empirical article - journal of advances in … prasad--bindu--final.pdf · e-circulars of hdfc....

TRANSCRIPT

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 204

A STUDY ON CREDIT: APPRAISAL WITH REFERENCE TO HDFC BANK Kalidas Prasad1 HOW TO CITE THIS ARTICLE: Kalidas Prasad. “A Study on Credit: Appraisal with Reference to HDFC Bank”. Journal of Advances in Business Management; Vol. 1, Issue 3, July-September 2015; Page: 204-215, DOI: 10.14260/jadbm/2015/24

ABSTRACT: Credit Appraisal means an investigation/assessment done by the banks before providing

any Loans & advances/project finance & also checks the commercial, financial & technical viability of

the project proposed, its funding pattern & further checks the primary & collateral security cover

available for recovery of such funds. Credit Appraisal is a process to ascertain the risks associated with

the extension of the credit facility. It is generally carried by the financial institutions, which are involved

in providing financial funding to its customers. Credit risk is a risk related to non-repayment of the

credit obtained by the customer of a bank. Thus it is necessary to appraise the credibility of the

customer in order to mitigate the credit risk. Proper evaluation of the customer is performed this

measures the financial condition and the ability of the customer to repay back the Loan in future.

Generally the credits facilities are extended against the security know as collateral. But even though

the Loans are backed by the collateral, banks are normally interested in the actual Loan amount to be

repaid along with the interest. Thus, the customer's cash flows are ascertained to ensure the timely

payment of principal and the interest.

KEYWORDS: Credit Appraisal, assessment, Loans, project Finance, collateral, risk, financial

institutions, Credit risk, financial funding, credibility, cash flows, principal, interest etc.,

INTRODUCTION: Credit appraisal means an investigation/assessment done by the bank prior before

providing any loans & advances/project finance & also checks the commercial, financial & technical

viability of the project proposed its funding pattern & further checks the primary & collateral security

cover available for recovery of such funds.

The assessment of the various risks that can impact on the repayment of loan is credit appraisal.

In short, you are determining "Will I get my money back?” Depending on the purpose of loan and the

quantum, the appraisal process may be simple or elaborate. For small personal loans, credit scoring

based on income, life style and existing liabilities may suffice. But for project financing, the process

comprises technical, commercial, marketing, financial, managerial appraisals as also implementation

schedule and ability.

Credit Appraisal means an investigation/assessment done by the banks before providing any

Loans & advances/project finance & also checks the commercial, financial & technical viability of the

project proposed, its funding pattern & further checks the primary & collateral security cover available

for recovery of such funds.

The last year financial crises have become the main cause for recession which was started in

2006 from US and was spread across the world. The world economy has been majorly affected from

the crisis. The securities in stock exchange have fallen down drastically which has become the root

cause of bankruptcy of many financial institutions and individuals. The root cause of the economic and

financial crisis is credit default of big companies and individuals which has badly impacted the world

economy. So in the present scenario analysing one’s credit worthiness has become very important for

any financial institution before providing any form of credit facility so that such situation doesn’t arise

in near future again.

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 205

Analysis of the credit worthiness of the borrowers is known as Credit Appraisal. In order to

understand the credit appraisal system followed by the banks this project has been conducted. The

project has analyzed the credit appraisal procedure with special reference to HDFC Bank which

includes knowing about the different credit facilities provided by the banks to its customers, how a

loan proposal is being made, what are the formalities that is to be satisfied and most importantly

knowing about the various credit appraisal techniques which are different for each type of credit

facility.

OBJECTIVES OF THE STUDY: This study would involve working out and interpreting the financial

ratios in case of working capital financing and term loans.

The study also involves the study of procedural formalities included in sanctioning the finance

to its clients.

This study would involve analyzing the balance sheets of their clients in determining their

financial needs.

To study the credit appraisal methods and to understand the commercial, financial & technical

viability of the proposal proposed and it's finding pattern.

Period of the Study: The period for the present study ranges from 2009to 2014(Budgeted).

Sources and Analysis of Data: The proposed study is carried with the help of both primary and

secondary sources of data.

