enhanced financial reporting for state government: comparing cost to performance

DESCRIPTION

ÂTRANSCRIPT

July 2009

Oklahoma Councilof Public Affairs

1

seeking to hold government to account for itsperformance will have far better information withwhich to do so, and find what is currently avail-able on transparency websites more relevant andunderstandable.

For decades, Oklahoma has lagged behind therest of the country in per capita personal income,perhaps the broadest available measure of gen-eral prosperity. Not surprisingly, Oklahoma alsotrails in most indicators of health and education.While Oklahoma has shown improvement relativeto the rest of the country over the last 12 years, thestate’s per capita personal income remains miredin the lower half of the states.

Along with most other states, Oklahoma’selected officials struggle to adequately fundprograms to improve the health, education, trans-portation, and safety of Oklahomans. Advocates ineach of these areas can show accurate statisticsindicating that current funding is inadequate tothe task at hand. Others can make similarlycompelling arguments that the current funding isspent on programs that do not work.

Meanwhile, the problems our national leadersface dwarf those with which Oklahoma leaderswrestle. At this writing, avowed terrorist enemies ofthe United States are threatening to take control ofa country that has nuclear weapons, more than 45million Americans are reputed to be withoutadequate health insurance, and the economy isattempting to digest unprecedented levels ofgovernment intervention into private markets.

At the same time, the national government facesobligations for Social Security and Medicarebenefits it cannot meet without significant andpossibly very painful reform.

Yet, since the earliest days of the Republic,Americans have rallied in times of crisis and havefound the means to solve the problems facing thecountry.

As in the past, the first step is to realize andaccept the fact that we have a problem. The nextstep is to determine the extent of the problem andto begin evaluating the cost and potential effec-tiveness of alternative solutions.

Better accounting and financial reporting canplay a significant role in identifying and quantify-ing our problems and developing solutions. UsingOklahoma as an example, this paper attempts toshow how enhanced financial reporting can helpus better understand the nature of the issuesconfronting us and better evaluate our options.

Preface

Oklahoma and the United States face manyserious problems. We face enormous financialissues in the unfunded obligations of SocialSecurity and Medicare. Many in our society arenot sufficiently educated to lead productive lives.Many others suffer from social pathologies thatresist the efforts of existing government programsto alleviate them. At the same time, we facethreats to our very existence from terrorists thatmay make substantial unexpected demands onour fiscal resources.

At the state level, Oklahoma faces a majorproblem with the unfunded liabilities of its retire-ment systems. Meanwhile, it struggles with thesame problems as other states to provide for theeducation, health care, transportation, and otherneeds of its citizens.

Governments at all levels must balance bud-getary demands with available resources. At thesame time, they must deliver quality services thatsolve problems. The public has reason to fretabout the financial position of its governments.

The public also needs assurances that we areeducating our children well enough to compete inthe global economy; that all citizens have accessto adequate health care; that our roads are wellmaintained; and that other programs their taxdollars fund contribute to a better society. Despitecontinued efforts by our government leaders,progress seems slow or even non-existent.

Have poor accounting practices contributed tothese problems, or at least failed to provideinformation critical to developing workablesolutions? Have government accounting practicesallowed or even facilitated government servicesthat are ineffective and too costly? This paper willexplore the relationship between our system ofgovernment and its accounting and financialreporting practices.

This paper is written with the belief that whilethe problems we face are not without solutions, wemust recognize those problems and address thempragmatically. It is also written with the belief thatimproved accounting and financial reportingpractices can improve the quality of governmentservices, lowering their cost with both immediateand long-term positive impacts on our society.Accounting and reporting can contribute far moreto solving our problems than they do at present.

As we shall see, improved accounting andfinancial reporting practices can make currenttransparency initiatives more potent. A citizen

2

Accounting and societal values

We don’t always relate accounting and finan-cial reporting to values, but understanding theconnection between them is crucial to making theimprovements we need.

When the United States won its independence,most people in the world lived as subjects of amonarch or other ruler and his or her vassals. Anindividual’s existence relative to the governmentwas simple. The subject owed obedience to theking or queen and the monarch was expected toat least provide a degree of protection to his orher subjects.

An individual in such a society had no need offinancial reporting from the government. Theindividual played no role in directing the affairs ofthe government and,strictly speaking, thegovernment owed itscitizens nothing.

The ruler organizedthe government andwhatever benefits thegovernment providedwere for the ruler’sultimate ben-efit. The ruler’sprincipalinterest was inmaintainingorder andprovidingenough ser-vices to makeorganizedinsurrectionunappealing. The subject simply eked out anexistence within this system and did not need toconcern himself with how well or how efficientlygovernment delivered its services.

The ruler’s subjects lived to tend to the ruler’sbusiness, most often by working the ruler’s fields.The subjects bought the ruler’s goods and wor-shipped according to the ruler’s religion. Thosewho violated these duties often learned that theruler did not bear the sword for nothing.

At that time, the government was simply theruler’s means of enforcing his or her desires.Similar arrangements can be found today incountries mired in despotism. Until 20 years ago,the Soviet Union, the second most powerful nationon earth militarily, organized its society on the

basis that man’s duty was to serve the state.The important aspect of this for our purposes is

to consider what information a well-designedfinancial report from such a despotic governmentwould convey. We would first observe that thegovernment officials would report to the ruler.Accordingly, any reports would be prepared forhis or her benefit (Figure 1).

However, our country was founded on differentprinciples, the most basic being that men haveGod-given rights and that their governmentshould only govern by their consent. This beliefcompletely overturned the previous arrangementand said, in effect, that the government is to serveits citizens rather than the other way around.

Our founders did not institute anarchy. How-ever, they did establisha system where thepeople could ultimatelycontrol their governmentand make it answerableto them.

While Americans mayhave replaced a kingwith a constitution, their

government’sreports on itsactivities seembetter suited toa monarchy.Our system ofaccountingand financialreporting usedin every stateand at the

federal level is designed as if to hold appointedofficials responsible to the elected officials. Weshould be holding the elected officials respon-sible to those who elect them and pay the taxes tosupport their activities (Figure 2).

We should also note that our system of govern-ment is inherently a bottom-up design while thesystem it replaced was a top-down arrangement.This difference is worth more than passing notice,because the nature of the accountability demandsa systematic and orderly reporting in order toachieve the desired level of accountability. A rulercan ask questions or demand information as theneed arises. However, the diffuse nature of theelectorate renders an ad hoc reporting systemineffective.

3

A citizen in a republic needs a comprehensivesystem that reports what the elected leaders havedone with the power the citizens have delegatedto them. What assets have been created for publicuse? What liabilities have been incurred for whichthe citizen bears ultimate responsibility? Whatproblems have been addressed? What have beenthe results and at what cost?

The purpose of government

The preamble to our Constitution explains whyit was established:

We the people of the United States, in order

to form a more perfect union, establish justice,

insure domestic tranquility, provide for the

common defense, promote the general welfare,

and secure the blessings of liberty to ourselves

and our posterity, do ordain and establish this

Constitution for the United States of America.

With thisfamiliar pas-sage in mind,we should askwhy we havegovernmentprograms. Dothese pro-grams exist tomeet society’sneeds? Or, dothese programs exist to favor one interest groupover another or over the general public?

Most of us would prefer that our governmentaddress problems on behalf of all citizens ratherthan simply act on behalf of special interests. Yet,as we shall see, our current policies of financialreporting are more appropriate for a governmentthat sees itself as an arbiter of competing specialinterests rather than as an instrument to securethe blessings of liberty for its citizens.

Our elected leaders have a duty to the elector-ate to account for the effectiveness and cost ofwhatever programs they implement. Currently, oursystem of accounting and financial reportingstops short of this ideal, largely limiting itself toreporting whether the legally adopted budget wasfollowed and various regulations regardingexpenditures were observed. Budgetary compli-

ance should not be the focus of accounting and

financial reporting in America.

To illustrate, let us hypothesize that the purposeof government is not to serve the general welfare

but to reallocate resources from taxpayers tovarious competing special interest groups. If thiswere the purpose of the American system ofgovernment and the system had not degeneratedinto despotism, we would probably expect it toreport its results in a manner very similar to whatwe do now under generally accepted accountingprinciples (GAAP) (Figure 3).

