elliott d. pollack & company freudian economics to: gfoaz budget forum october 21, 2011 by: jim...

TRANSCRIPT

Elliott D. Pollack & Company

Freudian EconomicsTo:

GFOAz Budget Forum

October 21, 2011

By:Jim Rounds

Senior V.P., Elliott D. Pollack & Company

Elliott D. Pollack & Company

Freudian EconomicsThe Stooges Go to Washington

To:

GFOAz Budget Forum

October 21, 2011

By:Jim Rounds

Senior V.P., Elliott D. Pollack & Company

Elliott D. Pollack & Company

Freudian EconomicsD.C. Budget Balancing Tools:LOTS OF SEATS STILL AVAIL!

To:

GFOAz Budget Forum

October 21, 2011

By:Jim Rounds

Senior V.P., Elliott D. Pollack & Company

Elliott D. Pollack & Company

Going from Economic to

Psychological

“Tell me about your mother”

Elliott D. Pollack & Company

Going from Economic to

Political…

“Whoop whoop!”

Elliott D. Pollack & Company

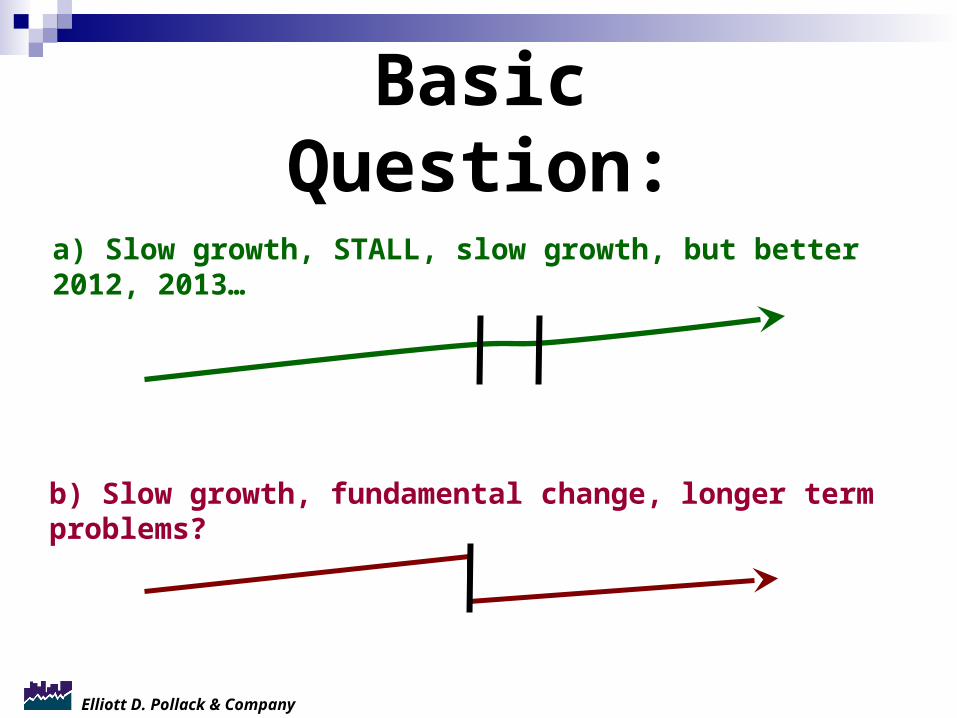

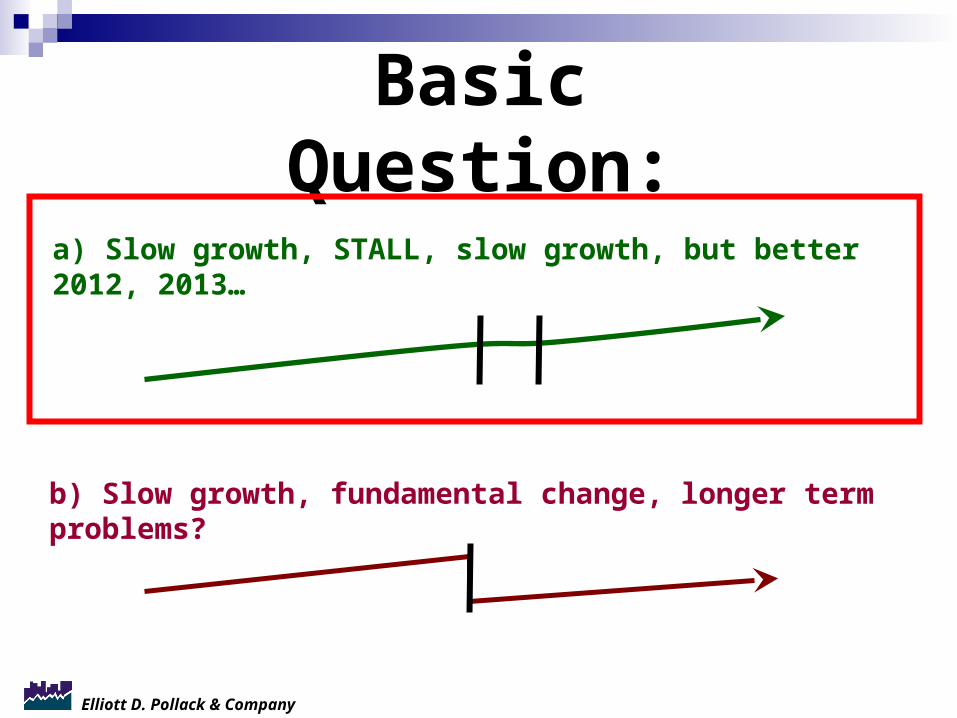

a) Slow growth, STALL, slow growth, but better 2012, 2013…

b) Slow growth, fundamental change, longer term problems?

Basic Question:

Elliott D. Pollack & Company

U.S. Conditions

Elliott D. Pollack & Company

Signs of a Double Dip – Look for Declines in these Main

Economic Categories

Real GDP Real Income Employment Industrial Production Wholesale – Retail Sales

Elliott D. Pollack & Company

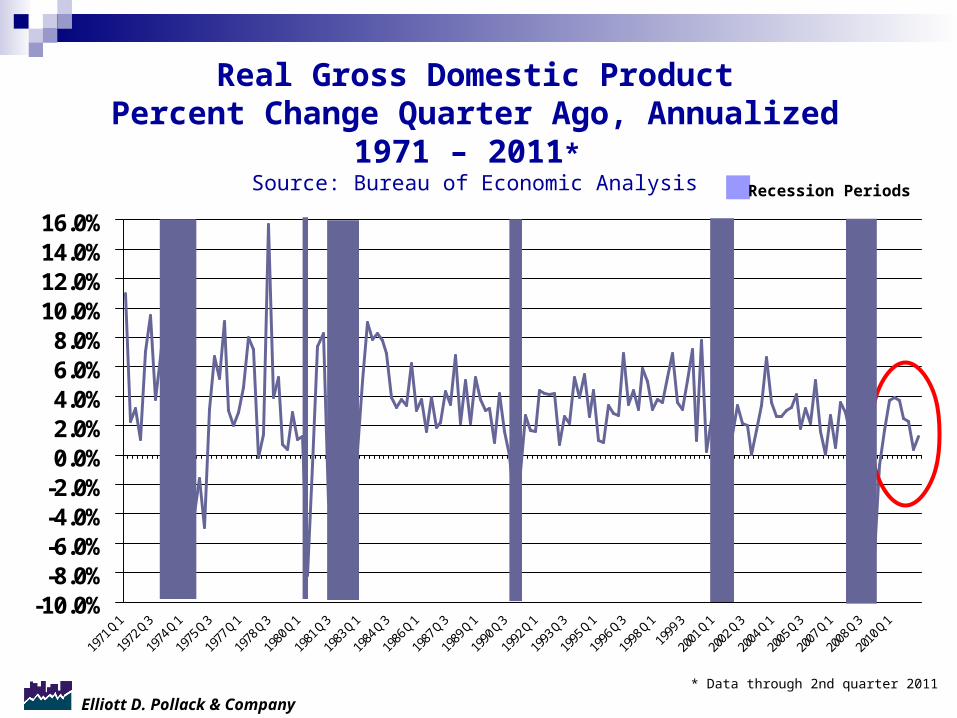

Real Gross Domestic ProductPercent Change Quarter Ago, Annualized

1971 – 2011* Source: Bureau of Economic Analysis

-10.0%-8.0%-6.0%-4.0%-2.0%0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%

