eicher motors (eicmot) -...

TRANSCRIPT

February 18, 2015

ICICI Securities Ltd | Retail Equity Research

Result Update

Great franchises rarely come cheap! • Eicher Motors’ (EML) Q4CY14 results were below our estimates on

the margins front while PAT was impacted by lower other income and higher depreciation

• The performance of Royal Enfield (RE) on the margins front has been strong with EBITDA margin improving 23.6%. It could have been better if not for various front loaded expenses

• VECV’s performance has also been admirable in a tough CV cycle, posting implied EBITDA margins of ~7%, easily the best in industry

RE – Are we seeing first signs of a customer shift in India 2-W industry? Royal Enfield (RE), the world’s oldest active motorcycle brand, with its uniquely classical and powerful bikes, always had cult status among bike lovers. However, in the recent past, the new India’s emerging higher middle class have taken it to few comparables. Our analysis from a demographic perspective highlights that as we move into the next decade bulk of the young population i.e. (>15<30 years - Gen Z) would have been born 90s & beyond, thereby having vastly different purchase habits and priorities (e.g. mileage/affordability vs. brand perception/comfort to their fathers (born <1980’s- Gen Y). We believe as the share of leisure bikes is still at a measly ~2% currently, as RE launches new products it will continue to grab more mind space among the young of India (already reflective in increasing first time buyers), thereby leading to sustained outperformance from RE. This when coupled with ~25% EBITDA margins shows Royal Enfield is a shining gem of the Indian 2-W industry. VECV has best business profile among CV manufacturers! In our view, on the business/financial front, the VECV JV boasts of the best business model among its peers, reflected in the fact that even in the worst CV cycle seen by the industry, VECV’s margins have stayed in the positive territory throughout the weak demand scenario, declining to 5.3% in Q4FY13 vis-à-vis incumbents Tata Motors and Ashok Leyland whose operating margins slipped in the red. VECV has already managed to increase its market share in the M&HCV segment to ~12% in FY14 from ~8% in FY09. With the new launches of the “Pro-series” trucks, we believe as the market expands in coming years VECV would gain market share in the higher tonnage space, maintain dominance in the ICV space. RE in strong growth phase; valuations set to trace HOG’s historical path With unrelenting demand likely to render expanded capacity inadequate in coming two years, RE is likely to double capacity beyond the ~600,000 unit capacity post CY16E. With demand remaining high, high waiting periods reflecting customer loyalty and association, we believe RE is set to trace a similar path to Harley-Davidson’s (HOG) high growth phase (1998-2003). During this period, where topline, bottomline grew ~2.5x, ~3.5x, respectively, with EBITDA margins expanding from ~19% to ~27% and RoEs improving from 23% to 29%, HOG’s average valuations were ~30x on a forward basis. We believe with similar financials for RE, its valuations may also trace a similar premium path akin to HOG. Uncontested business, margins in new orbit = multiples re-rating EML has justifiably commanded a premium over other auto OEs as RE’s business is in full throttle and VECV reaps benefits of economic revival. We maintain peer valuation parameters (relative valuation vis-à-vis HOG’s high growth phase) and ascribe a higher multiple of 30xCY16E EPS for RE (PEG 0.4x CAGR CY14-16E), VECV at 14x CY16E EV/EBITDA, respectively, to arrive at an SOTP target price of | 18800. We upgrade the stock to BUY with an upside potential of ~12%.

Rating matrix Rating : BuyTarget : | 18799Target Period : 12 monthsPotential Upside : 12%

What’s Changed?

Target Changed from | 15000 to | 18799EPS CY15E Changed from | 443.9 to | 393.8EPS CY15E Changed from | 682.2 to | 703.9Rating Unchanged

Quarterly Performance

Q4CY14 Q4CY13 YoY (%) Q3CY14 QoQ (%)Revenue 2,293.8 1,679.5 36.6 2,275.0 0.8EBITDA 303.1 166.6 82.0 305.3 -0.7EBITDA (%) 13.2 9.9 330 bps 13.4 -21 bpsPAT 153.8 96.2 59.8 165.0 -6.8

Key Financials | Crore CY13 CY14E CY15E CY16ENet Sales 6,685 8,599 11,786 16,561 EBITDA 713 1,115 1,766 2,992 Net Profit 394 616 1,064 1,901 EPS (|) 145.9 228.0 393.8 703.9

Valuation summary

CY13 CY14E CY15E CY16EP/E (x) 115.1 73.7 42.7 23.9 Adj. EV/E (x) 137.0 94.5 54.0 34.0 Tgt.Adj.EV/E(x) 122.2 84.3 48.2 30.3 P/BV (x) 22.1 17.8 13.2 8.8 RoNW (%) 19.2 24.2 30.8 36.8 RoCE (%) 18.3 23.9 31.0 38.6

Stock data Particular AmountMarket Capitalization | 45376.8 CroreTotal Debt (CY13) | 83.9 CroreCash and Investments (CY13) | 682.6 CroreEV (CY13) | 44778.2 Crore52 week H/L (|) 16937 / 4805Equity capital (| crore) | 27 CroreFace value (|) | 10

Price performance (%)

1M 3M 6M 12M

Eicher Motors Ltd 9.9 23.3 57.0 237.6

Tata Motors Ltd 8.9 7.4 19.4 50.4

M&M Ltd -4.5 -5.0 -9.4 31.6

Eicher Motors (EICMOT) | 16937

Research Analyst

Nishant Vass

ICICI Securities Ltd | Retail Equity Research Page 2

Variance analysis Q4CY14 Q4CY14E Q4CY13 YoY (%) Q3CY14 QoQ (%) Comments

Total Operating Income 2,294 2,184 1,680 36.6 2,275 0.8 Beat on the back of better realisations in VECVRaw Material Expenses 1,210 1,191 891 35.8 1,218 -0.7Purchase of traded goods 283 259 223 27.0 276 2.5Employee Expenses 167 152 142 17.9 169 -1.3 Higher payouts and bonuses coupled with new hiring lead to increase in payouts

Other expenses 330 281 257 28.4 306 8.0 Higher-than-expected other expenses have been due to front loading of expenses related to new products and techologies

EBITDA 303 301 167 82.0 305 -0.7EBITDA Margin (%) 13.2 13.8 9.9 330 bps 13.4 -21 bpsOther Income 15 36 15 3.8 19 -21.5 Lower-than-expected other income more of a timing issueDepreciation 60 35 39 52.4 56 6.5 Higher-than-expected depreciation due to change in accounting standard

requirementsInterest 2 3 4 -48.1 1 112.0Total Tax 75 73 17 349.2 81 -7.3PAT before MI 181 0 121 49.3 186 -2.7Minority Interest 27 32 25 9.1 21 29.5PAT 154 213 96 59.8 165 -6.8Key MetricsRoyal Enfield ASP(|) 109,298 108,660 107,573 1.6 108,660 0.6VECV ASP (| lakhs) 14.4 13.9 13.8 3.9 14.0 2.9 Source: Company, ICICIdirect.com Research Change in estimates

(| Crore) Old New % Change Old New % Change CommentsRevenue 12,078 11,995 -0.7 16645 16,847 1.2 Increase in estimates owing to increase in estimates for RE and VECVEBITDA 1,952 1,766 -9.5 2955 2,992 1.3EBITDA Margin (%) 16.2 14.7 -144 bps 17.8 17.8 1 bps Cut in margins in CY15E is only because of front loading of expenses on account of new products and