If the purpose of government is not to runeffective programs that maintain justice anddomestic tranquility, defend us against the forcesof those who mean us harm, promote the generalwelfare, and secure the blessings of liberty, butrather to carve up a budgetary pie among com-peting special interests, would we not want areporting system that focuses on the budget ratherthan on results? We would see the carving up ofthe pie as the end in itself rather than as a steptoward providing useful services to the public.

In such anenvironment,we wouldexpect thereportingsystem to focuson the ex-change ofresourceseasily gatheredand currently

redistributed. We would expect a reporting systemthat looks very much like what we have had formost of the last century.

To use our social safety net as an example, arewe primarily interested in helping those lessfortunate improve their lot, or are we primarilyinterested in transferring resources from thegeneral public to special interests? These specialinterests may either profit or earn a living from theprograms directly, perhaps only doing enough forthe poor so that the transfer can be justified assomething other than outright theft.

This is not meant to disparage the motives ofsocial workers or vendors to social service pro-grams. I have spent most of my career either ingovernment directly or as a consultant to govern-ment and have gained a great sympathy for theplight of civil servants and contractors. But,speaking as a government employee or contrac-tor, my concern is not about what we receive, butabout what we do with what we receive.

I am proposing in this paper that our elected

4

leaders have an inherent duty under our system toexplain their goals, what they are doing toachieve those goals, and to what effect and atwhat cost. And, yes, if our elected leaders refuseto explain themselves in this way, we shouldremove them.

If the government exists for the benefit of thegoverned, and because the governed delegatepower to those they elect, it follows that theelected are accountable to those who electedthem for the performance of the entire governmentunder their charge. How effective are their pro-grams in addressing our collective problems?How efficiently are those programs run? What istheir output? Are they achieving their goals? And,beneath these questions, we should know at whatcost the programs are carried out and how muchof that cost remains to be borne by future taxpayers.

How should we design a reporting system for

government in America?

If we are to have a reporting system that servescitizens as its first order, we must have a systemthat reports to those citizens and reports theinformation they need. These citizens have del-egated authority to the government, which meansthat, in return, the government should report back:

• What it does• What it costs to do it• What it providesWe can distinguish between what financial

reporting is needed from a government focusedon promoting the general welfare and one fo-cused on patronage and the transfer of resources.Special interests do not require extensive finan-cial reporting to know what they have received.The special interest advocate is focused on only arelatively small part of the overall picture. Thespecial interests will know the size of the contract,tax credit or even employment they receive as aresult of their lobbying.

However, the general citizen-taxpayer needsinformation precisely because, when it comes tolobbying, he or she is “out of the loop” and inneed of facts objectively presented.

In reporting to its citizens, the governmentshould outline what it does. It should include allactivities undertaken through the authority del-egated to it by the electorate. The electorateauthorizes the formation of a government and setsthe limit of its powers. This means that the entityof the government is defined by the limits of its

power. All things over which the elected leadersexercise control, either directly or indirectlythrough appointments, should be included as partof the entity. All matters outside that delegation,regardless of the financial interplay, are not partof the entity.

At the same time, not all citizens have the samelevel of interest in all the programs a governmentadministers. For example, some citizens may wantmore information about programs focused oneducation, others may be more concerned aboutprotecting the environment and still others aboutpublic safety. A large complex government canfulfill its responsibility to the general public andstill publish more detailed financial reports on itsprograms for those who have greater interest inthose programs. In all cases, the focus of thereports should be on the results and the cost.

As explored in an earlier stage of this project,1

the financial statements should focus on what itcosts the government to carry out its activities.That cost should be measured just as the publicgenerally understands cost, consistent with privatesector reporting.

The financial statements should also providerelevant information about what the governmentprovides in return for the costs it incurs on thepublic’s behalf. This is a major departure fromcommercial accounting because, unlike a for-profitenterprise, the benefit of the government’s activitycan often not be measured in dollars and cents.

A corporation incurs costs in order to sell itsgoods and services. It can measure those costs indollars. In return for its efforts, the corporationmakes sales and collects revenue, which are alsomeasured in dollars. An analyst may compare thedollars in sales to the cost of making those sales andbegin to evaluate the corporation’s performance.

However, while the cost of government activitiescan be measured in dollars, the output of govern-ment programs must usually be measured byother means.• How many students were educated• How many tests of water quality were completed• How many mentally ill patients were evaluated

Adding more complexity, the outputs are usuallynot the end in themselves, but a means of solvingother problems. For instance, we test water qualityso we can better monitor and lessen the amount ofpollution in our water. We maintain roads so thatcitizens can travel to different places.

This does not mean that government cannot

5

compare the benefit of its programs with the costof those programs. It does mean that such com-parisons will be more difficult and require carefulthought and design.

As part of our research into how we couldimprove the value of government financial reports,we conducted an informal, non-scientific survey ofmembers of the press and subscribers to Perspec-

tive, OCPA’s monthly publication. We asked if theycurrently made use of the state’s annual auditedfinancial statements and/or the performancemeasures in the budget book submitted to thelegislature.

Forty-three people responded to our survey, ofwhom fewer than 10 owned up to actually usingeither the financial statements or the budget bookdirectly. We also asked aboutareas where they might liketo see additional perfor-mance information.

While additional informa-tion concerning education,roads, and child welfarewas most prevalent, whatcame across to me was aninherent mistrust of govern-ment on the part of many ofthe respondents. Severalcame right out and said they didn’t trust what theyread in official reports.

This response points to a need for auditedfinancial statements that provide information tothe public in ways it can interpret for itself. Thesurvey was not scientific and was only conductedto glean some suggestions for performance mea-sures, but the clear message of those who re-sponded to our informal survey was to providebetter, more transparent information that has beensubjected to an independent audit.

The government should consistently report on atimely basis. Public companies must publish theirfinancial statements within three months of the endof their fiscal year. Few governments currentlyreport so promptly. With the helpful prodding of theGovernment Finance Officers Association, manygovernments now report their results within sixmonths of the end of the year, although the federalgovernment will allow up to 13 months beforeconsidering any adverse action toward its grantees.

Most state governments are no more financiallycomplicated than major corporations. In fact, theyare usually less so, owing to the foreign operations

and transactions that often complicate evenroutine corporate reporting and the dearth amongcorporations of the privilege resulting from sover-eignty that governments enjoy. It should be easier

to prepare a set of financial statements for a stategovernment than for a major corporation. Thepermitted limit of time for publication of a state’sfinancial statements should be no more than 90days after the end of the year.

We should also note that one very bright spot inthis regard is the U.S. Government. The ActingComptroller General signed the Auditor’s Reporton the accrual basis consolidated financialstatements for the year ended September 30,2009, on December 9, 2009. Unfortunately, lest Iencourage more sanguinity than is merited, I

should divulge that theletter included a dis-claimer of opinion on thefinancial statements andan adverse opinion oninternal control.2 But, atleast the sobering reportwas prompt!

Of course the financialstatements should bereadily disseminatedthrough government

websites. However, just as in the private sector,where the financial press acts as an intermediarybetween corporations and the investing public, weshould recognize the role the press plays in analyz-ing information, organizing it, and presenting it sothat we can make informed decisions withoutwading through all the minutiae of official reports.

Like many Americans, I personally follow thestock market and manage a small personalportfolio of investments. Each company in which Iinvest sends me an annual report. I have neverread an entire annual report. I usually do little morethan glance at it, yet I consider myself sufficientlyinformed to make my own investment decisions.

How? I rely on intermediaries to read thereports and summarize them in ways that enableme to act intelligently. I read both the local and anational newspaper regularly. I take advantage ofservices my brokers make available to me, and Ialso subscribe to an independent service thatanalyzes investment opportunities.

We should encourage the development ofsimilar institutions for government. We alreadyhave those institutions, but what we need is better,

Our system of accounting and

financial reporting used in

Oklahoma and at the federal level

is designed as if to hold appointed

officials responsible to elected

officials. We should be holding the

elected officials responsible to

voters and taxpayers.

6

more organized information for their analysis.Currently, the information with which the pressmust work comes mostly from ad hoc sources andis often unaudited. The information available tobusiness journalists is superior in helping thebusiness press inform its readers. Governmentneeds to catch up.

Experience elsewhere

This paper has sought to draw parallels be-tween the American system of government and asystem of reporting that combines consolidatedaccrual accounting with relevant performancemeasures. The proposals put forward represent asubstantial departure from the status quo.

