electricity reform in mexico: achievements and next … · the 2013 reform: a clean-energy-ready...

TRANSCRIPT

Marcelino Madrigal*, Ph.D.Commissioner

Energy Regulatory Commission

Electricity Reform In Mexico 3rd Annual Conference

September 27, San Antonio, Texas*The views and opinions expressed in this presentation are those of the author

and do not necessarily reflect a position of CRE or other government agency

Electricity Reform in Mexico:

Achievements and Next Steps

The Reform and New Industry Structure

Industrial Security and Environmental

Protection of Hydrocarbons Sector

Hydrocarbons Law

Hydrocarbons Revenue Law

Petróleos Mexicanos Law

Mexican Oil Fund

Natural Gas

Mid & Downstream, Electricity Industry

State Productive Enterprise

3

New Legal Framework in order to boost the Mexican Energy Sector

3

Constitutional Reform (Arts. 27 & 28)

Electric Industry Law

Federal Electricity Commission Law

Law of the Coordinated Regulatory Agencies of the Energy Sector

Independent system operators created for:

Electricity Grid and Market

General Law in Climate Change

Geothermal Energy Law

Energy Transition Law Law on the Promotion and

Development of Bioenergetics

Policy maker

State Productive Enterprise

Upstream

The 2013 Reform: A Clean-Energy-Ready Market Reform

Generation

• Free participation

• Activity only with permit (CRE)

Distribution

• Public service provided by state and can make contracts for public-private investment

• Subject to regulation(CRE)

Transmission

• Public service provided by state and can make contracts for public-private investment

• Subject to regulation (CRE)

Grid and market Independent System Operator

•Decentralized public institution, before was part of Federal Energy Commission (CFE)

•Operate the national market and wholesale electricity market (MEM), ensuring access to Transmission and Distribution grids.

Marketing-Supply

• Competence for operations in MEM and qualified users

• Basic supply service is subject to regulation

Liberalizes and provides the new industrial organization, from generation to distribution and marketing, including the creation of a wholesale electricity market

Mexican Electricity System and Clean Energy Targets

2018

25%

2021

30%

2024

35%

5

Clean energy generation targets

Law of energy transition

2016-2030

1.9

2031-2050

3.7

Average annual rate of reduction of final energy consumption*

*Source: Press release, Ministry of Energy of Mexico, 2016

Transition Strategy

Source: Programa de Desarrollo del Sistema Eléctrico Nacional 2017-2031, Secretaria de Energía

40 millions of users

6

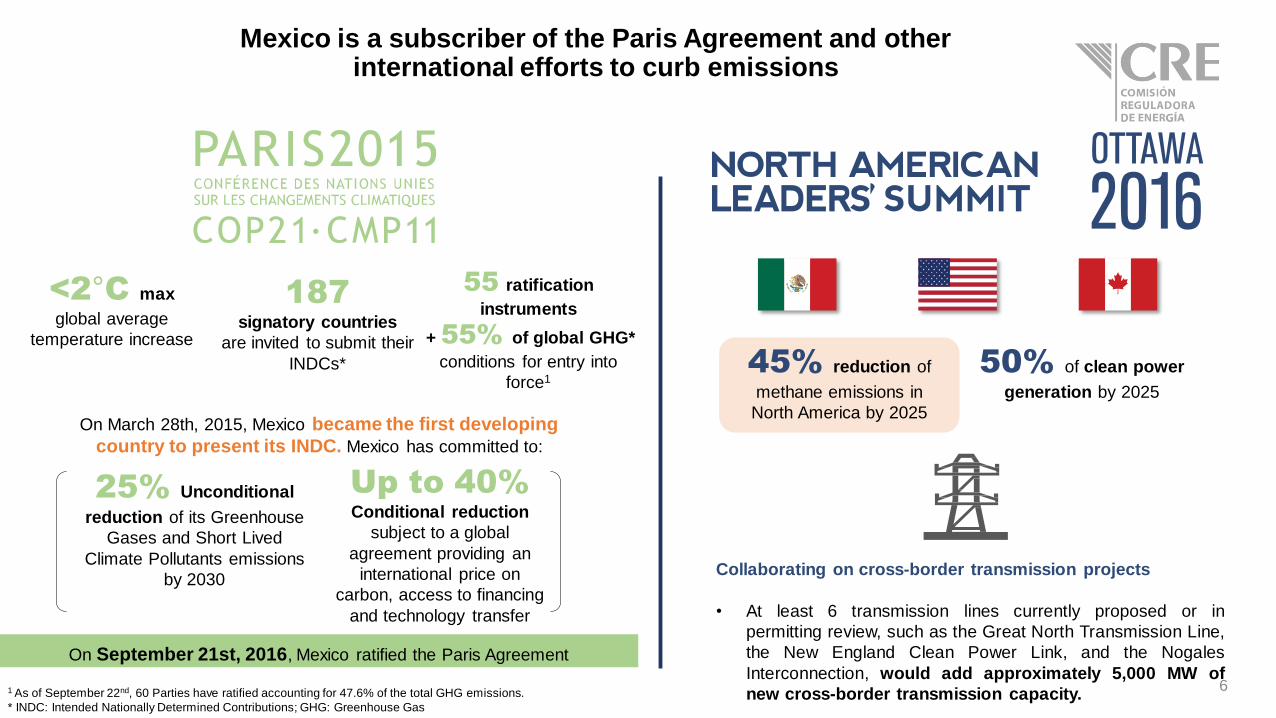

Mexico is a subscriber of the Paris Agreement and other international efforts to curb emissions

187

signatory countries

are invited to submit their

INDCs*

<2°C max

global average

temperature increase

55 ratification

instruments

+ 55% of global GHG*

conditions for entry into

force145% reduction of

methane emissions in

North America by 2025

50% of clean power

generation by 2025

Collaborating on cross-border transmission projects

• At least 6 transmission lines currently proposed or in

permitting review, such as the Great North Transmission Line,

the New England Clean Power Link, and the Nogales

Interconnection, would add approximately 5,000 MW of

new cross-border transmission capacity.1 As of September 22nd, 60 Parties have ratified accounting for 47.6% of the total GHG emissions.

