ekonomi, keuangandanakuntansi syariahmenyongsongera fintech · hotel & motel brick-n-mortar...

TRANSCRIPT

Department of AccountingFaculty of Economics and Business

Universitas Padjadjaran

Ekonomi, Keuangan dan AkuntansiSyariah menyongsong Era Fintech

Unpad Training CenterJl. Ir. H. Djuanda No.4

Pendidikan Profesional Berkelanjutan – IAI Jawa Barat

24-May-18

------

Hamzah [email protected]

BSc – Universitas PadjadjaranMBIT – UniversityofMelbourneDr – HumboldtUniversität zu Berlin

Activities:LecturerandResearcher@Universitas Padjadaran

PartnerinResearch@VedaPraxis

linkedin.com/in/hamzahritchi/

34-May-18

TakeawaysFinTech Landscape Opportunity & Challenge

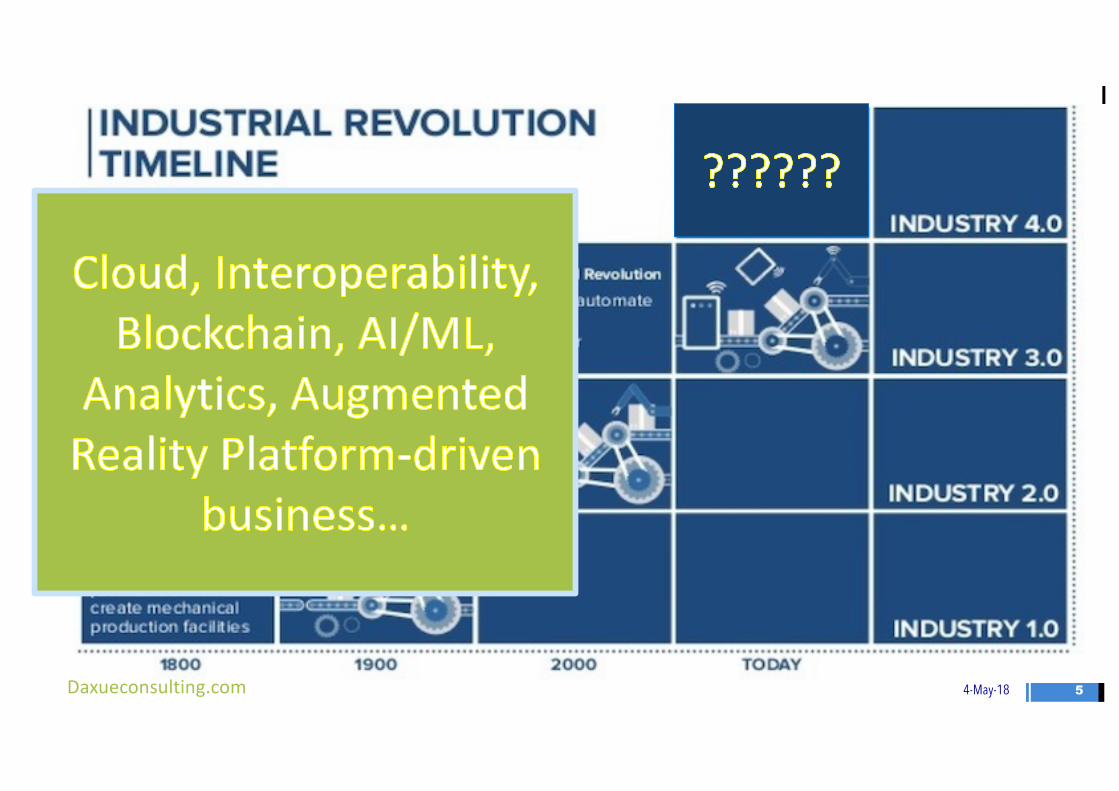

Current Evolvement

4

Current Evolvement

4-May-18

TakeawaysFinTech Landscape Opportunity & Challenge

“You could not step twice into the same rivers, for other waters flow on”

― Heraclitus”

54-May-18Daxueconsulting.com

64-May-18

Ecosystem is reshaping

Preservingproprietary

Etablished structure

Dictatingconsumersandusers

Fromeconomyofscarcity

Encouragingtransparency

Agilityandflexibility.

Moreexercisingtheirpower.

Economyofabundance.

