emerging scenario in life insurance sector in...

TRANSCRIPT

Chapter V

Emerging Scenario in Life Insurance Sector in India

In a period of half a century more or less, the insurance sector in the country has

undergone circuitous movement, from an open competitive market to full

nationalization, and then back again to a liberalized market. Before liberalization, the

sector suffered from lack of marketing strategy, poorly trained agents, inadequate

infrastructure, investment restrictions and absence of uniqueness in services.

Consequently, the insurance sector was opened up in the year 1999 facilitating the entry

of private players into the industry. The year saw major structural changes with the

ending of government monopoly and the passage of the IRDA bill, lifting entry

restrictions for private players and allowing foreign players to enter the market with

some limits on direct foreign ownership (IRDA, Annual Report 2004-05).

The purpose of opening up the insurance industry was to enable the customers to have

better options with attractive array of products with salient features and benefits. It also

helped in bringing in huge foreign capital and offered employment opportunities

through insurance agency as a career to a large number of educated youth, both in urban

and rural areas. In other words, it can be said that liberalization has a positive impact on

the economy in terms of income generation and employment opportunities (IRDA,

Annual Report 2006-07). It is logical to surmise that in a country where there is a heavy

demand for life insurance which, in turn, should reflect a high level of insurance

penetration (Committee on Banking, Insurance and Pension, News updates, 17th

June

2009).

At the moment, the insurance sector in India has completed ten years in the liberalized

environment. The life insurance industry has undergone a total change and become

highly competitive and challenging. LIC, a Government monopoly till 2000, is now

experiencing the emergence of a competitive market. Besides, new players focus their

attention on smart marketing, efficient customer services and also on increasing the

coverage of the life insurance market. LIC is facing competitive challenges and IRDA is

playing a significant role in regulating and promoting life insurance business in India

(IRDA, Annual Report 2001-02).

Emerging Scenario in Life Insurance Sector in India

101

This chapter is an attempt to study the emerging scenario of life insurance sector in post

liberalization. It contains four sections. Section 5.1 provides detail of private players

entering the market. Section 5.2 refers to the innovations made by the insurers. Section

5.3 indicates performance of life insurers. Section 5.4 presents the challenges ahead for

life insurers while section 5.6 offers growth prospects.

5.1 Private Players

Liberalization of insurance sector has opened up tremendous business opportunities to

Indian and to foreign operators, to win the confidence of the people by providing them

better services and offering innovative products. A license to start up insurance business

was issued to the first private life insurance company as a sequel to liberalization in the

year 2000 (Sathe, 2009). Most of the new companies in the industry have entered the

market as joint ventures with the foreign partner holding 26 per cent of the total paid-up

equity capital (IRDA, Annual Report 2001-02). A proposal to increase this limit to 49

per cent is pending with the government (http://prasathr.sulekha.com).

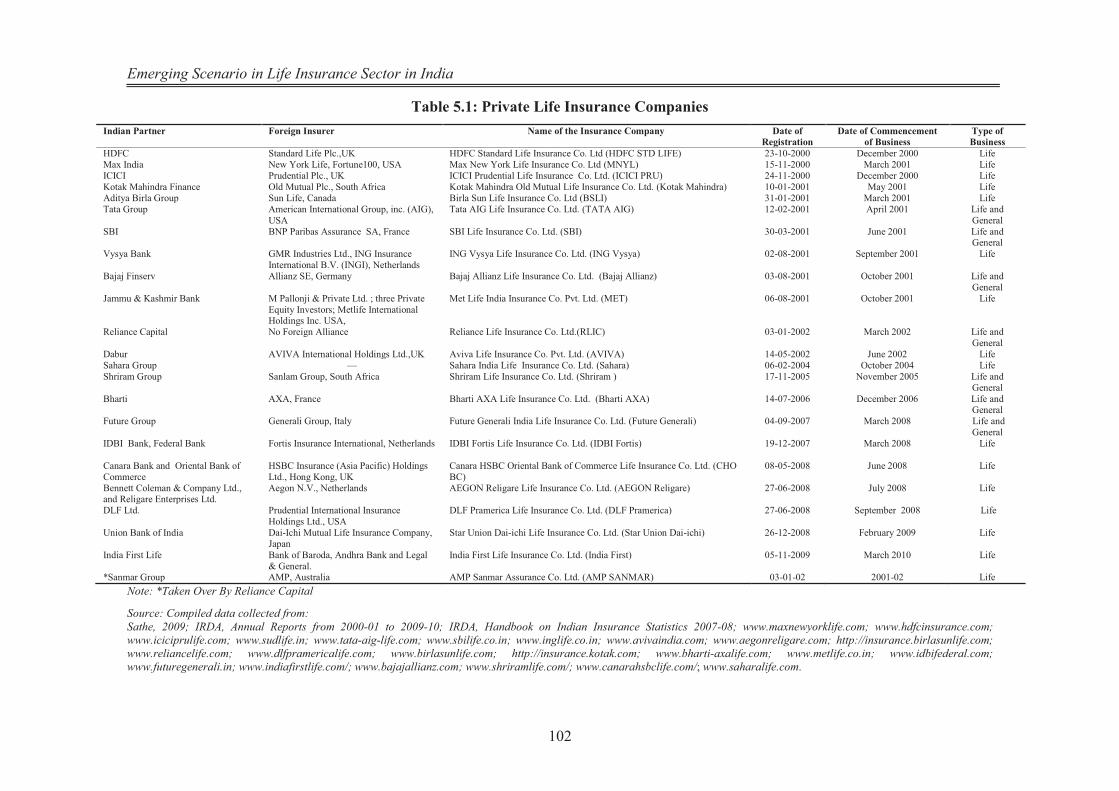

Table (5.1) gives a picture of the entry of the private players, the foreign partners, the

commencement as well as the fields of operation. Table shows that with the registration

of IndiaFirst Life Insurance Company in 2010-11, the total number went up to twenty

two and there could be more to follow in the near future. For instance, Canada-based

multinational insurance group, Manulife, is looking to partner with an Indian corporate

house in a life insurance joint venture. Other overseas insurance groups, such as South

Korea’s Samsung life, Scor Global of France and Japan’s Mitsui Sumitomo have also

shown interest to enter the Indian life insurance sector (Towers Watson, May 2010).

The private players with attractive as well as aggressive plans have created a niche for

themselves (IRDA, Annual Report 2000-01). They even predict good prospects for new

business through alliances and partnerships with domestic outfits. Their focus has been

on need based selling of life insurance business, which allows integration of assets,

liabilities, fund inflows and outflows and reconciles them with the important life events

such as children’s education, marriages, death, disability, critical illness and retirement

(Prudy, 2003).

Emerging Scenario in Life Insurance Sector in India

102

Table 5.1: Private Life Insurance Companies

Indian Partner Foreign Insurer Name of the Insurance Company Date of

Registration

Date of Commencement

of Business

Type of

Business

HDFC Standard Life Plc.,UK HDFC Standard Life Insurance Co. Ltd (HDFC STD LIFE) 23-10-2000 December 2000 Life

Max India New York Life, Fortune100, USA Max New York Life Insurance Co. Ltd (MNYL) 15-11-2000 March 2001 Life

ICICI Prudential Plc., UK ICICI Prudential Life Insurance Co. Ltd. (ICICI PRU) 24-11-2000 December 2000 Life

Kotak Mahindra Finance Old Mutual Plc., South Africa Kotak Mahindra Old Mutual Life Insurance Co. Ltd. (Kotak Mahindra) 10-01-2001 May 2001 Life

Aditya Birla Group Sun Life, Canada Birla Sun Life Insurance Co. Ltd (BSLI) 31-01-2001 March 2001 Life

Tata Group American International Group, inc. (AIG),

USA

Tata AIG Life Insurance Co. Ltd. (TATA AIG) 12-02-2001 April 2001 Life and

General

SBI BNP Paribas Assurance SA, France SBI Life Insurance Co. Ltd. (SBI) 30-03-2001 June 2001 Life and General

Vysya Bank GMR Industries Ltd., ING Insurance

International B.V. (INGI), Netherlands

ING Vysya Life Insurance Co. Ltd. (ING Vysya)

02-08-2001 September 2001 Life

Bajaj Finserv Allianz SE, Germany Bajaj Allianz Life Insurance Co. Ltd. (Bajaj Allianz) 03-08-2001 October 2001 Life and

General

Jammu & Kashmir Bank

M Pallonji & Private Ltd. ; three Private

Equity Investors; Metlife International Holdings Inc. USA,

Met Life India Insurance Co. Pvt. Ltd. (MET) 06-08-2001 October 2001 Life

Reliance Capital

No Foreign Alliance Reliance Life Insurance Co. Ltd.(RLIC) 03-01-2002 March 2002 Life and

General

Dabur AVIVA International Holdings Ltd.,UK Aviva Life Insurance Co. Pvt. Ltd. (AVIVA) 14-05-2002 June 2002 Life

Sahara Group — Sahara India Life Insurance Co. Ltd. (Sahara) 06-02-2004 October 2004 Life

Shriram Group Sanlam Group, South Africa Shriram Life Insurance Co. Ltd. (Shriram )

17-11-2005 November 2005 Life and

General

Bharti AXA, France Bharti AXA Life Insurance Co. Ltd. (Bharti AXA) 14-07-2006 December 2006 Life and General

Future Group Generali Group, Italy Future Generali India Life Insurance Co. Ltd. (Future Generali) 04-09-2007 March 2008 Life and

General

IDBI Bank, Federal Bank

Fortis Insurance International, Netherlands IDBI Fortis Life Insurance Co. Ltd. (IDBI Fortis)

19-12-2007 March 2008 Life

Canara Bank and Oriental Bank of

Commerce

HSBC Insurance (Asia Pacific) Holdings

Ltd., Hong Kong, UK

Canara HSBC Oriental Bank of Commerce Life Insurance Co. Ltd. (CHO

BC)

08-05-2008 June 2008 Life

Bennett Coleman & Company Ltd., and Religare Enterprises Ltd.

Aegon N.V., Netherlands AEGON Religare Life Insurance Co. Ltd. (AEGON Religare) 27-06-2008 July 2008 Life

DLF Ltd. Prudential International Insurance

Holdings Ltd., USA

DLF Pramerica Life Insurance Co. Ltd. (DLF Pramerica) 27-06-2008 September 2008 Life

Union Bank of India Dai-Ichi Mutual Life Insurance Company,

Japan

Star Union Dai-ichi Life Insurance Co. Ltd. (Star Union Dai-ichi) 26-12-2008 February 2009 Life

India First Life Bank of Baroda, Andhra Bank and Legal

& General.

