employee v. partner - · pdf file10 llc membership units $200 appreciated assets ... issuance...

TRANSCRIPT

1

EMPLOYEE V. PARTNER

Entrepreneurial Risk Permanent or Transitory Status

Related to the Performance of ServicesTax MotivatedRelative Size

2

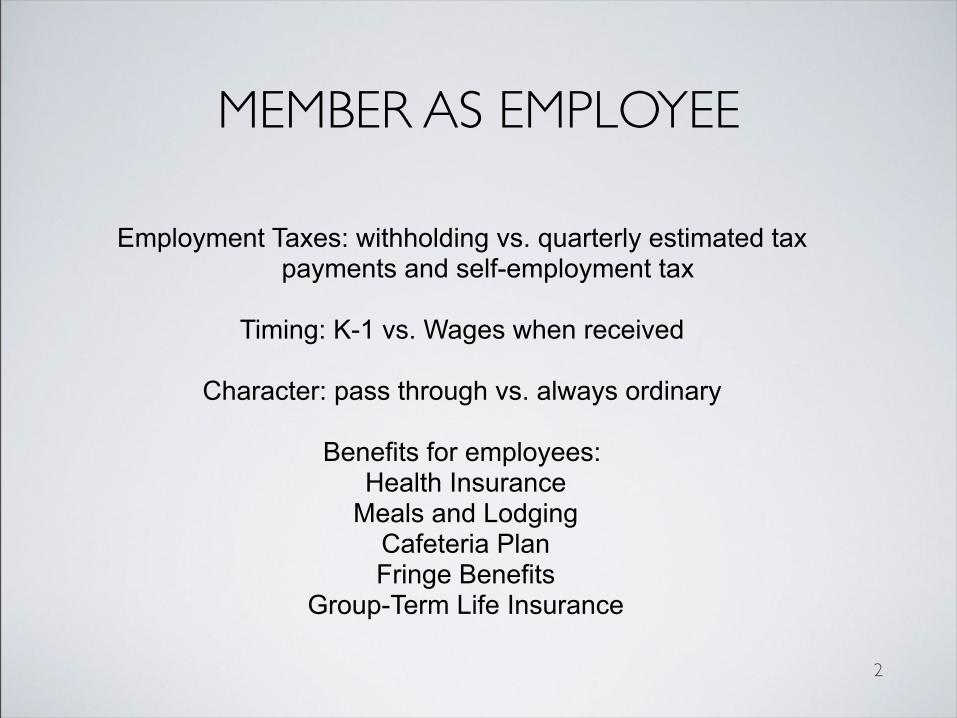

MEMBER AS EMPLOYEE

Employment Taxes: withholding vs. quarterly estimated tax payments and self-employment tax