1971 Q

1

1972 Q

3

1974 Q

1

1975 Q

3

1977 Q

1

1978 Q

3

1980 Q

1

1981 Q

3

1983 Q

1

1984 Q

3

1986 Q

1

1987 Q

3

1989 Q

1

1990 Q

3

1992 Q

1

1993 Q

3

1995 Q

1

1996 Q

3

1998 Q

1

1999 3

2001 Q

1

2002 Q

3

2004 Q

1

2005 Q

3

2007 Q

1

2008 Q

3

2010 Q

1

* Data through 2nd quarter 2011

Recession Periods

Elliott D. Pollack & Company

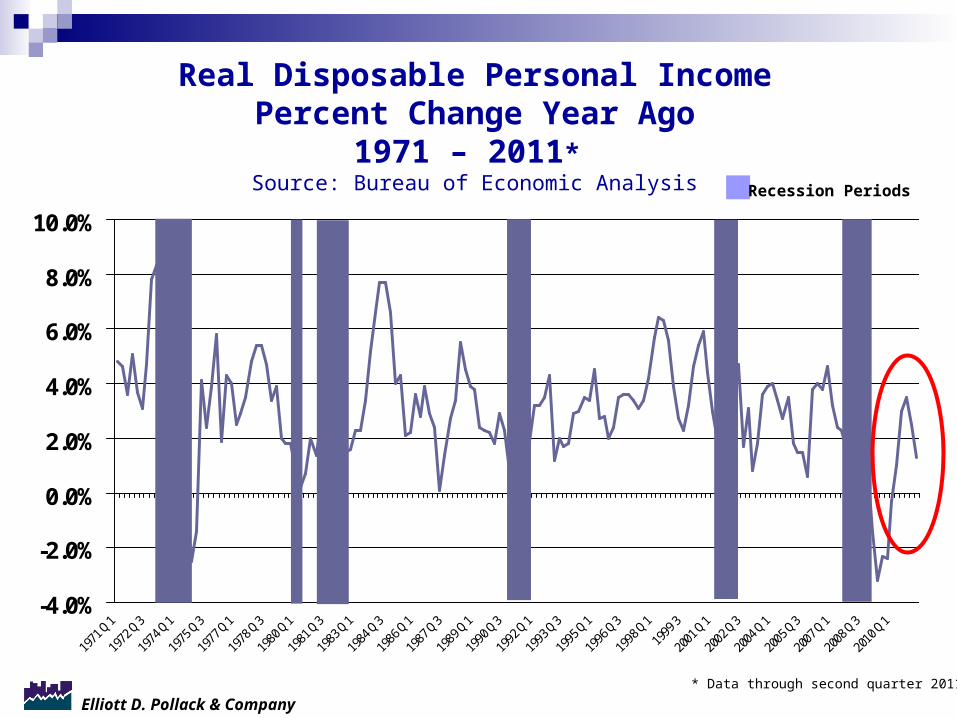

Real Disposable Personal IncomePercent Change Year Ago

1971 – 2011* Source: Bureau of Economic Analysis

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1971 Q

1

1972 Q

3

1974 Q

1

1975 Q

3

1977 Q

1

1978 Q

3

1980 Q

1

1981 Q

3

1983 Q

1

1984 Q

3

1986 Q

1

1987 Q

3

1989 Q

1

1990 Q

3

1992 Q

1

1993 Q

3

1995 Q

1

1996 Q

3

1998 Q

1

1999 3

2001 Q

1

2002 Q

3

2004 Q

1

2005 Q

3

2007 Q

1

2008 Q

3

2010 Q

1

* Data through second quarter 2011

Recession Periods

Elliott D. Pollack & Company

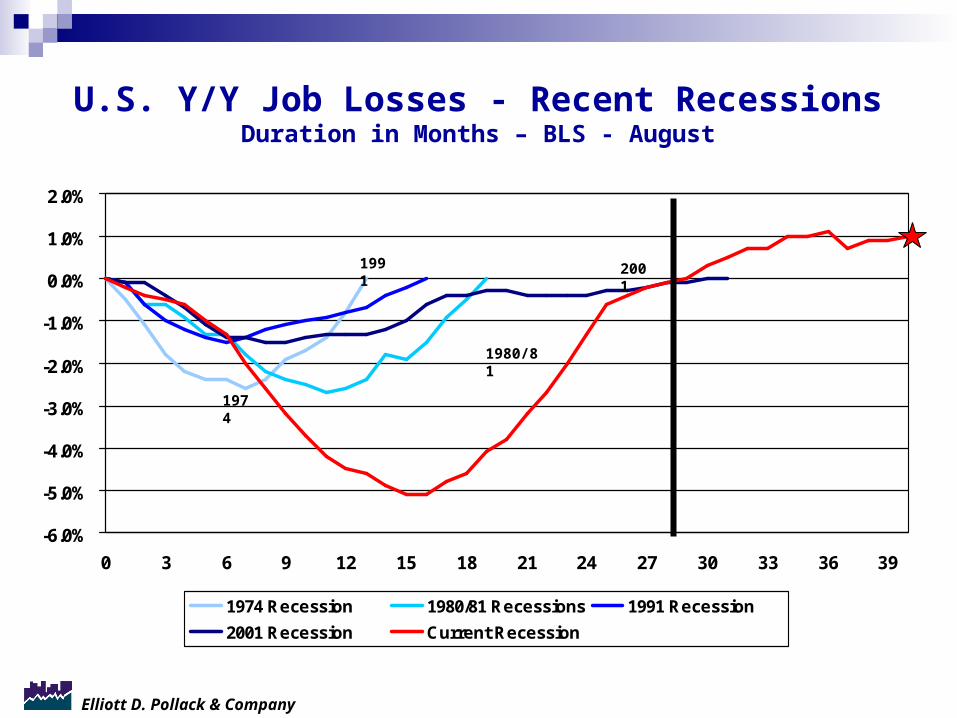

U.S. Y/Y Job Losses - Recent RecessionsDuration in Months – BLS - August

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

0 3 6 9 12 15 18 21 24 27 30 33 36 39

1974 Recession 1980/81 Recessions 1991 Recession

2001 Recession Current Recession

1980/81

1974

20011991

Elliott D. Pollack & Company

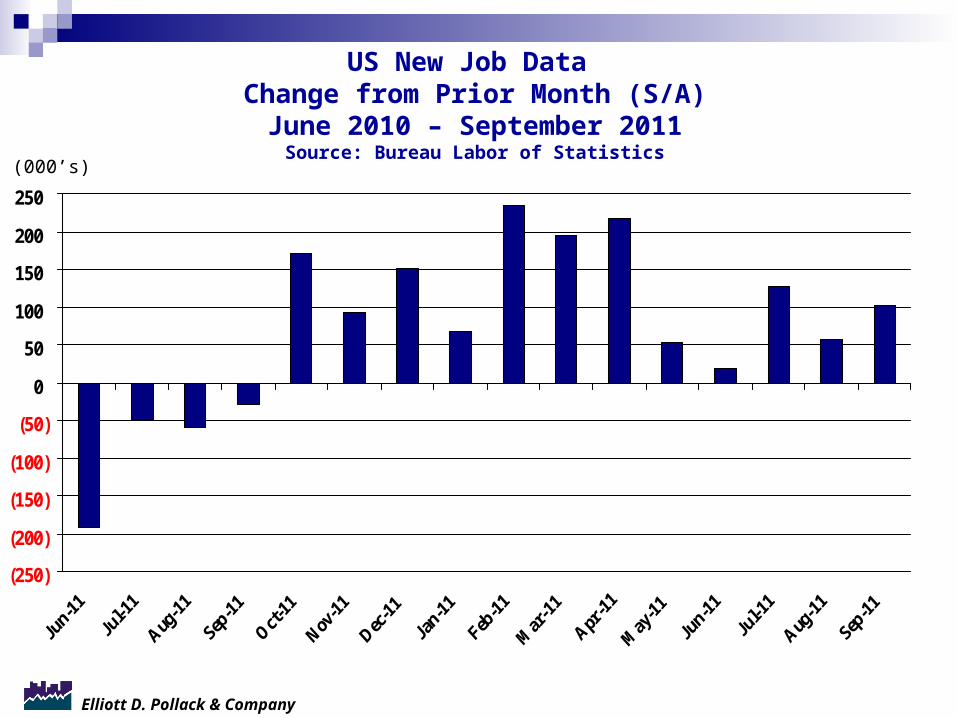

US New Job Data Change from Prior Month (S/A)June 2010 – September 2011

Source: Bureau Labor of Statistics

(250)

(200)

(150)

(100)

(50)

0

50

100

150

200

250

(000’s)

Elliott D. Pollack & Company

Industrial ProductionPercent Change Year Ago

1973 – 2011* Source: The Conference Board

-16%-14%-12%

-10%-8%-6%-4%-2%0%

2%4%6%8%

10%

12%14%16%

*Data through July 2011

Recession Periods

Elliott D. Pollack & Company

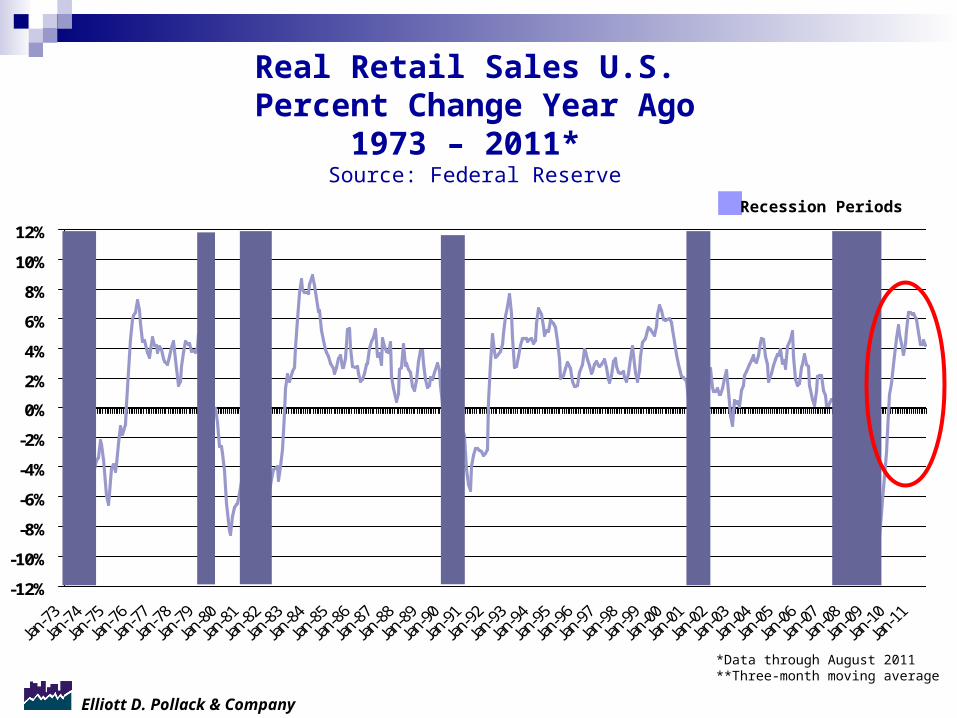

Real Retail Sales U.S. Percent Change Year Ago

1973 – 2011* Source: Federal Reserve

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

*Data through August 2011**Three-month moving average

Recession Periods

Elliott D. Pollack & Company

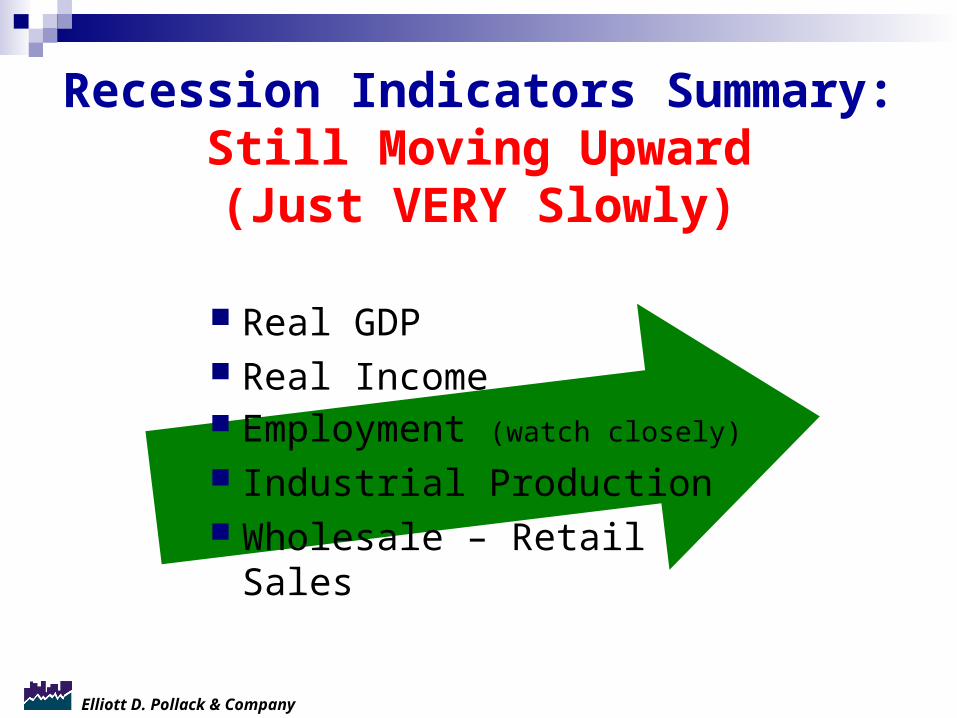

Recession Indicators Summary:Still Moving Upward(Just VERY Slowly)

Real GDP Real Income Employment (watch closely)

Industrial Production Wholesale – Retail Sales

Elliott D. Pollack & Company

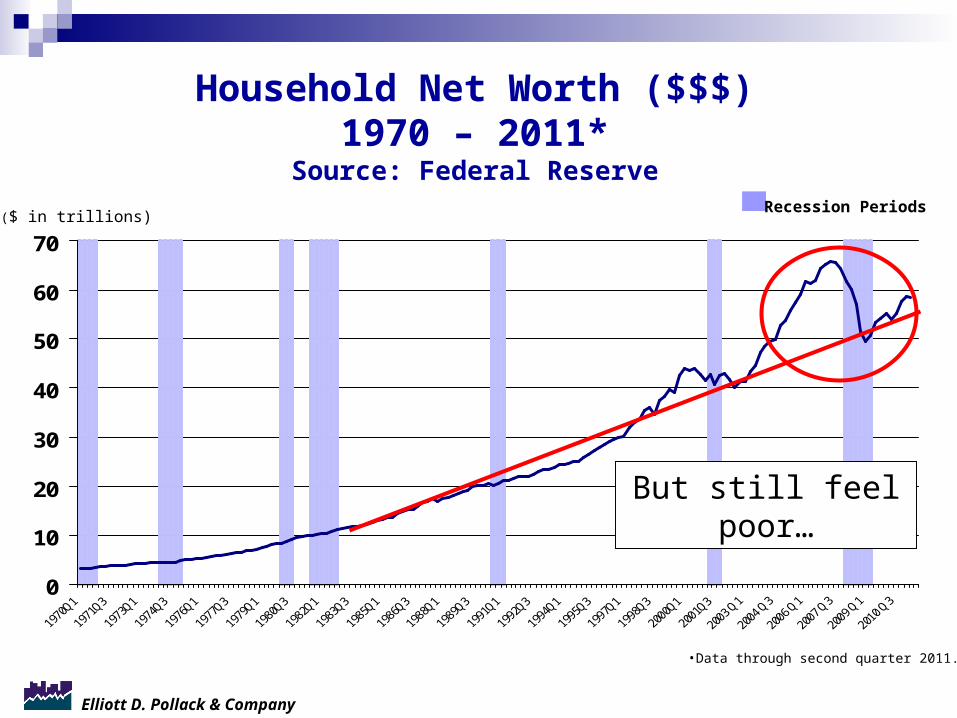

Household Net Worth ($$$)1970 – 2011*

Source: Federal Reserve

0

10

20

30

40

50

60

70

•Data through second quarter 2011.