74-May-18Source:“DigitalGlobalisation:TheNewEraofGlobalFlows”,MGI,Mar2016

84-May-18

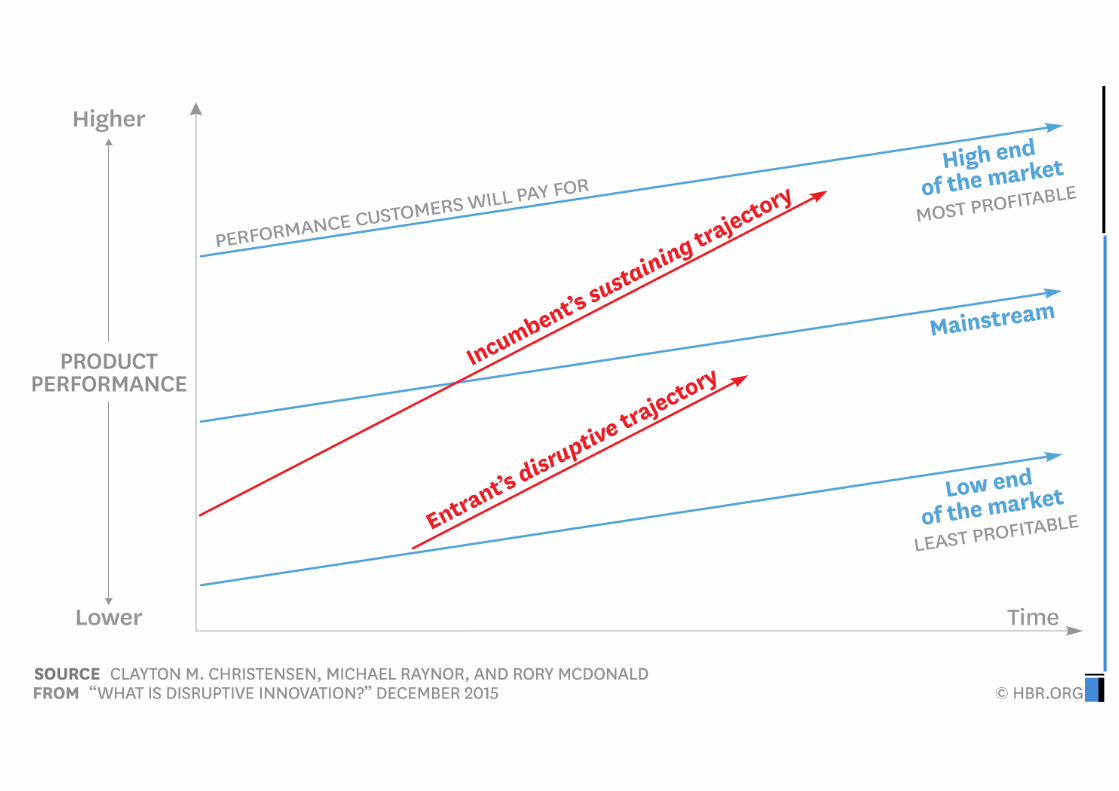

Process by which a product or service takes root initially in simple

applications at the bottom of a market and then relentlessly moves up market,

eventually displacing established competitors.

~ Clayton Christensen

Understanding Disruptive Technology

94-May-18

104-May-18

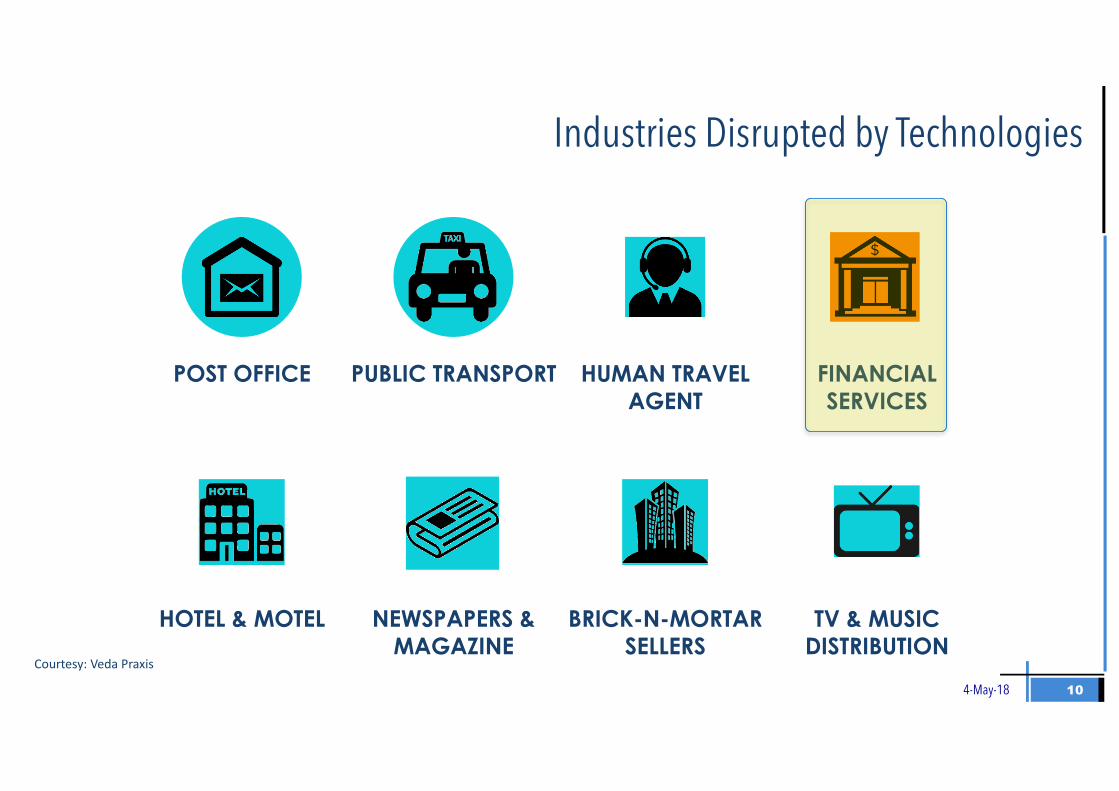

Industries Disrupted by Technologies

PUBLIC TRANSPORTPOST OFFICE HUMAN TRAVEL AGENT

FINANCIAL SERVICES

NEWSPAPERS & MAGAZINE

HOTEL & MOTEL BRICK-N-MORTAR SELLERS

TV & MUSIC DISTRIBUTION

Courtesy:VedaPraxis

114-May-18

- Improves Budgeting Accuracy

- Improves Planning / Forecasting

- Secured Process- Immediate Evaluate Risks

- Uninterrupted Auditing- Gain Access to Real-Time

Transactional Data- Immediate Respond to

Issues

- Save time- Reduce Cost- Increase Productivity- Overcome Human Limits- Better Accuracy

- Automated Data Entry- Data Categorization- Organized Administration- Cloud Based System