Timing: K-1 vs. Wages when received

Character: pass through vs. always ordinary

Benefits for employees: Health Insurance

Meals and Lodging Cafeteria Plan Fringe Benefits

Group-Term Life Insurance

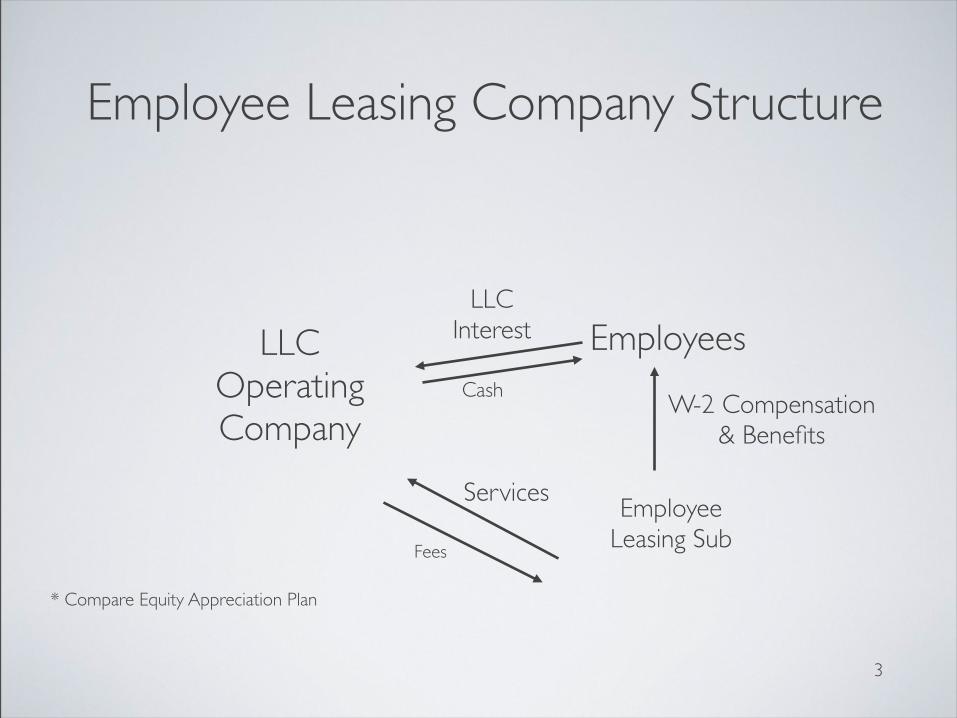

3

Employees

W-2 Compensation& Benefits

LLCInterestLLC

Operating Company

EmployeeLeasing Sub

Services

Employee Leasing Company Structure

Fees

Cash

* Compare Equity Appreciation Plan

4

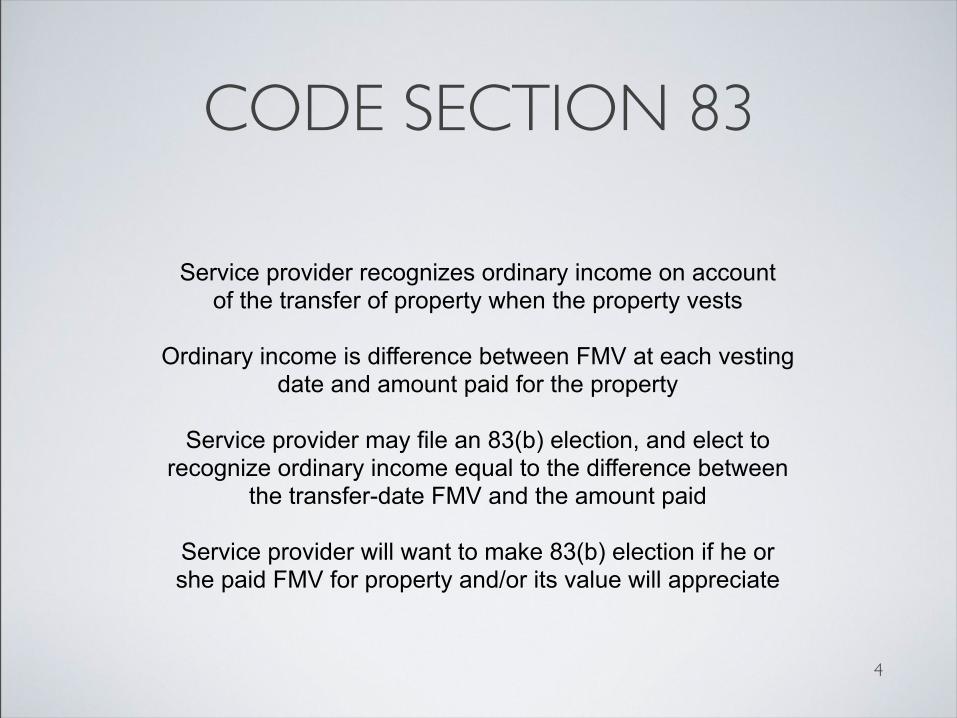

CODE SECTION 83

Service provider recognizes ordinary income on account of the transfer of property when the property vests

Ordinary income is difference between FMV at each vesting date and amount paid for the property

Service provider may file an 83(b) election, and elect to recognize ordinary income equal to the difference between

the transfer-date FMV and the amount paid

Service provider will want to make 83(b) election if he or she paid FMV for property and/or its value will appreciate

5

REV. PROC. 2001-43IRS will not tax service provider (SP) or the partnership

on grant of a non-vested profits interest if:

* The partnership and SP treat SP as the owner of the partnership interest from the date of grant;

* Neither the partnership nor any of the partners deducts any amount for the fair market value of the interest; and

* All other conditions of Rev. Proc. 93-27 are satisfied:

- interests relating to a substantially certain and predictable stream of income,

- interests disposed of within two years of receipt, and - interests in publicly traded partnerships.

No Section 83(b) Election Required

6

REV. PROC. 2001-43ALLOCATION OF INCOME AND

DISTRIBUTIONS

Non-Service Partners

Yr. 1 Income $90 Yr. 1 Distributions $90

Service Partner

Yr. 1 Income $10Yr. 1 Distributions $10

10% Non-vested profits interest granted to SP$100 of allocable Income

7

ALLOCATION OF INCOME AND DISTRIBUTIONS

PROFITS BONUS ALTERNATIVE

Non-Service Partners

Income $100 Comp Deduction ($10)

Distributions ($90)

Service Partner

Compensation $10

* Unfunded, Unsecured Equity Appreciation Right

8

CAPITAL VS. PROFITS INTERESTNO BOOK UP

Capital Accounts ofNon-Service Members $1,000

Net Fair Value of LLC’s Assets $2,000

10% Profits Interest Granted to Service Member

Capital Accounts

Non-Service Members $1,000Service Member 0

9

CAPITAL VS. PROFITS INTERESTNO BOOK UP/ SALE OR LIQUIDATION

Capital Accounts ofNon-Service Members $1,000

Net Fair Value of LLC’s Assets $2,000

10% Profits Interest Granted to Service Member

Proceeds

Non-Service Members $1,900Service Member 100

10

CAPITAL VS. PROFITS INTERESTBOOK-UP

Capital Accounts ofNon-Service Members $2,000

Net Fair Value of LLC’s Assets $2,000

10% Profits Interest Granted to Service Member

Capital Accounts Book Tax

Non-Service Members $2,000 $1,000 Service Member 0 0

Treas. Reg. Sec. 1.704-1(b)(2)(iv)(f)

11

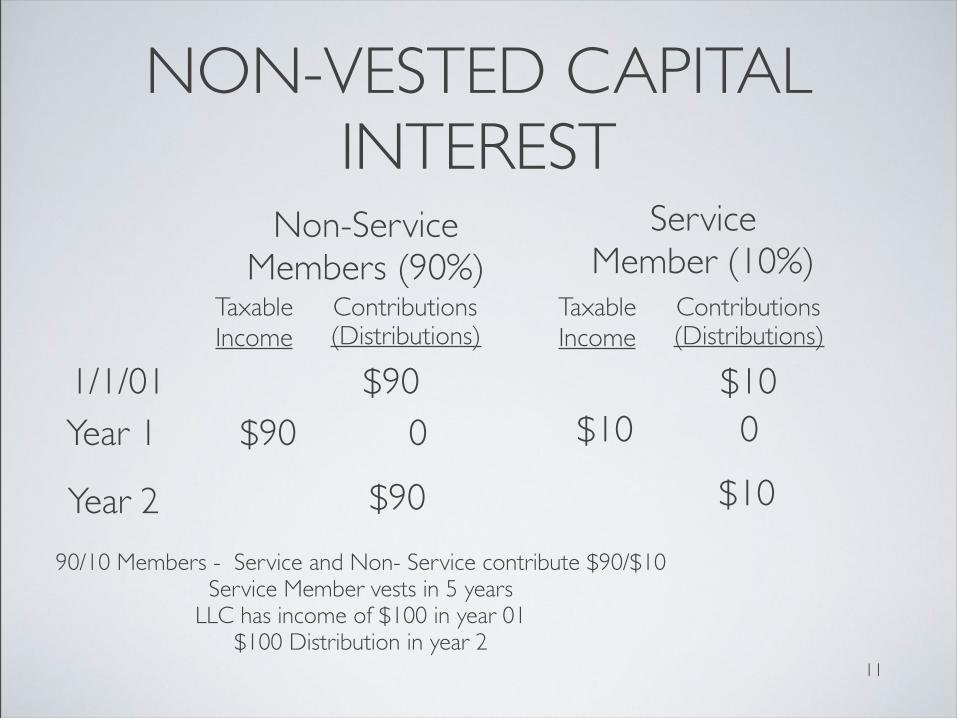

NON-VESTED CAPITAL INTEREST

ServiceMember (10%)