India First Life Insurance Co. Ltd. (India First) 05-11-2009 March 2010 Life

*Sanmar Group AMP, Australia AMP Sanmar Assurance Co. Ltd. (AMP SANMAR) 03-01-02 2001-02 Life

Note: *Taken Over By Reliance Capital

Source: Compiled data collected from:

Sathe, 2009; IRDA, Annual Reports from 2000-01 to 2009-10; IRDA, Handbook on Indian Insurance Statistics 2007-08; www.maxnewyorklife.com; www.hdfcinsurance.com;

www.iciciprulife.com; www.sudlife.in; www.tata-aig-life.com; www.sbilife.co.in; www.inglife.co.in; www.avivaindia.com; www.aegonreligare.com; http://insurance.birlasunlife.com;

www.reliancelife.com; www.dlfpramericalife.com; www.birlasunlife.com; http://insurance.kotak.com; www.bharti-axalife.com; www.metlife.co.in; www.idbifederal.com;

www.futuregenerali.in; www.indiafirstlife.com/; www.bajajallianz.com; www.shriramlife.com/; www.canarahsbclife.com/; www.saharalife.com.

Emerging Scenario in Life Insurance Sector in India

103

5.2 Innovations in the Competitive Life Insurance Sector

One of the most essential requirements for survival and growth of an organization in a

competitive environment is to innovate continually (Biswas, 2008). Innovation

represents the adoption of new ideas, processes, products or services, developed

internally or acquired from the external environment (Mulford, 2005). The purpose of

innovation is not mere satisfaction of existing needs in a more delightful manner, i.e. by

means of value addition etc., but to create new and newer needs not existent before

(Tripathy, 2009). Service innovation, as defined here, is a process involved with the

transformation of an organization’s dormant assets (service elements which include

technology, service processes, environment and people) into something of substantially

greater value to both the customer and the organization (Crosby and Stephens, 1987;

Gronroos, 1990b; Parasuraman et al., 1985; Solomon et al., 1985).

The role of innovation, in the context of insurance, also assumes very high significance.

Consumers today not only need insurance, but also look for value added benefits like

premium waiver, free insurance in some form, premium holiday, guaranteed additions,

money-back at shorter intervals, competitive returns, accident/illness riders and what

not! (Tripathy, 2009). Growth in insurance industry has been spurred by product

innovations, vibrant distribution channels coupled with targeted publicity and

promotional campaigns by the insurers (IRDA, Annual Report 2003-04). All the new

entrants in the sector have established their own distribution channels and there has

been an energetic thrust for market share by all new players. The ancient behemoth,

LIC, is also energized to protect its falling market share by aggressively launching

innovative new plans. Meanwhile the insurance ‘cake’ itself has grown bigger, thanks to

the marketing initiatives of the new players. But there is enough potential for everyone

to tap more (David, 2009). The private players are coming out with innovative add

campaigns, more sophisticated and intelligent workforce and properly trained agents.

With the combined forces of increasing technological expertise, transformation in the

industry and innovative techniques working in the Indian market, the distribution

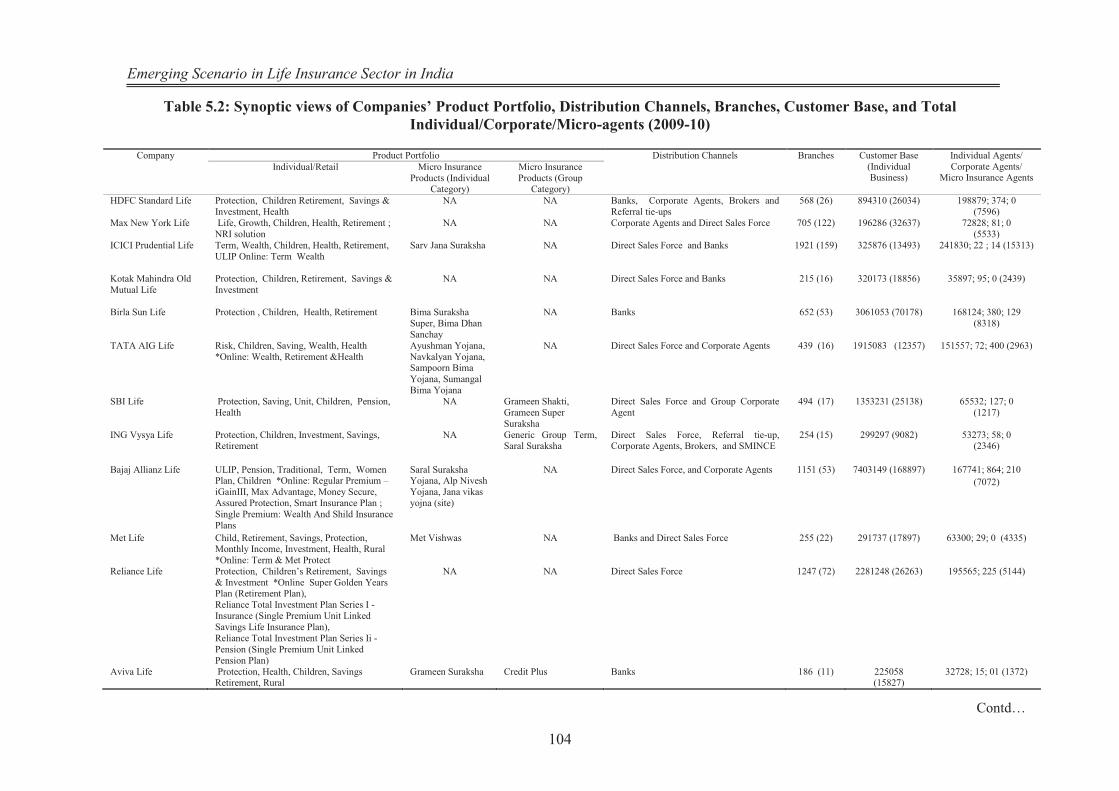

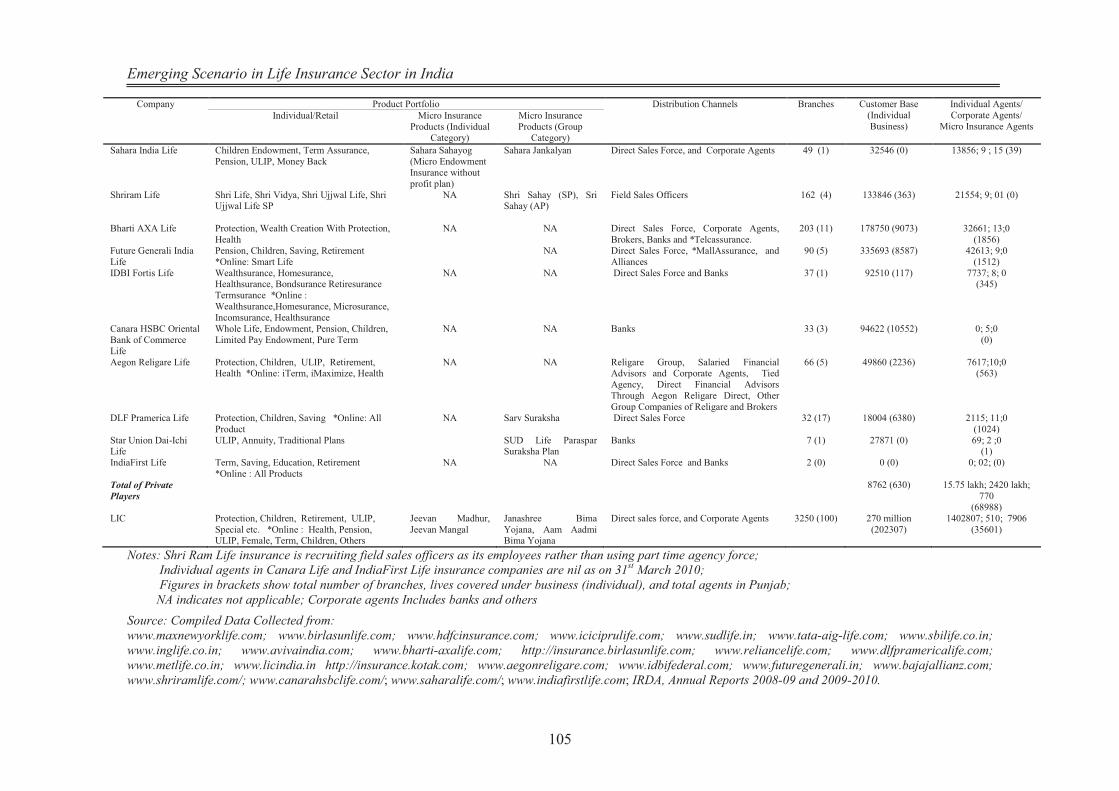

system seems to be widening. (Agrawal, 2002). Table 5.2 shows the synoptic views of

companies’ product portfolio, distribution channels, total number of branches, customer

base and total no. of individual/ corporate/ micro insurance agents till 2009-10.

