effects of terrorism on the u.s. stock market: evidence

TRANSCRIPT

Western Kentucky UniversityTopSCHOLAR®Honors College Capstone Experience/ThesisProjects Honors College at WKU

Spring 2019

Effects of Terrorism on the U.S. Stock Market:Evidence from High Frequency DataKyla ScanlonWestern Kentucky University, [email protected]

Follow this and additional works at: https://digitalcommons.wku.edu/stu_hon_theses

Part of the Business Analytics Commons, Finance Commons, and the Finance and FinancialManagement Commons

This Thesis is brought to you for free and open access by TopSCHOLAR®. It has been accepted for inclusion in Honors College Capstone Experience/Thesis Projects by an authorized administrator of TopSCHOLAR®. For more information, please contact [email protected].

Recommended CitationScanlon, Kyla, "Effects of Terrorism on the U.S. Stock Market: Evidence from High Frequency Data" (2019). Honors College CapstoneExperience/Thesis Projects. Paper 781.https://digitalcommons.wku.edu/stu_hon_theses/781

EFFECTS OF TERRORISM ON THE U.S. STOCK MARKET: EVIDENCE FROM

HIGH FREQUENCY DATA

A Capstone Project Presented in Partial Fulfillment

of the Requirements for the Degree Bachelor of Science in Financial Management and

Economics with Honors College Graduate Distinction at

Western Kentucky Univeristy

By

Kyla M. Scanlon

May 2019

*****

CE/T Committee: Approved by

Professor Alexander Lebedinsky, Chair __________________

Professor Brian Strow Advisor

Professor Dennis Wilson Department of Economics

Copyright by

Kyla Scanlon

2019

iv

ABSTRACT

This paper investigates the effects that terrorist attacks and mass shootings had on

the U.S. stock market, using high frequency intraday data to identify stock price and

variability reactions in the hours after the attack. The impact that terrorist attacks had on

price level variability was examined using the generalized autoregressive conditional

heteroskedasticity (GARCH) model. The market reaction to domestic versus foreign

attacks was examined to measure a potential for contagion across financial markets. The

potential for flight-to-safety/quality and capital reallocation in response to terrorist

attacks were measured using ordinary least squares (OLS) model, measuring the

respective betas of small cap and large cap stocks. The results indicated that domestic

attacks cause a large increase in variability and a decrease in price level in the hour after

the incident, whereas attacks that occurred in foreign countries had virtually no impact on

the U.S. stock market. There is evidence that the price levels recover from the attacks

within the same day. There is a significant flight to safety after the attacks occur, with

small cap stocks severely underperforming compared to large cap stocks. All of these

contribute to the possibility of desensitization, suggesting that the market response to

terrorist attacks have diminished over the past decade.

Keywords: Terrorism, Regression Analysis, Stock Market, Finance, Market Efficiency,

Desensitization

v

ACKNOWLEDGEMENTS

This project would not have been possible without the help, knowledge, and

support of so many people. I am endlessly thankful to Dr. Alex Lebedinsky, my CE/T

advisor, for his thorough critiques of my work, for his ability to explain the most complex

topics in the simplest terms, and his support and constant encouragement to push me to

be the best that I can be. Many thanks to Dr. Brian Strow, for offering me the

opportunitity to begin my research journey with the BB&T Center for the Study of

Capitalism Student Research grant, and for serving on my committee. I would also like to

thank Dr. Dennis Wilson for serving on my committee and for the time he spent helping

me prepare for this.

I would like to thank the Honors College for creating a community that challenges

its scholars to grow, both personally and professionally. I would also like to thank

Western Kentucky University for the financial support of an iteration of this research

through the Faculty-Undergraduate Student Engagement (FUSE) Grant. Without the

support from both the BB&T Center and WKU, I would not have been able to travel to

Indianapolis, Las Vegas, and Frankfort to present my research at many conferences.

Finally, I would like to thank my friends and family. Their support and

encouragement enabled me to complete this project, as well as all the other amazing

activities I’ve done here at WKU and in the GFCB.

vi

VITA

EDUCATION

Western Kentucky University , Bowling Green, KY May 2019

B.S in Finance and Economics – Mahurin Honors College Graduate

Honors Capstone: Effects of Terrorism on the U.S. Stock Market:

Evidence from High Frequency Data

Eastern High School, Louisville, KY May 2015

PROFESSIONAL EXPERIENCE

The Gordon Ford College of Business, WKU August 2017 - Present

Student Researcher

Investment Strategy and Research Team, Hilliard Lyons May 2018 – August 2018

Intern

Hyundai Division, Oxmoor Auto Group May 2017 – August 2018

Sales Intern

AWARDS & HONORS

Summa Cum Laude, WKU, May 2019

Charles B & Anita Hardin McDole Scholarship Winner, WKU, May 2018

Outstanding Junior in Economics, Gordon Ford College of Business, May 2017

Commissioners Academic Medal, WKU, 2017

PROFESSIONAL MEMBERSHIPS

Beta Gamma Sigma

Omicron Delta Epsilon

PRESENTATIONS

Scanlon, K. & Lebedinsky A. (2018, April). Effects of Terrorism on the U.S. Stock

Market: Evidence from High Frequency Data. Oral Presentation presented at the

Butler University Student Research Conference. Indianapolis, IN.