Recession Periods($ in trillions)

But still feel poor…

Elliott D. Pollack & Company

Consumer Confidence1978 – 2011*

Source: The Dismal Scientist

20

30

40

50

60

70

80

90

100

110

120

130

140

150

*Data through September 2011

Recession Periods

1985 Benchmark = 100

Elliott D. Pollack & Company

Jobs are being created but not quickly enough.

Those that have jobs are spending a little more but will remain cautious.

Most of those that don’t have jobs probably won’t anytime soon.

Wealth levels are improving but people still feel poor.

Will the additional uncertainty translate into reduced consumer spending?

Consumer Summary:

Elliott D. Pollack & Company

BusinessDepends on the sector…

Elliott D. Pollack & Company

Corporate Profit (Billions of Dollars, SA)

1975-2011*Source: BEA

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

*Data through second quarter 2011

Recession Periods

Elliott D. Pollack & Company

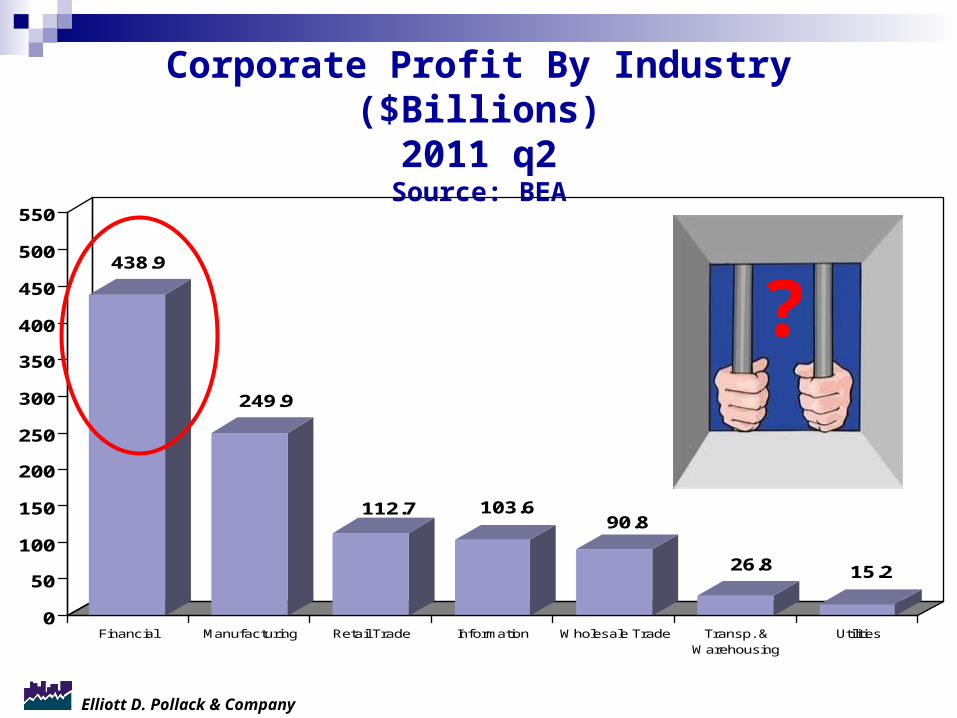

Corporate Profit By Industry ($Billions)2011 q2

Source: BEA

438.9

249.9

112.7 103.690.8

26.8 15.2

0

50

100

150

200

250

300

350

400

450

500

550

Financial Manufacturing Retail Trade Information Wholesale Trade Transp. &Warehousing

Utilities

?

Elliott D. Pollack & Company

U.S. Real Exports as a Percent of Real GDP

1971 – 2011* Source: Bureau of Economic Analysis

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1971 Q

1

1973 Q

1

1975 Q

1

1977 Q

1

1979 Q

1

1981 Q

1

1983 Q

1

1985 Q

1

1987 Q

1

1989 Q

1

1991 Q

1

1993 Q

1

1995 Q

1

1997 Q

1

1999 Q

1

2001 Q

1

2003 Q

1

2005 Q

1

2007 Q

1

2009 Q

1

2011 Q

1

Recession Periods

*Data through second quarter 2011

Elliott D. Pollack & Company

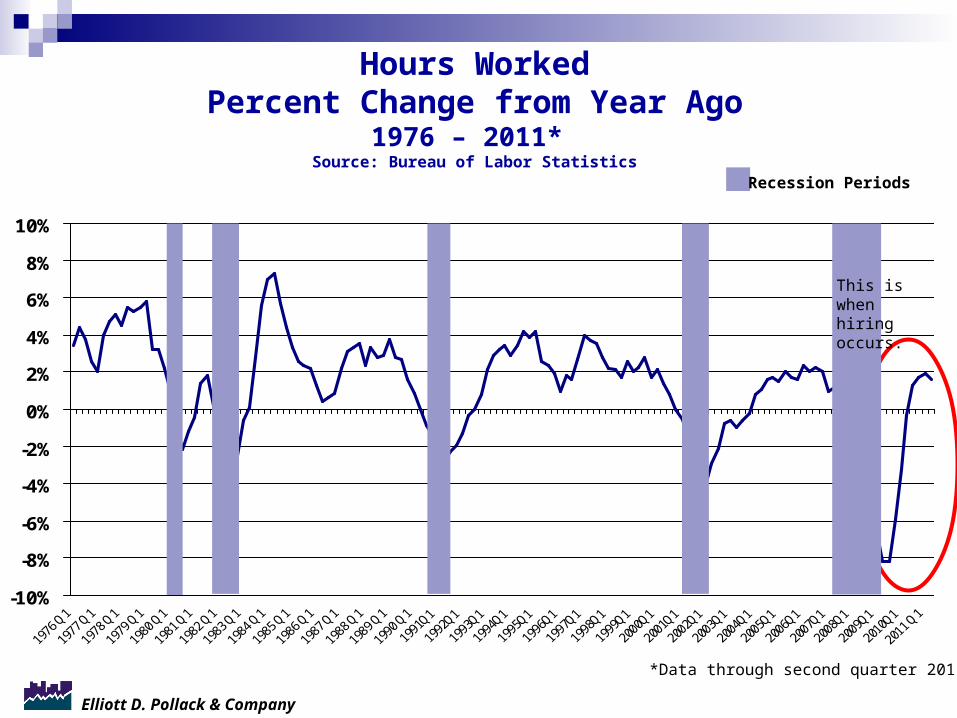

Hours WorkedPercent Change from Year Ago

1976 – 2011* Source: Bureau of Labor Statistics

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Recession Periods

*Data through second quarter 2011

This is when hiring occurs.

Elliott D. Pollack & Company

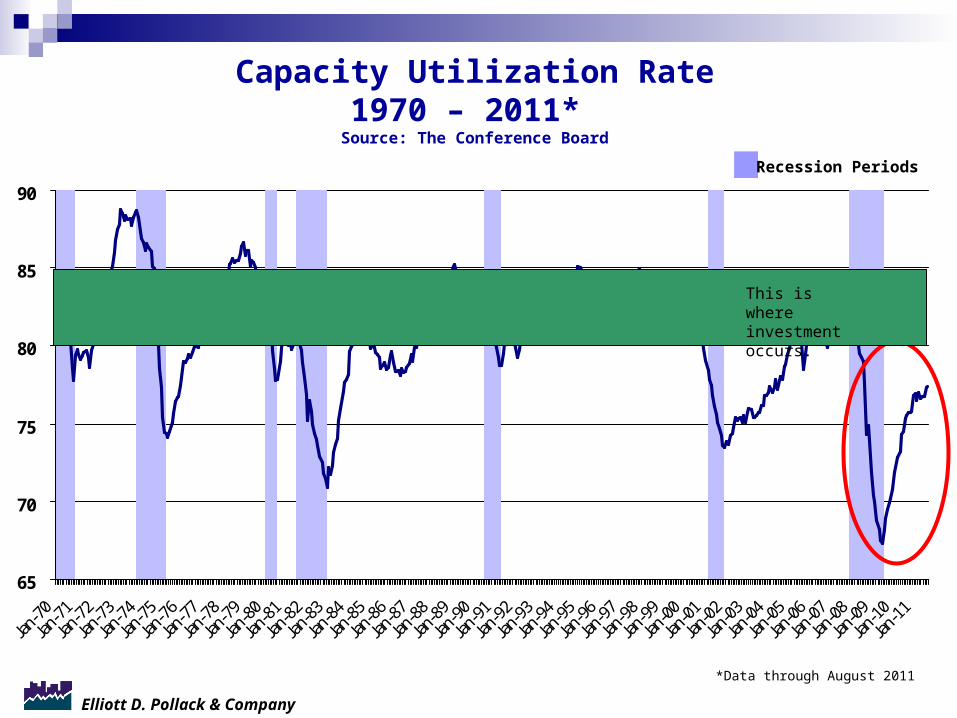

Capacity Utilization Rate1970 – 2011*

Source: The Conference Board

65

70

75

80

85

90

Jan-

70

Jan-

71

Jan-

72

Jan-

73

Jan-

74

Jan-

75

Jan-

76

Jan-

77

Jan-

78

Jan-

79

Jan-

80

Jan-

81

Jan-

82

Jan-

83

Jan-

84

Jan-

85

Jan-

86

Jan-

87

Jan-

88

Jan-

89

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

*Data through August 2011

Recession Periods

This is where investment occurs.

Elliott D. Pollack & Company

Profits are high, but…

Business spending on plant will be slow for now, but getting closer to seeing some limited investment. Delayed?

Hiring will still be relatively slow, but more pressure to hire soon. Delayed?

Lots of money sitting on the sidelines.

Business Summary:

Elliott D. Pollack & Company

U.S. Summary:Recovering but not recovered.

Lots of small shocks thus far but none have been game changers (Europe could possibly be

one though; anything unexpected possible?).

Stimulus package doesn’t address the real problem. Feds need to balance their

checkbook.

Elliott D. Pollack & Company

a) Slow growth, STALL, slow growth, but better 2012, 2013…

b) Slow growth, fundamental change, longer term problems?