However, some governments have taken tenta-tive steps toward a reporting system by which theywould hold themselves more accountable to theircitizens. Ironically, most progress seems to betaking place outside the United States. In Novem-ber 2008 the International Federation of Accoun-tants (IFAC) published an information paper,“Developments in Performance MeasurementStructures in Public Sector Entities,” that reportedon an international survey of the use of performancemeasurement, both financial and non-financial, andrelated issues in government reporting.

Only 23 of the IFAC’s 250 respondents werebased in the United States, and, in many in-stances, the responses of the Americans surveyeddiffered significantly from those based elsewhere.After reviewing the IFAC survey, it is difficult not toconclude that other countries lead the UnitedStates in the introduction of relevant performancemeasures.

While a thorough worldwide survey of reportingpractices is outside the scope of this project, theIFAC study is very helpful in shedding light on theprogress being made elsewhere in improvinggovernment reporting practices. The IFAC re-ported that its survey “responses centered on thesame themes and respondents seemed to agreethat it is the combination (emphasis in the origi-nal) of financial and non-financial measurementthat shows the performance of the public sectorentity in a broader perspective.”3

The IFAC study surveyed government account-ing officials, or “insiders,” while this paper isprimarily concerned with how to improve report-ing to those outside the government. However,many of the conclusions drawn in the IFAC studyare consistent with the themes expressed here,

including the advantages of well-designed perfor-mance measures, accrual accounting and bud-geting, and independent audits.

It is also worth noting that while this paper hasbeen written from a limited-government, free-market perspective, the benefits of this approachdo not all go to fellow conservatives. The enemyof this approach is not likely to be the liberalcamp, as many in that camp are very seriousabout using government to achieve desirablesocial ends.

Those who would have the most to fear fromthis approach would be those special interestsseeking to use the budget process to acquirespecial favors at the expense of the generalpublic. If their goal is not really to provide superiorservice but to profit from providing services to theprogram, the approach to financial reportingpresented here will make life more difficult for them.

The financial statements, now coupled withperformance data, will remind the public why wehave the program and give them an idea of howwell it is doing. Programs that are ineffective orinefficient are likely to see significant reform if notoutright termination. Those whose main interest isnot in getting results but in selling things to thegovernment at a profit will find that they musteither improve performance or suffer loss.

At the same time, liberals interested in usinggovernment as a tool for social improvements willfind a rich source of data to advocate for expan-sion of things that are working and spendingpublic resources effectively. Of course, manyliberals are no more interested in protectingspecial interests than are most conservatives, asthey also see those special interests as a drain onresources that could be put to more productive use.

What should the report look like?

While it is one thing to outline the principlesthat should govern accounting and financialreporting in government, it is yet another tooutline a workable design for the actual format ofthe statements themselves. While the principlesthat underlie our system of government may bestraightforward, the government itself is extremelycomplex, even at the state level.

An earlier paper, “Enhanced Financial Report-ing for State Government,” upon which this paperattempts to build, examined the superiority ofcost-focused accounting and reporting andoutlined a basic structure for financial statements.

As discussed in the previous paper, governmentsneed to report the results of their activities andcompare those results to the cost of delivering theservices in order to give the public a picture of itsoperations.

With each program, the government shoulddefine what the program is trying to accomplish,provide a measure of its progress toward thatgoal, and explain how the program attempts toaccomplish the goal. A measure of programoutput should accompany this explanation.

Two stages may be discerned in trying toachieve a public goal. First, the government mustidentify a program or course of action that itthinks will accomplish the goal, and second, itmust implement its program efficiently and effec-tively enough to have thedesired impact.

In other words, the pro-gram may fail to achieve thedesired goal for two rea-sons. First, it may fail toadminister its program in amanner that is effective orefficient, and second, a well-run program that is inher-ently unable to achieve thedesired outcome will alsofall short of the desired goal. This requires thegovernment to measure both outputs (what theprogram produces) and outcomes (the changes inthe social or economic indicator where change isdesired).

For instance, a state may want to reduce thenumber of traffic fatalities on its highways. In aneffort to realize this desired outcome, it mayorganize and fund a highway patrol to enforcelaws related to traffic safety and assist motoristsin need. If a well-run highway patrol is an effec-tive means of reducing traffic accidents and thestate administers an effective highway patrol, thestate’s citizens should be safer when travelingstate roads.

Conversely, if the presence of a highway patrolhas only a small impact on traffic fatality rates,we would have an ineffective program. At the sametime, if the highway patrol, while potentially effectiveat curbing accidents, failed to realize its potentialbecause of ineffective management, poorly trainedpersonnel, or counterproductive internal practices,we would not see the desired outcome.

Of course, a failure to adequately fund a

program would deprive that program of the abilityto achieve its potential impact. However, even withinsufficient funding, we would expect to see atleast some progress toward the desired goal.

“Enhanced Financial Reporting for StateGovernment” elaborated some of the reasons whyaccounting and financial reporting in governmentshould focus upon cost rather than budgetarycompliance. A focus on cost will tell us what wegive up for government programs. However, wealso need to measure results in order to tell uswhat we are getting in return for the expense weultimately bear.

There is also evidence that the use of well-designed performance measures can help keepprogram administrators directed toward their

goals with fewer politicalor extraneous distractionsthat impede progress. TheIFAC survey found that“respondents from publicsector entities with non-financial performanceobjectives are significantlymore satisfied … thanthose without non-finan-cial performance objec-tives.”4

At a minimum, our elected officials should tellus exactly what they are attempting to accomplishwith the resources we make available to them. Wealso have a right to some objective measure ofhow well they are doing and at what cost.

The elected officials should set the performancemeasures. As part of the appropriation process,the elected officials should tell the appointedofficials what they expect the program managersto accomplish with the resources being provided.

At present, relatively few governments makesystematic use of performance measures as partof their financial reporting. Many of the perfor-mance measures that are used are developed bythose administering the programs and measureprogram inputs. Most of those inputs are directlyor indirectly related to inputs or financial re-sources made available. Most of this informationis irrelevant for our purposes.

If a program is underfunded, it will have diffi-culty meeting its goals. If it is meeting its goals,we should question whether it is reallyunderfunded. After all, is our goal to simply spendmoney or to accomplish something with what we

7

Improved accounting and

financial-reporting practices

can improve the quality of

government services,

lowering their cost with both

immediate and long-term

positive impacts.

spend? Most citizens want accomplishments, andthat is where our financial reporting shouldconcentrate.

One of the best performance reports availableat the state level is prepared by the OklahomaHealth Care Authority.5 Since the Medicaidprogram that the Authority delivers is probablythe most complex in state government, it does notlend itself to a concise explanation. However, thereport is an excellent step toward better account-ability.

As a result of the analysis summarized in thispaper, I am proposing a multi-level system ofreporting. The top level would relate government-wide information while the bottom level wouldrelate individual transactions. The followingchart shows the relation-ship of the different levels,which will be further ex-plained in the followingsections of this paper.

Level I: Government-wide

financial statements

Governmental account-ing has long used a pyra-mid (or at least a truncatedpyramid) to illustratefinancial reporting. Itcontains broadly presentedgovernment-wide information at the top withmore specific information as we move down. Inour illustration, reprinted from “Enhanced Finan-cial Reporting for State Government,” we seehigh-level data for the entire government, pre-senting its financial position and spendingpriorities.

The presentation is made on the full accrualbasis so that the cost of government services isemphasized rather than budgetary compliance.The use of accrual accounting has the addedadvantage of making it more difficult for schem-ing officials to start or build programs for whichthey may presently take credit without having tofully disclose the real long-term cost of what theyare doing.

The reader is referred to the earlier report formore detail, but the idea is to provide a summary

of all assets created or acquired and liabilitiesincurred on behalf of the taxpayers. Of course,any liabilities incurred in exchange for services oractions to benefit the state results in a charge toexpense as well as a liability. Legislators maycontinue to vote for increased pension benefitsand fail to fund them. However, those legislatorswill have to incur an estimate of the liability towhich they obligate their constituents.

Conversely, elected officials who by theiractions create assets for future use, such asroads, classrooms, or dams, will incur only theportion of the cost attributable to the servicesprovided during their term of office. Future offi-cials who do not want to continue incurring thecost of the services may always discontinue the

service and dispose of theassets. If the assets arecarried at the lower ofcost or market value,which is proper, they willnot incur a loss in doingso except for terminationexpense.

