endeavour (rdr) proprietary limited - ey · pdf fileproprietary limited 31 december 2015 (and...

TRANSCRIPT

•

Endeavour (RDR) Proprietary Limited Illustrative financial statements for 31 December 2015 (and 30 June 2016) year ends Complying with Australian Accounting Standards – Reduced Disclosure Requirements

EndeavourTM (RDR) Pty Ltd i

Foreword In 2010 the Australian Accounting Standards Board (AASB) took the first step in simplifying financial reporting by introducing a two tier reporting system for reporting entities required to prepare general purpose financial statements (GPFS). This differential reporting regime enables certain entities to minimise the costs involved in meeting financial reporting requirements by reducing the disclosures otherwise required by Australian Accounting Standards.

Whether an entity is able to apply the reduced disclosure requirements is dependent upon whether or not it is considered to be publicly accountable. In Australia, practice is still emerging as to which entities are eligible for the reduced disclosures given that this determination requires judgement to be applied.

This new edition of Endeavour (RDR) Pty Ltd provides illustrative financial statements prepared in accordance with Australian Accounting Standards – Reduced Disclosure Requirements (RDR). It also illustrates how these financial statements will differ to other larger entities that prepare general purpose financial reports complying with all disclosure requirements in Australian Accounting Standards (i.e., Tier 1).

At the September 2015 meeting, the AASB amended the principles for determining RDR. Based on these amended principles, the AASB is drafting new RDR, which are expected to be exposed in February 2016. During October 2015, the AASB tentatively decided to propose that the new RDR, when finalised, would apply to annual reporting periods beginning on or after 1 January 2018, with early application permitted.

When entities are considering their financial reporting obligations and the type of financial report they should be preparing, they should be cognisant of the current regulatory deliberations with respect to special purpose financial statements. Of particular relevance is the AASB’s tentative decision, in May 2014, to reduce its remit to creating accounting standards for the preparation of GPFS only. This tentative decision, along with the recent amendments to the Tax Law which now requires significant global entities to lodge GPFS with the Australian Taxation Office, suggests that we can expect change in relation to the financial reporting requirements for some entities. Accordingly, for those entities considering a switch to general purpose financial reporting, this publication will be useful for determining the extent of disclosures that would be required in Tier 2 general purpose financial statements.

I trust this publication will prove useful when preparing GPFS under the reduce disclosure regime.

Tracey Waring Partner and EY Oceania IFRS Leader Ernst & Young Australia

ii EndeavourTM (RDR) Pty Ltd

Contents Abbreviations and key ............................................................................................................................................ iii Introduction ........................................................................................................................................................... iv Consolidated statement of profit or loss ................................................................................................................... 3 Consolidated statement of other comprehensive income ........................................................................................... 5 Consolidated statement of financial position ............................................................................................................ 7 Consolidated statement of changes in equity ............................................................................................................ 9 Consolidated statement of cash flows .................................................................................................................... 11 Notes to the consolidated financial statements ....................................................................................................... 12 Directors' declaration ......................................................................................................................................... 117 Independent auditor's report to the members of Endeavour (RDR) Pty Ltd ............................................................. 118 Appendix A — Closed Group class order disclosures ............................................................................................... 121 Appendix B — Agricultural assets example disclosures ........................................................................................... 123 Appendix C — AASB 1053 Application of tiers of Australian Accounting Standards .................................................. 125 Appendix D — RDR adoption and transition ........................................................................................................... 127

EndeavourTM (RDR) Pty Ltd iii

Abbreviations and key The following styles of abbreviation are used in this set of illustrative financial statements:

IAS 33.41 International Accounting Standard No. 33, paragraph 41

IAS 1.BC13 International Accounting Standard No. 1, Basis for Conclusions, paragraph 13

IFRS 2.44 International Financial Reporting Standard No. 2, paragraph 44

SIC 29.6 Standing Interpretations Committee Interpretation No. 29, paragraph 6

IFRIC 4.6 IFRS Interpretations Committee (formerly IFRIC) Interpretation No. 4, paragraph 6

IAS 39.IG.G.2 International Accounting Standard No. 39 — Guidance on Implementing IAS 39 Section G: Other, paragraph G.2

IAS 39.AG71 International Accounting Standard No. 39 — Appendix A — Application Guidance, paragraph AG71

ISA 700.25 International Standard on Auditing No. 700, paragraph 25

Commentary The commentary explains how the requirements of Australian Accounting Standards have been implemented in arriving at the illustrative disclosure

GAAP Generally Accepted Accounting Principles/Practice

IASB International Accounting Standards Board

Interpretations Committee

IFRS Interpretations Committee (formerly International Financial Reporting Interpretations Committee (IFRIC))

SIC Standing Interpretations Committee

AASB Australian Accounting Standards that are issued by the Australian Accounting Standards Board (AASB). The numbering convention is as follows:

► AASB 1 – AASB 15 represents Australian Accounting Standards issued by the AASB that are equivalent to the IFRS issued by the IASB. For example, AASB 15 is the equivalent of IFRS 15.

► AASB 101 – AASB 141 represents Australian Accounting Standards issued by the AASB that are equivalent to the IAS issued by the IASB. For example, AASB 108 is the equivalent of IAS 8.

► AASB 1004 – AASB 1057 represents Australian Accounting Standards issued by the AASB that have no equivalent in IFRS. That is, they are Australian-specific reporting requirements.

AASB Int Australian Interpretations that are issued by the AASB. The numbering convention is as follows:

► AASB Interpretations 1 – 21 represents Australian Interpretations issued by the AASB that are equivalent to the Interpretations issued by the IFRS Interpretations Committee. For example, AASB Interpretation 14 is the equivalent to Interpretation 14.

► AASB Interpretations 107 – 132 represents Australian Interpretations issued by the AASB that are equivalent to the Interpretations issued by the SIC. For example, AASB Interpretation 115 is the equivalent of SIC 15.

► AASB Interpretations 1003 – AASB 1055 represents Australian Interpretations issued by the AASB that have no equivalent international Interpretation. That is, they are Australian-specific reporting requirements.

CA 300A Corporations Act 2001, section 300A

Reg 2M.3.03(1) Corporations Regulations 2001, Chapter 2M, Regulation 3.03, paragraph 1

ASIC CO Australian Securities & Investments Commission Class Order

ASIC IR Australian Securities & Investments Commission Information Release

ASIC INFO Australian Securities & Investments Commission Information Sheet

ASIC RG Australian Securities & Investments Commission Regulatory Guidance

ASX Rec 2.5 Australian Stock Exchange Corporate Governance Council, Principles of Good Corporate Governance and Best Practice Recommendations, Recommendation 2.5

ASX 4.10.5 Australian Stock Exchange Listing Rules Chapter 4, Rule 10.5

iv EndeavourTM (RDR) Pty Ltd

Introduction Tiers of Australian Accounting Standards AASB 1053 Application of tiers of Australian Accounting Standards introduces two tiers of reporting requirements for preparing general purpose financial statements:

► Tier 1: Australian Accounting Standards ► Tier 2: Australian Accounting Standards – Reduced Disclosure Requirements

Tier 1 incorporates International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB) and includes requirements that are specific to Australian entities.

Tier 2 comprises the recognition and measurement requirements of Tier 1 but substantially reduced disclosure requirements. Except for the presentation of a third statement of financial position in particular circumstances under Tier 1, the presentation requirements under Tier 1 and Tier 2 are the same.

This document is a supplement to Endeavour (International) Limited (December 2015 edition) and contains the consolidated financial statements of a fictitious entity, Endeavour (RDR) Pty Ltd, an industrial company with subsidiaries (the Group). Endeavour (RDR) Pty Ltd is incorporated in Australia, with a reporting date of 31 December 2015.

The entity applies Tier 2 (reduced disclosure) requirements as described in AASB 1053 Application of Tiers of Australian Accounting Standards and AASB 2010-02 Amendments to Australian Accounting Standards arising from Reduced Disclosure, plus other amendments to Tier 2 requirements subsequently issued by the AASB and effective at 30 November 2014, while still complying with full AASB recognition and measurement requirements.

How to use these illustrative financial statements The enclosed financial statements contain full Australian Accounting Standards disclosures, highlighting those disclosures that are not required by entities applying the tier 2 requirements of AASB 1053 and AASB 2010-02. In addition, blue text indicates a disclosure requirement specific for tier 2 entities.

The financial statements are intended to illustrate the disclosure requirements of the Accounting Standards, including providing interpretive commentary where necessary. Other annual reporting information required by the Corporations Act 2001 is not included. For a full illustrative annual report, refer to the December 2015 version of Endeavour (International) Limited.

The financial statements are illustrative only and do not attempt to show all possible accounting and disclosure requirements. It is essential to refer to the relevant authoritative source and, where necessary, seek appropriate professional advice. Although the illustrative financial statements attempt to show the most common disclosure requirements for industrial companies, it should not be regarded as a comprehensive checklist. For a more comprehensive list of disclosure requirements, please refer to EY’s Financial Reporting Standards Disclosure Checklist. Enquiries regarding specialised industries and areas of accounting (e.g., insurance, US GAAP) should be directed to an EY professional.

Each section of the financial statements of the Group is cross-referenced to commentary. Source references to the authoritative literature are also provided. The commentary follows the disclosure contained in each section of the financial statements and is intended to support disclosure requirements of the note or to explain the approach taken in providing the illustrative disclosure. The commentary has been highlighted or amended where relevant to reflect the tier 2 requirements.

Notations shown in the right-hand margin of each page are references to accounting standards or other pronouncements that describe the specific disclosure requirements. References made to International Financial Reporting Standards should be read as the Australian equivalent standard as set out in the ‘Abbreviations and key’ section above. Commentary is provided to explain the basis for the disclosure or to address alternative disclosures not included in the illustrative financial statements.

Users of this publication are encouraged to prepare entity-specific disclosures, for which these illustrative financial statements may serve as a useful reference. Transactions and arrangements other than those applicable to the Group may require additional disclosures. It should be noted that the illustrative financial statements of the Group are not designed to satisfy any stock market or country-specific regulatory requirements, nor is this publication intended to reflect disclosure requirements that apply mainly to regulated or specialised industries.

Australian Accounting Standards as at 31 November 2015 As a general approach, these illustrative financial statements do not early adopt standards or amendments before their effective date. The standards applied in these illustrative financial statements are those that were in issue as at 31 November 2015 and effective for annual periods beginning on or after 1 January 2015. Standards issued, but not yet effective, as at 30 November 2015, have not been early adopted. It is important to note that these illustrative financial statements will require continual updating as standards are issued and/or revised.