Emerging Scenario in Life Insurance Sector in India

104

Table 5.2: Synoptic views of Companies’ Product Portfolio, Distribution Channels, Branches, Customer Base, and Total

Individual/Corporate/Micro-agents (2009-10)

Company Product Portfolio Distribution Channels Branches Customer Base

(Individual Business)

Individual Agents/

Corporate Agents/ Micro Insurance Agents

Individual/Retail Micro Insurance

Products (Individual Category)

Micro Insurance

Products (Group Category)

HDFC Standard Life Protection, Children Retirement, Savings &

Investment, Health

NA NA Banks, Corporate Agents, Brokers and

Referral tie-ups

568 (26)

894310 (26034)

198879; 374; 0

(7596)

Max New York Life Life, Growth, Children, Health, Retirement ;

NRI solution

NA NA Corporate Agents and Direct Sales Force 705 (122) 196286 (32637) 72828; 81; 0

(5533)

ICICI Prudential Life Term, Wealth, Children, Health, Retirement,

ULIP Online: Term Wealth

Sarv Jana Suraksha NA Direct Sales Force and Banks 1921 (159)

325876 (13493)

241830; 22 ; 14 (15313)

Kotak Mahindra Old

Mutual Life

Protection, Children, Retirement, Savings &

Investment

NA NA Direct Sales Force and Banks 215 (16)

320173 (18856)

35897; 95; 0 (2439)

Birla Sun Life Protection , Children, Health, Retirement Bima Suraksha

Super, Bima Dhan

Sanchay

NA Banks 652 (53)

3061053 (70178)

168124; 380; 129

(8318)

TATA AIG Life Risk, Children, Saving, Wealth, Health

*Online: Wealth, Retirement &Health

Ayushman Yojana,

Navkalyan Yojana, Sampoorn Bima

Yojana, Sumangal

Bima Yojana

NA Direct Sales Force and Corporate Agents 439 (16)

1915083 (12357) 151557; 72; 400 (2963)

SBI Life Protection, Saving, Unit, Children, Pension,

Health

NA Grameen Shakti,

Grameen Super

Suraksha

Direct Sales Force and Group Corporate

Agent

494 (17)

1353231 (25138) 65532; 127; 0

(1217)

ING Vysya Life

Protection, Children, Investment, Savings, Retirement

NA Generic Group Term, Saral Suraksha

Direct Sales Force, Referral tie-up, Corporate Agents, Brokers, and SMINCE

254 (15)

299297 (9082) 53273; 58; 0 (2346)

Bajaj Allianz Life ULIP, Pension, Traditional, Term, Women Plan, Children *Online: Regular Premium –

iGainIII, Max Advantage, Money Secure,

Assured Protection, Smart Insurance Plan ;

Single Premium: Wealth And Shild Insurance

Plans

Saral Suraksha Yojana, Alp Nivesh

Yojana, Jana vikas

yojna (site)

NA Direct Sales Force, and Corporate Agents 1151 (53)

7403149 (168897)

167741; 864; 210

(7072)

Met Life Child, Retirement, Savings, Protection, Monthly Income, Investment, Health, Rural

*Online: Term & Met Protect

Met Vishwas NA Banks and Direct Sales Force 255 (22)

291737 (17897)

63300; 29; 0 (4335)

Reliance Life Protection, Children’s Retirement, Savings

& Investment *Online Super Golden Years Plan (Retirement Plan),

Reliance Total Investment Plan Series I -

Insurance (Single Premium Unit Linked

Savings Life Insurance Plan),

Reliance Total Investment Plan Series Ii -

Pension (Single Premium Unit Linked

Pension Plan)

NA NA Direct Sales Force 1247 (72)

2281248 (26263)

195565; 225 (5144)

Aviva Life Protection, Health, Children, Savings Retirement, Rural

Grameen Suraksha Credit Plus Banks 186 (11) 225058 (15827)

32728; 15; 01 (1372)

Contd…

Emerging Scenario in Life Insurance Sector in India

105

Company Product Portfolio Distribution Channels Branches Customer Base

(Individual

Business)

Individual Agents/

Corporate Agents/

Micro Insurance Agents Individual/Retail Micro Insurance

Products (Individual

Category)

Micro Insurance

Products (Group

Category)

Sahara India Life Children Endowment, Term Assurance,

Pension, ULIP, Money Back

Sahara Sahayog

(Micro Endowment

Insurance without

profit plan)

Sahara Jankalyan Direct Sales Force, and Corporate Agents 49 (1) 32546 (0)

13856; 9 ; 15 (39)

Shriram Life Shri Life, Shri Vidya, Shri Ujjwal Life, Shri Ujjwal Life SP

NA Shri Sahay (SP), Sri Sahay (AP)

Field Sales Officers 162 (4)

133846 (363)

21554; 9; 01 (0)

Bharti AXA Life Protection, Wealth Creation With Protection,

Health

NA NA Direct Sales Force, Corporate Agents,

Brokers, Banks and *Telcassurance.

203 (11)

178750 (9073)

32661; 13;0

(1856)

Future Generali India

Life

Pension, Children, Saving, Retirement

*Online: Smart Life

NA Direct Sales Force, *MallAssurance, and

Alliances

90 (5)

335693 (8587)

42613; 9;0

(1512)

IDBI Fortis Life Wealthsurance, Homesurance, Healthsurance, Bondsurance Retiresurance

Termsurance *Online :

Wealthsurance,Homesurance, Microsurance,

Incomsurance, Healthsurance

NA NA Direct Sales Force and Banks 37 (1)

92510 (117) 7737; 8; 0 (345)

Canara HSBC Oriental

Bank of Commerce

Life

Whole Life, Endowment, Pension, Children,

Limited Pay Endowment, Pure Term

NA NA Banks 33 (3) 94622 (10552)

0; 5;0

(0)

Aegon Religare Life Protection, Children, ULIP, Retirement, Health *Online: iTerm, iMaximize, Health

NA NA Religare Group, Salaried Financial Advisors and Corporate Agents, Tied

Agency, Direct Financial Advisors

Through Aegon Religare Direct, Other

Group Companies of Religare and Brokers

66 (5)

49860 (2236)

7617;10;0 (563)

DLF Pramerica Life Protection, Children, Saving *Online: All

Product

NA Sarv Suraksha Direct Sales Force 32 (17) 18004 (6380)

2115; 11;0

(1024)

Star Union Dai-Ichi Life

ULIP, Annuity, Traditional Plans SUD Life Paraspar Suraksha Plan

Banks 7 (1) 27871 (0)

69; 2 ;0 (1)

IndiaFirst Life Term, Saving, Education, Retirement

*Online : All Products

NA NA Direct Sales Force and Banks 2 (0) 0 (0) 0; 02; (0)

Total of Private

Players

8762 (630) 15.75 lakh; 2420 lakh;

770

(68988)

LIC Protection, Children, Retirement, ULIP,

Special etc. *Online : Health, Pension, ULIP, Female, Term, Children, Others

Jeevan Madhur,

Jeevan Mangal

Janashree Bima

Yojana, Aam Aadmi Bima Yojana

Direct sales force, and Corporate Agents 3250 (100)

270 million

(202307)

1402807; 510; 7906

(35601)

Notes: Shri Ram Life insurance is recruiting field sales officers as its employees rather than using part time agency force; Individual agents in Canara Life and IndiaFirst Life insurance companies are nil as on 31st March 2010;

Figures in brackets show total number of branches, lives covered under business (individual), and total agents in Punjab;

NA indicates not applicable; Corporate agents Includes banks and others

Source: Compiled Data Collected from:

www.maxnewyorklife.com; www.birlasunlife.com; www.hdfcinsurance.com; www.iciciprulife.com; www.sudlife.in; www.tata-aig-life.com; www.sbilife.co.in;

www.inglife.co.in; www.avivaindia.com; www.bharti-axalife.com; http://insurance.birlasunlife.com; www.reliancelife.com; www.dlfpramericalife.com;

www.metlife.co.in; www.licindia.in http://insurance.kotak.com; www.aegonreligare.com; www.idbifederal.com; www.futuregenerali.in; www.bajajallianz.com;

www.shriramlife.com/; www.canarahsbclife.com/; www.saharalife.com/; www.indiafirstlife.com; IRDA, Annual Reports 2008-09 and 2009-2010.

Emerging Scenario in Life Insurance Sector in India

106

5.2.1 Products Portfolio

One of the prominent results of privatisation of insurance industry is the innovation of

products to cater to the needs of various sections of the population (Prabhakara, 2010).

Product innovation covers calls for a host of new things like a completely new product,

new product lines, in addition to the existing ones, improved or revised versions of the

product, and product repositioning (Tripathy, 2009). For the average customer, a

product is the most visible component that functions as the link between the corporate

entity and its clients. Considering the changing demands of the society, products need to

be revisited from time to time; and wherever necessary, appropriately tweaked

(Jawaharlal, 2010b).

By introducing new products like micro-insurance (for weaker sections of the

economy), unit linked plans (ULIP), health plans, pension plans etc., LIC and private

players are pushing up the insurance market (IRDA, Annual Report 2006-07). In the

changing scenario, consumers are increasingly becoming aware and are actively

managing their financial affairs. They are looking not just at products, but also at

integrated financial solutions that can offer stability of returns along with total

protection. In terms of returns, insurance products offer competitive returns ranging

between 7 percent and 9 percent. Moreover, the returns, the benefits of life protection

from life insurance products along with health cover are also going to increase (Kundu,

2004b). Besides providing affordable insurance protection against risks, the players’

achievements could also be assessed in terms of their sensitivity to the needs of the

market through introduction of tailor-made products aimed at specific segments of the

society, adoption of modern practices to upgrade technical skills, and a deeper

penetration of the insurance market in terms of Gross Domestic Product (GDP).

(IRDA, Annual Reports 2003-04, 2004-05). The comprehensive packaged products

have been popularized with features of endowment, money back, whole life, single

premium, regular premium, rebate in premium for higher sum assured, premium mode

rebate, etc., together with riders to the base products (IRDA, Annual Reports 2003-04,

2004-05).

Emerging Scenario in Life Insurance Sector in India

107

5.2.1.1 Health Protection Plans

In a modern competitive era, availability of riders, particularly health riders, has been a

positive development (Sathe, 2009). Jha (1999) commented that improvement in life

span and advancement in medical science had changed the customers’ needs for

insurance products worldwide. The focus of the insurers in the matured market of the

west had shifted to pension, health care and protection products.

Till date, only 12 (namely, Max Life, BSLI, Tata AIG Life, SBI Life, MetLife, Aviva,

IDBI Life, Bharti AXA Life, Aegon Life and LIC) out of 23 players have been taking

initiative to provide health insurance (as shown in Table 5.2) and others are in the

process of doing the same. Targeting to tap the country’s Rs. two lakh crore health care

industry, BSLI has entered the health insurance business with health solutions through

two plans namely, BSLI health plan and BSLI Universal Health Plan launched across

all key centers and states in the country (http://acumenbusinesshub.blogspot.com).