R&D that the company intends to do

PAT 1,199 1,064 -11.3 1843 1,901 3.2EPS (|) 444 394 -11.3 682 704 3.2

CY15E CY16E

Source: Company, ICICIdirect.com Research Assumptions

Current Earlier CommentsCY13 CY14E CY15E CY16E CY15E CY16E

Royal Enfield volumes 177646 302601 433617.3 588206.2 424776 588788Royal Enfield ASP/unit (|) 107,257 109,177 111,743 116,326 110,789 114,168 Better ASPs on the back of a better product mix, new launches in CY15E, CY6EVECV volumes 41,421 40,978 51,097 63,140 51,782 63,822VECV ASP/unit (| lakh) 12.6 13.5 13.9 15.1 14.1 15.2

Source: Company, ICICIdirect.com Research CY14E is for twelve months ending Dec’14

ICICI Securities Ltd | Retail Equity Research Page 3

Company Analysis Our demographic analysis reveals that in the coming decade (2021) we could witness the share of the 15-40 years age population declining to 60% from 64% of total driveable population (>15<70 years). We observe that the first generation Splendor (Launched 1994) driving population (15>) would have been born <1980s. The same generation in 2014 would be aged ~ 34+ highlighting that as we move into 2021 the same class of buyers would be >42+. We assume that a bulk of 2-W drivers would be young (15-40 years). We, thus, interpret the fact that as we move into the next decade bulk of the young population i.e. (>15<30 years- Gen Z) would have been born in 90s and beyond, thereby having vastly different purchase habits and priorities (e.g. mileage/affordability vs. brand perception/comfort to their fathers (born <1980’s- Gen Y). Royal Enfield (RE), the world’s oldest active motorcycle brand, with its uniquely classical and powerful bikes, was always a cult among bike lovers. However, in the recent past, the new India emerging higher middle class have taken to it with few comparables. Exhibit 1: Young India to be big buyer class in next decade

30 24 20

2728

27

1415

15

18 21 22

5 5 6

5 7 9

0%

20%

40%

60%

80%

100%

2011 2016 20210 year> 15 year> 30 year> 40 year> 60 year> 70 year>

Source: Company, CIA World Fact book, ICICIdirect.com Research Assumed 1.25% CAGR population growth

Exhibit 2: Shift in popular products preferences between Gen Y to Gen Z

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 4

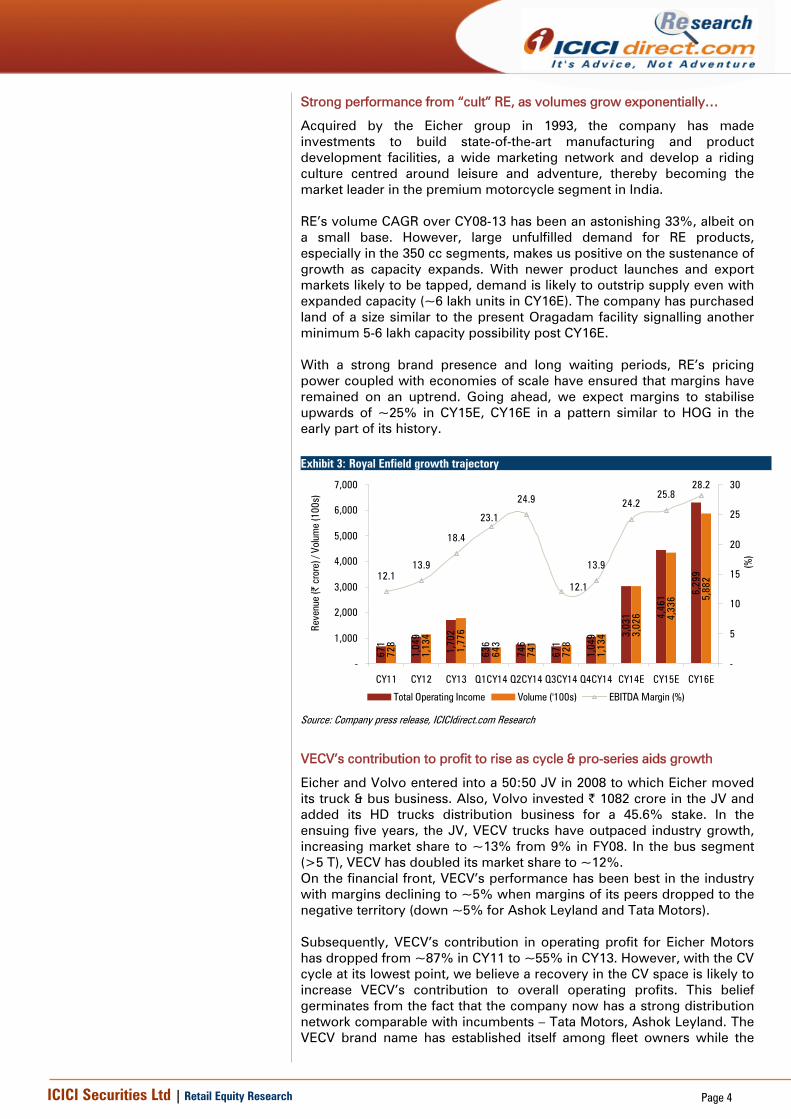

Strong performance from “cult” RE, as volumes grow exponentially…

Acquired by the Eicher group in 1993, the company has made investments to build state-of-the-art manufacturing and product development facilities, a wide marketing network and develop a riding culture centred around leisure and adventure, thereby becoming the market leader in the premium motorcycle segment in India. RE’s volume CAGR over CY08-13 has been an astonishing 33%, albeit on a small base. However, large unfulfilled demand for RE products, especially in the 350 cc segments, makes us positive on the sustenance of growth as capacity expands. With newer product launches and export markets likely to be tapped, demand is likely to outstrip supply even with expanded capacity (~6 lakh units in CY16E). The company has purchased land of a size similar to the present Oragadam facility signalling another minimum 5-6 lakh capacity possibility post CY16E. With a strong brand presence and long waiting periods, RE’s pricing power coupled with economies of scale have ensured that margins have remained on an uptrend. Going ahead, we expect margins to stabilise upwards of ~25% in CY15E, CY16E in a pattern similar to HOG in the early part of its history.