* INDC: Intended Nationally Determined Contributions; GHG: Greenhouse Gas

On September 21st, 2016, Mexico ratified the Paris Agreement

25% Unconditional

reduction of its Greenhouse

Gases and Short Lived

Climate Pollutants emissions

by 2030

Up to 40%

Conditional reduction

subject to a global

agreement providing an

international price on

carbon, access to financing

and technology transfer

On March 28th, 2015, Mexico became the first developing

country to present its INDC. Mexico has committed to:

7

Trading

Transmission

System and market

Operator

Generation

Legacy

Generation

New

Market Oriented Transformation of the Energy Sector: Unbundling of Utility and Consumer Empowerment

Distribution

Supply

Free

Supply

Regulated

Transmission*

CFE Subsidiaries

+

Private Sector

Distribution*

CFE Subsidiaries

+

Private Sector

Commercialization

Pure Commercializati

on

Suppliers of Regulated Consumers

Generation

CFE

Split into Gencos

Private Generatos

System and Market Operations

CENACE

OSI/OM

Spot, Medium, and long Term Markets

Open Access

Final Consumers

Qualified Users

Regulated Users

Suppliers of Qualified Users

After: Unbundled with Deepened Competition

Policy Making

Regulation

1 MW

The Wholesale Markets: Status and Results

Market Design: Various Markets and Products

10

Nodal, co-optimized energy and reserve

Day Ahead & Real Time Market

To balance and needs principally acquired in

a long-term market

Capacity Designed as availability in Critical

Hours

Procure 3-year energy contracts

Financial Transmission Rights

One organized, one bulleting (voluntary) at the certificated system

Long-term auctions

Purchase of 15+ year contracts for Energy, Capacity, and Clean Energy Certificates

Financial Transmission Rights

I. Short Term Energy & Reserve Markets

II. Short Term Capacity Market

III. Medium Term Energy Markets

IV. Clean Energy Certificates Market

V. Long-term markets

Started in January ,2016

Started in March, 2017 August, 2017 Start in 2018

Started 3rd Auction in April, 2017

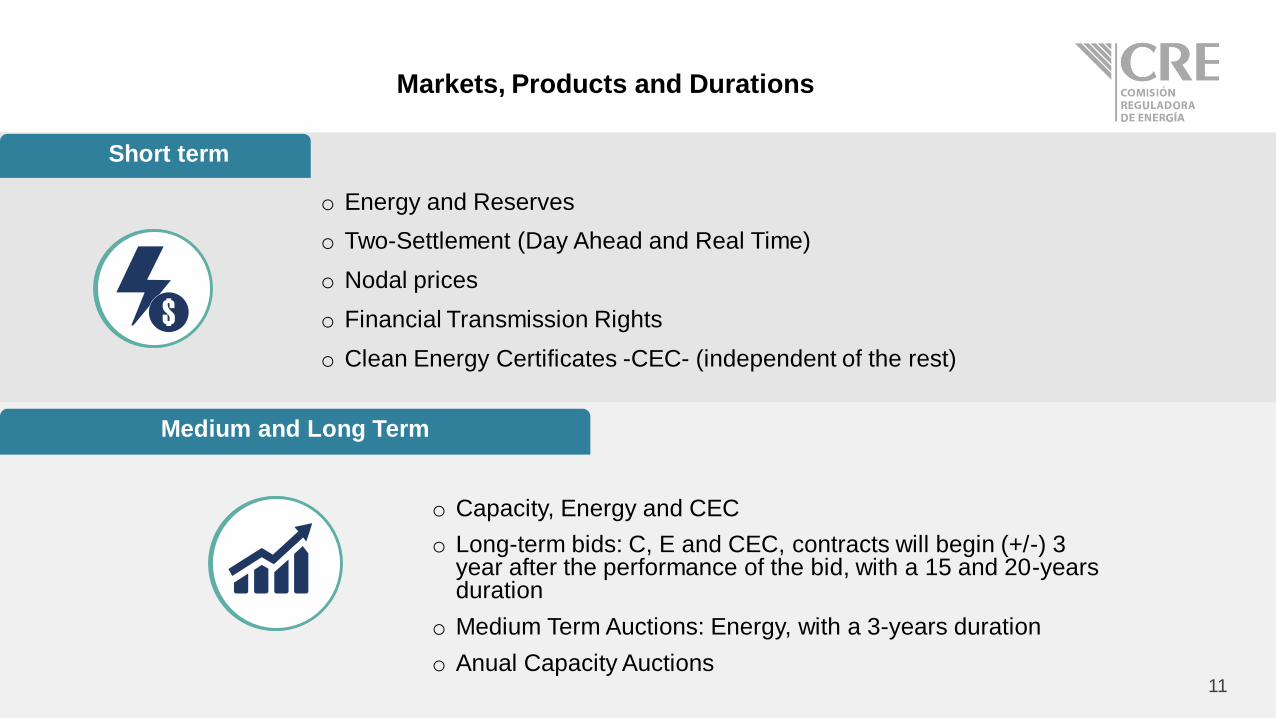

Markets, Products and Durations

o Energy and Reserves

o Two-Settlement (Day Ahead and Real Time)

o Nodal prices

o Financial Transmission Rights

o Clean Energy Certificates -CEC- (independent of the rest)

11

Short term

Medium and Long Term

o Capacity, Energy and CEC

o Long-term bids: C, E and CEC, contracts will begin (+/-) 3 year after the performance of the bid, with a 15 and 20-years duration

