egyptian natural gas industry development- final - unece · cairo alexandria n. alamein ... natural...

TRANSCRIPT

Egyptian Natural Gas Industry Development

By Dr. Hamed Korkor

Chairman Assistant

Egyptian Natural Gas Holding Company EGAS

United Nations – Economic Commission for Europe

Working Party on Gas 17th annual Meeting

Geneva, Switzerland

January 23-24, 2007

Early Gas Discoveries: Early Gas Discoveries: 19671967

First Gas Production:First Gas Production: 19751975

Egyptian Natural Gas Industry History

Natural Gas Share of HydrocarbonsNatural Gas Share of HydrocarbonsEnergy Production (2005/2006)Energy Production (2005/2006)

Natural Gas

54%Oil

46 %

Total = 71 Million Tons

.

0 100 km

UMBARKAKHALDAKHALDA

QANTARA

ELQANTARAELQANTARAEL MANSOURA

MERLONMERLON

MANZALACENTURIONCENTURIONEL WASTANI

N BARDAWIL

IEOCIEOCRAS ELBARR

bpbp.

W. MEDITERRANEAN

bp BALTIM NEMED GASMED GAS DENISESETH

HA'PY

AKIK

TUNA

TEMSAHPETROTTEMSAHPETROTTEMSAHTAO

SET I- PLIO

28°00E 32°00E

32°00N

26°00E 34°00E30°00E

BALTIM N

GIZA

CAIRO

ALEXANDRIA

N. ALAMEINNALPETCONALPETCO

N.E. MED DEEPWATER

SHELLSHELL

TAREKKHALDAKHALDA

KHALDA OFFSETAPACHEAPACHE

KHALDA/ KHALDA WEST / SALLAMKHALDAKHALDA

OBAIYEDBAPETCOBAPETCO

MELIHAAGIBAAGIBA

MATRUHAPACHEAPACHE

KHALDAKHALDAKHALDA

SIDI KRIER

WEST MEDITERRANEANAPACHEAPACHE

EL HAMRA

RAS KANAYESAPACHEAPACHE

RAS EL HEKMAAPACHEAPACHE

W.MEDAPACHEAPACHE

N.ABU QIRA /QIR/A QIR WEGPCEGPC

RestrictedArea

N.ALEXbpbp

N.ALEXbp

ABU MADIEGPCEGPC

ABU MADI WNIDOCONIDOCOEL QARAANIDOCONIDOCO

BALTIM EMED GAS

EDDMIEOCIEOC

RESTRICTED

NWDEMIATTASHELLSHELL

CENTURION

MERLON / EL QANTARA

APACHE / KHALDA

Bp/ GUPCO

BG / RASHPETCO

EGPC

GEOGE

IEOC / PETROBEL / AGIBA

SHELL / BAPETCO

OPEN AREA

BALTIM SMED GASMED GAS

KHEPRI/SETHOS KHALDAKHALDA

MATRUHON/OFFSHORE

SHELLSHELL

WDDMBG

KAROUS

KALABSHA KHALDAKHALDA

ROSETTA BG

N.IDKUGEOGE

BALTIM E

P. FOUADPETROBELPETROBEL

MEDITERRANEAN MEDITERRANEAN SEASEA

AREAKAMOSE

IEOC

Up

Stre

am A

ctiv

ities

(Agr

eem

ents

)

Western Desert11%

Gulf of Suez8%

Delta3%

Mediterranean78%

Up

Stre

am A

ctiv

ities

(Res

erve

s)

4852

5862 65 67 68.2

0

10

20

30

40

50

60

70

80

99/00 00/01 01/02 02/03 03/04 04/05 June 2006

TCF

Natural Gas Proven Reserves Development

Natural Gas Industry Main Indicators(November 2006)

