emerging wireless opportunities for the rural operator opastco 44th annual winter convention...

TRANSCRIPT

Emerging Wireless Opportunities for the Rural Operator

OPASTCO 44th Annual Winter Convention

Orlando, FLJanuary 16, 2007

Carri Bennet, CEO

Spectrum Opportunities• Cellular and PCS• Advanced Wireless Services• 700 MHz• BRS/EBS• 1.4 MHz - Auction Begins 2/7/2007• WCS (2.3 GHz)• AWS-2• MVDDS• LMDS• Unlicensed Bands

Cellular & PCS• Cellular

• Must have spectrum– Strategic roaming alliance with Cingular– Unserved areas are still being built out

• PCS• T-Mobile willing to sell 10 MHz of spectrum

– Reserves at least 20 MHz– Favorable roaming rates

• Sprint PCS already covered• Distressed spectrum still available• Auction Scheduled for May 16, 2007

– 38 PCS licenses

Advanced Wireless Services (AWS-1)

1710-1755 MHz and

2110-2155 MHz bands

Advanced Wireless Services• Spectrum auction ended September 18,

2006– Previously allocated for federal government

use; Now being transferred for commercial fixed and mobile application

– Band clearing reimbursement required– Fifteen-year license term– Available Equipment

AWS Auction

• 1,122 licenses: – 36 Regional Economic Area Grouping (REAG)

licenses– 352 Economic Area (EA) licenses– 734 Cellular Market Area (CMA) licenses

• 168 Qualified bidders

AWS Auction

Bidder High Bids Total Gross BidsT-Mobile 120 $4,182,312,000Verizon Wireless 13 $2,808,599,000SpectrumCo LLC 137 $2,377,609,000MetroPCS AWS, LLC 8 $1,391,410,000Cingular AWS, LLC 48 $1,334,610,000Cricket 99 $710,214,000

• 104 bidders won 1,087 licenses

• $13.7 Billion net bids

• Top six bidders

AWS AuctionLicense Size Mean Price/POP Mean Price/MHz-POPREAGs 8.82 0.662EAs 6.89 0.46CMAs 7.95 0.398RSAs 2.22 0.111Licenses with POPs 250k-1M 2.77 0.162Licenses with POPs <=250k 2.44 0.122

The median price of a license was $0.12 MHz-POP(around $2.40/POP for a 20 MHz license)

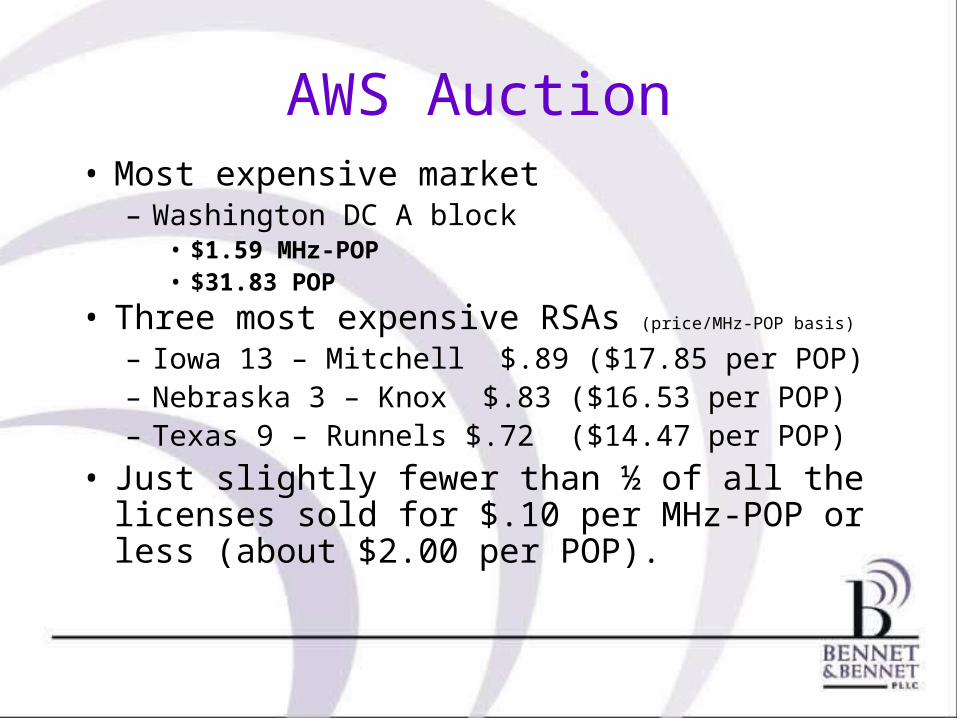

AWS Auction• Most expensive market

– Washington DC A block • $1.59 MHz-POP• $31.83 POP

• Three most expensive RSAs (price/MHz-POP basis)

– Iowa 13 – Mitchell $.89 ($17.85 per POP)– Nebraska 3 – Knox $.83 ($16.53 per POP)– Texas 9 – Runnels $.72 ($14.47 per POP)

• Just slightly fewer than ½ of all the licenses sold for $.10 per MHz-POP or less (about $2.00 per POP).