o Medium Term Auctions: Energy, with a 3-years duration

o Anual Capacity Auctions

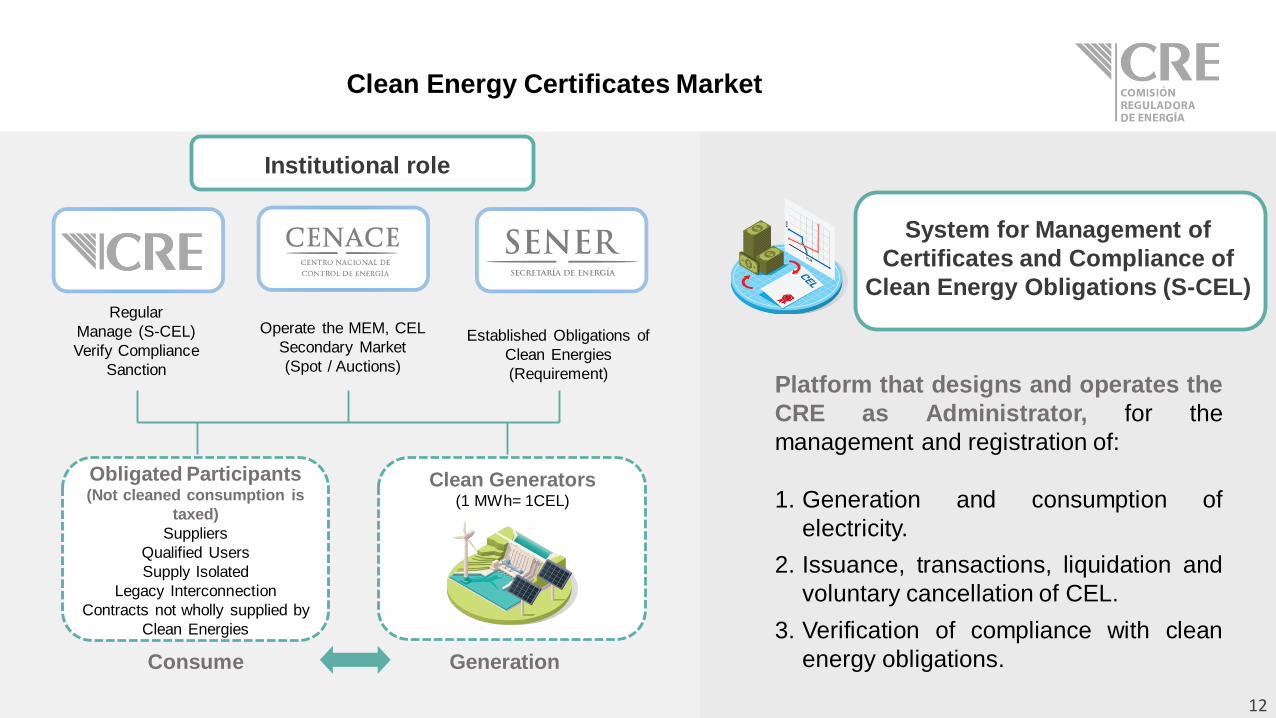

Regular

Manage (S-CEL)

Verify Compliance

Sanction

Operate the MEM, CEL

Secondary Market

(Spot / Auctions)

Established Obligations of

Clean Energies

(Requirement)

Clean Generators(1 MWh= 1CEL)

Obligated Participants (Not cleaned consumption is

taxed)

Suppliers

Qualified Users

Supply Isolated

Legacy Interconnection

Contracts not wholly supplied by

Clean Energies

Consume Generation

Institutional role

System for Management of

Certificates and Compliance of

Clean Energy Obligations (S-CEL)

Clean Energy Certificates Market

12

Platform that designs and operates the

CRE as Administrator, for the

management and registration of:

1. Generation and consumption of

electricity.

2. Issuance, transactions, liquidation and

voluntary cancellation of CEL.

3. Verification of compliance with clean

energy obligations.

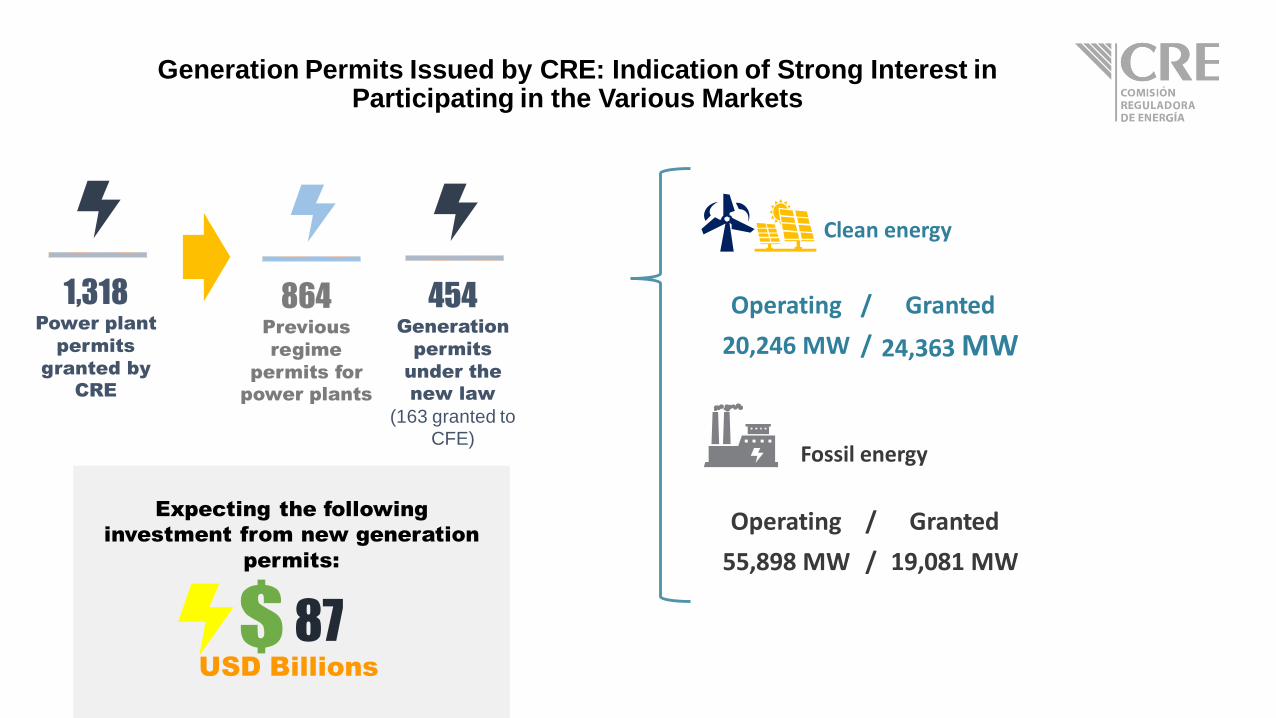

Generation Permits Issued by CRE: Indication of Strong Interest in Participating in the Various Markets

Expecting the following

investment from new generation

permits:

454Generation

permits

under the

new law

(163 granted to

CFE)

USD Billions

87

864Previous

regime

permits for

power plants

1,318Power plant

permits

granted by

CRE

Clean energy

Operating / Granted

20,246 MW / 24,363 MW

Operating / Granted

55,898 MW / 19,081 MW

Fossil energy

Short-term DA Market

DA Price Duration Curve SIN (2016 & 2017)

Fuente: Centro Nacional de Energía

Participation in the Short-term Markets is Increasing

Basic service retailerGenerators

Non-retailer marketer6 generation

companies5 Generators

18

CFE qualified

retailer

Qualified user

• 27 qualified users (1,019 load

centers) have a market

participation contract, but only:

o 6 qualified users (33 load

centers) have in operation a

market participation contract.

Potential of 4,274 load

centers with demand

equal or greater than 1

MW

3

Qualified Retailer

5

28

Energía Azteca X, S.A. de C.V.

Grupo Energético Elan, S.A.P.I. de

C.V.