The Statement ofActivities will disclose thecost of various functionscarried out by the state.While the government-wide report is not specific

enough to gauge the cost of most programs, itdoes present a clear picture of where the electedofficials are placing priority.

The government-wide financial statements mayalso include a statement of cash flows or changesin financial position and a separate statement ofreconciliation between the expenses shown onthe statement of activities and the legallyadopted budget.

The government should also include appropri-ate notes to the financial statements, providingexplanations of amounts carried on the face ofthe financial statements and disclosing contin-gencies, unusual risks, and other importantinformation about the government’s activities. Anillustrative balance sheet, statement of activities,and notes to the financial statements are shownon pages 10-17.

8

The use of accrual accounting

has the added advantage of

making it more difficult for

scheming officials to start to

build programs without fully

disclosing the long-term cost

of what they are doing.

$5,110,404,000

Education

$2,562,831,000

Health andWelfare

$1,045,707,000

PublicSafety

$176,161,000

Transportation

($53,107,000)

PublicInsurance

($90,866,000)

PublicUtilities

$172,903,000

Assis. to LocalGovernments

$376,689,000

Cost of Inc. Pen.Ben. to Former

Employees

$93,604,000

EconomicDevelopment

$103,237,000

Regulation

$88,517,000

GeneralGovernment

$103,147,000

Natural andCultural

Total Liabilitiesand Equity

$52,838,908

LEVEL I: Provides picture of financial position and overall costs of entire government

LEVEL II: Transition from Level I to Level III

LEVEL III:Focus is on individual programs and includes performance data:• objectives with measurements of outputs• goals with measurements of oucomes

Notes to statements would cover:• sales (descriptions of items sold, pricing and terms, including special exclusions)• grants and contributions (grantor, amount likelihood of renewal, terms and conditions)• capital assets employed and related deprecitation• estimates of deferred maintenance

LEVEL IV: Individual transactions

9

10

A W O R D A B O U T T H E I L L U S T R A T I V E F I N A N C I A L S T A T E M E N T S

face of the statements, such as subsequent events.Most items covered by existing notes generally

included with state government financial state-ments would remain under a cost-focused sce-nario. As such, the notes that currently appear inOklahoma’s financial statements are referencedbut not further addressed. However, there areadditional disclosures that should be consideredunder the approach outlined in this project. Theseadditional disclosures include a discussion of taxpreferences, sometimes called “tax expenditures,”where the government grants preferential taxtreatment. Additional disclosure may be helpfulwith regard to the government workforce as therecruitment and retention of qualified workers isoften more difficult in the government environment.

The notes to Oklahoma’s financial statementsare referenced below with explanations andexamples where changes from the existing contentare recommended. Existing GAAP may requirenotes that are excessively detailed beyond what isconstructive. However, a critique of this practice isbeyond the scope of this project.

This project focuses on the cost of governmentactivity. Elsewhere in this report, the merit ofincluding information about the value added bygovernment activity, often called “service, efforts,and accomplishments reporting,” is discussed.Including such information is beyond the scope ofthis project. However, financial statements that doinclude information about the value added bygovernment activity should include notes relatingto that information.

The illustrative financial statements that accom-pany this report are not prepared in accordance withgenerally accepted accounting principles thatcurrently apply to government. They are prepared toillustrate how generally accepted accountingprinciples in government can be more useful.

The amounts shown in the illustrative financialstatements are often taken from official statesources, including the state’s own comprehensiveannual financial report and its OpenBooks trans-parency website. Other data were acquired infor-mally from knowledgeable officials, and still otherdata presented were estimates prepared by meand the team that helped me complete this project.

The illustrative financial statements are shownonly for the purpose of discussion about financialreporting and may not fairly present the state’sfinancial position or results of operations. Thedata have not been audited or, in some cases,even independently verified and may containmaterial errors and omissions.

This project presents a new approach to finan-cial accounting for government. The project usesdata for the State of Oklahoma to prepare illustra-tive financial statements that focus on cost andaccountability of the elected government to itscitizens. The notes are an integral part of thefinancial statements. They explain the policiesused in the accounting process and provideimportant detail to aid the reader in understand-ing. The notes also provide important informationthat cannot be readily quantified, such as contin-gencies, or that would be inappropriate on the

11

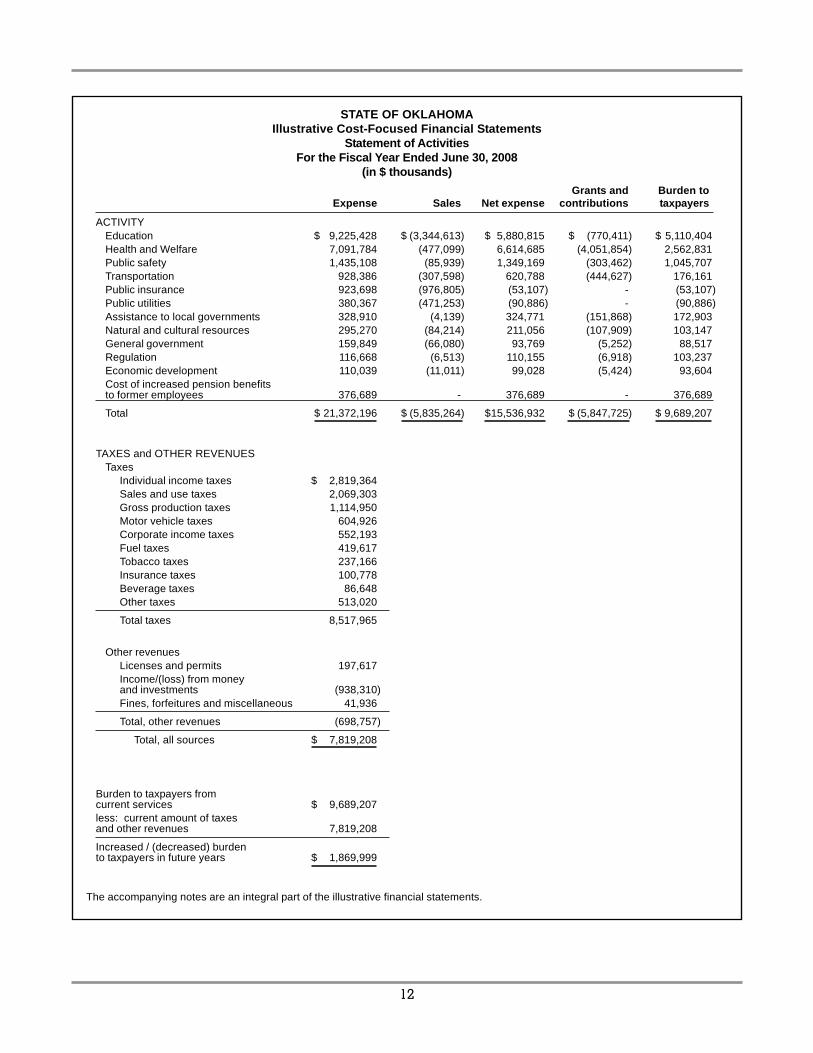

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Balance SheetJune 30, 2008

(in $ thousands)

ASSETS LIABILITIESCurrent assets Current liabilities

Cash and equivalents $ 6,134,672 Accounts payable and accrued liabilities $ 2,041,149Short-term investments 4,617,295 Current portion, long-term debt 514,813Accounts receivable 1,385,986 Current portion, pension liabilities 1,651,971Current portion, long-term receivables 92,108 Deferred revenue 778,025Inventory 121,092 Other current liabilities 267,923Pension assets 1,651,971 Total Current liabilities 5,253,881Other current assets 28,041Total Current assets 14,031,165 Noncurrent liabilities

Accrued liabilities not currently payable 799,911Noncurrent assets Capital lease obligations 174,273

Long-term investments 3,794,870 Long-term debt 7,033,369Long-term receivables 1,998,465 Pension liabilities 32,880,756Land 1,824,367 Liability for other post employment benefits 283,233Construction in progress 811,668 Deferred revenue 4,308,281Depreciable assets, net 10,760,363 Liability for assets held only as fiduciary 482,756Pension assets 18,706,963 Other noncurrent liabilities 507,134Assets held only as fiduciary 482,756 Total Noncurrent liabilities 46,469,713Other noncurrent assets 428,291

Total Noncurrent assets 38,807,743 Total liabilities 51,723,594

Total assets $52,838,908 EQUITYCitizen equity 1,115,314

Total liabilities and equity $52,838,908

The accompanying notes are an integral part of the illustrative financial statements.