AWS Auction

• What does it mean?• Will it be just another 2-2.5G mobile service?

– CMRS carriers pathway to WiMAX?• Voice, data, music, video• Multimedia• Content is king• How will it play with existing CMRS high-speed

broadband networks?

AWS Auction

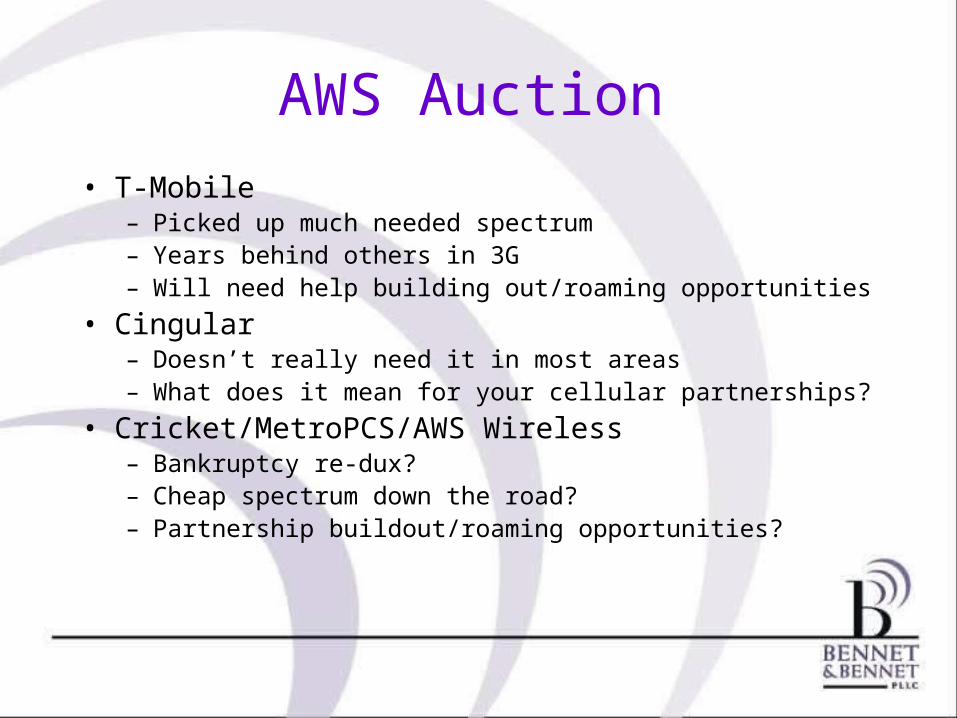

• T-Mobile– Picked up much needed spectrum– Years behind others in 3G– Will need help building out/roaming opportunities

• Cingular– Doesn’t really need it in most areas– What does it mean for your cellular partnerships?

• Cricket/MetroPCS/AWS Wireless– Bankruptcy re-dux?– Cheap spectrum down the road?– Partnership buildout/roaming opportunities?

AWS Auction

• SpectrumCo– Cable JV with Sprint– Will not be a fifth CMRS competitor– Streaming video?– How does this fit with Sprint’s WiMAX deployment

at 2.5 GHz?– Is it just a $2 billion insurance policy?

AWS Auction

• Increased data speeds• Mobile high-speed access• Mobile media services• Multi-mode devices• My phone, my internet, my games, my music,

my wallet, my total connection to my life!

AWS Auction

• DEs acquired 181,252,312 covered POPs (duplicative) out of a possible 1,713,722,670...about 11%.

• What does this mean for future DE rules? • What does this mean for 700 MHz band

auction in 2008?

700 MHz Spectrum

- Lower 700 MHz Band Plan- Upper 700 MHz Band Plan

Lower 700 MHz

Lower 700 MHz Areas (MSA/RSAs)

Upper 700 MHz Bandplan

Upper 700 MHz Areas (MEAs)

Upper 700 MHz Areas (EAGs)

Proposed Rebanding of 700 MHz

• Will allow rural operators to participate with smaller licensed areas (MSAs/RSAs)

• Major industry support

Balanced Consensus Plan

• Mix of licenses of varying sizes and geographic regions

• Facilitates the competitive and rapid deployment of innovative wireless services in the 700 MHz bands.

• Advances Section 309(j) by– promoting economic opportunity and competition– disseminating licenses across a wide variety of

applicants

Balanced Consensus 700 MHz Band Plan

Upper 700 MHz Band

*Blocks have been auctioned.+Please note that this Consensus Plan is submitted without prejudice to the signatories ability to support or oppose the Cyren Call proposal that would remove the Upper 700 MHz Band from the auction.

Balanced Consensus 700 MHz Band Plan

Lower 700 MHz Band

*Blocks have been auctioned.*Blocks have been auctioned.+Please note that this Consensus Plan is submitted without prejudice to the signatories+Please note that this Consensus Plan is submitted without prejudice to the signatories ability to support or oppose the Cyren Call proposal that would remove the Upper 700 ability to support or oppose the Cyren Call proposal that would remove the Upper 700 MHz Band from the auction.MHz Band from the auction.

