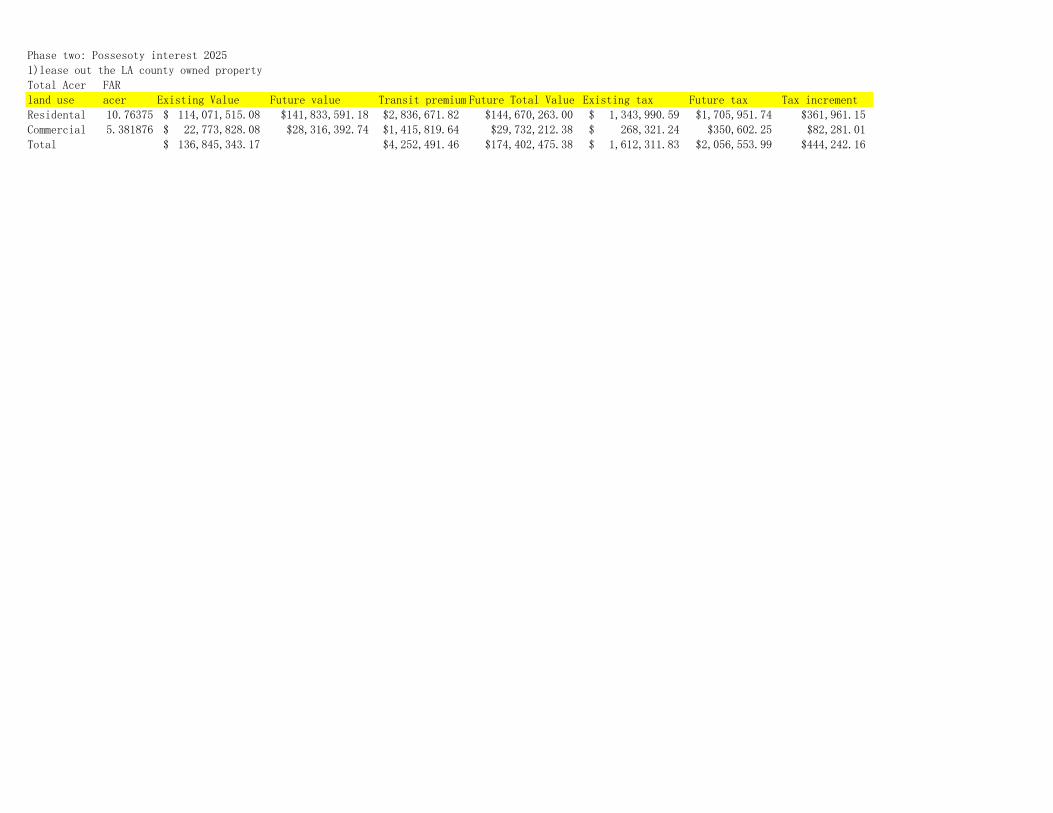

In the northeastern side of the Gardendale/Downey Station, there is approximately 74 acres of Los Angeles

County owned mixed-use land known as the “Rancho Campus.” According to Rancho Los Amigos Campus

Plan, the Rancho Campus will consolidate a revitalized rehabilitation center and administrative campus

housing with public amenities and recreational spaces. By constructing physical improvement and leasing

out near 20 acre of parcels in adjacent to the South Rancho Campus, there becomes an enriched the

revenue stream through taxable possessory interest. This South Rancho Campus includes office,

commercial uses, industrial uses, daycare center and other community and county offices with total

1,808,116 building SF available for real estate improvements which should include imposing a 2:8 retail to

residential uses ratio and 3.0 FAR. The City of South Gate’s property tax is suggested for tax rate of

possessory interest.

Under the jurisdiction of the City of South Gate, the Imperial Industrial District is situated between the

proposed Downey-Gardendale Station and the Los Angeles River. As of the currently, the district is mainly

comprise of heavy manufacturing, light industrial, warehouses and sporadic parcels of commercial uses

(City of South Gate General Plan 2035, 2009). According to the General Plan, land uses along the major

corridors of Garfield Avenue and Imperial Highway is envisioned to be converted to multi-family residential

buildings in support of the potential Eco-Rapid Transit station (City of South Gate General Plan 2035, 2009).

Land uses adjacent to the LA River can still be utilized as light manufacturing; however, Office and Research

& Development (R&D) land uses are highly desirable (City of South Gate General Plan 2035, 2009). In the

opening transit year of 2025, currently vacant and/or undesirable land uses were converted to the vision

listed above.