Scanlon, K. (2018, October). Effects of Terrorism on Consumer Sentiment: Evidence

from Twitter Data. Oral Presentation presented at Teradata Analytics Universe.

Las Vegas, NV.

vii

TABLE OF CONTENTS

Abstract .............................................................................................................................. iv

Acknowledgements ............................................................................................................ vi

Vita .................................................................................................................................... vii

List of Figures and Graphs ............................................................................................... viii

List of Tables ..................................................................................................................... ix

Chapters:

1. Introduction ........................................................................................................... 10

2. Literature Review.................................................................................................. 11

3. Data and Methodology ............................................................................................ 15

4. Results ..................................................................................................................... 15

Price Level

Variability

GARCH Model

Ordinary Least Squares Model

5. Discussion ............................................................................................................... 15

References ......................................................................................................................... 21

Appendix ........................................................................................................................... 23

viii

LIST OF FIGURES AND GRAPHS

Graph ........................................................................................................................... Page

1a. Changes in Cumulative Return of Large and Small Cap Stocks. ............................... 27

1b. Changes in Cumulative Return of Large and Small Cap Stocks. ............................... 28

2a. 5-Minute Moving Avg of Minute/Minute Standard Deviation of Returns ................. 29

2b. 5-Minute Moving Avg of Minute/Minute Standard Deviation of Returns ................. 30

3a. Conditional Variance Estimates from the GARCH Model – Large Cap .................... 31

3b. Conditional Variance Estimates from the GARCH Model – Large Cap .................... 32

4a. Conditional Variance Estimates from the GARCH Model – Small Cap .................... 33

4b. Conditional Variance Estimates from the GARCH Model – Small Cap .................... 34

5. Conditional Variance Estimates from the GARCH Model – Small Cap ...................... 35

ix

LIST OF TABLES

Table ............................................................................................................................. Page

1. List of Attacks .............................................................................................................. 24

2. Estimates from GARCH Model. .................................................................................. 25

3. Estimates from OLS Model .......................................................................................... 26

10

INTRODUCTION

Terrorist attacks create a significant level of uncertainty in the marketplace. After the 9/11

attacks, the New York Stock Exchange was closed for a week. The Federal Reserve added $100

billion in liquidity to the market after the attacks to prevent an economic crisis. Gold, a safe

harbor for capital and a result of panic selling, increased in price by one-third due to asset

reallocation. Equity markets around the world fell sharply, and the U.S. market lost $1.4T the

week it reopened.

Terrorist attacks carry a financial and an emotional shock. They cannot be hedged against and

cannot be priced into the market, because they are unpredictable. There are direct and indirect

costs, as our global economy is so intertwined that an attack in one country negatively impacts

the economy of other nations.

The motivation of this study is to examine how market sentiment regarding terrorism has

evolved across developed nations over time. Due to the increasing frequency of terrorist attacks

in modern society, the impact that they have on the financial markets might have diminished.

The results of this study should be interpreted with caution because they are only based on a

small sample of 16 events.

This paper adds to the current literature by examining the global impact of terrorism on U.S.

financial markets. Data was collected from the Global Terrorism Database (GTD), a dataset that

covers terrorist attacks across the world from 2011 - 2017. From that, terrorist attacks that

occurred in 6 developed countries during US stock market trading hours were identified. The

GTD was then combined with high frequency intraday data from the Center for Research on

11

Security Prices (CRSP) to identify overall price movements and changes in market volatility in

the hour after the attack.

Data from both small cap and large cap stocks are examined, to determine if terrorism has a

different impact on small and large cap companies. The analysis also accounts for a potential

“flight to safety”, by measuring changes in return of small cap versus large cap stocks. The

market reaction to domestic attacks versus international attacks was examined to measure the

potential of contagion across financial markets.

The paper employs the generalized autoregressive conditional heteroscedasticity (GARCH)

model to measure changes in volatility immediately after a terrorist attack. It also employs

Ordinary Least Squares (OLS) Regression model to measure changes in capital flows from small

cap to large cap stocks after the attacks occur, which can be used as a proxy for investor fear.

LITERATURE REVIEW

Terrorism has gained more academic attention in recent years, as the frequency of such attacks

have increased, and a growing body of literature examines how the attacks impact the stock

market. Beyond the increased uncertainty and loss of lives, there are many economic

consequences, such as the resource costs of recovery, the stunted flow of capital across countries,

and a potential reduction in overall economic activity as noted by Kollias, Papadamiu, and

Stagiannis (2010).

Abadie and Gardeazabal (2003) provided a quantification of the impact of terrorism through

their analysis of the Basque Country, an area in Spain that has been riddled with conflict and

terrorist attacks, most notably by the ETA Group. Their findings concluded that an increase of

terrorist activity in Basque Country resulted in a 10% average GDP gap between Basque Country

12

and the area that didn’t experience terrorism. But economic recovery can be quick, as evidenced

by the cease fire in 1998-1999, in which Basque Country economically outperformed the

nonterrorism region. The quick recovery time and economic decline due to frequency of terrorist

attacks is similar to what most studies have concluded.

Kollias et al (2010) also examined recovery time after attacks. Examining attacks in Madrid and

London using the GARCH model, they found that London was able to respond and recover in a

more efficient manner compared to Madrid, with 1 day of recovery versus 16 days, respectively.