VECV’s contribution to profit to rise as cycle & pro-series aids growth

Eicher and Volvo entered into a 50:50 JV in 2008 to which Eicher moved its truck & bus business. Also, Volvo invested | 1082 crore in the JV and added its HD trucks distribution business for a 45.6% stake. In the ensuing five years, the JV, VECV trucks have outpaced industry growth, increasing market share to ~13% from 9% in FY08. In the bus segment (>5 T), VECV has doubled its market share to ~12%. On the financial front, VECV’s performance has been best in the industry with margins declining to ~5% when margins of its peers dropped to the negative territory (down ~5% for Ashok Leyland and Tata Motors). Subsequently, VECV’s contribution in operating profit for Eicher Motors has dropped from ~87% in CY11 to ~55% in CY13. However, with the CV cycle at its lowest point, we believe a recovery in the CV space is likely to increase VECV’s contribution to overall operating profits. This belief germinates from the fact that the company now has a strong distribution network comparable with incumbents – Tata Motors, Ashok Leyland. The VECV brand name has established itself among fleet owners while the

Exhibit 3: Royal Enfield growth trajectory

671

1,04

9

1,70

2

746

671

1,04

9 3,03

1 4,46

1 6,29

9

728

1,13

4

1,77

6

741

728

1,13

4 3,02

6 4,33

6 5,88

2

636

643

12.113.9

18.4

24.9

13.9

24.225.8

28.2

12.1

23.1

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

CY11 CY12 CY13 Q1CY14 Q2CY14 Q3CY14 Q4CY14 CY14E CY15E CY16E

Reve

nue

(| c

rore

) / V

olum

e (1

00s)

-

5

10

15

20

25

30

(%)

Total Operating Income Volume ('100s) EBITDA Margin (%)

Source: Company press release, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 5

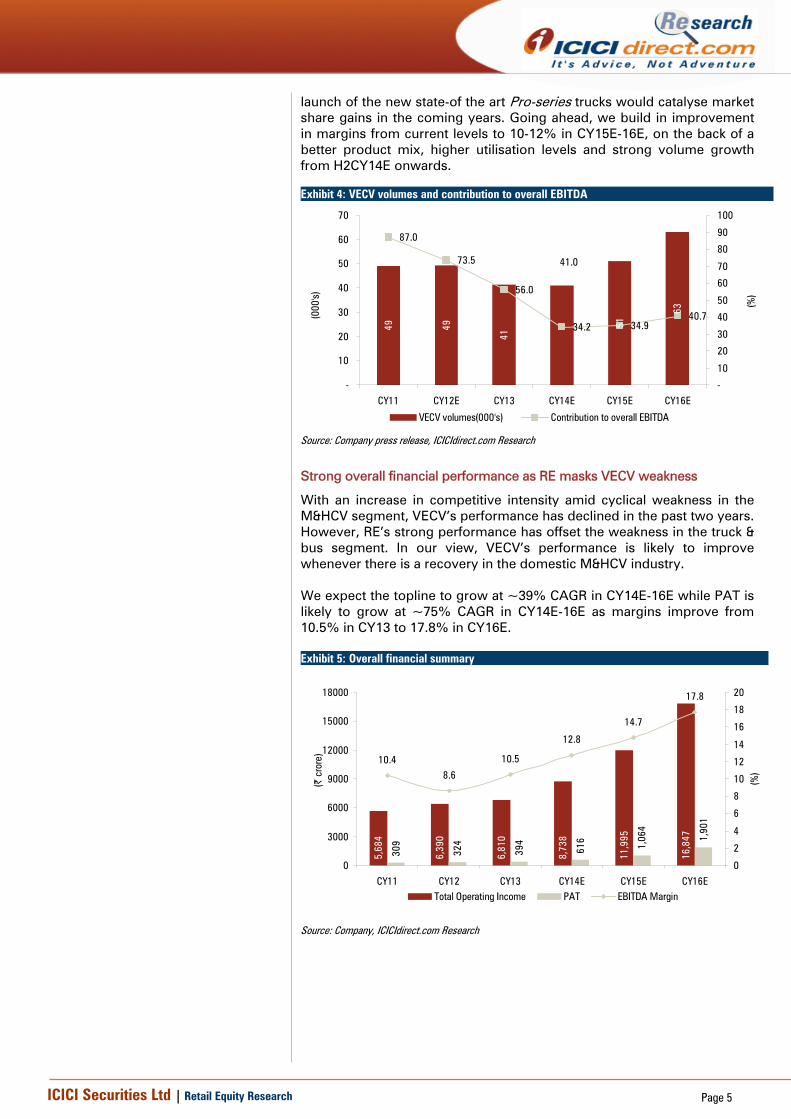

launch of the new state-of the art Pro-series trucks would catalyse market share gains in the coming years. Going ahead, we build in improvement in margins from current levels to 10-12% in CY15E-16E, on the back of a better product mix, higher utilisation levels and strong volume growth from H2CY14E onwards.

Strong overall financial performance as RE masks VECV weakness

With an increase in competitive intensity amid cyclical weakness in the M&HCV segment, VECV’s performance has declined in the past two years. However, RE’s strong performance has offset the weakness in the truck & bus segment. In our view, VECV’s performance is likely to improve whenever there is a recovery in the domestic M&HCV industry. We expect the topline to grow at ~39% CAGR in CY14E-16E while PAT is likely to grow at ~75% CAGR in CY14E-16E as margins improve from 10.5% in CY13 to 17.8% in CY16E. Exhibit 5: Overall financial summary

5,68

4

6,39

0

6,81

0

8,73

8

11,9

95

16,8

47

309

324

394

616 1,06

4

1,90

1

10.48.6

10.5

12.8

14.7

17.8

0

3000

6000

9000

12000

15000

18000

CY11 CY12 CY13 CY14E CY15E CY16E

(| c

rore

)

0

2

4

6

8

10

12

14

16

18

20

(%)

Total Operating Income PAT EBITDA Margin

Source: Company, ICICIdirect.com Research

Exhibit 4: VECV volumes and contribution to overall EBITDA

49 49

41

51

63

41.0

87.0

73.5

56.0

34.2 34.940.7

-

10

20

30

40

50

60

70

CY11 CY12E CY13 CY14E CY15E CY16E

(000

's)

-

10

20

30

40

50

60

70

80

90

100

(%)

VECV volumes(000's) Contribution to overall EBITDA

Source: Company press release, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 6