Primary Data:

Informal interviews with Branch Manager and other staff members at HDFC bank.

E-circulars of HDFC.

Secondary Data:

Books and magazines.

Database at HDFC.

Internal reports of the banks.

Library research.

Websites.

RESEARCH METHODOLOGY:

Research design or research methodology is the procedure of collecting, analyzing and

interpreting the data to diagnose the problem and react to the opportunity in such a way where

the costs can be minimized and the desired level of accuracy can be achieved to arrive at a

particular conclusion.

The methodology used in the study for the completion of the project and the fulfilment of the

project objectives.

The sample of the stocks for the purpose of collecting secondary data has been selected on the

basis of Random Sampling. The stocks are chosen in an unbiased manner and each stock is

chosen independent of the other stocks chosen. The stocks are chosen from the banking sector.

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 206

Limitations of the Study:

As the credit rating is one of the crucial areas for any bank, some of the technicalities are not

revealed which may have cause destruction to the information and our exploration of the

problem.

As some of the information is not revealed, whatever suggestions generated, are based on certain

assumptions.

Credit appraisal system includes various types of detail studies for different areas of analysis, but

due to time constraint, our analysis was of limited areas only.

The study aims at gaining the practical knowledge by taking help of bank personals. So there

might have been tendencies among the personals to amplify or filter their responses due to time

limitation.

Credit appraisal for working capital finance is study that needed specialized knowledge of the

area, so there is chance for interpretational error on my par.

BANK: A bank is a profit seeking business firm, which deals with money and credit. It accepts deposits

from the public and makes these funds available to those who need them. It helps in the remittance of

money from one place to another. A banking company is defined as a company, which transacts the

business of banking in India. A banking company in India has been defined in the banking companies

act 1949 as "one which transacts the business of banking which means the purpose of lending or

investment, of deposits of money from the public. Repayable on demand and withdraw able by cheque,

draft, order or otherwise".

Brief Overview of Loans: Loans can be of two types fund base & non-fund base:

Fund Base Includes:

Working Capital.

Term Loan.

Non-fund Base Includes:

Letter of Credit.

Bank Guarantee.

Bill Discounting.

FUND BASE:

WORKING CAPITAL:

General: The objective of running any industry is earning profits. An industry will require funds to

acquire

“Fixed assets” like land, building, plant, machinery, equipments, vehicles, tools etc., & also to

run the business i.e. its day to day operations.

Funds required for day to-day working will be to finance production & sales. For production,

funds are needed for purchase of raw materials/stores/fuel, for employment of labor, for power

charges etc., for storing finishing goods till they are sold out & for financing the sales by way of sundry

debtors/receivables.

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 207

Capital or funds required for an industry can therefore be bifurcated as fixed capital & working

capital. Working capital in this context is the excess of current assets over current liabilities. The excess

of current assets over current liabilities is treated as net working capital or liquid surplus & represents

that portion of the working capital, which has been provided from the long-term source.

Definition: Working capital is defined as the funds required carrying the required levels of current

assets to enable the unit to carry on its operations at the expected levels uninterruptedly.

Thus Working Capital required is Dependent on:

a. The volume of activity (viz. level of operations i.e. Production & sales)

b. The activity carried on viz. mfg process, product, production programme, the materials &

marketing mix.

METHODS & APPLICATION:

SEGMENT LIMITS METHOD

SSI Upto Rs 5 cr

Traditional Method & Nayak

Committee method

Above Rs 5 cr Projected Balance Sheet Method

SBF All loans Traditional/ Turnover Method

C & I Trade

& Services

Up to Rs 1 cr Traditional Method for Trade &

Projected Turnover Method

Above Rs 1 cr

& up to Rs 5 cr

Projected Balance Sheet Method &

Projected Turnover Method

Above Rs 5 cr Projected Balance Sheet Method

C & I

Industrial Units

Below

Rs 25 lacs Traditional Method

Rs 25 lacs &

Over but up to

Rs 5 cr

Projected Balance Sheet Method &

Projected Turnover Method

Above Rs 5 cr Projected Balance Sheet Method

HDFC NORMS FOR CREDIT APPRAISAL: Credit appraisal means an investigation/assessment done

by the bank prior before providing any loans & advances/project finance & also checks the commercial,

financial & technical viability of the project proposed its funding pattern & further checks the primary

& collateral security cover available for recovery of such funds.

