ed5 im - solutions manual

TRANSCRIPT

Solutions

End-of-Chapter

Questions and Problems

to accompany

Multinational Finance

by Kirt C. Butler

Fifth Edition (2012) John Wiley & Sons

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

1

PART I Overview and Background

Chapter 1 An Introduction to Multinational Finance

Answers to Conceptual Questions

1.1 List the MNC’s key stakeholders. How does each have a stake in the MNC?

Stakeholders narrowly defined include shareholders, debtholders, and management. More broadly defined, stakeholders also would include employees, suppliers, customers, host governments, and residents of host countries.

1.2 In what ways do cultural differences impact the conduct of international business?

Because they define the rules of the game, national business and popular cultures impact each of the functional disciplines of business from research and development right through to marketing, production, and distribution.

1.3 What is country risk? Describe several types of country risk one might face when conducting business in another country.

Country risks refer to the political and financial risks of conducting business in a particular foreign country. Country risks include foreign exchange risk, political risk, and cultural risk.

1.4 What is political risk?

Political risk is the risk that a sovereign host government will unexpectedly change the rules of the game under which businesses operate.

1.5 What is foreign exchange risk?

Foreign exchange risk is the risk of unexpected changes in foreign currency exchange rates.

1.6 What investment opportunities might MNCs enjoy that are not available to local firms?

Operating cash flows can be increased by increasing revenues or decreasing operating expenses. The text mentions revenue enhancing opportunities such as global branding, advantages of size and scope, and flexibility in marketing and distribution; operating cost reductions through access to low-cost labor or raw materials, flexibility in sourcing or production, and economies of scale or vertical integration; and business strategies such as follow the customer, lead the customer, follow the leader, and building capacity directly in a foreign market (going local).

1.7 How can MNCs can reduce operating expenses relative to domestic firms.

MNCs can enjoy several advantages over domestic firms including global brands, size, and flexibility in marketing and distribution. Strategies for enhancing revenues include follow the customer, lead the customer, follow the leader, and establishing local production. Operating costs can be reduced through access to low-cost raw materials and labor, flexibility in sourcing, production, or site selection, and economies of scale or vertical integration.

1.8 What are the perfect financial market assumptions? What is their implication for multinational financial management.

In a perfect market, rational investors have equal access to prices and information in a frictionless market. If financial policy is to increase firm value, it must increase expected cash flows or decrease the discount rate in a way that cannot be replicated by investors. MNCs are in a better position than domestic firms to take advantage of financial market imperfections through financial market arbitrage, hedging policy, access to international sources of capital, and multinational tax strategy.

1.9 Describe the ways in which multinational financial management is different from domestic financial management.

Multinational financial management is conducted in an environment that is influenced by more than one cultural, social, political, or economic environment.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

2

Chapter 2 World Trade and the International Monetary System

Answers to Conceptual Questions

2.1 List one or more trade pacts in which your country is involved. Do these trade pacts affect all residents of your country in the same way? On balance, are these trade pacts good or bad for residents of your country?

Figure 2.1 lists the major international trade pacts. The World Trade Organization (WTO) is a supranational organization that oversees the General Agreement on Tariffs and Trade (GATT). Important regional trade pacts include the North American Free Trade Agreement (NAFTA includes the U.S., Canada, and Mexico), the European Union (EU), and the Asia-Pacific Economic Cooperation pact (APEC encompasses most countries around the Pacific Rim including Japan, China, and the United States). Trade pacts are designed to promote trade, but industries that have been protected by local governments can find that they are uncompetitive when forced to compete in global markets.

2.2 Do countries tend to export more or less of their gross national product today than in years past? What are the reasons for this trend?

Most countries export more of their gross national product today than in years past. Reasons include: a) the global trend toward free market economies, b) the rapid industrialization of some developing countries, c) the breakup of the former Soviet Union and the entry of China into international trade, d) the rise of regional trade pacts and the General Agreement on Tariffs and Trade, and e) advances in communication and in transportation.

2.3 How has globalization in the world’s goods markets affected world trade? How has globalization in the world’s financial markets affected world trade?

Some of the economic consequences of globalization in the world’s goods markets include: a) an increase in cross-border investment in real assets (land, natural resource projects, and manufacturing facilities), b) an increasing interdependence between national economies leading to global business cycles that are shared by all nations, and c) changing political risk for multinational corporations as nations redefine their borders as well as their national identities. The demise of capital flow barriers in international financial markets has had several consequences including: a) an increase in cross-border financing as multinational corporations raise capital in whichever market and in whatever currency offers the most attractive rates, b) an increasing number of cross-border partnerships including many international mergers, acquisitions, and joint ventures, and c) increasingly interdependent national financial markets.

2.4 What distinguishes developed, less developed, and newly industrializing economies?

Developed economies have a well-developed manufacturing base. Less developed countries (LDCs) lack this industrial base. Countries that have seen recent growth in their industrial base are called newly industrializing countries (NICs).

2.5 Describe the International Monetary Fund’s balance-of-payments accounting system.

The IMF publishes a monthly summary of cross-border transactions that tracks each country’s cross-border flow of goods, services, and capital.

2.6 How would an economist categorize exchange rate systems? How would the IMF make this classification? In what ways are these the same? How are they different?

Economists have traditionally classified exchange rate systems as either fixed rate or floating rate systems. The IMF has adapted this system to the plethora of systems in practice today. The IMF’s classification scheme includes “more flexible,” “limited flexibility,” and “pegged” exchange rate systems.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

3

2.7 Describe the Bretton Woods agreement. How long did the agreement last? What forced its collapse?

After World War II, representatives of the Allied nations convened at Bretton Woods, New Hampshire to stabilize financial markets and promote world trade. Under Bretton Woods’ “gold exchange standard,” currencies were pegged to the price of gold (or to the U.S. dollar). Bretton Woods also created the International Monetary Fund and the International Bank for Reconstruction and Development (the World Bank). The Bretton Woods fixed exchange rate system lasted until 1970, when high U.S. inflation relative to gold prices and to other currencies forced the dollar off the gold exchange standard.

2.8 What factors contributed to the Mexican peso crisis of 1995 and to the Asian crises of 1997?

In each instance, the government tried to maintain the value of the local currency at artificially high levels. This depleted foreign currency reserves. Local businesses and governments were also borrowing in non-local currencies (primarily the dollar), which heavily exposed them to a drop in the value of the local currency.

2.9 What is moral hazard and how does it relate to IMF rescue packages?

Moral hazard occurs when the existence of a contract changes the behaviors of parties to the contract. When the IMF assists countries in defending their currencies, it changes the expectations and hence the behaviors of lenders, borrowers, and governments. For example, lenders might underestimate the risks of lending to struggling economies if there is an expectation that the IMF will intervene during difficult times.

2.10 What were the causes and consequences of the global financial crisis of 2008?

Securitization of U.S. home loans combined with lax U.S. credit standards to create a subprime crisis in the market for collateralized debt obligations (CDOs). This subprime crisis impaired liquidity in the CDO market and eventually spilled over to other markets including real estate, stocks, bonds, other credit markets. Many governments had budget deficits from the drop in tax revenues and the increase in expenses from fiscal stimulus programs. Some governments (e.g., Greece and Iceland) saw their bond prices fall because of the increased perception of default risk.

Problem Solutions

2.1 This open-ended question is intended to engage the student and bring their knowledge up-to-date. Useful websites are listed on the inside-front cover of the text, and include:

Bank for International Settlements www.bis.org International Monetary Fund (IMF) www.imf.org World Trade Organization (WTO) www.wto.org International Labor Organization www.ilo.org International Chamber of Commerce www.iccwbo.org Michigan State University Global Edge globaledge.msu.edu United Nations www.un.org United Nations’ Commission on International Trade Law www.uncitral.org World Bank www.worldbank.org World Bank’s Multilateral Investment Guarantee Agency www.miga.org World Economic Forum www.weforum.org

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

4

Chapter 3 Foreign Exchange and Eurocurrency Markets

Answers to Conceptual Questions

3.1 Define liquidity.

Liquidity: the ease with which you can exchange an asset for another asset of equal value.

3.2 What is the difference between a money market and a capital market?

Money markets are markets for financial assets and liabilities of short maturity, usually considered to be less than one year. Capital markets are markets for financial assets and liabilities with maturities greater than one year.

3.3 What is the difference between an internal and an external market?

Debt placed in an internal market is denominated in the currency of a host country and placed within that country. Debt placed in an external market is placed outside the borders of the country issuing the currency.

3.4 What is the Eurocurrency market and what is its function?

The Eurocurrency market is an external credit market in bank deposits and loans. Like a national credit market, the Eurocurrency market permits the transfer of value over time in a given currency.

3.5 In what way is the Eurocurrency market different from an internal credit market?

There are typically no reserve requirements, interest rate regulations or caps, withholding taxes, deposit insurance requirements, or regulations influencing credit allocation decisions. There are also less stringent disclosure requirements.

3.6 What is the London Interbank Offer Rate (LIBOR)?

LIBOR is the rate at which a Euromarket bank offers to make a loan to another Euromarket bank.

3.7 What are the Basel Accords? What effects have they had on international banks?

The first Basel Accord – now called Basel I – set out to establish regulations governing the capital adequacy of financial institutions such as commercial banks. Basel I required that banks set aside equity capital as a protection against the credit risk of the banks’ loan portfolios. Basel II further refined this framework by assessing credit risk based on internal or external ratings. This increased capital requirements, and unfortunately contributed to the 2008 global financial crisis and reducing bank lending just at the time that credit was most needed. Basel III responded to the problems of the 2008 crisis by further refining the Basel Accords’ review of bank capital adequacy, leverage, and liquidity, with a focus on creating policies that are countercyclical to economic fluctuations.

3.8 What is the difference between spot and forward markets for foreign exchange?

In the spot market, trades are for immediate delivery. In the forward market, trades are for future delivery according to an agreed-upon delivery date, exchange rate, and amount.

3.9 What is Rule #1 when dealing with foreign exchange? Why is it important?

Rule #1 says to “Keep track of your currency units.” It is important because foreign exchange prices have a currency in both the numerator and the denominator. Most prices (for instance, a $15,000/car price on a new car) have a non-currency asset in the denominator and a currency in the numerator.