•• Gas ProductionGas Production 5.6 BCF/D5.6 BCF/D

•• Gas SalesGas Sales 5.1 BCF/D 5.1 BCF/D

•• LPG ProductionLPG Production 2.6 K Ton/D2.6 K Ton/D

•• Propane ProductionPropane Production 0.6 K Ton/D0.6 K Ton/D

•• CC22/C/C33 mix mix Production Production 1.4 K Ton/D1.4 K Ton/D

•• Condensates Production Condensates Production 105 KBBL/D105 KBBL/D

HapyLTS

Design Capacity : 340 MMscf/DSales Gas : 320 MMscf/D

Cond. : 1200 bbl / D

East BaltimGas to Abu Madi

Facilities

RosetteLTS

Design Capacity : 300 MMscf/DSales Gas : 275 MMscf/D

Cond. : 1200 bbl / D

Abu Madi & N. Abu MadiLTS

Design Capacity : 360 MMscf/DLPG

Design Capacity : 540 MMscf/DSales Gas : 540 MMscf/D

Cond. : 8500 bbl / DLPG : 400 Ton /D

AmyriaLPG

Design Capacity : 300 MMscf/DSales Gas : 275 MMscf/D

Cond. : 800 bbl / DLPG : 350 Ton /D

SalamLTS

Design Capacity : 200 MMscf/DSales Gas : 180 MMscf/D

Cond. : 9000 bbl / D

LTSObayied

LTSDesign Capacity : 420 MMscf/D

Sales Gas : 400 MMscf/D Cond. : 40000 bbl / D

Bed 2 , 3LTS

Design Capacity : 315 MMscf/DSales Gas : 300 MMscf/D

Cond. : 7000 bbl / D

Abu GhradikLTS

Design Capacity : 160 MMscf/DSales Gas : 140 MMscf/D

Cond. : 1800 bbl / D Abu SannanLTS

Design Capacity : 85 MMscf/DSales Gas : 75 MMscf/D

Cond. : 400 bbl / D

DahshourLPG

Design Capacity : 138 MMscf/DSales Gas : 125 MMscf/D

LPG : 300 Ton /D

Trans GulfLPG

Design Capacity : 130 MMscf/DSales Gas : 70 MMscf/D

Cond. : 3400 bbl / DLPG : 900 Ton /D

Ras ShoukierLPG

Design Capacity : 220 MMscf/DSales Gas : 170 MMscf/D

Cond. : 5000 bbl / DLPG : 1000 Ton /D

Zeit BayLPG

Design Capacity : 90 MMscf/DSales Gas : 20 MMscf/D

Cond. : 3400 bbl / DLPG : 500 Ton /D

Abu RudiesLPG

Design Capacity : 50 MMscf/DSales Gas : 40 MMscf/D

Cond. : 3400 bbl / DLPG : 400 Ton /D

Abu Madi

EL QARA

Alexandria

Abu Qir

Sedikreir

Ameriya

TarekEL - Obayied

SalamSouthOm Barka

Abu Sannan

Abu El Ghradik

Bed-2,3

AyounMoussaDahshour

Tebbin

CairoSuez

ZafranaKoraymat

Ras Bakr

Ras Shoukier

Asiout

ELMenia

NGL UnitDesign Capacity : 550 MMscf / DSales Gas : 470 MMscf / DEthane / Propane : 1400 Ton / DPropane : 600 Ton / D LPG : 850 Ton / DCond. : 700 bbl / D

Port Fouad / Darfeel /Temsah

LTSDesign Capacity : 600 MMscf/D

Sales Gas : 580 MMscf/D Cond. : 22000 bbl / D

LT SL P GLT S & L P GN G LL N G

Abu Qir

Design Capacity : 240 MMscf/DSales Gas : 220 MMscf/D

Cond. : 3500 bbl / DLPG : 200 Ton /D

LTSDesign Capacity : 300 MMscf/D

N. Abu Madi

Port Said

Port FouadLPG

Damietta

LNG (Idku)Feed :500 MMscf / DLNG : 9155 Ton / D

2 TrainsDesign Capacity : 100 MMscf/DSales Gas : 85 MMscf/D

Cond. : 5000 bbl / D

TarekLTS

MED. NGL (UGDC)Feed : 1100 MMscf/DPropane : 790 Ton / D

LPG : 930 BBL / DCond. : 2800 BB / D

LNG (Damietta)Feed : 750 MMscf / DLNG : 14232Ton / D

LNG (Damietta)Feed : 750 MMscf / DLNG : 14232Ton / D

Baltim

Damietta

Talkha

ShabshirTanta

OyounMoussa

Sadat City

Abu Zaabal

10 of the Ramadan

Dahshour Tebbin

SuezCity Gas

City Gas

Zafrana

City Gas

Koraymat

Nile Valley Co.