1

Short-Term Capacity Market

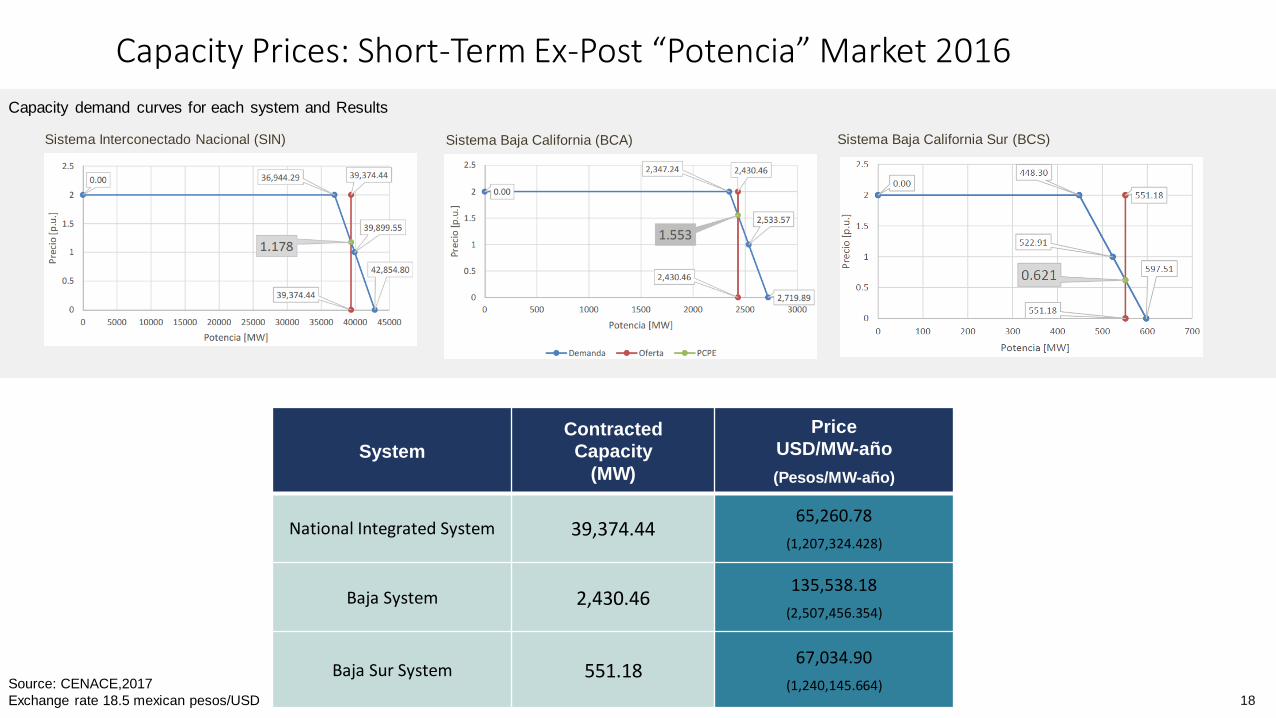

Capacity Prices: Short-Term Ex-Post “Potencia” Market 2016

18

System

Contracted

Capacity

(MW)

Price

USD/MW-año

(Pesos/MW-año)

National Integrated System 39,374.4465,260.78

(1,207,324.428)

Baja System 2,430.46135,538.18

(2,507,456.354)

Baja Sur System 551.1867,034.90

(1,240,145.664)

Capacity demand curves for each system and Results

Source: CENACE,2017

Exchange rate 18.5 mexican pesos/USD

Sistema Interconectado Nacional (SIN) Sistema Baja California Sur (BCS)Sistema Baja California (BCA)

Long-Term Market

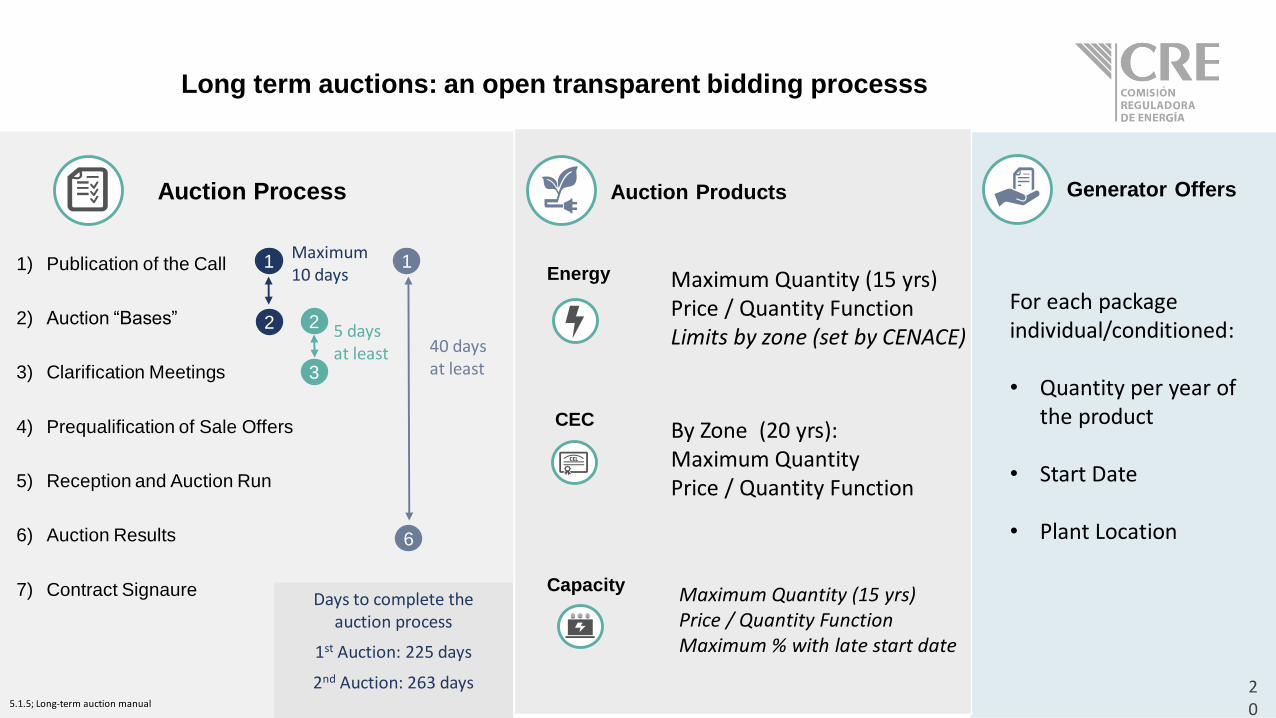

Long term auctions: an open transparent bidding processs

20

1) Publication of the Call

2) Auction “Bases”

3) Clarification Meetings

4) Prequalification of Sale Offers

5) Reception and Auction Run

6) Auction Results

7) Contract Signaure

40 days at least

1

6

1

2

Maximum 10 days

2

3

5 days at least

Auction Process

5.1.5; Long-term auction manual

Capacity

Energy

CEC

Maximum Quantity (15 yrs)Price / Quantity FunctionMaximum % with late start date

Maximum Quantity (15 yrs)Price / Quantity FunctionLimits by zone (set by CENACE)

By Zone (20 yrs):Maximum QuantityPrice / Quantity Function

Auction Products Generator Offers

For each packageindividual/conditioned:

• Quantity per year of the product

• Start Date

• Plant Location

Days to complete the auction process

1st Auction: 225 days

2nd Auction: 263 days

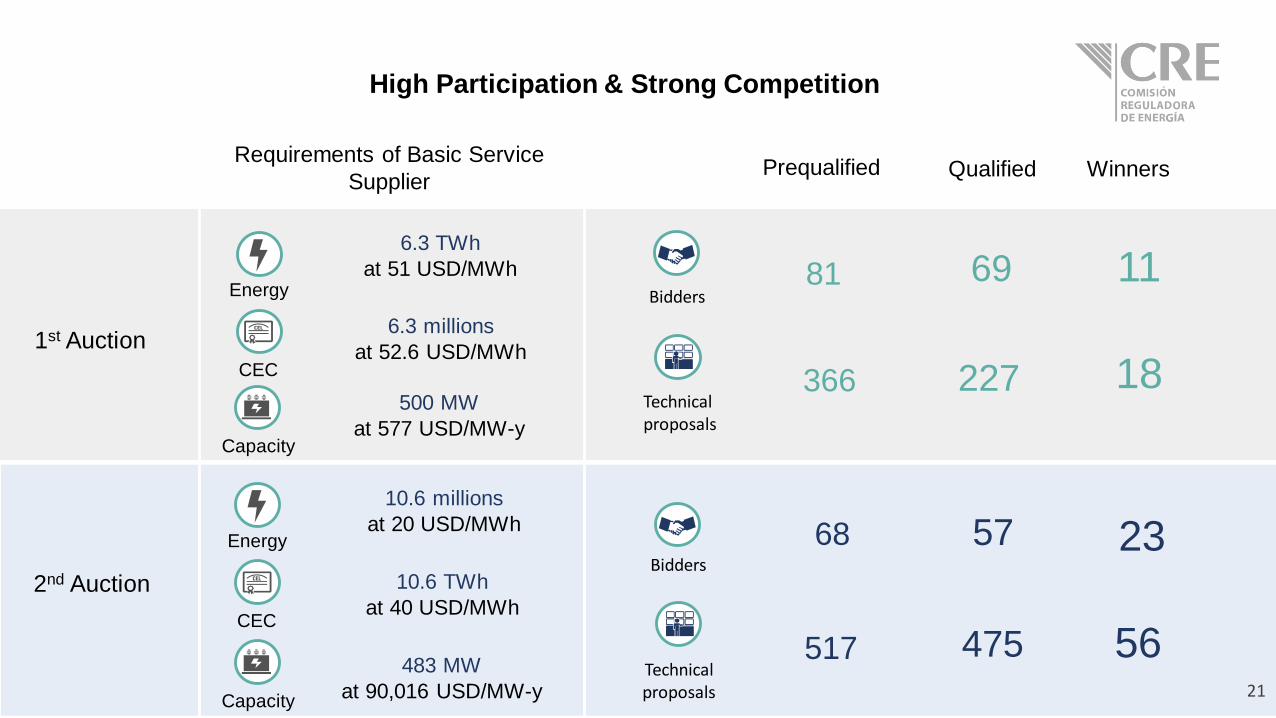

High Participation & Strong Competition

21

1st Auction

Requirements of Basic Service

Supplier

6.3 TWh

at 51 USD/MWh

2nd Auction

Prequalified Qualified

366

81

68

517

57

475

69

227

Bidders

Technical proposals

Bidders

Technical proposals

Winners

11

18

23

56

Capacity

500 MW

at 577 USD/MW-y

Energy

CEC

6.3 millions

at 52.6 USD/MWh

Capacity

Energy

CEC

483 MW

at 90,016 USD/MW-y

10.6 TWh

at 40 USD/MWh

10.6 millions

at 20 USD/MWh

Chih

Coah

BC

NL

Tamps

Oax

SLP

Gto

Ags

Mor

Pue

Son

Yuc

Jal

TX

22

Solar

Wind

HydroCombined

Cycle

34 companies from

more than 10 countries,

including Mexico

6.6 billion

of investment in the

coming years

Results of the first two long-term auctions

Increase of 5,000 MW to the current generation

capacity in Mexico

44.97

55.33

31.70

35.50

USD/MWh

USD/MWh

1st 2nd

Clearing prices

Solar Wind

23

1st Auction / 11 companies 2nd Auction / 24 companies

Winning companies of the two long-term auctions

Access to Networks & New Regulatory and Contractual Scheme for Transmission Expansions

New Rules that Guarantee Access to Networks

25

Open Access and Service Terms for Transmission and Distribution

(RES/948/2017)

Allows open access to transmission and distribution networks.

Transmission Rates(A/045/2015)

Income required 2016 2,335 millions USD. Example: Tension

rates greater than or equal to 220 kV, generators: 2.77 USD/MWh &

consumers: 3.49 USD/MWh.

Distribution Rates(A/074/2015)

16 distribution divisions, income required 5,092 millions of USD. An average tariff of 0.1296 USD/MWh

System Operator Charges: Cenace

(A/001/2017)