I L L U S T R A T I V E G O V E R N M E N T - W I D E F I N A N C I A L S T A T E M E N T S

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of ActivitiesFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

ACTIVITYEducation $ 9,225,428 $ (3,344,613) $ 5,880,815 $ (770,411) $ 5,110,404Health and Welfare 7,091,784 (477,099) 6,614,685 (4,051,854) 2,562,831Public safety 1,435,108 (85,939) 1,349,169 (303,462) 1,045,707Transportation 928,386 (307,598) 620,788 (444,627) 176,161Public insurance 923,698 (976,805) (53,107) - (53,107)Public utilities 380,367 (471,253) (90,886) - (90,886)Assistance to local governments 328,910 (4,139) 324,771 (151,868) 172,903Natural and cultural resources 295,270 (84,214) 211,056 (107,909) 103,147General government 159,849 (66,080) 93,769 (5,252) 88,517Regulation 116,668 (6,513) 110,155 (6,918) 103,237Economic development 110,039 (11,011) 99,028 (5,424) 93,604Cost of increased pension benefitsto former employees 376,689 - 376,689 - 376,689

Total $ 21,372,196 $ (5,835,264) $15,536,932 $ (5,847,725) $ 9,689,207

TAXES and OTHER REVENUESTaxes

Individual income taxes $ 2,819,364Sales and use taxes 2,069,303Gross production taxes 1,114,950Motor vehicle taxes 604,926Corporate income taxes 552,193Fuel taxes 419,617Tobacco taxes 237,166Insurance taxes 100,778Beverage taxes 86,648Other taxes 513,020

Total taxes 8,517,965

Other revenuesLicenses and permits 197,617Income/(loss) from moneyand investments (938,310)Fines, forfeitures and miscellaneous 41,936

Total, other revenues (698,757)

Total, all sources $ 7,819,208

Burden to taxpayers fromcurrent services $ 9,689,207less: current amount of taxesand other revenues 7,819,208

Increased / (decreased) burdento taxpayers in future years $ 1,869,999

The accompanying notes are an integral part of the illustrative financial statements.

12

13

Note 1. Summary of Significant Accounting Policies

The illustrative financial statements includeseveral features that differ from existing GAAPpresentation. Most of these differences are relatedto entity definition, measurement focus, matching,intergenerational equity, and symmetry in society.

Entity definition—The illustrative financialstatements include all activities under the direc-tion, either directly or indirectly, of officials electedby the voters of Oklahoma. This includes allactivities where a board is appointed by stateelected officials or by others appointed by thoseofficials. Consistent with the fact that the state is apolitical unit accountable to its citizens, thefinancial statements report on all activity con-ducted by that unit on behalf of those who electedits decision makers.

As a result, the illustrative financial statementsdo not distinguish between general government,component units, or other relationships. If the dulyelected officials of the state can ultimately directthe operations of an agency, board, commission,or public trust, it is included as part of the illustra-tive financial statements.

Accordingly, the illustrative financial statementsrecognize indirect expenses incurred for thebenefit of other agencies as part of the expense ofproviding services through those agencies. Forinstance, in the illustrative financial statements,the cost of collecting taxes is allocated among allactivities financed by those taxes.

The illustrative financial statements alsoallocate other overhead costs among the activitiesmeant to benefit from those activities. Centralfiscal operations, personnel management, centralpurchasing, and other general managementfunctions are allocated to activities based uponappropriate criteria, such as expenditures, appro-priations, or number of personnel. This policy ismaintained even though the purpose may be toprevent misappropriation or abuse rather thanbenefit the activity charged directly.

The illustrative financial statements alsodistinguish between transfers that are truly apayment from one agency to another and trans-fers that are made on behalf of third parties. Forinstance, the Oklahoma State and EducationEmployees Group Insurance Board (OSEEGIB) isa state agency that provides insurance benefits tostate and county employees and teachers. How-

ever, state employees are not automaticallyenrolled in OSEEGIB. Rather, OSEEGIB mustcompete with several private sector providers forthe business of those it serves. The State offers itsemployees a choice between OSEEGIB and itscompetitors and withholds the cost of premiumsfrom its employees’ pay and benefit allowances. Itthen transfers the funds withheld to the providersas chosen by its employees.

When the transfer is made from the State toOSEEGIB, it is treated as an arm’s length transac-tion rather than a transfer. The State has compen-sated its employees. Separately, the State, throughOSEEGIB, has sold insurance to its employees.The transfer to OSEEGIB is treated as revenue tothe State, specifically a charge for service.

Special considerations arise when more thanone level of government funds, manages, ordelivers a service. The illustrative financial state-ments report the cost of programs primarilymanaged and delivered by the State of Okla-homa as a state activity. Funds provided by thefederal government for state activities are in-cluded in grants and contributions. Funds theState provides to local governments for servicesprimarily managed and delivered by local gov-ernment are reported as assistance to localgovernments.

The factors considered in determining whichlevel of government primarily manages anddelivers a service include which level of govern-ment is responsible for:• determining the extent of program coverage• determining eligibility to participate by estab-

lishing rules for participation• determining eligibility to participate by apply-

ing the rules to individual situations• determining the type and level of benefits

delivered• employing workers and/or contractors to

deliver services includingo establishing criteria for employees and

contractorso establishing rules that govern the firing of

employees and retaining of contractorso selecting individual employees and contractorso supervising employees and contractorsCommon schools are funded primarily by the

State of Oklahoma, although federal assistanceand local taxes are also important sources. Voters

N O T E S T O T H E I L L U S T R A T I V E C O S T- F O C U S E D F I N A N C I A L S T A T E M E N T S

14

elect local school boards, but important decisionsabout who is to be educated, the amount ofeducation services provided, the overall curricu-lum, and qualifications for teachers are made bythe State of Oklahoma apart from local schooldistricts. Accordingly, Oklahoma’s common schoolsare treated as a state function, although the finan-cial statements do not include local tax revenues.

Similarly, the activities of the Department ofCareer Technology and Education, the OklahomaConservation Commission, and the District Attor-neys Council are treated as state functions,although local districts make many decisions andprovide important funding. In all cases, thepurpose, scope, and rules are determined at thestate level, although locally accountable officialsimplement the decisions made at the state level.The illustrative financial statements do not in-clude funds provided by local sources.

However, other county activities are not treatedas state functions because the locally electedcounty officials exercise more decision-makingcontrol. However, the State provides major fund-ing for many county activities. The illustrativefinancial statements report this financing underassistance to local governments. The major areasof assistance reported include funding for countyhealth departments and county roads and bridges.

In addition, the State manages pension sys-tems for firefighters and police officers. Almost allparticipants in both systems are local governmentemployees. However, while both employees andemployers contribute to the pension plans, theState underwrites the benefits, establishes therules of participation, and sets the benefit deter-mination formulas. Increases in the unfundedliability of the systems are treated as an expenseof the state, while declines in the unfunded liabil-ity (or gains in surplus funding) are treated asrevenue to the state.

Another area of consideration is communitydevelopment. The largest program, the Commu-nity Development Block Grant, is a federallyfunded pass-through intended to spur localeconomic growth. The federal assistance isincluded in grants and contributions, while thegrants to local governments are included inassistance to local governments. However, com-munity development also includes funds appropri-ated by the state for sub-state planning districts.

There are many other instances in which astate agency will provide funds or services to a

local government on an ad hoc basis or where thelevel of funding is not significant. These situationsare all treated as an expense related to a stateactivity, although a local government may exer-cise considerable control over the managementand delivery of the ultimate service. Examples ofsuch situations are found as part of the Office ofJuvenile Affairs, the Oklahoma State Bureau ofInvestigation, the Arts Council, the Water Re-sources Board, the Department of Libraries, andmany other agencies.

Measurement focus—The illustrative financialstatements are presented using the economicresources measurement focus and the accrualbasis of accounting. Consistent with the principlesthat follow, revenue is recognized when earnedand expenses are recorded when a liability isincurred, regardless of the timing of related cashflows. Similarly, grants and similar items are recog-nized as revenue as soon as the State has met alleligibility requirements imposed by the provider.