Basic Question:

Elliott D. Pollack & Company

Arizona

Elliott D. Pollack & Company

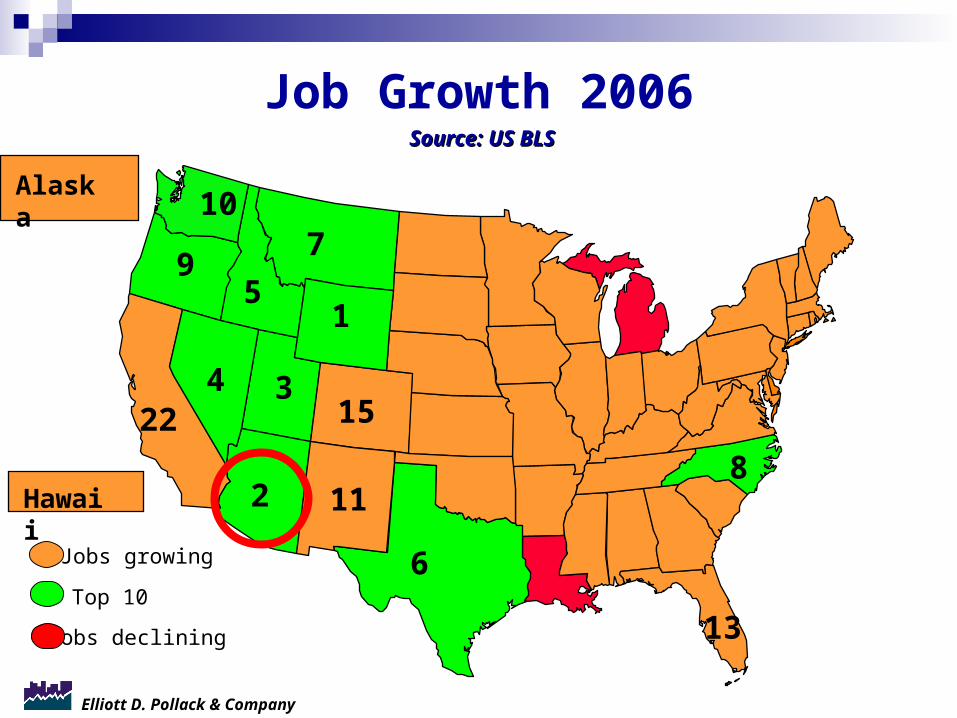

9

4

15

2

10

3

7

Job Growth 2006

11

15

6

22

8

Source: US BLSSource: US BLS

13

Jobs growing

Jobs declining

Top 10

Hawaii

Alaska

Elliott D. Pollack & Company

5

49

23

3545

4

32

8

24

47

50

44

1

16

3

Alaska 2

13

1830

Job Growth 2009Source: US BLSSource: US BLS

46

Jobs growing

Jobs declining

Top 10

Hawaii

Elliott D. Pollack & Company

19

9

August 2011 v August 2010

32

2

24 30

3

39

16

Job Growth Update: Arizona Ranked 32nd

45

29

1

5

20

Alaska 6

50

815

35Jobs growing

Jobs decliningTop 10

Hawaii

18

10

25

11

21

4

7

Elliott D. Pollack & Company

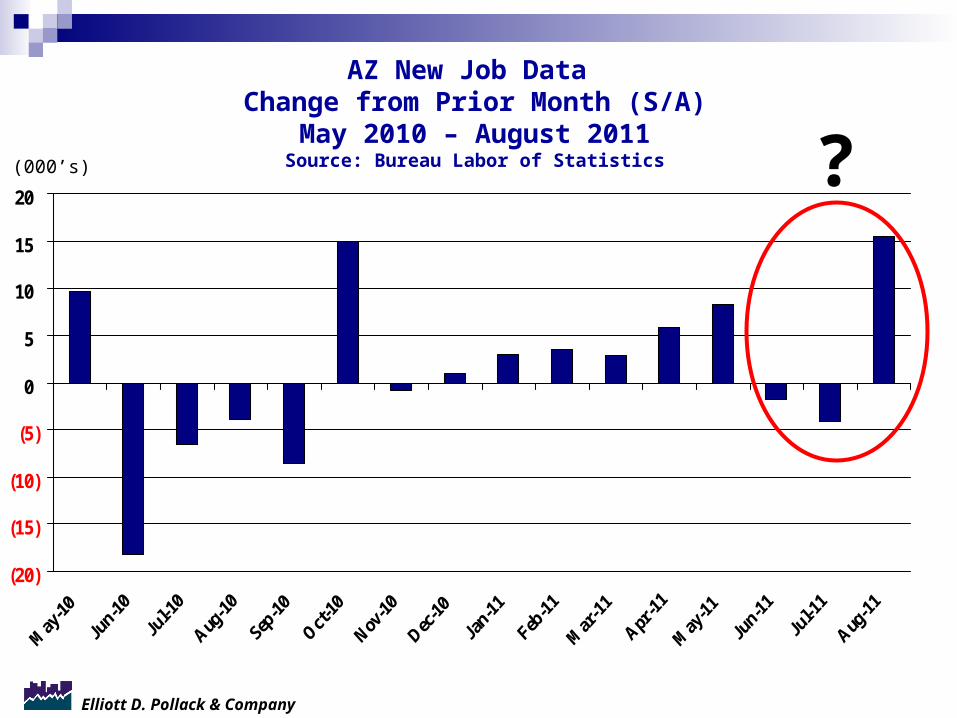

AZ New Job Data Change from Prior Month (S/A)

May 2010 – August 2011Source: Bureau Labor of Statistics

(20)

(15)

(10)

(5)

0

5

10

15

20

(000’s) ?

Elliott D. Pollack & Company

In 2008, 2009, and 2010 no one showed up! Or, at least

very few.

Elliott D. Pollack & Company

2.1%

3.7%

4.2%

4.7%

3.9%

3.3%

3.0%

3.1%

4.3%

5.1%

4.2%4.4%

2.9%

2.5%

1.3%

2.4%

2.8%

3.5%

4.3%

4.6%

4.2%4.2%

3.8%

4.3% 4.3%

3.1%

3.2%3.3%

3.4% 3.4%

2.7%2.5%

1.6%

1.0%1.0%

1.5%

2.0%

0%

2%

4%

6%

1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

Greater Phoenix Population Annual Percent Change 1976–2012*

Source: Arizona State University & Department of Commerce, Research Administration

2008 and 2009 are estimates put out by ADES and may be subject to substantial revision.

* 2011 & 2012 forecast is from Elliott D. Pollack & Co. Recession Periods

*2000-2010 estimates based on 2010 Census release

?

Elliott D. Pollack & Company

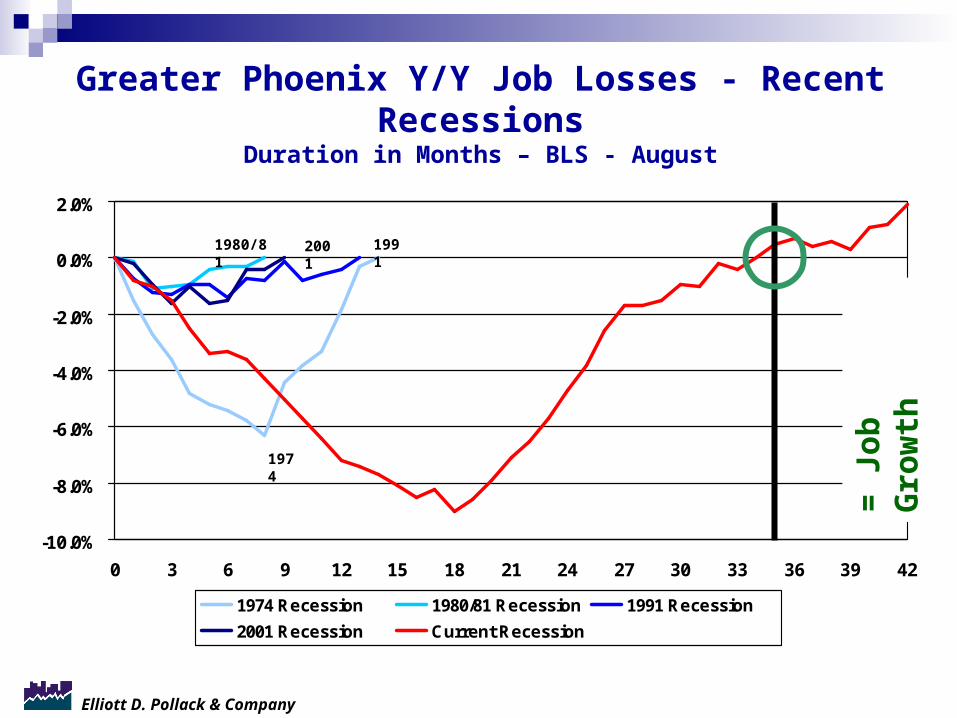

Greater Phoenix Y/Y Job Losses - Recent RecessionsDuration in Months – BLS - August

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42

1974 Recession 1980/81 Recession 1991 Recession

2001 Recession Current Recession

1980/81

1974

2001 1991

= J

ob

Gro

wth

Elliott D. Pollack & Company

Greater Phoenix Employment* Source: Bureau of Labor Statistics

Sectors in Decline

Net

Change

Federal Government -1,000

Prof. & Bus. Services -4,200

*August 2011/August 2010

Sectors Improving

Net

Change

Education & Health Services 14,700

Leisure & Hospitality 7,100

Transp, Trade, & Utilities 4,900

Construction 2,300

Financial Activities 2,300

Manufacturing 1,900

Other services 1,800

State Government 600

Local Government 400

Mining 300

Information 200

Elliott D. Pollack & Company

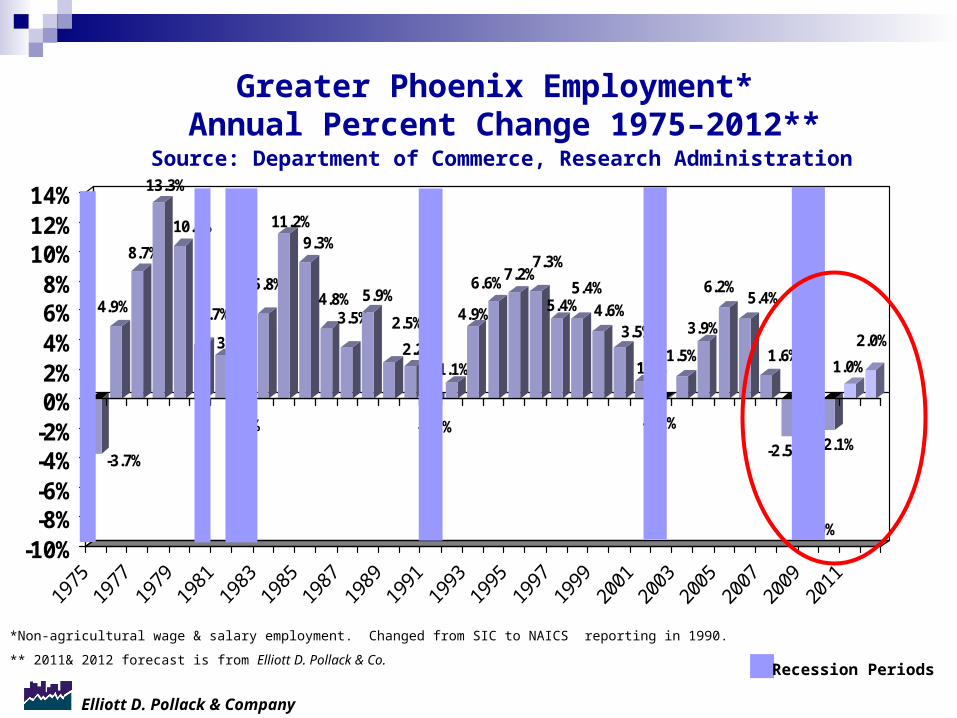

Greater Phoenix Employment* Annual Percent Change 1975–2012**

Source: Department of Commerce, Research Administration

-3.7%

4.9%

8.7%

13.3%

10.4%

3.7%

3.0%

-0.1%

5.8%

11.2%9.3%

4.8%3.5%

5.9%

2.5%

2.2%

-0.3%

1.1%

4.9%

6.6%7.2%7.3%

5.4%5.4%

4.6%3.5%

1.2%

-0.1%

1.5%

3.9%

6.2%5.4%

1.6%

-2.5%

-7.9%

-2.1%

1.0%

2.0%

-10%-8%-6%-4%-2%0%2%4%6%8%

10%12%14%

*Non-agricultural wage & salary employment. Changed from SIC to NAICS reporting in 1990.