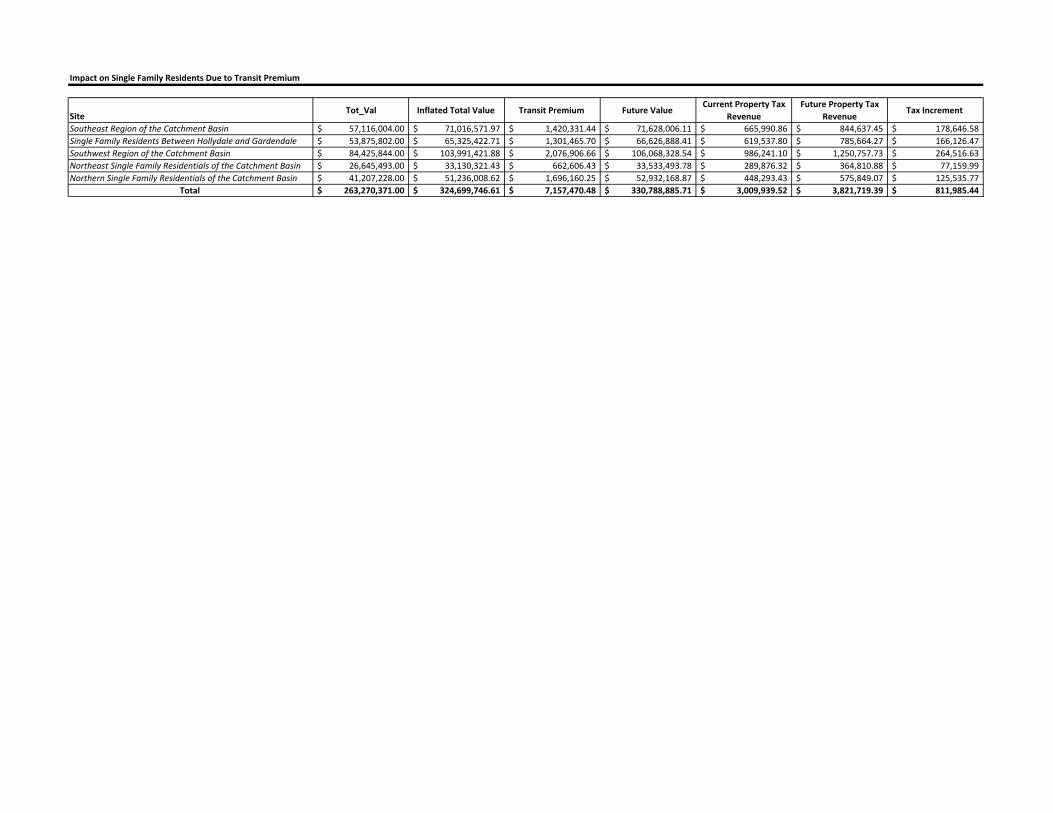

In the second-phase of our business strategy, we are estimated to successfully generate $3,471,410 future

tax increment per annum, $444,242 of which results from taxable possessory interest. Through real estate

improvement on South Rancho Campus, we could capture around $955,263 tax increment per annum and

$2,629,427 in developer fees available 2025. The opening of the Gardendale/ Downey Station will bring

$328,321 transit premium exclusively on condominium and apartment. Imperial industrial area and

surrounding residential SFR will generate $931,598 and $811,598 tax increment respectively.

Combining both phase one and phase two, the total tax increment per annum reaches $9,061,765 with an

amount of $56,313,368 developer fees. More tax increment detail is showed in the following table:

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

25 | P a g e

Table 4: Tax Increment and Developer Fees of Gardendale-Downey Station

Phase 1 (2014-2019)

Existing Property

Value

Existing Property

Tax

Future Property

Value

Transit Premium

Future Property

Tax

Tax Increment

Impact and Developer

Fees

Garfield Corridor

$21,856,754 $257,735 $418,819,387 $14,484,396 $4,938,718 $4,680,983 $46,937,379

Hollydale $14,125,230 $166,565 $91,242,919 $585,236 $1,075,937 $909,372 $6,746,562

Phase 2 (2020-2025)