Under existing GAAP, financial statementsprepared at the government-wide level are pre-pared using the accrual basis of accounting anda measurement focus on economic resources.However, existing GAAP use a modified accrualbasis of accounting and a measurement focus oncurrent financial resources in all general govern-ment statements below the entity level. Theillustrative financial statements make no suchdistinction. The illustrative financial statementsapply the measurement focus consistently, fromthe entity-wide financial statements to the moredetailed activity-level statements.

The illustrative financial statements also refinethe measurement focus by recognizing a liabilityto the State when others have taken action ingood faith with a reasonable expectation ofreceiving a future benefit. Therefore, when theState, in an effort to achieve a public goal, offersto pay the college tuition of high school studentswho meet certain requirements, such as taking amore rigorous set of classes than would otherwisebe required, the illustrative financial statementsrecognize a liability when students and theirparents, in good faith, sign up for the programand begin complying with its requirements. Theliability is adjusted to the extent the students areexpected to complete those requirements.

Similarly, the State also recognizes the presentvalue of pension and other post-employmentbenefits as a liability at the time they are earned

15

by state employees. This is discussed in moredetail below, under intergenerational equity.

Matching principle—The matching principle isbasic to accounting and financial reporting. Asgenerally applied in the private sector, the match-ing principle means expenses are recognizedwhen the revenue to which the expenses give isrecognized. Thus, expenses are matched torevenue and the financial statements give aclearer picture of the profitability.

However, government is not in business tomake a profit, but to provide services for thepublic good. Rather than incurring expenses toproduce revenue and profit, the governmentcollects taxes and other revenues in order to fundits services. Whereas in the private sector, thedesire for revenue drives the need for expense, ingovernment, the desire to provide services drivesthe need for revenue.

The matching principle is relevant in govern-ment. However, rather than matching expense torevenue, the illustrative financial statementsmatch revenue to expense. For example, when thefederal government provides funds for capitalimprovements such as roads, the State wouldgenerally record revenue when it has met all theeligibility requirements of the grant. This wouldusually mean building a road in compliance withthe terms of the federal assistance.

However, the road, a capital asset, will provideservice to the public over many years. In theillustrative financial statements, the State recog-nizes the expense of providing that service throughdepreciation. Accordingly, the illustrative financialstatements defer revenue from federal grants thathelp pay for road and bridge construction andrecognize it over the same period that the expenseof providing the public service is recognized.

The application of the matching principle isfurther refined by two additional principles:symmetry in society and intergenerational equity.

Symmetry in society—In the private sector,when a transaction occurs between two parties,each party will usually make correspondingaccounting entries at the same time. For instance,if X sells to Y on credit, X will record a receivableand Y will record a payable at the time the sale isexecuted. The illustrative financial statementsapply this same principle to the State’s financialstatements.

When an individual or business earns incomethat is subject to income tax, the illustrative

financial statements recognize revenue to theState. The taxpayer would recognize an expenseand a liability for any tax due at the time incomeis earned. Accordingly, the State recognizesrevenue and a receivable at the same time,regardless of when the tax is paid or due. Simi-larly, sales taxes are recognized when salessubject to the tax are made, and gross productiontaxes are recognized when oil or gas is produced.

Intergenerational equity—Intergenerationalequity measures the extent to which public offi-cials have postponed or accelerated the incidenceof cost related to program benefits. To the extentpracticable, the illustrative financial statementscharge the cost of actions taken by current offi-cials to the current time period. For instance, thepresent value of the cost of added pension orother post-employment benefits related to servicesalready performed is recognized when thosebenefits are voted in by the legislature rather thanbeing amortized over some future period.

Note 2. Deposits and Investments

No significant change is contemplated exceptthat the effect of securities lending agreements isnot displayed on the balance sheet. The notedisclosures would remain as at present.

Note 3. Receivables

The State has amounts due from numeroussources: taxpayers, the federal government, andthose purchasing state services, etc. No change iscontemplated except that income earned bytaxpayers that is subject to state income tax resultsin the State recognizing a receivable for taxrevenue at the time the taxpayer earns the income.

Note 4. Interfund Accounts and Transfers

Interfund transactions and balances, includingthose between what is currently referred to as theprimary government and component units, areeliminated. This is consistent with private sectorconsolidated reporting.

Note 5. Capital Assets

No significant change is contemplated. How-ever, one issue raised but not resolved by thisproject is the reporting of replacement cost ofcapital assets in use.

Note 6. Risk Management and Insurance

No significant change is contemplated.

16

Note 7. Operating Lease Commitments

No significant change is contemplated.

Note 8. Lessor Agreements

No significant change is contemplated. How-ever, lease agreements between different agen-cies of the State of Oklahoma are consolidated.

Note 9. Long-Term Obligations

Oklahoma’s Promise—The State Regents forHigher Education promote and administer aprogram to assist students from families withincome below $50,000 to attend college in Okla-homa. To remain eligible, the student’s familyincome cannot exceed $100,000 in the year thestudent enters college. To participate, a studentmust apply before his or her final two years ofhigh school. The student’s parent(s), custodian(s),or guardian(s) must agree to help the studentmeet the program’s requirements. The studentmust take a more rigorous curriculum than isgenerally necessary to graduate from high schoolaccording to the following schedule of requiredcourses:

4 years of English3 years of lab science3 years of mathematics3 years of history and citizenship skills2 years of foreign language or 2 years ofcomputer technology1 year additional of any of the above1 year of fine arts or speech

In addition, the student must maintain a 2.5GPA in the required courses and a cumulative 2.5GPA for high school, abstain from abusing drugsand alcohol, abstain from criminal activity, andmeet certain other requirements.

For a student who successfully completes theprogram, the State will pay the student’s collegetuition according to schedules published by theRegents for Higher Education. The programcovers only tuition and does not cover books,room and board, activities, and special fees.Students are encouraged to apply for otherfinancial aid for assistance with these other costs.

The statutes provide a mechanism to reducethe number of awards in the event that funding isinsufficient to cover anticipated costs. However,this provision is not widely discussed inOklahoma’s Promise promotional literature. Sincestudents must complete actions that they mightnot in the absence of Oklahoma’s Promise, the

very name of the program indicates the State hasobligated itself to fund the scholarships and hastherefore incurred a liability.

Approximately 28,500 Oklahoma high schoolstudents are enrolled in the Oklahoma’s Promiseprogram. The State projects the cost of tuition forthe program for the current year to be $54 million.The liability for future tuition payments for highschool students enrolled in the program and forcollege students in the program for whom addi-tional tuition payments beyond the current yearwill be made is estimated to be $313.8 million.

No other significant change is contemplatedexcept that the illustrative financial statementswould not distinguish between the obligationsrelated to governmental activities, business-typeactivities, or component units.

Note 10. Restatements of Balances

No significant change is contemplated.

Note 11. Nonrecourse Debt and Debt Guarantees

No significant change is contemplated.

Note 12. Retirement and Pension Systems

No significant change is contemplated in thenotes, but the full extent of the present value ofpension assets and pension liabilities is reportedon the balance sheet.

Note 13. Other Postemployment Benefits

No significant change is contemplated in thenotes, but the full extent of the present value ofother postemployment benefits is reported on thebalance sheet. The State does not maintainassets to offset this liability.

Note 14. On-Behalf Payments

No significant change is contemplated.

Note 15. Tax Preferences

The State levies taxes to finance many of itsactivities. As part of its system of taxation, theState grants certain tax preferences includingexemptions, credits, exclusions, deferrals, prefer-ential rates, and other provisions. In alternateyears, the Oklahoma Tax Commission attempts toestimate the amount of revenue the State wouldhave collected but for the existence of the taxpreference. The tax preferences with the largestestimated impacts on revenue as calculated bythe Oklahoma Tax Commission are listed below.