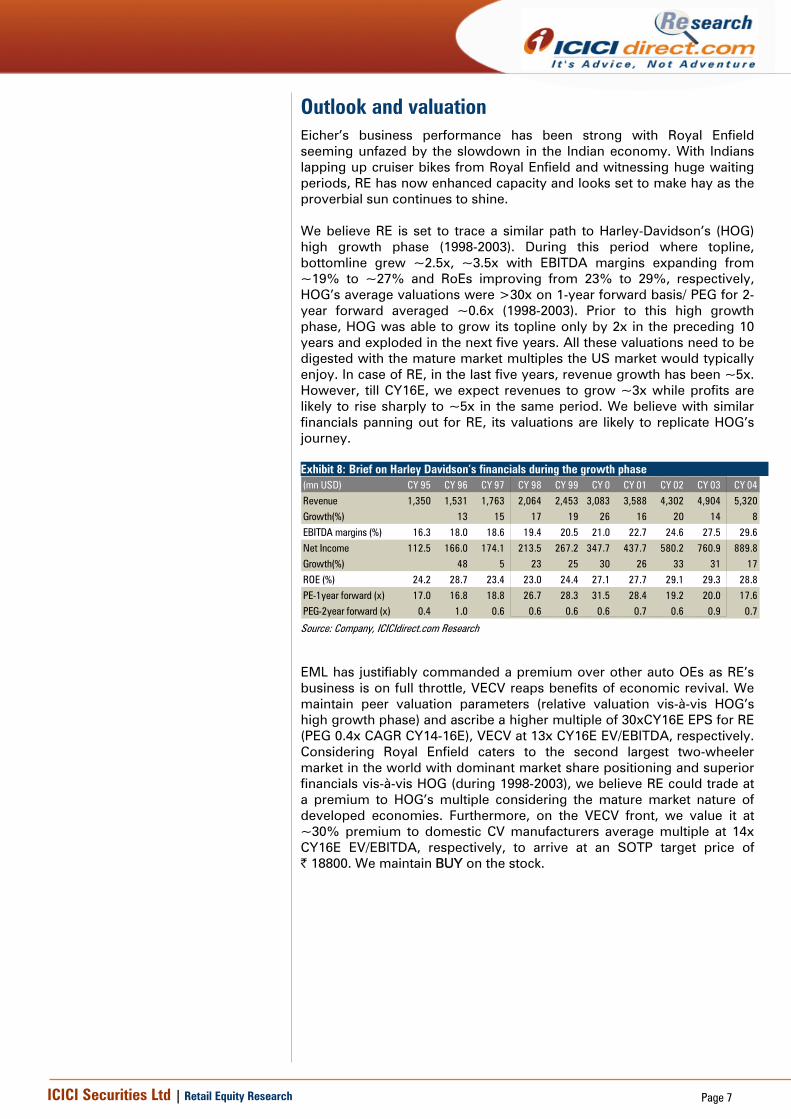

Return ratios remain on uptrend margins/profitability improves

With Royal Enfield’s strong franchisee driving profitability, the overall business has been able to maintain decent return ratios despite the weakness in the VECV side of the business, which has seen a sharp drop in capacity utilisation levels. Going ahead, as RE volumes ramp up in the new facility, coupled with better performance from VECV on revival in industrial activity levels, return ratios are likely to remain on the uptrend.

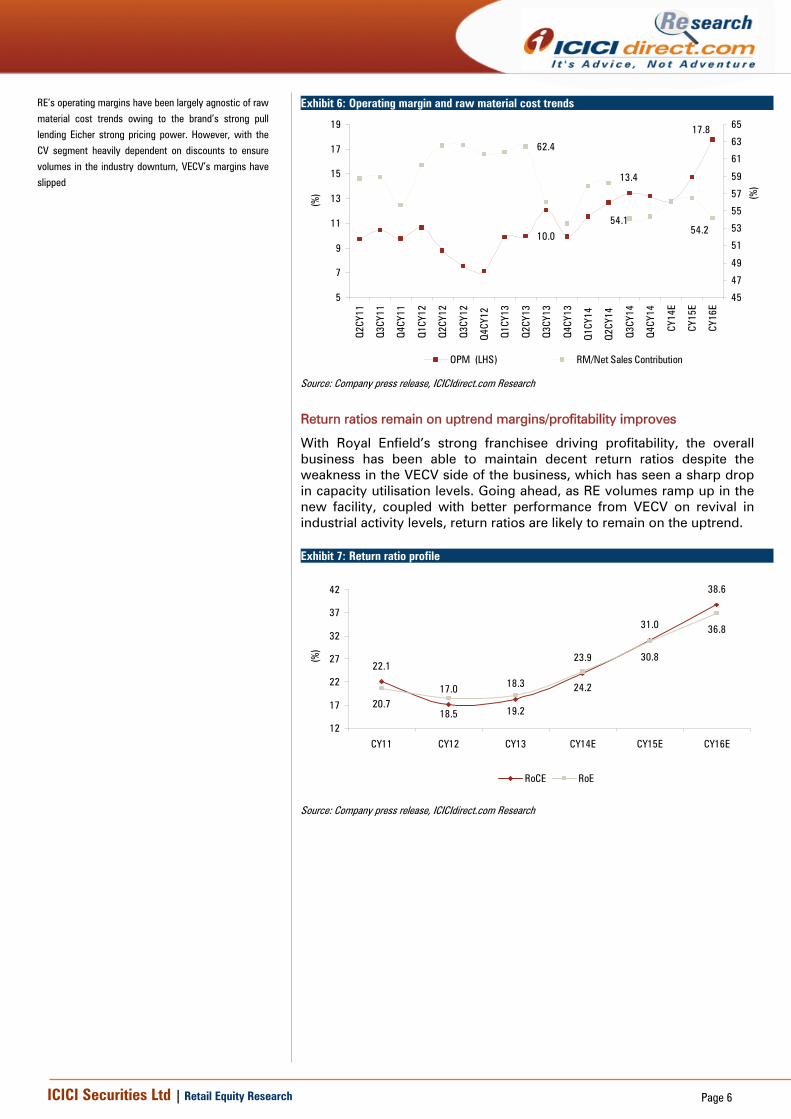

RE’s operating margins have been largely agnostic of raw

material cost trends owing to the brand’s strong pull

lending Eicher strong pricing power. However, with the

CV segment heavily dependent on discounts to ensure

volumes in the industry downturn, VECV’s margins have

slipped

Exhibit 6: Operating margin and raw material cost trends

13.4

10.0

17.8

54.1

62.4

54.2

5

7

9

11

13

15

17

19

Q2CY

11

Q3CY

11

Q4CY

11

Q1CY

12

Q2CY

12

Q3CY

12

Q4CY

12

Q1CY

13

Q2CY

13

Q3CY

13

Q4CY

13

Q1CY

14

Q2CY

14

Q3CY

14

Q4CY

14

CY14

E

CY15

E

CY16

E

(%)

45

47

49

51

53

55

57

59

61

63

65

(%)

OPM (LHS) RM/Net Sales Contribution

Source: Company press release, ICICIdirect.com Research

Exhibit 7: Return ratio profile

22.1

20.7

38.6

31.0

23.9

18.317.0

18.5 19.2

24.2

30.8

36.8

12

17

22

27

32

37

42

CY11 CY12 CY13 CY14E CY15E CY16E

(%)

RoCE RoE

Source: Company press release, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 7