Existing Property

Value

Existing Property

Tax

Future Property Value

Transit Premium

Future Property

Tax

Tax Increment

Impact and Developer

Fees

LA County owned Parcel

$6,030,881 $1,612,311 $174,402,475 $212,442 $2,056,554 $444,242 N/A

Rancho Campus

$25,755,431 $303,708 $106,764,888 $34,905,769 $1,258,972 $955,264 $2,629,427

Apartment in ½ catchment basin

$56,210,758 $638,111 $85,673,578 $1,595,277 $966,432 $328,321 N/A

Imperial Industrial Area

$46,272,188 $545,642 $125,274,720 $7,855,989 $1,477,240 $931,598 $4,573,382

Surrounding Residential SFR

$263,270,371 $3,009,940 $330,788,886 $7,157,470 $3,821,719 $811,985 N/A

Total $170,251,243 $3,524,072 $1,002,177,969 $59,639,109 $11,773,852 $9,061,765 $60,886,750

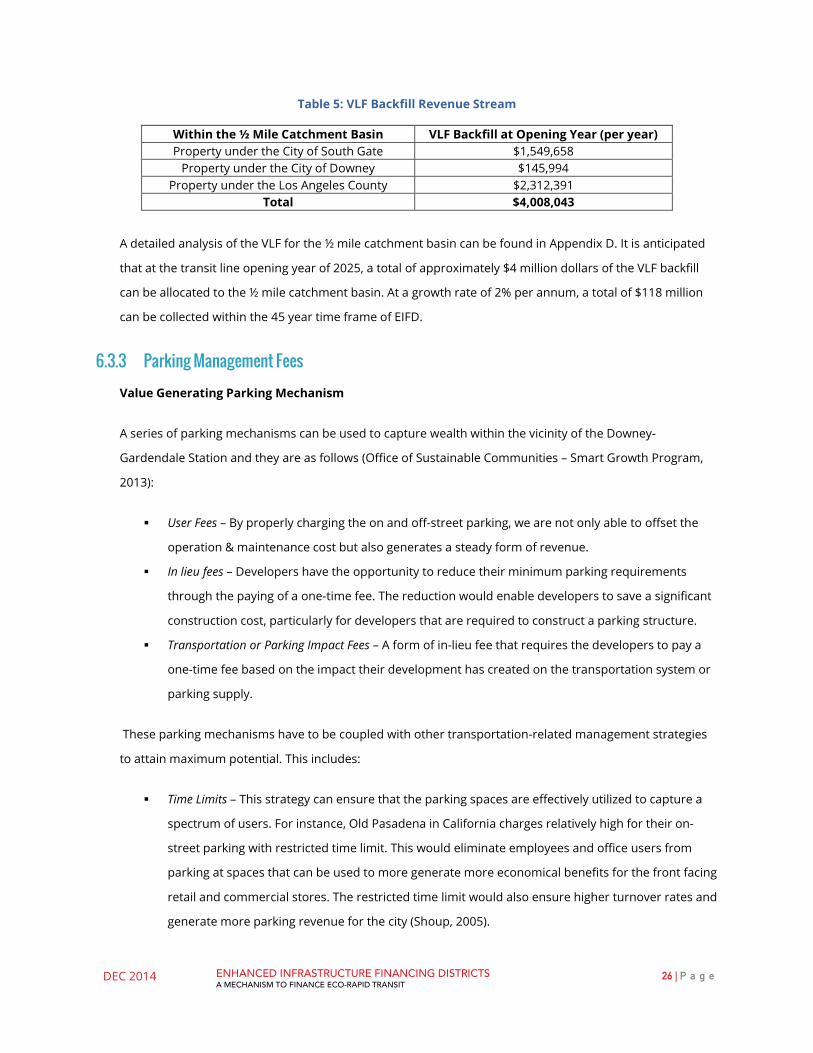

6.3.2 Motor Vehicle-in-Lieu Fees (VLF)

Also known as the “Vehicle License Fee”, VLF is a revenue source collected by California State as part of

driver’s annual registration fee. The State collects the VLF from the Department of Motor Vehicles in which

a certain portion of these VLF is the reallocated back to the City in the form of additional property tax

revenue. Through EIFD, cities have an opportunity to pledge a portion of this VLF to support of the transit

infrastructure improvement (F. Silva, Personal Communication, November 2014).