Non-ServiceMembers (90%)

TaxableIncome (Distributions) (Distributions)

TaxableIncome

0 0$90 $10

90/10 Members - Service and Non- Service contribute $90/$10Service Member vests in 5 years

LLC has income of $100 in year 01$100 Distribution in year 2

Year 1

Contributions Contributions

1/1/01 $90 $10

Year 2 $90 $10

12

NON-VESTED CAPITAL INTEREST

ServiceMember (10%)

Non-ServiceMembers (90%)

TaxableIncome (Distributions) (Distributions)

TaxableIncome

0 0$100 $0Year 1

Contributions Contributions

1/1/01 $90 $10

Year 2 (10) $90 $10 Guaranteed Payment

Same facts as previous illustration - no 83(b) election

13

REPURCHASE OF 100% OF CAPITAL INTEREST

SECTION 83(B) ELECTION

Capital AccountNon-Service Partners

1/1/2001 $90 Yr. 1 Income $90

Yr. 1 Distributions $0 Yr. 1 Capital Acct $180

!/1/2002 Repurchase at Cost

Capital Shift $10 Ending Cap Acct $190

Capital AccountService Partner1/1/2001 $10

Yr. 1 Income $10Yr. 1 Distributions $0Yr. 1 Cap Acct $20

Distribution ($10)Forfeited ($10)

Ending Cap Acct $0Capital Loss $10

14

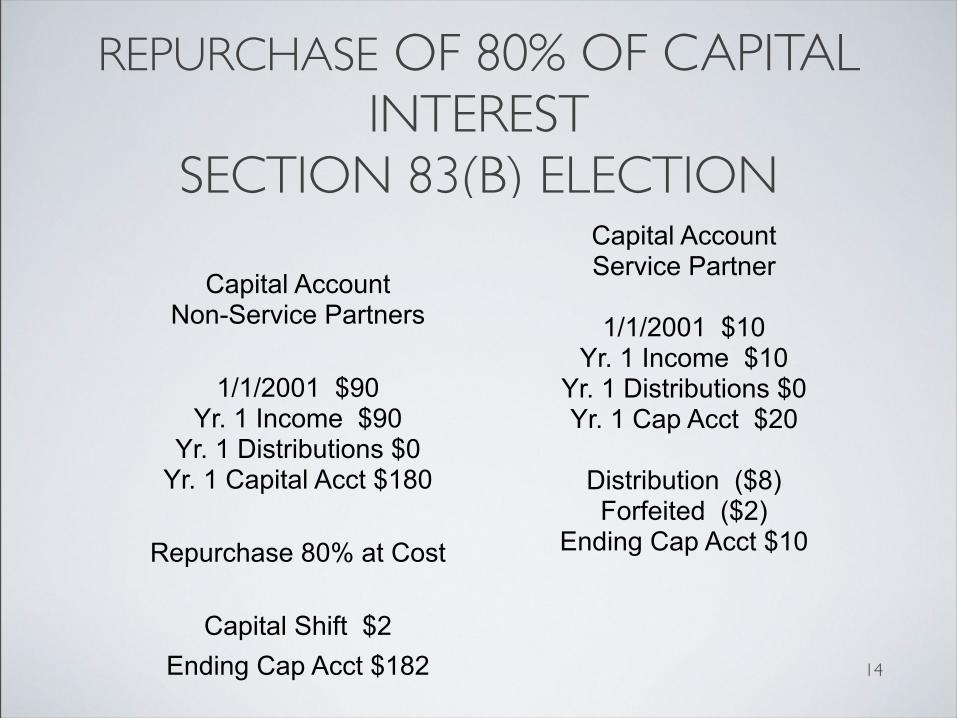

REPURCHASE OF 80% OF CAPITAL INTEREST

SECTION 83(B) ELECTION

Capital AccountNon-Service Partners

1/1/2001 $90 Yr. 1 Income $90

Yr. 1 Distributions $0 Yr. 1 Capital Acct $180

Repurchase 80% at Cost

Capital Shift $2Ending Cap Acct $182

Capital AccountService Partner

1/1/2001 $10Yr. 1 Income $10

Yr. 1 Distributions $0Yr. 1 Cap Acct $20

Distribution ($8)Forfeited ($2)

Ending Cap Acct $10

15

FORFEITURE OF CAPITAL INTEREST

Capital AccountService Partner

1/1/2001 $10Yr. 1 Income $10

Yr. 1 Distributions $0Yr. 1 Cap Acct $20

Distribution $8Forfeited $2

Ending Cap Acct $10

SP’s Tax BasisContribution $10

Income $10Distribution ($8)