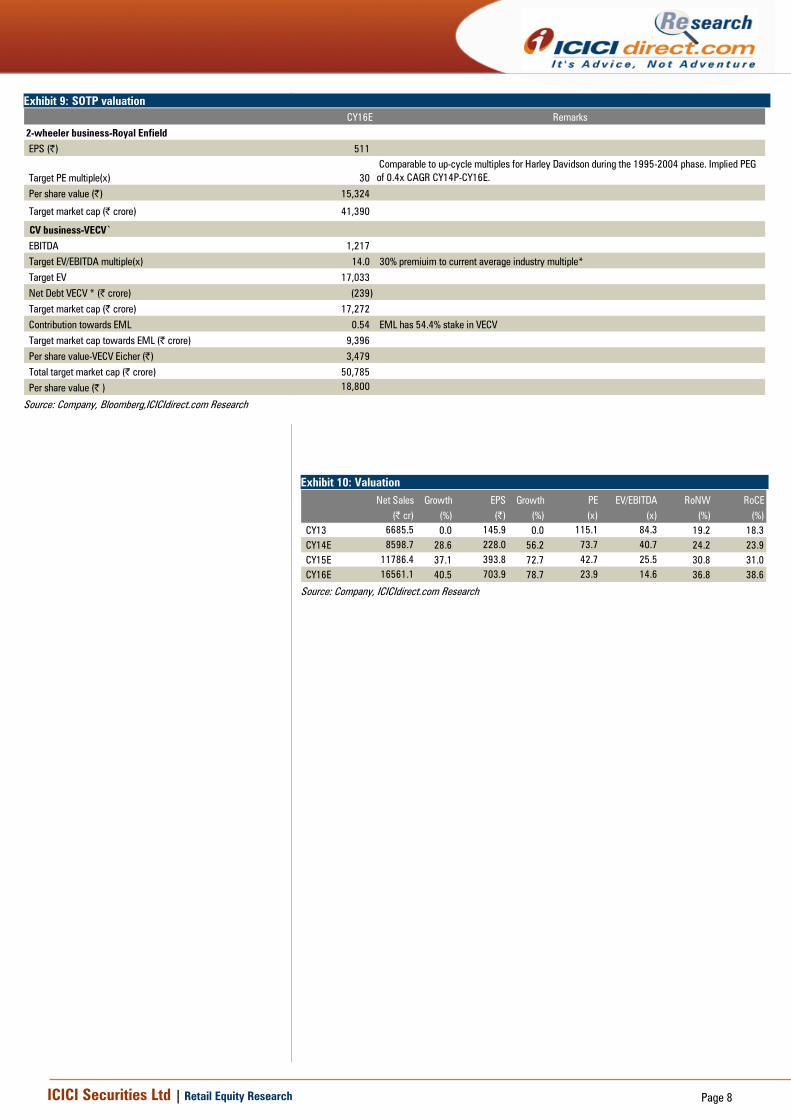

Outlook and valuation Eicher’s business performance has been strong with Royal Enfield seeming unfazed by the slowdown in the Indian economy. With Indians lapping up cruiser bikes from Royal Enfield and witnessing huge waiting periods, RE has now enhanced capacity and looks set to make hay as the proverbial sun continues to shine. We believe RE is set to trace a similar path to Harley-Davidson’s (HOG) high growth phase (1998-2003). During this period where topline, bottomline grew ~2.5x, ~3.5x with EBITDA margins expanding from ~19% to ~27% and RoEs improving from 23% to 29%, respectively, HOG’s average valuations were >30x on 1-year forward basis/ PEG for 2-year forward averaged ~0.6x (1998-2003). Prior to this high growth phase, HOG was able to grow its topline only by 2x in the preceding 10 years and exploded in the next five years. All these valuations need to be digested with the mature market multiples the US market would typically enjoy. In case of RE, in the last five years, revenue growth has been ~5x. However, till CY16E, we expect revenues to grow ~3x while profits are likely to rise sharply to ~5x in the same period. We believe with similar financials panning out for RE, its valuations are likely to replicate HOG’s journey. Exhibit 8: Brief on Harley Davidson’s financials during the growth phase (mn USD) CY 95 CY 96 CY 97 CY 98 CY 99 CY 0 CY 01 CY 02 CY 03 CY 04

Revenue 1,350 1,531 1,763 2,064 2,453 3,083 3,588 4,302 4,904 5,320Growth(%) 13 15 17 19 26 16 20 14 8

EBITDA margins (%) 16.3 18.0 18.6 19.4 20.5 21.0 22.7 24.6 27.5 29.6

Net Income 112.5 166.0 174.1 213.5 267.2 347.7 437.7 580.2 760.9 889.8Growth(%) 48 5 23 25 30 26 33 31 17

ROE (%) 24.2 28.7 23.4 23.0 24.4 27.1 27.7 29.1 29.3 28.8

PE-1year forward (x) 17.0 16.8 18.8 26.7 28.3 31.5 28.4 19.2 20.0 17.6PEG-2year forward (x) 0.4 1.0 0.6 0.6 0.6 0.6 0.7 0.6 0.9 0.7 Source: Company, ICICIdirect.com Research

EML has justifiably commanded a premium over other auto OEs as RE’s business is on full throttle, VECV reaps benefits of economic revival. We maintain peer valuation parameters (relative valuation vis-à-vis HOG’s high growth phase) and ascribe a higher multiple of 30xCY16E EPS for RE (PEG 0.4x CAGR CY14-16E), VECV at 13x CY16E EV/EBITDA, respectively. Considering Royal Enfield caters to the second largest two-wheeler market in the world with dominant market share positioning and superior financials vis-à-vis HOG (during 1998-2003), we believe RE could trade at a premium to HOG’s multiple considering the mature market nature of developed economies. Furthermore, on the VECV front, we value it at ~30% premium to domestic CV manufacturers average multiple at 14x CY16E EV/EBITDA, respectively, to arrive at an SOTP target price of | 18800. We maintain BUY on the stock.

ICICI Securities Ltd | Retail Equity Research Page 8

Exhibit 9: SOTP valuation CY16E Remarks

2-wheeler business-Royal EnfieldEPS (|) 511

Target PE multiple(x) 30 Comparable to up-cycle multiples for Harley Davidson during the 1995-2004 phase. Implied PEG of 0.4x CAGR CY14P-CY16E.

Per share value (|) 15,324

Target market cap (| crore) 41,390

CV business-VECV`

EBITDA 1,217 Target EV/EBITDA multiple(x) 14.0 30% premiuim to current average industry multiple*

Target EV 17,033

Net Debt VECV * (| crore) (239)

Target market cap (| crore) 17,272 Contribution towards EML 0.54 EML has 54.4% stake in VECV

Target market cap towards EML (| crore) 9,396

Per share value-VECV Eicher (|) 3,479 Total target market cap (| crore) 50,785

Per share value (| ) 18,800 Source: Company, Bloomberg,ICICIdirect.com Research

Exhibit 10: Valuation

Net Sales Growth EPS Growth PE EV/EBITDA RoNW RoCE (| cr) (%) (|) (%) (x) (x) (%) (%)

CY13 6685.5 0.0 145.9 0.0 115.1 84.3 19.2 18.3CY14E 8598.7 28.6 228.0 56.2 73.7 40.7 24.2 23.9CY15E 11786.4 37.1 393.8 72.7 42.7 25.5 30.8 31.0CY16E 16561.1 40.5 703.9 78.7 23.9 14.6 36.8 38.6