The following Table 5 summarizes the amount of VLF backfill that can be captured during opening year.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

26 | P a g e

Table 5: VLF Backfill Revenue Stream

Within the ½ Mile Catchment Basin VLF Backfill at Opening Year (per year) Property under the City of South Gate $1,549,658

Property under the City of Downey $145,994 Property under the Los Angeles County $2,312,391

Total $4,008,043

A detailed analysis of the VLF for the ½ mile catchment basin can be found in Appendix D. It is anticipated

that at the transit line opening year of 2025, a total of approximately $4 million dollars of the VLF backfill

can be allocated to the ½ mile catchment basin. At a growth rate of 2% per annum, a total of $118 million

can be collected within the 45 year time frame of EIFD.

6.3.3 Parking Management Fees

Value Generating Parking Mechanism

A series of parking mechanisms can be used to capture wealth within the vicinity of the Downey-

Gardendale Station and they are as follows (Office of Sustainable Communities – Smart Growth Program,

2013):

User Fees – By properly charging the on and off-street parking, we are not only able to offset the

operation & maintenance cost but also generates a steady form of revenue.

In lieu fees – Developers have the opportunity to reduce their minimum parking requirements

through the paying of a one-time fee. The reduction would enable developers to save a significant

construction cost, particularly for developers that are required to construct a parking structure.

Transportation or Parking Impact Fees – A form of in-lieu fee that requires the developers to pay a

one-time fee based on the impact their development has created on the transportation system or

parking supply.

These parking mechanisms have to be coupled with other transportation-related management strategies

to attain maximum potential. This includes:

Time Limits – This strategy can ensure that the parking spaces are effectively utilized to capture a

spectrum of users. For instance, Old Pasadena in California charges relatively high for their on-

street parking with restricted time limit. This would eliminate employees and office users from

parking at spaces that can be used to more generate more economical benefits for the front facing

retail and commercial stores. The restricted time limit would also ensure higher turnover rates and

generate more parking revenue for the city (Shoup, 2005).

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

27 | P a g e

Shared Parking – Allowing various land uses to share the same parking facility instead of

constructing parking facilities separately (Office of Sustainable Communities – Smart Growth

Program, 2013). Having one parking facility can also enable motorist to visit multiple destinations

without having drive. In addition, developers are also able to reduce their parking requirements

when parking facilities are shared. For instance, the peak parking demand for restaurants are at

weekend nights while another land use like office has peak parking demand during weekday

(Litman, 2013).

Reducing Parking Requirements – The introduction of transit corridor encourages the surrounding

community’s reliance on automobiles as their primary form of transportation. Hence, conventional

parking requirements can be significantly reduced to accommodate the lower automobile trips

(Shoup, 2005).

There are opportunities to utilize all the parking management strategies to capture revenue. However, for

the purpose of the study, emphases have been made on in-lieu fees, and reduce parking requirements.

User fees was not take into consideration as it would require a detailed understanding of the potential

market condition of the area as well as the forecasted transit ridership that the station.