Basis $12

16

GRANT OF LLC OPTION

$1,000 FMV$1,000 Capital Accounts

Founders

LLC

ServiceProvider

Exercise Price $10 per UnitFair Value at Grant Date $10 per Unit

Total Exercise Price $100

Option on 10 LLC Membership Units

17

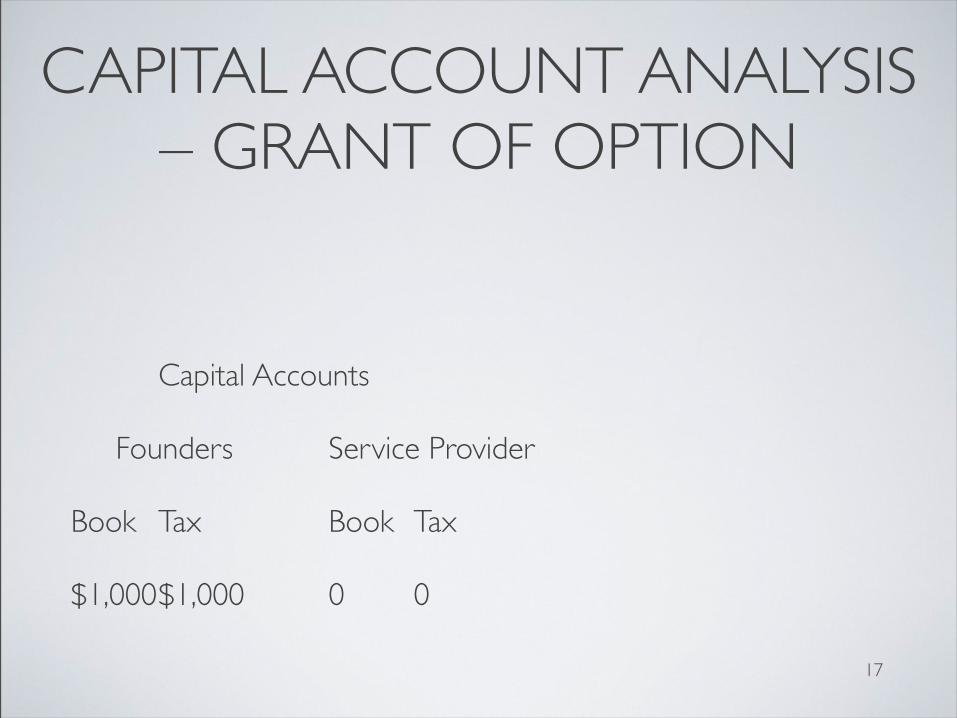

CAPITAL ACCOUNT ANALYSIS – GRANT OF OPTION

Capital Accounts

Founders Service Provider

Book Tax Book Tax

$1,000 $1,000 0 0

18

EXERCISE OF LLC OPTIONFounders

LLC

ServiceProvider

Exercise Price $10 per UnitFair Value at Exercise Date $20 per Unit

Total Exercise Price $100

10 LLC Membership Units$100

$2,000 FMV$1,000 Capital Accounts

19

EXERCISE OF LLC OPTIONCONSEQUENCES TO OPTIONEE - NO BOOK UP

Founders

LLC

ServiceProvider

Exercise Price $10 per UnitFair Value at Exercise Date $20 per Unit

Total Exercise Price $100

10 LLC Membership Units$100

Optionee's Capital Contribution $100Optionee's share of deemed

liquidation proceeds (Rev. Proc. 93-27) $200Compensation income (sec. 83 or 721) $100

20

ALLOCATION OF DEDUCTION

ServiceMember (10%)

Non-ServiceMember (90%)

Taxable Income(Deduction) Resulting

From Issuance $100($100)

21

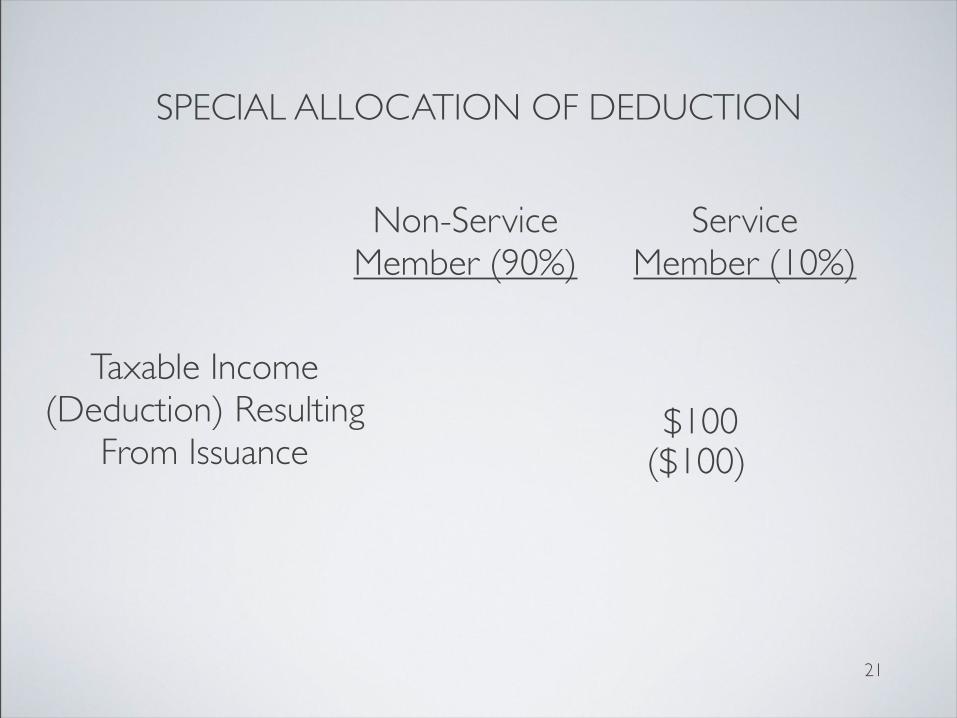

SPECIAL ALLOCATION OF DEDUCTION

ServiceMember (10%)

Non-ServiceMember (90%)

Taxable Income(Deduction) Resulting

From Issuance$100

($100)