** 2011& 2012 forecast is from Elliott D. Pollack & Co.

Recession Periods

Elliott D. Pollack & Company

This is NOT a multi decade recovery…

Think 2015 – 2016 for full recovery, but growth before

then.

Elliott D. Pollack & Company

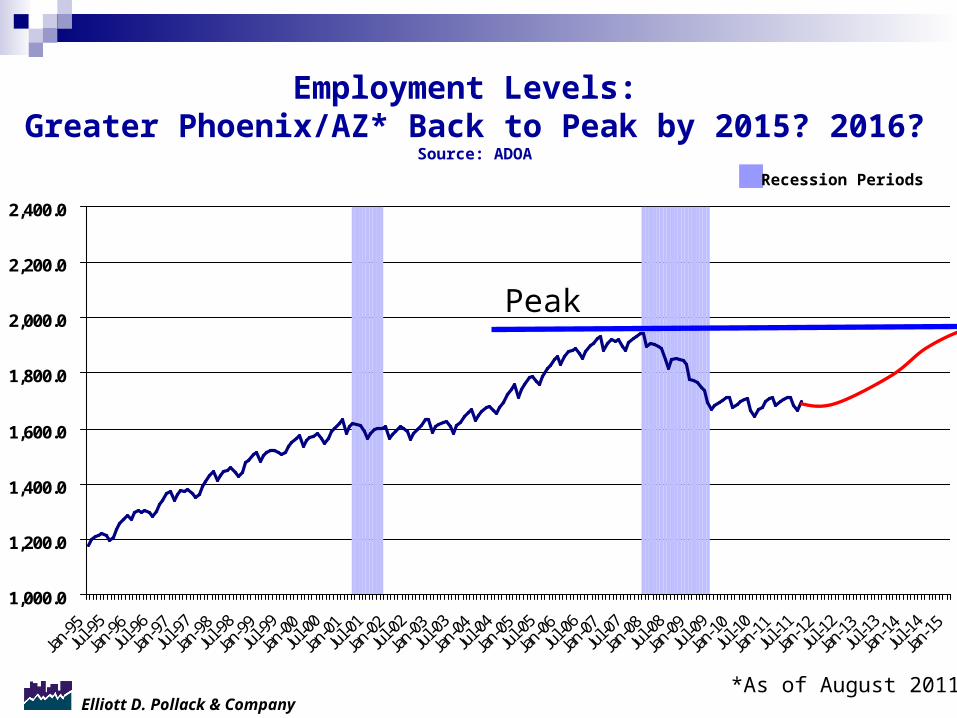

Employment Levels: Greater Phoenix/AZ* Back to Peak by 2015? 2016?

Source: ADOA

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2,000.0

2,200.0

2,400.0

Recession Periods

Peak

*As of August 2011

Elliott D. Pollack & Company

For individual communities: similar issues, just different

scale of impact.

Elliott D. Pollack & Company

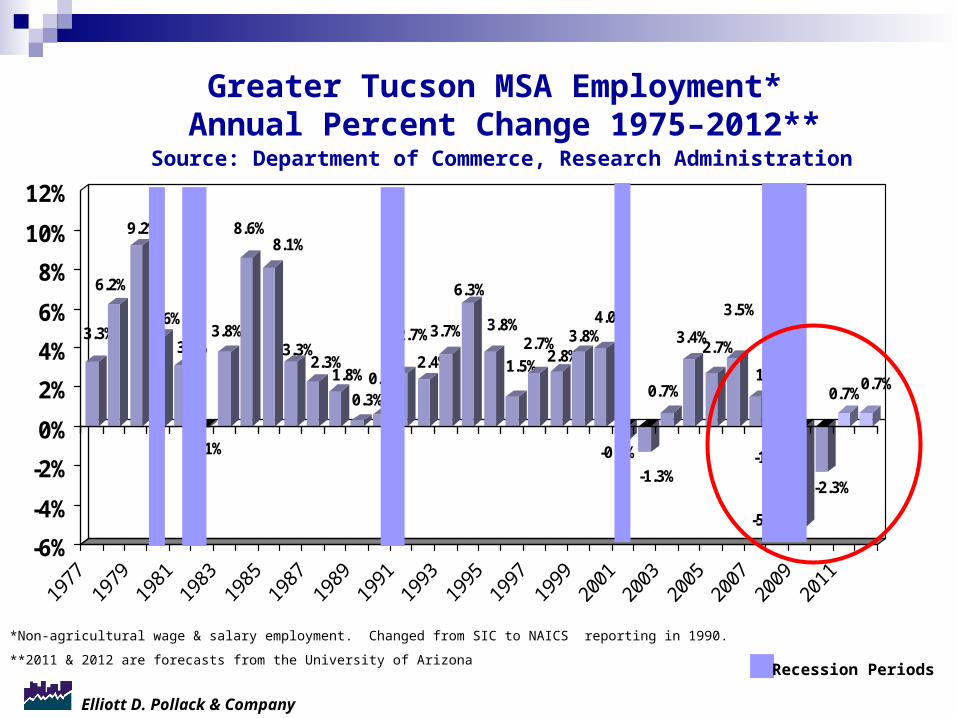

Greater Tucson MSA Employment* Annual Percent Change 1975–2012**

Source: Department of Commerce, Research Administration

3.3%

6.2%

9.2%

4.6%

3.1%

-0.1%

3.8%

8.6%8.1%

3.3%2.3%

1.8%

0.3%0.6%

2.7%

2.4%

3.7%

6.3%

3.8%

1.5%2.7%

2.8%3.8%

4.0%

-0.7%

-1.3%

0.7%

3.4%2.7%

3.5%

1.5%

-1.0%

-5.1%

-2.3%

0.7%0.7%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

*Non-agricultural wage & salary employment. Changed from SIC to NAICS reporting in 1990.

**2011 & 2012 are forecasts from the University of Arizona

Recession Periods

Elliott D. Pollack & Company

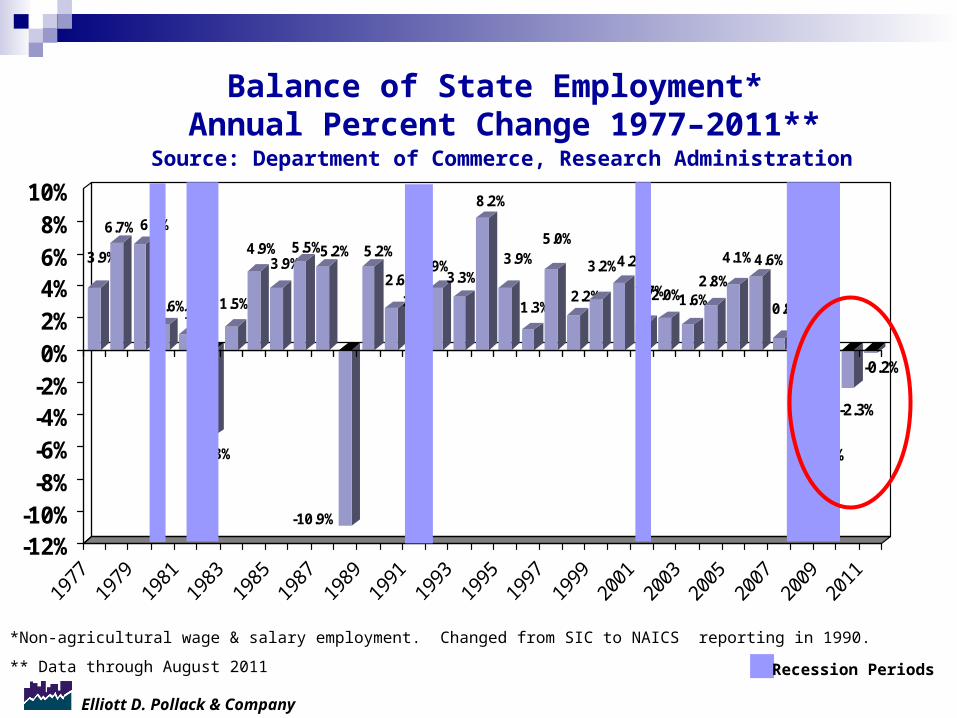

Balance of State Employment* Annual Percent Change 1977–2011**

Source: Department of Commerce, Research Administration

3.9%

6.7% 6.6%

1.6%1.0%

-5.3%

1.5%

4.9%3.9%

5.5%5.2%

-10.9%

5.2%

2.6%

2.2%

3.9%3.3%

8.2%

3.9%

1.3%

5.0%

2.2%

3.2%4.2%

1.7%2.0%1.6%2.8%

4.1%4.6%

0.8%

-2.2%

-5.5%

-2.3%

-0.2%

-12%-10%

-8%-6%-4%-2%0%2%4%6%8%

10%

*Non-agricultural wage & salary employment. Changed from SIC to NAICS reporting in 1990.

** Data through August 2011

Recession Periods

Elliott D. Pollack & Company

Single Family Housing

Elliott D. Pollack & Company

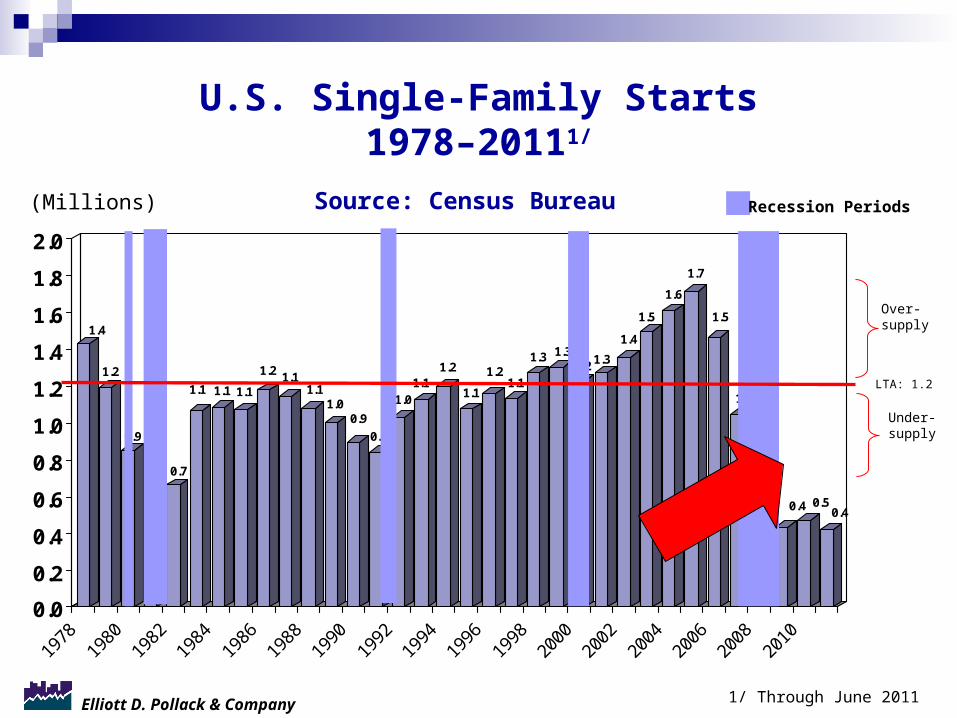

U.S. Single-Family Starts1978–20111/

Source: Census Bureau

1.4

1.2

0.9

0.7 0.7

1.1 1.1 1.1

1.2 1.11.1

1.00.9

0.8

1.01.1

1.2

1.1

1.21.1

1.3 1.31.2 1.3

1.4

1.5

1.6

1.7

1.5

1.0

0.6

0.4 0.50.4

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

(Millions)