6 October

Alexandria

Sedi kreir

AmeriyaMahmudya

Egypt Gas

TarekEL - Obyed

SalamSouth

Om Barka

Matruh

Abu Sannan

Abu El Ghradik

Bed-2,3

Ras Bakr

Ras Shoukir

EL - ShababAbu Sultan

Asiout

Beni Suef

ELMenia

Cairo

Hapy

Ameriya Cement

Borg Elarab

Abu Hommos

Abu Madi

EL sheikhzowayed

Port Fouad

Port Said

East PortSaid P.S

P.SArish

CementSinai

& Ind. Area

ElQara

To Eastern pipeline

Taba

Arish

24 ”- 45 km36 ”-194 km24 ”-145 km

16 ”-165 km

16 ”-22 km

42 ”- 40 km

24 ”-50 km

32 ”-167 km

32 ”- 85 km

24 ”- 215 km

16 ”- 114 km

32 ”- 75 km

16 ”-192 km

18 ”-162 km

16 ”-256 km

24 ”- 25 km

22 ”- 87 km

16 ”-38.5 km

28 ”- 46 km

20 ”- 65 km

32 ”-170 km

30 ”- 28 km22 ”- 40 km

12 ”- 40 km

28”-118 km

28 ”- 86 km

24 ”- 45 km

32 ”-200 km24 ”-

22 km12 ”-14 km

22 ”- 40 km

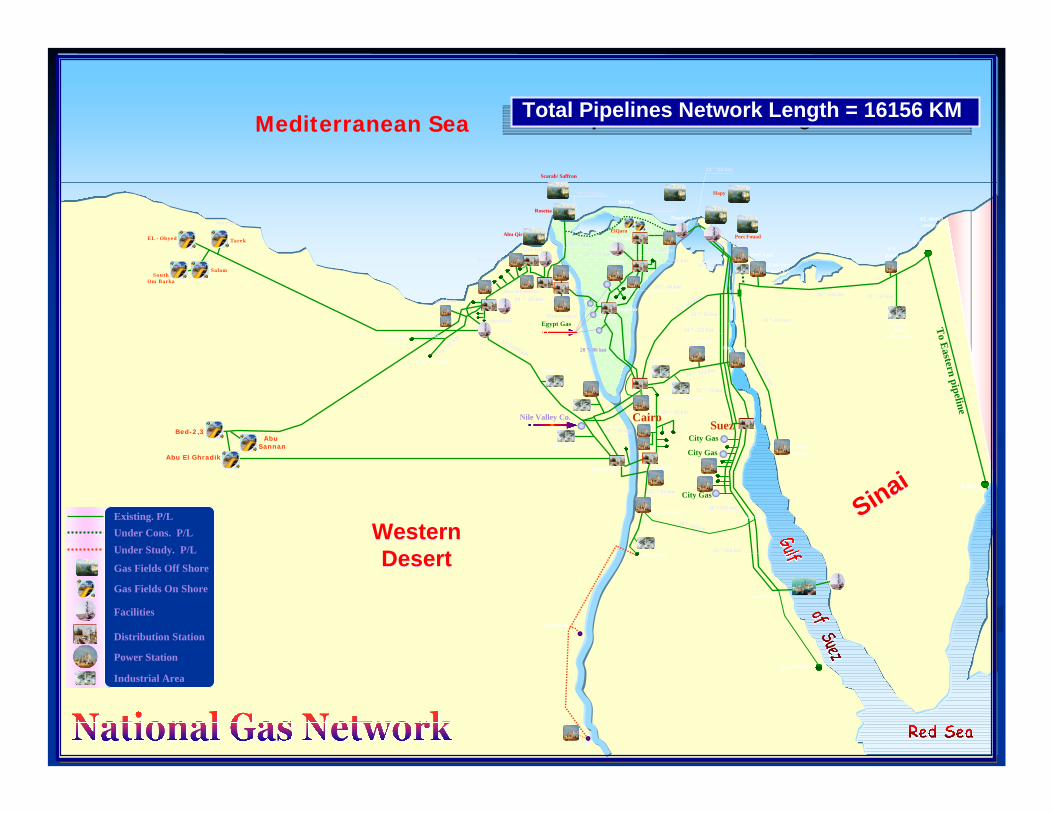

Existing. P/LUnder Cons. P/LUnder Study. P/L

Gas Fields Off Shore

Facilities

Distribution Station

Power Station

Industrial Area

Gas Fields On Shore

Mediterranean Sea

WesternDesert

WesternDesert

SinaiSinai

Abu Qir

Scarab/ Saffron

Rosetta

Abu Qir

Total Pipelines Network Length = 16156 KMTotal Pipelines Network Length = 16156 KM

National Gas Transmission Lines Development(High Pressure)