22

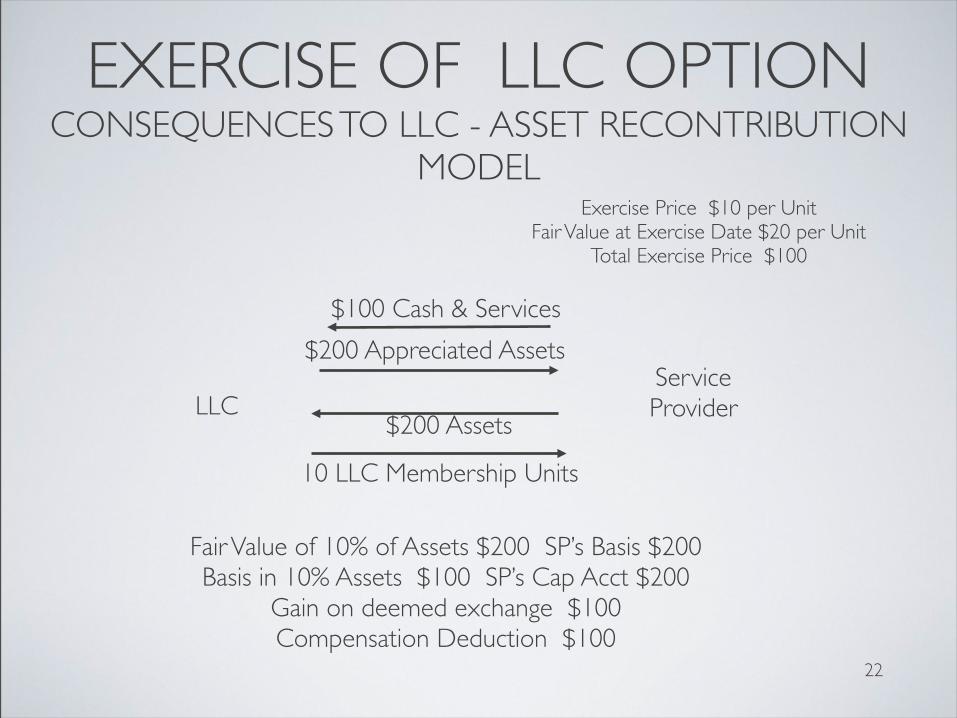

EXERCISE OF LLC OPTIONCONSEQUENCES TO LLC - ASSET RECONTRIBUTION

MODEL

LLC

Exercise Price $10 per UnitFair Value at Exercise Date $20 per Unit

Total Exercise Price $100

Fair Value of 10% of Assets $200 SP’s Basis $200Basis in 10% Assets $100 SP’s Cap Acct $200

Gain on deemed exchange $100Compensation Deduction $100

ServiceProvider

10 LLC Membership Units

$200 Appreciated Assets

$200 Assets

$100 Cash & Services

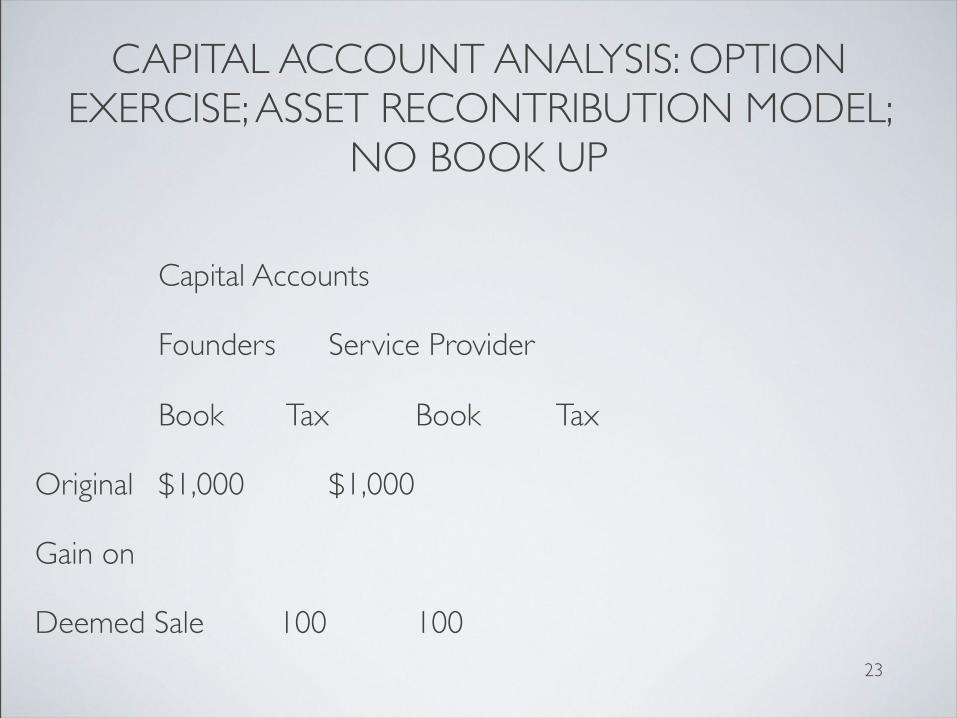

23

CAPITAL ACCOUNT ANALYSIS: OPTION EXERCISE; ASSET RECONTRIBUTION MODEL;

NO BOOK UP

Capital Accounts

Founders Service Provider

Book Tax Book Tax

Original $1,000 $1,000

Gain on

Deemed Sale 100 100

24

CAPITAL ACCOUNT ANALYSIS: OPTION EXERCISE; ASSET RECONTRIBUTION MODEL;

BOOK UP

Capital Accounts

Founders Service Provider

Book Tax Book Tax

Original $1,000 $1,000

Gain on Deemed Sale 100

Compensation (100) (100) $100

25

EXERCISE OF LLC OPTIONCONSEQUENCES TO LLC - CASH COMPENSATION

MODEL

LLCServiceProvider

Exercise Price $10 per Unit SP’s Comp $100Fair Value at Exercise Date $20 per Unit SP’s Basis $200