Loan Policy–An Introduction:

1. State Bank of India’s (SBI) Loan Policy is aimed at accomplishing its mission of retaining the

bank’s position as a Premier Financial Services Group, with World class standards & significant

global business, committed to excellence in customer, shareholder & employee satisfaction & to

play a leading role in the expanding & diversifying financial services sector, while continuing

emphasis on its Development Banking role.

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 208

2. The Loan Policy of the any bank has successfully withstood the test of time and with inbuilt

flexibilities, has been able to meet the challenges in the market place. The policy exits & operates

at both formal & informal levels. The formal policy is well documented in the form of circular

instructions, periodic guidelines & codified instructions, apart from the Book of Instructions,

where procedural aspects are highlighted.

3. The policy, at the holistic level, is an embodiment of the Bank’s approach to sanctioning,

managing & monitoring credit risk & aims at making the systems & controls effective.

4. The Loan Policy also aims at striking a balance between underwriting assets of high quality, and

customer oriented selling. The objective is to maintain Bank’s undisputed leadership in the

Indian Banking scene.

5. The Policy aims at continued growth of assets while endeavouring to ensure that these remain

performing & standard. To this end, as a matter of policy the Bank does not take over any Non-

Performing Asset (NPA) from other banks.

6. The Central Board of the Bank is the apex authority in formulating all matters of policy in the

bank. The Board has permitted setting up of the Credit Policy & Procedures Committee (CPPC)

at the Corporate Centre of the Bank of which the Top Management are members, to deal with

issues relating to credit policy & procedures on a Bank-wide basis. The CPPC sets broad policies

for managing credit risk including industrial rehabilitation, sets parameters for credit portfolio

in terms of exposure limits, reviews credit appraisal systems, approves policies for compromises,

write offs, etc. & general management of NPAs besides dealing with the issues relating to

Delegation of Powers.