Likewise, Met Life has introduced: health care; HDFC Life: critical care & surgicare;

ICICI: health saver, hospital care II, crisis cover; Max Life: LifeLine medicash plus,

LifeLine safety net; SBI Life: group criti9 & hospital cash; TATA AIG Life: health

first, health protector, health investor, hospi cash back; and Bharti AXA Life: easy

health. LIC started a new health insurance division in 2007-08, to tap the vast potential

for health insurance business and to devise health products and services. The first

product ‘health plus’ was launched in February, 2008 and the second ‘health protection

plus’ in April, 2009. Both are unit linked health insurance policies providing for

hospitalization and major surgery cover for 49 specified surgeries. The plans also have a

facility of withdrawal, linked to domiciliary treatment. During 2009-10, 94135 health

insurance policies were sold by LIC for a premium income of Rs. 85.95 crore (LIC, 53rd

Annual Report 2009-10). In the year of 2009, LIC won the prestigious golden peacock

award (for innovative product) for its product viz., health plus (Kandwal, 2009a,b).

5.2.1.2 Unit-Linked Insurance Plans (ULIPs)

Unveiling the Unit Linked Life Insurance products is the biggest innovation in the life

insurance industry during the last decade (Prabhakara, 2010). The concept involved in

these unit or equity linked policies is that the major part of premium amounts paid over

Emerging Scenario in Life Insurance Sector in India

108

a period of years is invested in equities and other capital market instruments year after

year, the returns will be as per market orientation. In case of ULIP, the risk of death is

passed on to the re-insurer to a great extent, even as the risk of return and risk of

investment is passed on to the customers. Thereby the insurance companies retain a

very small portion of mortality risk with them. The lesser the risk retained, the lesser is

the requirement for solvency margin (Sathe, 2009). The launching of ULIP by various

companies is also significant example of innovation at work for the benefit of customers

who want high returns though it may involve an amount of risk (Tripathy, 2009). ULIP

is a form of product innovation in a specific market segment which represents majority

of the new business (Lepaud, 2008). ULIP are also responsible for enhancing

customers’ expectations of higher returns (15%-20%) in a short span of time (3yrs-

5yrs.). Every insurance company started rolling out ULIP products one after another

and the focus has shifted from ‘protection to investments’ (Ghosh, 2010).

In the case of new insurers, a significant contribution to the life insurance premium has

been from ULIP (IRDA, Annual Report 2003-04). IRDA approved the first Unit Linked

product on March 13, 2001, at that time the regulator wasn’t thinking at all that ULIP

products would have represented more than 90 percent of the new premium income for

the private players and more than 80 percent for LIC (Lepaud, 2008). AVIVA Life is

among the first companies to introduce the contemporary ULIP (www.avivaindia.com),

it has launched ‘wealth protect’ which guarantees the highest Net Asset Value (NAV).

Over the first seven years or that at maturity in the calculation of the maturity value

Future Generali Life launched ‘nivesh plan’, a single premium ULIP with the death

benefit of fund value plus sum assured. At maturity, policyholder may opt to receive the

entire fund value or a settlement option, under which the fund value will be payable in

annual installments up to five years from the date of maturity. Reliance Life has

introduced ‘super golden years’, term 10 years, a senior citizen plan, a ULIP with a

single or regular premium payment option (Towers Watson, May 2010). The Reliance

Life insurance company’s 97 percent income generates from ULIP (Committee on

Insurance and Pension, News updates, 10th

September, 2008). BSLI has introduced

group unit linked plan (www.birlasunlife.com). HDFC standard life has launched

Emerging Scenario in Life Insurance Sector in India

109

‘endowment champion ‘suvidha’, a ULIP plan. At maturity, along with the fund value,

the policyholder will also receive bumper additions’ depending on the policy term, in

lumpsum or in periodic installments over a period of up to five years, as chosen

(Towers Watson, May 2010). SBI Life’s unit-linked product inflows, contributed

almost 54 percent to its total premium income, ensuring a balanced mix of market-

linked and traditional products (www.sbilife.co.in). Tata AIG Life has introduced,

‘InvestAssure’, ‘InvestAssure II’ & ‘InvestAssure Plus’ etc. (www.tata-aig-life.com).

Although, Bajaj Allianz Life has also focused on women requirements by introducing a

plan namely, women insurance (miss confident plans); it’s also dealing in ULIP which

is further divided in regular premium (new unitgain, unitgain plus gold) and single

premium (new unitgain plus sp, new unitgain premier sp). It has just launched two more

products i.e., invest plus, and unit gain protection plus (www.bajajallianz.com). Sahara

Life has ULIP ‘group savings plus insurance’, ‘group term insurance’ and ‘group social

security schemes (www.saharalife.com). Aegon Religare Life has launched growth

plan, with zero premium allocation charges and an option of four funds. This product

also offers an invest-protect-option under which the policyholders’ funds are

automatically shifted from equity to debt in the last policy years (Towers Watson, May

2010). LIC has been a significant player in traditional life insurance products, it is now

gearing up to meet the competition and intends to introduce more unit linked products

in the market (IRDA, Annual Report 2003-04). LIC entered the niche marketing of the

unit linked product line when ‘bima plus’ was launched on February 12, 2001 (LIC

pamphlet). It also launched two new policies i.e., ‘bima gold’ and ‘jeevan plus’ both of

which are ULIP (Mathew, 2006, p 45). ‘Bima gold’ went on to win the golden peacock

award for the product innovation. It caught the fancy of customers and sales

intermediaries and its acceptability by the customers helped it cross the unimaginable

figure of one crore standing at 103,42,935 in a mere span of seven months that it was up

for sale. Never in the history of LIC had any new launch created anything near such

stupendous performance (Shukla, 2006b). Along with flagship product offerings –

namely, youngstar (children plan) and endowment (now branded as ProGrowth), HDFC

Life also has introduced a new product ‘sl crest’ , offering highest NAV guarantee fund

Emerging Scenario in Life Insurance Sector in India

110

option and a minimum guaranteed NAV of Rs. 15.0 at maturity. This new guaranteed

NAV fund has also been extended to other new products (www.hdfclife.com).

5.2.1.3 Other Plans

Met Life, Aegon Religare Life and DLF Life are providing individual rather than group

solution to the customers. IDBI Fortis Life is giving individual solution as well as group

solution in the form of micro insurance to its customers. Max New York Life and Bajaj

Life are also providing some of its group insurance plans in the form of ULIP and micro

insurance. Up to 2009-10, there were only two companies (namely, LIC and BSLI) in

the industry which are giving insurance solution to NRI (non residence of India). LIC

and Bajaj Allianz Life realized the need and designed special plan (jeevan bharti-I and

ul mahila gain I & II) exclusively for women (for detail see table 5.2).

BSLI is the first private life insurance player to introduce a pure term plan in the Indian

market (www.adityabirlanuvo.net). LIC’s ‘jeevan saral’ and ‘bima gold’ have done

precisly that for which these products have won the golden peacoack award from the

institute of directors for product innovation (Shukla, 2006b; Tripathy, 2009). India First

Life has launched two group plans, viz., group term and group credit life. The former is

a yearly renewable, pure term plan which offers life cover of a minimum of Rs. 5000

per member. The latter is offered against the loan to the borrowers of any common

lender, providing an option of a level or a reducing term insurance cover. Reliance Life

has also introduced traditional investment insurance plan, regular premium non-

participating saving plan. At maturity, the policyholder receives the accumulated value

of premium paid. BSLI recently launched ‘bachat (endowment) plan, a traditional non-

participating endowment plan with an option to pay premium through any mode. At

maturity, policyholders receive all monthly base premiums paid, earned bachat

additions and loyalty addition. DLF Pramerica has launched ‘dhan suraksha’ a saving-

cum-protection plan providing guaranteed benefits and guaranteed additions. It offers

money back equal to 15 percent of the sum assured at the end of every five years. At

maturity, policyholder will receive the guaranteed additions accrued and the sum

assured, less the money back benefit already paid (Towers Watson, May 2010). The

Economic Times dated January 31, 2011 has given Star Union Dai-ichi Life insurance

Emerging Scenario in Life Insurance Sector in India

111

company’s product ‘dhan suraksha – 3’ a 5-Star rating on product pricing. This is a

testimony to its endeavour in designing and launching of unmatched products. It is the

only product on reverse mortgage available in India with any life insurer in the country.

The company shall be coming out with similar unbeatable products in future

(http://sudlife.in/).

Moreover, several players have combined the riders or the add-ons to base products to

create several useful combinations that have caught the attention of the policyholders.

With the emphasis currently on ‘combi-products’, the policyholder fraternity will be

looking forward to packages that answer their personal financial planning requirements

(Jawaharlal, 2010b). The IRDA also issued guidelines on ‘health plus life combi

products’ paving the way for combined products whereby pure term life insurance

products can be offered by life insurance companies and standalone health insurance

products offered by non-life insurance companies under the umbrella of a single product

(IRDA, Annual Report 2009-10). Aviva Life Insurance, unveiled the ‘Aviva education

insights’, a research report with IMRB international. The report was based on the saving

habits of young parents, as well as threw light on the key concerns regarding a ‘child

education’. Keeping this in mind the company has launched a need-based product

portfolio with three new insurance products, ‘aviva young scholar secure’, ‘aviva young

scholar advantage’ and ‘aviva i-life’ (Committee on Banking, Insurance and Pension,

News updates, 3rd

March 2011). Star Union Dai-ichi Life has come out with a new

traditional endowment product ‘defined benefit endowment plan'. The product ensures

regular tax -free monthly benefit for 15 years (Committee on Banking, Insurance and

Pension, News updates, 15th

September 2010). Being the county’s largest life insurer,

the products of LIC have an edge over other private insurance products on the cost

structure. LIC endowment plan, a vanilla type I plan, offers the highest net yield among

its peer group. The product is simple and efficient. The equity fund offered under the

scheme has generated a return of 118 percent in five years, making the scheme an

investor’s delight (Committee on Banking, Insurance and Pension, News updates, 6th

January 2011).

Emerging Scenario in Life Insurance Sector in India

112

5.2.1.4 IRDA Initiatives towards Policyholder Protection

IRDA has a very important role to play among the insurance players in the market. Its

primary function is to regulate the insurance sector allowing a healthy competition but

without compromising on consumer interest. This means ensuring proper disclosures,

keeping affordable prices and making sure that the claims are paid by the insurers.

Consumer education is also one of the important functions that the regulator has to

perform. IRDA issues guidelines on all aspects of insurance business like product

pricing, intermediaries, social responsibility, rural business, investment, solvency

margin etc. (Sathe, 2009).