17

Preference (in $ thousands) Amount

Sales tax on sales of items used in the manufacturing process ...................................................... $1,623,110

Sales of items for the purpose of resale .............................................................................................. $1,493,000

Use of itemized and standard deductions on individual income tax ................................................. $685,506

Use of personal exemption on individual income tax .......................................................................... $137,911

Sales tax on sales to counties, municipalities, and other local governments .................................. $104,750

Sales tax on utilities for residential use ................................................................................................... $99,592

Cigarette tax on sales to Indian tribes that have compacted with the State ...................................... $96,648

Sales tax on sales to the State of Oklahoma .......................................................................................... $85,105

Motor vehicle excise tax on used motor vehicles held for sale by dealers ......................................... $70,726

Sales tax on sales of livestock, agricultural products,and certain items used in agricultural production ................................................................................. $63,905

Prorated motor vehicle excise tax on registered trucks and trailers .................................................... $63,516

Tax on sales of prescription drugs and similar items ............................................................................ $60,967

Rebate of 6/7 of gross production tax paid on oil and gas produced fromdeep wells, horizontally drilled wells, and other special wells ............................................................ $57,000

Exclusion from income tax for up to $7,500 of most government retirementand Social Security benefits ...................................................................................................................... $50,215

Use tax on livestock brought into Oklahoma for eventual sale ............................................................ $48,049

Sales tax on advertising ............................................................................................................................. $46,794

Use tax on property to be used by airlines or railroads ........................................................................ $45,706

Credit for sales tax paid by individuals with gross income of less than

$20,000 or families with less than $50,000 ............................................................................................. $37,813

Credit for income tax paid to another state on personal services income .......................................... $33,321

Income tax credit equal to 5 percent of federal earned income tax credit .......................................... $30,243

Nonrefundable income tax credit for an investment in depreciable propertyor to increase in employment .................................................................................................................... $28,680

Sales tax on food purchased with food stamps ...................................................................................... $20,731

Other tax preferences may not be includedbecause the Oklahoma Tax Commission does notcalculate an estimate of the revenue impact orhas determined that a meaningful estimatedcannot be made. The Tax Expenditures Report isprepared by the Tax Policy Division of the Okla-homa Tax Commission and is available from theCommission.

Note 16. Commitments

No significant change is contemplated.

Note 17. Litigation and Contingencies

No significant change is contemplated.

Note 18. Workforce Resources and Qualifications

Most State agencies are required to hire newemployees through the Merit System, a central

personnel system, and comply with Merit Systemrules in the management, promotion, and termi-nation of its employees. At June 30, 2007, agenciesrequired to operate under the Merit System had32,532 employees, of which 27,098 were in classi-fied Merit System positions. Other state agenciesemployed 4,379 individuals. In addition,Oklahoma’s system of higher education operatesoutside Merit System regulations.

For the year ended June 30, 2007, the Stateexperienced employee turnover of 13.2 percent.For the ten-year period ended June 30, 2007,employee turnover ranged between 11.7 percentand 14.2 percent.

Note 19. Subsequent Events

No significant change is contemplated.

18

Level II: Statements of activities by program

grouping

This level of statement provides additionaldetail not found on the government-wide finan-cial statements. However, for most programs inmost states, there is too much complex activity toattempt to link the amounts for program costswith the government-wide statements. Accord-ingly, we have made this level of reporting toserve as a bridge between the government-widefinancial statements and program-specificstatements.

While this paper is written to address issuesfacing state governments, the format shown canbe followed by any type of government. For asmall government, such as a small municipalityor single-purpose government such as a schoolor water district, it might be appropriate to elimi-nate this level of financial statement altogether.

The purpose is to provide a bridge from thegovernment-wide financial statements to theprogram-level financial statements. When such abridge is not helpful or necessary, it should notbe used.

Conversely, while small or single-purposegovernments may not need this intermediatestage, a truly large government, such as thefederal government, may find it advantageous touse more than a single level of reporting to link

the programs with the entire government. Flexibil-ity in this regard is encouraged.

From funds to programs

Financial reporting in government has tradi-tionally revolved around funds. A governmentalfund accounts for all sources of funds with similarrestrictions. The general fund represents re-sources which can be used for any purpose. Whilegovernment is no longer tied as closely to the useof a myriad of funds in its financial statements aspreviously, it may still use special revenue fundsto account for all revenue that can only be usedfor specific purposes.

Repeated discussions with interested citizenshave found relatively little public interest in theactivity of a particular fund or group of funds.However, there is interest in the financial activitiesof programs. GAAP has moved away from rigidadherence to a fund structure in recent years.However, current financial reporting stops short ofreporting on programs.

A goal of this paper is to demonstrate thatreporting by program is possible and even desir-able. However, in large governments with manyvaried programs, an intermediate statement thatlinks the programs with the entire governmentmay be helpful. Illustrative statements of activitiesfor program groupings follow.

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for EducationFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

Elementary and secondary education $ 5,069,833 $ (112,890) $ 4,956,943 $ (599,803) $ 4,357,140Higher education 3,793,083 (3,165,217) 627,866 (141,351) 486,515Vocational education 270,965 (5,160) 265,805 (18,328) 247,477Oklahoma Student Loan Authority 67,045 (60,391) 6,654 - 6,654School for the Deaf 9,481 (59) 9,422 (6,307) 3,115School for the Blind 6,479 (41) 6,438 (4,310) 2,128Other education 8,542 (855) 7,687 (312) 7,375

Total Education $ 9,225,428 $ (3,344,613) $ 5,880,815 $ (770,411) $ 5,110,404

The accompanying notes are an integral part of the illustrative financial statements.

I L LU S T R AT I V E S TAT E M E N T S O F A C T I V I T I E S F O R E A C H A C T I V I T Y G R O U P I N G

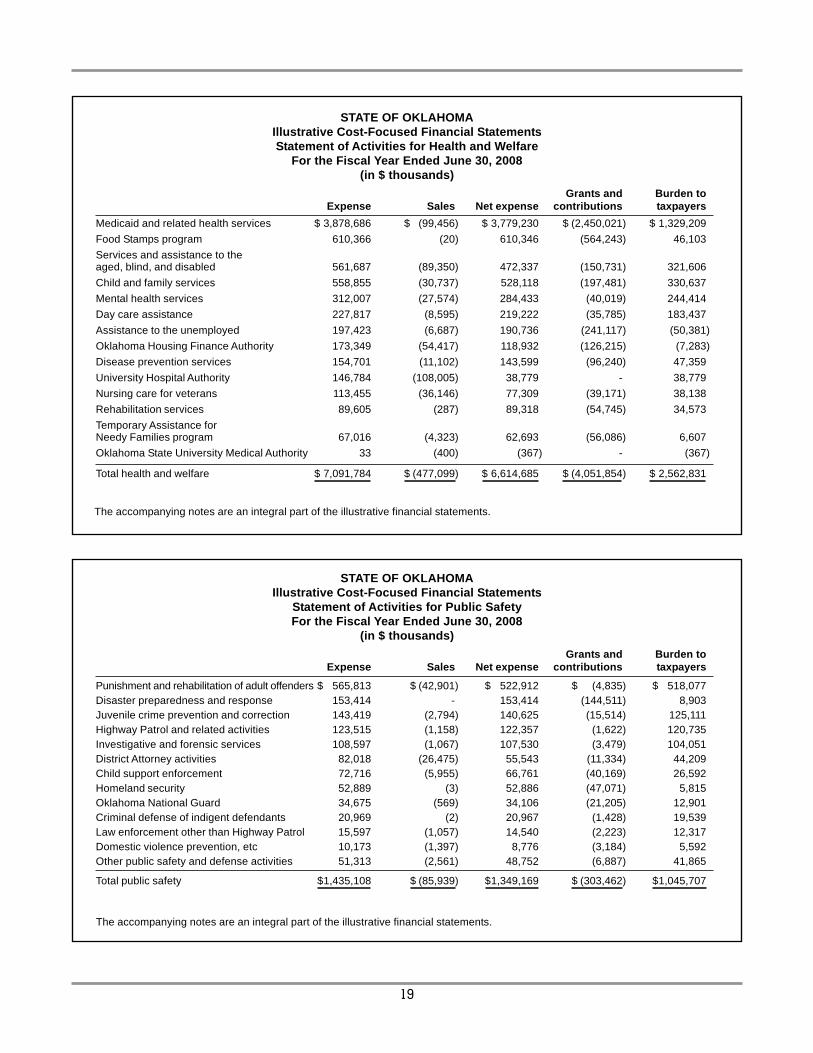

STATE OF OKLAHOMAIllustrative Cost-Focused Financial StatementsStatement of Activities for Health and Welfare

For the Fiscal Year Ended June 30, 2008(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

Medicaid and related health services $ 3,878,686 $ (99,456) $ 3,779,230 $ (2,450,021) $ 1,329,209

Food Stamps program 610,366 (20) 610,346 (564,243) 46,103

Services and assistance to theaged, blind, and disabled 561,687 (89,350) 472,337 (150,731) 321,606

Child and family services 558,855 (30,737) 528,118 (197,481) 330,637

Mental health services 312,007 (27,574) 284,433 (40,019) 244,414

Day care assistance 227,817 (8,595) 219,222 (35,785) 183,437

Assistance to the unemployed 197,423 (6,687) 190,736 (241,117) (50,381)

Oklahoma Housing Finance Authority 173,349 (54,417) 118,932 (126,215) (7,283)

Disease prevention services 154,701 (11,102) 143,599 (96,240) 47,359

University Hospital Authority 146,784 (108,005) 38,779 - 38,779

Nursing care for veterans 113,455 (36,146) 77,309 (39,171) 38,138

Rehabilitation services 89,605 (287) 89,318 (54,745) 34,573

Temporary Assistance forNeedy Families program 67,016 (4,323) 62,693 (56,086) 6,607

Oklahoma State University Medical Authority 33 (400) (367) - (367)

Total health and welfare $ 7,091,784 $ (477,099) $ 6,614,685 $ (4,051,854) $ 2,562,831

The accompanying notes are an integral part of the illustrative financial statements.