Introduction (continued)

EndeavourTM (RDR) Pty Ltd v

Users of this publication are cautioned to check that there has been no change in requirements of Australian Accounting Standards between 31 November 2015 and the date on which their financial statements are authorised for issue. In accordance with paragraph 30 of AASB 108, specific disclosure requirements apply for standards and interpretations issued but not yet effective (see Note 34 of these illustrative financial statements). Furthermore, if the financial year of an entity is other than the calendar year, new and revised standards applied in these illustrative financial statements may not be applicable. For example, the Group had applied Interpretation 21 Levies for the first time in its 2014 illustrative financial statements. An entity with a financial year that commences from, for example, 1 October and ends on 30 September would have to apply Interpretation 21 for the first time in the annual financial statements beginning on 1 October 2014. Therefore, Interpretation 21 would not have been applicable in the financial statements of an entity with a year-end of 30 September 2014, unless it voluntarily chose to early adopt Interpretation 21.

The disclosure requirements of the following Australian Accounting Standards are not applicable to the Group and have therefore not been illustrated in these financial statements:

AASB 1 First-time Adoption of Australian Accounting Standards AASB 4 Insurance Contracts AASB 6 Exploration for and Evaluation of Mineral Resources AASB 8 Operating Segments* AASB 9 Financial Instruments AASB 14 Regulatory Deferral Accounts AASB 15 Revenue from Contracts with Customers AASB 111 Construction Contracts AASB 127 Separate Financial Statements AASB 129 Financial Reporting in Hyperinflationary Economies AASB 133 Earnings per Share* AASB 134 Interim Financial Reporting** AASB 141 Agriculture*** AASB 1004 Contributions AASB 1023 General Insurance Contracts AASB 1038 Life Insurance Contracts AASB 1039 Concise Financial Reports AASB 1049 Whole of Government and General Government Sector Financial Reporting AASB 1050 Administered Items AASB 1051 Land Under Roads AASB 1052 Disaggregated Disclosures AASB 1055 Budgetary Reporting AASB 1056 Superannuation Entities AASB 1057 Application of Australian Accounting Standards AAS 25 Financial Reporting by Superannuation Plans Interpretation 2 Members’ Shares in Co—operative Entities and Similar Instruments Interpretation 5 Rights to Interests arising from Decommissioning, Restoration and Environmental Rehabilitation

Funds Interpretation 7 Applying the Restatement Approach under AASB 129 Financial Reporting in Hyperinflationary

Economies Interpretation 12 Service Concession Arrangements Interpretation 14 AASB 19 — The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their

Interaction Interpretation 15 Agreements for the Construction of Real Estate Interpretation 19 Extinguishing Financial Liabilities with Equity Instruments Interpretation 20 Stripping Costs in the Production Phase of a Surface Mine Interpretation 107 Introduction of the Euro Interpretation 110 Government Assistance — No Specific Relation to Operating Activities Interpretation 125 Income Taxes – Changes in the Tax Status of an Entity or its Shareholders Interpretation 129 Service Concession Arrangements: Disclosures Interpretation 131 Revenue — Barter Transactions Involving Advertising Services Interpretation 132 Intangible Assets — Web Site Costs Interpretation 1003 Australian Petroleum Resource Rent Tax Interpretation 1038 Contributions by Owners Made to Wholly-Owned Public Sector Entities Interpretation 1042 Subscriber Acquisition Costs in the Telecommunications Industry Interpretation 1047 Professional Indemnity Claims Liabilities in Medical Defence Organisations Interpretation 1055 Accounting for Road Earthworks

* Example disclosures prepared in accordance with these standards are included in Endeavour (International) Limited. *** An example half-year financial report in accordance with AASB 134 is included in Endeavour (International) Limited. *** Example disclosures for agricultural assets are included as a guide in Appendix B.

Introduction (continued)

vi EndeavourTM (RDR) Pty Ltd

Accounting policy choices Accounting policies are broadly defined in AASB 108 and include not just the explicit elections provided for in some standards, but also other conventions and practices that are adopted in applying principle-based standards.

In some cases, Australian Accounting Standards permit more than one accounting treatment for a transaction or event. Preparers of financial statements should select the treatment that is most relevant to their business and circumstances as their accounting policy.

AASB 108 requires an entity to select and apply its accounting policies consistently for similar transactions, events and/or conditions, unless an Australian Accounting Standard specifically requires or permits categorisation of items for which different policies may be appropriate. Where an Australian Accounting Standard requires or permits such categorisation, an appropriate accounting policy is selected and applied consistently to each category. Therefore, once a choice of one of the alternative treatments has been made, it becomes an accounting policy and must be applied consistently. Changes in accounting policy should only be made if required by a standard or interpretation, or if the change results in the financial statements providing reliable and more relevant information.

In this publication, when a choice is permitted by Australian Accounting Standards, the Group has adopted one of the treatments as appropriate to the circumstances of the Group. In these cases, the commentary provides details of which policy has been selected, the reasons for this policy selection, and summarises the difference in the disclosure requirements.

Changes in the 2015 edition of Endeavour (RDR) Pty Ltd annual financial statements The standards and interpretations listed below have become effective since 31 October 2014 for annual periods beginning on 1 January 2015. While the list of new standards is provided below, not all of these new standards will have an impact on these illustrative financial statements. To the extent these illustrative financial statements have changed since the 2014 edition due to changes in standards and interpretations, we have indicated what has changed in Note 2.4.

Other changes from the 2014 edition have been made in order to reflect practice developments and to improve the overall quality of the illustrative financial statements.

Changes to Australian Accounting Standards The following new standards and amendments became effective as of 1 January 2015:

• Annual Improvements Cycle - 2010-2012

• Annual Improvements Cycle - 2011-2013

• Amendments to AASB 119 Defined Benefit Plans: Employee Contributions

Not all of these standards and amendments impact the Group’s consolidated financial statements. If a standard or amendment affects the Group, it is described, together with the impact, in Note 2.4 of these consolidated financial statements.

Caveat The names of people and corporations included in these illustrative financial statements are fictitious and have been created for the purpose of illustration only. Any resemblance to any person or business is purely coincidental.

These financial statements are illustrative only and do not attempt to show all possible accounting and disclosure requirements. In case of doubt as to the requirements, it is essential to refer to the relevant source and, where necessary, seek appropriate professional advice. Although the illustrative financial statements attempt to show the most likely disclosure requirements for industrial entities, it should not be regarded as a comprehensive checklist of disclosure requirements.

EndeavourTM (RDR) Pty Ltd 1

Contents to annual report Consolidated statement of profit or loss ................................................................................................................... 3 Consolidated statement of other comprehensive income ........................................................................................... 5 Consolidated statement of financial position ............................................................................................................ 7 Consolidated statement of changes in equity ............................................................................................................ 9 Consolidated statement of cash flows .................................................................................................................... 11 Notes to the consolidated financial statements ....................................................................................................... 12 1. Corporate information ............................................................................................................................. 12 2. Significant accounting policies .................................................................................................................. 12 2.1 Basis of preparation ................................................................................................................................. 12 2.2 Basis of consolidation .............................................................................................................................. 13 2.3 Summary of significant accounting policies ............................................................................................... 14 2.4 Changes in accounting policies and disclosures .......................................................................................... 34 2.5 Correction of an error .............................................................................................................................. 36 3. Significant accounting judgements, estimates and assumptions .................................................................. 37 4. Segment information ............................................................................................................................... 42 5. Capital management ................................................................................................................................ 42 6. Group information ................................................................................................................................... 43 7. Business combinations and acquisition of non-controlling interests ............................................................. 44 8. Material partly-owned subsidiaries ............................................................................................................ 48 9. Interest in a joint venture ......................................................................................................................... 51 10. Investment in an associate ....................................................................................................................... 52 11. Fair value measurement ........................................................................................................................... 53 12. Other income/expenses and adjustments .................................................................................................. 57 12.1 Other operating income ........................................................................................................................... 57 12.2 Other operating expenses ........................................................................................................................ 57 12.3 Finance costs .......................................................................................................................................... 58 12.4 Finance income ....................................................................................................................................... 58 12.5 Depreciation, amortisation, foreign exchange differences and costs of inventories included in the consolidated

statement of profit or loss ........................................................................................................................ 58 12.6 Employee benefits expense ...................................................................................................................... 59 12.7 Research and development costs .............................................................................................................. 59 12.8 Components of OCI .................................................................................................................................. 60 12.9 Administrative expenses .......................................................................................................................... 60 13. Discontinued operations........................................................................................................................... 61 14. Income tax .............................................................................................................................................. 64 15. Earnings per share (EPS) .......................................................................................................................... 68 16. Property, plant and equipment ................................................................................................................. 69 17. Investment properties .............................................................................................................................. 71 18. Intangible assets...................................................................................................................................... 73 19. Goodwill and intangible assets with indefinite lives ..................................................................................... 73 20. Financial assets and financial liabilities ...................................................................................................... 76 20.1 Financial assets ....................................................................................................................................... 76 20.2 Financial liabilities: Interest-bearing loans and borrowings ......................................................................... 77 20.3 Hedging activities and derivatives ............................................................................................................. 79 20.4 Fair values .............................................................................................................................................. 81 20.5 Financial instruments risk management objectives and policies .................................................................. 86 21. Inventories .............................................................................................................................................. 92 22. Trade and other receivables ..................................................................................................................... 92

Contents to annual report (continued)

2 EndeavourTM (RDR) Pty Ltd

23. Cash and short-term deposits ................................................................................................................... 93 24. Issued capital and reserves ...................................................................................................................... 95 25. Distributions made and proposed .............................................................................................................. 97 26. Provisions ............................................................................................................................................... 98 27. Government grants .................................................................................................................................. 99 28. Deferred revenue .................................................................................................................................... 99 29. Employee benefit liability ....................................................................................................................... 100 30. Share-based payments ........................................................................................................................... 106 31. Trade and other payables ....................................................................................................................... 108 32. Commitments and contingencies ............................................................................................................ 109 33. Related party disclosures ....................................................................................................................... 112 34. Standards issued but not yet effective .................................................................................................... 114 35. Events after the reporting period ............................................................................................................ 115 36. Auditors' remuneration .......................................................................................................................... 115 37. Information relating to Endeavour (RDR) Pty Ltd (the Parent) .................................................................. 116 Directors' declaration ......................................................................................................................................... 117 Independent auditor's report to the members of Endeavour (RDR) Pty Ltd ............................................................. 118

EndeavourTM (RDR) Pty Ltd 3

Consolidated statement of profit or loss For the year ended 31 December 2015 IAS 1.49

IAS 1.10(b) IAS 1.10A

IAS 1.51(c)

2015 2014

Restated* IAS 8.28

Notes $000 $000 IAS 1.51(d),(e)

Continuing operations IAS 1.81A

Sale of goods 161,927 142,551 IAS 18.35(b)(i)

Rendering of services 17,131 16,537 IAS 18.35(b)(ii)

Rental income 17 1,404 1,377

Revenue 180,462 160,465 IAS 1.82(a)