3.10 What is Rule #2 when dealing with foreign exchange? Why is it important?

Rule #2 says to “Always think of buying or selling the currency in the denominator of a foreign exchange quote.” The importance of this rule is related to that of Rule #1. Foreign exchange quotes have a currency in both the numerator and the denominator. The rule “buy low and sell high” only works for the currency in the denominator.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

5

3.11 What are the functions of the foreign exchange market?

Currency markets transfer purchasing power from one currency to another, either today (in the spot market) or at a future date (in the forward market). When used with Eurocurrency markets, foreign exchange markets allow investors to move value both across currencies and over time. Foreign exchange markets also facilitate hedging and speculation.

3.12 Define operational, informational, and allocational efficiency.

Operational efficiency refers to how large an influence transactions costs and other market frictions have on a market’s operation. Informational efficiency refers to whether or not prices reflect value. Allocational efficiency refers to how efficiently a market channels capital toward its most productive uses.

3.13 What is a forward premium? What is a forward discount?

A currency is trading at a forward premium when the nominal value of that currency in the forward market is higher than in the spot market. A currency is trading at a forward discount when the nominal value of that currency in the forward market is lower than in the spot market.

3.14 Describe the empirical behavior of exchange rates.

Over daily intervals, spot rate changes are random with a nearly equal probability of rising or falling. As the forecast horizon is lengthened, the correlation between interest and inflation differentials and nominal spot rate changes rises. Eventually, the international parity conditions exert themselves and the forward rate begins to dominate the current spot rate as a predictor of future nominal exchange rates. Finally, exchange rate volatility is not constant. Instead, volatility comes in waves.

Problem Solutions

3.1 a. The bid is less than the offer, so Citicorp is quoting the currency in the denominator. Citicorp is buying dollars at the DKK5.62/$ bid rate and selling dollars at the DKK5.87/$ offer rate.

b. In American terms, the bid price is $0.1704/DKK and the ask price is $0.1779/DKK. Citicorp is buying and selling the kroner at these quotes.

c. In direct terms, the bid quote for the dollar is $0.1779/DKK and the ask price is $0.1704/DKK. Citicorp is buying dollars at $0.1779/DKK (which is equivalent to DKK5.62/$) and selling dollars at $0.1704/DKK (or DKK5.87/$).

d. The bank will receive the bid-ask spread on each dollar. When buying one million dollars at DKK5.62/$ and selling one million dollars at DKK5.87/$, the bank’s profit on the bid-ask spread will be (DKK5.87/$–DKK5.62/$)($1,000,000) = DKK250,000.

3.2 The ask price is higher than the bid, so these are rates at which the bank is willing to buy or sell dollars (in the denominator). You’re selling dollars, so you’ll get the bank’s dollar bid price. You need to pay SKr10,000,000/(SKr7.5050/$) ≈ $1,332,445.

3.3 The U.S. dollar (in the denominator) is selling at a forward premium, so the Canadian dollar must be selling at a forward discount. Annualized forward premia on the U.S. dollar are:

Bid ($) Ask ($) Six months forward +0.681% +0.761%

Percent per annum on the Canadian dollar from the U.S. perspective are as follows:

Bid (C$) Ask (C$) Six months forward –0.678% –0.758%

The premiums/discounts on the two currencies are opposite in sign and nearly equal in magnitude. Forward premiums and discounts are of slightly different magnitude because the bases (U$ vs. C$) on which they are calculated are different. Forward premiums/discounts are as stated above regardless of where a trader resides.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

6

3.4 a. The forward premium is equal to (F1$/¥ – S0

$/¥) = ($0.008772945/¥ – $0.009057355/¥) = –$0.000284410/¥, or –2.8441 basis points. As a percentage over the 90-day period, this is

(F1$/¥ – S0

$/¥) / S0$/¥ = –0.031401, or –3.1401 percent.

b. As an annualized forward premium following the U.S. convention, this is equal to (n)(F1

$/¥–S0$/¥)/S0

$/¥ = (4)(–0.031401) = –0.125604, or –12.5604 percent. c. As an APR, the premium is (F1

$/¥/S0$/¥)4–1 = –0.119811, or –11.9811 percent.

3.5 1984 DM1.80/$ or $0.56/DM 1987 DM2.00/$ or $0.50/DM 1992 DM1.50/$ or $0.67/DM 1997 DM1.80/$ or $0.56/DM a. 1984-87 The dollar appreciated 11.1%; ((DM2.0/$)–(DM1.8/$)/(DM1.8/$) = +0.111 1987-92 The dollar depreciated 25%; ((DM1.5/$)–(DM2.0/$)/(DM2.0/$) = –0.25 1992-97 The dollar appreciated 20%; ((DM1.8/$)–(DM1.5/$)/(DM1.5/$) = +0.20 b. 1984-87 The mark depreciated 10.7%; ($0.50/DM)/($0.56/DM)–1= –0.107

1987-92 The mark appreciated 34.0%; ($0.67/DM)/($0.50/DM)–1= +0.340 1992-97 The mark depreciated 16.4%; ($0.56/DM)/($0.67/DM)–1 = –0.164

3.6 a. (PZ5,000,000) / (PZ4.0200/$) = $1,243,781. Warsaw’s bid price for PZ is its ask price for dollars. So, PZ4.0200/$ is equivalent to $0.2488/PZ.

b. (PZ20,000,000) / (PZ3.9690/$) = $5,039,053 PZ3.9690/$ is equivalent to $0.2520/PZ Payment is made on the second business day after the 3-month expiration date.

3.7 You initially receive P0$ = P0

¥/S0¥/$ = (¥104,000,000)/(¥104/$) = $1 million. When you buy back

the yen, you pay P1$ = P1

¥/S1¥/$ = (¥104,000,000)/(¥100/$) = $1.04 million. Your loss is $40,000.

3.8 When buying one currency, you are simultaneously selling another, so a yen bid price is a euro ask price. Yen quotes yield S¥/€ = 1/S€/¥ = 1/(€0.007634/¥) = ¥130.99/€ and S¥/€ = 1/(€0.007643/¥) = ¥130.84/€, so euro quotes (in the denominator) are ¥130.84/€ BID and ¥130.99/€ ASK.

3.9 a. (1+s¥/$) = 0.90 = 1/(1+s$/¥) s$/¥ = (1/0.90)–1 = +0.111, or an 11.1% appreciation. b. (1+sRbl/$) = 11 = 1/(1+s$/Rbl) s$/Rbl = (1/11)–1 = –0.909, or a 90.9% depreciation.

3.10 The 90-day dollar forward price is 33 bps below the spot price: F1SFr/$–S0

SFr/$ = (SFr0.7432/$–SFr0.7465/$) = –SFr0.0033/$. The percentage dollar forward premium is (F1

SFr/$–S0SFr/$)/S0

SFr/$ = (SFr0.7432/$–SFr0.7465/$)/(SFr0.7465/$) = –0.442% per 90 days, or (–0.442%)×4 = –1.768% on an annualized basis.

3.11 Banks make a profit on the bid-ask spread. A bank quoting $0.5841/SFr BID and $0.5852/SFr ASK is buying francs (in the denominator) at $0.5841/SFr and selling francs at $0.5852/SFr ASK. A bank quoting $0.5852/SFr BID and $0.5841/SFr ASK is buying dollars (in the numerator) at $0.5852/SFr BID and selling dollars at $0.5841/SFr ASK. Hence, these are equivalent.

3.12 DKK is at a forward discount 30 day: ($0.18519/DKK–$0.18536/DKK)/$0.18536/DKK = –0.092% 90 day: ($0.18500/DKK–$0.18536/DKK)/$0.18536/DKK = –0.194% 180 day: ($0.18488/DKK–$0.18536/DKK)/$0.18536/DKK = –0.259%

3.13 a. S1$/¥ = S0

$/¥ (1+ s$/¥) = ($0.0100/¥)(1.2586) = ($0.012586/¥) b. (1+ s¥/$) = S1

¥/$/S0¥/$ = (1/S1

$/¥) / (1/S0$/¥) = 1 / (S1

$/¥/S0$/¥) = 1 / (1+ s$/¥)

= 1 / (1.2586) = 0.7945, so s$/¥ = 0.7945 – 1 = –.2055, or = –20.55%

3.14 (Ftd/f–S0

d/f)/S0d/f = [(1/Ft

f/d)–(1/S0f/d)]/(1/S0

f/d) = [(S0f/d/Ft

f/d)–(S0f/d/S0

f/d)]/(S0f/d/S0

f/d) = [(S0

f/d /Ftf/d) – 1] = (S0

f/d – Ftf/d) / Ft

f/d.

3.15 σt2 = (0.0034) + (0.40)(0.05)2 + (0.20)(0.10)2 = 0.0064 σt = 0.08, or 8%.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

7

Chapter 4 The International Parity Conditions

Answers to Conceptual Questions

4.1 What is the law of one price?

The law of one price states identical assets must have the same price wherever they are bought or sold. The law of one price is enforced by arbitrage activity between identical assets. In a perfect market without transaction costs, the law of one price must hold for there to be no arbitrage opportunities.

4.2 What is an arbitrage profit?

Arbitrage profit is a profit obtained through the simultaneous purchase and sale of the same or equivalent securities such that there is no net investment or risk. Arbitrage will drive the prices of identical assets into equilibrium and enforce the law of one price.

4.3 What is the difference between locational, triangular, and covered interest arbitrage?

Locational arbitrage is conducted between two physical locations, such as between currency prices at two different banks (such that ASf/d BSd/f 1 for banks A and B and currencies d and f). Triangular arbitrage is conducted across three different cross exchange rates (such that Sd/e Se/f Sf/d 1 for currencies d, e, and f). Covered interest arbitrage takes advantage of a disequilibrium in the interest rate parity condition [(Ft

d/ f) / (S0d/ f)] (1+id) / (1+i f)]t between currency and Eurocurrency markets.

4.4 Is interest rate parity a reliable relation in the interbank markets?

Interest rate parity is a reliable relation in the interbank markets. Each of the prices in the IRP relation (Ft

d/f/S0d/ f) = [(1+id)/(1+i f)]t is a traded contract in the interbank markets, and so covered interest

arbitrage is able to enforce the no-arbitrage condition within the bounds of transaction costs (which are small in the interbank market).

4.5 What is relative purchasing power parity?

Relative purchasing power parity is a form of the law of one price in which the expected change in the spot exchange rate is influenced by the difference in expected inflation according to E[St

d/f]/S0d/f =

[(1+E[pd])/(1+E[pf])]t.