What Disruptive Technology Would Mean

124-May-18 12

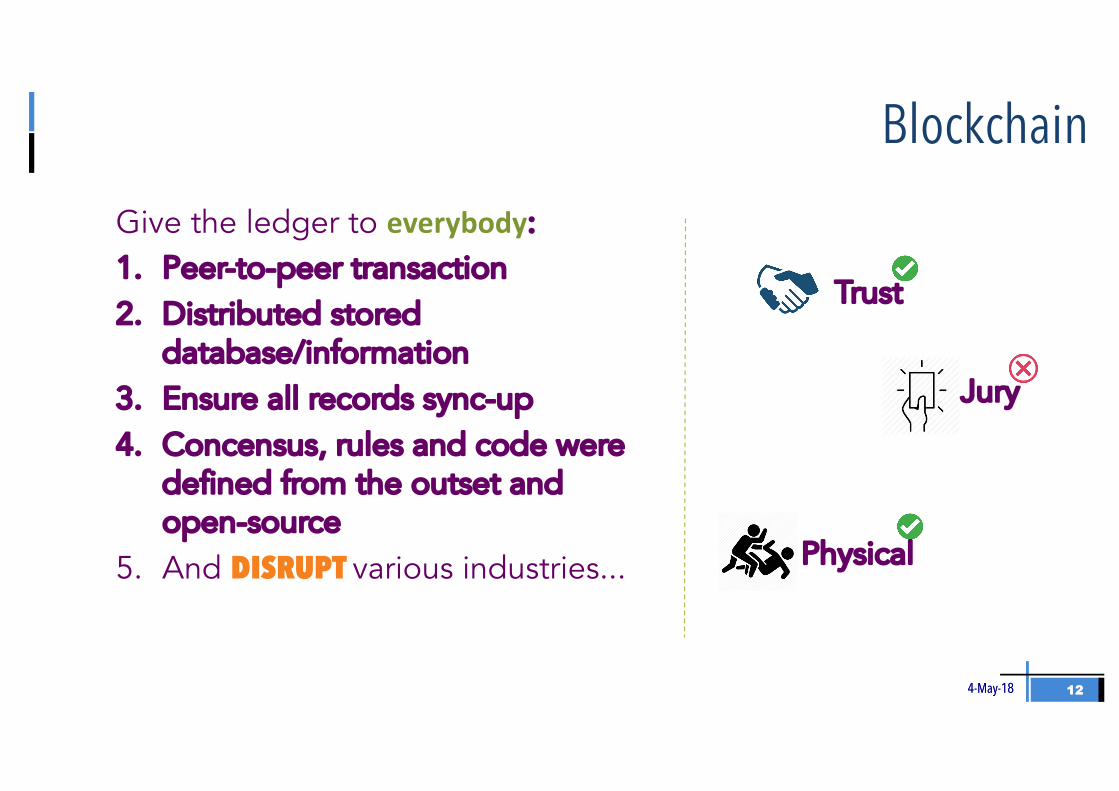

Blockchain

4-May-18

Give the ledger to everybody:1. Peer-to-peer transaction2. Distributed stored

database/information3. Ensure all records sync-up4. Concensus, rules and code were

defined from the outset and open-source

5. And DISRUPT various industries... Physical

Jury

Trust

134-May-18

TakeawaysOpportunity & Challenge

Current Evolvement

FinTechLandscape

“Technology has always been destroying jobs, and it has

always been creating ― Erik Brynjolfsson”