Cost of sales (136,549) (128,386) IAS 1.103

Gross profit 43,913 32,079 IAS 1.85, IAS 1.103

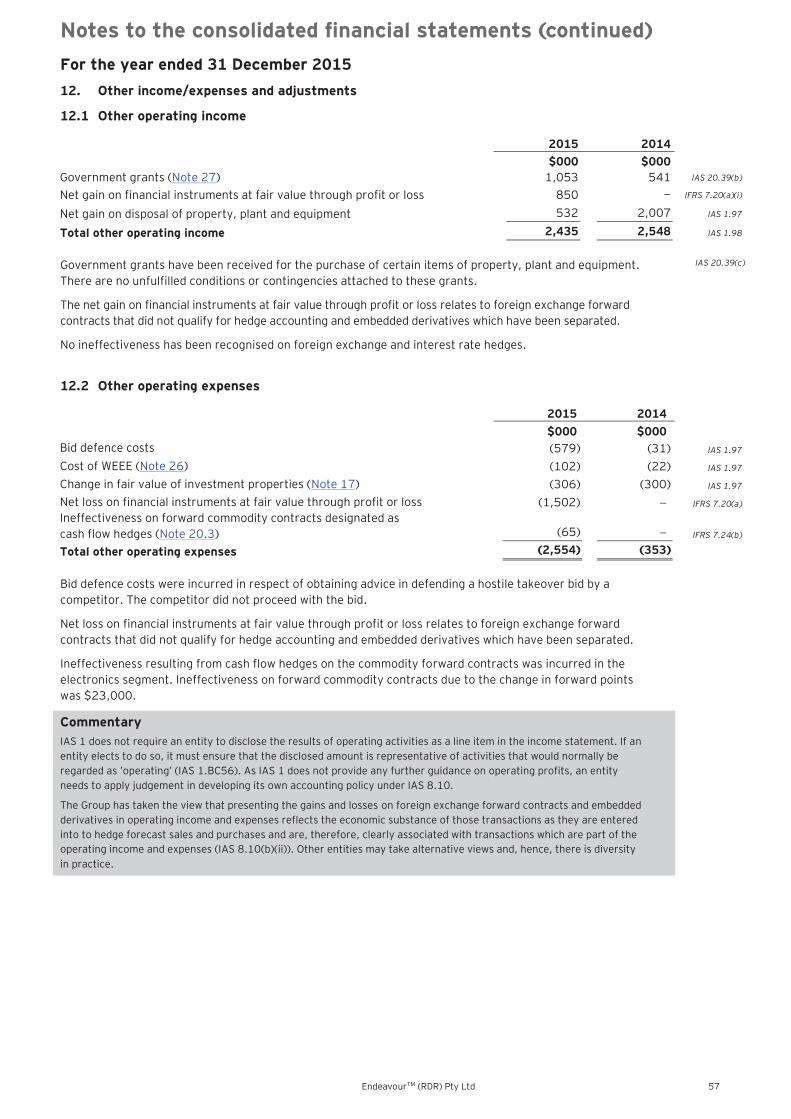

Other operating income 12.1 2,435 2,548 IAS 1.103

Selling and distribution expenses (14,001) (12,964) IAS 1.99, IAS 1.103

Administrative expenses 12.9 (18,428) (12,156) IAS 1.99, IAS 1.103

Other operating expenses 12.2 (2,554) (353) IAS 1.99, IAS 1.103

Operating profit 11,365 9,154 IAS 1.85, IAS 1.BC55-56

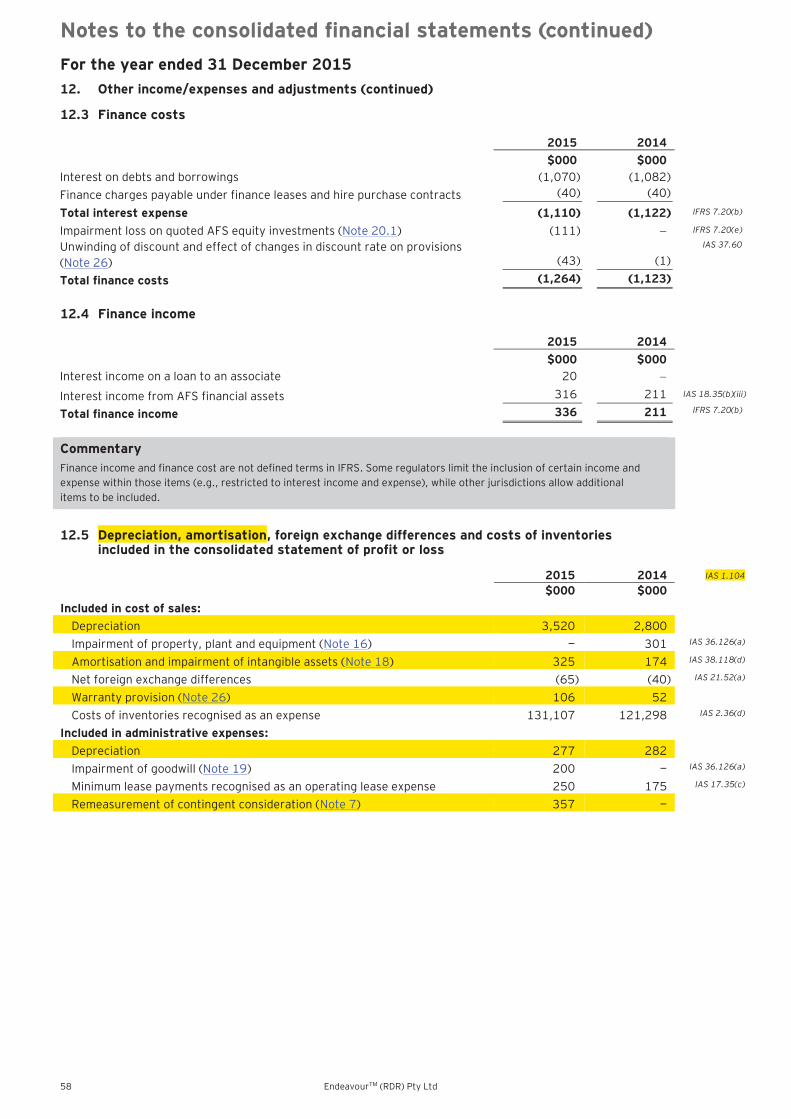

Finance costs 12.3 (1,264) (1,123) IAS 1.82(b), IFRS 7.20

Finance income 12.4 336 211 IAS 1.82(a)

Share of profit of an associate and a joint venture 9,10 671 638 IAS 1.82(c)

Profit before tax from continuing operations 11,108 8,880 IAS 1.85

Income tax expense 14 (3,098) (2,233) IAS 1.82(d), IAS 12.77

Profit for the year from continuing operations 8,010 6,647 IAS 1.85

Discontinued operations Profit/(loss) after tax for the year from discontinued operations 13 220 (188)

IAS 1.82 (ea)

IFRS 5.33(a)

Profit for the year 8,230 6,459 IAS 1.81A(a)

Attributable to:

Equity holders of the parent 7,942 6,220 IAS 1.81B (a) (ii)

Non-controlling interests 288 239 IAS 1.81B (a)(i)

8,230 6,459

Earnings per share 15 IAS 33.66 Basic, profit for the year attributable to ordinary equity holders of the parent $0.38 $0.33 Diluted, profit for the year attributable to ordinary equity holders of the parent

$0.38 $0.32

Earnings per share for continuing operations 15

Basic, profit from continuing operations attributable to ordinary equity holders of the parent

$0.37 $0.34

Diluted, profit from continuing operations attributable to ordinary equity holders of the parent

$0.37 $0.33

* Certain amounts shown here do not correspond to the 2014 financial statements and reflect adjustments made, refer to Note 2.5.

4 EndeavourTM (RDR) Pty Ltd

Consolidated statement of profit or loss (continued) For the year ended 31 December 2015

Commentary IAS 1.10 suggests titles for the primary financial statements, such as ‘statement of profit or loss and other comprehensive income’ or ‘statement of financial position’. Entities are, however, permitted to use other titles, such as ‘income statement’ or ‘balance sheet’. The Group applies the titles suggested in IAS 1.

There is no specific requirement to identify restatements to prior period financial statements on the face of the financial statements. IAS 8 requires details to be provided only in the notes. The term ‘restatement’ is used here to refer to retrospective application of accounting policies, correction of errors, and reclassifications collectively. The Group illustrates how an entity may supplement the requirements of IAS 8 so that it is clear to the reader that amounts in the prior period financial statements have been adjusted in comparative period(s) of the current period financial statements. It should be noted that the fact that the comparative information is restated does not necessarily mean that there were errors and omissions in the previous financial statements. Restatements may also arise for other reasons, for example, retrospective application of a new accounting policy.

IAS 1.82(a) requires disclosure of total revenue as a line item on the face of the statement of profit or loss. The Group also presents the various types of revenue on the face of the statement of profit or loss in accordance with IAS 1.85.

IAS 1.99 requires expenses to be analysed either by their nature or by their function within the statement of profit or loss, whichever provides information that is reliable and more relevant. If expenses are analysed by function, information about the nature of expenses must be disclosed in the notes. The Group has presented the analysis of expenses by function. In Appendix 2, the consolidated statement of profit or loss is presented with an analysis of expenses by nature.

The Group presents operating profit in the statement of profit or loss; this is not required by IAS 1. The terms ‘operating profit’ or ‘operating income’ are not defined in IFRS. IAS 1.BC56 states that the IASB recognises that an entity may elect to disclose the results of operating activities, or a similar line item, even though this term is not defined. The entity should ensure the amount disclosed is representative of activities that would normally be considered to be ‘operating’. For instance, “it would be inappropriate to exclude items clearly related to operations (such as inventory write-downs and restructuring and relocation expenses) because they occur irregularly or infrequently or are unusual in amount. Similarly, it would be inappropriate to exclude items on the grounds that they do not involve cash flows, such as depreciation and amortisation expenses” (IAS 1.BC56). In practice, other titles, such as EBIT, are sometimes used to refer to an operating result.

The Group has presented its share of profit of an associate and joint venture using the equity method under IAS 28 Investments in Associates and Joint Ventures after the line-item ‘operating profit’. IAS 1.82(c) requires ‘share of the profit or loss of associates and joint ventures accounted for using the equity method’ to be presented in a separate line item on the face of the statement profit or loss. In complying with this requirement, the Group combines the share of profit or loss from associates and joint ventures in one line item. Regulators or standard-setters in certain jurisdictions recommend or accept share of the profit/loss of equity method investees being presented with reference to whether the operations of the investees are closely related to that of the reporting entity. This may result in the share of profit/loss of certain equity method investees being included in the operating profit, while the share of profit/loss of other equity method investees being excluded from operating profit. In other jurisdictions, regulators or standard-setters believe that IAS 1.82(c) requires that share of profit/loss of equity method investees be presented as one line item (or, alternatively, as two or more adjacent line items, with a separate line for the sub-total). This may cause diversity in practice.

IAS 33.68 requires presentation of basic and diluted earnings per share (EPS) for discontinued operations either on the face of the statement of profit or loss or in the notes to the financial statements. The Group has elected to show this information with other disclosures required for discontinued operations in Note 13 and to show the EPS information for continuing operations on the face of the statement of profit or loss.