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 9

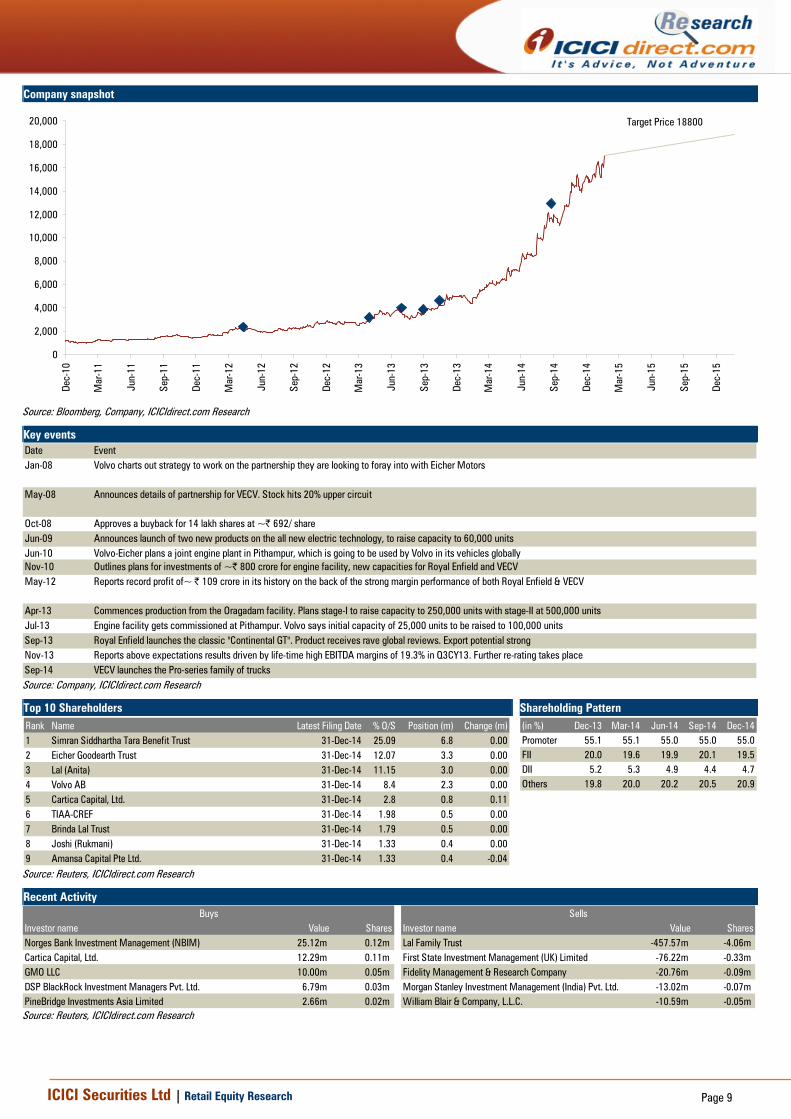

Company snapshot

Target Price 18800

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Dec-

10

Mar

-11

Jun-

11

Sep-

11

Dec-

11

Mar

-12

Jun-

12

Sep-

12

Dec-

12

Mar

-13

Jun-

13

Sep-

13

Dec-

13

Mar

-14

Jun-

14

Sep-

14

Dec-

14

Mar

-15

Jun-

15

Sep-

15

Dec-

15

Source: Bloomberg, Company, ICICIdirect.com Research

Key events Date EventJan-08 Volvo charts out strategy to work on the partnership they are looking to foray into with Eicher Motors

May-08 Announces details of partnership for VECV. Stock hits 20% upper circuit

Oct-08 Approves a buyback for 14 lakh shares at ~| 692/ shareJun-09 Announces launch of two new products on the all new electric technology, to raise capacity to 60,000 unitsJun-10 Volvo-Eicher plans a joint engine plant in Pithampur, which is going to be used by Volvo in its vehicles globallyNov-10 Outlines plans for investments of ~| 800 crore for engine facility, new capacities for Royal Enfield and VECVMay-12 Reports record profit of~ | 109 crore in its history on the back of the strong margin performance of both Royal Enfield & VECV

Apr-13 Commences production from the Oragadam facility. Plans stage-I to raise capacity to 250,000 units with stage-II at 500,000 unitsJul-13 Engine facility gets commissioned at Pithampur. Volvo says initial capacity of 25,000 units to be raised to 100,000 unitsSep-13 Royal Enfield launches the classic "Continental GT". Product receives rave global reviews. Export potential strongNov-13 Reports above expectations results driven by life-time high EBITDA margins of 19.3% in Q3CY13. Further re-rating takes placeSep-14 VECV launches the Pro-series family of trucks Source: Company, ICICIdirect.com Research

Top 10 Shareholders Shareholding Pattern Rank Name Latest Filing Date % O/S Position (m) Change (m)1 Simran Siddhartha Tara Benefit Trust 31-Dec-14 25.09 6.8 0.002 Eicher Goodearth Trust 31-Dec-14 12.07 3.3 0.003 Lal (Anita) 31-Dec-14 11.15 3.0 0.004 Volvo AB 31-Dec-14 8.4 2.3 0.005 Cartica Capital, Ltd. 31-Dec-14 2.8 0.8 0.116 TIAA-CREF 31-Dec-14 1.98 0.5 0.007 Brinda Lal Trust 31-Dec-14 1.79 0.5 0.008 Joshi (Rukmani) 31-Dec-14 1.33 0.4 0.009 Amansa Capital Pte Ltd. 31-Dec-14 1.33 0.4 -0.04

(in %) Dec-13 Mar-14 Jun-14 Sep-14 Dec-14Promoter 55.1 55.1 55.0 55.0 55.0FII 20.0 19.6 19.9 20.1 19.5DII 5.2 5.3 4.9 4.4 4.7Others 19.8 20.0 20.2 20.5 20.9

Source: Reuters, ICICIdirect.com Research

Recent Activity

Investor name Value Shares Investor name Value SharesNorges Bank Investment Management (NBIM) 25.12m 0.12m Lal Family Trust -457.57m -4.06m Cartica Capital, Ltd. 12.29m 0.11m First State Investment Management (UK) Limited -76.22m -0.33m GMO LLC 10.00m 0.05m Fidelity Management & Research Company -20.76m -0.09m DSP BlackRock Investment Managers Pvt. Ltd. 6.79m 0.03m Morgan Stanley Investment Management (India) Pvt. Ltd. -13.02m -0.07m PineBridge Investments Asia Limited 2.66m 0.02m William Blair & Company, L.L.C. -10.59m -0.05m

Buys Sells

Source: Reuters, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 10

.