144-May-18

Indonesia Digital Economy Landscape

154-May-18

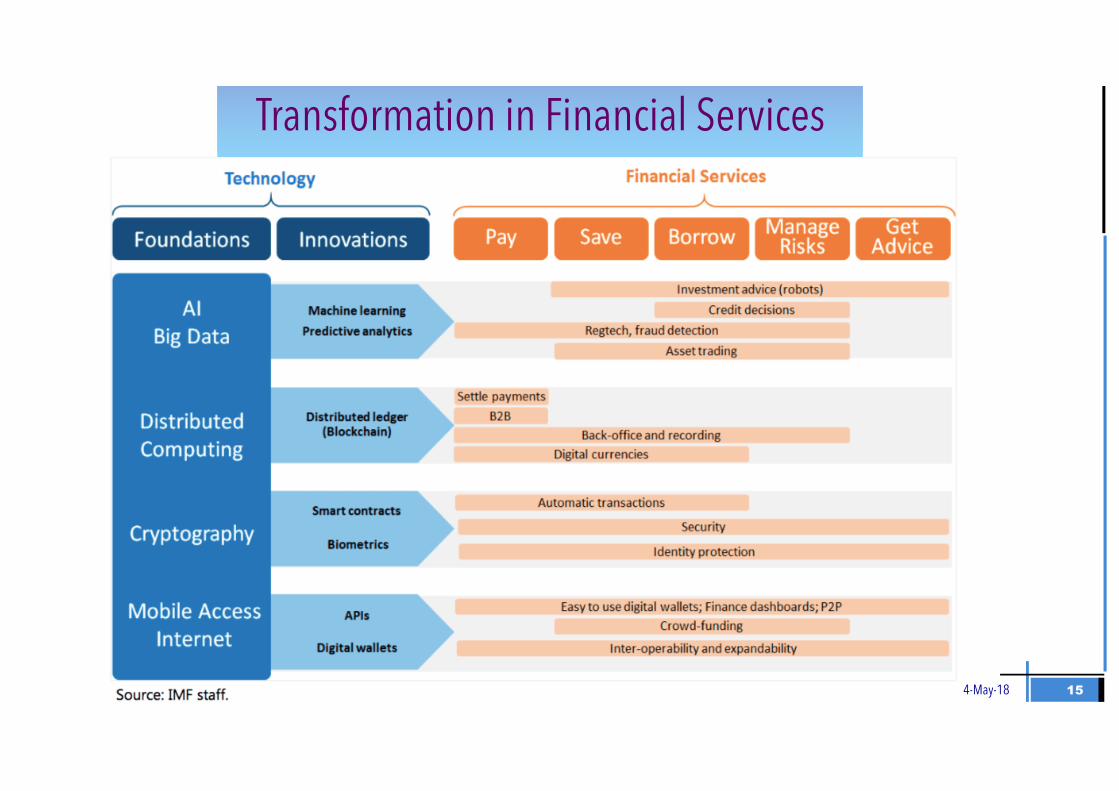

Transformation in Financial Services

164-May-18Source:“ValueofFinTech (KPMG)”,October2017

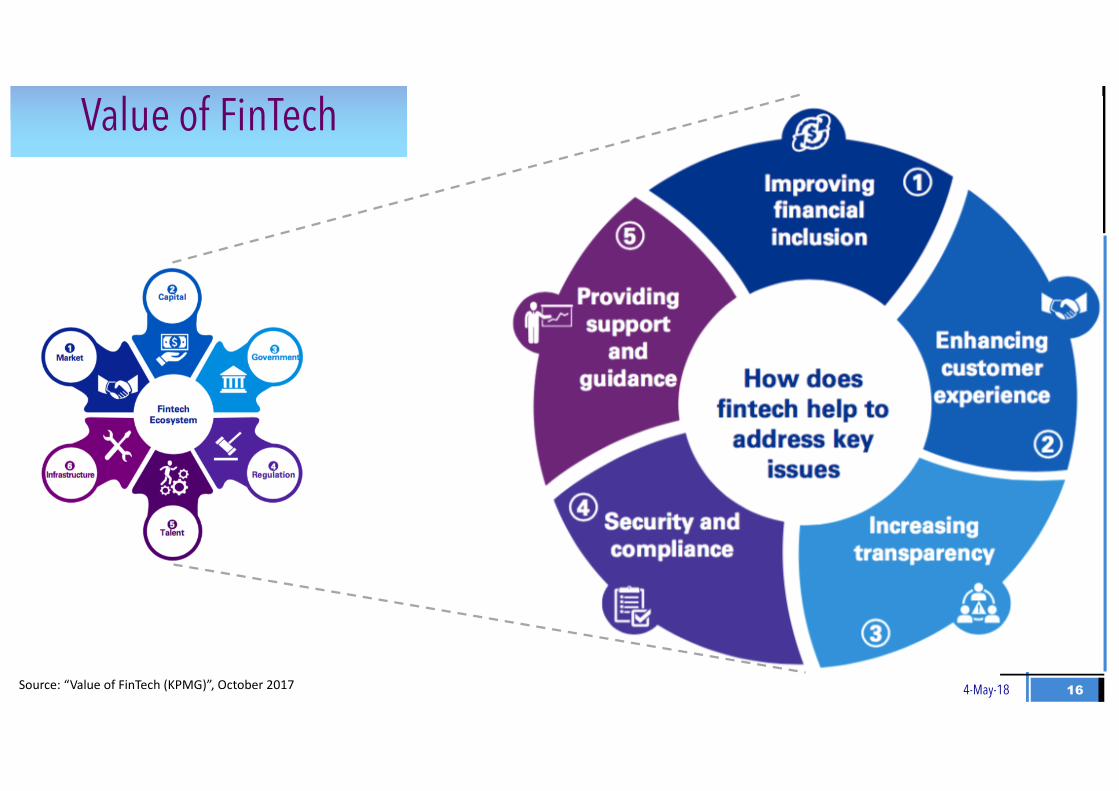

Value of FinTech

17

Indonesia Fintech Start-up Map

4-May-18Source: (http://fintechnews.sg , 2016)