EndeavourTM (RDR) Pty Ltd 5

Consolidated statement of other comprehensive income For the year ended 31 December 2015

2015 2014

IAS 1.49 IAS 1.51(c)

IAS 1.81A IAS 1.10(b)

Restated* IAS 8.28

Notes $000 $000 IAS 1.51(d),(e)

IAS 1.90 IAS 12.61A

Profit for the year 8,230 6,459 IAS 1.81A (a)

Other comprehensive income IAS 1.82A

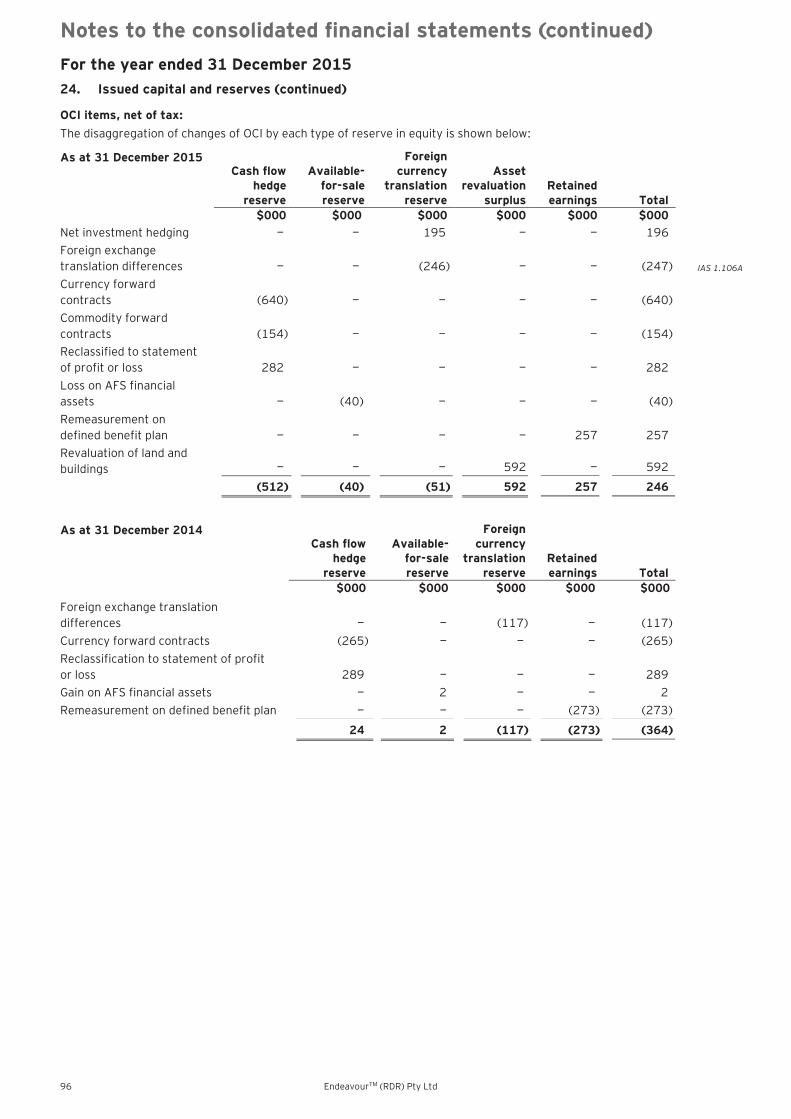

Other comprehensive income to be reclassified to profit or loss in subsequent periods (net of tax):

Net gain on hedge of a net investment 195 IAS 39.102(a)

Exchange differences on translation of foreign operations (246) (117) IAS 21.32

IAS 21.52(b)

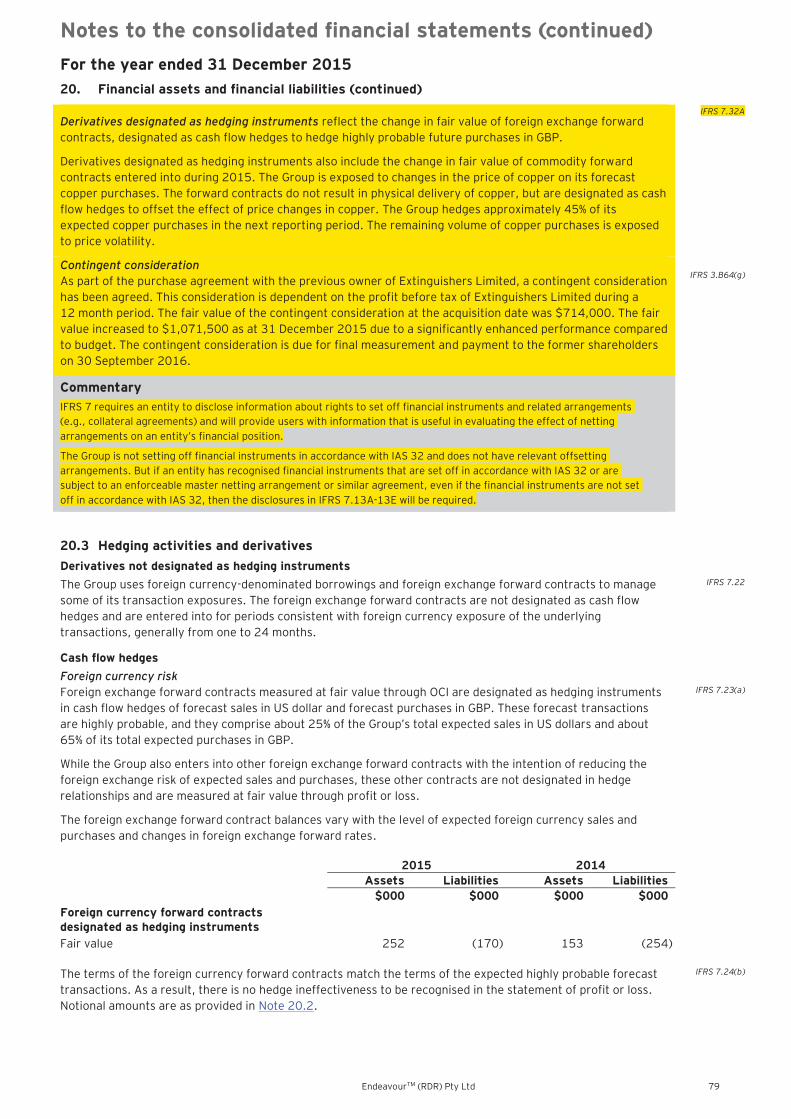

Net (loss)/gain on cash flow hedges 24 (512) 24 IFRS 7.23(c)

Net (loss)/gain on available-for-sale financial assets 24 (40) 2 IFRS 7.20(a)(ii)

Income tax relating to these items 155 (10) AASB 112.RDR.81.1

Net other comprehensive loss to be reclassified to profit or loss in subsequent periods (603) (91)

IAS 1.82A

Other comprehensive income not to be reclassified to profit or loss in subsequent periods (net of tax): IAS 19.120(c)

IAS 19.122 Remeasurement gains (losses) on defined benefit plans 29 257 (273) Revaluation of land and buildings 16 592 IAS 16.39

Income tax relating to these items (366) 116 AASB 112.RDR.81.1

Net other comprehensive income/(loss) not to be reclassified to profit or loss in subsequent periods 849 (273)

IAS 1.82A

Other comprehensive income/(loss) for the year, net of tax 246 (364) IAS 1.81A(b)

Total comprehensive income for the year, net of tax 8,476 6,095 IAS 1.81A(c)

Attributable to: Equity holders of the parent 8,188 5,856 IAS 1.81B (b) (ii)

Non-controlling interests 288 239 IAS 1.81B (b) (i)

8,476 6,095

* Certain amounts shown here do not correspond to the 2014 financial statements and reflect adjustments made, refer to Note 2.5.

6 EndeavourTM (RDR) Pty Ltd

Consolidated statement of other comprehensive income (continued) For the year ended 31 December 2015

Commentary The Group has elected to present two statements, a statement of profit or loss and a statement of other comprehensive income (OCI), rather than a single statement of comprehensive income combining the two elements. If a two-statement approach is adopted, the statement of profit or loss must be followed directly by the statement of OCI.

There is no specific requirement to identify restatements to prior period financial statements on the face of the financial statements. IAS 8 requires details to be provided only in the notes. The Group illustrates how an entity may supplement the requirements of IAS 8 so that it is clear to the reader that amounts in the prior period financial statements have been adjusted in comparative period(s) of the current period financial statements. It should be noted that the fact that the comparative information is restated does not necessarily mean that there were errors and omission in the previous financial statements. Restatements may also arise due to other instances, for example, retrospective application of a new accounting policy.

The different components of OCI are presented on a net basis in the statement above. Therefore, an additional note is required to separately present the amount of reclassification adjustments and current year gains or losses (see Note 12.8). Alternatively, the individual components could have been presented within the statement of OCI.

An entity applying Australian Accounting Standards – Reduced Disclosure Requirements shall disclose the aggregate amount of current and deferred income tax relating to items recognised in other comprehensive income (AASB 112 RDR.81.1).

The Group has elected to present the deferred tax effects net on an individual basis. Therefore, additional note disclosures are required and provided in Note 14.

Remeasurement gains and losses on defined benefit plans are recognised in OCI and transferred immediately to retained earnings (see IAS 1.96 and IAS 19.122).

IAS 1.82A requires that items that will be reclassified subsequently to profit or loss, when specific conditions are met, must be grouped on the face of the statement of OCI. Similarly, items that will not be reclassified must also be grouped together. In order to make these disclosures, an entity must analyse whether its OCI items are eligible to be subsequently reclassified to profit or loss under IFRS.

Under the requirements of IAS 1.82A and the Implementation Guidance to IAS 1, entities must present the share of the OCI items of equity method investees (i.e., associates and joint ventures), in aggregate as single line items within the ’to be reclassified’ and the ‘not to be reclassified’ groups. The Group’s associate and joint venture do not have OCI items and as such, these disclosures do not apply.