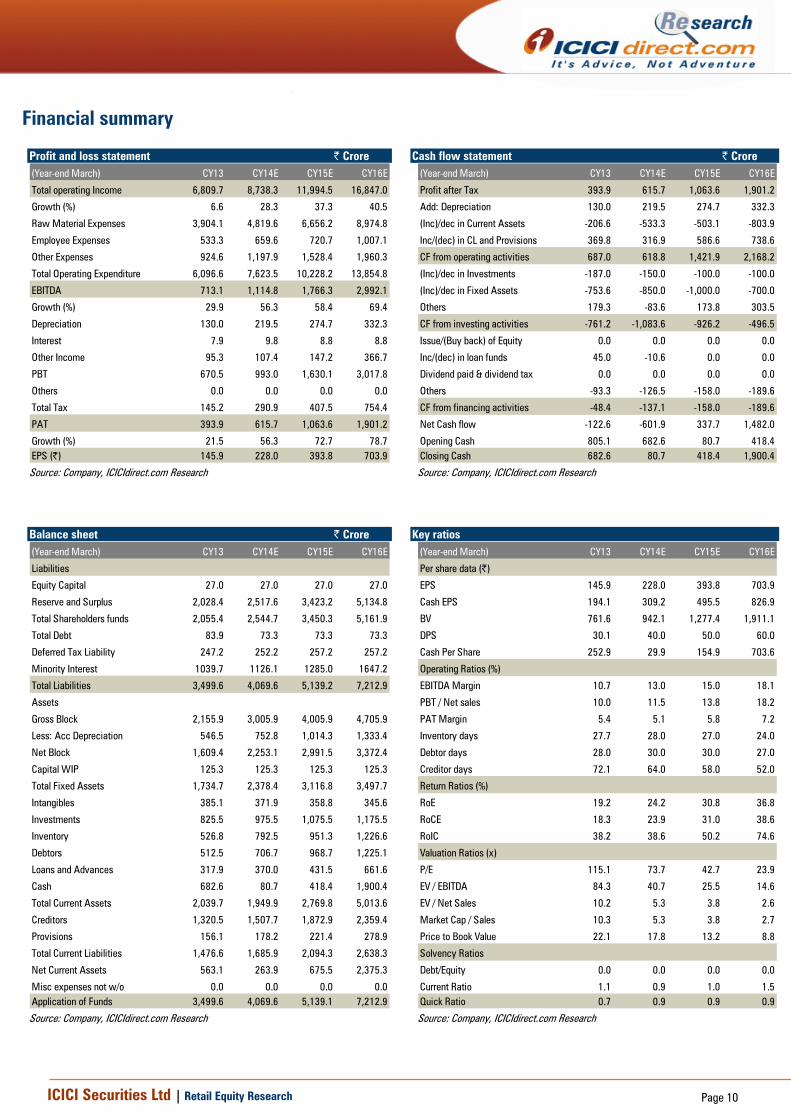

Financial summary

Profit and loss statement | Crore (Year-end March) CY13 CY14E CY15E CY16E

Total operating Income 6,809.7 8,738.3 11,994.5 16,847.0

Growth (%) 6.6 28.3 37.3 40.5

Raw Material Expenses 3,904.1 4,819.6 6,656.2 8,974.8

Employee Expenses 533.3 659.6 720.7 1,007.1

Other Expenses 924.6 1,197.9 1,528.4 1,960.3

Total Operating Expenditure 6,096.6 7,623.5 10,228.2 13,854.8

EBITDA 713.1 1,114.8 1,766.3 2,992.1

Growth (%) 29.9 56.3 58.4 69.4

Depreciation 130.0 219.5 274.7 332.3

Interest 7.9 9.8 8.8 8.8

Other Income 95.3 107.4 147.2 366.7

PBT 670.5 993.0 1,630.1 3,017.8

Others 0.0 0.0 0.0 0.0

Total Tax 145.2 290.9 407.5 754.4

PAT 393.9 615.7 1,063.6 1,901.2

Growth (%) 21.5 56.3 72.7 78.7EPS (|) 145.9 228.0 393.8 703.9 Source: Company, ICICIdirect.com Research

Cash flow statement | Crore (Year-end March) CY13 CY14E CY15E CY16E

Profit after Tax 393.9 615.7 1,063.6 1,901.2

Add: Depreciation 130.0 219.5 274.7 332.3

(Inc)/dec in Current Assets -206.6 -533.3 -503.1 -803.9

Inc/(dec) in CL and Provisions 369.8 316.9 586.6 738.6

CF from operating activities 687.0 618.8 1,421.9 2,168.2

(Inc)/dec in Investments -187.0 -150.0 -100.0 -100.0

(Inc)/dec in Fixed Assets -753.6 -850.0 -1,000.0 -700.0

Others 179.3 -83.6 173.8 303.5

CF from investing activities -761.2 -1,083.6 -926.2 -496.5

Issue/(Buy back) of Equity 0.0 0.0 0.0 0.0

Inc/(dec) in loan funds 45.0 -10.6 0.0 0.0

Dividend paid & dividend tax 0.0 0.0 0.0 0.0

Others -93.3 -126.5 -158.0 -189.6

CF from financing activities -48.4 -137.1 -158.0 -189.6

Net Cash flow -122.6 -601.9 337.7 1,482.0

Opening Cash 805.1 682.6 80.7 418.4Closing Cash 682.6 80.7 418.4 1,900.4 Source: Company, ICICIdirect.com Research

Balance sheet | Crore (Year-end March) CY13 CY14E CY15E CY16E

Liabilities

Equity Capital 27.0 27.0 27.0 27.0

Reserve and Surplus 2,028.4 2,517.6 3,423.2 5,134.8

Total Shareholders funds 2,055.4 2,544.7 3,450.3 5,161.9

Total Debt 83.9 73.3 73.3 73.3

Deferred Tax Liability 247.2 252.2 257.2 257.2

Minority Interest 1039.7 1126.1 1285.0 1647.2

Total Liabilities 3,499.6 4,069.6 5,139.2 7,212.9

Assets

Gross Block 2,155.9 3,005.9 4,005.9 4,705.9

Less: Acc Depreciation 546.5 752.8 1,014.3 1,333.4

Net Block 1,609.4 2,253.1 2,991.5 3,372.4

Capital WIP 125.3 125.3 125.3 125.3

Total Fixed Assets 1,734.7 2,378.4 3,116.8 3,497.7

Intangibles 385.1 371.9 358.8 345.6

Investments 825.5 975.5 1,075.5 1,175.5

Inventory 526.8 792.5 951.3 1,226.6

Debtors 512.5 706.7 968.7 1,225.1

Loans and Advances 317.9 370.0 431.5 661.6

Cash 682.6 80.7 418.4 1,900.4

Total Current Assets 2,039.7 1,949.9 2,769.8 5,013.6

Creditors 1,320.5 1,507.7 1,872.9 2,359.4

Provisions 156.1 178.2 221.4 278.9

Total Current Liabilities 1,476.6 1,685.9 2,094.3 2,638.3

Net Current Assets 563.1 263.9 675.5 2,375.3

Misc expenses not w/o 0.0 0.0 0.0 0.0Application of Funds 3,499.6 4,069.6 5,139.1 7,212.9 Source: Company, ICICIdirect.com Research

Key ratios (Year-end March) CY13 CY14E CY15E CY16E

Per share data (|)

EPS 145.9 228.0 393.8 703.9

Cash EPS 194.1 309.2 495.5 826.9

BV 761.6 942.1 1,277.4 1,911.1

DPS 30.1 40.0 50.0 60.0

Cash Per Share 252.9 29.9 154.9 703.6

Operating Ratios (%)

EBITDA Margin 10.7 13.0 15.0 18.1

PBT / Net sales 10.0 11.5 13.8 18.2

PAT Margin 5.4 5.1 5.8 7.2

Inventory days 27.7 28.0 27.0 24.0

Debtor days 28.0 30.0 30.0 27.0

Creditor days 72.1 64.0 58.0 52.0

Return Ratios (%)

RoE 19.2 24.2 30.8 36.8

RoCE 18.3 23.9 31.0 38.6

RoIC 38.2 38.6 50.2 74.6

Valuation Ratios (x)

P/E 115.1 73.7 42.7 23.9

EV / EBITDA 84.3 40.7 25.5 14.6

EV / Net Sales 10.2 5.3 3.8 2.6

Market Cap / Sales 10.3 5.3 3.8 2.7

Price to Book Value 22.1 17.8 13.2 8.8

Solvency Ratios

Debt/Equity 0.0 0.0 0.0 0.0

Current Ratio 1.1 0.9 1.0 1.5Quick Ratio 0.7 0.9 0.9 0.9 Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 11