4.6 Are forward exchange rates good predictors of future spot rates?

Forward rates are poor predictors of future spot rates over short-term forecast horizons, because exchange rate volatility masks the signal from the international parity condition. Over longer forecast horizons, the signal-to-noise ratio improves and the forecast performance of forward rates (as well as inflation differentials from RPPP) improves.

4.7 What does the international Fisher relation say about interest rate and inflation differentials?

If real interest rates are constant across currencies, nominal interest rates should reflect inflation differentials according to [(1+id) / (1+if)]t = [(1+E[pd]) / (1+E[pf])]t.

4.8 What are real changes in exchange rates?

Real exchange rate changes reflect changes in currencies’ relative purchasing power.

4.9 Are real exchange rates in equilibrium at all times?

Real exchange rates show large and persistent deviations from purchasing power parity. These deviations can last for several years.

4.10 What is the effect of a real appreciation of the domestic currency on the purchasing power of domestic residents?

A real appreciation of the domestic currency increases the wealth and purchasing power of domestic residents relative to foreign residents. It can also hurt the economy by raising the price of domestic goods relative to foreign goods.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

8

4.11 Will an appreciation of the domestic currency help or hurt a domestic exporter?

A nominal appreciation in the domestic currency is likely to have little effect on domestic importers and exporters. A real appreciation of the domestic currency can hurt domestic exporters by raising the price of domestic goods relative to foreign goods. Domestic importers will see their purchasing power increase relative to foreign competitors, and so are likely to be helped by a real appreciation of the domestic currency.

4.12 Describe the behavior of real exchange rates.

Although real exchange rates revert to their long run average, in the short run there can be substantial deviations from purchasing power parity and the long run average.

4.13 What methods can be used to forecast future spot rates of exchange?

Market-based forecasts are obtained from forward exchange rates or from interest rate parity when forward prices are unavailable. Model-based forecasts can be generated from technical analysis (analyzing patterns in exchange rates) or from fundamental analysis (from a larger set of economic relationships).

4.14 How can the international parity conditions allow you to forecast next year’s spot rate?

In theory, any of the international parity conditions could be used: E[Std/f]/S0

d/f = Ftd/f/S0

d/f = [(1+id)/(1+if)]t = [(1+E[pd])/(1+E[pf])]t. In practice, forward rates are usually used to predict spot rates. At the least, forwards have the advantage of reflecting the opportunity costs of capital through the interest rate parity relation, Ft

d/f/S0d/f = [(1+id)/(1+if)]t.

Problem Solutions

4.1 a. S¥SFr = S¥/$S$/SFr = (¥200/$)($0.50/SFr) = ¥100/SFr b. S¥SFr = S¥/$/SSFr/$ =(¥100/$)/(SFr1.60/$) = ¥62.5/SFr

4.2 SSFr/$ S$/¥ S¥/SFr = 1.0326 > 1. Spot rates are “too high” relative to the parity condition, so you should sell the currencies in the denominators for the currencies in the numerators at the relatively high prices. This means that you should a) sell dollars for francs, b) sell yen for dollars, and c) sell francs for yen. Alternatively, a) buy francs with dollars, b) buy dollars with yen, and c) buy yen with francs. Triangular arbitrage would yield a profit of 3.26 percent of the starting amount. For triangular arbitrage to be profitable, transactions costs on a “round turn” cannot be more than this amount.

4.3 Each of these prices is a traded contract in the interbank forex market, and so arbitrage (either bilateral or triangular) will ensure that the relations Ft

d/f(Y)/Fd/f(X) = 1 and Ftd/eFt

e/fFtf/d = 1 hold within the

bounds of transaction costs.

4.4 The forward price is at a 9 bp discount over six months, or 18 bps on an annualized basis. The six-month percentage premium is (F1

£/$/S0£/$)–1 = (£0.6352/$)/(£0.6361/$)–1 = 0.9986–1 = –0.14%, or a

discount of 0.28% on an annualized basis. Because Ft£/$ = E[St

£/$] according to forward parity (the unbiased forward expectations hypothesis), the spot rate is expected to depreciate by 0.14% over the next six months.

4.5 a. The percentage bid-ask spread depends on which currency is in the denominator. Tokyo quote for the peso: (¥28.77/MXN – ¥28.74/MXN)/(¥28.74/MXN) = 0.00104, or 0.104%. Mexico City quote for yen: (MXN0.03420/¥ – MXN0.03416/¥)/(MXN0.03416/¥) = 0.00117, or

0.117%. b. The Mexican bank’s yen quote can be converted into a quote for the Mexican peso as follows: S¥/MXN = 1/(MXN0.03416/¥) ≈ ¥29.27/MXN bid on the yen and ask on the peso. S¥/MXN = 1/(MXN0.03420/¥) ≈ ¥29.24/MXN ask on the yen and bid on the peso. So “MXN0.03416/¥ BID and MXN0.03420/¥ ASK” on the yen is equivalent to ¥29.24/MXN

BID and ¥29.27/MXN ASK on the Mexican peso. The winning strategy is to buy pesos (and sell yen) from the Tokyo bank at the ¥28.77/MXN ask

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

9

price for pesos and sell pesos (and buy yen) to the Mexican bank at the ¥29.24/MXN bid price for pesos. Buying pesos in Tokyo yields (¥1,000,000)/(¥28.77/MXN) = MXN34,758. Selling pesos in Mexico City yields (MXN34,758)(¥29.24/MXN) = ¥1,016,336. Your arbitrage profit is 16,336 yen, or about MXN559 at the Mexican bank’s ¥29.24/MXN bid price for pesos.

4.6 From the Fisher relation: (1+iCNY) = (1+E[pCNY])(1+E[ʀCNY]) E[ʀCNY]) = (1+iCNY)/(1+ E[pCNY]) – 1 = (1.071/1.05) – 1 = 0.0200, or 2 percent.

4.7 a. From interest rate parity, (¥210/$)/(¥190/$) = (1+i¥)/(1.15) i¥ = 27.11%. b. Because the forward rate of ¥210/$ is greater than the spot rate of ¥190/$, the dollar is at a forward

premium. If forward rates are unbiased predictors of future spot rates, the dollar is likely to appreciate against the yen by (¥210/$)/(¥190/$)–1 = 10.526%.

4.8 a. In this problem, we know the spot and forward rates and U.S. inflation. The real and nominal interest rates are not needed: F1

$/£/S0$/£ = ($1.20/£)/($1.25/£) = 0.96 = E(1+p$)/E(1+p£) =

(1.05)/E(1+p£) => E(p£) = (1.05/0.96)–1 = 9.375% b. From the Fisher equation: i£ = (1+p£)(1+ʀ£)–1 = (1.09375)(1.02)–1 = 11.56%.

4.9 a. E[P1D] = P0

D(1+pD) = D100(1.10) = D110 E[P1

F] = P0F(1+pF) = F1(1.21) = F1.21

E[S1D/F] = E[P1

D] / E[P1F] = D110 / F1.21 = D90.91/F.

b. E[P2D] = P0

D(1+pD)2 = D100(1.10)2 = D121 E[P2

F] = P0F(1+pF)2 = F1(1.21)2 = F1.4641

E[S2D/F] = E[P2

D]/E[P2F] = D121/F1.4641

= S0D/F[(1+pD)/(1+pF)]2 = (D100/F)(1.10/1.21)2 = D82.64/F.

4.10 a. A 7% annualized rate with quarterly compounding is equivalent to 7%/4 = 1.75% per quarter. From interest rate parity, the 3-month MR interest rate is FMR/$/SMR/$ = (MR3.9888/$)/(MR4.0200/$) = (1+iMR)/(1+i$) = (1+iMR)/(1+0.0175) => iMR = 0.009603, or 0.9603% per three months. Annualized, this is equivalent to (0.9603%)×4 = 3.8412% per year with quarterly compounding. Alternatively, the annual percentage rate is (1.009603)4–1 = 0.03897, or 3.897% per year.

b. $10,000,000 invested at the 3-month U.S. rate yields $10,175,000. Changed into MR at the forward rate, this is worth ($10,175,000)(MR3.9888/$) = MR40,586,040. You can finance your $10,000,000 by borrowing MR40,200,000. Your obligation on this contract will be (MR40,200,000)(1.009603) MR40,586,040 which is exactly offset by the proceeds from your forward contract.

4.11 a. FtBt/$/S0

Bt/$ = (1 + iBt)t/(1 + i$)t = (Bt 25.64/$)/(Bt 24.96/$) = (1 + iBt)/(1.06125) 1.02724 = (1 + iBt)/1.06125 iBt = 9.02% b. F1

Bt/$/S0Bt/$ = (Bt25.64/$)/(Bt24.96/$) = 1.027 < (1+iBt)/(1+i$) = (1.1)/(1.06125) = 1.037. So,

borrow at i$ and lend at iBt.

Bt24,960,000

$1,000,000

Convert to baht at the spot exchange rate

Bt27,456,000

Bt24,960,000

Invest at the 10% baht interest rate

$1,061,250

+$1,000,000 Borrow at the 6.125% dollar interest rate

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

10

This leaves a net gain at time 1 of $1,070,827 – $1,061,250 = $9,577, which is worth

$9,577/1.06125 = $9,024 in present value.

4.12 F1MXN/$/S0

MXN/$=(MXN11/$)/(MXN10/$)=1.1<1.1132=(1.18)/(1.06)=(1+iMXN)/(1+i$). The ratio of interest rates is too high and must fall, so borrow at the relatively low dollar rate and invest at the relatively high peso rate. Similarly, the forward premium is too low and must rise, so buy dollars (and sell pesos) at the relatively low forward rate for the dollar and sell dollars (and buy pesos) at the relatively high dollar spot rate.

- Borrow $1 million so that $1,060,000 is due in six months. - Sell $1 million and buy MXN10,000,000 at the relatively high spot price. - Invest MXN10,000,000 at 18% to yield MXN11,800,000 in six months. - Cover by selling MXN11,800,000 at the MXN11/$ forward rate to yield $1,072,727.

This leaves a profit of $1,072,727–$1,060,000 = $12,727 at time t=1 in six months.