Income required 140 millions of USD, tariffs in USD/MWh for generators

0.1404 & loads 0.3669

Operation

Operational

conditions to ensure

the electrical supply

in conditions of safety

and continuity

6

Planning

Conditions that are

mandatory compliance

in the elaboration of the

programs of Expansion

and Modernization of

the National

Transmission Grid

(NTG) and the General

Grid of Distribution

Generation

Technical

requirements that

must be met by the

Power Plant Units

that wish to

interconnect to the

NTG

Load Center

Technical requirements

to be met by Load

Centers that intend or

are connected to the

NTG

Grid Code Includes

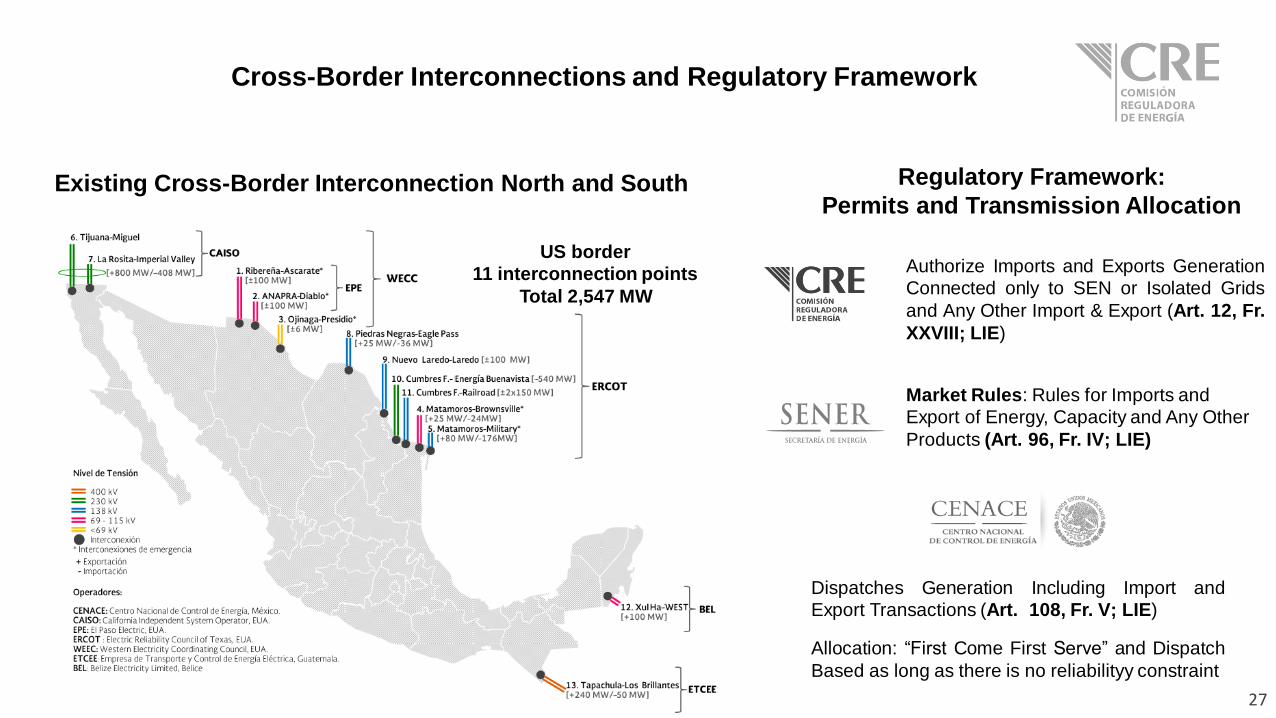

Cross-Border Interconnections and Regulatory Framework

27

US border

11 interconnection points

Total 2,547 MW

Authorize Imports and Exports Generation

Connected only to SEN or Isolated Grids

and Any Other Import & Export (Art. 12, Fr.

XXVIII; LIE)

Dispatches Generation Including Import and

Export Transactions (Art. 108, Fr. V; LIE)

Allocation: “First Come First Serve” and Dispatch

Based as long as there is no reliabilityy constraint

Market Rules: Rules for Imports and

Export of Energy, Capacity and Any Other

Products (Art. 96, Fr. IV; LIE)

Regulatory Framework:

Permits and Transmission AllocationExisting Cross-Border Interconnection North and South

Private Investment for Transmission ExpanssionsRegulation That Sets Revenue Requirements for Private and PP Transmission

Expansion Projects (Arts. 30, 31 Electric Industry Law)

28(A/009/2016)

• In the auction winner is the bidder with lowest (NPV) annual revenue requirement

• The annual requirement (annuity) includes all expenses and returns as per bidder expectations

• The annual income will an adder to overall transmission rates and passes to consumers

• Annual requirement adjusted to annual indexes indicated in the regulation

The Regulation is applicable to projects included in the Program of Development of the National Electrical System

Annual income will be set as a result of the competitive process

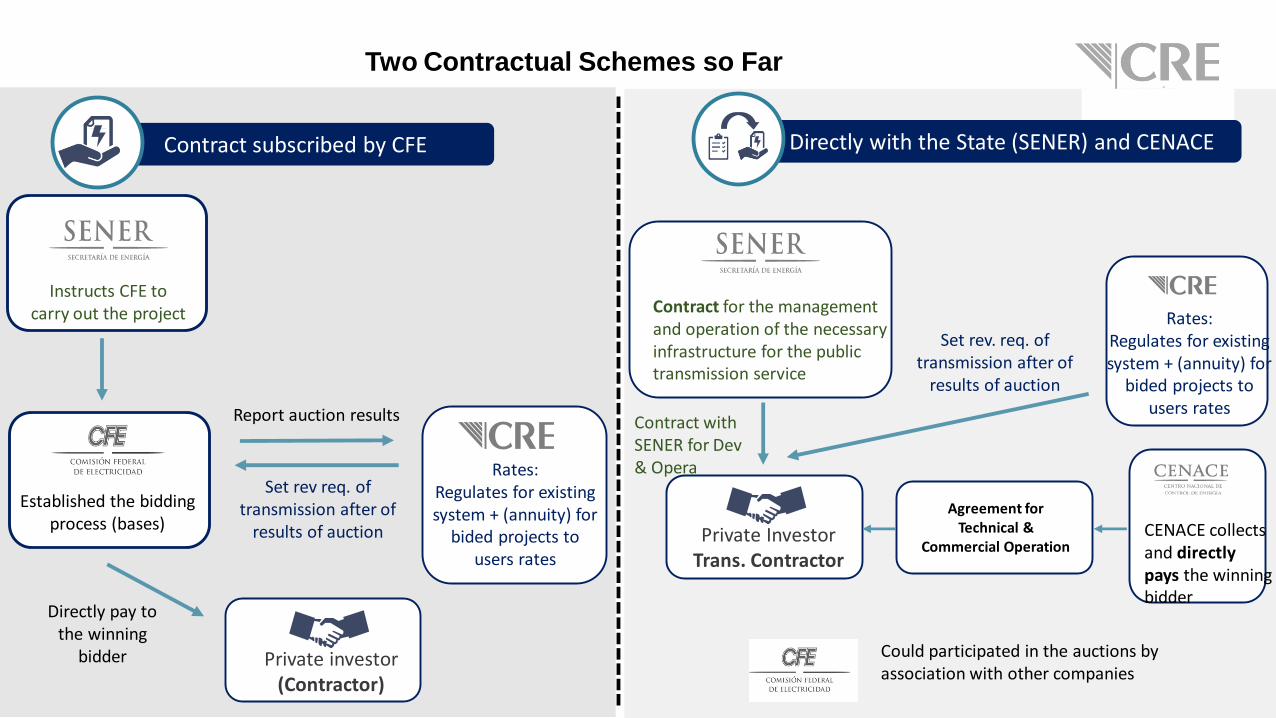

Two Contractual Schemes so Far

Contract subscribed by CFE Directly with the State (SENER) and CENACE

Established the bidding process (bases) CENACE collects

and directly pays the winning bidder

Could participated in the auctions by association with other companies

Agreement for Technical &

Commercial OperationPrivate Investor

Trans. Contractor

Contract for the management and operation of the necessary infrastructure for the public transmission service

Instructs CFE to carry out the project

Rates:Regulates for existing system + (annuity) for

bided projects to users rates

Private investor(Contractor)