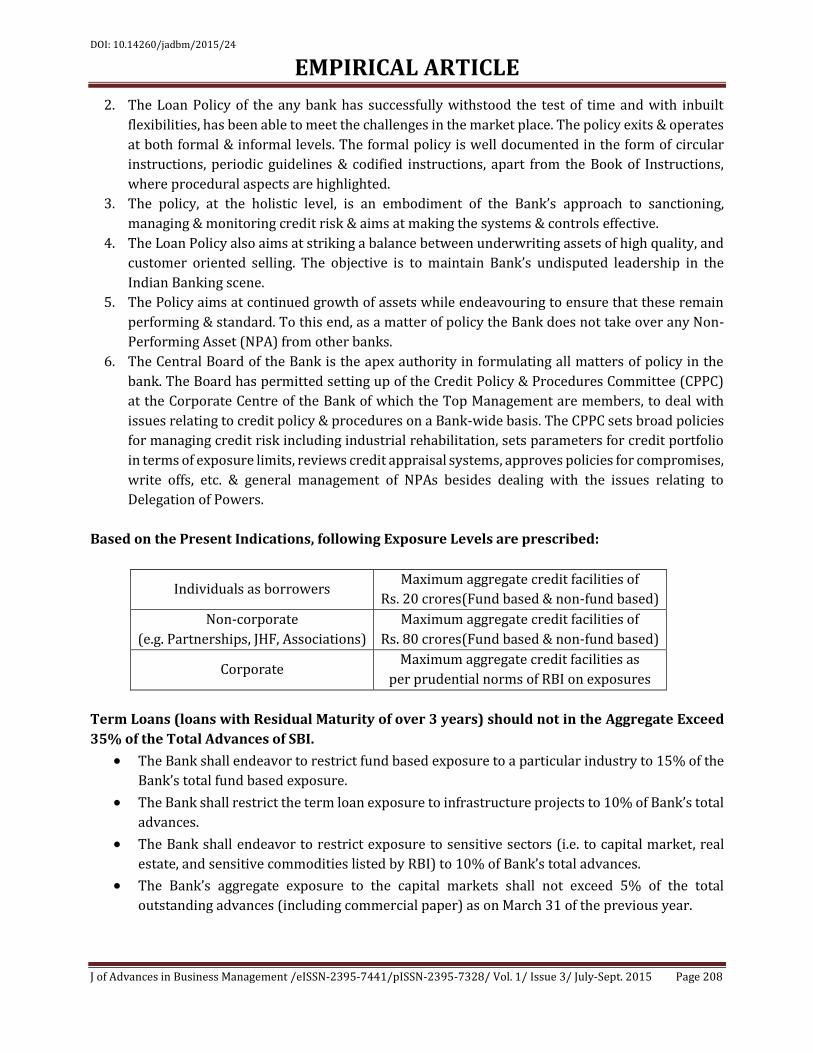

Based on the Present Indications, following Exposure Levels are prescribed:

Individuals as borrowers Maximum aggregate credit facilities of

Rs. 20 crores(Fund based & non-fund based)

Non-corporate

(e.g. Partnerships, JHF, Associations)

Maximum aggregate credit facilities of

Rs. 80 crores(Fund based & non-fund based)

Corporate Maximum aggregate credit facilities as

per prudential norms of RBI on exposures

Term Loans (loans with Residual Maturity of over 3 years) should not in the Aggregate Exceed

35% of the Total Advances of SBI.

The Bank shall endeavor to restrict fund based exposure to a particular industry to 15% of the

Bank’s total fund based exposure.

The Bank shall restrict the term loan exposure to infrastructure projects to 10% of Bank’s total

advances.

The Bank shall endeavor to restrict exposure to sensitive sectors (i.e. to capital market, real

estate, and sensitive commodities listed by RBI) to 10% of Bank’s total advances.

The Bank’s aggregate exposure to the capital markets shall not exceed 5% of the total

outstanding advances (including commercial paper) as on March 31 of the previous year.

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 209

CASE STUDY OF THE COMPANIES WHICH TAKEN THE LOANS FROM HDFC BANK:

Details of Case:

Company: Akshat Polymers.

Company: Akshat Polymers.

Firm: Partnership Firm (M/S Umiya Polymers)

* Shri Amrutbhai Laljibhai Desai.

* Shri Gunvantbhai Ambaramdas Patel.

* Shri Natvarlal Mohanlal Patel.

* Shri Dharamsinhbhai Lallubhai Desai.

* Shri Kanjibhai Maljibhai Desai.

Industry: Manufacturing.

Activity: Manufacturing of HDPP woven sacks.

Segment: SSI.

Date of Incorporation: 19.11.07.

Banking Arrangement: Sole Banking.

Proposal:

Sanction for:

i) FBWC(Fair Work Building and Construction) limits of Rs.2.25crores

ii) Fresh Term Loan of Rs.2.00 crores

Approval for:

i) CRA (Credit Rating Agency) rating of SB- 6 (71marks) based on

Projected financials as on 31.03.2010.

ii) Pricing for WC facilities @1.00% above SBAR as applicable for SB-5

minimum @13.75and for TL1.50% above SBAR minimum @14.25%

PERFORMANCE & FINANCIAL INDICATORS :( Rs. in Crores):

Year 2009 2010 2011 2012 2013 2014

(budgeted))

Installed cap Qty.

(MT/pa.) 2520 2520 2520 2520 2520 2520

Net Sales Qty.