With a view to protect the interests of policyholders, the IRDA has taken a number of

initiatives in the current financial year 2010-11. The objective of these initiatives is to

rationalise the product features through such clauses as: (i) minimum lock-in period

being increased from three years to five years; (ii) individual products to have a

minimum policy term of five years, although group products continue to be on annual

renewable basis; (iii) all products including pension/annuity to have a minimum sum

assured payable on death; (iv) the facility of partial withdrawal to be permissible only

after the fifth policy anniversary for individual products (IRDA, Annual Report 2009-

10); (v) life insurance companies are directed to disclose in the benefit illustration

issued to the policyholders, the level of commission paid to the distributor (Towers

Watson, May 2010); (vi) all ULIPs other than pension and annuity products shall

compulsorily provide minimum life/mortality/health cover; (vii) ULIPs other than

single premium period shall have minimum premium paying term of five years; (viii)

all regular premium/limited premium ULIPs shall have uniform/level paying premiums.

Any additional payments shall be treated as single premium for the purpose of

insurance cover; and (xi) as regards pension products, all ULIP pension/annuity

products shall offer a minimum guaranteed return of 4.5 percent per annum or as

specified by IRDA from time to time. The objective of the same is to protect the

lifetime savings of pension policyholders from any adverse fluctuations at the time of

maturity (Prabhakara, 2010).

Emerging Scenario in Life Insurance Sector in India

113

5.2.2 Alternate Distribution Channels

Innovations come not only in the form of benefits attached to the products, but also in

the delivery mechanism through various marketing tie-ups both in the realm of financial

services and outside. All these efforts have brought life insurance closer to the customer

as well as made it more relevant (IRDA, Annual Reports 2005-06, 2007-08). In a

competitive scenario, the scope of alternative channels along with their potential is seen

as an important or an encouraging feature to extend insurance coverage (Mathur, 2003).

Distribution plays an important role for a company not only in hawking their products

but also providing exemplary customer service. Typically, alternate channel in the

insurance industry comprises of different verticals which are institutions such as

corporate agents, brokers, cooperative banks and other business associates. Most of

these institutions have a common ground in terms of dealing with financial products,

but their customer segments and profiles may vary (Bajaj Allianz, 2010).

5.2.2.1 Agency Force

Personal selling is a major promotional tool of many companies. One industry that uses

predominantly sales personnel to promote its products and services is insurance.

Although some insurers employ direct mail, print, and broadcast advertising to market

their programs, insurance agents tend to be the driving marketing force for many

insurers (Meidan, 1982). The most common model for distributing and servicing

insurance is through one of several varieties of an agency model (Redja, 1998). The

contracted agency receives a commission from the insurer for each policy it sells

(Brown and Churchill, 1999). An insurance policy is almost always sold by an agent

who, in 80 percent of the cases, is the customer’s only contact (Richard and Allaway,

1993; Clow and Vorhies, 1993; Crosby and Cowles, 1986). The quality of the agent’s

service and his/her relationship with the customer serves to either mitigate or aggravate

the perceived risk in purchasing the life insurance product. Putting the customer first,

and, exhibiting trust and integrity have been found to be essential in selling insurance

(Slattery, 1989). Customer surveys by Prudential have identified that customer wants

more responsive agents with better contact, personalized communications from the

insurer, accurate transactions, and quickly solved problems (Pointek, 1992). A different

Emerging Scenario in Life Insurance Sector in India

114

study by the National Association of Life Underwriters found other important factors

such as financial stability of the company, reputation of the insurer, agent integrity and

the quality of information and guidance from the agent (King, 1992). According to

Chowdhury et al. (2007), insurer must have to carefully choose smart & presentable

personnel and train and make them knowledgeable regarding the services of the

organization to interact well with the customers. Moreover, communicative training

must be provided to the sales people.

Agents are brand ambassadors of the insurer. Agency channel with immense potential is

the flagship channel of the company contributing substantially to the profit of the

company (Bajaj Allianz, 2010). Private players are competing with over 14 lakh strong,

experienced, and skilled agency force of LIC. So far the Star Union Dai-ichi Life has

been selling its products through its bank partners, now it has launched a tied agency in

the country, at Patna. The company, through the tied-agency channel, aspires to

approach the customers in person, addressing their needs and providing them assurance

for a happy and secure living. Therefore, the company has special and strong focus on

training of its insurance advisors (http://sudlife.in). BSLI is the first company to start

toll free line for agent services and provide various services to the agents and customers

over phone (www.maxnewyorklife.com). Besides, Bajaj Allianz has developed a

dedicated team which understands the requirement of different distributors and provides

them need-based services such as customized solution, administrative, training and

operational support like offsite receipting, etc. to process proposals at an expressed

speed and service the customer better (Bajaj Allianz, 2010). In India, insurance agency

is still seen as a part-time occupation. The challenge before insurance companies is to

turn agents into professionals (Committee on Banking, Insurance and Pension, News

updates, 17th

June 2009).

Table 5.2 shows, as on 31st March 2010, in India, the total number of agents registered

with LIC stood at 14.03 lakh (13.45 lakh in 2008-09). The corresponding number for

private sector insurers was 15.75 lakh (15.93 lakh in 2008-09) (IRDA, Annual Report

2009-10). While, private life insurers reported a decrease of 1.13 percent, LIC showed

an increase of 4.31 percent in number of individual agents. The attrition was higher in

Emerging Scenario in Life Insurance Sector in India

115

case of private sector insurers as against LIC. As on 31st March, 2010, the number of

corporate agents registered with LIC stood at 510 lakh (415 lakh in 2008-09). The

corresponding number for private sector insurers was 2420 lakh (2091 lakh in 2008-09)

(IRDA, Annual Report 2008-09, 2009-10). Private life insurers and LIC reported an

increase of 15.73 percent and 22.89 percent, respectively. Overall, there is an increase

of 16.9 percent in corporate agents in the life insurance industry. Furthermore, Table 5.2

depicts that in Punjab, total number of agents of private players decreased by 13 percent

during 2009-10 (68988 during 2009-10 as against 79209 during 2008-09), whereas, LIC

had 35601 agents during 2009-10 as against 33184 agents during 2008-09, this shows

an increase of 7.28 percent.

5.2.2.2 Bancassurance

Bancassurance as a channel for distributing insurance products through banks has

picked up in India in a big way. Bancassurance model provides a win-win situation for

the partners i.e. Banks – who get alternate revenue stream by fee income besides

offering their customers a one-stop shop for all their financial needs and for the

Insurers– it is increasing their presence through the bank's network of branches (Bajaj

Allianz, 2010). For example, bancassurance is highly developed in France where

banking networks account for a significant proportion of life insurance sales, although

they are taking longer to make inroads into the non-life market (Benoist, 2002).

Bergendahl (1995) claimed that the economic reasons for banks selling multiple

products include efficiently using fixed capacity resources, customer demand for

several products from a single channel, and product combination strategy.

As far as bancassurance channel is concerned, banks can either have their own

executives to sell multiple policies or have a referral model where the agent of the

company sits in the branch. The stakes are high indeed on bancassurance. There are a

couple of banks that earned nearly Rs. 400 crore each through insurance commissions,

and around eight private and foreign banks that earned commissions, of up to Rs 100

crore by way of insurance sales (Committee on Banking, Insurance and Pension, News

updates, 17th

June 2009). The bancassurance model is a cost effective and is also quite

efficient for market penetration. This is for the simple reason that since the banking and

Emerging Scenario in Life Insurance Sector in India

116

insurance industry share a common target of financial services to customers, the

existing customer base of banks can be targeted rather than building a new one

(Agrawal, 2002). The bancassurance channel accounts for about 25 per cent of the total

new premium collected by the life insurance industry. For insurers, based on the

business strategy and the number of tie-ups, the contribution from bancassurance varies.

It also helps life insurance companies spread their distribution networks. By entering

into a tie-up, life insurance companies leverage on the partner bank’s customer base and

branch presence. BSLI is the first player in the industry to sell its policies through

bancassurance route (www.adityabirlanuvo.net). Bajaj Allianz currently has over 160

bancasurrance partners in the life and non-life domains (Bajaj Allianz, 2010).

ICICI Prudential Life has tie-ups with its parent ICICI bank and Bank of India (BOI). It

ties-up with many other co-operative banks to sell policies (www.mydigitalfc.com).

Aviva Life is also accredited with the introduction of bancassurance in India. Its

bancassurance collaborations offer five hundred towns and cities connectivity

(www.indiahousing.com/aviva-life). Bharti AXA Life is reportedly keen to secure a

bank as a third partner in its life insurance business. IndiaFirst Life has recently

launched joint venture of legal and general of UK with two state owned banks, viz.,

Bank of Baroda and Andhra bank, and plans to have a multi-channel approach rather

than remaining a bancassurance channel only insurer. Its products are currently

available at 1750 branches of its partner banks. Reliance Life has tie-up with 25

cooperative banks for bancassurance business and intends to use their network for

insurance sales. Tata AIG Life has entered into a tie-up with Chennai central

cooperative bank limited (CCCB), to sell insurance products across the state of

Tamilnadu through the 64 branches of the bank (Towers Watson, Jan-March 2010).

Private life insurance companies have designed various innovative distribution channels

to sell policies, but these channels are not free from challenges. While most of the

players having a bank as a joint venture partner and many life insurance companies in

operation are finding it difficult to find bancassurance partners since most of the banks

already have existing tie-ups with one or the other insurers. For example, Bharti AXA

Life, Aegon Religare Life have been looking for partners for a long time, but in vain.

Emerging Scenario in Life Insurance Sector in India

117

Though sectoral regulator IRDA rules permit life insurance companies to tie up with

only two national banks for bancassurance, some insurers that are joint ventures

between non-bank entities are finding it hard to locate even a single bancassurance

partner. Max New York Life has entered into a ten year exclusive corporate agency

distribution agreement with Axis bank, a leading private sector bank. Axis bank

previously had a distribution tie-up with Met life (Towers Watson, Jan-March 2010). As

shown in Table 5.2, except Dlf Pramerica Life, Future Generali Life, Shriram Life ,

Reliance Life, all other players have entered into a tie-up with the banks for

bancassurance business.