Set rev req. of transmission after of

results of auction

Directly pay to the winning

bidder

Report auction results Contract with SENER for Dev & Opera

Set rev. req. of transmission after of

results of auction

Rates:Regulates for existing system + (annuity) for

bided projects to users rates

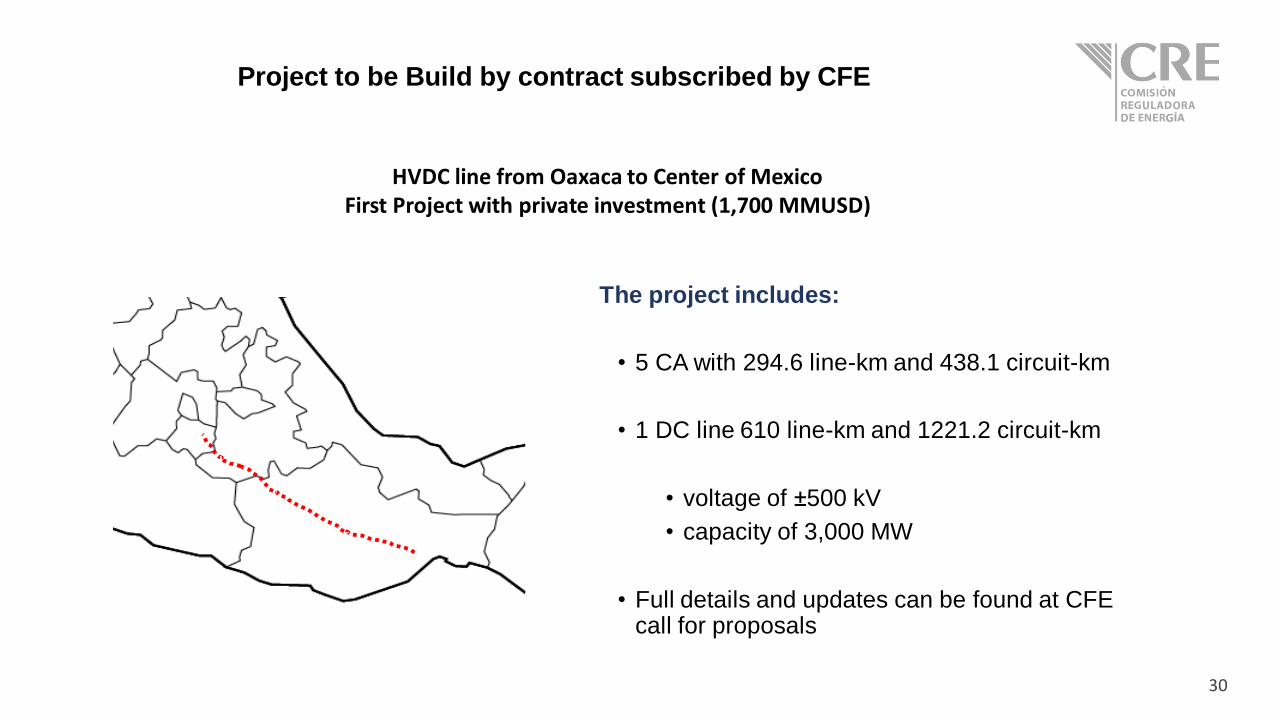

Project to be Build by contract subscribed by CFE

30

The project includes:

• 5 CA with 294.6 line-km and 438.1 circuit-km

• 1 DC line 610 line-km and 1221.2 circuit-km

• voltage of ±500 kV

• capacity of 3,000 MW

• Full details and updates can be found at CFE call for proposals

HVDC line from Oaxaca to Center of MexicoFirst Project with private investment (1,700 MMUSD)

Potential Projects Under New Contractual Scheme

Development transmission Grid between 2017 and 2029:

• Investment of 11,899 MMUSD• Increment of 104,133 km

National Grid -Baja Tamaulipas

Start operation date: April, 2021

• Investment: 1,109 MMUSD• Technology: HVDC + CA• Length: 104,133 km-c (CD)

and 496 km-c (CA)

Start operation date: June, 2021

• Investment: 176 MMUSD• Technology: CA• Length: 275 km-c

Sources:Sub-secretary of electricity, Secretary of Energy.

The Retail Markets

Size of the Potential Qualified Users Market

3.8%

6.1%

14.1%

23.1%

27.2%

34.2%

40.1%

43.7%

52.9%

58.3%

64.5%

100%

16

46

429

1,753

3,052

7,344

18,295

30,391

104,354

220,340

738,501

40,251,336

521,514,367

170,269,608

46,054,896

14,999,543

7,030,063

3,566,949

1,199,742

657,149

273,813

102,394

26,498

1,984

0 100,000,000 200,000,000 300,000,000 400,000,000 500,000,000 600,000,000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

>= 100,000

>= 50,000 y < 100,000

>= 10,000 y < 50,000

>= 3,000 y < 10,000

>= 2,000 y < 3,000

>= 1,000 y < 2,000

>= 500 y < 1,000

>= 300 y < 500

>= 100 y < 300

>= 50 y < 100

>= 10 y < 50

>= 0 y < 10

Number of users accumulated

Demanda Contratada

KW

% of total energy consumption per KWh

Average annual consumption per user (KWh)

3381 users / 1,319 load centers

Qualified UserRegistration

Nuevos Agentes y Participantes en Mercado de Corto Plazo

Suministro

Básico

Generadores

Comercializadores

no Suministradores

6 Empresas de

Generación5 Generadores

18

1CFE Suministro

Calificado

Usuarios

Calificados

Permisos otorgados por la

CRE a septiembre 2017

454

31

84• 27 Usuarios Calificados (que representan 1,019

centros de carga) celebraron un contrato con algún

Suministrador Calificado, de los cuales:

o 6 Usuarios Calificados (que representan 33

centros de carga) ya reciben el suministro

por parte de un Suministrador Calificado.

De 4,422 centros de

carga potenciales con

demanda igual o mayor

a 1 MW

Permisos de generación

Permisos de

suministro calificado

Registro de Usuarios

Calificados (representan

1,349 centros de carga)

3Registros de Comercializadores

no Suministradores

13

Suministradores Calificados

5 1Permisos de

suministro básico

28

Energía Azteca X, S.A. de C.V.

Grupo Energético Elan, S.A.P.I. de C.V.

Qualified Supply by New Companies Has Started

35

De los 20 Suministradores Calificados,

5* cuentan con Usuarios Calificados

registrados para brindarles servicio.