1/ Through June 2011

Recession Periods

Over-supply

Under-supply

LTA: 1.2

Elliott D. Pollack & Company

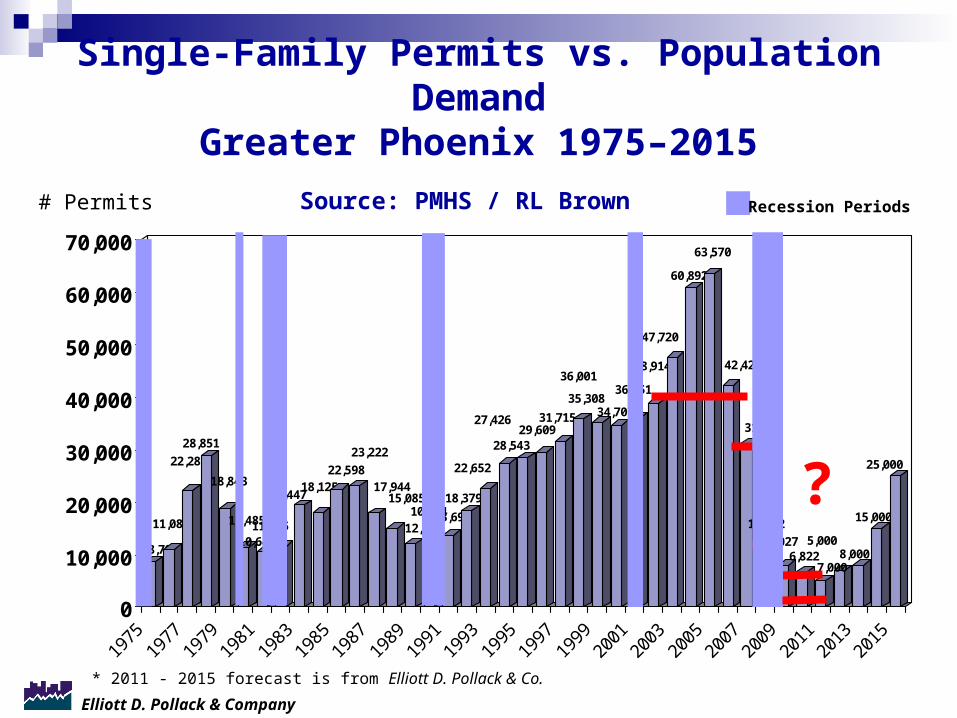

Single-Family Permits vs. Population DemandGreater Phoenix 1975–2015

Source: PMHS / RL Brown

8,705

11,081

22,281

28,851

18,843

11,485

10,64911,625

19,44718,125

22,598

23,222

17,94415,085

12,00010,61413,698

18,379

22,652

27,426

28,54329,609

31,715

36,001

35,30834,701

36,151

38,914

47,720

60,892

63,570

42,423

31,172

12,582

8,0276,822

5,000

7,0008,000

15,000

25,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

# Permits Recession Periods

* 2011 - 2015 forecast is from Elliott D. Pollack & Co.

?

Elliott D. Pollack & Company

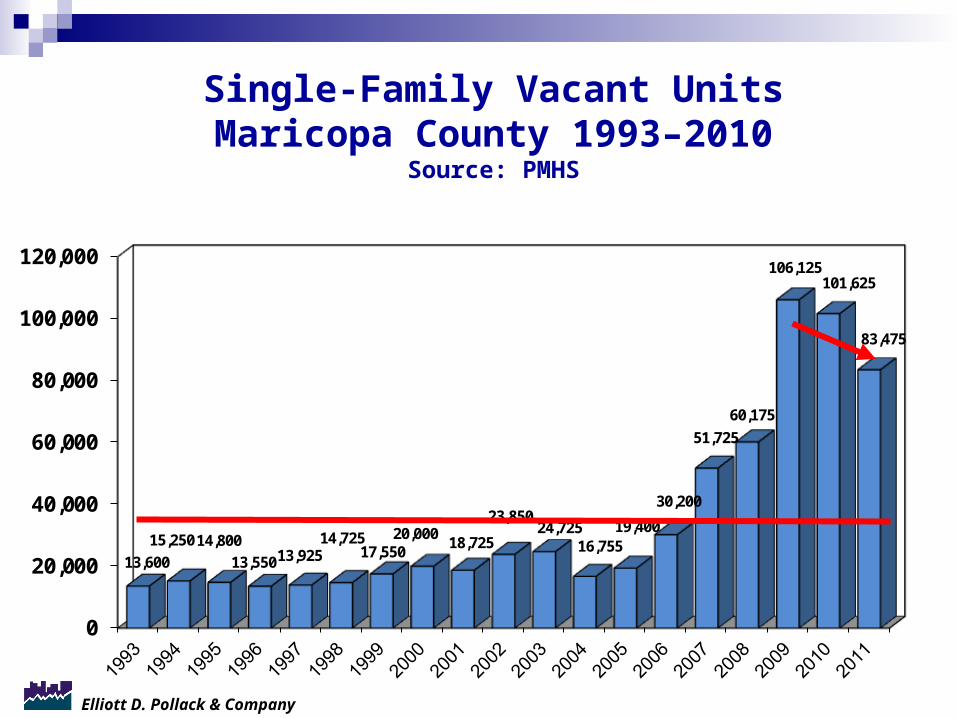

Single-Family Vacant UnitsMaricopa County 1993–2010

Source: PMHS

0

20,000

40,000

60,000

80,000

100,000

120,000

13,600

15,250 14,800

13,550 13,925 14,725

17,550 20,000

18,725

23,850 24,725

16,755 19,400

30,200

51,725

60,175

106,125 101,625

83,475

Elliott D. Pollack & Company

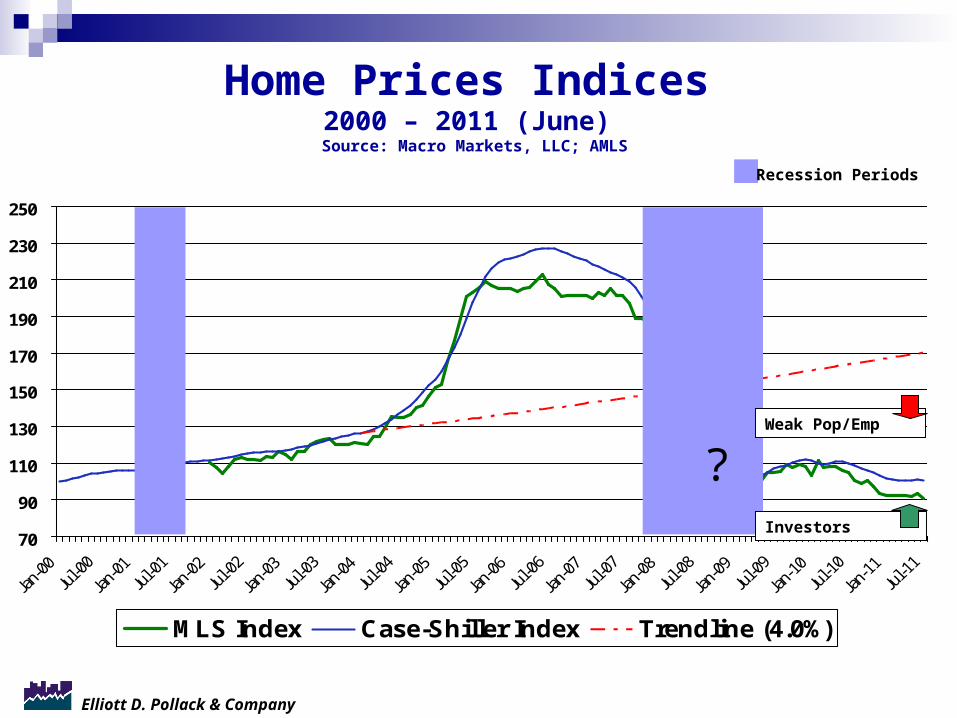

Home Prices Indices 2000 – 2011 (June)

Source: Macro Markets, LLC; AMLS

70

90

110

130

150

170

190

210

230

250

MLS Index Case-Shiller Index Trendline (4.0%)

Recession Periods

Weak Pop/Emp

Investors

?

Elliott D. Pollack & Company

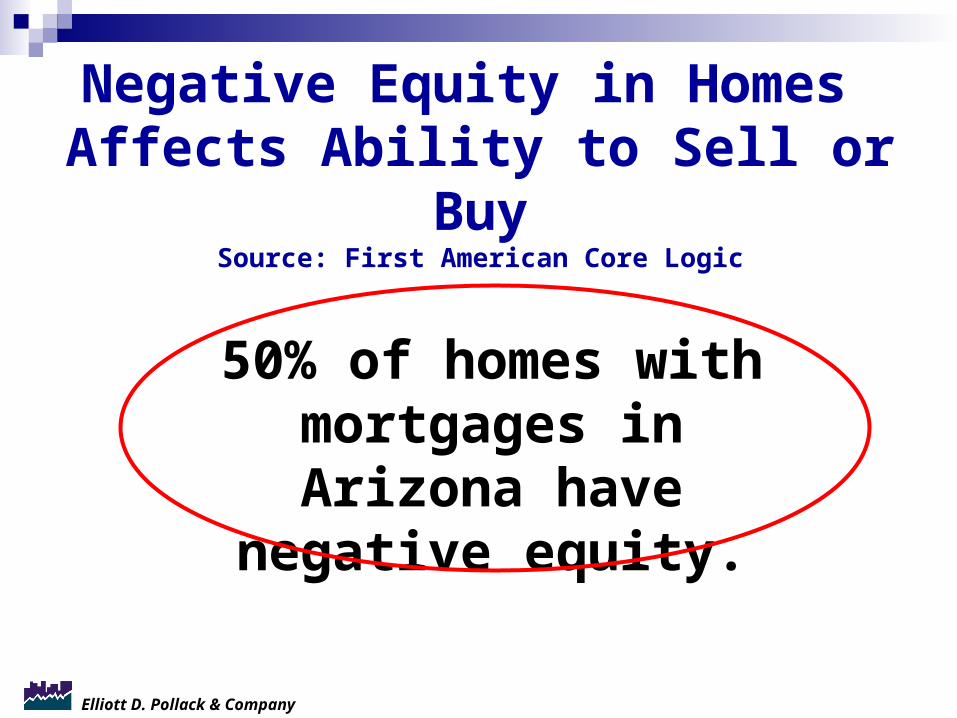

Negative Equity in Homes Affects Ability to Sell or Buy

Source: First American Core Logic

50% of homes with mortgages in Arizona have negative equity.

Elliott D. Pollack & Company

Commercial

Elliott D. Pollack & Company

Commercial Markets

(Not making things worse anymore)

Elliott D. Pollack & Company

Revenue Question:

How long will commercial values be depressed?

Elliott D. Pollack & Company

Commercial Summary:

Flat or only slightly improving indicators but declining prices?

Maybe. Will vary by location though.

When do investors come in?

Elliott D. Pollack & Company

Back to Normal Vacancy?

• Office = 2014 - 2015

• Industrial = 2014 - 2015

• Retail = 2014 - 2015

Elliott D. Pollack & Company

Tax Revenues

Elliott D. Pollack & Company

Gains Needed to Reach Previous Peak

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 6 11 16 21 26 31 36 41 46

Realized Percent Loss

Re

qu

ire

d P

erc

ent

Ga

in

Sales Tax: -23% / 30%

Corporate Income Tax: -58% / 139%

Individual Income Tax: -36% / 55%

?

