effectiveness of carbon accounting methodologies for...

TRANSCRIPT

Effectiveness of carbon accounting

methodologies for LULUCF and

harvested wood products in

supporting climate-conscious

policy measures

Robert MatthewsForest Research UK

Rebecca HeatonCardiff University

OBJECTIVES OF THE STUDY

• To evaluate the impact of different

LULUCF and HWP accounting methods

on the reduction estimates reported by

participating countries.

• Explore gross-net, net-net and article

3.7.

• Examine the baseline on which to

compare reductions.

PentagonLand area; 900000000

Forest area; 180000000

Fossil emissions; 1500

CircleLand area; 90000000

Forest area; 36000000

Fossil emissions; 1

OvalLand area; 900000000

Forest area; 540000000

Fossil emissions; 100

TrapeziumLand area; 900000000

Forest area; 270000000

Fossil emissions; 150

OblongLand area; 30000000

Forest area; 21000000

Fossil emissions; 15

DiamondLand area; 30000000

Forest area; 9000000

Fossil emissions; 10

TriangleLand area; 20000000

Forest area; 2000000

Fossil emissions; 150

StarLand area; 800000000

Forest area; 40000000

Fossil emissions; 100

HYPOTHETICAL COUNTRIES OF BERNHARD-WORLD

Projected land cover in country Trapezium

BUSINESS AS USUAL

0

10

20

30

40

50

60

70

80

90

100

1990 2010 2030 2050 2070 2090 2110 2130 2150

Year

Lan

d c

over

(%)

non-forest

exploited

unexploited

Projected land cover in country Star

BUSINESS AS USUAL

0

10

20

30

40

50

60

70

80

90

100

1990 2010 2030 2050 2070 2090 2110 2130 2150

Year

La

nd

co

ve

r (%

)

non-forested

exploited

unexploited

0%

20%

40%

60%

80%

100%

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100 2110 2120 2130 2140 2150

Year

La

nd

co

ve

r (

%)

non-forest

exploited

unexploited

Projected land cover in country Diamond,

BUSINESS AS USUAL

0%

20%

40%

60%

80%

100%

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100 2110 2120 2130 2140 2150

Year

La

nd

co

ve

r (%

)

non-forest

exploited

unexploited

Projected land cover in country Triangle,

BUSINESS AS USUAL

Projected land cover in country Pentagon,

BUSINESS AS USUAL

Country Pentagon

0

20

40

60

80

100

1990 2010 2030 2050 2070 2090 2110 2130 2150

Year

Perc

enta

ge L

and A

rea

Projected land cover in country Oval,

BUSINESS AS USUAL

Country Oval

0

20

40

60

80

100

1990 2010 2030 2050 2070 2090 2110 2130 2150

Year

Perc

enta

ge L

and A

rea

0%

20%

40%

60%

80%

100%

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100 2110 2120 2130 2140 2150

Year

La

nd

co

ve

r (%

)

non-forest

exploited

unexploited

Projected land cover in country Circle,

BUSINESS AS USUAL

Projected land cover in country Oblong

BUSINESS AS USUAL

0

10

20

30

40

50

60

70

80

90

100

1990 2010 2030 2050 2070 2090 2110 2130 2150

Year

La

nd

co

ve

r (%

)