4.13 The Singapore dollar is at a forward premium; F1$/S$/S0

$/S$ = ($0.51/S$)/($0.50/S$) = 1.02, or 2% per year. This is less than is warranted by the difference in interest rates (1+i$)/(1+iS$) = (1.06)/(1.04) = 1.019231, so F1

$/S$/S0$/S$ > (1+i$)/(1+iS$). The forward/spot ratio is too high and must fall, so sell S$

(and buy dollars) at the relatively high S$ forward rate and buy S$ (and sell dollars) at the relatively low S$ spot rate. Conversely, the ratio of interest rates is too low and must rise, so borrow at the relatively low dollar interest rate and invest at the relatively high S$ rate. (Even though S$ interest rates are lower than dollar interest rates in nominal terms, S$ interest rates are high and dollar interest rates are low relative to the forward/spot ratio.) Suppose you borrow ($1,000,000)/(1+i$) = $1,060,000 at i$ = 6.0%.

-$1,060,000

+$1,000,000

Convert to S$2,000,000 = ($1,000,000)/($0.50/S$) at S0$/S$ = $0.50/S$.

-$1,000,000

+S$2,000,000

Invest S$2,000,000 at the Singapore interest rate of iS$ = 4.0%.

-S$2,000,000

+S$2,080,000

Cover this S$ forward obligation by selling S$ in the forward market.

-S$2,080,000

+$1,060,800

The result is a dollar profit of $1,060,800–$1,060,000 = $800. These transactions are worth undertaking only if the costs of executing the four transactions is less than $800.

4.14 a. E[P1F] = P0

F(1+pF) = 1.21 E[P1

D] = P0D(1+pD) = 110

E[S1D/F] = (S0

D/F)(1+pD)/(1+pF) = (D100/F)(1.10/1.21) D90.91/F. b. Because nominal exchange rates should adjust to reflect changes in relative purchasing power, the

expected real exchange rate is 100% of the beginning rate: E[X1D/F] = (E[S1

D/F]/S0D/F)((1+pF)/(1+pD))

Bt27,456,000

$1,070,827Cover baht forward

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

11

= ((D90.91/F)/(D100/F))(1.21/1.10) = 1.00, or 100%. c. E[P2

F]) = P0F(1+pF)2 = F1.4641

E[P2D]) = P0

D(1+pD)2 = D121 E[P2

F]) = P0F(1+pF)2 = F1.4641

E[P2D]) = P0

D(1+pD)2 = D121 E[S2

D/F] = S0D/F((1+pD)/(1+pF))2 = (D100/F)(1.10/1.21)2 D82.64/F

The real exchange rate is not expected to change: E[X2D/F] = (E[S2

D/F]/E[S0D/F]) [(1+pF)/(1+pD)]2

= ((D82.64/F)(D100/F)) / (1.21/1.10)2 = 1.00, or 100%.

4.15 a. s¥/SFr = (S0¥/SFr)/(S–1

¥/SFr) –1 = (¥155/SFr)/(¥160/SFr) – 1 = –3.125%. b. From relative purchasing power parity, the spot rate should have been: E[S0

¥/SFr] = (S–1¥/SFr) [(1+p¥)/(1+pSFr)] = (¥160/SFr) [(1.02)/(1.03)] = ¥158.45.

c. As a difference from the expectation, the real change in the spot rate is: x¥/SFr = (Actual-Expected)/(Expected) = (S0

¥/SFr –E[S0¥/SFr])/E[S0

¥/SFr]) = (¥155/SFr–¥158.45/SFr)/¥158.45/SFr = –2.18%. Alternatively, change in the real exchange rate is equal to: x¥/SFr = ((S0

¥/SFr)/(S–1¥/SFr)) ((1+pSFr)/(1+p¥)) – 1

= ((¥155/SFr)/(¥160/SFr)) ((1.03)/(1.02)) – 1 = –2.18%. d. The franc depreciated by 2.18% in purchasing power. e. In real terms, the yen rose by xSFr/¥ = ((S0

SFr/¥) / (S–1SFr/¥)) ((1+p¥) / (1+pSFr)) – 1

= ((S0¥/SFr)–1 / (S–1

¥/SFr)–1) ((1+p¥) / (1+pSFr)) – 1 = ((¥155/SFr)–1 / (¥160/SFr)–1 ) ((1.02)/(1.03)) – 1 = +2.23% = ((SFr.0064516/¥)/(SFr.00625000/¥)) ((1.02)/(1.03)) – 1 = +2.23%. Because the SFr fell by 2.18% in real terms, the yen rose by 1/(1–0.0218) 2.23%.

4.16 a. technical analysis b. technical analysis c. fundamental analysis d. fundamental analysis e. technical analysis Appendix 4-A Continuous Time Finance

4A.1 Total two-period return is [V2/V0]–1 = [(1+i1)(1+i2)]–1. Mean geometric return is iavg = [(1+i1)(1+i2)]

1/2–1. Total wealth after two periods is the same as beginning wealth; $100(1+1)(1–0.5) = $100. Notice that the order of the rates of return does not matter. A loss of 50% followed by a gain of 100% leaves your initial value unchanged. For the pair of returns (100%,–50%), the average period return is iavg = [(1+1)(1–0.5)]1/2–1 = 0.

With continuously compounded returns, periodic rates are given by i1 = ln(1+i1) = ln(2) = +0.69315 and i2 = ln(1+i2) = ln(0.5) = –0.69315. The (arithmetic) average return using continuously compounded rates is (i1+ i2)/2 = (+0.69315–0.69315)/2 = 0. Either way, your ending value is the same as your beginning value. These methods are equivalent.

4A.2 Inflation rates are pD = ln(1+pD) = ln(1.10) = 9.531% and pF = ln(1+pF) = ln(1.21) = 19.062% in continuously compounded returns. Expected price levels and spot rates are:

E[P1D] = P0

D e(0.09531) = (D100)(1.10) = D110 E[P2

D] = P0D e(2)(0.09531) = (D100)(1.21) = D121

E[P1F] = P0

F e(0.19062) = (F1)(1.21) = F1.21 E[P2

F] = P0F e(2)(0.19062) = (F1)(1.4641) = F1.4641

E[S1D/F] = E[P1

D] / E[P1F] = D110 / F1.21 = D90.91/F

E[S2D/F] = E[P2

D] / E[P2F] = D121 / F1.4641 = D82.64/F

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

12

PART II Derivative Securities for Currency Risk Management

Chapter 5 Currency Futures and Futures Markets

Answers to Conceptual Questions

5.1 How do currency forward and futures contracts differ with respect to maturity, settlement, and the size and timing of cash flows?

Currency forward contracts are traded in an interbank market, have negotiated terms (maturity, amount, and collateral), and are traded with a bid-ask spread. Nearly all forward contracts are held until maturity. Currency futures contracts are exchange-traded, standardized instruments that are traded on a fee basis rather than with a bid-ask spread. Less than 5% of futures contracts are held until maturity.

5.2 What is the primary role of the exchange clearinghouse?

The Chicago Board of Trade Clearing Board’s slogan is “A party to every trade.” This is the primary role of a futures exchange. Users of futures always know the reputation and credit-worthiness of the party on the other side of the trade.

5.3 Draw and explain the payoff profile associated with a currency futures contract.

Payoff profiles for an underlying exposure and for the corresponding futures hedge:

5.4 What is a delta-hedge? a cross-hedge? a delta-cross-hedge?

When there is a maturity mismatch between an underlying transaction exposure and the expiration date of the nearest futures contract, the hedge that minimizes the variance in the hedged position is called a delta-hedge. When there is a currency mismatch but not a maturity mismatch, the variance-minimizing hedge is called a cross-hedge. When there is both a currency mismatch and a maturity mismatch, the variance-minimizing hedge is called a delta-cross-hedge.

5.5 What is the basis? What is basis risk?

The basis is the difference in nominal interest rates, (id–if). The relationship between futures prices and spot prices changes if interest rate levels in the two currencies rise and fall unexpectedly. The risk of unexpected change in the relationship between the futures prices and spot prices is called basis risk.

5.6 How do you measure the quality of a futures hedge?

The quality of a currency hedge is measured by the r-square of a regression of the underlying spot rate change on change in the appropriate futures contract. This measures the percentage variation in one variable that is explained by variation in another variable. If there is both a currency and a maturity mismatch, then hedge quality is measured by the r-square of st

d/f2 on futtd/f1, where d = the

Sd/f

Vd/f

Underlying exposure

Long the foreign currency

Sd/f

Vd/f

Futures hedge

Short the foreign currency

Sd/f

Vd/f

Underlying exposure

Short the foreign currency

Sd/f

Vd/f

Futures hedge

Long the foreign currency

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

13

domestic currency, f2 = the currency in which transaction exposure is denominated, and f1 = the currency used to hedge against st

d/f2. If there is neither a currency nor a maturity mismatch, then futures prices converge to spot prices at expiration and exposure to currency risk can be hedged exactly (an r-square of one) with a futures contract.