EndeavourTM (RDR) Pty Ltd 7

Consolidated statement of financial position As at 31 December 2015

2015 2014 As at

1 January 2014

IAS 1.10(a) IAS 1.10(f)

IAS 1.49, IAS 1.51(c)

Restated* Restated* IAS 8.28

Notes $000 $000 $000 IAS 1.51(d),(e)

Assets IAS 1.40A, IAS 1.40B

Current assets IAS 1.60, IAS 1.66

Cash and short-term deposits 23 17,112 14,916 11,066 IAS 1.54(i)

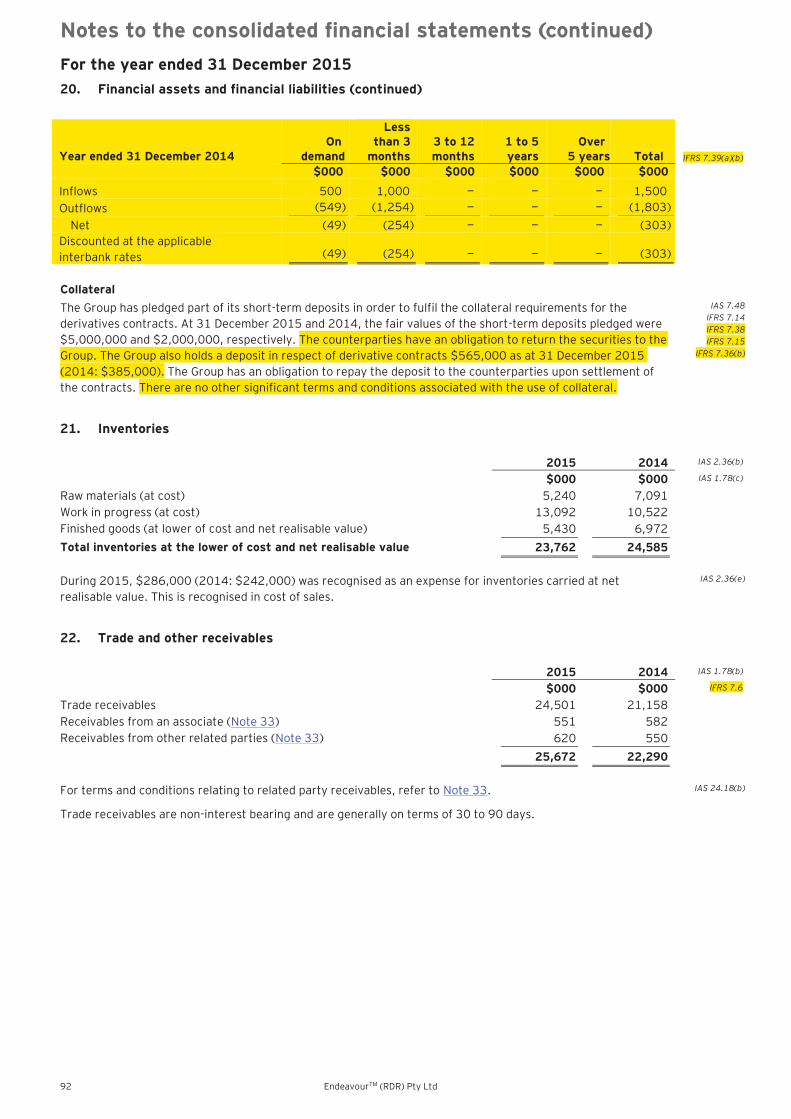

Inventories 21 23,762 24,585 26,563 IAS 1.54(g)

Trade and other receivables 22 25,672 22,290 24,037 IAS 1.54(h)

Prepayments 244 165 226 IAS 1.55

Other current financial assets 20 551 153 137 IAS 1.54(d), IFRS 7.8

67,341 62,109 62,029

Assets held for distribution 13 13,554 — — IAS 1.54(j), IFRS 5.38

80,895 62,109 62,029

Non-current assets IAS 1.60

Property, plant and equipment 16 32,979 24,329 18,940 IAS 1.54(a)

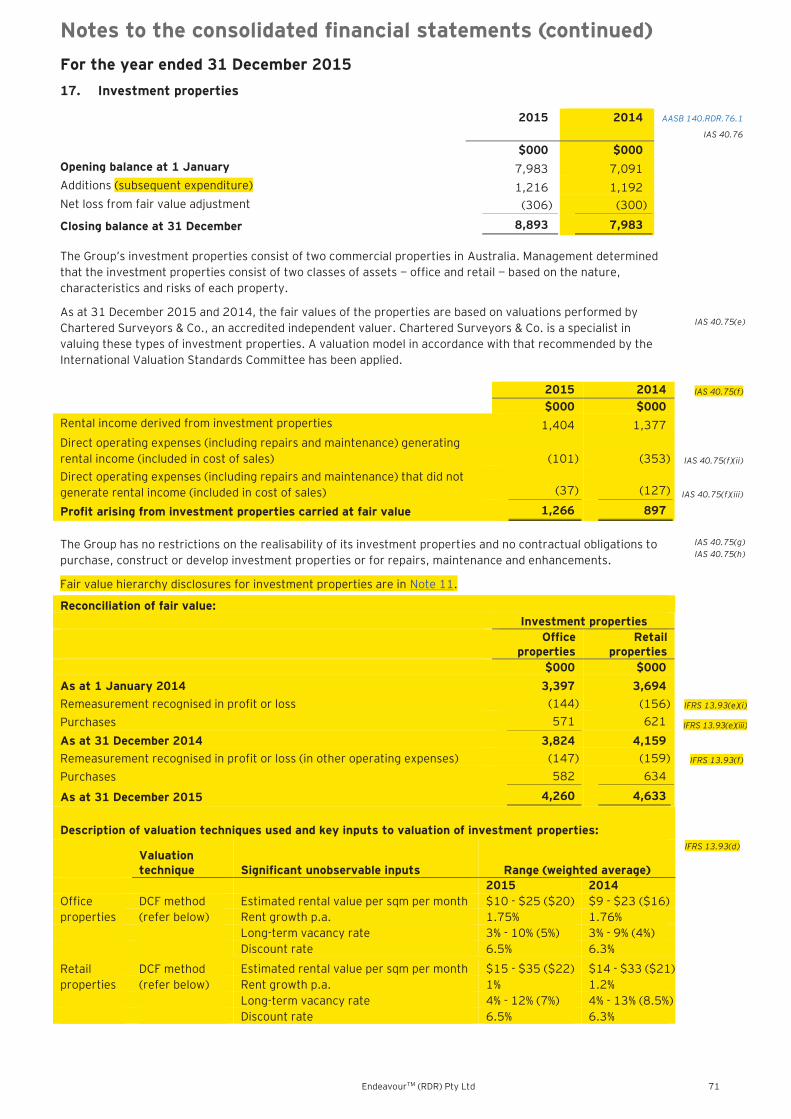

Investment properties 17 8,893 7,983 7,091 IAS 1.54(b)

Intangible assets 18 6,019 2,461 2,114 IAS 1.54(c)

Investment in an associate and a joint venture 9,10 3,187 2,516 1,878 IAS 1.54(e), IAS 28.38

Non-current financial assets 20 6,425 3,491 3,269 IAS 1.54(d), IFRS 7.8

Deferred tax assets 14 383 365 321 IAS 1.54(o), IAS 1.56

57,886 41,145 33,613

Total assets 138,781 103,254 95,642

Liabilities and equity Current liabilities IAS 1.60, IAS 1.69

Trade and other payables 31 19,444 20,730 19,850 IAS 1.54(k)

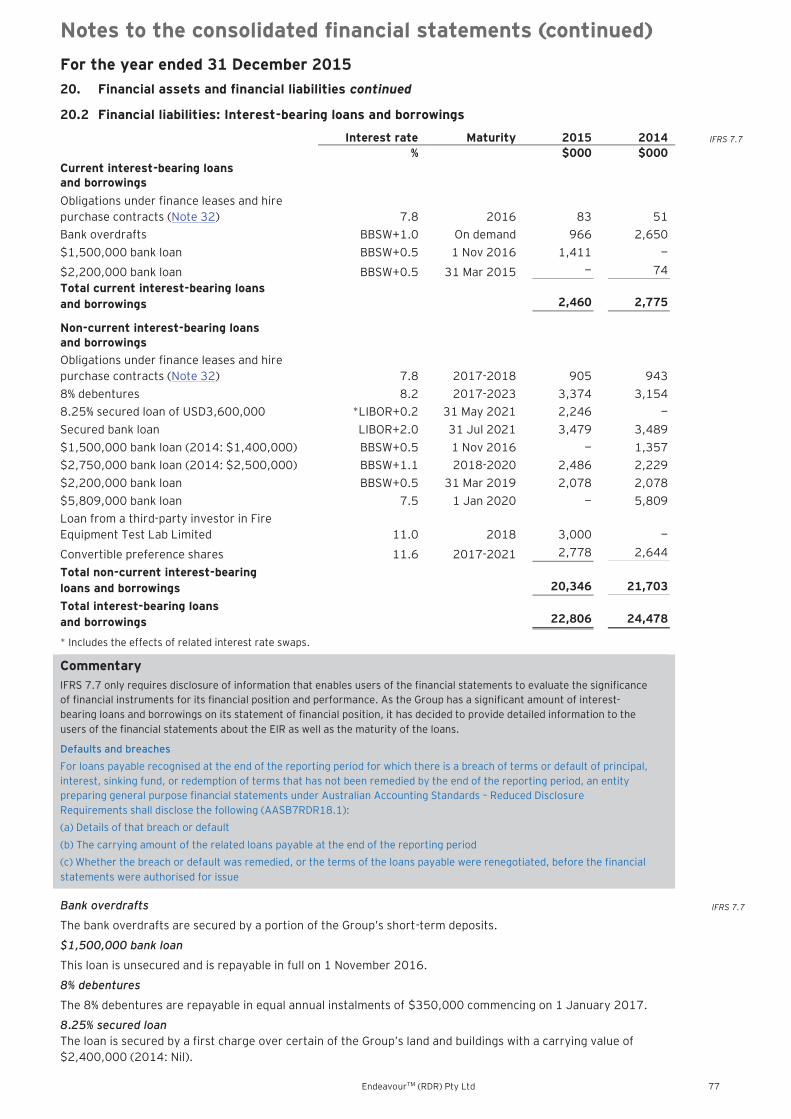

Interest-bearing loans and borrowings 20 2,460 2,775 4,555 IAS 1.54(m), IFRS 7.8(g)

Other current financial liabilities 20 3,040 303 303 IAS 1.54(m), IFRS 7.8

Government grants 27 149 151 150 IAS 1.55, IAS 20.24

Deferred revenue 28 220 200 190 IAS 1.55

Income tax payable 3,511 3,563 4,325 IAS 1.54(n)

Employee benefit liabilities 29 28 25 10

Provisions 26 822 73 30 IAS 1.54(l)

Non-cash distribution liability 25 410 — —

30,084 27,820 29,413 Liabilities directly associated with the assets held for distribution 13 13,125 — — IAS 1.54(p), IFRS 5.38

43,209 27,820 29,413

Non-current liabilities IAS 1.60

Interest-bearing loans and borrowings 20 20,346 21,703 19,574 IAS 1.54(m)

Other non-current financial liabilities 20 806 — — IAS 1.54(m), IFRS 7.8

Provisions 26 1,926 58 37 IAS 1.54(l)

Government grants 27 3,300 1,400 795 IAS 20.24

Deferred revenue 28 196 165 174 IAS 1.55

Net employee defined benefit liabilities 29 3,074 2,996 2,549 IAS 1.55, IAS 1.78(d)