Total Exercise Price $100 SP’s Cap Acct $200

Section 83(h) Deduction of $100

10 LLC Membership Units

$100 Compensation

$200 Cash

Services

26

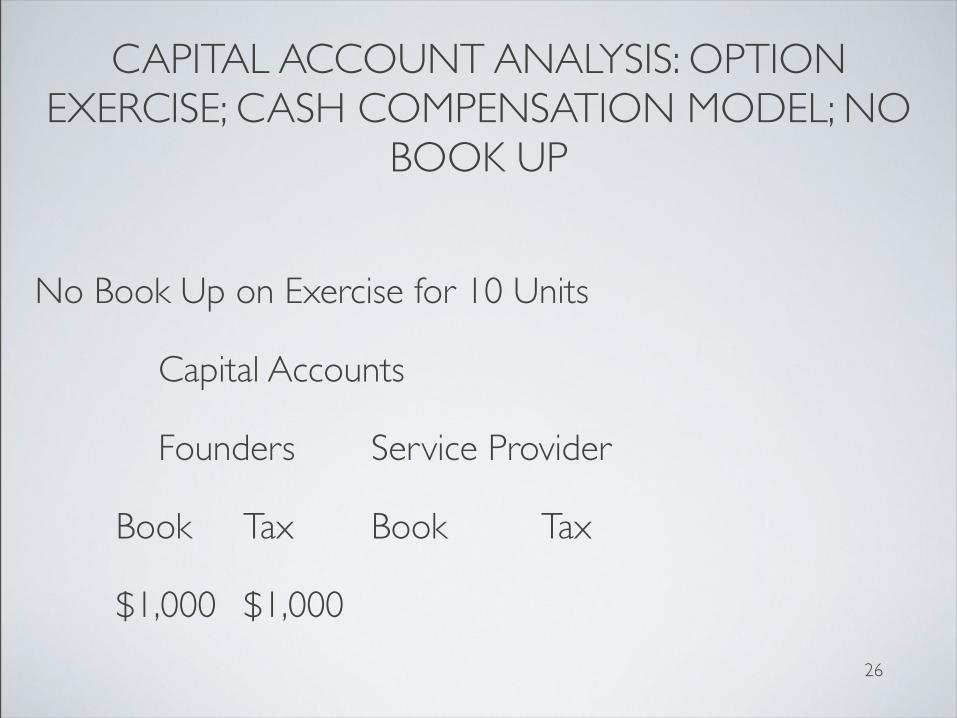

CAPITAL ACCOUNT ANALYSIS: OPTION EXERCISE; CASH COMPENSATION MODEL; NO

BOOK UP

No Book Up on Exercise for 10 Units

Capital Accounts

Founders Service Provider

Book Tax Book Tax

$1,000 $1,000

27

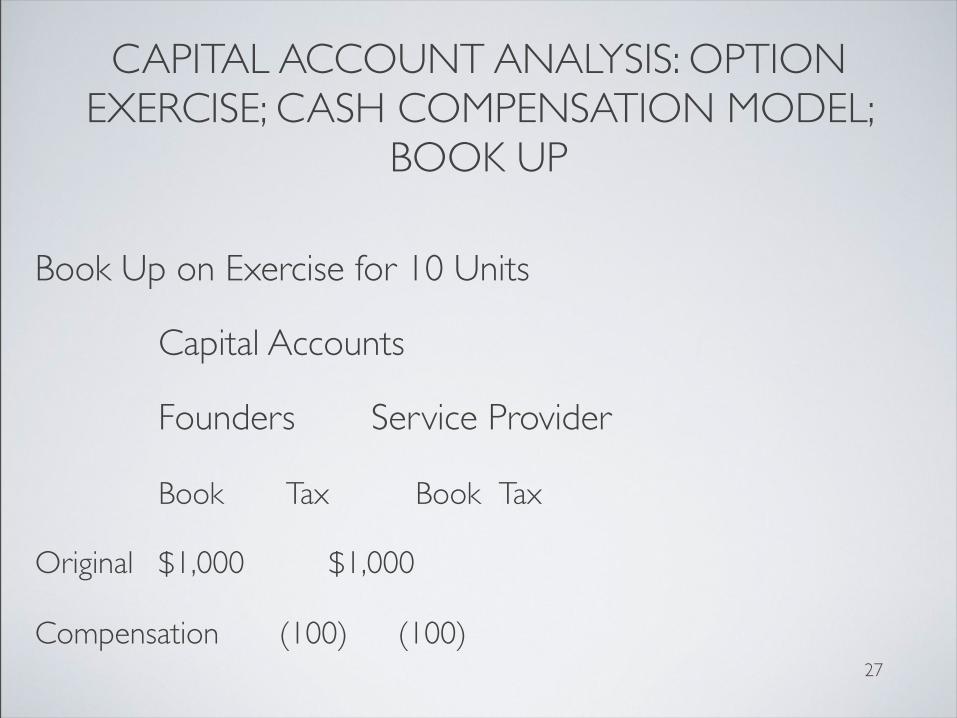

CAPITAL ACCOUNT ANALYSIS: OPTION EXERCISE; CASH COMPENSATION MODEL;

BOOK UP

Book Up on Exercise for 10 Units

Capital Accounts

Founders Service Provider

Book Tax Book Tax

Original $1,000 $1,000

Compensation (100) (100)

28

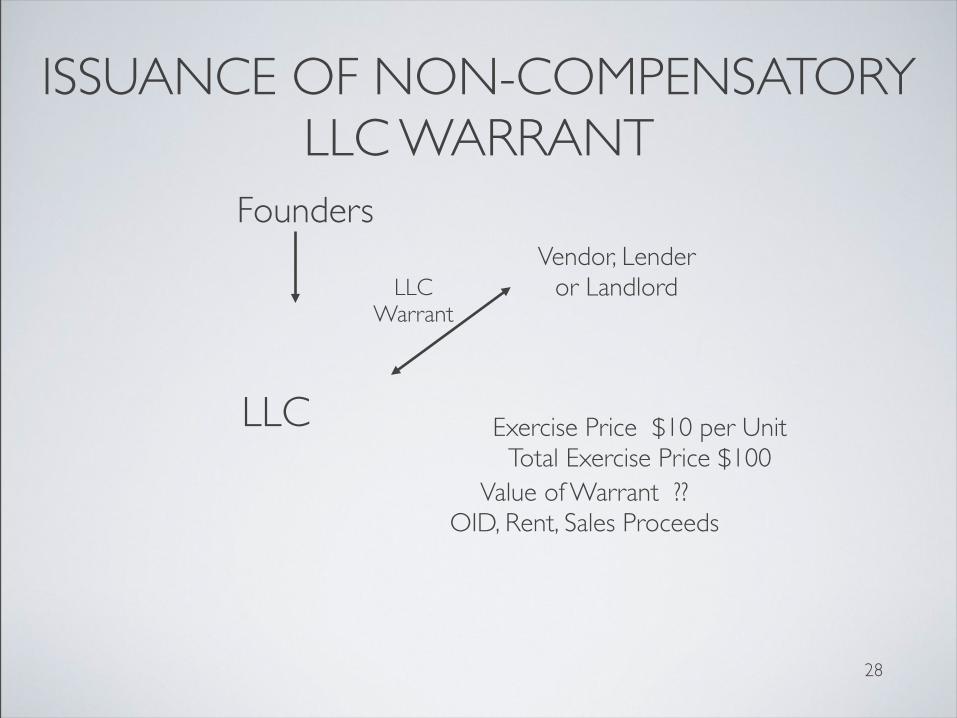

ISSUANCE OF NON-COMPENSATORY LLC WARRANT

Founders

LLC

Vendor, Lenderor Landlord

Exercise Price $10 per UnitTotal Exercise Price $100

LLCWarrant

Value of Warrant ??OID, Rent, Sales Proceeds

29

EXERCISE OF NON-COMPENSATORY LLC WARRANT

LLC

WarrantHolder

Exercise Price $10 per UnitTotal Exercise Price $100

10 LLC Membership Units$100

$2,000 FMV(post-exercise)