Problem Solutions

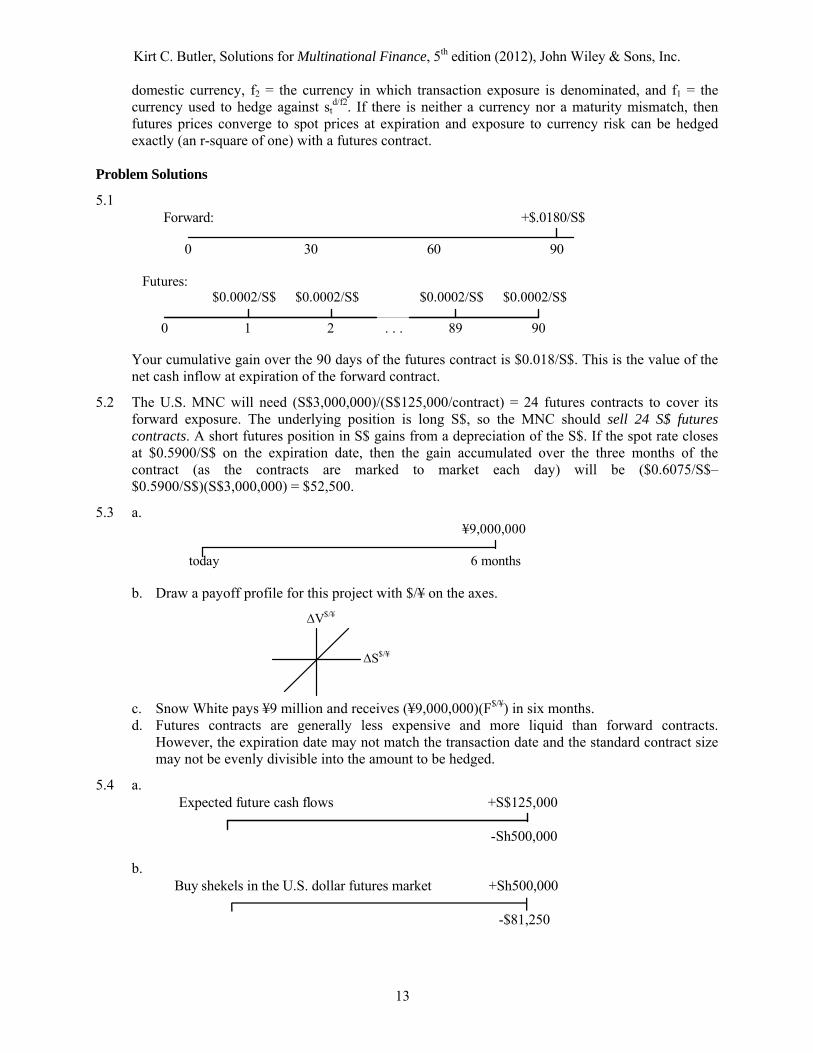

5.1

Forward: +$.0180/S$

0 30 60 90

Futures:$0.0002/S$ $0.0002/S$ $0.0002/S$ $0.0002/S$

0 1 2 . . . 89 90

Your cumulative gain over the 90 days of the futures contract is $0.018/S$. This is the value of the net cash inflow at expiration of the forward contract.

5.2 The U.S. MNC will need (S$3,000,000)/(S$125,000/contract) = 24 futures contracts to cover its forward exposure. The underlying position is long S$, so the MNC should sell 24 S$ futures contracts. A short futures position in S$ gains from a depreciation of the S$. If the spot rate closes at $0.5900/S$ on the expiration date, then the gain accumulated over the three months of the contract (as the contracts are marked to market each day) will be ($0.6075/S$–$0.5900/S$)(S$3,000,000) = $52,500.

5.3 a.

b. Draw a payoff profile for this project with $/¥ on the axes.

c. Snow White pays ¥9 million and receives (¥9,000,000)(F$/¥) in six months. d. Futures contracts are generally less expensive and more liquid than forward contracts.

However, the expiration date may not match the transaction date and the standard contract size may not be evenly divisible into the amount to be hedged.

5.4 a.

Expected future cash flows +S$125,000

-Sh500,000

b.

Buy shekels in the U.S. dollar futures market +Sh500,000

-$81,250

¥9,000,000

today 6 months

V$/¥

S$/¥

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

14

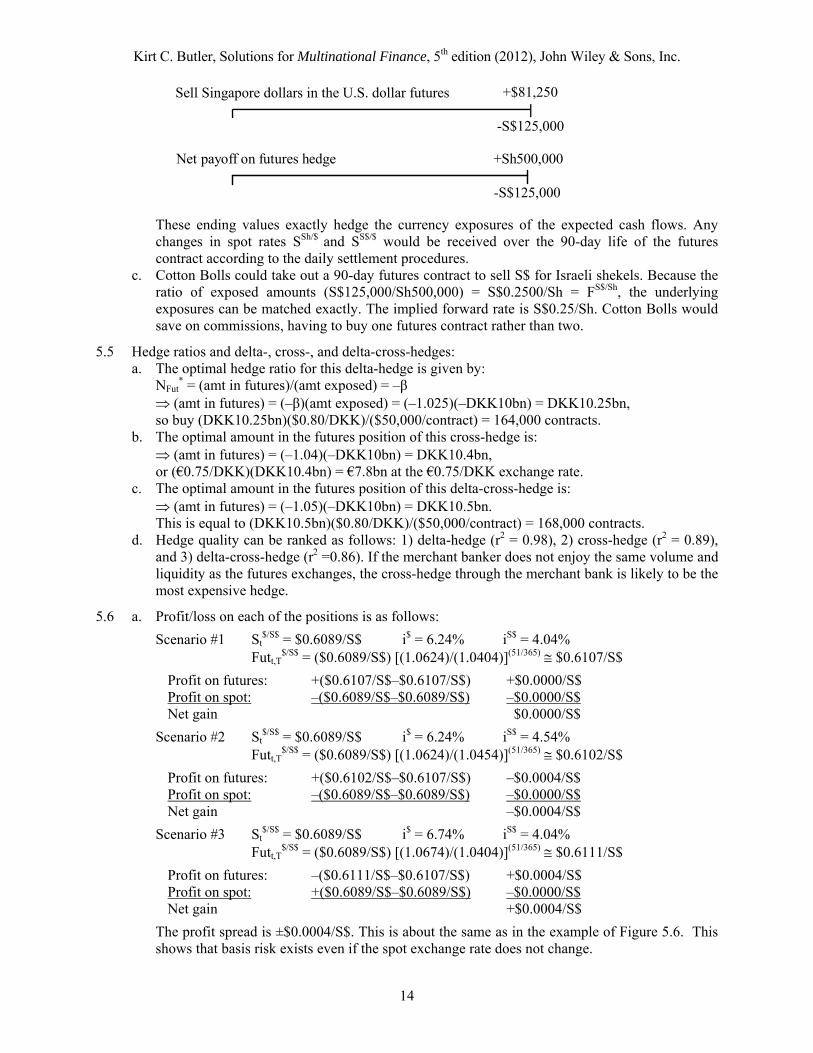

Sell Singapore dollars in the U.S. dollar futures +$81,250

-S$125,000

Net payoff on futures hedge +Sh500,000

-S$125,000

These ending values exactly hedge the currency exposures of the expected cash flows. Any changes in spot rates SSh/$ and SS$/$ would be received over the 90-day life of the futures contract according to the daily settlement procedures.

c. Cotton Bolls could take out a 90-day futures contract to sell S$ for Israeli shekels. Because the ratio of exposed amounts (S$125,000/Sh500,000) = S$0.2500/Sh = FS$/Sh, the underlying exposures can be matched exactly. The implied forward rate is S$0.25/Sh. Cotton Bolls would save on commissions, having to buy one futures contract rather than two.

5.5 Hedge ratios and delta-, cross-, and delta-cross-hedges: a. The optimal hedge ratio for this delta-hedge is given by: NFut

* = (amt in futures)/(amt exposed) = –β (amt in futures) = (–β)(amt exposed) = (–1.025)(–DKK10bn) = DKK10.25bn, so buy (DKK10.25bn)($0.80/DKK)/($50,000/contract) = 164,000 contracts. b. The optimal amount in the futures position of this cross-hedge is: (amt in futures) = (–1.04)(–DKK10bn) = DKK10.4bn, or (€0.75/DKK)(DKK10.4bn) = €7.8bn at the €0.75/DKK exchange rate. c. The optimal amount in the futures position of this delta-cross-hedge is: (amt in futures) = (–1.05)(–DKK10bn) = DKK10.5bn. This is equal to (DKK10.5bn)($0.80/DKK)/($50,000/contract) = 168,000 contracts. d. Hedge quality can be ranked as follows: 1) delta-hedge (r2 = 0.98), 2) cross-hedge (r2 = 0.89),

and 3) delta-cross-hedge (r2 =0.86). If the merchant banker does not enjoy the same volume and liquidity as the futures exchanges, the cross-hedge through the merchant bank is likely to be the most expensive hedge.

5.6 a. Profit/loss on each of the positions is as follows:

Scenario #1 St$/S$ = $0.6089/S$ i$ = 6.24% iS$ = 4.04%

Futt,T$/S$ = ($0.6089/S$) [(1.0624)/(1.0404)](51/365) $0.6107/S$

Profit on futures: +($0.6107/S$–$0.6107/S$) +$0.0000/S$ Profit on spot: –($0.6089/S$–$0.6089/S$) –$0.0000/S$ Net gain $0.0000/S$

Scenario #2 St$/S$ = $0.6089/S$ i$ = 6.24% iS$ = 4.54%

Futt,T$/S$ = ($0.6089/S$) [(1.0624)/(1.0454)](51/365) $0.6102/S$

Profit on futures: +($0.6102/S$–$0.6107/S$) –$0.0004/S$ Profit on spot: –($0.6089/S$–$0.6089/S$) –$0.0000/S$ Net gain –$0.0004/S$

Scenario #3 St$/S$ = $0.6089/S$ i$ = 6.74% iS$ = 4.04%

Futt,T$/S$ = ($0.6089/S$) [(1.0674)/(1.0404)](51/365) $0.6111/S$

Profit on futures: –($0.6111/S$–$0.6107/S$) +$0.0004/S$ Profit on spot: +($0.6089/S$–$0.6089/S$) –$0.0000/S$ Net gain +$0.0004/S$

The profit spread is ±$0.0004/S$. This is about the same as in the example of Figure 5.6. This shows that basis risk exists even if the spot exchange rate does not change.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