(approx) (MT) 1029 2016 2091 2142 2217 2268

Net Sales(Value) 9.26 19.77 20.58 21.09 21.82 22.34

(Export) 0.00 0.00 0.00 0.00 0.00 0.00

Operating profit 0.44 1.18 1.19 1.23 1.31 1.33

Profit before tax

0.43 1.17 1.18 1.22 1.30 1.32

PBT/Net sales (%) 4.64 5.92 5.73 5.78 5.96 5.91

Profit after tax 0.29 0.78 0.79 0.82 0.87 0.88

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 210

Cash accruals 0.66 1.10 1.09 1.15 1.24 1.32

PBDIT 1.20 2.04 1.96 1.97 2.02 2.05

Paid up capital 0.95 0.95 0.95 0.95 0.95 0.95

Tangible net worth 1.23 2.01 2.80 3.62 4.49 5.38

Adjusted TNW 1.73 2.51 3.30 4.12 4.99 5.88

TOL/TNW 4.11 2.50 1.67 1.19 0.88 0.66

TOL/Adjusted TNW 2.64 1.80 1.27 0.92 0.81 0.62

Current ratio 1.34 1.52 1.53 1.53 1.57 1.81

NWC 1.01 1.71 2.40 2.57 2.74 3.28

BALANCE SHEET: (Rs. In crores)

Sources of Funds 31.03.2009 31.03.2010

Share Capital 0.95 0.95

Reserves and Surplus 0.29 1.07

Secured Loans :short term CC 2.25 2.25

:long term TL 2.00 1.60

Unsecured Loans 0.50 0.50

Deferred Tax Liability

Total 5.99 6.37

Application of Funds

Fixed Assets (Gross Block) 2.67 2.67

Less Depreciation 0.37 0.69

Net Block 2.30 1.98

Capital Work in Progress

Investments

Inventories 1.73 2.13

Sundry debtors 1.85 2.40

Cash & bank balances 0.15 0.15

Loans & advances tosuppliers of

Raw material/ spares 0.14 0.12

Advance tax 0.10 0.23

(Less : Current liabilities) 0.31 0.67

(Less : Provisions)

Net Current Assets 3.66 4.36

Misc. Expenditure

(To the extent not written off or adjusted)

Non-Current Assets/ Deposits 0.03 0.03

Total 5.99 6.37

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 211

MOVEMENT IN TANGIBLE NET WORTH:

Movement in TNW Projected

31.03.2009 31.03.2010 31.03.2011

Opening TNW 0.00 1.23 2.01

+PAT 0.29 0.78 0.79

+Inc. in Equity/ Premium 0.95

+/-Change inInt. Assets -0.01

+/- Adj. of prior year exp.

- Dividend payment

Closing in TNW 1.23 2.01 2.80

BANK INCOME ANALYSIS: (Rs. in crores)

From Projection

31.03.2009

Projection

31.03.2010

WC Int. 0.16 0.27

TL Int. 0.14 0.29

LC - -

BG - -

Bill - -

Others loan

processing 0.03 0.01

Total 0.33 0.57

DEVIATIONS IN LOAN POLICY:

Parameters

Indicative

Min/Max level

as per loan policy

Company's

level as on

31.03.2009 @

Company's

level as on

31.03.2010

Liquidity 1.33 1.34 1.52

TOL(Total operating

leverage)/TNW

(tangible net worth)

TOL/Adj. TNW

3.00 4.11

2.64

2.50

1.80

Average gross DSCR

(TL) 1.75 2.54 2.54

Debt/ equity

Debt/Quasi equity 2:1

2.01:1

1.15:1

1.03:1

0.64:1

Any others - - -

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 212

COMMERCIAL VIABILITY :( Rs.in crores)

Year ending 31st

March

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

2013-

14 Total

Net Sales 9.26 19.77 20.58 21.09 21.82 22.34

Net Profit 0.29 0.78 0.79 0.82 0.87 0.88

Cash Accruals 0.66 1.10 1.09 1.15 1.24 1.32 6.56

Interest on TLs 0.16 0.27 0.22 0.16 0.11 0.05 0.97

Sub Total(A) 0.82 1.37 1.31 1.31 1.35 1.37 7.53

Total repayment 0.00 0.40 0.40 0.40 0.40 0.40 2.00

Interest on TL 0.16 0.27 0.22 0.16 0.11 0.05 0.97

Sub Total (B) 0.16 0.67 0.62 0.56 0.51 0.45 2.97

DSCR (Gross) 5.13 2.04 2.11 2.34 2.65 3.04

Net DSCR - 2.75 2.73 2.88 3.10 3.30

Average Gross DSCR 2.54

Average Net DSCR 3.28

BREAK-EVEN AND SENSITIVITY ANALYSIS AND WHETHER ACCEPTABLE :( Rs. in crores)