Now

State forecast revisions in our future?

Elliott D. Pollack & Company

But, local revenues related to single family and

commercial taxation will remain weak.

Elliott D. Pollack & Company

Hey Jim, your speeches suck. How about some

positive news?

Enjoy the rock!!!

Elliott D. Pollack & Company

Positives?

Elliott D. Pollack & Company

Phoenix-Mesa Employment Growth(Ranking among all metro areas greater than 1,000,000; 2011 August/August)

Source: Arizona State University, U.S. Bureau of Labor Statistics

YEAR RANK # of MSAs

1991 4 20 1992 5 20 1993 2 20 1994 1 20 1995 1 21 1996 1 23 1997 2 23 1998 1 24 1999 3 26 2000 8 26 2001 6 28 2002 5 28 2003 3 29 2004 4 29 2005 1 30 2006 1 31 2007 10 32 2008 29 32 2009 31 32 2010 31

32 2011 5 32

Elliott D. Pollack & Company

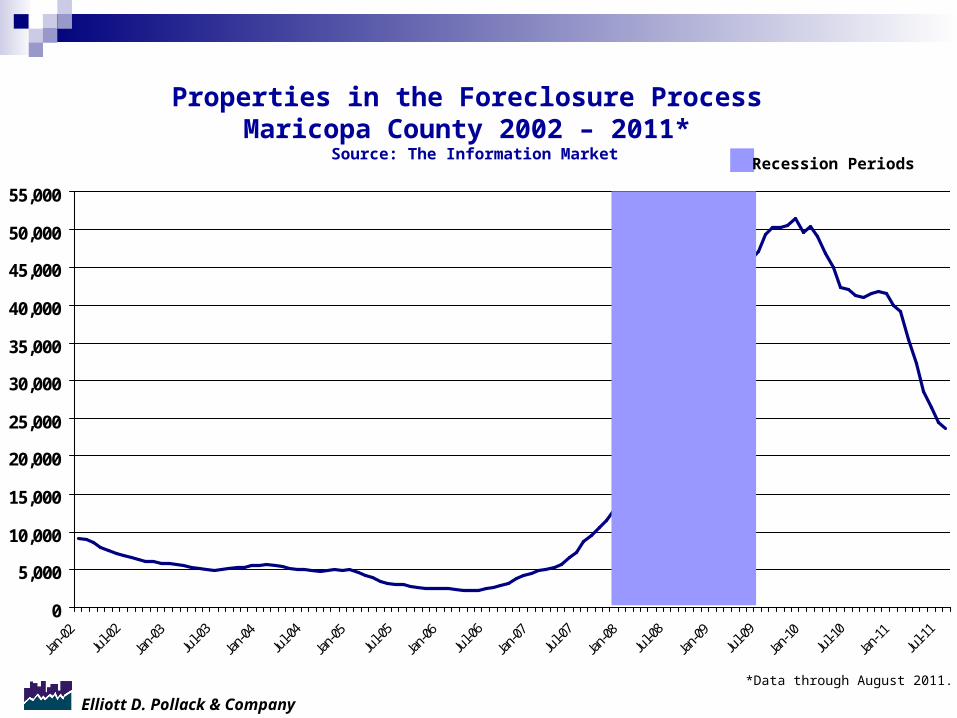

Properties in the Foreclosure Process Maricopa County 2002 – 2011*

Source: The Information Market

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

*Data through August 2011.

Recession Periods

Elliott D. Pollack & Company

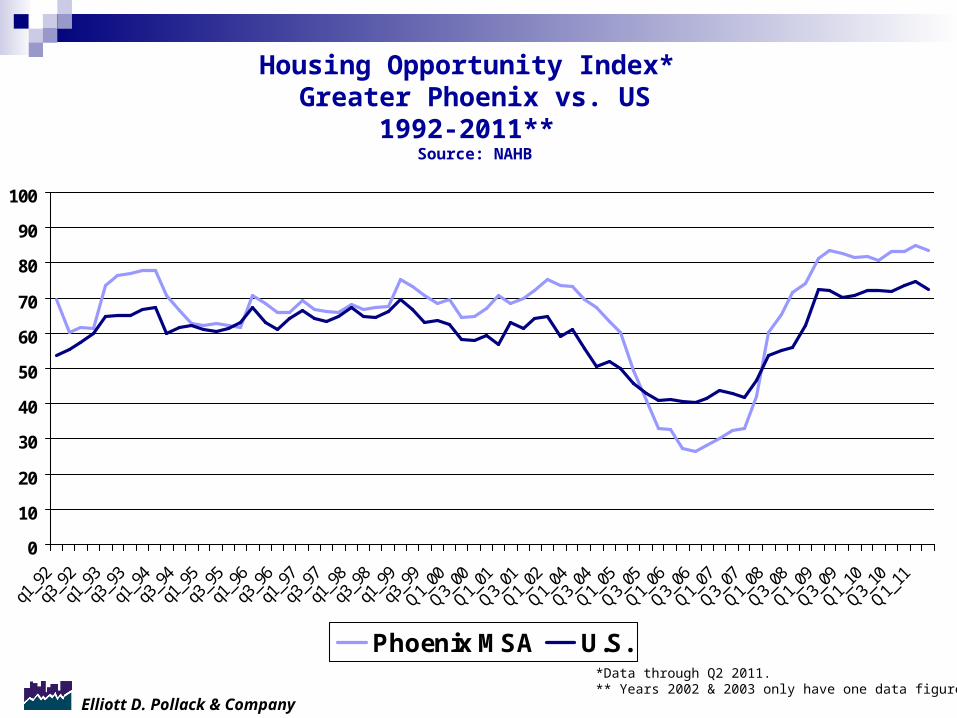

Housing Opportunity Index* Greater Phoenix vs. US

1992-2011** Source: NAHB

0

10

20

30

40

50

60

70

80

90

100

Phoenix MSA U.S.*Data through Q2 2011.** Years 2002 & 2003 only have one data figure

Elliott D. Pollack & Company

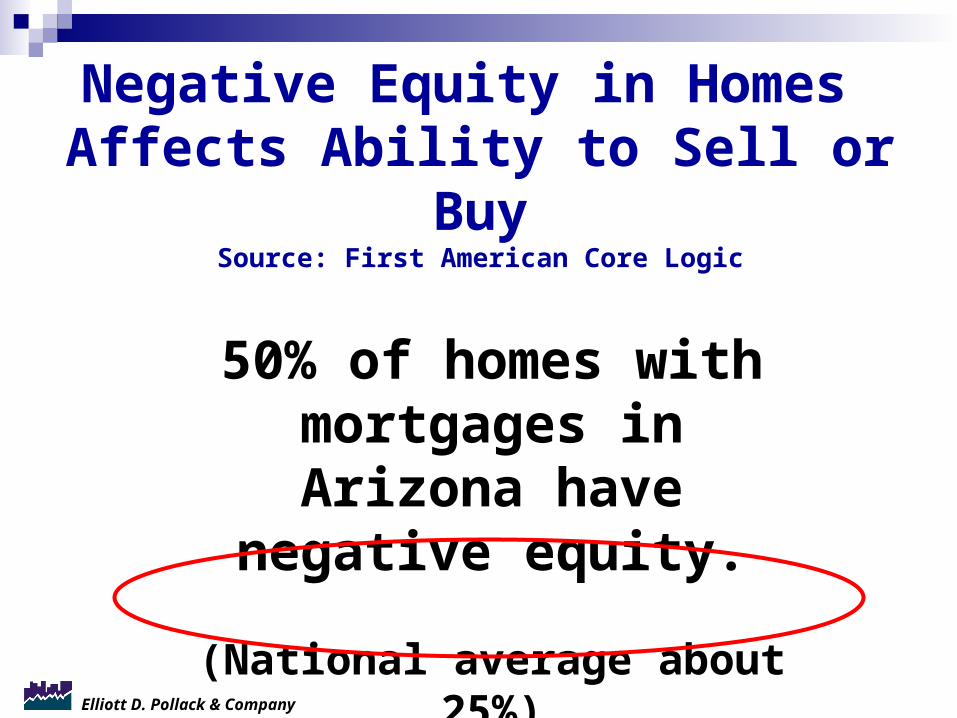

Negative Equity in Homes Affects Ability to Sell or Buy

Source: First American Core Logic

50% of homes with mortgages in Arizona have negative equity.

(National average about 25%)

Elliott D. Pollack & Company

5

910

Benefits of the “SUNBELT”

Alaska

Hawaii

Industrial Northwest

Elliott D. Pollack & Company

What about the bad national press?

Yes, SB1070

Elliott D. Pollack & Company

• Governor impeached• Real estate depression• Defense cutbacks• AZ Scam• Martin Luther King Holiday Crisis• Keating• Keating 5• Every S&L taken over by RTC

Between 1987 and 1992

Elliott D. Pollack & Company

One survey shows that over 80% of current single family RENTERS would like to soon

own.

Some of these homes are thus permanently absorbed.

Elliott D. Pollack & Company

9

4

15

2

10

3

7

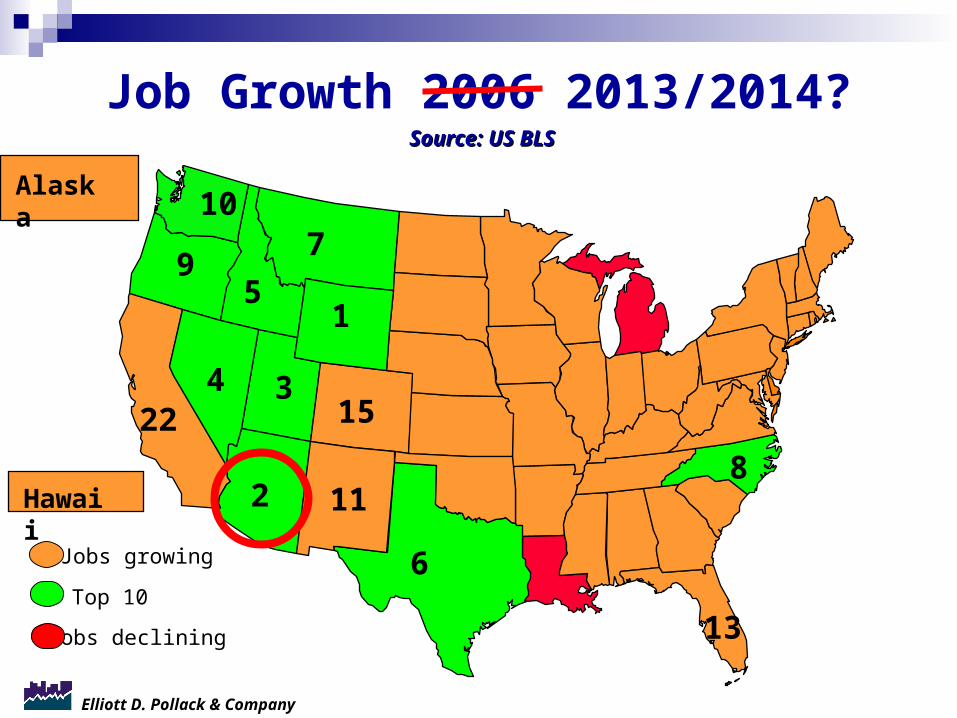

Job Growth 2006 2013/2014?