15

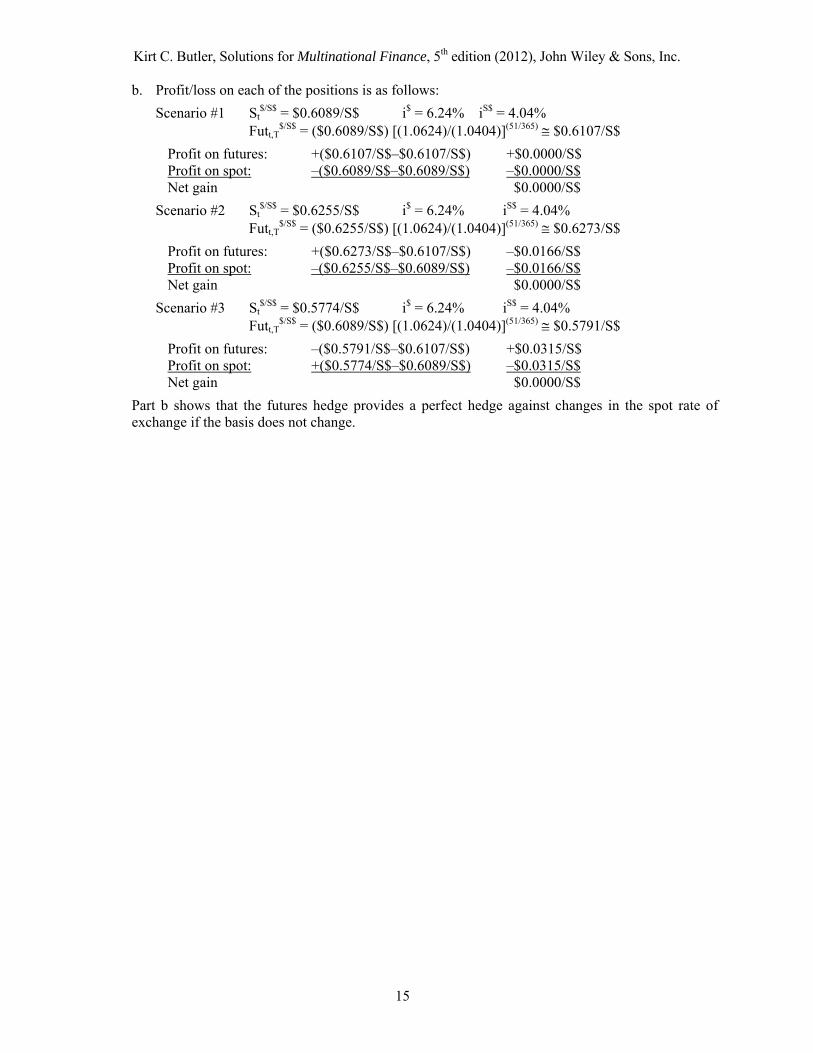

b. Profit/loss on each of the positions is as follows:

Scenario #1 St$/S$ = $0.6089/S$ i$ = 6.24% iS$ = 4.04%

Futt,T$/S$ = ($0.6089/S$) [(1.0624)/(1.0404)](51/365) $0.6107/S$

Profit on futures: +($0.6107/S$–$0.6107/S$) +$0.0000/S$ Profit on spot: –($0.6089/S$–$0.6089/S$) –$0.0000/S$ Net gain $0.0000/S$

Scenario #2 St$/S$ = $0.6255/S$ i$ = 6.24% iS$ = 4.04%

Futt,T$/S$ = ($0.6255/S$) [(1.0624)/(1.0404)](51/365) $0.6273/S$

Profit on futures: +($0.6273/S$–$0.6107/S$) –$0.0166/S$ Profit on spot: –($0.6255/S$–$0.6089/S$) –$0.0166/S$ Net gain $0.0000/S$

Scenario #3 St$/S$ = $0.5774/S$ i$ = 6.24% iS$ = 4.04%

Futt,T$/S$ = ($0.6089/S$) [(1.0624)/(1.0404)](51/365) $0.5791/S$

Profit on futures: –($0.5791/S$–$0.6107/S$) +$0.0315/S$ Profit on spot: +($0.5774/S$–$0.6089/S$) –$0.0315/S$ Net gain $0.0000/S$

Part b shows that the futures hedge provides a perfect hedge against changes in the spot rate of exchange if the basis does not change.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

16

Chapter 6 Currency Options and Options Markets

Answers to Conceptual Questions

6.1 What is the difference between a call option and a put option?

A call option is an option to buy the underlying asset at a predetermined exercise price. A put option is an option to sell the underlying asset at the exercise price.

6.2 What are the differences between exchange-traded and over-the-counter currency options?

Exchange-traded currency options are standardized as to currencies, maturity, exercise prices, and settlement procedures. Over-the-counter options traded by commercial and investment banks can be tailored to fit the needs of the client.

6.3 In what sense is a currency call option also a currency put option?

Because an option to buy one currency is simultaneously an option to sell another currency, currency options are both a call (on one currency) and a put (on the other currency).

6.4 In what sense is a currency forward contract a combination of a put and a call?

A currency forward contract to buy currency f at a forward price of FTd/f at time T can be replicated

by purchasing a European call option on currency f with the same expiration date and an exercise price Kd/f = FT

d/f and simultaneously selling a put option at the same exercise price and maturity date. Conversely, a short forward contract on currency f is a combination of a written call on f and a purchased put on f with the same expiration date and exercise price.

6.5 What are the six determinants of a currency option value?

The determinants of currency option values are riskless domestic and foreign interest rates, the exercise price, the underlying spot (or futures) price, the expiration date, and the volatility of the underlying exchange rate.

6.6 What determines the intrinsic value of an option? What determines time value of an option?

The intrinsic value is the value if exercised today. For a call on the spot rate Sd/f, intrinsic value is equal to max(Sd/f–Kd/f,0). For a put option, intrinsic value is equal to max(Kd/f–Sd/f,0). Time value is the difference between the market value and the intrinsic value of an option and reflects the additional value of waiting until expiration before exercise. Time value primarily depends on time to expiration and volatility in the underlying exchange rate. Foreign and domestic interest rates play a lesser role for most currency options.

6.7 Currency volatility is a key determinant of currency option value, but it is not directly observable. In what ways can you estimate currency volatility?

The other determinants of option value (foreign and domestic interest rates, exercise price, time to expiration, and underlying exchange rate) are usually observable, but the volatility of the underlying exchange rate is not. Volatility can be estimated in two ways: (a) from historical currency movements (e.g., unconditional standard deviations of return, conditional volatilities such as GARCH, or realized volatilities based on intra-day price movements), or (b) implied volatilities (volatilities implied by the five observable determinants of option values and the observed market price of an option) if the other determinants of option values are observable.

Problem Solutions

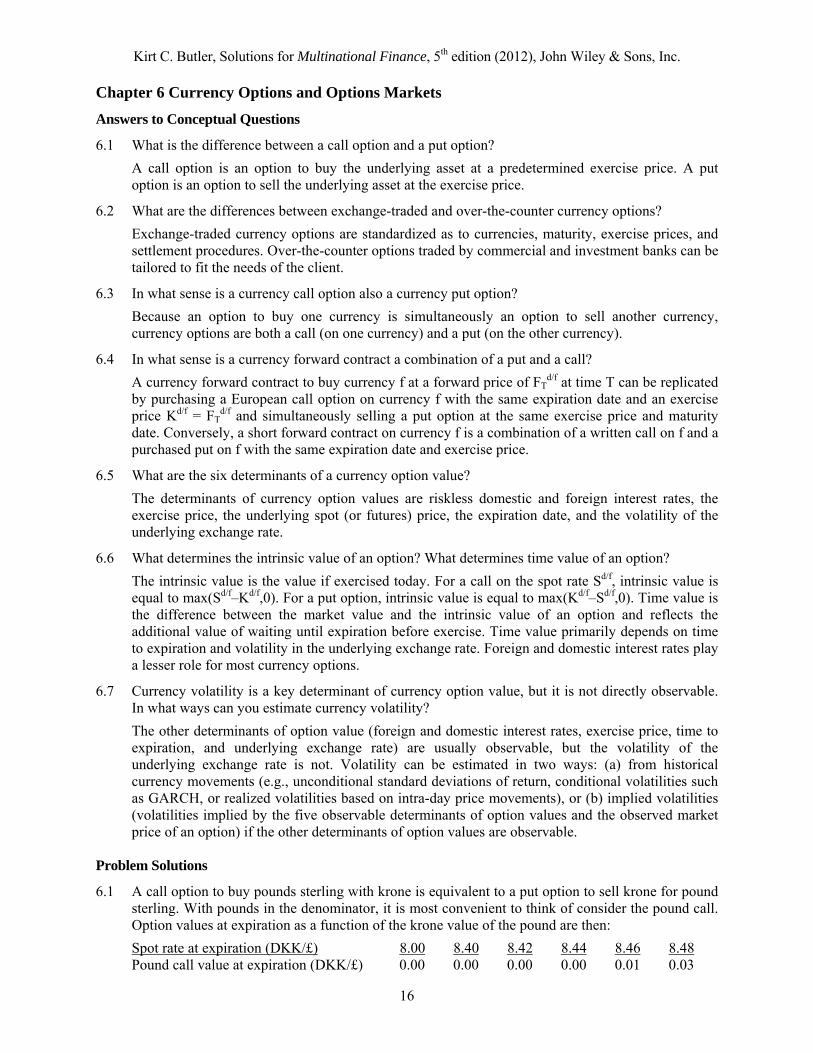

6.1 A call option to buy pounds sterling with krone is equivalent to a put option to sell krone for pound sterling. With pounds in the denominator, it is most convenient to think of consider the pound call. Option values at expiration as a function of the krone value of the pound are then:

Spot rate at expiration (DKK/£) 8.00 8.40 8.42 8.44 8.46 8.48 Pound call value at expiration (DKK/£) 0.00 0.00 0.00 0.00 0.01 0.03

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

17

6.2 An exercise price of DKK8.45/£ is equivalent to £0.11834/DKK. The corresponding krone put option values are:

Spot rate at expiration (£/DKK) 0.12500 0.11905 0.11876 0.11848 0.11820 0.11792 Krone put value at expiration (£/DKK) 0.00 0.00 0.00 0.00 0.14 0.42

The profit/loss graph is as follows.

£0.11834/DKK

£0.11834/DKK

PutT£/DKK

ST£/DKK

6.3 A short krone put is equivalent to a short pound call. Here are their payoff profiles.

£0.11834/DKK DKK8.45/£

£0.11834/DKK

CallTDKK/£PutT

£/DKK

ST£/DKK ST

DKK/£

For long option positions, an option to buy pounds at KDKK/£ = DKK8.45/£ is equivalent to an

option sell DKK at K£/DKK = 1/KDKK/£ = 1/(DKK8.45/£) £0.11834/DKK. Conversely, for the short option positions an obligation to sell pounds at KDKK/£ = DKK8.45/£ is

equivalent to an obligation to buy DKK at K£/DKK = 1/KDKK/£ = 1/(DKK8.45/£) £0.11834/DKK.