Break even Analysis 31/03/09 31-Mar-10 31-Mar-11 30-Mar-12 31-Mar-13 31-Mar-14

Capacity Utilization 70% 80% 83% 85% 88% 90%

Net Sales (A) 9.26 19.77 20.58 21.09 21.82 22.34

Variable Costs

Raw material 8.74 17.13 17.77 18.20 18.84 19.27

Consumable spares 0.00 0.00 0.00 0.00 0.00 0.00

Power and Fuel 0.26 0.47 0.50 0.53 0.56 0.59

Other operating Exp. 0.09 0.13 0.15 0.16 0.17 0.18

Stock Changes 0.73 0.39 0.06 0.03 0.04 0.04

Total Variable Cost(B) 8.36 17.34 18.36 18.86 19.53 20.00

Fixed Costs

Direct Labor 0.08 0.13 0.14 0.15 0.16 0.17

Selling, Admin. &

General Expenses 0.06 0.10 0.11 0.12 0.13 0.14

Interest Expenses 0.40 0.55 0.48 0.42 0.35 0.29

Depreciation 0.37 0.32 0.30 0.33 0.37 0.44

Total Fixed Cost (C) 0.91 1.10 1.03 1.02 1.01 1.04

Contribution (D=A-B) 0.90 2.43 2.22 2.23 2.29 2.34

Contribution ratio (E=D/A) 0.10 0.12 0.11 0.11 0.10 0.10

BE sales (F=C/E) 9.10 9.17 9.36 9.27 10.10 10.40

BE sales as % of Net Sales 98.27 46.38 45.48 43.95 46.29 46.55

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 213

INTERFIRM COMPARISON: (To be given only where Data from Comparable Units is Available.)

(Rs. in Crores)

Name of Company FBL NFBL Year Sales PBT/

Sales %

TOL/

TNW CR

Ahmedabad Packaging

Industries Ltd. 3.30 1.20 2007 23.11 2.16 1.47 1.16

Singhal Industries Pvt. Ltd 6.70 -- 2010 15.19 6.52 2.90 1.90

Asia Woven Sacks Pvt. Ltd. 7.44 1.00 2008 22.98 4.53 3.14 1.08

Akshat Polymers 4.25 -- 2010 19.77 5.92 2.50 1.52

Raw Material: The major raw material for this plant is HDPP in the form of granules. This raw material

is available locally by sales & distribution network of the major suppliers as under:

Reliance Industries Limited.

Nand Agencies.

Labdhi International.

Hadlia petrochemicals Ltd.

Sharada Polymers.

IPCL.

The raw materials are purchased from the suppliers against the advance payment only and

cash discounts are offered resulting in the increase in profitability. Any variation in the cost of raw

material is proposed to be passed on to the finished products and will not affect the profitability.

Analysis of Case:

The firm is into manufacturing of HDPP woven sacks which are widely used as packaging

material in cement, fertilizer, etc.

As per ICRA report, grading and research services (2006) Flexible packaging sector is expected

to grow at the rate of 12.40%.

The promoters have sufficient experience in the line of activity. The promoters had already made

negotiations of the some of the industries as detailed under for selling the HDPP woven sacks:

GUJCOMASOL.

Birla cement.

Sanghi cement.

Ambuja cement.

Various grain & Food Export Unit of Gujarat.

The orders worth Rs.2.50 crores is expected to be finalized by end of August, 2008 and before

commissioning of the plant as advised.

The company’s borrower rating is SB-6 based on projected financials as on 31.03.2010 (the first

full year of operations).

Projected financials are in line with the financials of the some of the unit in similar line of activity

and production level.

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 214

The promoters are having experience of more than 15 years in the line of the activity. The affairs

of the firm are expected to be managed on professional lines based on their past experience.

The conduct of accounts of associate with the existing bankers has been satisfactory. The short

and medium term outlook for the industry is stable

Availability of collateral security reflected in collateral coverage of 50.566%.