There were several factors that determined the quickened recovery time, including the method of

attack (backpack bombs in Madrid vs. suicide bombers in London) as well as differences in

access to capital. The role of being a more financially developed nation was key in London’s

recovery. However, the overall findings concluded that the market in both Madrid and London

bounced back quickly after the attacks occurred.

Brouren and Derwall (2010) compared the impact of terrorist attacks to natural events, such as

earthquakes. An interesting point that this study and most studies like it found is that “very few

terror attacks have had a significant price impact that lasted longer than the event day itself”

providing further evidence for a quick recovery time. Compared to a natural event, terrorist

attacks have a larger impact, but that impact disappears within the trading day.

It is also important to note the immediate reverberation across markets that these attacks, despite

quick recovery times, can have. Bilson, Brailsford, Hallett, and Shi (2012) measured financial

contagion from terrorism to see if there is evidence that an attack in one country can affect the

entire global equity market. If a country can use a strong central bank for liquidity, have an

attack recovery plan in place, as well as coordinate recovery across industries, they will be able

to absorb the attacks and stabilize the markets quickly (Johnston & Nedelescu, 2005).

13

There is an interconnectedness among financial markets. When attacks occur, they “induce

substantial contagion consequences, particularly for developed nation equity markets.” (Bilson et

al., 2012). An attack in America will affect all equity markets and depending on the overall

impact and scale of the attack, that could be detrimental for global growth.

Arin and Spagnolo (2008) examined how terror shocks reverberate across countries, comparing

European and non-European countries. They found that developed Western European market

exchanges experience less of a financial impact from terrorist attacks as compared to developing

nations. From their GARCH model calculations, they concluded that the developed European

countries were more resilient to the shocks than the developing nations.

It might also be the case that the sheer frequency of attacks since 9/11 has diminished their

impact as we, unfortunately, grow more accustomed to them. Baumbert, Buesa, and Lynch

(2013) examine the impact of Boston Marathon Bombing on different financial markets,

comparing it to 3 past terrorist events. They found that the markets followed a similar pattern

with regard to price movement as compared to the other attacks, but there was a decline in

overall impact, pointing again to the possibility of desensitization.

Coleman (2012) found a reduction in impact from individual attacks over time since 9/11, noting

that the markets usually take a little over one hour to incorporate the terrorist attacks into the

price data. He also notes that the markets did not follow a certain pattern of movement after the

attacks, with “most changes were not significant, and those that were significant were likely to

be up as down” (Coleman, 2012). This provides evidence that there is not a set direction that we

can expect the stock market to move after an attack occurs.

Wang and Young (2017) provide evidence for mutual fund outflows following the month after a

terrorist attack occurs. They noted that the initial reactions disappear in the second month after

14

the attack. They also found no change in relative market risk in the aftermath of the attack, or a

change in the CBOE Volatility Index. This provides further evidence for quick recovery time, as

well as investor capital reallocation.

Kollias, Papadamou, and Arvanitis provide further evidence for capital reallocation through

investor shift into a flight-to-quality/safety when a terrorist attack occurs. Using the GARCH

model, the authors find that a flight-to-quality reaction exists, especially when a domestic

terrorist attack occurs. They found that both transnational and domestic terrorist attacks impact

the markets and result in a measurable movement of capital.

Historically, small cap stocks are more volatile than their large cap counterparts, as small cap

companies are more effected by various news reports as compared to large cap companies.

(Schwert, 2003). This is for a variey of reasons, but overall small cap stocks carry a higher level

of risk, with less access to financial resources to recover from events such as terrorist attacks.

Thus, with an increasing frequency of terrorist attacks, there could be an increasing frequency

flight to safety from riskier or smaller stocks to safer or larger stocks, as studied by Kollias et al.

This paper contributes to the field of existing research by examining events with high-frequency

data to get a more detailed look at the immediate effects of the attacks. None of the paper in the

literature attempted to use high-frequency data in this context, with most studies using daily data

to our knowledge.

We also examine whether small-cap and large-cap stocks react differently to the attacks, by

measuring the difference in return between the two. As we will discuss below, our results largely

confirm the findings in the existing literature – there is not much evidence of terrorist attacks

having a large impact on the stock markets, and if there is an impact, it disappears within the

same day.

15

DATA AND METHODOLOGY

In the analysis, I use data collected from the Global Terrorism Database and other public sources

to select events that have occurred since 2011, which is the earliest year for CRSP high-

frequency data. The study was limited to the attacks that occurred in developed countries, and

only to those attacks that occurred during trading hours. The focus of this paper is on developed

countries because attacks tend to be rarer in those areas, and thus are more likely to have a

greater impact on financial markets.

The GTD contains thousands of incidents that have occurred across the globe during 2011 –

2018. Most of these incidents were minor and did not receive significant news coverage. In this

analysis, I selected 16 different events that either had many casualties (e.g. San Bernandino or

Parkland Shooting) or attacks that occurred in public spaces or popular tourist sites (e.g. the

Parliament Hill Shootings or the Boston Marathon Bombing).

The sample was also limited to attacks that occurred at a distinct point in time during trading

hours to determine the immediate impact on the stock market. For that reason, events such as the

2011 Norway attacks were not included because the attack occurred over a period of time.

After identifying the terrorist attacks that occurred during trading hours, I extracted price level

data from CRSP’s Intraday U.S. Index History Files for the days on which the attacks occurred.