184-May-18

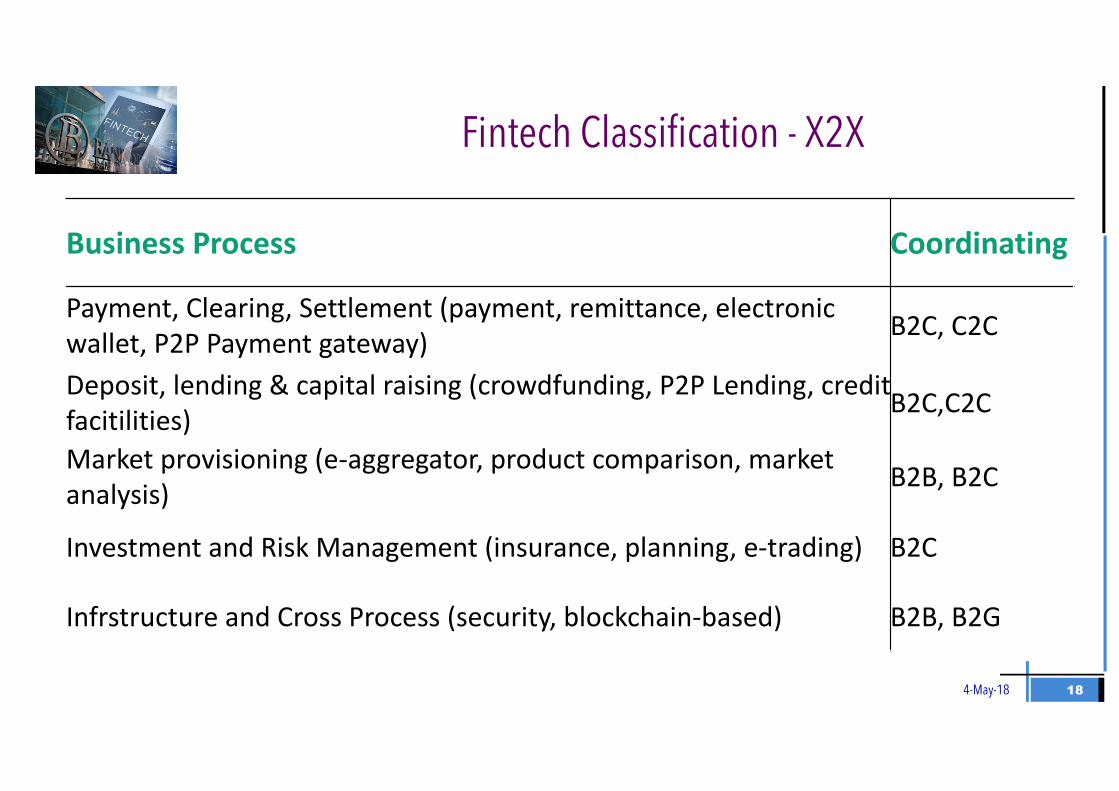

Fintech Classification - X2X

BusinessProcess Coordinating

Payment,Clearing,Settlement(payment,remittance,electronicwallet,P2PPaymentgateway) B2C,C2C

Deposit,lending&capitalraising(crowdfunding,P2PLending,creditfacitilities) B2C,C2C

Marketprovisioning(e-aggregator,productcomparison,marketanalysis) B2B,B2C

InvestmentandRiskManagement(insurance,planning,e-trading) B2C

Infrstructure andCrossProcess(security,blockchain-based) B2B,B2G

194-May-18

CATEGORIES

1. PaymentSystem2. MarketSupport3. Investment

Management&RiskManagement

4. Lending,Financing,andProvisionofCapital

5. OtherFinancialService

BI Regulations on FinTech

Source:BankIndonesiaRegulationNumber19/12/PBI/2017

REQUIREMENTS

1. Innovative2. Caninfluence

products,services,technologyand/orexistingfinancialbusinessmodels

3. Canbenefitthepublic4. Canbewidelyused5. OthercriteriasetbyBI

CRITERIAS

1. Innovative2. Caninfluence

products,services,technologyand/orexistingfinancialbusinessmodels

3. Canbenefitthepublic4. Canbewidelyused5. Othercriteriasetby

BI

204-May-18

BI Regulations on FinTech

Implementtheprincipleofconsumerprotection1

Maintainconfidentialityofconsumerdataand/orinformationincludingtransactiondataand/orinformation

2

Implementriskmanagementandprudentialprinciples

UseRupiahineverytransactionconductedinIndonesia,inaccordancewithprevailinglawsandregulationsoncurrency

Implementanti-moneylaunderingandpreventionofterrorismfundingprinciplesinaccordancewithprevailinglawsandregulations