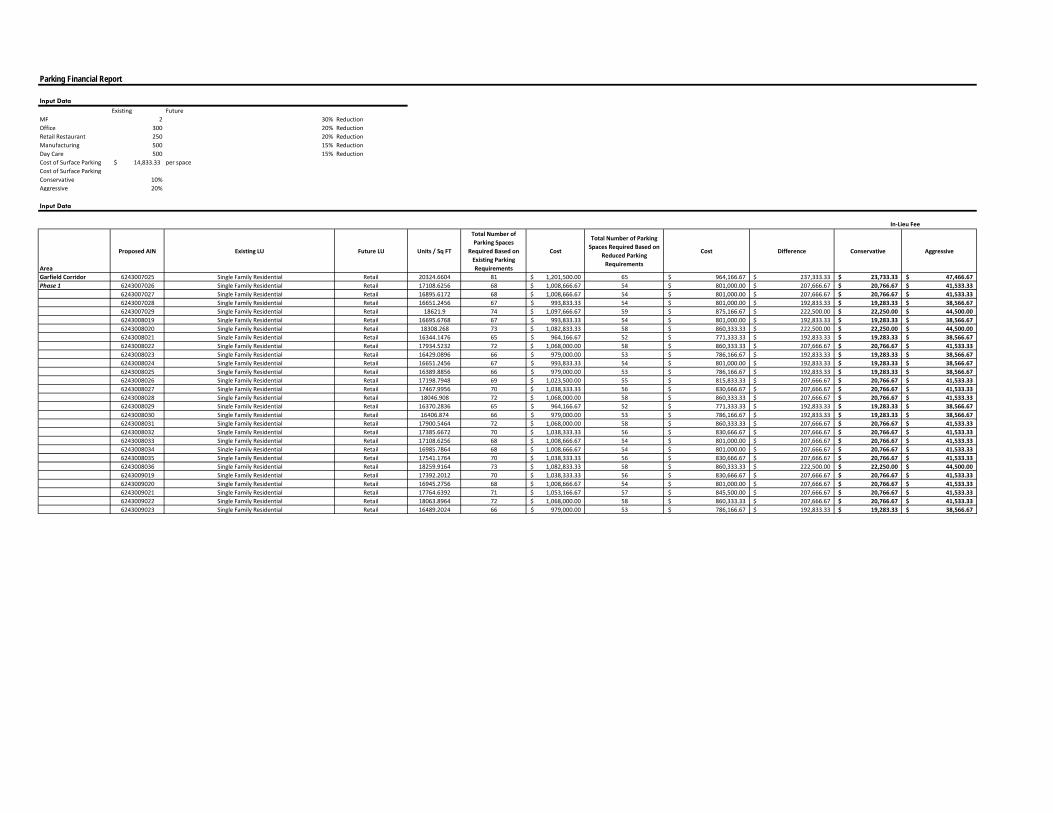

Parking Analysis In-Lieu Fees

As mentioned previously, the purpose of the in-lieu fee is to enable developers to reduce their parking

requirements in replacement of a one-time development fee. This parking mechanism is favourable

towards developers as they can significantly reduce their burden in attempts to meet the conventional

parking requirements. In-Lieu fee is also valuable to the City as revenue can be obtained from reducing

parking requirement which then can be used for facilitate other transportation improvements.

In order to determine the in-lieu fee generated by the half-mile catchment basin, the following approach

was utilized:

1. Identify the required parking spaces for every proposed development based on the existing

standards.

2. Generate the construction cost associated with the required parking spaces.

3. Reduce the parking requirement and identified the reduced parking spaces required for every

proposed development.

4. Generate a construction cost associated with the reduced parking spaces.

5. It is then assumed that 20% (aggressive approach) of the different between cost of required

and reduce parking spaces would be the in-lieu fee paid by the developer as form of

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

28 | P a g e

development fee. A conservative approach of 10% was also taken into consideration (see

Appendix E).