6.4 Buy a A$ call and sell a A$ put, each with an exercise price of F1$/A$ = $0.75/A$ and the same

expiration date as the forward contract. Payoffs at expiration look like this:

CallT$/A$ FT

$/A$

ST$/A$ ST

$/A$+

PutT$/A$

ST$/A$ =

6.5 The arguments are the same as for call options. As the variability of end-of-period spot rates

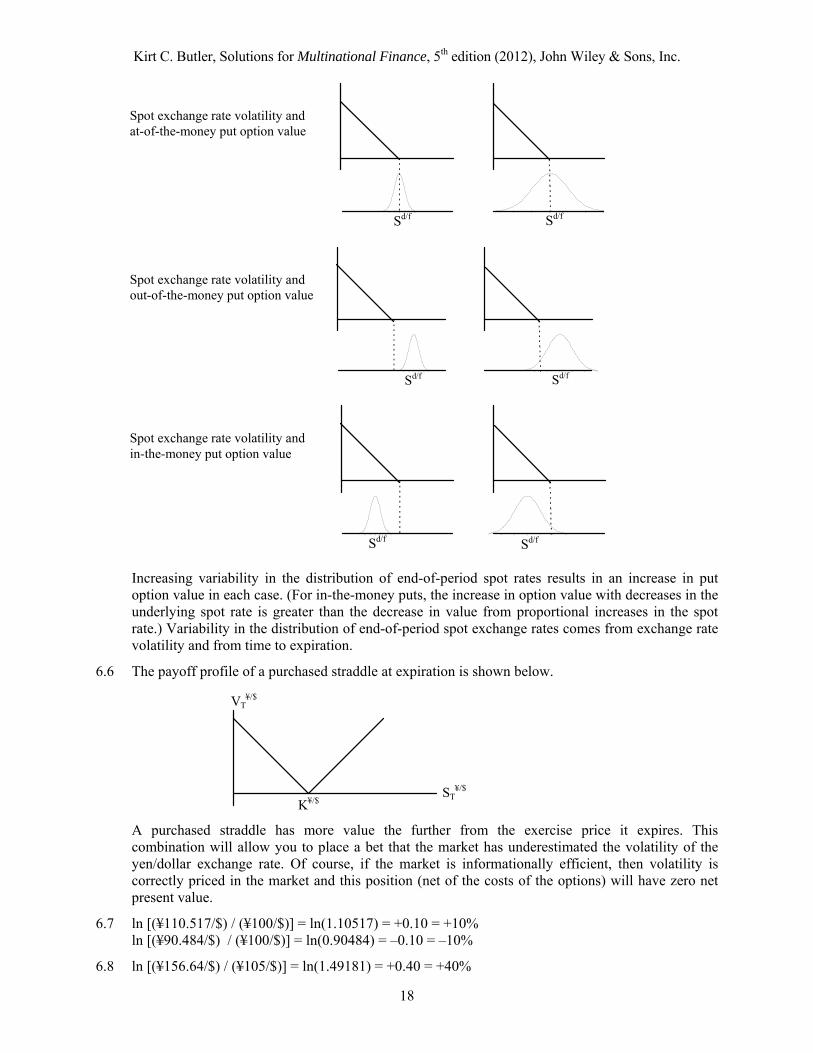

becomes more dispersed, the probability of the spot rate closing below the exercise price increases and put options gain value. Here are the three sets of graphs:

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

18

Increasing variability in the distribution of end-of-period spot rates results in an increase in put

option value in each case. (For in-the-money puts, the increase in option value with decreases in the underlying spot rate is greater than the decrease in value from proportional increases in the spot rate.) Variability in the distribution of end-of-period spot exchange rates comes from exchange rate volatility and from time to expiration.

6.6 The payoff profile of a purchased straddle at expiration is shown below.

A purchased straddle has more value the further from the exercise price it expires. This

combination will allow you to place a bet that the market has underestimated the volatility of the yen/dollar exchange rate. Of course, if the market is informationally efficient, then volatility is correctly priced in the market and this position (net of the costs of the options) will have zero net present value.

6.7 ln [(¥110.517/$) / (¥100/$)] = ln(1.10517) = +0.10 = +10% ln [(¥90.484/$) / (¥100/$)] = ln(0.90484) = –0.10 = –10%

6.8 ln [(¥156.64/$) / (¥105/$)] = ln(1.49181) = +0.40 = +40%

-3

-2 -1 0 1 2 3 -3

-2 -1 0 1 2 3

Sd/f Sd/f

-3

-2 -1 0 1 2 3 -3

-2 -1 0 1 2 3

Sd/f Sd/f

-3

-2 -1 0 1 2 3 -3

-2 -1 0 1 2 3

Sd/f Sd/f

VT¥/$

ST¥/$

K¥/$

Spot exchange rate volatility and at-of-the-money put option value

Spot exchange rate volatility and out-of-the-money put option value

Spot exchange rate volatility and in-the-money put option value

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

19

ln [(¥70.38/$) / (¥105/$)] = ln(0.50819) = –0.40 = –40%

6.9 Exchange rate volatility and standard deviations: a. A daily standard deviation of 0.742% measured over 252 trading days implies T = (0.742%)(252) = 11.78% per year. b. +2: e2(+0.1178) = e+0.2356 = 1.2657 (A$1.4/$)(1.2657) = A$1.7719/$ –2: e2(–0.1178) = e–0.2356 = 0.7901 (A$1.4/$)(0.7901) = A$1.1061/$ c. +2: r = ln((A$1.7719/$)/(A$1.4/$)) = ln(1.2657) = +0.2356 0.1178/year –2: r = ln((A$1.1061/$)/(A$1.4/$)) = ln(0.7901) = –0.2356 0.1178/year Alternatively, S$/A$ = 1/SA$/$

= 1/(A$1.4/$) = $0.714285/A$. +2: e2×(+0.1178) = 1.2657 ($0.7143/A$)(1.2657) = $0.9040/A$ A$1.1061/$ –2: e2×(–0.1178) = 0.7901 ($0.7143/A$)(0.7901) = $0.5644/A$ A$1.7719/$ Appendix 6-A Currency Option Valuation

6A.1 Option determinants are as follows: i¥ = i$ = 0.05, T = ½ year = 0.5, S¥/$ = $80, K¥/$ = $100, and σ = 0.10. Assume these are continuously compounded rates calculated from holding period rates according to i = ln(1+i). Then,

d1 = [ln(Sd/f/Kd/f) + (id–if+σ2/2)T] / (σ√T) = [ln((¥80/$)/(¥100/$)) + (0.05–0.05+(0.10)2/2)(0.5)] / (0.10)(0.5)1/2 = –3.120371 => N(d1) = 0.000903 d2 = d1 – σ√T = –3.1204 – (0.10)(0.5)1/2 = –3.191082 => N(d2) = 0.000709

Calld/f = [Sd/f N(d1)] – [Kd/f N(d2)]

= e(–0.05×.5)[(¥80/$)(0.000903)]–e(–0.05×.5)[(¥100/$)(0.000709)] = ¥0.0013/$. This deep-out-of-the-money dollar call has almost no chance of being exercised.

6A.2 Option determinants are as follows: i¥ = i$ = 0.05, T = ½ year = 0.5, S¥/$ = $80, K¥/$ = $100, and σ = 0.20. Assume these are continuously compounded rates calculated from holding period rates according to i = ln(1+i). Then,

d1 = [ln(Sd/f/Kd/f) + (id–if+ σ2/2)T] / (σ√T) = [ln((¥80/$)/(¥100/$)) + (0.05–0.05+(0.20)2/2)(0.5)] / (0.20)(0.5)1/2 = –1.5071 => N(d1) = 0.065886 d2 = d1 – σ√T = –1.5071 – (0.20)(0.5)1/2 = –1.6486 => N(d2) = 0.049617

Calld/f = e(–ifT) [Sd/f N(d1)] – e(–i

dT) [Kd/f N(d2)]

= e(–0.05×.5)[(¥80/$)(0.065886)]–e(–0.05×.5)[(¥100/$)(0.049617)] = ¥0.3015/$. With 10% annual volatility as in Problem 6A.1, the call option pricing model yields a value of

¥0.0013/$. If the true volatility is 20% per year and this option is priced as if the volatility is 10% per year, then the option will be undervalued by (¥0.3015/$–¥0.0013/$) = ¥0.3015/$-¥0.0013/$ =

¥0.3002/$.

6A.3 From the currency option pricing model, the implied volatility (or standard deviation) of S$/¥ is about 0.0296 (or 2.96%) per year. As verification, here are the calculations of call option value:

d1 = [ln(Sd/f/Kd/f) + (id–if+σ2/2)T] / (σ√T) = [ln(($.008345/¥)/($.008400/¥)) + (0.04–0.04+(0.0296)2/2) (2.5/12)] / [(0.0296)(2.5/12)1/2] = –0.1169 d2 = d1 – σ√T = –0.1169 – (0.0296)(2.5/12)1/2 = –0.1637

Calld/f = [Sd/f N(d1)] – [Kd/f N(d2)]

= e(–0.04×2.5/12)[($.008345/¥)(0.5465)]–e(–0.04×2.5/12)[($0.0084/¥)(0.4535)] = $0.000118/¥. This is an unusually low volatility. Annual dollar/yen volatilities are typically between 8% and

- Tfe i - Td

e i

- Tfe i - Td

e i

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

20

16%. Although a variety of factors could lead to inaccurate implied volatilities, most difficulties in volatility estimation are associated with low volume. (Hence the rule: “Beware of prices in thinly traded markets.”) In this problem, it would be wise to calculate implied volatilities from several other yen options with different exercise prices.

6A.4 a. Interest rate parity provides forward rates according to: Ftd/f / S0

d/f = [(1+id)/(1+if)]t. A problem arises because the options are on Danish krone but the krone appears in the numerator

(a violation of Rule #2 from Chapter 3) of the exchange rates. This is not unusual, as the pound is often left in the denominator of a foreign exchange quote. Historically, the pound was composed of shillings and pence rather than decimal units. (Nobody understands cricket, either.) For clarity, the table below includes forward rates in £/DKK and quotes option prices in direct £/DKK terms from a Londoner’s perspective. The current spot rate is S0

£/DKK = 1/(DKK8.4528/£) = £0.11830/DKK and the exercise price is K£/DKK = 1/(DKK8.5/£) = £0.11765/DKK.