3

4

5

AdheretootherprevailinglawsandregulationsinIndonesia6

Source:BankIndonesiaRegulationNumber19/12/PBI/2017

214-May-18

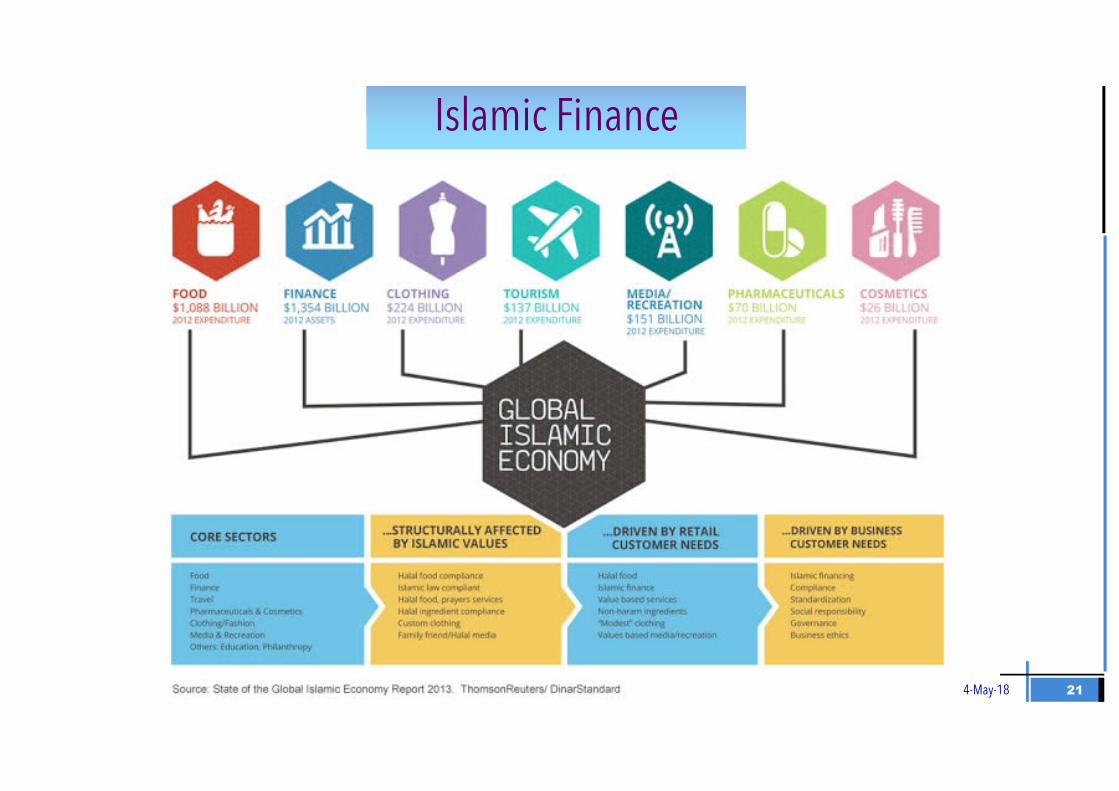

Islamic Finance

224-May-18

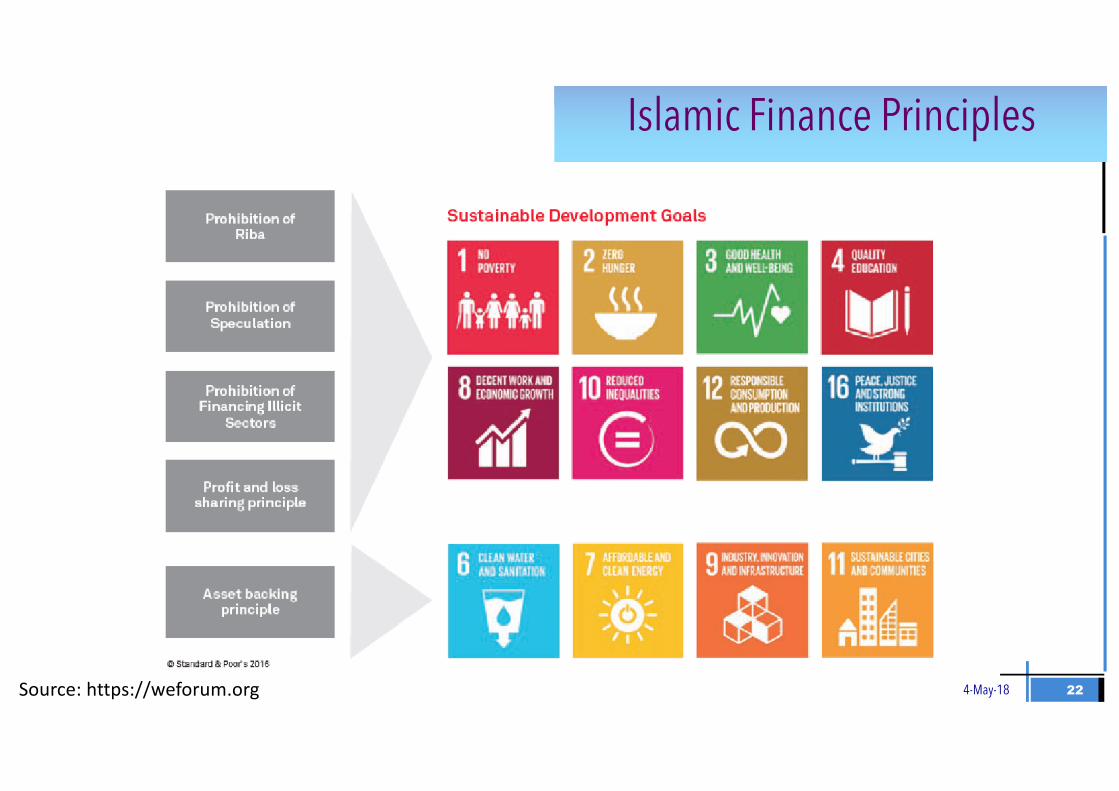

Islamic Finance Principles

Source:https://weforum.org

234-May-18

Islamic Finance Performance

Source:https://islamicbankers.me

244-May-18 234-May-18Source:https://bahrainfintechbay.com

Top Islamic FinTech Hubs

254-May-18Source:https://thumbor.forbes.com

264-May-18

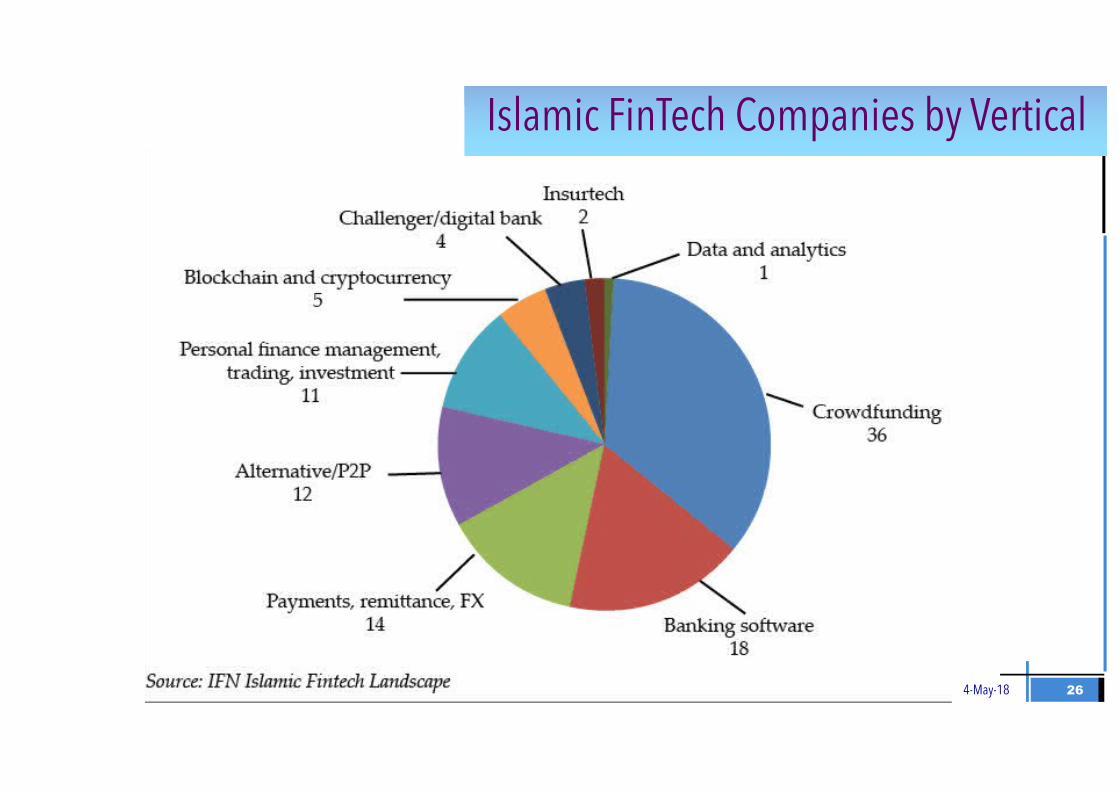

Islamic FinTech Companies by Vertical

274-May-18

Mechanics of Investment Account Platform

Source:“FinTech inIslamicFinanceasMalaysialaunchesInvestmentAccountPlatform(IAP)