non-forest

exploited

unexploited

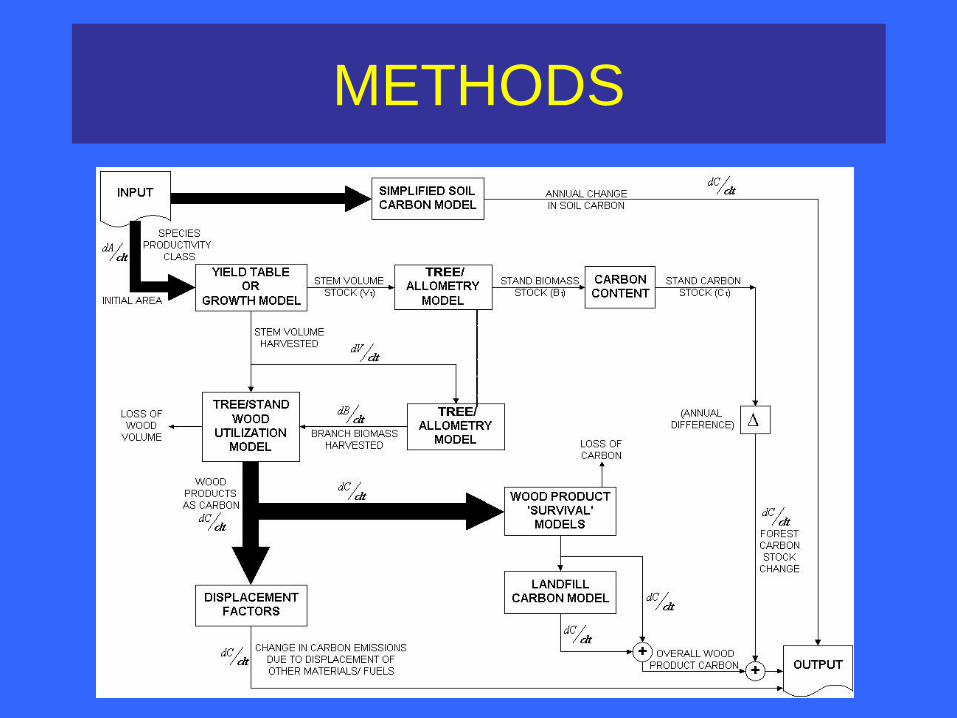

METHODS

METHODS

LULUCF Accounting:

Real-time, One-off, Benchmark, Simplified

benchmark.

Tonne-year, Advanced tonne-year, Rental

HWP Accounting:

IPCC, Stock Change, Production, Atmospheric Flow

METHODS

Article 3.7:

Strict interpretation, gross-net, net-net

Baselines:

