“employment effects of a payroll-tax cut – evidence from a regional tax exemption experiment”

DESCRIPTION

“EMPLOYMENT EFFECTS OF A PAYROLL-TAX CUT – EVIDENCE FROM A REGIONAL TAX EXEMPTION EXPERIMENT” Authors: Ossi Korkeamaki and Roope Uusitalo IFAU Working Paper 2006:10 Presented by: Svetlana Parshina. Program Description. - PowerPoint PPT PresentationTRANSCRIPT

“EMPLOYMENT EFFECTS OF A PAYROLL-TAX CUT – EVIDENCE FROM A REGIONAL TAX EXEMPTION

EXPERIMENT”

Authors: Ossi Korkeamaki and Roope Uusitalo

IFAU Working Paper 2006:10

Presented by: Svetlana Parshina

Program DescriptionExperiment: abolished employer contributions to the National Pension Scheme and to the National Health Insurance for firms located in the targeted high unemployment regions (on average payroll-taxes for the eligible firms were lowered by 4.1percentage points, but maximum annual reduction was 30,000 Euro per firm).

Start: January 1st 2003.

Duration: 3 years (was extended to the end of 2009 in December 2005).

Target: 20 municipalities located in the Northern Finland – high unemployment area.

How it should work: lower wage costs demand for labor

Reduction in payroll-tax increase in wages no effect on employment

Data

Source: Register of Enterprises and Establishments by Statistics Finland (data on sales and wage bill for each plant in Finland).

Initial Sample: 2 809 firms in the target area and 7 544 in the control area.

Restrictions: Private sector firms that had a positive turnover, paid at least some wages and employed at least one worker in 2001.

Final Sample: 1 592 firms in the target area and 4 265 firms in the control area.

Simplified procedure for the tax exemption high rates of participation:

by December 2003, a starting declaration was signed by:

• 100% of eligible employers with at least 50 employees

• 90% of the eligible employers with at least five employees

• 75% of the firms with 2-4 employees

Data

Main Problem: No data for Employment, hence it is calculated as:

1. Finland Statistics: Wage bill divided by the average wages for various employee groups, adjusted for composition of employment.

2. Data from Finnish Tax Administration: list of all wages and salaries paid during the calendar year (# of employees that have received some wages from the firm during the year).

3. Data from 2 large employer organizations: Confederation of Finnish Industry and Employers (TT) and Employers Federation of the Service Industries (PT). Contain individual data on all workers in all their member firms. But both of them cover only 60% of private sector employment.

Empirical Strategy

Two-stage procedure of creating a control group:

First: Selected the “counties” that were most comparable to the target region in terms of unemployment rates, industrial structure and workforce characteristics in 2002.

Similar industry composition, unemployment and employment rates, and population structure before the beginning of experiment (+big difference with national average).

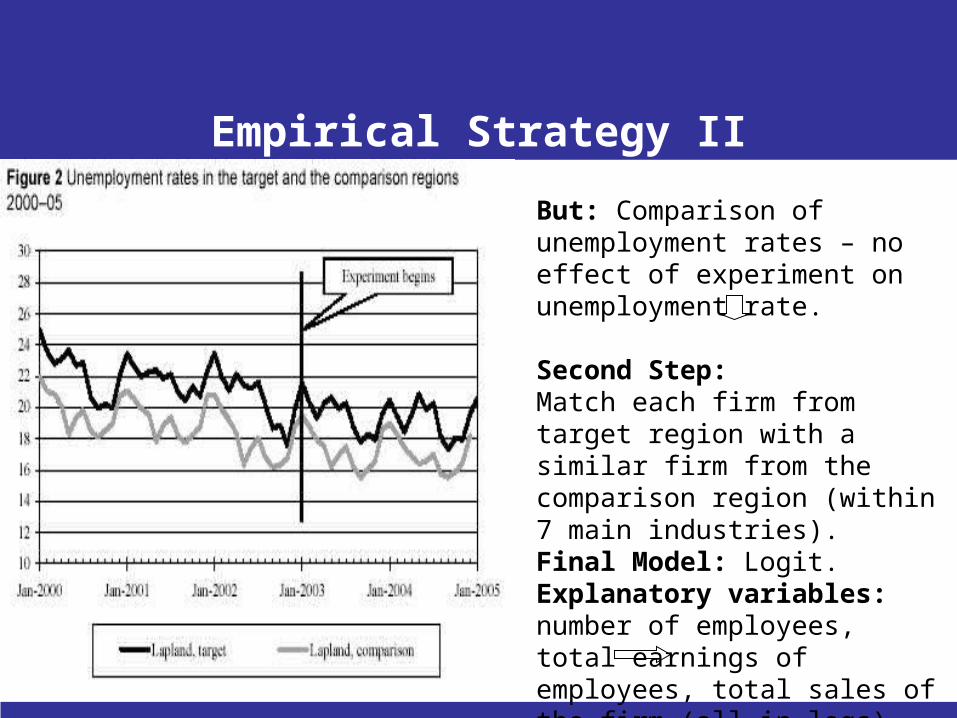

Empirical Strategy II

But: Comparison of unemployment rates – no effect of experiment on unemployment rate.

Second Step:Match each firm from target region with a similar firm from the comparison region (within 7 main industries).Final Model: Logit. Explanatory variables: number of employees, total earnings of employees, total sales of the firm (all in logs), +set of 3-digit industry codes propensity scores.

Results I (Checking for comparability btw treatment and control groups)

I. Covariate balancing II. Estimated propensity score densities for target and control region firms:

III. Pre-experiment trends in the key variables:

Results II (Employment and wage sum responses to experiment)

1. Employment growth is rather similar for both groups.

2. None of the differences is even close to being significant

3. Economic significance??? (2002-04: 0.067*1 430 firms=96 new jobs (0.8% growth in employment)).

Results III

1. Difference has mainly the “right” sign indicating stronger wage bill growth in the treatment group after the start of experiment in 2003.

2. Not significant.

Results IV

Effect differs for small and large firms?

Divide the whole sample to 4 quartiles based on firm’s average wage.

Nothing is significant.

Results VEffect on hourly wages:

(Reduced sample due to lack of data).

• Service sector: 2003 – wages grew 2% faster in the target region (statistically significant)

• Manufacturing sector: coefficients are insignificant

Conclusion

• In general reduction in the labor costs did not have a significant effect of employment growth (insignificant result is mainly due to small sample size).

• About half of the effect of the payroll tax reduction on the labor costs was offset by faster wage growth in the target region.

Do I believe in the results and could I do that better with the same data available?

Yes No(Respectively)

Do I believe in the results and could I do that better with the same data available?

1. Very thoroughly done matching

2. Separate examination for different firm size, sector and type of worker

BUT:

1. Problems with measuring Employment

small sample difficult to catch effects of reasonably small changes in payroll taxes.

2. Even within this sample there is no way to capture the variation in working hours.

3. Three years may not be a sufficiently long period for the firms to adjust their demand for labour to a relatively small change in the labour costs.

4. It is a temporary program it is likely to have a smaller effect than permanent one.