Other liabilities 263 232 212 IAS 1.55

Deferred tax liabilities 14 2,931 1,089 1,083 IAS 1.54(o), IAS 1.56

32,842 27,643 24,424

Total liabilities 76,051 55,463 53,837

8 EndeavourTM (RDR) Pty Ltd

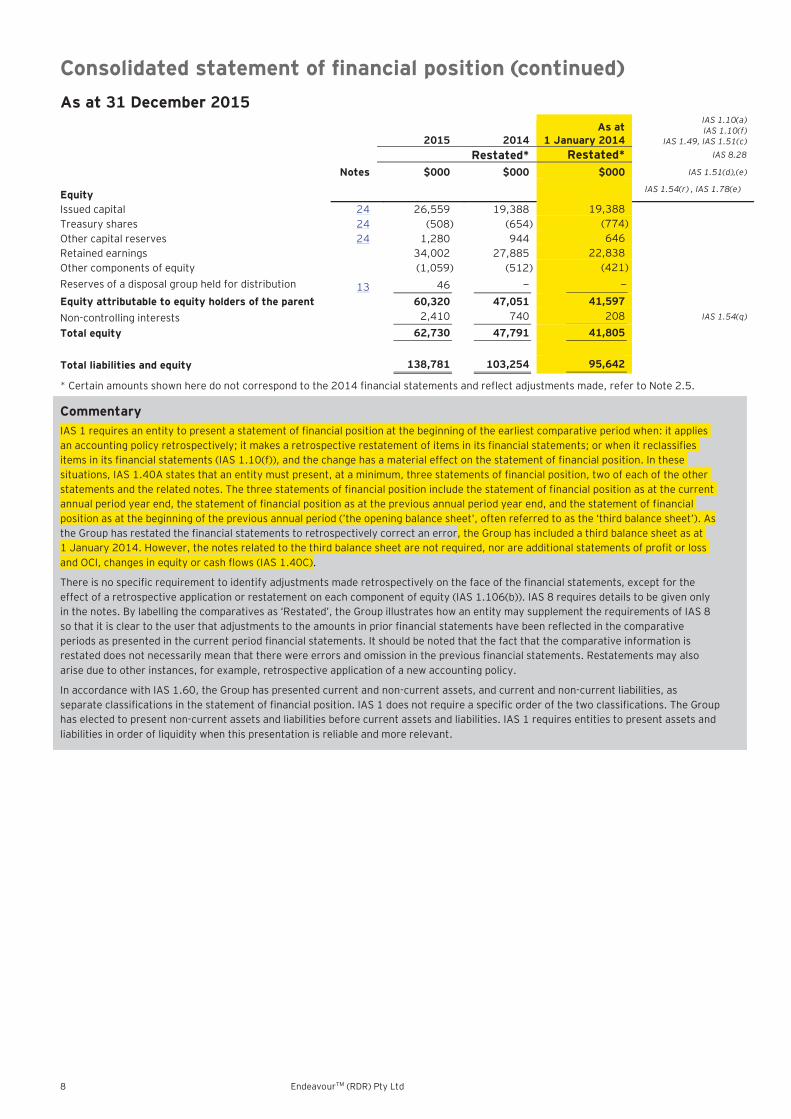

Consolidated statement of financial position (continued) As at 31 December 2015

2015 2014 As at

1 January 2014

IAS 1.10(a) IAS 1.10(f)

IAS 1.49, IAS 1.51(c)

Restated* Restated* IAS 8.28

Notes $000 $000 $000 IAS 1.51(d),(e)

Equity IAS 1.54(r) , IAS 1.78(e)

Issued capital 24 26,559 19,388

19,388 Treasury shares 24 (508) (654) (774)

Other capital reserves 24 1,280 944 646

Retained earnings 34,002 27,885 22,838

Other components of equity (1,059) (512) (421)

Reserves of a disposal group held for distribution 13 46 — —

Equity attributable to equity holders of the parent 60,320 47,051 41,597 Non-controlling interests 2,410 740 208 IAS 1.54(q)

Total equity 62,730 47,791 41,805 Total liabilities and equity 138,781 103,254 95,642

* Certain amounts shown here do not correspond to the 2014 financial statements and reflect adjustments made, refer to Note 2.5.

Commentary IAS 1 requires an entity to present a statement of financial position at the beginning of the earliest comparative period when: it applies an accounting policy retrospectively; it makes a retrospective restatement of items in its financial statements; or when it reclassifies items in its financial statements (IAS 1.10(f)), and the change has a material effect on the statement of financial position. In these situations, IAS 1.40A states that an entity must present, at a minimum, three statements of financial position, two of each of the other statements and the related notes. The three statements of financial position include the statement of financial position as at the current annual period year end, the statement of financial position as at the previous annual period year end, and the statement of financial position as at the beginning of the previous annual period (’the opening balance sheet’, often referred to as the ‘third balance sheet’). As the Group has restated the financial statements to retrospectively correct an error, the Group has included a third balance sheet as at 1 January 2014. However, the notes related to the third balance sheet are not required, nor are additional statements of profit or loss and OCI, changes in equity or cash flows (IAS 1.40C).

There is no specific requirement to identify adjustments made retrospectively on the face of the financial statements, except for the effect of a retrospective application or restatement on each component of equity (IAS 1.106(b)). IAS 8 requires details to be given only in the notes. By labelling the comparatives as ‘Restated’, the Group illustrates how an entity may supplement the requirements of IAS 8 so that it is clear to the user that adjustments to the amounts in prior financial statements have been reflected in the comparative periods as presented in the current period financial statements. It should be noted that the fact that the comparative information is restated does not necessarily mean that there were errors and omission in the previous financial statements. Restatements may also arise due to other instances, for example, retrospective application of a new accounting policy.

In accordance with IAS 1.60, the Group has presented current and non-current assets, and current and non-current liabilities, as separate classifications in the statement of financial position. IAS 1 does not require a specific order of the two classifications. The Group has elected to present non-current assets and liabilities before current assets and liabilities. IAS 1 requires entities to present assets and liabilities in order of liquidity when this presentation is reliable and more relevant.

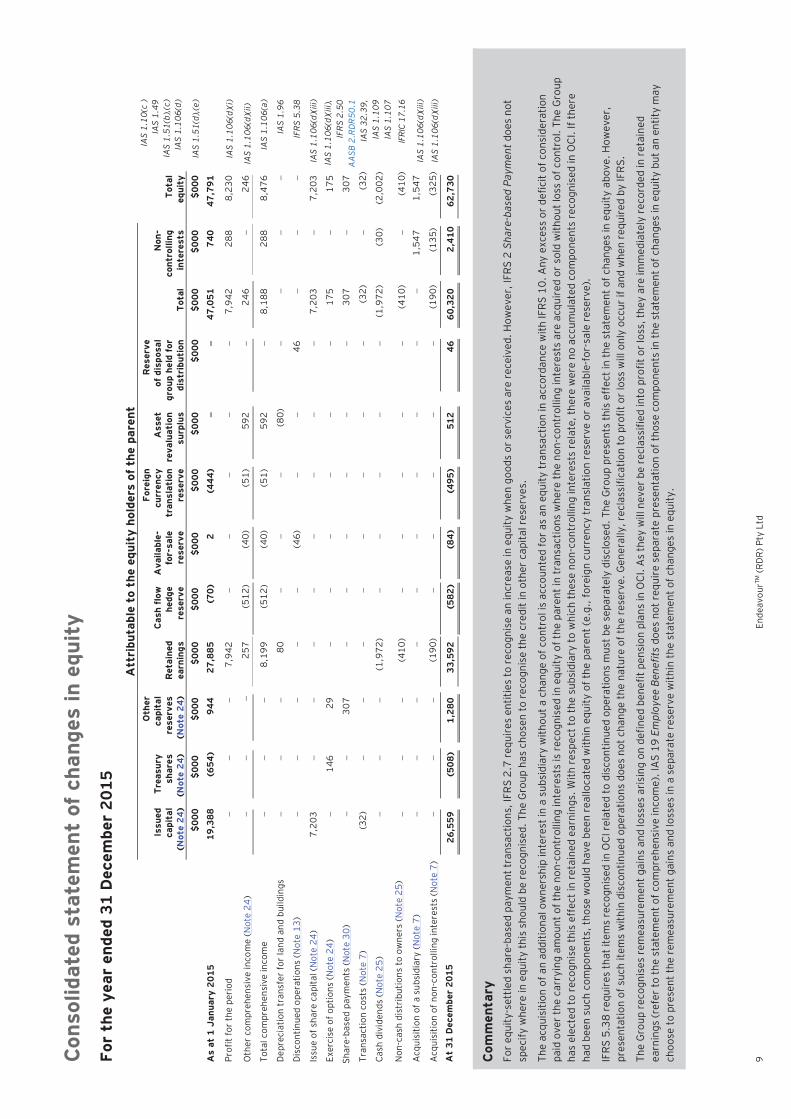

9 En

deav

ourTM

(RD

R) P

ty L

td

Cons

olid

ated

sta

tem

ent

of c

hang

es in

equ

ity

For

the

year

end

ed 3

1 D

ecem

ber

2015

A

ttri

buta

ble

to t

he e

quit

y ho

lder

s of

the

par

ent

Issu

ed

capi

tal

(Not

e 24

)

Trea

sury

sh

ares

(N

ote

24)

Oth

er

capi

tal

rese

rves

(N

ote

24)

Ret

aine

d ea

rnin

gs

Cas

h flo

w

hedg

e re

serv

e

Ava

ilabl

e-fo

r-sa

le

rese

rve

Fore

ign

curr

ency

tr

ansl

atio

n re

serv

e

Ass

et

reva

luat

ion

surp

lus

Res

erve

of

dis

posa

l gr

oup

held

for

di

stri

buti

on

Tota

l

Non

-co

ntro

lling

in

tere

sts

Tota

l eq

uity

IAS

1.10

(c )

IAS

1.49

IAS

1.51

(b),(

c)IA

S 1.

106(

d)

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

IA

S 1.

51(d

),(e)

As

at 1

Jan

uary

201

5 19

,388

(6

54)

944

27,8

85

(70)

2

(444

)

47

,051

74

0 47

,791

Prof

it fo

r th

e pe

riod

7,94

2

7,94

2 28

8 8,

230

IAS

1.10

6(d)

(i)

Oth

er c

ompr

ehen

sive

inco

me

(Not

e 24

)

257

(512

) (4

0)

(51)

59

2

246

24

6 IA

S 1.

106(

d)(ii

)

Tota

l com

preh

ensi

ve in

com

e

8,19

9 (5

12)

(40)

(5

1)

592

8,

188

288

8,47

6 IA

S 1.

106(

a)

Dep

reci

atio

n tr

ansf

er fo

r la

nd a

nd b

uild

ings

80

(8

0)

IAS

1.96

Dis

cont

inue

d op

erat

ions

(Not

e 13

)

(46)

46

IFRS

5.3

8

Issu

e of

sha

re c

apita

l (N

ote

24)

7,20

3

7,

203

7,

203

IAS

1.10

6(d)

(iii)

Exer

cise

of o

ptio

ns (N

ote

24)

14

6 29

17

5

175

IAS

1.10

6(d)

(iii),

IFRS

2.5

0A

ASB

2.R

DR50

.1IA

S 32

.39,

IAS

1.10

9IA

S 1.