This dataset contains second-by-second values for portfolios of stock (e.g. large cap, small cap

etc.) traded on major U.S. exchanges. For each day, the changes in price level and variation in

price level for Large Cap and Small Cap indices (CRSP variables CRSPLC1 and CRSPSC1)

were examined. To examine the effect of the attack on the price level, cumulative return for each

day was computed:

16

𝑅𝑒𝑡𝑡 = ln 𝑝𝑠 − ln 𝑝0, (1)

where 𝑝𝑠 is the index level in second s and 𝑝0 represents the first recorded value of the index for

that day. I use cumulative returns to standardize the graphs, so that their scale is not impacted by

the starting value of the index. Then minute-by-minute variance for the indices was computed:

𝑉𝑎𝑟𝑚(𝛥𝑝) =1

60( ∑ (𝛥𝑝𝑠 − 𝛥𝑝𝑚

)2

𝑚×60

𝑠=(𝑚−1)×60+1

), (2)

where 𝛥𝑝𝑚 is the average change in price during the minute 𝑚 and the change in index value 𝑝

between seconds 𝑠 and 𝑠 − 1 is defined as

𝛥𝑝𝑠 = 𝑝𝑠 − 𝑝𝑠−1 (3)

To further examine the changes in volatility in the aftermath of an attack, I use a GARCH model

specified as

𝛥𝑝𝑠 = 𝛽0 + 𝛽1𝐸𝑣𝑒𝑛𝑡𝑠 + 𝑢𝑠 (4)

𝑢𝑠 = √ℎ𝑠 ∙ 𝑣𝑠 (5)

ℎ𝑠 = 𝜅0 + 𝜅1𝐸𝑣𝑒𝑛𝑡𝑠 + 𝛿ℎ𝑠−1 + 𝑎𝑢𝑠−12 (6)

where 𝐸𝑣𝑒𝑛𝑡𝑠 = 1 during the 30 minutes immediately after the attack and 0 otherwise, and 𝑣𝑠

follows standard normal distribution. This is a standard GARCH model (e.g. see Hamilton

(1994)) modified to include an exogeneous variable 𝐸𝑣𝑒𝑛𝑡𝑠 that changes both the level and the

variance of stock prices. In the first equation, the 𝛽1 coefficient captures the change in the

average of 𝑑𝑝𝑠. If 𝛽1 < 0 and 𝛽0 + 𝛽1 < 0, then after the event the stock prices are expected to

decrease. Coefficient 𝜅1 measures the change in price volatility after the attack: If 𝜅1 is positive,

then there is an increase in stock price volatility. The main purpose of using this model is to get

an estimate of the conditional variance h which provides an alternative way to examine how

variance changes around the attack.

17

As a third step in the analysis, I calculated the betas of the small cap stocks and compared them

to the betas of the large cap stocks for each event by using the following equation, where:

ln(𝑅𝑒𝑡𝑠𝑐) = 𝛼 + 𝐵1𝑅𝑒𝑡𝐿𝐶 + 𝐵2𝐸𝑣𝑒𝑛𝑡𝑖 + 𝐵3𝑅𝑒𝑡𝐿𝐶 ∗ 𝐸𝑣𝑒𝑛𝑡𝑖 + 휀 (1)

This equation assumes that the return of a small cap stock is going to be equal to the return of a

large cap stock, as well as considering whatever added effect the event had on the portfolio. B3,

or the slope dummy, serves as a measure for flight to safety in the market. This coefficienct

captures the relative beta change in small cap stocks, following the movement of capital from

small cap to large cap stocks after an attack occurs. Tracking the movement of capital provides

insight into investor sentiment and provides a rough estimate of “fear” in the market, especially

because emotions can be a driver of investment choices.