284-May-18

Islamic FinTech Products in Indonesia

294-May-18

More on Islamic FinTech in Indonesia

Source:“indonesiadrc.id

304-May-18

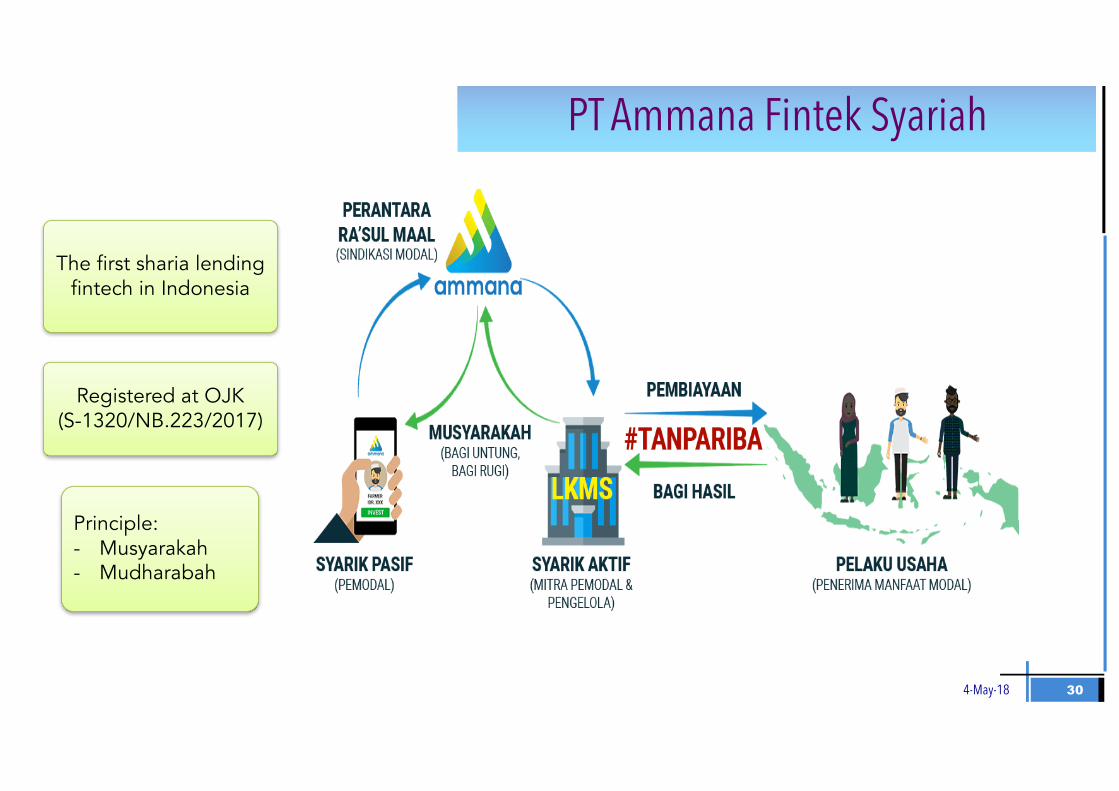

The first sharia lending fintech in Indonesia

Principle:- Musyarakah- Mudharabah

PT Ammana Fintek Syariah

Registered at OJK(S-1320/NB.223/2017)

314-May-18

Opportunity & Challenge

TakeawaysFinTech LandscapeCurrent Evolvement

“I could either watch it happen or be a part of it.”

― Elon Musk”

324-May-18

Islamic FinTech Challenges

Absenceofaregulatoryframework:1

Absenceofacentralizedshariagovernance2

WeakIslamicfinancecultureamongthepopulation

AbsenceofinnovationandR&DeffortsrelatedtoIslamicFinance

Networkbusinessofentry

3

4

5

334-May-18

Fintech Cyber RiskAccordingtoPwC’sGlobalFinTechSurvey2016,almost56%oftherespondentsidentifiedinformationsecurityandprivacyasthreatstotheriseoffintech

344-May-18

Meanwhile, in the start-up euphoria

#2 Run out of cash

#1 No Market need

#3 Not the right team

#4 Get outcompeted

#5 Cost/Pricing Issues

Source:CBInsights

354-May-18

willrobotstakemyjob.com

• Recording transaction is no longer on a manual basis and rely on manpower (POS, Reconciliation, Journal)

• Not every UMKM requires the whole package of accounting transaction

• Lack of automated financial practice on the industry

364-May-18

Courtesy:ManahanSialagan

37

Silver Lining

4-May-18

38

Membantu tujuan financial inclusion masyarakat Indonesia. Mendorong pertumbuhan sektor UMKM dan

perusahaan perintis berbasis digital.Memaksimalkan ekosistem yang tercipta antara

start-up digital dengan UMKM yang potensial.Menghadirkan solusi yang sistemik bagi

pertumbuhan industri dan bisnis digital

Peluang yang diciptakan Fintech

38

– Baru 36% penduduk Indonesia yang memiliki rekening bank (World Bank, 2014)

– Masyarakat tidak dapat dilayani industri keuangan tradisional:§ Perbankan terikat aturan yang ketat§ Keterbatasan industri perbankan dalam melayani

masyarakat di daerah tertentu.– Kebutuhan dukungan untuk mencapai Sektor Jasa

Keuangan Indonesia 2015 – 2019 yang kontributif, stabil, dan inklusif.