0

1000

2000

3000

4000

5000

6000

80/8

181

/82

82/8

383

/84

84/8

585

/86

86/8

787

/88

88/8

989

/90

90/9

191

/92

92/9

393

/94

94/9

595

/96

96/9

797

/98

98/9

999

/00

00/

01 0

1/02

02/

03 0

4/05

05/

06

570

KM

5700By December 2006:National Grid Length (High Pressure) = 5700 Km

Total Length = 16,156 Km

By December 2006:National Grid Length (High Pressure) = 5700 Km

Total Length = 16,156 Km

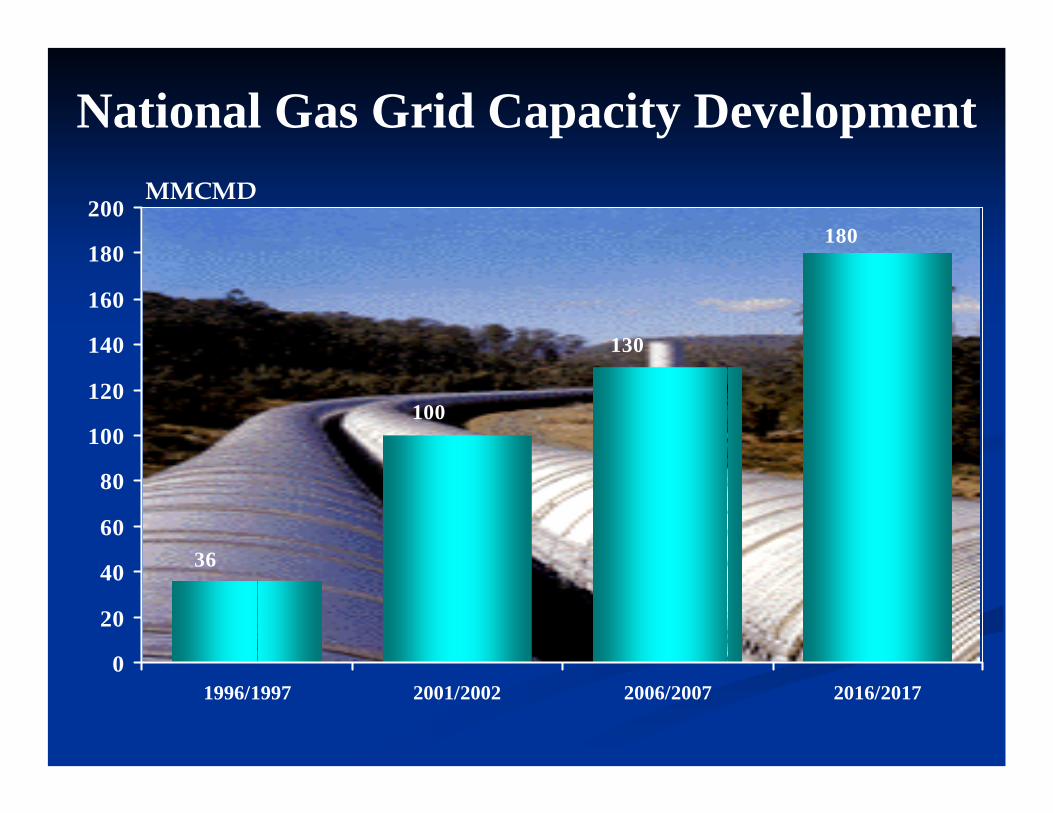

National Gas Grid Capacity Development

180

36

100

130

0

20

40

60

80

100

120

140

160

180

200

1996/1997 2001/2002 2006/2007 2016/2017

MMCMD

Natural Gas Demand DevelopmentNatural Gas Demand DevelopmentM

id S

tream

Act

iviti

es

0

10000

20000

30000

40000

50000

6000080

/81

81/8

282

/83

83/8

484

/85

85/8

686

/87

87/8

888

/89

89/9

090

/91

91/9

292

/93

93/9

494

/95

95/9

696

/97

97/9

898

/99

99/0

000

/01

01/

02 0

2/03

03/

04 0

4/05

05/

06

BSCM

2.4

52.4

18.1

3.70.7

Natural Gas Demand by Sector Share (2005/2006)

Dow

n S

tream

Act

iviti

es

Electricity39% Vehicles

1%

Fertilizers5%

Industry7%

Cement5%

Petroleum7% Residential

1%

Export35%

0

5000

10000

15000

20000

25000

30000

35000

40000

80/8

1

81/8

2

82/8

3

83/8

4

84/8

5

85/8

6

86/8

7

87/8

8

88/8

9

89/9

0

90/9

1

91/9

2

92/9

3

93/9

4

94/9

5

95/9

6

96/9

7

97/9

8

98/9

9

99/2

000

2000

/01

2001

/02

2002

/03

2003

/04

2004

/200

5

2005

/200

6

Ele c tric ity F e rt ilize r Indus try C e m e nt P e tro le um R e s . & C o m m . Ve hic le s

( 1980/81 – 2005/2006 )( 1980/81 – 2005/2006 )34.1

Average Annual GR = 11.2 %Average Annual GR = 11.2 %

Natural Gas Consumption DevelopmentNatural Gas Consumption DevelopmentNatural Gas Consumption Development