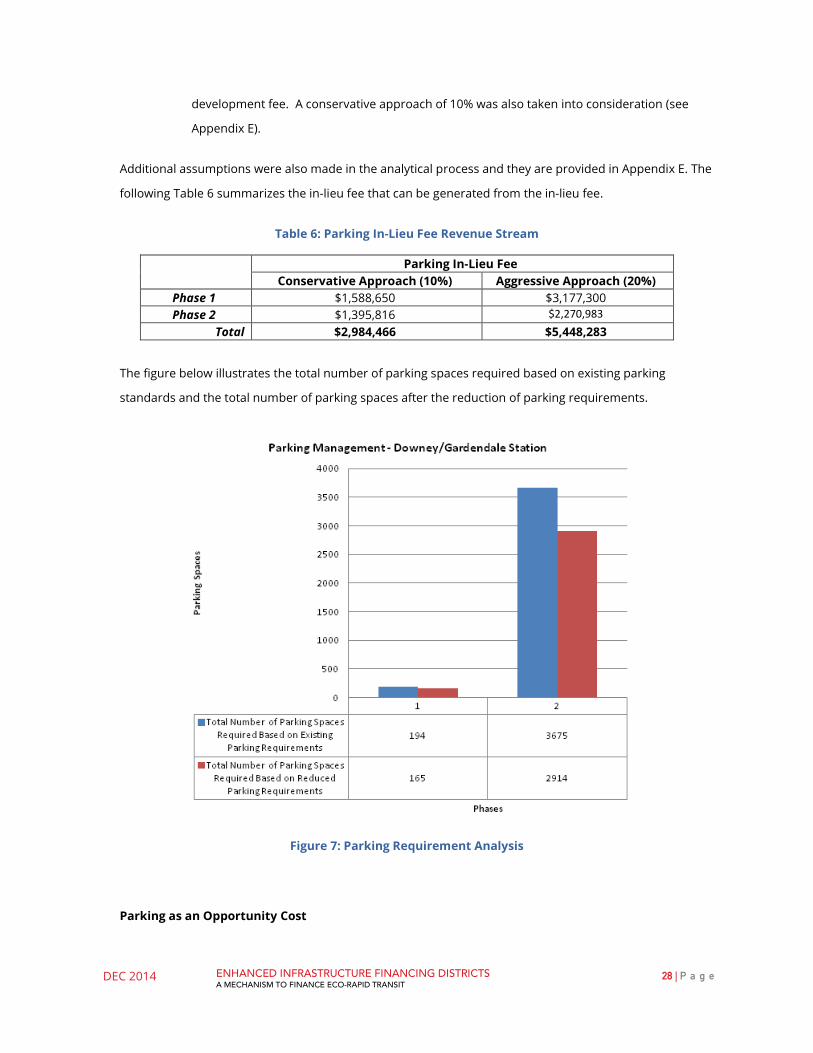

Additional assumptions were also made in the analytical process and they are provided in Appendix E. The

following Table 6 summarizes the in-lieu fee that can be generated from the in-lieu fee.

Table 6: Parking In-Lieu Fee Revenue Stream

Parking In-Lieu Fee Conservative Approach (10%) Aggressive Approach (20%)

Phase 1 $1,588,650 $3,177,300 Phase 2 $1,395,816 $2,270,983

Total $2,984,466 $5,448,283

The figure below illustrates the total number of parking spaces required based on existing parking

standards and the total number of parking spaces after the reduction of parking requirements.

Figure 7: Parking Requirement Analysis

Parking as an Opportunity Cost

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

29 | P a g e

For the past couple of decades, parking planning have been perceived as a public good in which there

should be (1) abundant supply of parking and; (2) free at majority of the traveller’s destination. This

perception of urban planning have resulted in the constructed of underutilized parking facilities that has

left local government to face budget shortfalls. In addition, conventional parking standards take on a

conservative approach in which further exacerbating the parking supply required (Shoup, 2005).

By reducing the parking requirement and applying in-lieu fee, we are able to capture the correct value of

parking. The reduction of parking supply enables developer to free up their land and utilized those

additional spaces for better community improvements (City of South Gate, 2009). As indicated previously,

the value of land within the vicinity of the Transit station increase with respect to time. The opportunity

cost of those parking spaces within the area would also increase proportionally. Through the identification

of various supportive parking policies and parking management strategies, we would be able to facilitate

developers in meeting the anticipated parking demands while being fiscally sustainable.

6.4 Summary of Value Capture The following Table 7 summarizes the value captured using various financials tools.

Table 7: Summary of Value Capture for Downey-Gardendale Station

Downey-Gardendale Station Tax Increment Financing (per year) $9,061,765 Developer Impact Fee (one-time fee) $60,886,750

VLF Backfill (per year) $4,008,043 Parking In-Lieu Fee (one-time fee) $5,448,283

Total Capture at Opening Year, 2025 $79,404,841 Total Net Value Capture (45 Year Time Frame) $464,835,576

Approximately $79 million dollars can be captured at the 2025 opening year of the transit station. Long-

term, the investments result in total value capture of $464 million for a 45 year time frame as per the

structure of the EIFD. By implementing the right investment strategies with the introduction of the Eco-

Rapid Transit, the total assessed value of the ½ mile catchment basin around the Gardendale / Downey

Station alone increased from $301 million in 2014 to $2.44 billion, 45 years later. This is approximately 7

times the original assessed value of property that once was considered to be a rust belt.

DEC 2014 ENHANCED INFRASTRUCTURE FINANCING DISTRICTS A MECHANISM TO FINANCE ECO-RAPID TRANSIT

30 | P a g e

7 TOOLS FOR SUCCESSFUL ANALYSIS The example analysis was a simplistic and rudimentary approach to gain understanding of an EIFD’s

magnitude; however, there are many products available to calculate the exact value capture for which

jurisdictions may issue debt.

Envision Tomorrow Plus (ET+) is a suite of urban and regional planning tools that support planning for the

future of cities and regions. The ET+ can be used to model development feasibility on a site-by-site basis as

well as create and evaluate multiple land use scenarios. In addition to the modeling and evaluating

functions, The ET+ can also test and refine transportation plans, produce small area concept plans, and

model complex regional issue. In this project, the ET + is applied to model the land use changes around the