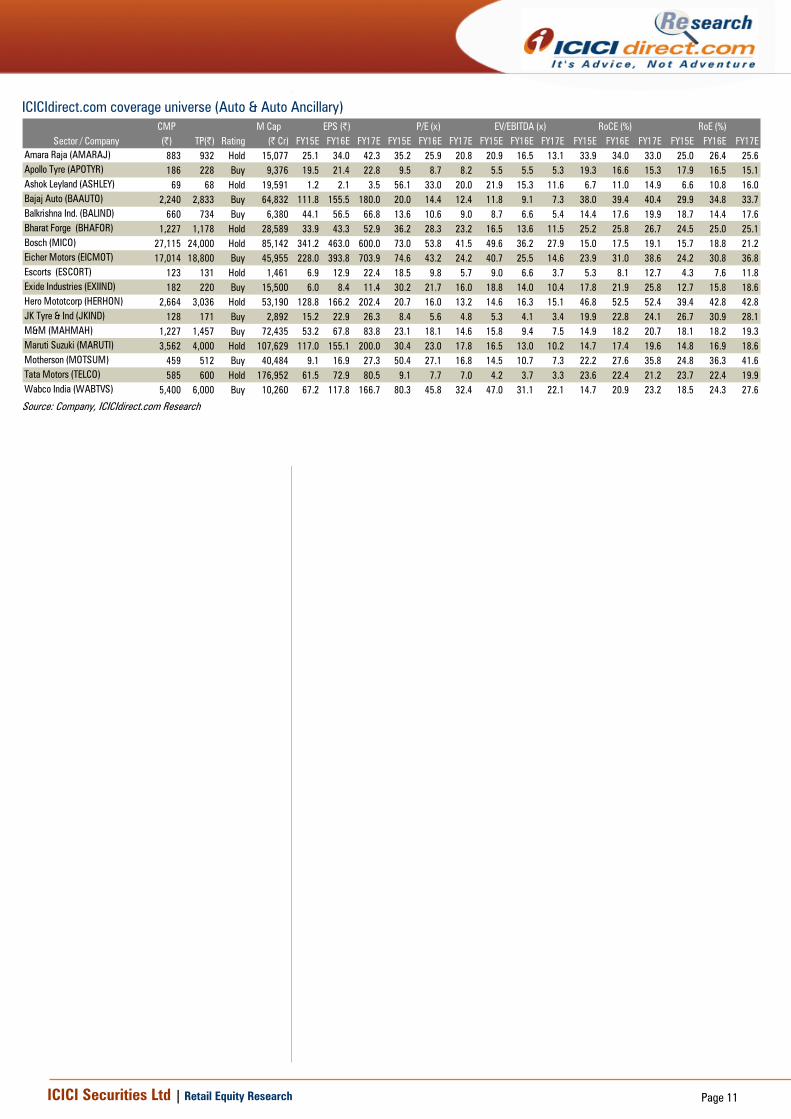

ICICIdirect.com coverage universe (Auto & Auto Ancillary) CMP M Cap(|) TP(|) Rating (| Cr) FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

Amara Raja (AMARAJ) 883 932 Hold 15,077 25.1 34.0 42.3 35.2 25.9 20.8 20.9 16.5 13.1 33.9 34.0 33.0 25.0 26.4 25.6Apollo Tyre (APOTYR) 186 228 Buy 9,376 19.5 21.4 22.8 9.5 8.7 8.2 5.5 5.5 5.3 19.3 16.6 15.3 17.9 16.5 15.1Ashok Leyland (ASHLEY) 69 68 Hold 19,591 1.2 2.1 3.5 56.1 33.0 20.0 21.9 15.3 11.6 6.7 11.0 14.9 6.6 10.8 16.0Bajaj Auto (BAAUTO) 2,240 2,833 Buy 64,832 111.8 155.5 180.0 20.0 14.4 12.4 11.8 9.1 7.3 38.0 39.4 40.4 29.9 34.8 33.7Balkrishna Ind. (BALIND) 660 734 Buy 6,380 44.1 56.5 66.8 13.6 10.6 9.0 8.7 6.6 5.4 14.4 17.6 19.9 18.7 14.4 17.6Bharat Forge (BHAFOR) 1,227 1,178 Hold 28,589 33.9 43.3 52.9 36.2 28.3 23.2 16.5 13.6 11.5 25.2 25.8 26.7 24.5 25.0 25.1Bosch (MICO) 27,115 24,000 Hold 85,142 341.2 463.0 600.0 73.0 53.8 41.5 49.6 36.2 27.9 15.0 17.5 19.1 15.7 18.8 21.2Eicher Motors (EICMOT) 17,014 18,800 Buy 45,955 228.0 393.8 703.9 74.6 43.2 24.2 40.7 25.5 14.6 23.9 31.0 38.6 24.2 30.8 36.8Escorts (ESCORT) 123 131 Hold 1,461 6.9 12.9 22.4 18.5 9.8 5.7 9.0 6.6 3.7 5.3 8.1 12.7 4.3 7.6 11.8Exide Industries (EXIIND) 182 220 Buy 15,500 6.0 8.4 11.4 30.2 21.7 16.0 18.8 14.0 10.4 17.8 21.9 25.8 12.7 15.8 18.6Hero Mototcorp (HERHON) 2,664 3,036 Hold 53,190 128.8 166.2 202.4 20.7 16.0 13.2 14.6 16.3 15.1 46.8 52.5 52.4 39.4 42.8 42.8JK Tyre & Ind (JKIND) 128 171 Buy 2,892 15.2 22.9 26.3 8.4 5.6 4.8 5.3 4.1 3.4 19.9 22.8 24.1 26.7 30.9 28.1M&M (MAHMAH) 1,227 1,457 Buy 72,435 53.2 67.8 83.8 23.1 18.1 14.6 15.8 9.4 7.5 14.9 18.2 20.7 18.1 18.2 19.3Maruti Suzuki (MARUTI) 3,562 4,000 Hold 107,629 117.0 155.1 200.0 30.4 23.0 17.8 16.5 13.0 10.2 14.7 17.4 19.6 14.8 16.9 18.6Motherson (MOTSUM) 459 512 Buy 40,484 9.1 16.9 27.3 50.4 27.1 16.8 14.5 10.7 7.3 22.2 27.6 35.8 24.8 36.3 41.6Tata Motors (TELCO) 585 600 Hold 176,952 61.5 72.9 80.5 9.1 7.7 7.0 4.2 3.7 3.3 23.6 22.4 21.2 23.7 22.4 19.9Wabco India (WABTVS) 5,400 6,000 Buy 10,260 67.2 117.8 166.7 80.3 45.8 32.4 47.0 31.1 22.1 14.7 20.9 23.2 18.5 24.3 27.6

Sector / CompanyRoE (%)EPS (|) P/E (x) EV/EBITDA (x) RoCE (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 12

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction; Buy: >10%/15% for large caps/midcaps, respectively; Hold: Up to +/-10%; Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk, ICICI Securities Limited, 1st Floor, Akruti Trade Centre, Road No 7, MIDC, Andheri (East) Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 13

ANALYST CERTIFICATION We /I, Nishant Vass, MBA (Finance) Research Analyst, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures: ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com. ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances. This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction. ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months. ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any material conflict of interest at the time of publication of this report. It is confirmed that Nishant Vass, MBA, Research Analyst of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Compensation of our Research Analyst is not based on any specific merchant banking, investment banking or brokerage service transactions. ICICI Securities or its subsidiaries collectively or Research Analysts do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report. Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. It is confirmed that Nishant Vass, MBA, Research Analyst do not serve as an officer, director or employee of the companies mentioned in the report. ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Neither the Research Analyst nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report. We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.