2.4

BCM

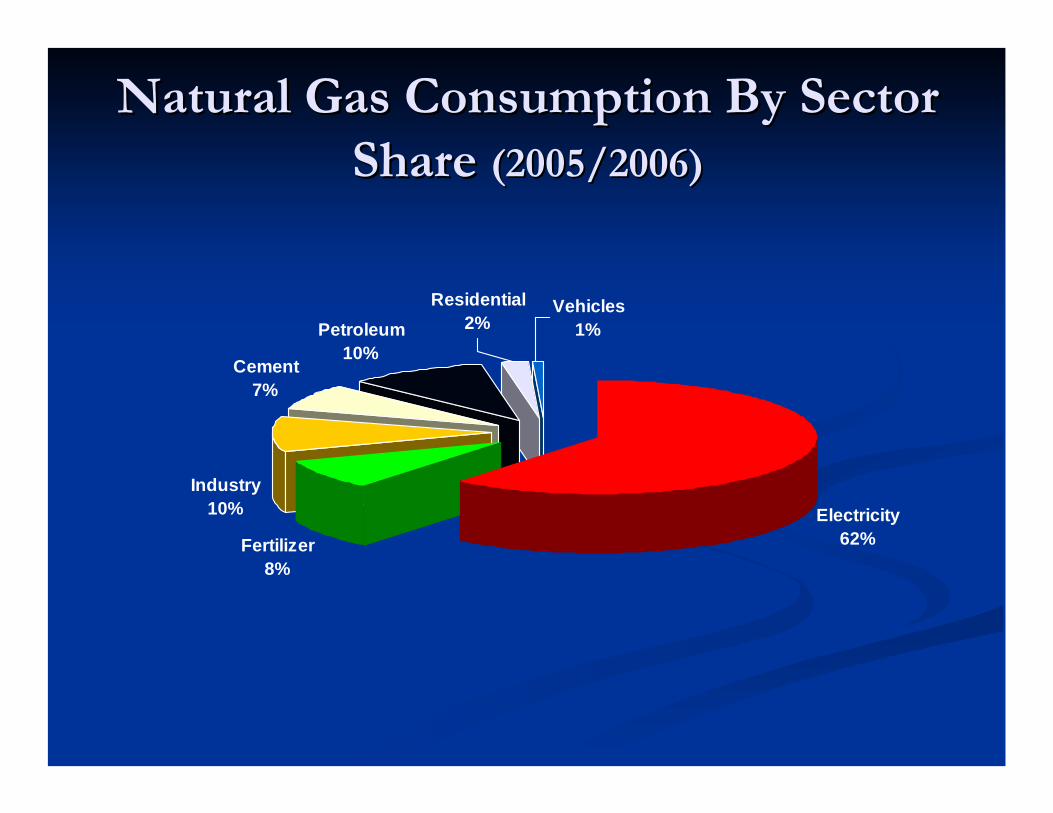

Natural Gas Consumption By SectorNatural Gas Consumption By SectorShare Share (2005/2006)(2005/2006)

Electricity62%Fertilizer

8%

Industry10%

Cement7%

Petroleum10%

Residential2%

Vehicles1%

NGV Industry Current Situation NGV Industry Current Situation (End of November 2006)(End of November 2006)

•• Operating CompaniesOperating Companies : 6: 6•• Converted VehiclesConverted Vehicles : 75 Thousand: 75 Thousand•• Fueling StationsFueling Stations

Operating Operating : 110: 110Under ConstructionUnder Construction : 17: 17

•• Conversion CentersConversion Centers : 54: 54•• Natural Gas Consumption Natural Gas Consumption : 27.4 MMCM/Month : 27.4 MMCM/Month (Nov.)(Nov.)

Taxi72%

Others3%

Buses2%

Light Trucks

1%

Private9%

Pik-up7%

Mirobuses3%

Fork Lift3%

Natural Gas ExportNatural Gas Export

Gas Export Projects – Cont.Gas Export Projects – Cont.

