energy transport technology and … · insurance regulation in china ... energy infrastructure,...

TRANSCRIPT

Insurance regulation in ChinaTen things to know

FINANCIAL INSTITUTIONSENERGYINFRASTRUCTURE, MINING AND COMMODITIESTRANSPORTTECHNOLOGY AND INNOVATIONPHARMACEUTICALS AND LIFE SCIENCES

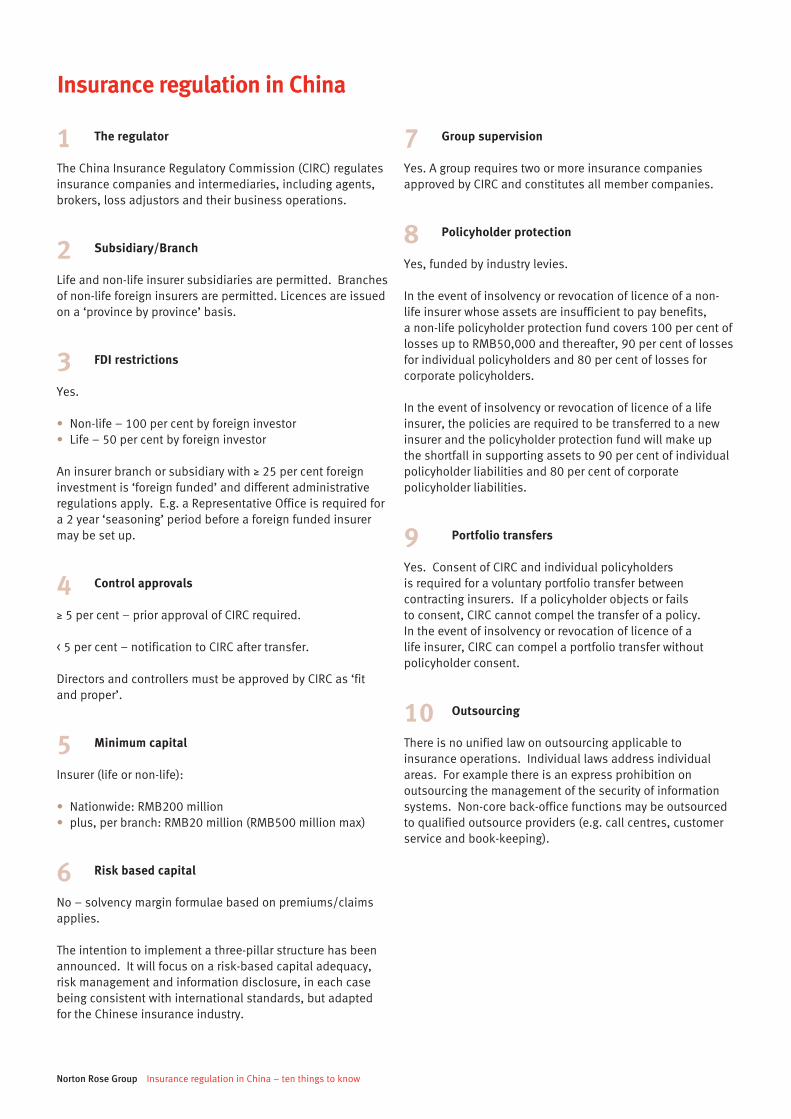

1 The regulator

The China Insurance Regulatory Commission (CIRC) regulates insurance companies and intermediaries, including agents, brokers, loss adjustors and their business operations.

2 Subsidiary/Branch

Life and non-life insurer subsidiaries are permitted. Branches of non-life foreign insurers are permitted. Licences are issued on a ‘province by province’ basis.

3 FDI restrictions

Yes.

• Non-life – 100 per cent by foreign investor• Life – 50 per cent by foreign investor

Aninsurerbranchorsubsidiarywith≥25percentforeigninvestment is ‘foreign funded’ and different administrative regulations apply. E.g. a Representative Office is required for a2year‘seasoning’periodbeforeaforeignfundedinsurermay be set up.

4 Control approvals

≥5percent–priorapprovalofCIRCrequired.

< 5 per cent – notification to CIRC after transfer.