RESULTS

4.1 Price Level

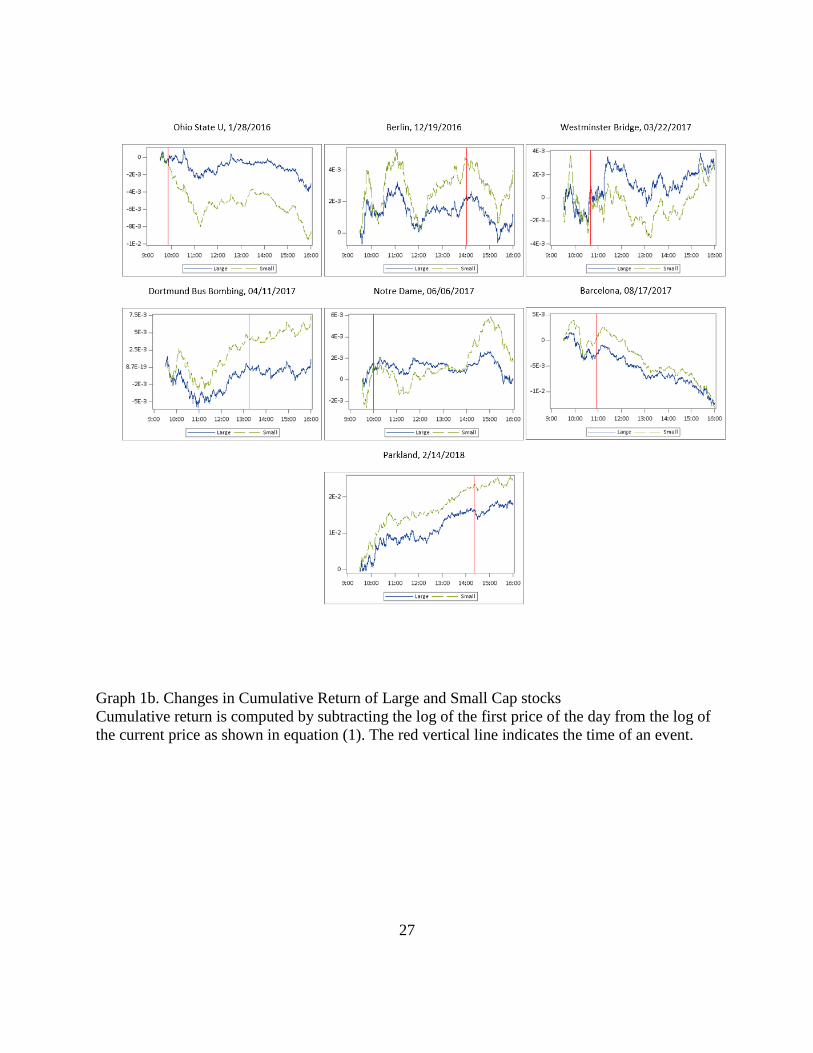

Graph 1-4 compares the effect that terrorist attacks had on the price level of small cap stocks vs

large cap stocks. In many cases, there was an instantenous decline in market price for the 30 – 60

trading minutes after the incident, and sometimes for the continuation of the trading day. For

many of the events, small cap stocks experienced a larger price movement albeit that price

movement was short-lived. This is seen in the Brussels Mosque Bombing, Parliament Hill

Shooting, and Parkland Shooting, all of which experienced small movements in stock prices

immediately after the attacks, but quickly bouncing back before the end of the trading day.

4.2 Variability

Graph 2 in the appendix show changes in variability of stock prices by plotting five-minute

moving averages of √𝑉𝑎𝑟𝑚(𝛥𝑝). Across the various attacks, large cap stocks experienced more

18

variability after the attack time as compared to their small cap counterparts. This disparity is

most pronounced for the attacks that occurred in the U.S., most notably the Boston Marathon

Bombings, Sandy Hook Shooting, and San Bernardino. Overall, U.S. stocks don’t appear to be as

reactive to transnational attacks because the levels of volatility do not appear to be noticeably

different on a day-to-day comparison.

4.3 GARCH Model

Table 2 shows the estimates from the GARCH model. Only the estimates of coefficients

𝛽1, 𝜅0 and 𝜅1, are reported, which correspond to the changes in the price level of the stocks after

an attack, baseline variance, and changes in variance after an attack, respectively. The results

for 𝛽1 coefficient show that small cap stocks, on average, had a -0.00029 point per second

decline in stock price index in the hour following the attack. This amounts to about 1.05 point or

roughly 0.06-0.1% drop in stock prices in the hour after the attack (stock index ranges from 1100

to 1700 in the sample). Large cap stocks, on average, had a much smaller drop of 0.000136

points per second, which amounts to only about 0.001-0.002% decline.

Coefficient 𝜅1 does not represent the size of increase in the variance of Δp because the overall

variance hs depends on its lagged value as well as other parameters. Therefore, the only

interpretation this coefficient provides is whether there is an increase in variance in the hour

following the attack. Almost all the estimates (except one) of 𝜅1 are statistically significant

indicating that variance does change after an attack.

Graphs 3 and 4 show the estimates of conditional variance from the GARCH model. The Boston

Marathon Bombing is the only event where there was an obvious increase in stock volatility. San

Berdanino attack created an increase in volatility, but only for large-cap stocks, which is an

anomaly. The spike in volatility after the Parkland shooting seemed to have lasted for less than

19

fifteen minutes. The attacks in other countries do not appear to have much of an effect on the

volatility of the U.S. stock market.