Gross average DSCR of 2.54.

Average security margin of 48%.

The company has adequate management skills and production/marketing infrastructure in

place to achieve the projected trajectory. There is steady demand for the product.

CONCLUSION: It is boom time for those working in the financial sector. There are opportunities galore

in finance and more will come in the next few years so finance is exciting is exciting both as a subject

and a career option with the greater expansion of the global economy.

Finance management is the backbone of any organizations and hence yields a number of job

options ranging from strategic financial planning to sales.

HDFC BANK load policy contains various norms for sanction of different types of loans. There

all norms does not apply to each & every case. HDFC BANK norms for providing loans are flexible & it

may differ from case to case.

The CRA models adopted by the bank take into account all possible factors, which go into

appraising the risk associated with a loan, these have been categorized broadly into financial, business,

industrial, and management risks & are rated separately.

Usually, it is seen that credit appraisal is basically done on the basis of fundamental soundness.

But, after different types of case studies, our conclusion was such that, in HDFC BANK, credit appraisal

system is not only looking for financial wealth. Other strong parameters also play an important role in

analyzing creditworthiness of the firm.

Moreover, the study at HDFC BANK gave a vast learning experience to us and has helped to

enhance our knowledge. During the study we learnt how the theoretical financial analysis aspects are

used in practice during the working capital finance assessment. We have realized during my project

that a credit analyst must own multi-disciplinary talents like financial, technical as well as legal know-

how.

The credit appraisal for working capital finance system has been devised in a systematic way.

There are clear guidelines on how the credit analyst or lending officer has to analyze a loan proposal.

It includes Phase-wise Analysis which Consists of 5 Phases:

1. Financial statement analysis.

2. Working capital and its assessment techniques.

3. Credit risk assessment.

4. Documentation.

5. Loan administration.

To ensure asset quality, proper risk assessment right at the beginning, is extremely important.

That is why Credit Risk Assessment system is an essential ingredient of the Credit Appraisal exercise.

DOI: 10.14260/jadbm/2015/24

EMPIRICAL ARTICLE

J of Advances in Business Management /eISSN-2395-7441/pISSN-2395-7328/ Vol. 1/ Issue 3/ July-Sept. 2015 Page 215

The HDFC BANK was the first to formulate a Credit Risk Assessment model. It considers

important parameters like profitability, repayment capacity, and efficiency of the unit, historical

/industry comparisons etc., which were not factored in other models. It is equally efficient as the

SIDBI’s CART (Credit Assessment and Rating Tool) model.

In all, the viability of the project from every aspect is analyzed, as well as type of business,

industry, promoters, past records, experience, projected data and estimates, goals, long term plans also

plays crucial role in increasing chances of getting project approved for loan.

REFERENCES:

1. Vaidhyanathan, T.S., “Credit Management” Internal circular of HDFC BANK.

2. “Credit and Banking” By: K. C. Nanda, Volume 33, PP 345-356, June 14 2005.

3. Agarwal, R. G., “Banking Finance” A Leading monthly of Banking and Finance Published by Sashi

Publications, Volume 24 , PP 145-156, April 09 2006.

4. K.Ramakrishnan, “Indian Bankers” Published by Indian Bank Association, Volume 26, PP 223-285,

July 21 2007.

5. www.indianbankassociation.com

6. www.bankersindia.com

7. www.iibf.co.in

8. www.rbi.org.in

9. www.wikipedia.com

AUTHORS:

1. Kalidas Prasad

PARTICULARS OF CONTRIBUTORS:

1. Associate Professor, Department of

Business Management, Sree Chaitanya

Post-Graduate College.

NAME ADDRESS EMAIL ID OF THE

CORRESPONDING AUTHOR:

Kalidas Prasad,

H. No. 8-5-649,

Kothirampur,

Karimnagar-505001.

E-mail: [email protected]

Date of Submission: 14/08/2015.

Date of Peer Review: 18/08/2015.

Date of Acceptance: 19/08/2015.

Date of Publishing: 20/08/2015.