Zero, 1990 value, 1990 projection, BAU projection

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

2060

2065

2070

2075

2080

2085

2090

2095

2100

2105

2110

2115

2120

2125

2130

2135

2140

2145

2150

Year

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

Default BAU Projection : Country Circle

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

2060

2065

2070

2075

2080

2085

2090

2095

2100

2105

2110

2115

2120

2125

2130

2135

2140

2145

2150

Year

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

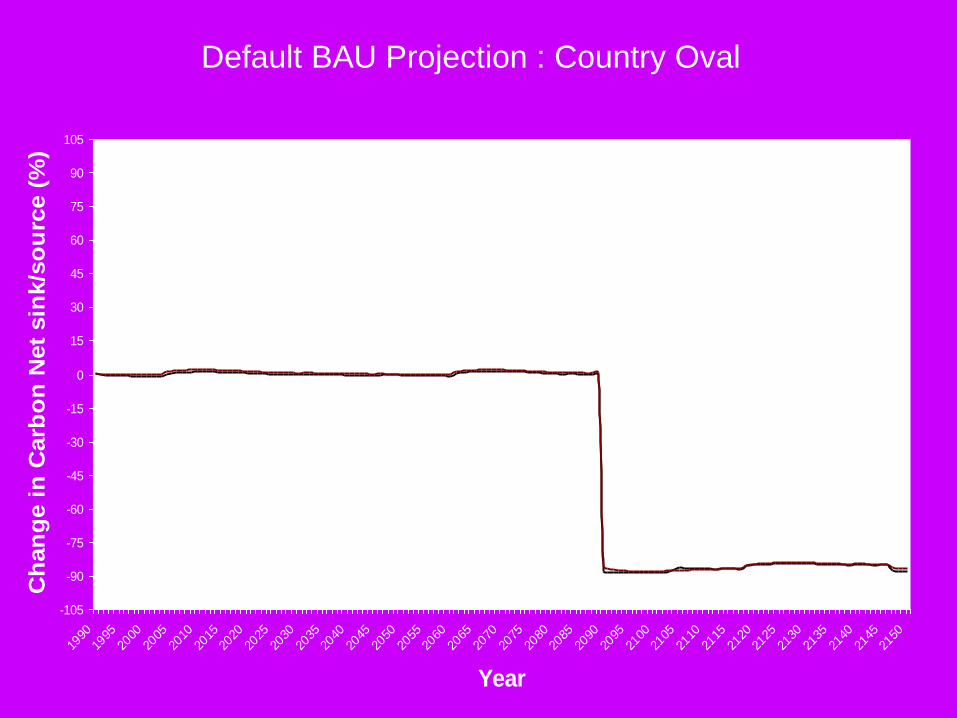

Default BAU Projection : Country Oval

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

2060

2065

2070

2075

2080

2085

2090

2095

2100

2105

2110

2115

2120

2125

2130

2135

2140

2145

2150

Year

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

Default BAU Projection : Country Trapezium

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

19901995

20002005

20102015

20202025

20302035

20402045

20502055

20602065

20702075

20802085

20902095

21002105

21102115

21202125

21302135

21402145

2150

Year

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

Default BAU Projection : Country Oblong

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

2060

2065

2070

2075

2080

2085

2090

2095

2100

2105

2110

2115

2120

2125

2130

2135

2140

2145

2150

Year

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

Default BAU Projection : Country Diamond

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

2060

2065

2070

2075

2080

2085

2090

2095

2100

2105

2110

2115

2120

2125

2130

2135

2140

2145

2150

Year

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

Default BAU Projection : Country Star

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

2060

2065

2070

2075

2080

2085

2090

2095

2100

2105

2110

2115

2120

2125

2130

2135

2140

2145

2150

Year

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

Default BAU Projection : Country Pentagon

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

19901995

20002005

20102015

20202025

20302035

20402045

20502055

20602065

20702075

20802085

20902095

21002105

21102115

21202125

21302135

21402145

2150

Year

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

Default BAU Projection : Country Triangle

-105

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

0 1 2 3 4

Calculation method

Ch

an

ge i

n C

arb

on

Net

sin

k/s

ou

rce (

%)

Star

Oval

Trapezium

Oblong

Triangle

Diamond

Circle

Pentagon

Influence of percentage calculation method 2008 - 2012

Net-net Gross-net Article 3.7

Influence of percentage calculation method 1990-2150

Net-net Gross-net Article 3.7

-100

-75

-50

-25

0

25

50

75

100

0 1 2 3 4

Article 3.7 calculation

Change in N

et carb

on s

ink/s

ourc

e

(%)

Star

Oval

Trapezium

Oblong

Triangle

Diamond

Circle

Pentagon

-100

-75

-50

-25

0

25

50

75

100

0 1 2 3 4 5 6 7 8 9

Country

Change in C

arb

on N

et sin

k/sourc

e

(%)

The impact of accounting for HWP, 2008-2012

-100

-75

-50

-25

0

25

50

75

100

0 1 2 3 4 5 6 7 8 9

Country

Ch

ange in C

arb

on N

et sin

k/s

ourc

e

(%)

The impact of accounting for HWP, 1990-2150

Impact of accounting indices, zero baseline

(1990-2150)

-105-90-75-60-45-30-15

0153045607590

105

0 1 2 3 4 5 6 7 8

Accounting index

Change in N

et carb

on

sin

k/s

ourc

e (

%)

Star

Oval

Trapezium

Oblong

Triangle

Diamond

Circle

Pentagon

Impact of accounting indices, zero baseline

(2008-2012)

-105

-85-65

-45-25

-515

3555

7595

0 1 2 3 4 5 6 7 8

Accounting index

Ch

ange in N

et carb

on

sin

k/s

ourc

e (

%)

Star

Oval

Trapezium

Oblong

Triangle

Diamond

Circle

Pentagon

Impact of accounting indices, 1990 value

Graph 7 (1990-2150)

-105-90-75-60-45-30-15

0153045607590

105

0 1 2 3 4 5 6 7 8

Accounting index

Ch

ange in N

et carb

on

sin

k/s

ourc

e (

%)

Star

Oval

Trapezium

Oblong

Triangle

Diamond

Circle

Pentagon

Impact of accounting indices, 1990 value

(2008-2012)

-100

-75

-50

-25

0

25

50

75

100

0 1 2 3 4 5 6 7 8

Accounting index

Ch

ange in N

et carb

on

sin

k/s

ourc

e (

%)

Star

Oval

Trapezium

Oblong

Triangle

Diamond

Circle

Pentagon

Impact of accounting indices, 1990 projection

(1990-2150)

-105-90-75-60-45-30-15

0153045607590

105

0 1 2 3 4 5 6 7 8

Accounting index

Ch

ange in N

et carb

on

sin

k/s

ourc

e (

%)

Star

Oval

Trapezium

Oblong

Triangle

Diamond

Circle

Pentagon

Impact of accounting indices, 1990 projection

(2008-2012)

-105-90-75-60-45-30-15

0153045607590

105

0 1 2 3 4 5 6 7 8

Accounting index

Ch

ange in N

et carb

on

sin

k/s

ourc

e (

%)

Star

Oval

Trapezium

Oblong

Triangle

Diamond

Circle

Pentagon

CONCLUSIONS

• If LULUCF is to be included in the Kyoto Protocol, the

accounting procedures can, indeed must, be kept as

simple as possible, otherwise anomalous results and

perverse incentives will arise.

• Tonne year understates the role of LULUCF.

• Article 3.7 appears to be acceptable.

CONCLUSIONS

•Carbon sequestration in wood products is not

as important at global level, as had been

thought.

•The differences in calculation methods for

HWP is small, apart from Atmospheric Flow

which is pessimistic.

•Need to look at the longer term impacts,

rather than the first accounting period only.

FUTURE WORK

•Explore the forest area constraints.

•Periodically re-set the year for the assigned

amount.

•Examine the impact of changes in land use

policy.

•Include the CDM.