19

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for Public SafetyFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

Punishment and rehabilitation of adult offenders $ 565,813 $ (42,901) $ 522,912 $ (4,835) $ 518,077Disaster preparedness and response 153,414 - 153,414 (144,511) 8,903Juvenile crime prevention and correction 143,419 (2,794) 140,625 (15,514) 125,111Highway Patrol and related activities 123,515 (1,158) 122,357 (1,622) 120,735Investigative and forensic services 108,597 (1,067) 107,530 (3,479) 104,051District Attorney activities 82,018 (26,475) 55,543 (11,334) 44,209Child support enforcement 72,716 (5,955) 66,761 (40,169) 26,592Homeland security 52,889 (3) 52,886 (47,071) 5,815Oklahoma National Guard 34,675 (569) 34,106 (21,205) 12,901Criminal defense of indigent defendants 20,969 (2) 20,967 (1,428) 19,539Law enforcement other than Highway Patrol 15,597 (1,057) 14,540 (2,223) 12,317Domestic violence prevention, etc 10,173 (1,397) 8,776 (3,184) 5,592Other public safety and defense activities 51,313 (2,561) 48,752 (6,887) 41,865

Total public safety $1,435,108 $ (85,939) $1,349,169 $ (303,462) $1,045,707

The accompanying notes are an integral part of the illustrative financial statements.

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for Public UtilitiesFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

Grand River Dam Authority $ 224,542 $ (314,287) $ (89,745) $ - $ (89,745)Oklahoma Municipal Power Authority 155,825 (156,966) (1,141) - (1,141)

Total public utilities $ 380,367 $ (471,253) $ (90,886) $ - $ (90,886)

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for Public InsuranceFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

OSEEGIB* $ 590,831 $ (602,576) $ (11,745) $ - $ (11,745)CompSource 299,566 (347,019) (47,453) - (47,453)Health insurance high risk pool 25,337 (25,270) 67 - 67Multiple injury trust fund 7,964 (1,940) 6,024 - 6,024

Total public insurance $ 923,698 $ (976,805) $ (53,107) $ - $ (53,107)

The accompanying notes are an integral part of the illustrative financial statements.

* Oklahoma State and Education Employees Group Insurance Board

The accompanying notes are an integral part of the illustrative financial statements.

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for TransportationFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

State highways and turnpikes $ 912,293 $ (304,515) $ 607,778 $ (435,818) $ 171,960Railroads 10,457 (1,380) 9,077 (6,378) 2,699Aeronautics 3,377 (1,414) 1,963 (1,093) 870Waterways 2,259 (289) 1,970 (1,338) 632

Total transportation $ 928,386 $ (307,598) $ 620,788 $ (444,627) $ 176,161

The accompanying notes are an integral part of the illustrative financial statements.

20

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for Assistance to Local GovernmentsFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

County health services $ 122,256 $ (3,890) $118,366 $ (78,066) $ 40,300Community development 100,259 (249) 100,010 (73,802) 26,208County roads and bridges 71,099 - 71,099 - 71,099Police and firefighter pension costs 35,296 - 35,296 - 35,296

Total assistance to local governments $ 328,910 $ (4,139) $324,771 $ (151,868) $172,903

The accompanying notes are an integral part of the illustrative financial statements.

21

STATE OF OKLAHOMAIllustrative Cost-Focused Financial StatementsStatement of Activities for General Government

For the Fiscal Year Ended June 30, 2008(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

Judiciary $ 107,564 $ (62,402) $ 45,162 $ (4,587) $ 40,575Legislature 35,754 (575) 35,179 (114) 35,065Elections 8,938 (27) 8,911 (10) 8,901Governor 3,507 (260) 3,247 - 3,247Other general government 4,086 (2,816) 1,270 (541) 729

Total general government $ 159,849 $ (66,080) $ 93,769 $ (5,252) $ 88,517

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for Natural and Cultural ResourcesFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

Operate state parks and golf courses $ 61,718 $ (26,821) $ 34,897 $ (2,967) $ 31,930Wildlife and fisheries activities 48,470 (4,912) 43,558 (24,002) 19,556Agriculture and food services 35,286 (4,593) 30,693 (4,633) 26,060Conservation of water resources 27,170 (37,374) (10,204) (14,232) (24,436)Conservation and reclamation services 24,392 (72) 24,320 (12,447) 11,873Okla Centennial Comm Fund 24,152 - 24,152 (21,701) 2,451Oklahoma history programs 21,878 (2,116) 19,762 (2,755) 17,007Forestry and fire fighting services 20,178 (3,102) 17,076 (4,731) 12,345Reclaim well sites 14,507 (538) 13,969 (17,434) (3,465)Public television 14,125 (4,289) 9,836 (2,485) 7,351Other natural and cultural resources activities 3,394 (397) 2,997 (522) 2,475

Total natural and cultural resources $ 295,270 $ (84,214) $ 211,056 $ (107,909) $ 103,147

The accompanying notes are an integral part of the illustrative financial statements.

The accompanying notes are an integral part of the illustrative financial statements.

STATE OF OKLAHOMAIllustrative Cost-Focused Financial StatementsStatement of Activities for Regulatory Activities

For the Fiscal Year Ended June 30, 2008(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

Regulation of businesses and professions $ 23,159 $ (1,242) $ 21,917 $ (355) $ 21,562Regulation of energy and environment 18,651 (695) 17,956 (1,725) 16,231Driver licensing 18,514 (2,545) 15,969 (185) 15,784Regulation of transportation 14,414 (715) 13,699 (784) 12,915Insurance regulation 11,495 (338) 11,157 (696) 10,461Workplace regulation 8,738 (41) 8,697 (1,609) 7,088Public utility regulation 5,840 (376) 5,464 (157) 5,307Regulation of retail fuel outlets 5,584 (40) 5,544 (1,407) 4,137Health services regulation 5,545 (324) 5,221 - 5,221Investment regulation 4,728 (197) 4,531 - 4,531

Total regulatory activities $116,668 $ (6,513) $110,155 $ (6,918) $103,237

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for Economic DevelopmentFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

Business development $ 57,530 $ (82) $ 57,448 $ (3,082) $ 54,366Support of scientific research and development 22,543 (880) 21,663 - 21,663Promote Oklahoma tourism 16,156 (1,208) 14,948 (1,369) 13,579Training for Industry program 5,979 (202) 5,777 (725) 5,052Oklahoma Industrial Finance Authority 3,002 (3,089) (87) - (87)Oklahoma Capital Investment Board 2,478 (4,140) (1,662) - (1,662)Oklahoma Development Finance Authority 1,231 (1,347) (116) - (116)Other economic development activities 1,120 (63) 1,057 (248) 809

Total economic development $110,039 $ (11,011) $ 99,028 $ (5,424) $ 93,604

The accompanying notes are an integral part of the illustrative financial statements.

The accompanying notes are an integral part of the illustrative financial statements.

22

23

Level III: Program financial statements

The financial statements presented here allowthe government to disclose its goals, what it isdoing to attain those goals, what progress it ismaking, and at what cost. At this level, the inclu-

sion of non-financial performance informationbecomes critical. The principal statement is astatement of activities with each program gettinga line in the statement.

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of Activities for Highway Patrol and Related ActivitesFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers