energy efficiency indicator -...

TRANSCRIPT

2010 North America Results

Findings Summary

Energy Efficiency Indicator

April 19, 2010

Agenda

� What is the Energy Efficiency Indicator?

� Who did we survey?

� What are their priorities and concerns?� What are their priorities and concerns?

� What are their investment plans and financial criteria for

making energy efficiency investments?

� What practices and technologies are most common?

2 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

What is the Energy Efficiency Indicator?

� A global survey of decision makers responsible for commercial

buildings and their energy use

� Examines trends in energy efficiency priorities and practices

� Founded by Johnson Controls and the International Facility

Management Association (IFMA) in 2007

� 4th annual survey completed for North America in March 2010

� Additional surveys underway in China, France, Germany, India,

Poland, Spain, and the United Kingdom, with results to be

released at events throughout the summer of 2010

3 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

RESPONDENT PROFILEEnergy Efficiency Indicator

2010 North America Results

4 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Who we surveyed: 2 qualifying criteria

1. Must have capital- or operations budget

responsibility for their organization’s

facilities.

2. Job responsibilities must include reviewing

or monitoring energy usage,

and/or

proposing or approving initiatives to make

organization’s facilities more efficient.

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

5

Who we surveyed

By Role By Region

By Industry Sector

C-level Executives

30%Facility

Owner/ Proprietors

11%

14351435 total respondents in North America

6

9%8%

16%

4%

8%4% 14%

13%

5%

19%

VPs and GMs32%

Facility Managers

27%Healthcare

20%

Consulting/Legal9%

Manufacturing7%

Finance7%

Government6%

Retail5%

Service5%

IT/Telcom4%

Media/ entertainment

4%

Other33%

Who we surveyed

14351435 total respondents in North America

11%

21%

8%

19%

10%

25%

30%

28%

500,000 to 999,999 sf

100,000 to 499,999 sf

50,000 to 99,999 sf

Less than 50,000 sf

Owner/ Proprietors

Facility Managers

VPs and GMs

C-level Executives

RolesRoles

Area ofResponsibility

Area ofResponsibility

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

7

33%

4%

4%

5%

5%

6%

6%

7%

9%

20%

9%

0 100 200 300 400 500

Other

Media/ entertainment

IT/Telcom

Service

Retail

Government

Finance

Manufacturing

Consulting/Legal

Healthcare

More than 1 million sf

Number of Respondents

Industry Sector

Industry Sector

PRIORITIES AND CONCERNSEnergy Efficiency Indicator

2010 North America Results

8 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Energy efficiency remains a strong business priority

65%... 65%... are paying more attention to energy

efficiency than last year

84%... 84%... Say energy efficiency is a priority for

new construction and retrofit projects

9 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Energy management more important to larger

organizations and varies by sector

44%43%

40%

38%

45%

45%34% 29%

39% 36%33%

47%

36%

40%

60%

80%

100%Not at all important

Not very important

Somewhat important

How important is energy management to your company/organization?

10

15%9% 10%

19% 23%15% 17% 22%

8%17%

37%

27%

41%

44%43%

40% 39%40%

32%

42%

0%

20%

40%Very important

Extremely important

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Importance of efficiency has decreased since 2009, but

remains quite high in light of the economic climate

77%

88%93%

84%

57% 58%60%

70%

80%

90%

100%

11

51%

57% 58%

52%

40%

50%

60%

2007 2008 2009 2010

Consider energy efficiency a priority in current/planned construction or retrofit projects

Energy management is extremely or very important to our organization

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Reducing energy costs remains the key driver

Public imaged is also notably high

0% 20% 40% 60% 80% 100%

Energy cost savings

Enhanced public image

Government/utility incentives

Greenhouse gas reduction

How significant an influence are the following in your organization's energy efficiency decisions?

12

40%

Attracting, retaining customers

Anticipated regulation

Existing legislation

Attracting, retaining employees

Investor reporting demands

Attracting tenants

Extremely significant Very significant Somewhat significant

Not very significant Not at all significant Not Applicable

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Incentives drop in importance while carbon emission

concerns become stronger

37%36%

14%12%

16%

8% 5%

9%

3% 4%12%

60%

80%

100%Don't know

Not at all significant

Not very significant

How influential are government/utility incentives in your organization's

energy efficiency decisions?

21%23%

17%11%

5% 4%

60%

80%

100%Don't know

Not at all significant

Not very significant

How significant are greenhouse gas emission reductions in your organization's energy

efficiency decisions?

13

12% 13% 9%

26%30%

22%

37%

31%

0%

20%

40%

2008 2009 2010

significant

Somewhat significant

Very significant

Extremely significant 7% 5%

15% 20%

35%37%

0%

20%

40%

2009 2010

significant

Somewhat significant

Very significant

Extremely significant

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Real estate leaders believe energy prices

will climb significantly this year

Average expected change in energy prices

over next 12 months = 7% increase

80%

100%

Cum

ula

tive D

istr

ibution

Do you believe the combined price of the energy that your facilities use will. . .

64% believe prices will increase

14

0%

20%

40%

60%

Cum

ula

tive D

istr

ibution

64% believe prices will increase over the next 12 months

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Climate legislation is viewed as both a risk

and a business growth opportunity

An equal risk and opportunity

A slightly greater opportunity

Primarily an opportunity

46%

9%

7%

Is climate change legislation a risk or a growth opportunity for your organization?

15

0%20%

40%60%

Primarily a risk

A slightly greater risk

An equal risk and opportunity

19%

19%

46%

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Despite lowered legislation expectations,

more organizations setting carbon goals

34%

60%

80%

100%

Somewhat

How likely is significant legislation mandating energy efficiency and/or

carbon reduction within the next 2 years?

76%

85%

75%

14%

13%

14%

15%

16%

Does your company/organization have a publicly stated carbon-reduction goal?

16

11% 16%9%

28%

35%

27%

37% 38%

0%

20%

40%

60%

2008 2009 2010

Somewhat likely

Very likely

Extremely likely

11%

12% 12%

8%

9%

10%

11%

12%

13%

2007 2008 2009 2010

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Many lack carbon strategies; those with strategies

choosing building efficiency first

2%

3%

4%

4%

5%

38%

Alternative transportation fuels

Energy efficiency in vehicle fleet

Renewable power purchases

Onsite renewable energy

Telecommuting, virtual meetings

Energy efficiency in buildings

What is your organization's top strategy to reduce its carbon emissions?

1%

1%

1%

2%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Supply chain carbon reductions

Carbon offset purchases

Real estate portfolio consolidation

Alternative transportation fuels

40% either don’t know or have not

yet prioritized among strategies

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

17

73% select building efficiency as one of

their top six strategies

10%

20%

12%

15%

23%

35%

2%

3%

4%

4%

5%

38%

Alternative transportation fuels

Energy efficiency in vehicle fleet

Renewable power purchases

Onsite renewable energy

Telecommuting, virtual meetings

Energy efficiency in buildings

Top Strategy

Other Strategies (up to 5)

What are your organization's top strategies for reducing its carbon emissions?

23%

16%

8%

3%

6%

10%

26%

15%

1%

1%

1%

2%

0% 10% 20% 30% 40% 50%

No prioritization amongst strategies

Don't know

Supply chain carbon reductions

Carbon offset purchases

Real estate portfolio consolidation

Alternative transportation fuels

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

18

INVESTMENT PLANS & INVESTMENT PLANS &

FINANCIAL CRITERIAEnergy Efficiency Indicator

2010 North America Results

19 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

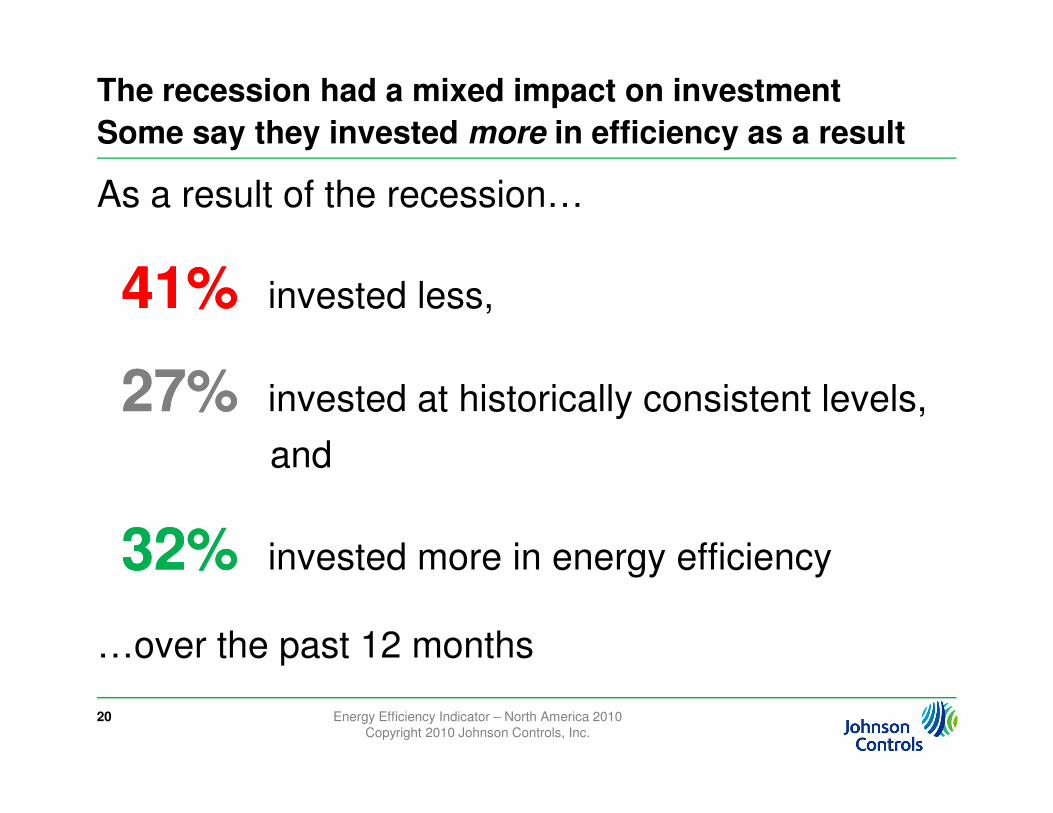

The recession had a mixed impact on investment

Some say they invested more in efficiency as a result

As a result of the recession…

41% 41% invested less,

27% 27% invested at historically consistent levels,

20

27% 27% invested at historically consistent levels,

and

32% 32% invested more in energy efficiency

…over the past 12 months

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Energy efficiency spending to rebound in 2010

64%

80%capital expenditures operating expenditures

Percentage planning to make energy efficiency investments over the next 12 months with…

21

57%56%

46%

52%

64%

61%

55%

60%

40%

60%

2007 2008 2009 2010

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Construction and retrofit starts plans are also

increasing among those surveyed

22%22%

30%

20%

25%

30%

35%

40%new construction retrofits

Percentage currently undergoing or planning to undergo

over the next 12 months

22

16%

0%

5%

10%

15%

20%

2009 2010

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Large and public organizations are most

likely to invest in efficiency; Retail sector lags

30%

47%

31%

25%

14%

27% 19%

23%

49%

21%

18%28%

19% 15%7%

14% 19%6%

26%

11%

60%

80%

100%

Don't Know

No

Do you expect your organization to make energy efficiency improvements financed with capital expenditures over the next 12 months

23 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

52%

25%

50%60%

79%

59% 62%71%

26%

67%

47%

0%

20%

40%

Yes

Capital budgets and incentives are primary

funding source; Use of financing is rare

52%

20%

14%

9%

0% 20% 40% 60%

Facilities capital budget

Grants or tax credits

Energy savings performance contract

Energy or climate set-asides in capital budget

Which options will your organization consider to pay for energy efficiency and renewable energy projects over the next 12 months? (Select all that apply)?

N = 1427

24 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

9%

8%

7%

5%

3%

3%

1%

1%

Energy or climate set-asides in capital budget

Power purchase agreement (PPA)

Traditional debt financing

Shared savings agreement

Utility on-bill financing (OBF)

Capital or municipal lease

PACE/tax lien financing

Energy efficient mortgage

Budget levels and expected impact remain consistent

7.3%

8.2%7.6% 7.8%

8%

10%

12%

capital budget

What percentage of your facilities-related budgets will be invested in

energy efficiency over next 12 months?

60%

80%

100%

Don't know

More than 10%

By how much do you expect energy improvements put in place over the

next 12 months to reduce your energy consumption?

25

5.2%6.2%

5.5% 5.5%

0%

2%

4%

6%

2007 2008 2009 2010

budget

operating budget

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

0%

20%

40%

60%

2007 2008 2009 2010

5% to 9%

1% to 4%

Less than 1%

Investment criteria also holds steady;

44% require less than 3 year payback

83% 83%87%

60%

80%

100%

Less than 10 years

What is the longest payback period you would allow for a significant energy

efficiency investment?

14%

27%

60%

80%

100%

How does that compare to what would have been allowed 5 years ago?

Don’t Know

Allowed longer payback 5 years ago

26

43% 44% 44%

5% 6% 4%

0%

20%

40%

60%

2008 2009 2010

Less than 3 years

Less than 1 year

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

15%

44%

14%

0%

20%

40%

60%

2008 2009 2010

Allowed longer payback 5 years ago

Allowable payback hasn’t changed

Will allow longer payback today

Limited internal capital is the greatest

barrier to energy efficiency

3.23.2Average maximum

6%

16%

21%

38%

Technical expertise

Uncertainty of savings/ROI

Insufficient payback/ROI

Lack of capital budget

What is the top barrier to capturing energy savings for your organization?

27

Average maximum payback period for energy efficiency

44% require a 3 year payback or less

3%

3%

4%

5%

5%

0% 10% 20% 30% 40%

Other (specify)

Inability to finance (credit rating, collateral, balance sheet)

Dedicated attention, ownership

Buy-in from senior leaders

Landlord/tenant split incentives

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

PRACTICES & TECHNOLOGIESEnergy Efficiency Indicator

2010 North America Results

28 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Most popular efficiency measures are

lighting retrofits and operational changes

72%

63%

61%

56%

40%

36%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Switched to energy efficient lamps, ballasts, or fixtures

Educated facilities operations staff

Educated building occupants

Adjusted controls to reduce time that heating/AC runs

Installed occupancy or daylight sensors

Replaced inefficient equipment before end of useful life

Upgraded existing building management system

Which measures has your company adopted to reduce energy costs?

33%

30%

29%

28%

27%

25%

25%

19%

19%

Upgraded existing building management system

Increased frequency of monitoring consumption

Negotiated energy contracts with suppliers

Attended or sent staff to energy management seminars

Installed or adjusted lighting timers

Increased preventive maintenance schedules

Installed variable speed/variable frequency drives …

Installed energy-saving glass in windows

Participated in demand response programs

Note: The 15 most popular measures of 33 included in the survey are listed above

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

29

Green buildings are accumulating;

Renewable energy on the radar

33% 33% seeking green building certification for new

construction projects

12% 12% have at least one green certified building, up

from 8%8% in 2009from 8%8% in 2009

31% 31% considering solar PV, 20% 20% considering

solar thermal, 14% 14% considering geothermal in

new construction and retrofit projects

30 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Green building goals staying constant

45%

12% 14% 13%18% 16% 20%

5%3% 2%

3% 3% 2%

60%

80%

100%

don't know

no goal for green buildings

What are your goals with respect to green buildings?

New Construction Retrofit Projects

31

34% 38%33%

20% 17% 18%

48% 45% 52%

59% 64% 60%

0%

20%

40%

60%

2008 2009 2010 2008 2009 2010

green elements, but not certified

certified to a recognized green standard

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Consideration levels for renewable

energy technologies fall in 2010

31%30%

35%

40%

45%

50%

2008 2009 2010

Which renewable energy technologies is your organization considering or utilizing in construction or retrofit projects?

32 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

20%

14%13%

7%5%

0%

5%

10%

15%

20%

25%

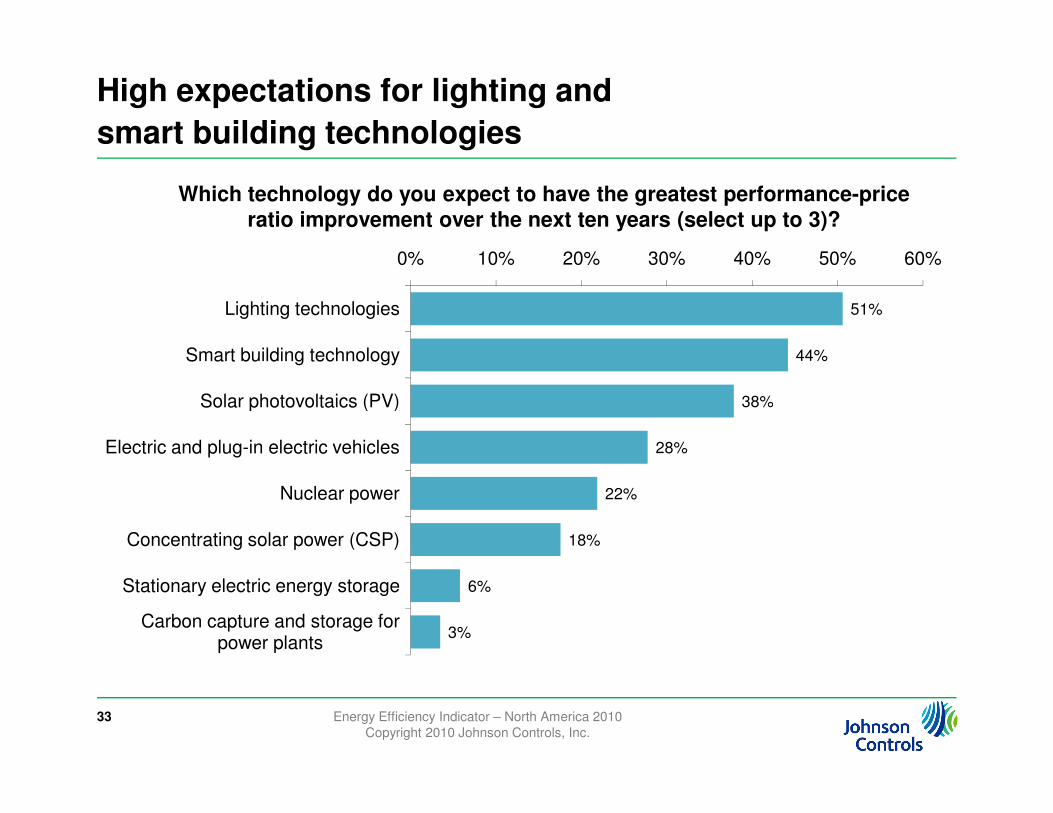

High expectations for lighting and

smart building technologies

51%

44%

38%

0% 10% 20% 30% 40% 50% 60%

Lighting technologies

Smart building technology

Solar photovoltaics (PV)

Which technology do you expect to have the greatest performance-price ratio improvement over the next ten years (select up to 3)?

33 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

38%

28%

22%

18%

6%

3%

Solar photovoltaics (PV)

Electric and plug-in electric vehicles

Nuclear power

Concentrating solar power (CSP)

Stationary electric energy storage

Carbon capture and storage for power plants

Observations & Conclusions

� Efficiency investment remains strongEnergy cost concerns, public image, and climate leadership

goals are driving investment. Larger organizations are more

likely to make efficiency investments.

� Buildings efficiency is top carbon strategy � Buildings efficiency is top carbon strategy Despite lowered legislation expectations,

more organizations setting voluntary GHG goals

� Capital availability remains a strong barrierOrganizations rely primarily on internal capital budgets for

efficiency & renewable energy investments rather than seeking

external financing

34 Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

For more complete EEI results

see online press kit

Go to johnsoncontrols.com

� media

� press materials

� press kits

� Building Efficiency

� 2010 Energy Efficiency Indicator

35

http://johnsoncontrols.mediaroom.com/index.php?s=112

Includes

link to

webcast

archive

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

Energy Efficiency Indicator – North America 2010

Energy Efficiency Indicator – North America 2010

Copyright 2010 Johnson Controls, Inc.

36