To Jordan, Syria & then to Lebanon, Cyprus and Europe To Jordan, Syria & then to Lebanon, Cyprus and Europe

Agreement : Signed in Jan. 2001.Export : 1.1 - 3 Billion CM / Y.Investment : US $ 200.Operation : July 2003.11

““Phase I Phase I ““ To Jordan:To Jordan:(Al (Al ArishArish –– TabaTaba-- AqabahAqabah))

Through Pipelines:Through Pipelines:ArabGasArabGas Pipeline:Pipeline:Total Capacity= 10 BCMTotal Capacity= 10 BCM

““Phase II Phase II ”” AqabaAqaba––Rehab :Rehab :

36”/393 Km Pipeline System

Investments: US $ 270 - 300 million

36”/ 540 Km Pipeline System

Investments: US $ 400 - 500 million

““Phase III Phase III ”” Jordan/Syria/TurkeyJordan/Syria/Turkey

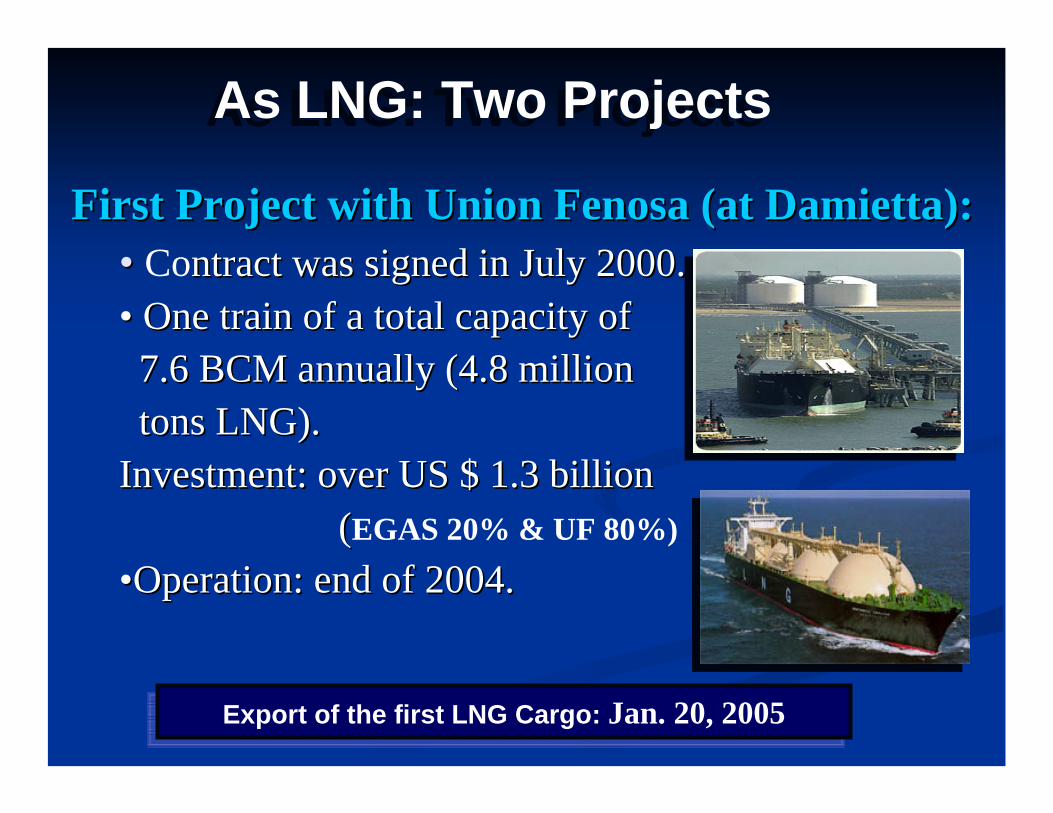

First Project with Union First Project with Union FenosaFenosa (at Damietta):(at Damietta):•• Contract was signed in July 2000.ntract was signed in July 2000.•• One train of a total capacity of One train of a total capacity of 7.6 BCM annually (4.8 million7.6 BCM annually (4.8 milliontons LNG).tons LNG).

Investment: over US $ 1.3 billion Investment: over US $ 1.3 billion ((EGAS 20% & UF 80%)

••Operation: end of 2004.Operation: end of 2004.

Export of the first LNG Cargo: Jan. 20, 2005Export of the first LNG Cargo: Jan. 20, 2005

As LNG: Two ProjectsAs LNG: Two Projects

Gas Exports Projects – Cont.Gas Exports Projects Gas Exports Projects –– Cont.Cont.