107

IFRI

C 17

.16

Shar

e-ba

sed

paym

ents

(Not

e 30

)

30

7

30

7

307

Tran

sact

ion

cost

s (N

ote

7)

(32)

(3

2)

(3

2)

Cash

div

iden

ds (N

ote

25)

(1

,972

)

(1,9

72)

(30)

(2

,002

)

Non

-cas

h di

stri

butio

ns to

ow

ners

(Not

e 25

)

(410

)

(410

)

(410

) A

cqui

sitio

n of

a s

ubsi

diar

y (N

ote

7)

1,54

7 1,

547

IAS

1.10

6(d)

(iii)

IAS

1.10

6(d)

(iii)

Acq

uisi

tion

of n

on-c

ontr

ollin

g in

tere

sts

(Not

e 7)

(190

)

(190

) (1

35)

(325

)

At

31 D

ecem

ber

2015

26

,559

(5

08)

1,28

0 33

,592

(5

82)

(84)

(4

95)

512

46

60,3

20

2,41

0 62

,730

Com

men

tary

Fo

r eq

uity

-set

tled

shar

e-ba

sed

paym

ent t

rans

actio

ns, I

FRS

2.7

requ

ires

ent

ities

to r

ecog

nise

an

incr

ease

in e

quity

whe

n go

ods

or s

ervi

ces

are

rece

ived

. How

ever

, IFR

S 2

Shar

e-ba

sed

Paym

ent d

oes

not

spec

ify w

here

in e

quity

this

sho

uld

be r

ecog

nise

d. T

he G

roup

has

cho

sen

to r

ecog

nise

the

cred

it in

oth

er c

apita

l res

erve

s.

The

acqu

isiti

on o

f an

addi

tiona

l ow

ners

hip

inte

rest

in a

sub

sidi

ary

with

out a

cha

nge

of c

ontr

ol is

acc

ount

ed fo

r as

an

equi

ty tr

ansa

ctio

n in

acc

orda

nce

with

IFRS

10.

Any

exc

ess

or d

efic

it of

con

side

ratio

n pa

id o

ver

the

carr

ying

am

ount

of t

he n

on-c

ontr

ollin

g in

tere

sts

is r

ecog

nise

d in

equ

ity o

f the

par

ent i

n tr

ansa

ctio

ns w

here

the

non-

cont

rolli

ng in

tere

sts

are

acqu

ired

or

sold

with

out l

oss

of c

ontr

ol. T

he G

roup

ha

s el

ecte

d to

rec

ogni

se th

is e

ffec

t in

reta

ined

ear

ning

s. W

ith r

espe

ct to

the

subs

idia

ry to

whi

ch th

ese

non-

cont

rolli

ng in

tere

sts

rela

te, t

here

wer

e no

acc

umul

ated

com

pone

nts

reco

gnis

ed in

OCI

. If t

here

ha

d be

en s

uch

com

pone

nts,

thos

e w

ould

hav

e be

en r

eallo

cate

d w

ithin

equ

ity o

f the

par

ent (

e.g.

, for

eign

cur

renc

y tr

ansl

atio

n re

serv

e or

ava

ilabl

e-fo

r-sa

le r

eser

ve).

IFRS

5.3

8 re

quir

es th

at it

ems

reco

gnis

ed in

OCI

rel

ated

to d

isco

ntin

ued

oper

atio

ns m

ust b

e se

para

tely

dis

clos

ed. T

he G

roup

pre

sent

s th

is e

ffec

t in

the

stat

emen

t of c

hang

es in

equ

ity a

bove

. How

ever

, pr

esen

tatio

n of

suc

h ite

ms

with

in d

isco

ntin

ued

oper

atio

ns d

oes

not c

hang

e th

e na

ture

of t

he r

eser

ve. G

ener

ally

, rec

lass

ifica

tion

to p

rofit

or

loss

will

onl

y oc

cur

if an

d w

hen

requ

ired

by

IFR

S.

The

Gro

up r

ecog

nise

s re

mea

sure

men

t gai

ns a

nd lo

sses

aris

ing

on d

efin

ed b

enef

it pe

nsio

n pl

ans

in O

CI. A

s th

ey w

ill n

ever

be

recl

assi

fied

into

pro

fit o

r lo

ss, t

hey

are

imm

edia

tely

rec

orde

d in

ret

aine

d ea

rnin

gs (r

efer

to th

e st

atem

ent o

f com

preh

ensi

ve in

com

e). I

AS

19 E

mpl

oyee

Ben

efits

doe

s no

t req

uire

sep

arat

e pr

esen

tatio

n of

thos

e co

mpo

nent

s in

the

stat

emen

t of c

hang

es in

equ

ity b

ut a

n en

tity

may

ch

oose

to p

rese

nt th

e re

mea

sure

men

t gai

ns a

nd lo

sses

in a

sep

arat

e re

serv

e w

ithin

the

stat

emen

t of c

hang

es in

equ

ity.

10

Ende

avou

rTM (R

DR)

Pty

Ltd

Cons

olid

ated

sta

tem

ent

of c

hang

es in

equ

ity

(con

tinu

ed)

For

the

year

end

ed 3

1 D

ecem

ber

2014

(re

stat

ed*)

A

ttri

buta

ble

to t

he e

quit

y ho

lder

s of

the

par

ent

Issu

ed

capi

tal

(Not

e 24

)

Trea

sury

sh

ares

(N

ote

24)

Oth

er c

apit

al

rese

rves

(N

ote

24)

Ret

aine

d ea

rnin

gs

Cas

h flo

w

hedg

e re

serv

e

Ava

ilabl

e-

for-

sale

R

eser

ve

Fore

ign

curr

ency

tr

ansl

atio

n re

serv

e

Tota

l

Non

-co

ntro

lling

in

tere

sts

Tota

l eq

uity

IAS

1.10

(c )

IAS

1.49

IA

S 1.

51(b

),(c)

IA

S 8.

28

IAS

1.10

6(d)

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

IA

S 1.

51(d

),(e

)

As

at 1

Jan

uary

201

4 19

,388

(7

74)

566

23,5

38

(94)

(327

) 42

,297

20

8 42

,505

Adj

ustm

ent o

n co

rrec

tion

of e

rror

(net

of t

ax)

(Not

e 2.

5)

(7

00)

(7

00)

(7

00)

IAS

1.10

6(b)

IAS

1.11

0

As

at 1

Jan

uary

201

4 (r

esta

ted*

) 19

,388

(7

74)

566

22,8

38

(94)

(327

) 41

,597

20

8 41

,805

Prof

it fo

r th

e pe

riod

as

repo

rted

in th

e 20

14

finan

cial

sta

tem

ents

7,27

0

7,27

0 23

9 7,

509

Adj

ustm

ent o

n co

rrec

tion

of e

rror

(net

of t

ax)

(Not

e 2.

5)

(1

,050

)

(1,0

50)

(1

,050

)

Rest

ated

pro

fit fo

r th

e pe

riod

6,22

0

6,22

0 23

9 6,

459

IAS

1.10

6(d)

(i)

Oth

er c

ompr

ehen

sive

inco

me

(Not

e 24

)

(273

) 24

2

(117

) (3

64)

(3

64)

IAS

1.10

6(d)

(ii)

Tota

l com

preh

ensi

ve in

com

e

5,94

7 24

2

(117

) 5,

856

239

6,09

5 IA

S 1.

106(

a)

Exer

cise

of o

ptio

ns (N

ote

24)

12

0 80

20

0

200

IAS

1.10

6(d)

(iii),

Shar

e-ba

sed

paym

ents

(Not

e 30

)

29

8

29

8

298

IFRS

2.5

0

Div

iden

ds (N

ote

25)

(1

,600

)

(1,6

00)

(49)

(1

,649

) IA

S 1.

107

Non

-con

trol

ling

inte

rest

s ar

isin

g on

a b

usin

ess

com

bina

tion

(Not

e 7)

34

2 34

2 IA

S 1.

106(

d)(ii

i)

At

31 D

ecem

ber

2014

(re

stat

ed*)

19

,388

(6

54)

944

27,8

85

(70)

2

(444

) 47

,051

74

0 47

,791

* Ce

rtai

n am

ount

s sh

own

here

do

not c

orre

spon

d to

the

2014

fina

ncia

l sta

tem

ents

and

ref

lect

adj

ustm

ents

mad

e, re

fer

to N

ote

2.5.

C

omm

enta

ry

Ther

e is

no

spec

ific

requ

irem

ent t

o id

entif

y ad

just

men

ts m

ade

retr

ospe

ctiv

ely

on th

e fa

ce o

f the

fina

ncia

l sta

tem

ents

, exc

ept f

or th

e ef

fect

of a

ret

rosp

ectiv

e ap

plic

atio

n or

res

tate

men

t on

each

com

pone

nt

of e

quity

(IA

S 1.

106(

b)).

IAS

8 re

quir

es d

etai

ls to

be

give

n on

ly in

the

note

s. B

y la

belli

ng th

e co

mpa

rativ

es ‘R

esta

ted’

, the

Gro

up il

lust

rate

s ho

w a

n en

tity

may

sup

plem

ent t

he r

equi

rem

ents

of I

AS

8 so

that

it

is c

lear

to th

e us

er th

at a

djus

tmen

ts to

the

amou

nts

in p

rior

fina

ncia

l sta

tem

ents

hav

e be

en r

efle

cted

in th

e co

mpa

rativ

e pe

riods

as

pres

ente

d in

the

curr

ent p

erio

d fin

anci

al s

tate

men

ts. I

t sho

uld

be n

oted

th

at th

e fa

ct th

at th

e co

mpa

rativ

e in

form

atio

n is

res

tate

d do

es n

ot n

eces

saril

y m

ean

that

ther

e w

ere

erro

rs a

nd m

ater

ial o

mis

sion

s in

the

prev

ious

fina

ncia

l sta

tem

ents

. Res

tate

men

ts m

ay a

lso

aris

e du

e to

ot

her

inst

ance

s, fo

r ex

ampl

e, r

etro

spec

tive

appl

icat

ion

of a

new

acc

ount

ing

polic

y.