#1: Finansial yang Inklusif

39

4-May-18 40

3rd Rank

#2:Pertumbuhan Start-Up

www.startupranking.com

414-May-18

Huge Connectivity Base

4-May-18 42

#3:Maksimalisasi EkosistemInovasi Bisnis berbasis teknologi memberikan peluang dalam:

Pencocokan produk keuangan dengan struktur biaya dari UMKM yang perlu bertumbuh (fitur aplikasi, proses bisnis, dll).Mengidentifikasi peluang pasar yang belum tersentuh atau belum dikembangkan dengan optimal.Membuka peluang terhadap penguatan ekonomi regional dimana ekosistem tersebut ada.

4-May-18 43

#4:Solusi SistemikTumbuhnya UMKM mendorong penggunaan digitalisasi transaksi ekonomi

Fasilitas pembayaran menumbuhkan marketplacepenyedia jasa pembayaran.Penyedia P2P lending mendorong pembiasaan Pendanaan usaha bagai unbankable society.

Kedepannya literasi keuangan yang meningkat diharapkan menguatkan kemandirian dunia usaha dari keterbatasan akses modal.

444-May-18

Real world /Phenomena

Modelling and Simulation

Big Data Analysis

Business Prototype

Courtesy:ManahanSialagan

454-May-18

FinTech Financing Potential INA 15-21

464-May-18

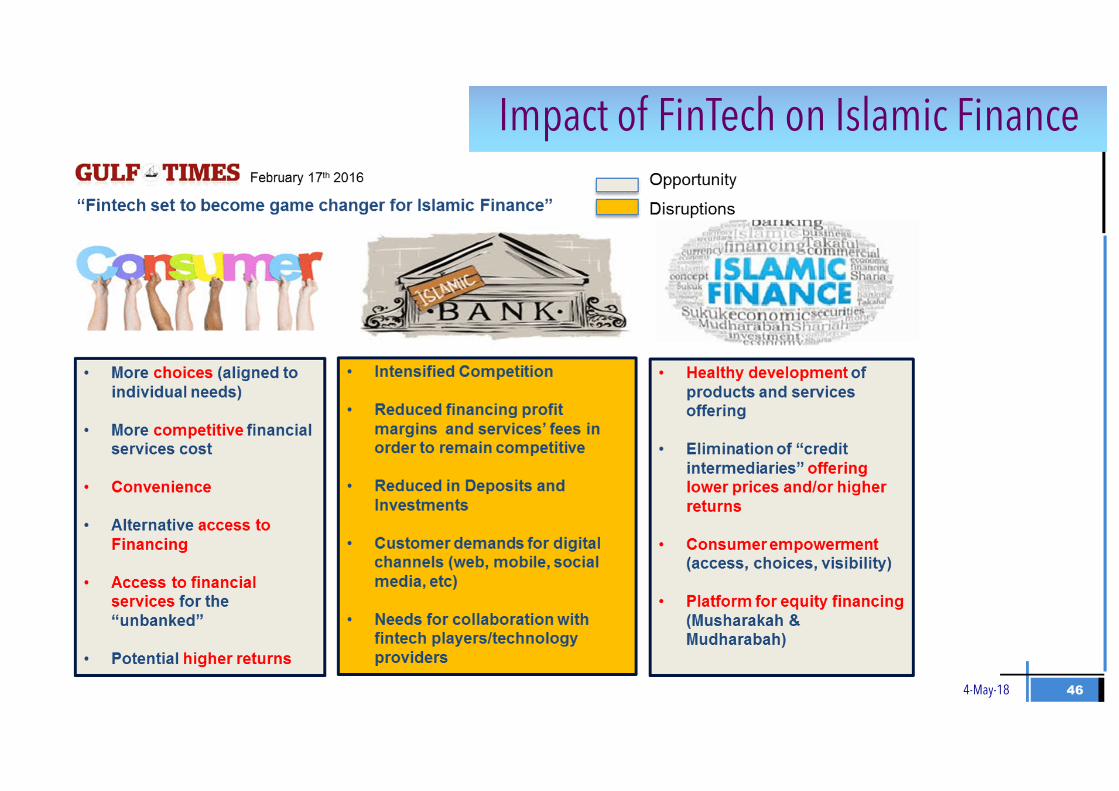

Impact of FinTech on Islamic Finance

474-May-18

Takeaways

FinTech Landscape Opportunity & Challenge

Current Evolvement

“a wealth of information creates a poverty of attention”

― Herbert Simon”

484-May-18

• TwoSidedMarket• PlatformOrganization• NetworkEffect• Search&TransactionCost• Demandeconomiesofscale–Feedbacks,claps,comments,stars,complaints

• EconomicsofAttention• SwitchingCostandLock-in• MetcalfeandMooreLaw

Technology disrupts, Wisdom stays

49

• Integrated platform digital sharia fintech• Maintain agility and adaptability • Able to analyze current development with evolving

econtech-wisdom• Team up to test new approaches and seek opportunity • Establish clear vision for transformation and to match

opportunities and value proposition. • Collaboration banking – fintech toreachcustomersand

to accesslowcostfunding.

Takeaways

4-May-18

50

• Regulatory risk-based supervision approach to fintechinnovation:– Regulation must take into account the innovation – Balancing the innovation environment with the mandate of

supervisors in consumer protection– Strenghtening insurance capital solvency due to increasing risk

and dynamic environment

• Better coordination with other authorities association and industry to create safe environment (e.g data protection, cyber security, better infrastructure

• Get involve and contribute in a completely new educational system that promotes agility and data driven awareness.

Takeaways

4-May-18

51

End

4-May-18

~ escape is an anti pattern ~