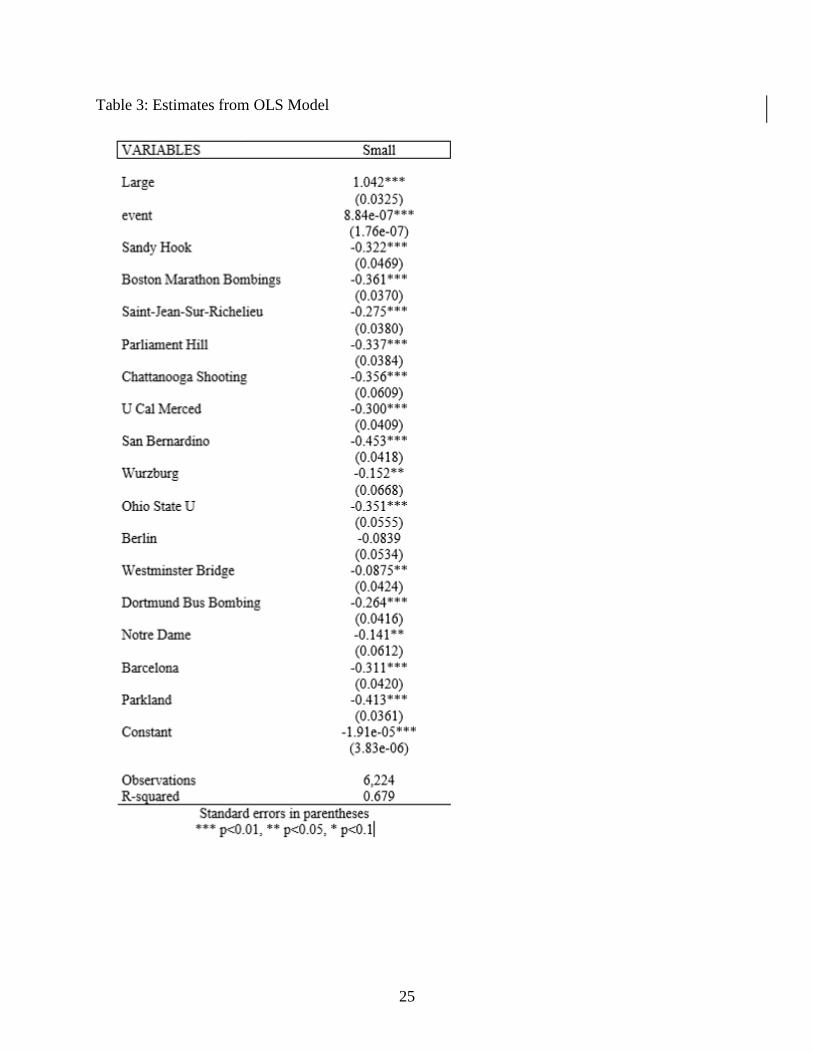

4.4 Ordinary Least Squares Model

Table 3 shows the estimates from the OLS model. Estimates from 15 attacks are shown, with 7

attacks occurring domestically, and 8 attacks occurring transnationally. All the attacks have a

statistically significant response at the 5% level, except for the Berlin Attack. This equation

computes the relative beta of large cap stocks plus the interaction effect of large cap stocks and

the event to determine the aggregate effect that the event had on the return of small cap stocks.

Based on this analysis, small cap stocks are much more responsive to a terrorist attack than large

cap stocks. For example, after the Sandy Hook Shooting attack, small cap stocks returned 32.2%

less than that of large cap stocks. For the more recent Parkland shooting, small cap stocks

returned 41.3% less.

This could provide evidence that investors are moving capital out of small cap stocks and into

large cap stocks when a terrorist attack occurs. This could be a relevant instance of flight-to-

safety/quality, as investors choose to invest in the historically safer large cap companies. Small

cap companies, like developing countries as described in the literature review, have less capital

and available to resources to recover from terrorsit attacks. Investors could be pricing this into

their investment thesis and choose to move their dollars from small cap companies, and into

large cap companies when a terrorist attack occurs.

Discussion

It is important to note that the scale of some of the attack in this study are relatively small, but

overall, the evidence presented in this paper suggests that terrorist attacks that have occurred

20

over the last decade have had little to no long-lasting impact on the U.S. stock markets. This

paper considers both foreign and domestic attacks, with evidence theat U.S. markets largely do

not respond to attacks that occurred in foreign countries. The response to domestic attacks is

mixed, with only one attack, the Boston Marathon Bombinds, leading to a decline in price level,

combined with higher volatility.

This paper also provides evidence that there is a semblance of flight-to-safety/quality when

terrorist attacks occur. There appears to be evidence of capital reallocation, with outflows from

small cap stocks into large cap stocks. Small cap stocks severely underperform large cap stocks

after an event; however, they do recover within the day.

Therefore, the findings in this paper partially support what has been reported in the literature,

supporting that the effect of terrorist attacks on the stock market are short-lived to non-existent.

There appears to be very little evidence of financial market contagion, as the attacks that

occurred in foreign countries had no immediate effect on the stock market in the United States.

21

REFERENCES

Abadie, A., and J. Gardeazabal (2003) The economic costs of conflict: A case study of the

basque country. The American Economic Review 93(1), 113-132. doi:10.3386/w8478

Arin, P. D.Ciferri, and N. Spagnolo (2008) The price of terror: The effects of terrorism on stock

market returns and volatility. Economic Letters 101(3), 164-167.

doi:10.1016/j.econlet.2008.07.007

Bekaert, G, Harvey, C, Ng, A (2005) Market integration and contagion. Journal of BU.S.iness

78, 39–69. doi:10.3386/w9510

Brounen, D. and J. Derwall. (2010) The impact of terrorist attacks on international stock

markets. European Financial Management. 16(4), 585-598. 10.1111/j.1468-

036x.2009.00502.x

Coleman, L (2012) Testing equity market efficiency around terrorist attacks. Applied Economics.

44, 4087-4099. 10.1080/00036846.2011.587778

Eldor, R and Melnick, R. (2004). Financial markets and terrorism. European Journal of Political

Economy, 20, 367–86. 10.2139/ssrn.1578850

Eun, CS., W. Huang and S. Lai (2008). International diversification with large- and small-cap

stocks. Journal of Financial and Quantitative Analysis 43, 489-524.