EndeavourTM (RDR) Pty Ltd 11

Consolidated statement of cash flows For the year ended 31 December 2015

2015 2014 IAS 1.10(d) IAS 1.51(c)

Note $000 $000 IAS 1.51(d),(e)

Operating activities IAS 7.10, IAS 7.18(a)

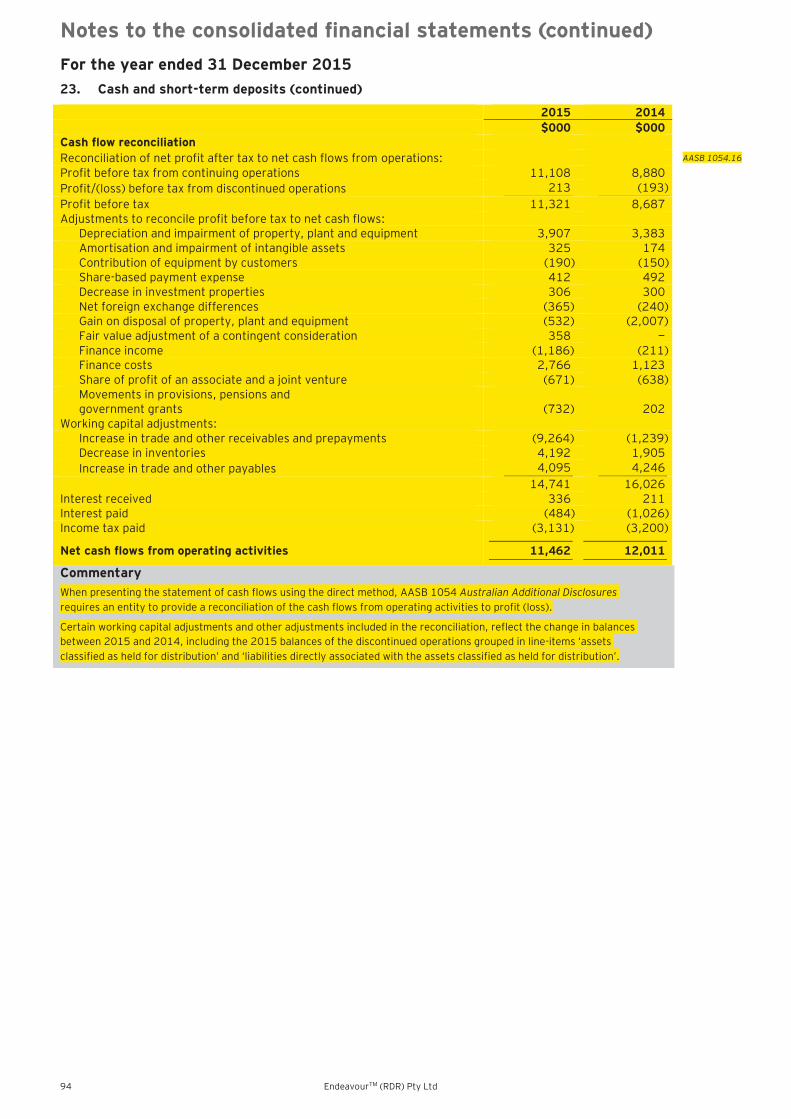

Receipts from customers 227,113 235,776 Payments to suppliers (176,557) (184,703) Payments to employees (35,815) (35,048) Interest received 336 211 IAS 7.31 Interest paid (484) (1,025) IAS 7.31 Income tax paid (3,131) (3,200) IAS 7.35

Net cash flows from operating activities 11,462 12,011

Investing activities IAS 7.10, IAS 7.21 Proceeds from sale of property, plant and equipment 1,990 2,319 IAS 7.16(b)

Purchase of property, plant and equipment 16 (10,162) (7,672) IAS 7.16(a)

Purchase of investment properties 17 (1,216) (1,192) IAS 7.16(a)

Purchase of financial instruments (3,054) (225) IAS 7.16(c)

Proceeds from sale of financial instruments 145 IAS 7.16(d)

Development expenditures 18 (587) (390) IAS 7.16(a)

Acquisition of a subsidiary, net of cash acquired 7 230 (1,450) IAS 7.39

Receipt of government grants 27 2,951 642

Net cash flows used in investing activities (9,848) (7,823)

Financing activities IAS 7.10, IAS 7.21

Proceeds from exercise of share options 175 200 IAS 7.17(a)

Acquisition of non-controlling interests 7 (325) IAS 7.42A

Transaction costs on issue of shares 24 (32) IAS 7.17(a)

Payment of finance lease liabilities (51) (76) IAS 7.17(e)

Proceeds from borrowings 5,577 2,645 IAS 7.17(c)

Repayment of borrowings (122) (1,684) IAS 7.17(d)

Dividends paid to equity holders of the parent 25 (1,972) (1,600) IAS 7.31

Dividends paid to non-controlling interests (30) (49) IFRS 12.B10(a)

Net cash flows from/(used in) financing activities 3,220 (564)

Net increase in cash and cash equivalents 4,834 3,624

Net foreign exchange difference 340 326 IAS 7.28

Cash and cash equivalents at 1 January 12,266 8,316

Cash and cash equivalents at 31 December 23 17,440 12,266 IAS 7.45

Commentary IAS 7.18 allows entities to report cash flows from operating activities using either the direct method or the indirect method. The Group presents its cash flows using the direct method.

There is no specific requirement to identify adjustments made retrospectively on the face of the financial statements, except for the effect of a retrospective application or restatement on each component of equity (IAS 1.106(b)). IAS 8 requires details to be given only in the notes. By labelling the comparatives ‘Restated’, the Group illustrates how an entity may supplement the requirements of IAS 8 so that it is clear to the user that adjustments to the amounts in prior financial statements have been reflected in the comparative periods as presented in the current period financial statements.

The Group has reconciled profit before tax to net cash flows from operating activities. However, reconciliation from profit after tax is also acceptable under IAS 7 Statement of Cash Flows.

IAS 7.33 permits interest paid to be shown as operating or financing activities and interest received to be shown as operating or investing activities, as deemed relevant for the entity. The Group has elected to classify interest received and interest paid as cash flows from operating activities.

12 EndeavourTM (RDR) Pty Ltd

Notes to the consolidated financial statements For the year ended 31 December 2015 1. Corporate information IAS 1.10(e)

IAS 1.49

The consolidated financial statements of Endeavour (RDR) Pty Ltd and its subsidiaries (collectively, the Group) for the year ended 31 December 2015 were authorised for issue in accordance with a resolution of the directors on 25 February 2016. Endeavour (RDR) Pty Ltd (the Company or the parent) is a for profit company limited by shares incorporated in Australia whose shares are publicly traded on the Australian Stock Exchange. The ultimate parent of Endeavour (RDR) Pty Ltd is S.J Limited which owns 52.85% of the ordinary shares.

The Group is principally engaged in the provision of fire prevention and electronics equipment and services and the management of investment property (see Note 4). The Group’s principal place of business is Bush Avenue, Mulberry Park, Australia. Further information on the nature of the operations and principal activities of the Group is provided in the directors’ report. Information on the Group’s structure is provided in Note 6. Information on other related party relationships of the Group is provided in Note 33.

IAS 1.113

IAS 1.51(a) IAS 1.51(b)

IAS 1.51(c)

IAS 1.138(a) IAS 10.17

AASB 1054.8(b)

IAS 1.138(b) IAS 1.138(c)

2. Significant accounting policies

Commentary The identification of an entity’s significant accounting policies is an important aspect of the financial statements. IAS 1.117 requires the significant accounting policies disclosures to summarise the measurement basis (or bases) used in preparing the financial statements, and the other accounting policies used that are relevant to an understanding of the financial statements. The significant accounting policies disclosed in this note is to illustrate some of the more commonly applicable disclosures. However, it is essential that entities consider their specific circumstances when determining which accounting policies are significant and relevant to be included.

2.1 Basis of preparation

The financial report is a general purpose financial report, which has been prepared in accordance with the requirements of the Corporations Act 2001, Australian Accounting Standards and other authoritative pronouncements of the Australian Accounting Standards Board.

IAS 1.16 AASB 1054.8(a)

AASB 1054.9

The financial report has been prepared on a historical cost basis, except for investment properties, land and buildings classified as property, plant and equipment, derivative financial instruments, available-for-sale (AFS) financial assets, contingent consideration and non-cash distribution liability that have been measured at fair value. The carrying values of recognised assets and liabilities that are designated as hedged items in fair value hedges that would otherwise be carried at amortised cost are adjusted to record changes in the fair values attributable to the risks that are being hedged in effective hedge relationships.

The financial report is presented in Australian dollars and all values are rounded to the nearest thousand ($000), except when otherwise indicated.

IAS 1.112(a) IAS 1.117(a)

IAS 1.51(d),(e) ASIC CO 98/100

The consolidated financial statements provide comparative information in respect of the previous period. In addition, the Group presents an additional statement of financial position at the beginning of the earliest period presented when there is a retrospective application of an accounting policy, a retrospective restatement, or a reclassification of items in financial statements. An additional statement of financial position as at 1 January 2014 is presented in these consolidated financial statements due to the correction of an error retrospectively. See Note 2.5.

IAS 1.40A

IAS 1.10 (ea)

IAS 1.38

IAS 1.38A

Compliance with International Financial Reporting Standards (IFRS)

The financial report also complies with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board.

IAS 1.16

Notes to the consolidated financial statements (continued) For the year ended 31 December 2015

EndeavourTM (RDR) Pty Ltd 13

2.1 Basis of preparation (continued)

Statement of compliance

The financial report is a general purpose financial report, which has been prepared in accordance with the requirements of the Corporations Act 2001, Australian Accounting Standards – Reduced Disclosure Requirements and other authoritative pronouncements of the Australian Accounting Standards Board. The Group is a for-profit, private sector entity which is not publicly accountable. Therefore, the consolidated financial statements for the Group are tier 2 general purpose financial statements which have been prepared in accordance with Australian Accounting Standards – Reduced Disclosure Requirements (AASB – RDRs) .

AASB 101.RDR.16.1

Commentary An entity whose financial statements comply with Australian Accounting Standards – Reduced Disclosure Requirements shall make an explicit and unreserved statement of such compliance in the notes. An entity shall not describe financial statements as complying with Australian Accounting Standards – Reduced Disclosure Requirements unless they comply with all the requirements of Australian Accounting Standards – Reduced Disclosure Requirements. Entities applying Australian Accounting Standards – Reduced Disclosure Requirements would not be able to state compliance with IFRS (AASB 101 RDR16.1).

2.2 Basis of consolidation The consolidated financial statements comprise the financial statements of the Group and its subsidiaries as at 31 December 2015. Control is achieved when the Group is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee. Specifically, the Group controls an investee if, and only if, the Group has:

► Power over the investee (i.e., existing rights that give it the current ability to direct the relevant activities of the investee)

► Exposure, or rights, to variable returns from its involvement with the investee

► The ability to use its power over the investee to affect its returns

Generally, there is a presumption that a majority of voting rights results in control. To support this presumption and when the Group has less than a majority of the voting or similar rights of an investee, the Group considers all relevant facts and circumstances in assessing whether it has power over an investee, including:

► The contractual arrangement(s) with the other vote holders of the investee

► Rights arising from other contractual arrangements

► The Group’s voting rights and potential voting rights

IFRS 10.7

IFRS 10.B38

The Group re-assesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control. Consolidation of a subsidiary begins when the Group obtains control over the subsidiary and ceases when the Group loses control of the subsidiary. Assets, liabilities, income and expenses of a subsidiary acquired or disposed of during the year are included in the consolidated financial statements from the date the Group gains control until the date the Group ceases to control the subsidiary.

IFRS 10.B80 IFRS 10.B86 IFRS 10.B99