5.2.2.3 Retail Outlets

As shown in Table 5.2, life insurers like Future Generali Life and Bharti Axa Life are

using their parent companies’ retail outlets for selling their policies. Future Generali

pioneered the concept of distributing insurance products through its ‘MallAssurance™

channel wherein it uses 192 malls of the Future Group to woo customers besides other

conventional sales channels to sell its insurance solutions (Kumar, 2009). It has seen

early positive acceptance from retail customers with over 2.75 lakh customers picking

up policies across the counter at retail outlets. About 50 per cent of the company’s

business is generated through the agency route, 30 per cent through Mallassurance and

the remaining 20 percent through alliances. Future Generali Life has MallAssurance

store at particular locations like Big Bazaar, e-zone, Food Bazaar, Furniture Bazaar,

Home Town, KB Fair Price and Pantaloons. Customer can reach the nearest Insurance

Desk by selecting the appropriate outlet (www.futuregenerali.in). In the financial year

2010, the company generated Rs. 42 crore or nearly 10 percent of its total first year

premium through this route and hopes to retain this at the same level in the ongoing

fiscal (Committee on Insurance and Pension, News updates, 3rd

September 2010).

Likewise, Bharti AXA Life launched national operations in December 2006 at Mumbai,

as a mass market player with a multi-channel distribution strategy comprising agents,

corporate agents and brokers, bancassurance and telcassurance. Telcassurance is Bharti

AXA Life’s innovation in life insurance distribution. This channel aims to reach out to

over 71 million customers of Bharti Airtel. As its first Telcassurance initiative, the

Emerging Scenario in Life Insurance Sector in India

118

company established its presence in 360 Airtel Relationship Centres (ARCs) spread

across 41 cities in India. Its initiative at the ARCs includes having dedicated financial

advisors, relevant branding and product literature (Chopra, 2008). Telcassurance

accounts for about 20 percent of the policies sold at Bharti Axa Life

(www.mydigitalfc.com).

5.2.2.4 Online Selling of Insurance Policies/ Direct Marketing

The increased price competition was expected to lead to a rise of lower-cost direct

distribution channels (e.g., Muth, 1999), backed by technological progress, which

permits selling of insurance products via the Internet (e.g., Cattani et al., 2004).

Insurance products are information products that can easily be converted into a digital

format. Hence, there is an obvious potential for electronic commerce in the insurance

industry. Insurance companies are becoming more visible on the Internet and it is

possible to buy certain types of insurance directly on the web. This will make cross-

border trade much more viable than today, as services can be delivered directly to the

customer without involvement of a local subsidiary (Falch, 1998). The benefits of using

this medium are manifold, ranging from availability round the clock, quick transactions,

instant payment and receipt and access to insurance experts just at a few clicks of the

mouse, besides convenience (Bajaj Allianz, 2010).

Direct-distribution insurers have the advantage that they are able to provide their

services at lower costs compared to insurance firms which use agents, bank branches

and other third parties to distribute their products. Cost advantages result from the

absence of commission costs, which leads to lower operating expenditures. The cost

advantage allows direct insurers to offer lower premiums (e.g., Ennew and Waite,

2007). In the UK, 60 percent of the motor insurance business is done over the Internet

and phone (Kumar, 2008). Private life insurers have taken to developing their online

channels to further spread their distribution in a cost effective manner. Typical products

offered include protection, endowment, pension, health and guaranteed plans. To attract

customers to buy online companies are offering a range of incentives including lower

premiums and reduced charges (Towers Watson, Jan-March 2010). However, this is an

excellent medium for routine transactions like renewals, checking NAVs, fund switch

Emerging Scenario in Life Insurance Sector in India

119

options for ULIPs and purchase of policies where detailed underwriting is not required

(Bajaj Allianz, 2010).

Table 5.2 indicates that due to technology advancement, some of the companies now- a-

day are able to provide online product buying facility to its customers. BSLI Life and

Reliance Life are the first companies which have started to provide life insurance

product online (retirement plan, total investment plan series I - insurance, and total

investment plan series II - pension) to the customers (www.adityabirlanuvo.net;

www.reliancelife.com). LIC is also providing some of its products relating to health,

pension, ULIP, term, children, female protection etc. online. Besides, as shown in table,

online product buying facility is also made available by other players viz., ICICI

Prudential Life (i.e. term & wealth plans); MetLife (term & met protect plan); Tata

AIG Life (wealth, retirement, health); Future Generally Life (smart life); IDBI Life

(wealth, home, micro, term., income, health plans); Aegon Life (iTerm, iMaximize,

health plans); DLF Life (any policy); and HDFC Life (youngstar super suvidha,

pension super, endowment super suvidha). If customers purchase HDFC Life’s

products online then they are entitled to a discount of 40 percent on the first and second

year premium allocation charges (Towers Watson, May 2010). It expects the online

channel to contribute around 2-3 percent of sales in the next five years (Towers Watson,

Jan-March 2010). In the case of IndiaFirst Life, all products are available online. Most

of these companies now-a-days are using only the Internet for marketing its products

and to provide general information. Some companies also offer quotation facilities

calculating the price for a specific type of insurance on the basis of information typed in

by the customer (e.g. age and health condition).

Moreover, the use of multi-channel distribution may be more able to meet the needs of

existing customers (Tsay and Agrawal, 2004). Firms with broad product lines will

particularly benefit from the distribution via multiple channels (Webb, 2002). The

customers may also save on search costs or transaction costs by holding a multiple-

product relationship with a single insurance firm. Wallace et al. (2004) observed that a

multiple channel distribution strategy serves as an instrument to increase customers’

satisfaction and customer loyalty in an increasingly competitive environment. It is

Emerging Scenario in Life Insurance Sector in India

120

expected that the future market will be intermediary driven, where agents, brokers, and

banks will play a major role. Moreover, MallAssurance and Telcassurance will also

have a significant function in the days to come. A strong focus on training of the

distribution force will help the industry to market the life insurance products through

multi-channel distribution network and to build long lasting relationship with

customers. India is estimated to have the third largest online population in the world by

2013. India’s number of Internet users was 52 million in 2008 and the average annual

growth rates will be 10 to 20 percent over the next five years i.e. 2008-2013

(http//hdfclife.com).

5.3.3 Branches and Customer Base

Financial year 2009-10 was the year for consolidating business for most players with

many of the leading private players rationalizing their branch and agency expansion to

focus on increasing distribution and operational efficiency (Towers Watson, Jan-March

2010).

Table 5.2 shows total number of branches and customer base of different players in

India and in Punjab. In respect of number of branches, LIC has 3250 branches in India

out of which 100 are operated in Punjab. Private players have 8768 branches in India

out of which 630 are established in Punjab. Among private players, ICICI Prudential

Life has a large number of branches - 1921 in India, out of which 159 have been opened

up in Punjab. There has been large increase in the branches setup from the year 2007-

08 to 2009-10, for example, branches of BSLI Life increased from 33 to 53 followed

by DLF Life (7 to 17); Future Gerarali Life (1 to 5); Kotak Life (9 to 16); Max Life (

33 to 122); Met Life (4 to 22); Reliance Life (57 to 72); SBI Life (6 to 17); Tata Life

(10 to 16); and LIC (75 to 100). Some of the private players’ viz., Shriram Life, Star

Union Life, Sahara Life, and IDBI Life have just launched their branches in Punjab.

Among the private players, Bajaj Allianz Life has covered the maximum number

(7403149) of lives out of which 168897 pertained to Punjab during 2009-10. LIC has

270 million customer base out of which 202307 are from Punjab (as shown in table

5.2).

Emerging Scenario in Life Insurance Sector in India

121

5.3.4 Rural/Micro-insurance

Tailor made products have been launched to meet the aspirations of the rural populace

and the evolving needs of a growing economy, both in the manufacturing and the

service sectors (IRDA, Annual Report 2003-04). According to Micro-insurance

Regulations, issued in 2005 by IRDA, ‘Micro’ refers to the small financial transaction

that each insurance policy generates and it is insurance with low premiums and low

caps/coverage (Arora, 2009). The micro-insurance may be defined as an insurance

solution directed at low-income groups who have small savings capacity; it incorporates

either or composite features of life, general, and health insurance and is managed by a

professional insurance company that operates on marketing principles (Shukla, 2006a).

In order to face competitive market, instead of depending on insurance agents, LIC and

private players have now entered the micro-insurance business to maintain a direct

contact with their customers by maximizing the use of technology.

As per the findings made by Associated Chambers of Commerce and Industry of India

(ASSOCHAM), the private sector insurance players have started exploring the rural

markets in which until recently, the state owned companies had the monopoly. The

Chamber has projected that in rural markets, the share of private insurance players

would increase substantially as these have been able to generate a faith among their

rural consumers. To understand the prospects for insurance companies in rural India, it

is very important to understand the requirements of India’s villagers-farmers, craftsmen,

milkmen, weavers, casual labourers, construction workers and shopkeepers and so on.

More often than not, they are into more than one profession. The ASSOCHAM found

that there are a total 124 million rural households. Nearly 20 per cent of all farmers in

rural India own Kissan Credit Cards. The 25 million credit cards used till date offer a

huge data base and opportunity for insurance companies. An extensive rural agent

network for sale of insurance products could be established. The agent can play a major

role in creating awareness, motivating purchase and rendering insurance services. There

should be nothing to stop insurance companies from trying to pursue their own unique

policies and target whatever needs they want in rural India. ASSOCHAM suggests that

Emerging Scenario in Life Insurance Sector in India

122

insurance needs to be packaged in such a form that it appears as an acceptable

investment to the rural people (www.asiaeconomywatch.co.uk).

Bajaj Allianz Life has put a cap on the size of the policy sold in rural areas to increase

sales, while Max New York Life has asked agents to find out how much life insurance

one would need in rural areas to cover their needs and provide a policy accordingly. For

selling policies in villages, most of the players are going to tie-up with district central

co-operative banks and regional rural banks. Bajaj Allianz Life has capped the ticket

size of the policies sold in rural areas at Rs. 10,000. This will help agent to change their

interest in the market, without focusing too much on commissions. Reliance Life is also

designing products to suit the emerging markets, as the company has observed that the

premium-paying capacity of people residing in rural areas is comparatively lower.

Focus on flexible mode of payment is also needed. LIC accounts for only 30 percent of

the total business premium from rural areas. Insurers are betting big on their rural

divisions and have lined up plans to aggressively increase their market share by cost-

effective distribution models (Committee on Insurance and Pension, News updates,

2009). Aviva Life kicked off a series of awareness road shows across 78 villages -

‘Khushiyan Di Gaddi’ in Punjab with its bank assurance partner Punjab and Sind Bank.