Balanced Consensus Plan Signatories

• Alltel Corporation• Aloha Partners, L.P.• Blooston Rural Carriers • C&W Enterprises, Inc.• ConnectME Authority• Corr Wireless Communications,

LLC• Dobson Communications

Corporation• Leap Wireless International, Inc.

Maine Office of the Chief Information Officer

• MetroPCS Communications, Inc.

• National Telecommunications Cooperative Association

• Nebraska Public Service Commission

• North Dakota Public Service Commission

• Rural Cellular Association• Rural Telecommunications Group,

Inc.• Union Telephone Company• United States Cellular Corporation• Vermont Department of Public

Service• Vermont Office of the Chief

Information Officer• Vermont Public Service Board• Vermont Telephone Company,

Inc.

Cyren Call Proposal’s Impact on 700 MHz

• Cyren Call filed FCC petition for reallocation of 30 MHz of spectrum in the 747-762 MHz and 777-792 MHz bands for shared commercial and public safety use

• FCC dismissed petition ruling that a change in Sections 337 and 309 of the Act is required.

• Cyren Call is lobbying congress for the change• DTV Coalition is concerned

– Broadcast TV transition date will be pushed past 2/2009 – equipment makers will delay deployment of new

technologies while awaiting resolution of the issue

BRS/EBS formerly known as MMDS/ITFS

• BRS/EBS Transition:– Transition underway for BRS and EBS licensees.– Sprint and Clearwire changing high-power

systems to low-power data systems– Spectrum increasing in value; Finally multiple

equipment options.– FCC targets spectrum take-back and possible

auction in 2009.

WCS/2.3 GHz Band

WCS/2.3 GHz Band

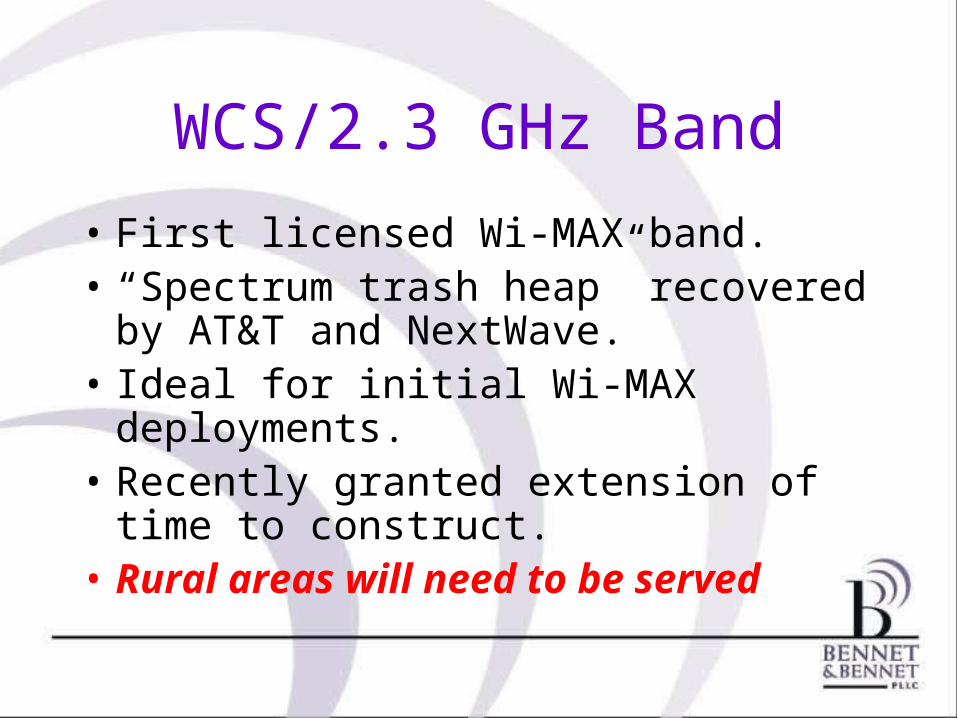

• First licensed Wi-MAX band.• “Spectrum trash heap” recovered by

AT&T and NextWave.• Ideal for initial Wi-MAX deployments.• Recently granted extension of time to

construct.• Rural areas will need to be served

Secondary Market Opportunities

• Partitioning and Disaggregation

• Spectrum leasing

• Resale/MVNO opportunities

Partitioning/Disaggregation

• Allows breaking larger areas up and recombining areas to tailor needs

• Occurs after auctions

• Build out requirements have to be considered

• Requires agreement from licensee

Leasing

• Using someone else’s spectrum through a lease arrangement

• Mainly on temporary basis while waiting on FCC approvals

• Bankruptcy issue• Affiliated companies• Not real popular among rural operators

MVNO

Mobile Virtual Network Operator• Cheap wireless entry – Available now• Position for 3 G, mobile data and m-commerce• Bundle with other existing service offerings• Utilizes large carrier network• Allows rural telcos to expand current telecom

service area• Positions telco to keep customer as landline

migration to wireless continues• Telispire® is choice of rural operators