Existing Partners' Warrant Holder'sCapital Accounts Capital Account

(90 Units) (10 Units)Before

Exercise $1,900 0After

Exercise $1,800 $200

30

EXERCISE OF WARRANTCAPITAL SHIFT

Capital Accounts

Founders Investor

(90%) (10%)

Book Tax Book Tax

Original

Contribution $1,000 $1,000 $100 $100

31

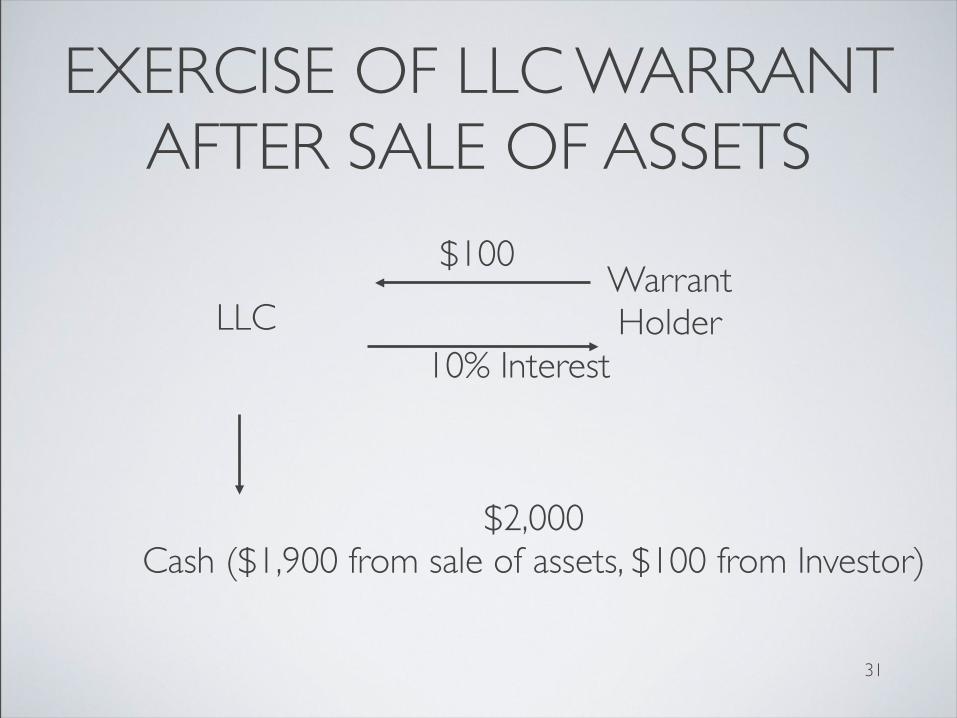

EXERCISE OF LLC WARRANT AFTER SALE OF ASSETS

WarrantHolderLLC

$2,000Cash ($1,900 from sale of assets, $100 from Investor)

$100

10% Interest

32

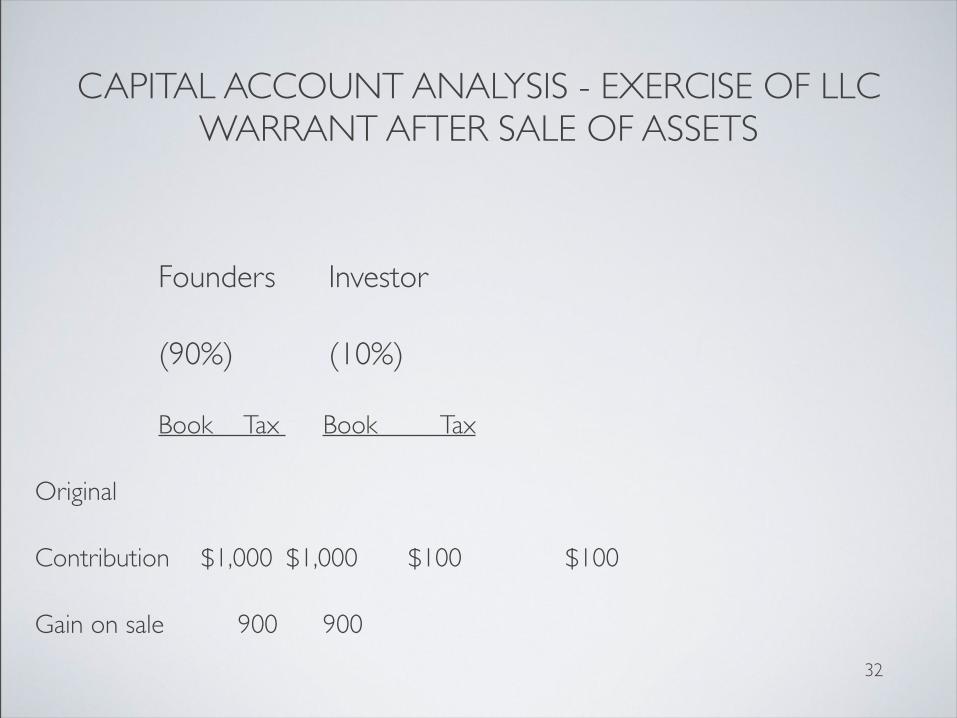

CAPITAL ACCOUNT ANALYSIS - EXERCISE OF LLC WARRANT AFTER SALE OF ASSETS

Founders Investor

(90%) (10%)

Book Tax Book Tax

Original

Contribution $1,000 $1,000 $100 $100

Gain on sale 900 900

33

CONVERTIBLE DEBT ISSUANCE

Debt-holder$$

Convertible DebtInstrument

Vs.