Directors and controllers must be approved by CIRC as ‘fit and proper’.

5 Minimum capital

Insurer (life or non-life):

• Nationwide:RMB200million• plus,perbranch:RMB20million(RMB500millionmax)

6 Risk based capital

No – solvency margin formulae based on premiums/claims applies.

The intention to implement a three-pillar structure has been announced. It will focus on a risk-based capital adequacy, risk management and information disclosure, in each case being consistent with international standards, but adapted for the Chinese insurance industry.

7 Group supervision

Yes. A group requires two or more insurance companies approved by CIRC and constitutes all member companies.

8 Policyholder protection

Yes, funded by industry levies.

In the event of insolvency or revocation of licence of a non-life insurer whose assets are insufficient to pay benefits, a non-life policyholder protection fund covers 100 per cent of losses up to RMB50,000 and thereafter, 90 per cent of losses for individual policyholders and 80 per cent of losses for corporate policyholders.

In the event of insolvency or revocation of licence of a life insurer, the policies are required to be transferred to a new insurer and the policyholder protection fund will make up the shortfall in supporting assets to 90 per cent of individual policyholder liabilities and 80 per cent of corporate policyholder liabilities.

9 Portfolio transfers

Yes. Consent of CIRC and individual policyholders is required for a voluntary portfolio transfer between contracting insurers. If a policyholder objects or fails to consent, CIRC cannot compel the transfer of a policy. In the event of insolvency or revocation of licence of a life insurer, CIRC can compel a portfolio transfer without policyholder consent.

10 Outsourcing

There is no unified law on outsourcing applicable to insurance operations. Individual laws address individual areas.Forexamplethereisanexpressprohibitiononoutsourcing the management of the security of information systems. Non-core back-office functions may be outsourced to qualified outsource providers (e.g. call centres, customer service and book-keeping).

Norton Rose Group Insurance regulation in China – ten things to know

Insurance regulation in China

Norton Rose Group Insurance regulation in China – ten things to know

Contacts

Norton Rose Group

Anna TippingPartnerNorton Rose (Asia) LLPTel +65 6309 5417 [email protected]

Lynn YangPartnerNorton Rose [email protected]

AmsterdamAthensBrusselsFrankfurtHamburgLondonMilan

MoscowMunichParisPiraeusPragueRomeWarsaw

Europe

BangkokBeijingHo Chi Minh City*Hong KongJakarta*ShanghaiSingaporeTokyo

Asia

CalgaryMontréalOttawa

QuébecToronto

Canada

Cape TownCasablancaDurbanJohannesburg

AfricaBrisbaneCanberraMelbournePerthSydney

AustraliaAbu DhabiBahrainDubai

Middle East

Almaty

BogotáCaracas

Latin America

*associate office

Kazakhstan

nortonrose.com

The purpose of this publication is to provide information as to developments in the law. It does not contain a full analysis of the law nor does it constitute an opinion of Norton Rose (Asia) LLP on the points of law discussed.

No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any constituent part of Norton Rose Group (whether or not such individual is described as a “partner”) accepts or assumes responsibility, or has any liability, to any person in respect of this publication. Any reference to a partner or director is to a member, employeeorconsultantwithequivalentstandingandqualificationsof,as the case may be, Norton Rose LLP or Norton Rose Australia or Norton Rose Canada LLP or Norton Rose South Africa (incorporated as Deneys ReitzInc)orofoneoftheirrespectiveaffiliates.

©NortonRose(Asia)LLPNR1352407/12Extractsmaybecopiedprovidedtheirsourceisacknowledged.

Norton Rose GroupNortonRoseGroupisaleadinginternationallegalpractice.Withmorethan2900lawyers, we offer a full business law service to many of the world’s pre-eminent financial institutions and corporations from offices in Europe, Asia, Australia, Canada, Africa, the Middle East, Latin America and Central Asia. We are strong in financial institutions; energy; infrastructure, mining and commodities; transport; technology and innovation; and pharmaceuticals and life sciences. Norton Rose Group comprises Norton Rose LLP, Norton Rose Australia, Norton Rose Canada LLP, Norton Rose South Africa (incorporated as Deneys Reitz Inc), and their respective affiliates.