Sum 30.01%

Sum 20.02%

Sum 11.13%

Otros (CFE y autoabasto)98.85%

Participación en las ventas realizadas en el mes

de Mayo por Suministrador

Permisos otorgados por la

CRE a septiembre 2017

454

31

84

Permisos de generación

Permisos de

suministro calificado

Registro de Usuarios

Calificados (representan

1,349 centros de carga)

Registros de Comercializadores

no Suministradores

13

1Permisos de

suministro básico

A New “Retail” Choice for Consumers:New Behind The Meter DG + Storage Regulations

Bi-directional meter

Excess energy accumulates in

favor of the generator

Missing energy is

compensated with

accumulated energy

Exchange

if credit in favor is

exhausted is charged

at applicable tariff

Net Metering

Energy delivered to the General Distribution Grid (GDG)

Energy delivered by Basic

Service Supplier (BSS)

Net Billing

Energy delivered to the GDG

Total sale

*Users can choose the scheme

The suggested recruitment period is one year

Variety of Schemes to Choose Billing

BSS

GDG

BSS

GDG

BSS

GDG

Energy delivered

by the supplier

Energy delivered

by the generator

Energy delivered

by the generator

It is paid based on the

benefit system ≈ PML

Energy delivered by

the supplier

The applicable

fee is charged

Energy delivered

by the generator

Market price

≈ PML

8

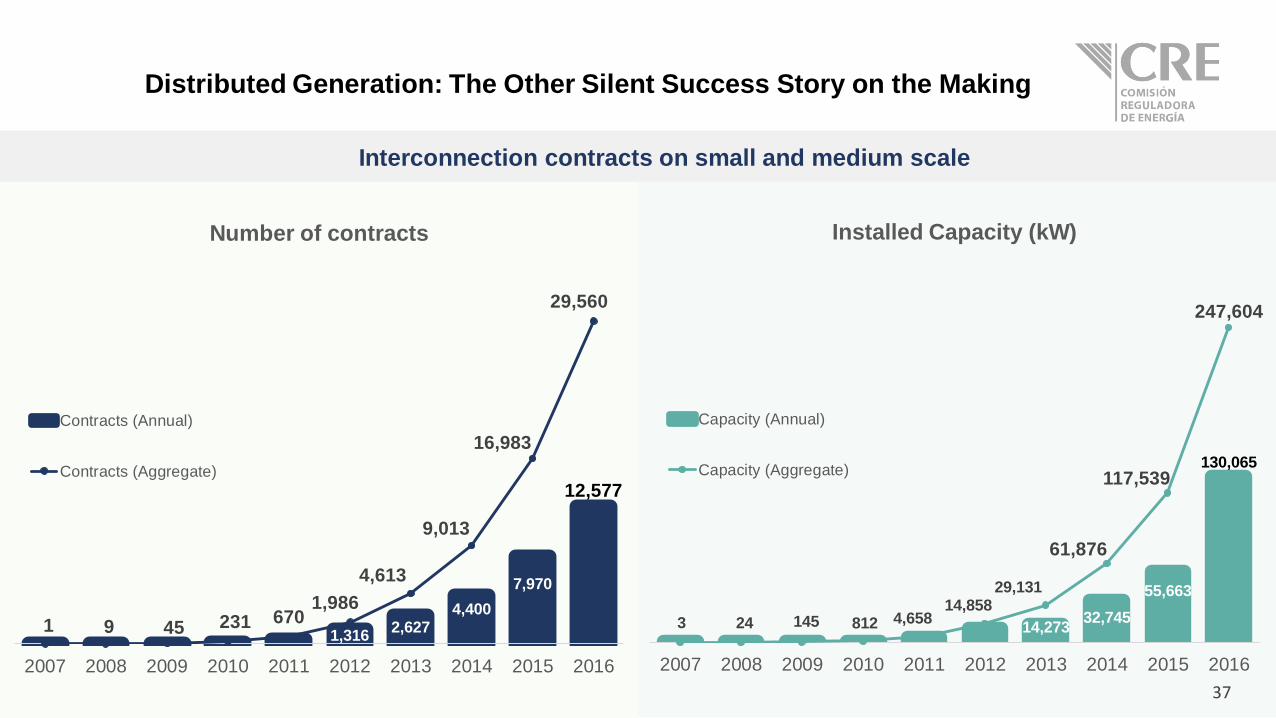

Interconnection contracts on small and medium scale

Distributed Generation: The Other Silent Success Story on the Making

37

14,27332,745

55,663

130,065

3 24 145 812 4,65814,858

29,131

61,876

117,539

247,604

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Installed Capacity (kW)

Capacity (Annual)

Capacity (Aggregate)

1,3162,627

4,400

7,970

12,577

1 9 45 231 6701,986

4,613

9,013

16,983

29,560

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Number of contracts

Contracts (Annual)

Contracts (Aggregate)

(*) Elaborated by CRE, with information from CFE. Data for 201638

2

831

14

106

3,361

12,611

Alta Tensión

Media Tensión

Agrícola

Servicios Públicos

General Baja Tensión

Residencial

Number of contracts2014-2016*

352

49,598

337

239

21,930

48,862

Installed capacity (kW)2014-2016*

Number of contracts and installed capacity per tariff group, distributed generation

Public services

Medium voltage

High voltage

Agriculture

Residential

General low voltage

Regulatory Perspectives

The Secretary of Energy will transfer market rules to CRE following the reform Act provisions

CRE will approve Call and Bidding Rules for the 4th Long-Term Auction

CRE will issue quarterly, if applicable, decisions based on independent market monitor reports

Launch of the "first stage" of the Clean Energy Certificates Market. Operation in 2018 of the clean energy certificate registry

2017

2018

Next steps: Wholesale Market Related

1

2

3

4

Issue terms for the accounting, operational and functional separation of the members of the electrical industry

General Administrative Provisions Relating to the access and distribution of restricted information between different market participants

5

6

Next Steps: Creation and Growth of the Qualified Supply Market

Basic supply

market rates

Regulated ratesGeneration cost

Final Supply Basic Tariffs

Basic service retailer

Transmission Distribution ISO Ancillary Services not included in

Wholesale Electrical Market

Standard on Energy Metering

SystemsEstablish specifications; test, review, quality assurance and evaluation

methods; as well as the functional requirements for meters

Fine tune regulatory instruments:

to precise metering rights and

obligations

Metering and Settlement

Manual of WEM Rules

Grid CodeInterconnection /

Connection Criteria

Document

General Administrative

Provisions Relating to

Contributions

General Administrative

Provisions Relating to

Supply

WEM “Bases”

1

2

3

Next steps: Related to Transmission Access, New Technologies & Standards

Development of a Standard for Electrical Installations of Generation, Transmission and Distribution of electrical energy. First with focus on interconnection infrastructure

Issuance of new Transmission and Distribution rates, applicable for the new regulatory period starting 2019

Installation of the Grid Code Committee for Ongoing Improvement: CENACE, Suppliers and Generators, others.1

2

3

Issue Storage Related Regulation: General Administrative Provisions or Related Instruments

4

2017

2018

Next steps: Isolated (Onsite) Supply and DG

A contract that allows several users to share generation from up-to 500 kW installations, eliminating barriers to

ownership of previous schemes

Collective Distributed Generation Contract

1 installation

1 owner(private or company)

Multiple users

Multiple users

2

Interpretation of "own needs" applicable to Isolated Supply

To clarify the scope of the concept "own needs" in Article 22 of the Law of the Electrical Industry, as well as to describe the general aspects applicable to the Isolated Supply Activity.

1

Mark your calendars:

1,000

46

Thank you !@M_Madrigal_M

@CRE_Mexico