Debt with Warrants

LLC

34

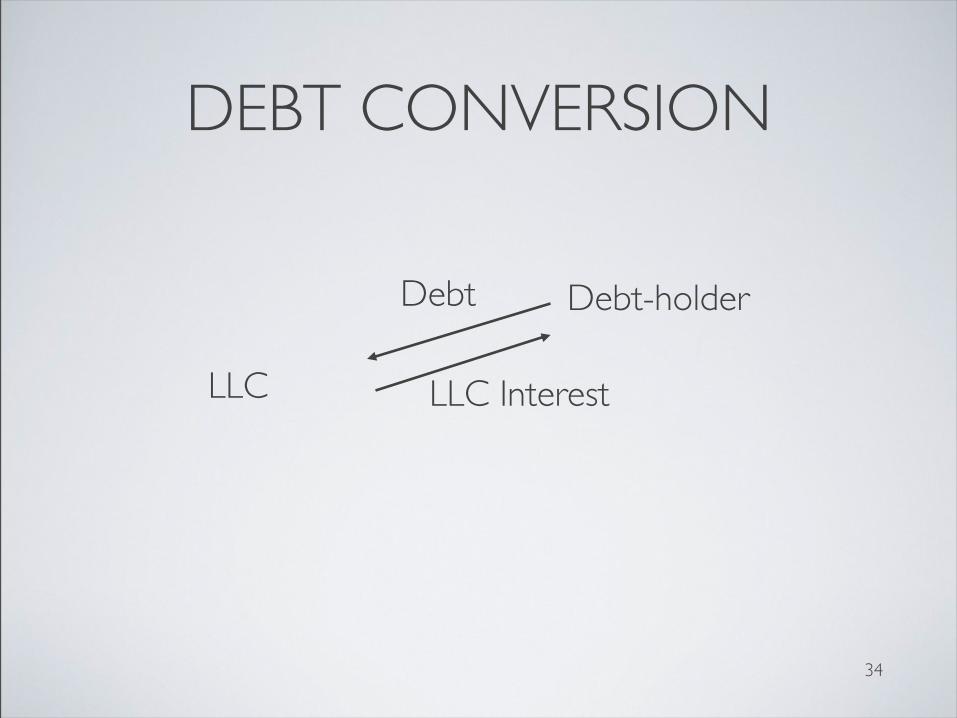

DEBT CONVERSION

Debt-holderDebt

LLC LLC Interest

35

CONVERSION OF PREFERRED LLC INTEREST

LLC

Preferred InterestHolder

10 LLC Membership Units

$2,000 FMV

Common Holders’ Preferred Holder'sCapital Accounts Capital Account

(90 Units) (10 Units)Before

Convert $1,900 $100

After Convert $1,800 $200

36

CAPITAL ACCOUNT ANALYSIS – CONVERSION OF PREFERRED LLC INTEREST, SALE BEFORE CONVERSION

Common Preferred

Book Tax Book Tax

Original

Contribution $900 $900 $100 $100

Gain on Sale $1,000 $1,000 0 0

Balance $1,900 $1,900 $100 $100

37

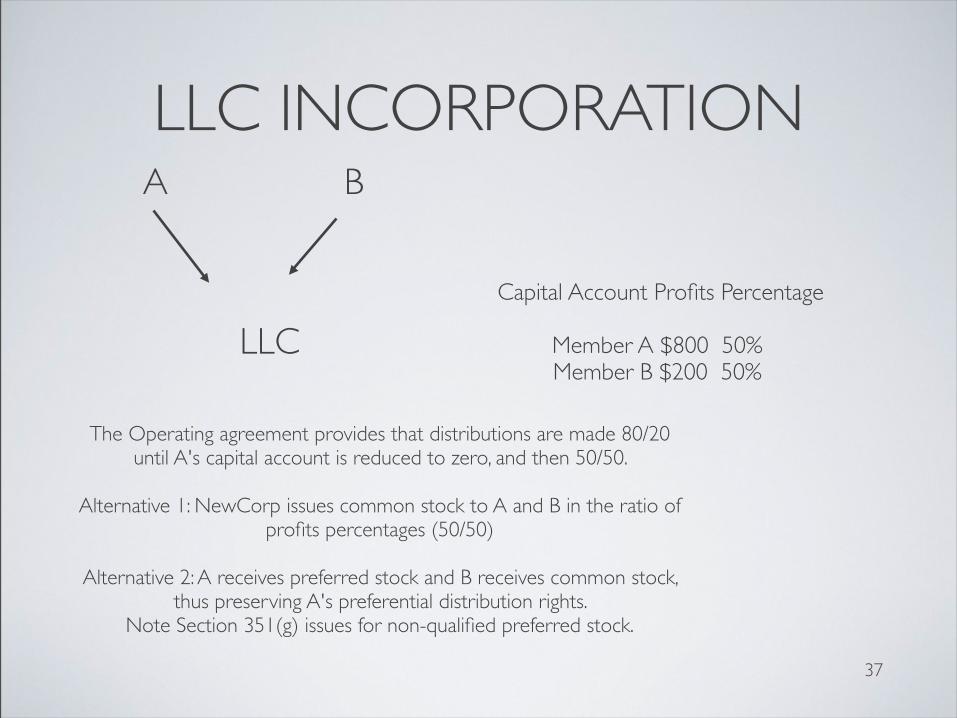

LLC INCORPORATION

LLC

A B

The Operating agreement provides that distributions are made 80/20 until A's capital account is reduced to zero, and then 50/50.

Alternative 1: NewCorp issues common stock to A and B in the ratio of profits percentages (50/50)

Alternative 2: A receives preferred stock and B receives common stock, thus preserving A's preferential distribution rights.

Note Section 351(g) issues for non-qualified preferred stock.

Capital Account Profits Percentage

Member A $800 50%Member B $200 50%

38

OPTION AND LLC INTEREST ASSUMPTION

LLC

Optionees &Interest Holders

NewCorp

NQSO’s

LLC Interests

Significant Tax Issues:

ISO Status of NewCorp Options (Code sec. 422(b)(4); 424(a); 424(h)(3)(A))New Holding Period

Deemed Exercise of NSO's

39

LLC INTEREST ASSUMPTIONPOST EXERCISE

LLC

Optionees &Interest Holders

NewCorpCommon

Stock

LLC Interests

Significant Tax & Legal Issues:

Section 351 property and compensatory transfer issues

Securities Issues (Federal Rule 701; California 25102(o) or (f))

40

CORPORATE PARTNER EQUITY COMPENSATION

A Corp B Corp

AB, LLC

A Corp Stock and $100 cash

A Corp StockEmployee

of ABFMV $100

$50 CashEmployee has $50 incomeA Corp has 0 gain or loss

AB has deduction

$100