The company also launched a new group product – Aviva Sampoorna Suraksha Bima

Yojna, customised for the customers of Punjab and Sind Bank (Committee on Banking,

Insurance and Pension, News updates, 27th

March, 2011). DLF Pramerica Life in

collaboration with “SREI Sahai e-village” has launched an awareness initiative called

“Tatkaal Baithaks” aimed at educating the rural customers about the need and benefits

of life insurance. The campaign expects to see a participation of about one million

customers in 93 villages across the states of Bihar, Orissa and Uttar Pradesh. Max New

York Life has invested in 130 offices in rural markets till 2009-10 and has around

10000 agents in the rural distribution channel (Towers Watson, May 2010).

So far, most of the insurance companies in India are not actively tapping the huge

potential of the rural markets. The present insurance business is not even able to

penetrate 20%–30% of the total population of 1.095 billion, and the projected

Emerging Scenario in Life Insurance Sector in India

123

population figure. The order of the day would be to refocus on micro-insurance in India

to capture the huge potential of rural customers (www.iijournals.com).

Recently most of the life insurance companies have developed a range of micro-

insurance products (mainly Pure Term, and Term with refund of premium) for the

benefit of the BPLP (below the poverty line population) (Lepaud, 2008). Table 5.2

exhibits micro-insurance products (under the heading of product portfolio) introduced

by life insurance companies. Fourteen life insurance players have, so far, launched 28

micro-insurance products to meet the needs and cover specific risk of household and a

few more are in the process of doing the same. LIC, Sahara India Life, and Aviva Life

have taken the initiative to give individual and as well as group solutions to the

customers in the form of micro-insurance. Each of them and TATA AIG launched four

products where as ING Vysya Life, ICICI Prudential Life, Met Life, IDBI Fortis Life,

DLF Pramerica Life, Star Union Dai-ichi Life launched only one product, followed by

Bajaj Allianz Life, Birla Sun Life, SBI Life, Shri Ram Life which has launched two

micro-insurance products each respectively. Through these various schemes, the life

insurance companies have insured 198.26 lakh individuals during 2009-10. Total

number of micro-insurance agents in the industry on 31st March 2010 were 8676 (LIC:

7906; private insurers: 770) as against 7250 during the year 2008-09. Among the private

players, Tata AIG Life and Bajaj Allianz Life have recruited maximum micro-insurance

agents i.e. 400 and 210 respectively. The total premium income under micro-insurance

portfolio for the year 2009-10 was Rs. 402 crore. It nearly doubled from the previous

year’s premium income of Rs. 206 crore. While LIC contributed 94 percent of the total

premium under micro-insurance, the remaining 6 percent was contributed by the private

insurers. Thus, micro-insurance vertical of LIC in its 3½ years of existence, has

provided risk cover protection to the most vulnerable sections of society through 4.5

million micro insurance policies. Micro-insurance policies have been sold through a

distribution channel comprising of non government organizations, self help groups,

micro finance institutions, non-profit associations, corporate agents, brokers, and non-

profit societies including companies registered under Section 25 of Companies Act and

business correspondents for banks and government agencies who have been appointed

Emerging Scenario in Life Insurance Sector in India

124

as micro-insurance agents by LIC (LIC, 53rd

Annual Report 2009-10). The launching of

‘jeevan madhur’ by LIC is a bright example of innovation that caters to the needs of

billions of poor and needy people who need insurance the most, but have low-paying

capacity. In fact micro insurance in LIC has ushered in an insurance revolution in a

micro way (Tripathy, 2009). Moreover in the year of 2009, LIC won the prestigious

SKOCH Challenger Award for micro-insurance business (http://licbidani.com).

BSLI has launched its rural program in 2001 to provide insurance to the rural populace

of India. This includes the endowment product that provides life cover and guarantees

returns to the insured on maturity. By virtue of the benefits it provides, this product has

been very well accepted and has gone on to become the most popular product in the

rural areas (http://insurance.birlasunlife.com/). It is observed that all players are

planning to establish more branches and trying to increase the strength of their agency

force in order to increase their market share in the months ahead. For all the players

there is a scope to tap rural sector as a part of social responsibility as well as to increase

their insurance business in terms of market share. The government has mooted a

separate regulatory authority for micro-insurance and IRDA is likely to initiate action

on this front (Committee on Insurance and Pension, News updates, 29th

September

2008).

5.3.5 Other Innovations or Miscellaneous

5.3.5.1 LifeMaker™ a simple tool

ING Life follows a "customer centric approach" while designing its products. It has

developed an exclusive tool - the LifeMakerTM

, a simple tool which helps customers to

choose a plan most suitable to them, based on their needs, requirements and current life

stage. This tool helps to build a complete financial plan for life at every lifestage,

whether the requirement is protection, savings, retirement or investment

(www.inglife.co.in).

5.3.5.2 National Premium Payment Service

Aviva Life insurance and India Post have announced a nation-wide strategic partnership

for National Premium Payment Service. Aviva Life insurance customers can make

Emerging Scenario in Life Insurance Sector in India

125

premium payments at any of the 8,294 computerized post offices across the country

without any additional cost. The premium amount collected by the post offices will be

transferred to Aviva Life insurance company through the e-payment system of India

Post (www.avivaindia.com).

5.3.5.3 Free Look Period

One dynamic process that could come into play here is the introduction of the free look

period. By studying the clauses of the insurance contract, the policyholder can decide

whether to hold on to the contract or not (Jawaharlal, 2010). BSLI is the first company

to provide free look period of 15 days to the customer. This was later made mandatory

by the regulator (www.maxnewyorklife.com).

5.3.5.4 Pick Ur Advisor

ING life has launched an online tool called “pick ur advisor” which allows prospective

customers to choose a financial advisor. The selection can be made using various

parameters such as location, qualification, and the agents’ tenure with the company

(Towers Watson, Jan-March 2010).

5.3.5.5 Customer Delight through the Customer Care Unit (CCU)

Customer Care Unit acts as the face of the insurance company by serving as the

interface for all customer queries and complaints. The CCU was setup at Bajaj Allianz

to streamline servicing customers. The 270-member multi-lingual call center team

functions as a single touchpoint for customers for requests on policy servicing, claims

intimation, product information or resolution of a complaint. To ensure that the team

responds to these queries and complaints in a benchmarked Turn-Around-Time (TAT),

CCU has put in place a number of initiatives that have helped to reduce the time taken

to respond, as well as to qualitatively enhance the information given to them (Bajaj

Allianz, 2010).

5.3.5.6 Interactive Voice Response System (IVRS)

First time entrant in the industry, AEGON Religare Life offers policy servicing on the

phone via Interactive Voice Response System (IVRS) by issuing the customer a T-Pin

Emerging Scenario in Life Insurance Sector in India

126

for authentication (www.aegonreligare.com). The company launched its pan-India

multi-channel operations in July, 2008 with over 30 branches spread across India

(www.India PRWire.com).

5.3.5.7 E-Portfolio Statement

ICICI Prudential Life launched its E-Portfolio statement, a first of its kind service in the

life insurance industry, which will provide consumers with a customised e-statement

with their complete investment details on a monthly basis. It will provide the customer a

detailed summary of all his ULIP policies with the company. E-portfolio statements will

be e-mailed to customers on a monthly basis as a ready reckoner of their investments

with the company (Committee on Banking, Insurance and Pension, News updates, 26th

August 2008).

5.3.5.8 LifeStore

IndiaFirst Life has announced the launch of LifeStore – a ‘do-it-yourself’ website which

aims to help customers transact their insurance requirements on the basis of authentic

information, online advice, services and realistic expectations. Through LifeStore,

IndiaFirst Life will now be tapping the approximately 70 million Internet users in India.

The digital medium is a growing category and is still untapped. The company is looking

at further expanding onto the mobile platform and interactive kiosks as well. Apart from

simplifying insurance and reducing fear about the category, this will bring the concept

of transparency to the fore and increase channels for the customers to reach insurance

service providers (Nandagopal, 2011).

5.3.5.9 Mobile Phones

Max New York Life has announced the launch of a convenient and secure payment

solution for its policyholders using their mobile phones. Powered by Citibank and

mChek, this smart and secure solution enable policyholders to pay their renewal

premiums, subscribe to and top-up investments in ULIPs and links the charges to their

preferred bank account (Sharma, 2008). Now Future Generali Life has joined hands

with ATOM Technologies to provide an IVR-based premium payment and renewal

facility. All the policyholder has to do is make payments using his/her credit card on the

Emerging Scenario in Life Insurance Sector in India

127

mobile itself. To avail of this service, the policyholder will need to get in touch with the

insurer’s call centre and talk to the customer service representative. The representative

will start the three way conference call between the customer, ATOM and himself.

Following that the IVR will prompt the customer to feed in the credit card details using

the mobile phone’s keypad. Then the authorization will be read out when the traction is

completed (www.bimadeals.com).