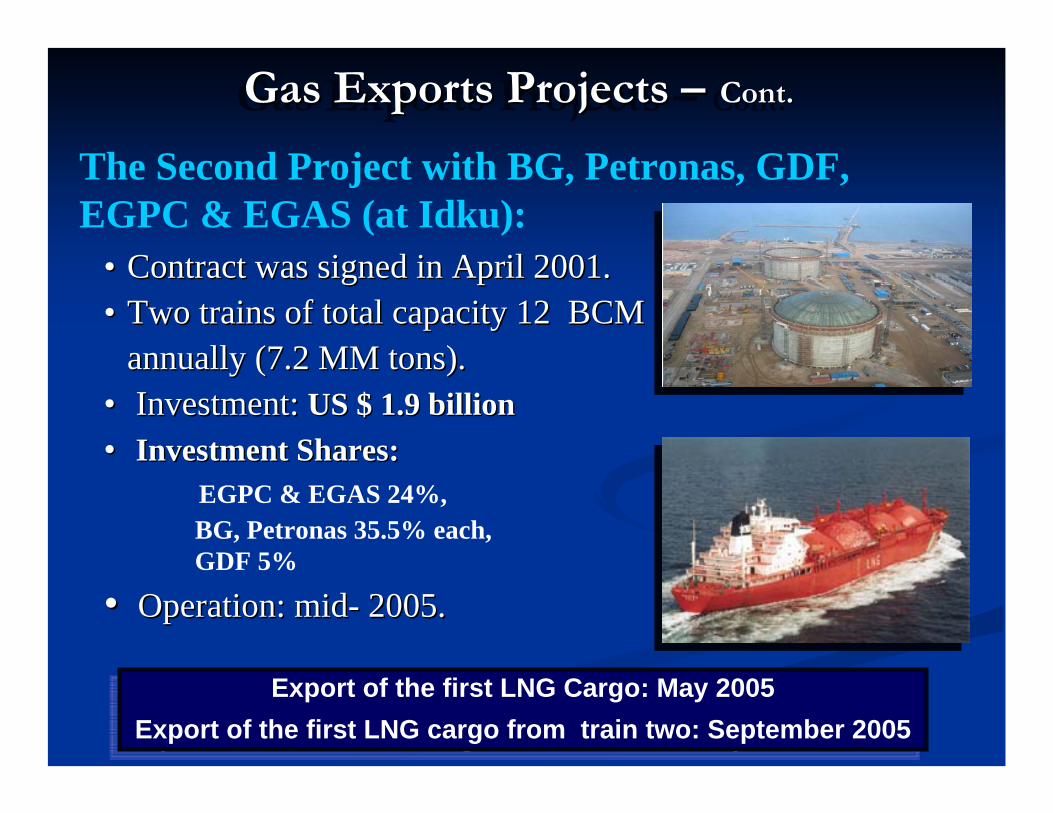

The Second Project with BG, Petronas, GDF, EGPC & EGAS (at Idku):

•• Contract was signed in April 2001.Contract was signed in April 2001.•• Two trains of total capacity 12 BCM Two trains of total capacity 12 BCM

annually (7.2 MM tons).annually (7.2 MM tons).•• Investment: Investment: US $ 1.9 billionUS $ 1.9 billion•• Investment Shares:Investment Shares:

EGPC & EGAS 24%,BG, Petronas 35.5% each,GDF 5%

•• Operation: midOperation: mid-- 2005.2005.

Export of the first LNG Cargo: May 2005 Export of the first LNG cargo from train two: September 2005

Export of the first LNG Cargo: May 2005 Export of the first LNG cargo from train two: September 2005