10.1017/s0022109000003604

Hobbs, J., L. Schaupp, and J. Gingrich (2016) Terrorism, militarism, and stock returns. Journal

of Financial Crime 23(1), 70-86. 10.15417/1881

Kollias, C., Papadamou, S., & Arvanitis, V. (2013). Does Terrorism Affect the Stock-Bond

Covariance? Evidence from European Countries. Southern Economic Journal, 79(4),

832-848.

22

Kollias, C., S. Papdamou and A. Stagiannis (2010) Terrorism and Capital Markets: The Effects

of the Madrid and London Bomb Attacks. International Review of Economics and

Finance 20, 532-541. 10.1016/j.iref.2010.09.004

Kumar, S. and J. Liu (2013) Impact of terrorism on international stock markets. Journal of

Applied BU.S.iness and Economics 12(4), 42-60. 10.4337/9781848449350.00011

Johnston, B and O. Nedelescu (2005). The impact of terrorism on financial markets. IMF

Working Paper. 5(60), 1 – 23

Levisohn, B. (2011) Why small-cap stocks could keep rallying; An improving U.S. economy and

healthy profit margins point the way to small-stock outperformance. Wall Street Journal

Makien, G. (2002) The economic effects of 9/11: A retrospective assessment. Congressional

Research Service, 1-60

Schwert, W. (2002) Anomalies and market efficiency. National Bureau of Economic Research.

Working Paper 9277, 1 – 54

Tavor, T. (2011) The impact of terrorist attacks on the capital market in the last decade.

International Journal of BU.S.iness and Social Science. 2(12), 70 – 80. 10.1111/j.1468-

036x.2009.00502.x

Wang, A. and M. Young (2017) Terrorist attacks and investor risk preference: evidence from

mutual fund flows. FMA Conference Paper, Auburn University and University of

Alabama

23

APPENDIX

Table 1: List of Attacks

Date Market Time Country Killed Wounded Event Description

12-Mar-12 13:00

Belgium 1 1

Brussels Mosque Attack

14-Dec-12 9:35

USA 26 2

Sandy Hook Shooting

15-Apr-13 14:49

USA 3 264

Boston Marathon Bombings

20-Oct-14 11:30

Canada 2 1

Saint-Jean-sur-Richelieu

22-Oct-14 9:52

Canada 2 3

Parliament Hill Shooting

16-Jul-15 10:45

USA 6 2

Chattanooga Shooting

4-Nov-15 10:45

USA 0 4

U California Merced Stabbing

2-Dec-15 10:58

USA 14 24

San Bernardino

18-Jul-16 15:00

Germany 1 5

Wurzburg Train Attack

28-Nov-16 9:52

USA 0 13

Ohio State Attack

19-Dec-16 14:02

Germany 12 56

Berlin Truck Attack

22-Mar-17 10:40

UK 5 49

Westminster Bridge

11-Apr-17 13:15

Germany 0 2

Borussia Dortmund Bus Bombing

6-Jun-17 11:00

France 0 2

Notre Dame Attack

17-Aug-17 10:56

Spain 15 131

Barcelona Van Ramming Attack

14-Feb-18 14:21 USA 17 17 Parkland Shooting

24

Event Level Intercept Variance Level Intercept Variance

Norway Attacks (1), 07/22/11 -.000074 -.000003 .000275*** .000598*** .000081** .000032***

(.00054) (.00011) (.000027) (.00022) (.00004) (.000002)

Norway Attacks (2), 07/22/11 .000235 -.000017 -.000024*** -.00019** .000194*** -.000003***

(.00054) (.00048) (.000006) (.00009) (.00004) (.000000)

Belgium Mosque Bomb, 03/12/12 -.00049*** .000115 -.000057*** .000037 -.000537*** -.000029***

(.00014) (.00009) (.000002) (.0001) (.00008) (.000001)

Sandy Hook Shooting, 12/14/12 -.000691** -.000278*** .000061*** -.000777*** -.000316*** .000008***

(.00036) (.00008) (.000005) (.00014) (.00003) (.000001)

Boston Marathon Bombings, 04/15/13 -.001725*** -.000253** .000511*** -.000657** .000405*** .000045***

(.00064) (.00013) (.000023) (.00038) (.00006) (.000002)

Murder of Lee Rigby, 05/22/13 .000423 -.000796*** .000057*** .001154*** -.000879*** .000038***

(.00067) (.00019) (.000006) (.00028) (.00008) (.000003)

La Defense Attack, 05/23/13 -.000827** .000667*** -.000002*** -.00017* .000402*** -.000008***

(.00036) (.00018) (.000000) (.00013) (.00007) (.000000)

Saint-Jean-sur-Richelieu Ramming

Attack, 10/20/14 .000677* .000649*** .000032*** .00046*** -.00087*** -.000007***

(.00046) (.00016) (.000009) (.00015) (.00007) (.000001)

Shootings at Parliament Hill, 10/22/14 .000584 -.001285*** .000006 .000467** -.000315*** .00001***

(.00054) (.0002) (.000018) (.00026) (.00009) (.000002)

Queens Hatchet, 10/23/14 .000469 .000397*** .000006*** -.000485** .000108* .000012***

(.00051) (.00016) (.000001) (.00023) (.00007) (.000001)

Chattanooga Shootings, 07/16/15 -.000341 -.000587*** .000036*** -.000694*** -.000187*** .000001***