11

15

6

22

8

Source: US BLSSource: US BLS

13

Jobs growing

Jobs declining

Top 10

Hawaii

Alaska

Elliott D. Pollack & Company

Economic Competitiveness

Elliott D. Pollack & Company

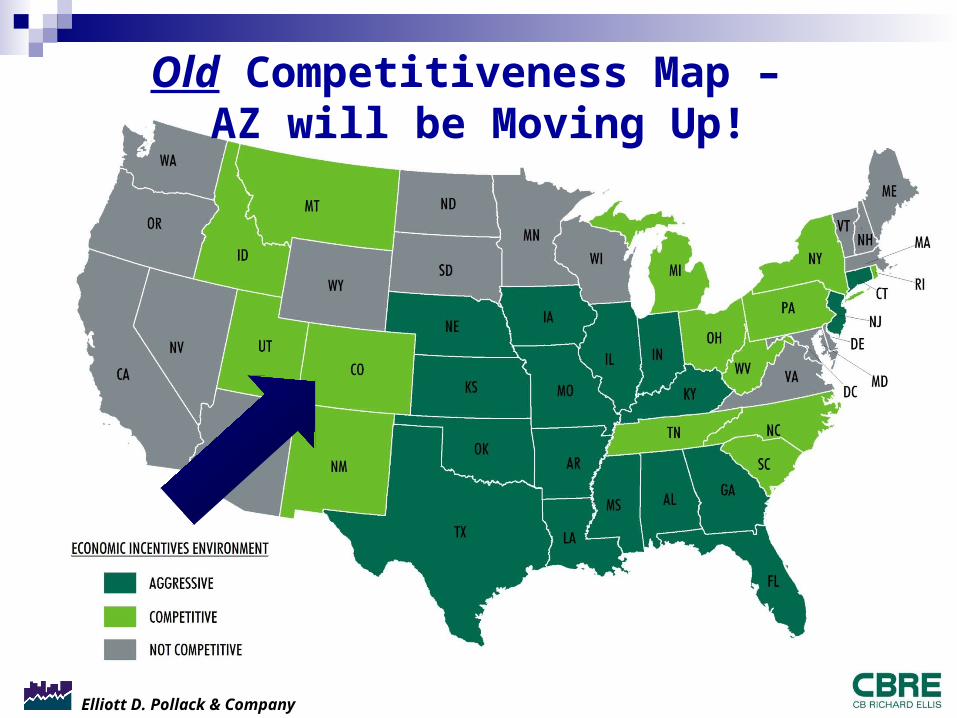

Old Competitiveness Map – AZ will be Moving Up!

Elliott D. Pollack & Company

Being addressed now…

Elliott D. Pollack & Company

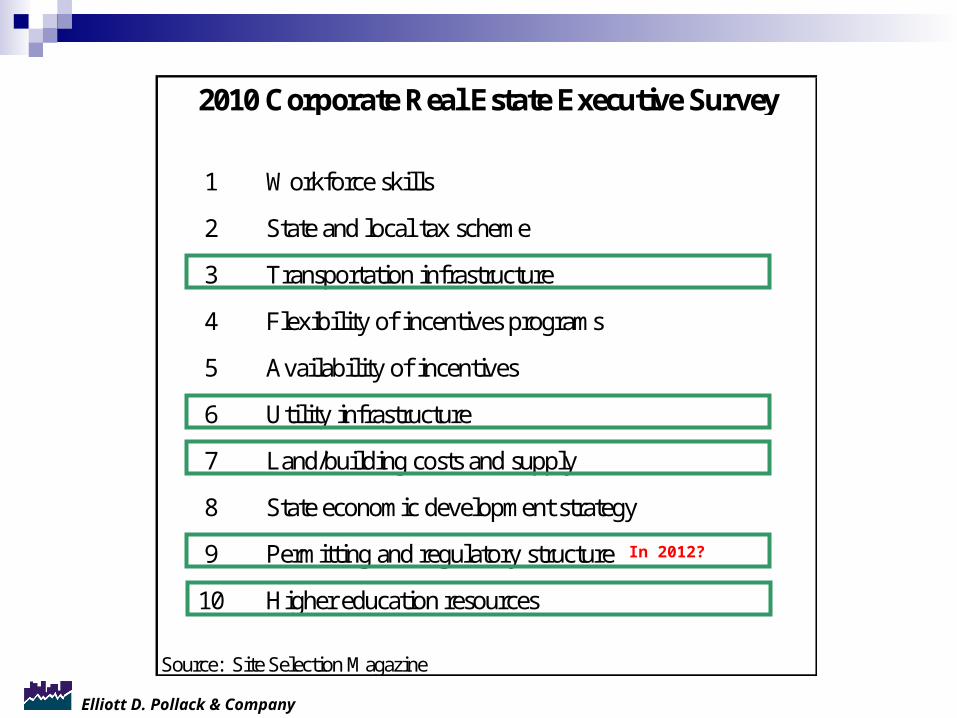

1 Workforce skills

2 State and local tax scheme

3 Transportation infrastructure

4 Flexibility of incentives programs

5 Availability of incentives

6 Utility infrastructure

7 Land/building costs and supply

8 State economic development strategy

9 Permitting and regulatory structure

10 Higher education resources

Source: Site Selection Magazine

2010 Corporate Real Estate Executive Survey

Elliott D. Pollack & Company

What about the rest?

Elliott D. Pollack & Company

1 Workforce skills

2 State and local tax scheme

3 Transportation infrastructure

4 Flexibility of incentives programs

5 Availability of incentives

6 Utility infrastructure

7 Land/building costs and supply

8 State economic development strategy

9 Permitting and regulatory structure

10 Higher education resources

Source: Site Selection Magazine

2010 Corporate Real Estate Executive Survey

In 2012?

Elliott D. Pollack & Company

Policymakers finally started to understand how our economy functions.

We now have some economic development “tools.”

But, we need to see if the state and locals, the “tool man,” can use the tools properly and with a common vision, or “blueprint.”

Economic Development Summary:

Elliott D. Pollack & Company

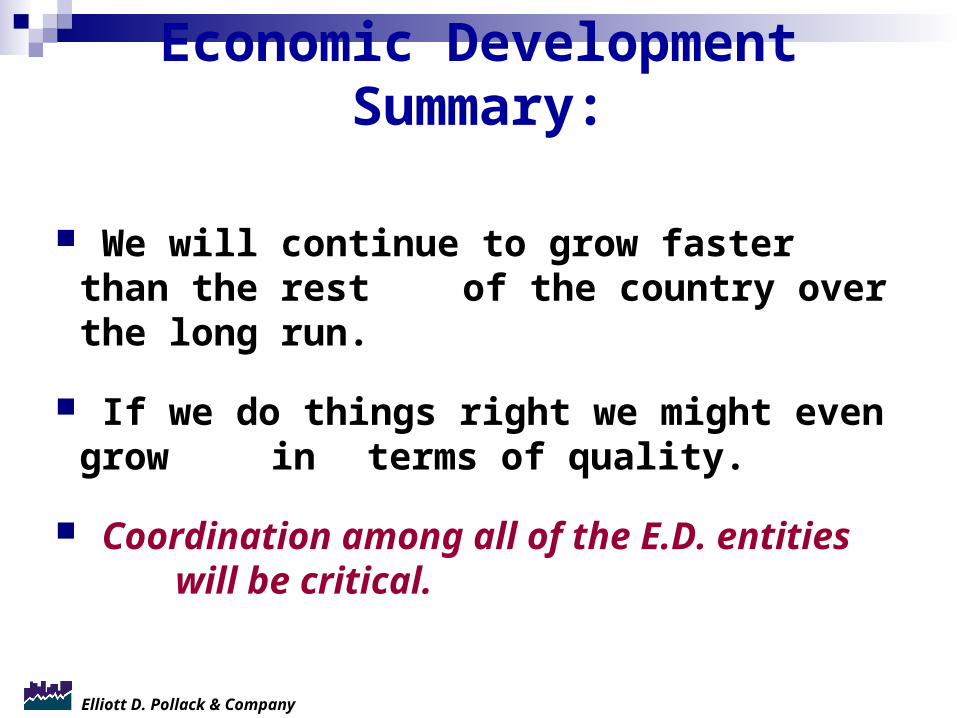

We will continue to grow faster than the rest of the country over the long run.

If we do things right we might even grow in terms of quality.

Coordination among all of the E.D. entities will be critical.

Economic Development Summary:

Elliott D. Pollack & Company

Something still needs to be done about statewide tourism

promotion.

Elliott D. Pollack & Company

Elliott D. Pollack & Company

Arizona Summary

Elliott D. Pollack & Company

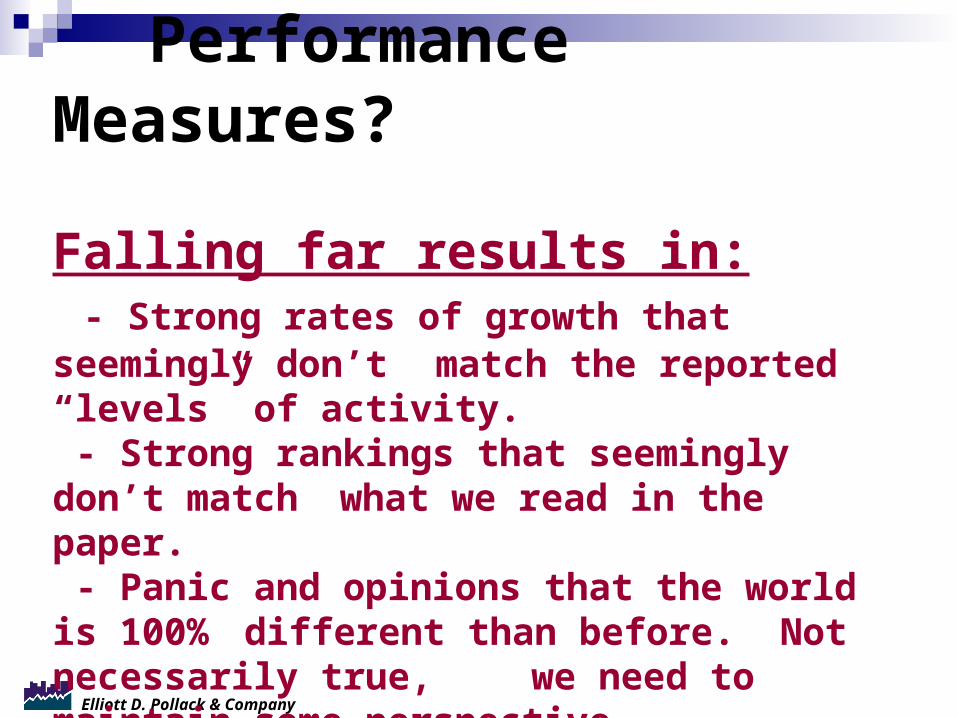

Performance Measures?

Falling far results in: - Strong rates of growth that seemingly don’t match the reported “levels” of activity. - Strong rankings that seemingly don’t match what we read in the paper. - Panic and opinions that the world is 100% different than before. Not necessarily true, we need to maintain some perspective.

Elliott D. Pollack & Company

Full Recovery: STILL 2015 / 2016?

Fully recovered in terms of: 1) Housing oversupply; 2) Commercial vacancy rates; 3) Retail sales activity; 4) Employment levels. 5) Tax revenues? Probably.

Elliott D. Pollack & Company

There is even a BOOM for Arizona out there…somewhere.

Elliott D. Pollack & Company

But, can we also grow in terms of quality?

Elliott D. Pollack & Company 83

ELLIOTT D. POLLACK & Company

7505 East Sixth Avenue, Suite 100 Scottsdale, Arizona 85251

480-423-9200 P / 480-423-5942 F / www.arizonaeconomy.com / [email protected]

• Economic and Fiscal Impact Analysis/Modeling

• Real Estate Market and Feasibility Studies

• Litigation Support

• Revenue Forecasting

• Keynote Speaking

• Public Finance and Policy Development

• Land Use Economics

• Economic Development