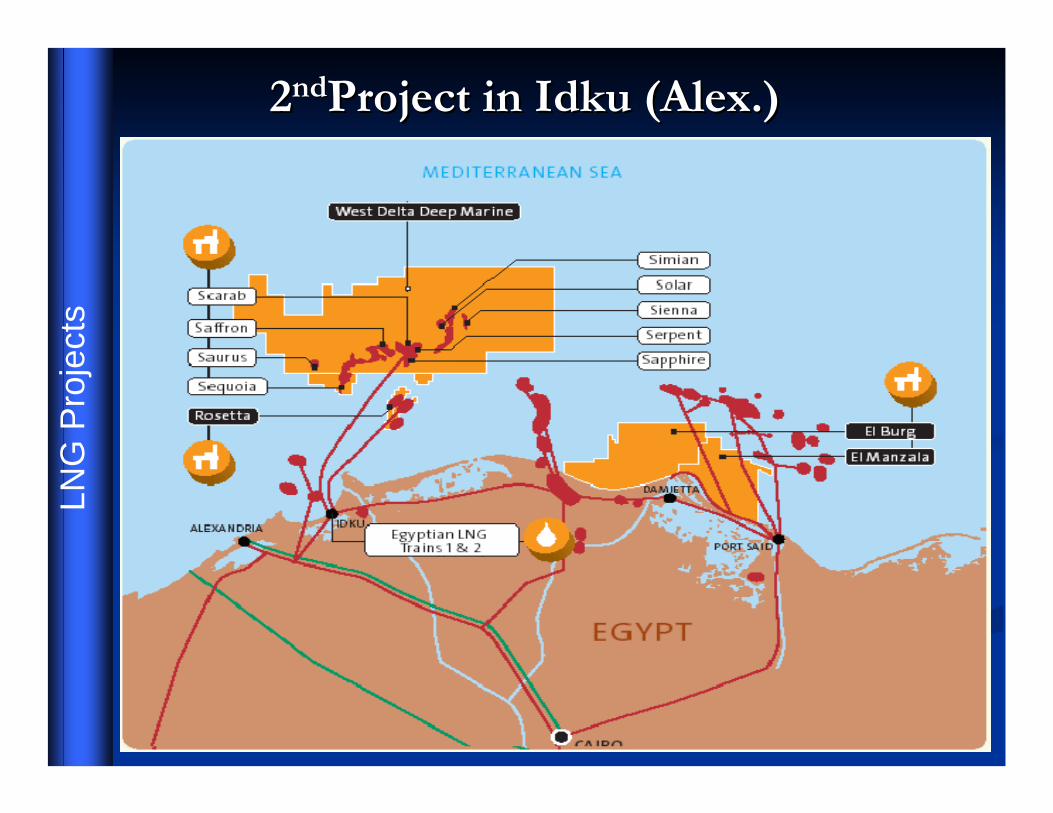

22ndndProject in Project in IdkuIdku (Alex.) (Alex.) LN

G P

roje

cts

Egyptian LNG Export

To USA

To Italy

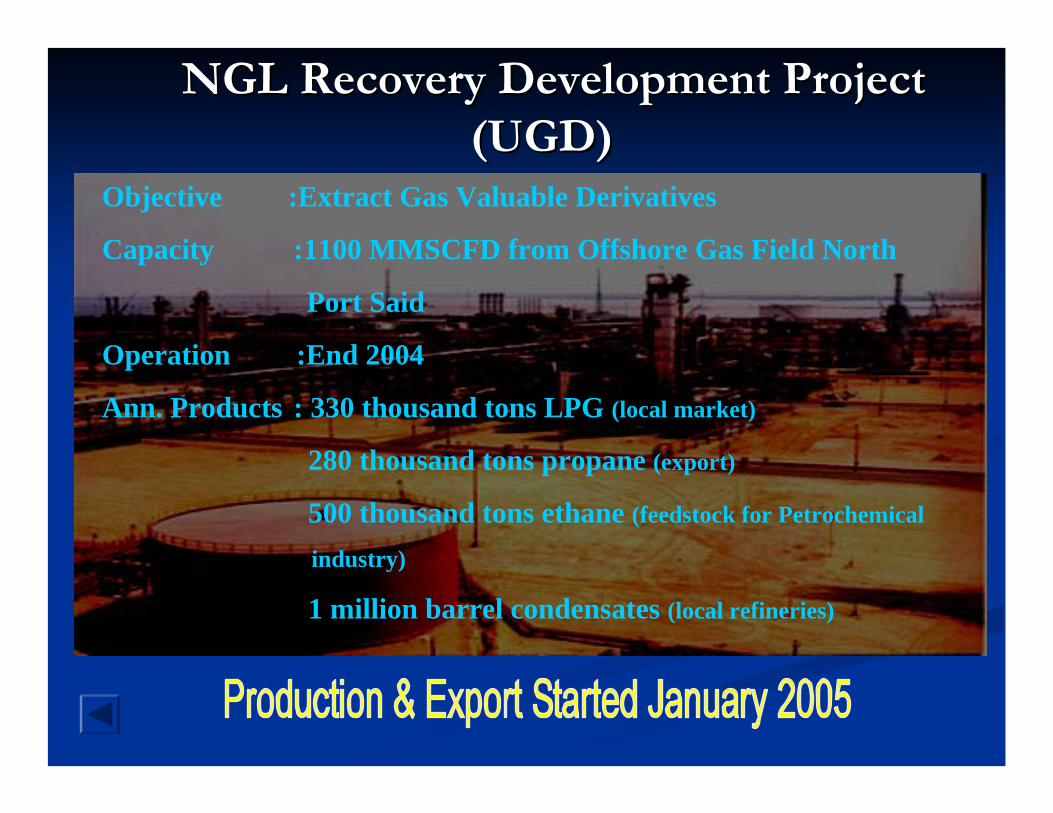

NGL Recovery Development Project NGL Recovery Development Project (UGD)(UGD)

Objective :Extract Gas Valuable Derivatives

Capacity :1100 MMSCFD from Offshore Gas Field North

Port Said

Operation :End 2004

Ann. Products : 330 thousand tons LPG (local market)

280 thousand tons propane (export)

500 thousand tons ethane (feedstock for Petrochemical

industry)

1 million barrel condensates (local refineries)

Thank YouThank You