(.00031) (.00008) (.000003) (.00017) (.00004) (.000000)

Thalys Train Attack, 08/21/15 .002633*** -.000885** -.000056*** -.000685*** .000389*** -.000028***

(.00088) (.00041) (.000012) (.00028) (.00013) (.000005)

University of California, Merced

Stabbing Attacks, 11/04/15 -.000519 -.000429*** .000056*** -.000593*** -.000535*** .000005***

(.00048) (.00016) (.000007) (.00023) (.00006) (.000001)

San Bernandino Attack, 12/02/15 -.000372 -.000963*** .000041*** .000619*** -.000432*** .000005***

(.00047) (.00014) (.000003) (.00016) (.00006) (.000001)

Wurzburg Train Attack, 07/18/16 .00046*** -.000359*** -.000007*** .000232*** -.000209*** 000000.*

(.00016) (.00007) (.000001) (.00009) (.00004) (.000000)

Ohio State University Stabbing, 11/28/16 .000099 -.001007*** .00002*** -.000903*** -.000542*** .000006***

(.0003) (.00009) (.000003) (.00018) (.00005) (.000001)

Berlin Attack, 12/19/16 -.000452** -.000181** -.000001** -.000921*** -.000782*** -.000004***

(.00022) (.0001) (.000000) (.00017) (.00007) (.000001)

Westminster Attack, 03/22/17 .001163** -.000345** .000134*** -.000892*** .001341*** .000013***

(.00055) (.00015) (.000010) (.00024) (.00008) (.000002)

Queanbeyan Crime Spree, 04/07/17 -.002792** .000222** .000353*** -.003955*** -.000162*** .000092***

(.00128) (.0001) (.000028) (.00064) (.00005) (.000008)

Borussia Dortmin Team Bus Bombing,

04/11/17 .002266*** -.000032 -.000012*** .001219*** -.000817*** -.000009***

(.00033) (.00016) (.000001) (.00013) (.00007) (.000001)

Paris Champs Elysees Attack, 04/20/17 -.000112 -.000665*** -.000023*** .000596*** -.000112* -.000013***

(.00028) (.00013) (.000002) (.00015) (.00007) (.000001)

Notre Dame Attack, 06/06/17 .00003 -.000035 .000006*** .000002 .000192*** .000012***

(.0003) (.00008) (.000001) (.00019) (.00005) (.000001)

Levallois-Perret Attack, 08/09/17 -.000133 -.000168* -.000005*** .000089 -.000062 -.000002***

(.00023) (.00011) (.000001) (.00012) (.00006) (.000000)

Barcelona Attacks, 08/17/17 -.000646* .001065*** -.000004** -.001558*** .001098*** -.000003***

(.00044) (.00018) (.000002) (.00015) (.00006) (.000001)

Large Cap Small Cap

Table 2: Estimates from the Garch Model

25

Table 3: Estimates from OLS Model

26

Graph 1a. Changes in Cumulative Return of Large and Small Cap stocks:

Cumulative return is computed by subtracting the log of the first price of the day from the log of

the current price as shown in equation (1). The red vertical line indicates the time of an event.

27

Graph 1b. Changes in Cumulative Return of Large and Small Cap stocks

Cumulative return is computed by subtracting the log of the first price of the day from the log of

the current price as shown in equation (1). The red vertical line indicates the time of an event.

28

Graph 2a. 5-Minute Moving Average of Minute-by-Minute Standard deviation of Returns

Standard deviation of returns was computed for each minute within the trading day (see equation

(2)). Five-minute moving average was applied to smooth out the series.

29

Graph 2b. 5-Minute Moving Average of Minute-by-Minute Standard deviation of Returns

Standard deviation of returns was computed for each minute within the trading day (see equation

(2)). Five-minute moving average was applied to smooth out the series.

30

Graph 3a. Conditional Variance Estimates from the GARCH Model – Large Cap

Conditional variance is the expected value of h computed Using the estimates from the GARCH

model (equation 6).

31

Graph 3b. Conditional Variance Estimates from the GARCH Model – Large Cap

Conditional variance is the expected value of h computed Using the estimates from the GARCH

model (equation 6).

32

Graph 4a. Conditional Variance Estimates from the GARCH Model – Small Cap

Conditional variance is the expected value of h computed Using the estimates from the GARCH

model (equation 6).

33

Graph 4b. Conditional Variance Estimates from the GARCH Model – Small Cap

Conditional variance is the expected value of h computed Using the estimates from the GARCH

model (equation 6).

34

Gra

ph 5

. C

han

ge

in R

etu

rn a

nd V

aria

nce

vs.

the

Num

ber

of

Cas

ual

ties

, b

y L

oca

tion

Aver

age

retu

rn a

nd v

aria

nce

wer

e co

mpute

d f

or

30

-min

ute

inte

rval

s bef

ore

and a

fter

att

ack (

less

if

the

atta

cks

occ

urr

ed c

lose

to t

he

beg

innin

g o

f th

e en

d o

f a

trad

ing d

ay).

The

bef

ore

-an

d-a

fter

dif

fere

nce

is

plo

tted

in t

he

gra

ph. T

he

size

of

the

bu

bble

s dep

ends

on t

he

nu

mber

of

fata

liti

es (

See

Tab

le 1

).