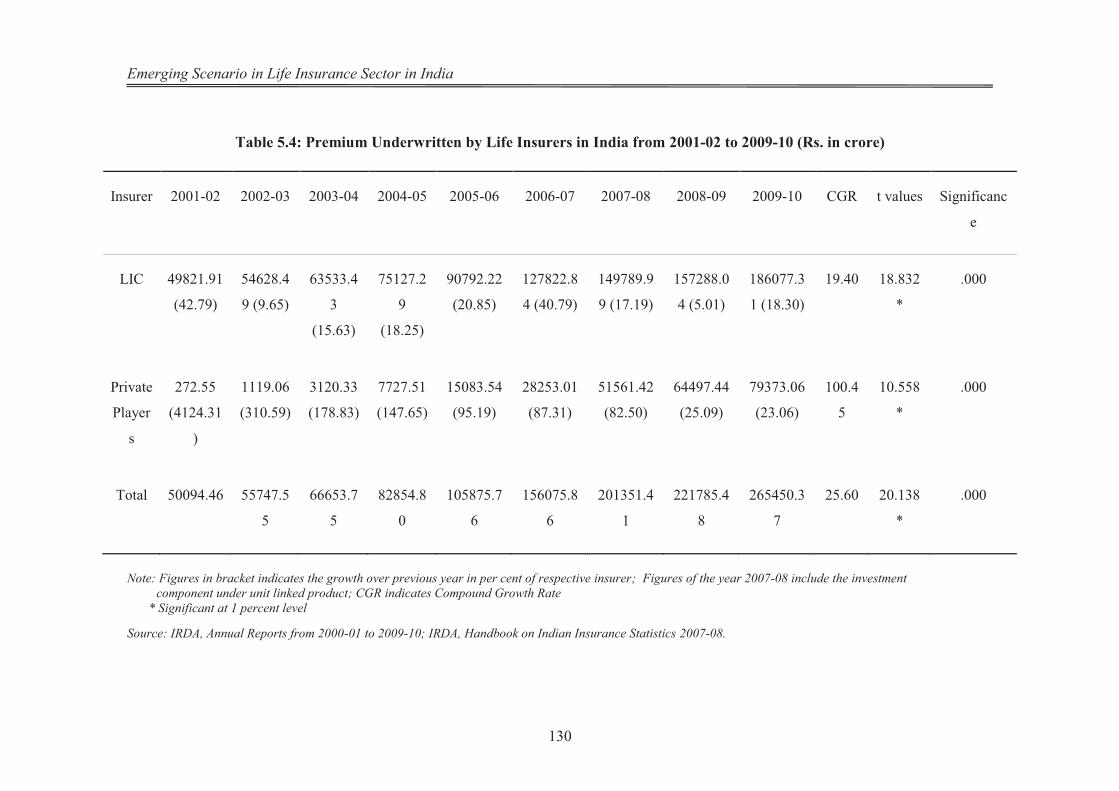

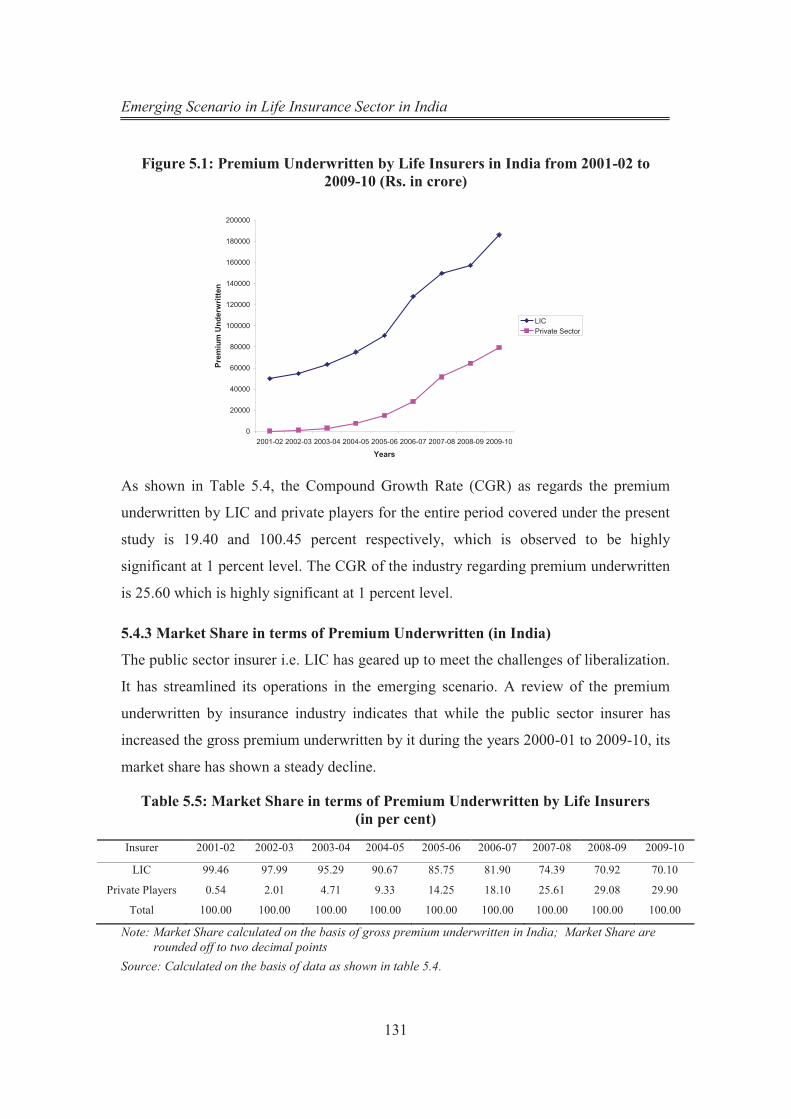

5.4 Performance of Life Insurers

The growth in the life insurance sector would also have a spiraling impact on the

economy as a whole in terms of employment generation, improvement in the standards

of living of the populace and the growth in the investment in the industry &

infrastructure (IRDA, Annual Report 2002-03). With a huge population base and large

untapped market, insurance industry is a big opportunity area in India for national as

well as foreign investors. India is the fifth largest life insurance market in the emerging

insurance economies globally and is growing at 32-34 per cent annually. This

impressive growth in the market has been driven by liberalization

(www.reportbuyer.com; www.bharatbook.com).

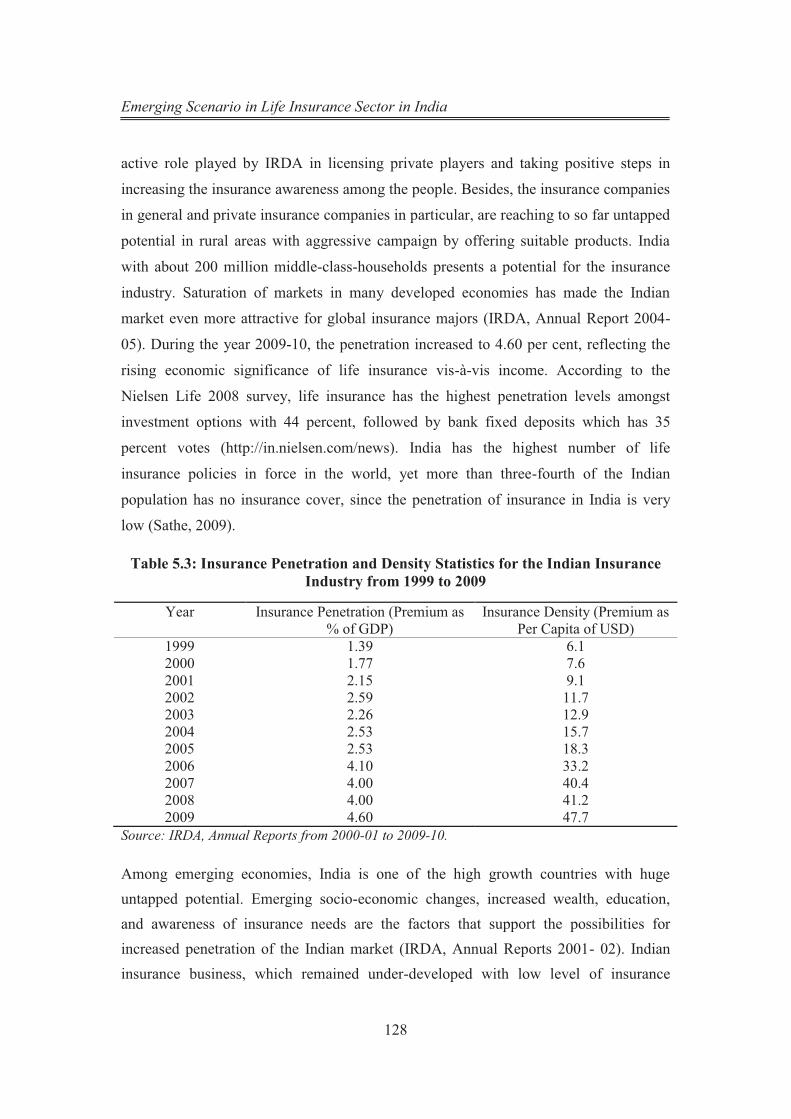

5.4.1 Penetration and Density of Life Insurance Sector in India

The insurance penetration in a country depends on its level of economic activity, risk

awareness among the people and the deepening of the financial system. It is therefore,

desirable to assess India’s position with respect to insurance penetration and density

(IRDA, Annual Report 2006-07). To increase market penetration, several insurers also

entered into strategic alliances with banking institutions to leverage on their branch

network to meet the financial needs of the banking customers (Vel, 2005). There are

indications exhibited in Table (5.3) that the advent of new players has increased both

the insurance density (premium as per capita) and the insurance penetration

(expenditure for insurance services expressed as a percentage of income or premium as

a percentage of Gross Domestic Product).

The life insurance penetration in India was less than 1 percent till 1990-91. During the

1990s, it hovered between 1 and 2 percent and from 2001 it was over 2 percent. During

the year 2006 the penetration increased to 4.10. The impetus for increase is due to the

Emerging Scenario in Life Insurance Sector in India

128

active role played by IRDA in licensing private players and taking positive steps in

increasing the insurance awareness among the people. Besides, the insurance companies

in general and private insurance companies in particular, are reaching to so far untapped

potential in rural areas with aggressive campaign by offering suitable products. India

with about 200 million middle-class-households presents a potential for the insurance

industry. Saturation of markets in many developed economies has made the Indian

market even more attractive for global insurance majors (IRDA, Annual Report 2004-

05). During the year 2009-10, the penetration increased to 4.60 per cent, reflecting the

rising economic significance of life insurance vis-à-vis income. According to the

Nielsen Life 2008 survey, life insurance has the highest penetration levels amongst

investment options with 44 percent, followed by bank fixed deposits which has 35

percent votes (http://in.nielsen.com/news). India has the highest number of life

insurance policies in force in the world, yet more than three-fourth of the Indian

population has no insurance cover, since the penetration of insurance in India is very

low (Sathe, 2009).

Table 5.3: Insurance Penetration and Density Statistics for the Indian Insurance

Industry from 1999 to 2009

Year Insurance Penetration (Premium as

% of GDP)

Insurance Density (Premium as

Per Capita of USD)

1999 1.39 6.1

2000 1.77 7.6

2001 2.15 9.1

2002 2.59 11.7

2003 2.26 12.9

2004 2.53 15.7

2005 2.53 18.3

2006 4.10 33.2

2007 4.00 40.4

2008 4.00 41.2

2009 4.60 47.7

Source: IRDA, Annual Reports from 2000-01 to 2009-10.

Among emerging economies, India is one of the high growth countries with huge

untapped potential. Emerging socio-economic changes, increased wealth, education,

and awareness of insurance needs are the factors that support the possibilities for