1-month 3-month 6-month 1-year Forward rate (DKK/£) 8.4404 8.4157 8.3787 8.3053 Forward rate (£/DKK) 0.11848 0.11883 0.11935 0.12040 Call option value (£/DKK) 0.00180 0.00294 0.00412 0.00583 Put option value (£/DKK) 0.00100 0.00178 0.00247 0.00326 b. Here is a sample calculation for the three-month (= one period) call and put values. d1 = [ln(Sd/f/Kd/f) + (id–if+σ2/2)T] / (σ√T) = [ln((£0.11830/DKK)/(£0.11765/DKK))+(0.0174–0.0130+(0.05)2/2)(1)]/(0.05)(1)1/2 = +0.2244 d2 = d1 – σ√T = +0.2244 – (0.05)(1)1/2 = +0.1744

Calld/f = [Ftd/f N(d1) – Kd/f N(d2)]

= e(–0.0174×1)[(£0.11883)(0.5888)–(£0.11765)(0.5692)] = £0.00294/DKK. c. Here are the call option payoff profiles for the four options prior to expiration. The one-year

option is plotted as the highest line in the graph.. The one-month option is the lowest (curved) line in the graph. The darkened forty-five degree line is the intrinsic value of the option.

d. Here are put option payoff profiles for the options prior to expiration. The one-year option has a

higher value at high spot rates and a lower value at low spot rates. The one-month option has

- Tde i

-0.002

0.000

0.002

0.004

0.006

0.008

0.010

0.012

0.014

0.016

0.018

0.0900 0.0950 0.1000 0.1050 0.1100 0.1150 0.1200 0.1250

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

21

lower value at high spot rates and a higher value at lower spot rates. The darkened 45o line is the intrinsic value of the option. European put option values can be below intrinsic value because they cannot be exercised until expiration.

6A.5 Let’s restate these exercise prices as pound per krone rates before proceeding.

Exercise prices Exercise prices (DKK/£) 8.2000 8.4000 8.6000 8.8000 Exercise prices (£/DKK) 0.12195 0.11905 0.11628 0.11364

Call option value 0.00114 0.00222 0.00377 0.00568 Put option value 0.00421 0.00244 0.00127 0.00058

-0.020

0.000

0.020

0.040

0.060

0.080

0.100

0.120

0.0000 0.0200 0.0400 0.0600 0.0800 0.1000 0.1200 0.1400 0.1600

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

22

Chapter 7 Currency Swaps and Swaps Markets

Answers to Conceptual Questions

7.1 How are swaps related to forward contracts?

A swap is a portfolio of simultaneous forward contracts each with a different maturity date.

7.2 What is a currency coupon swap?

A currency coupon swap is a fixed-for-floating rate non-amortizing currency swap. Currency coupon swaps are primarily traded through international commercial banks.

7.3 What is a fully covered currency coupon swap?

A fully covered currency coupon swap fully covers the customers interest rate obligations on the underlying exposure by adding a premium to both the fixed and the floating rate side of the swap. Interest payments on the fixed-rate side are set equal in present value to the interest payments on the floating rate side of the swap

7.4 What is a coupon swap?

A coupon swap is a fixed-for-floating rate non-amortizing interest rate swap. These swaps are also traded primarily through international commercial banks.

7.5 What is the difference between a bond equivalent yield and a money market yield?

U.S. Treasuries are quoted as a bond equivalent yield (BEY) assuming a 365-day year and semiannual interest payments. Floating rate Eurocurrencies such as those pegged to LIBOR are quoted as a money market yield (MMY) based on a 360-day year and semiannual coupons. The relation between the two is MMY = BEY(360/365).

Problem Solutions

7.1 Little Prince could form a coupon swap (an interest rate swap) of its existing fixed rate debt into floating rate debt. Consider the coupon swap pricing table from the text:

Bank Pays Bank Receives Current Maturity Fixed Rate Fixed Rate TN Rate 2 years 2 yr TN sa + 19bps 2 yr TN sa + 40bps 7.05% 3 years 3 yr TN sa + 24bps 3 yr TN sa + 47bps 7.42% 4 years 4 yr TN sa + 28bps 4 yr TN sa + 53bps 7.85% 5 years 5 yr TN sa + 33bps 5 yr TN sa + 60bps 7.92%

This schedule assumes non-amortizing debt and semiannual rates (sa). All quotes are against 6-month LIBOR flat. TN = Treasury Note rate.

LP would pay LIBOR flat on the floating rate side and receive the 2-year T-note rate of 7.24% (7.05%+19 bp) on the fixed rate side. Because LP is now paying 8.25% on its fixed rate debt, its interest shortfall would be (8.25%–7.24%) = 1.01%. This is equal to 1.01%(360/365) = 0.996% per year in money market yield. LP’s net cost of floating rate funds is then LIBOR + 99.6 bps in money market yield. In this example, the swap just barely beats the market rate on new floating rate debt of LIBOR + 100 bps.

7.2 a. Ford pays fixed-rate zloty interest at a bond equivalent yield of 7.98%+0.78% = 8.76% and receives floating rate zloty interest at the 6-month LIBOR rate. After converting the 45 bps premium above LIBOR to a bond equivalent yield, Ford’s cost of fixed rate zloty debt is 8.76%+0.45%(365/360) 9.22% in semiannually compounded bond equivalent yield.

b. PM receives fixed rate zloty interest from the swap bank at 7.98%+0.24% = 8.22%. PM pays floating rate zloty interest at 6-month LIBOR flat. After converting the difference between PM’s fixed-rate outflows and inflows (9.83%–8.22% = 161 bps) to a money market yield,

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

23

PM’s cost of floating rate zloty debt is LIBOR + (161 bps)(360/365) = LIBOR+159 bps in money market yield.

c. The swap bank pays LIBOR to Ford and receives LIBOR from PM for no net gain or loss in floating-rate zlotys. The swap bank receives 8.76% (sa) from Ford and pays 8.22% (sa) to PM for a net gain of (8.76%–8.22%) = 54 bps in bond equivalent yield on the notional principal.

7.3 a. The 6-month pound interest rate is (4.12%)/2 = 2.06%. The pound is selling at a 6-month forward discount of 0.58%, so the yen rate that corresponds to the 2.06% pound rate in present value is (1+i¥)/(1+i£) = F1

¥/£/S0¥/£ i¥ = (1+i£)(F1

¥/£/S0¥/£)–1 = (1.0206)(1–0.0058)–1 =

0.01468052, or about 1.468 percent per six months. Note in passing that the PV annuity factors that correspond to these interest rates are PVIFA(i¥=1.46805,T=6) = 5.70339081 and PVIFA(i£=2.06%,T=6) = 5.59010642.

b. Step (1): JI’s 105 bps spread to LIBOR translates into a BEY of (1.05%/2)(365/360) = 53.2292 bps per six months.

Step (2): Solving Equation 7.2 for the equivalent semiannual pound spread yields r£ = r¥ PVIFA(i¥=1.46805,T=6)/PVIFA(i£=2.06%,T=6) = (53.2292 bps)(5.70339081/5.59010642) = 54.3079 bps in bond equivalent yield.

Step (3): JI also must pay the fixed rate side of the swap to the swap bank at a rate of 4.12% + 5 bps, or a semiannual rate of 2.085%. JI’s all-in cost of fixed rate pound sterling debt is (2.085% + 0.543079%) = 2.628079 percent (BEY), or 5.256157 percent per year compounded semiannually.

c. Step (1): BD is paying 7.45% over the 4.07 pound swap rate that it receives from the swap bank, for a semiannual premium of (7.45%–4.07%)/2 = 169 bps.

Step (2): The corresponding yen premium to LIBOR is r¥ = r£ PVIFA(i£,6)/PVIFA(i¥,6) = (169 bps)(5.59010642/5.70339081) = 165.6432 bps (BEY).

Step (3): This is equivalent to (165.6432 bps)(360/365) = 163.3741 bps in money market yield. BD’s all-in cost of floating rate yen financing over the LIBOR yen rate is 2(163.3741 bps) = 3.267483% in money market yield, or about 3.27 percent.

d. The swap bank earns a (4.17%–4.07%) = 10 bp spread in bond equivalent yield on the notional principal regardless of whether the bank quotes fully covered rates or uses the swap pricing schedule given in the problem. When the bank quotes fully covered rates, it adds a premium to both the fixed and floating rate sides that leaves its net position unchanged.

7.4 a. The dollar interest rate that corresponds to the zloty swap mid-rate is ((1+iZ)/(1+i$))t = Ft

Z/$/S0Z/$ i$ = (1+iZ)/(Ft

Z/$/S0Z/$)–1 = (1.079)/(1.038)–1 = 0.03949904, or about 3.95 percent.

The corresponding present value annuity factors are PVIFA(iZ=7.9%,5) = 4.00325549 and PVIFA(i$=3.949904%,5) = 4.45809446.

Usually, we know the notional principal and need to calculate payments based on the swap pricing schedule. In this problem, GE knows the payments and needs to calculate the notional principal. GE wants zloty cash outflows of Z5 million per year to hedge one-half of its Z10 million expected after-tax operating cash flow. GE will be paying the fixed zloty cash flow, and so will pay the swap bank’s ask rate of 8.10%. This requires notional principal of PV0

Z = PMTZ PVIFA(iZ=8.1%,5) = (Z5 million)(3.98220886) = Z19,911,044 to generate a 5-year annuity of Z5 million. This is equivalent to $7,111,087 at the Z2.80/$ spot rate.

Step (1): GE’s cost of floating rate dollar debt is at LIBOR + 32 bps, or (32 bps)(365/360) = 32.4444 basis points in (dollar) bond equivalent yield.

Step (2): The zloty spread to LIBOR is rZ = (32.4444 bps)(4.45809446/4.00325549) = 36.1307 bps (BEY).

Step (3): GE’s all-in cost of fixed rate zloty debt is then (8.10% + 36.1307 bps) = 8.461307 percent (BEY).

b. Step (1): SP is paying 10.24% on its existing zloty debt, compared with the 7.70% it’ll receive from the swap bank, for a premium of (10.24%–7.70%) = 254 bps.

Step (2): The equivalent dollar premium is r$ = rZ PVIFA(iZ=7.9%,5)/PVIFA(i$=3.949904%,5)

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

24

= (2.54%)(4.00325549/4.45809446) = 228.0855 bps in bond equivalent yield, or (228.0855 bps)(360/365) = 224.9611 bps in money market yield.

Step (3): SP’s all-in cost of floating rate dollar financing is LIBOR + 224.9611 bps (MMY), or about 2.25 percent over the LIBOR Eurodollar rate.

c. The swap bank earns an (8.10%–7.70%) = 40 bp spread in bond equivalent yield on the notional principal. When the bank quotes fully covered rates, it adds a premium to both the fixed and floating rate sides of its swaps that leaves its net position unchanged.

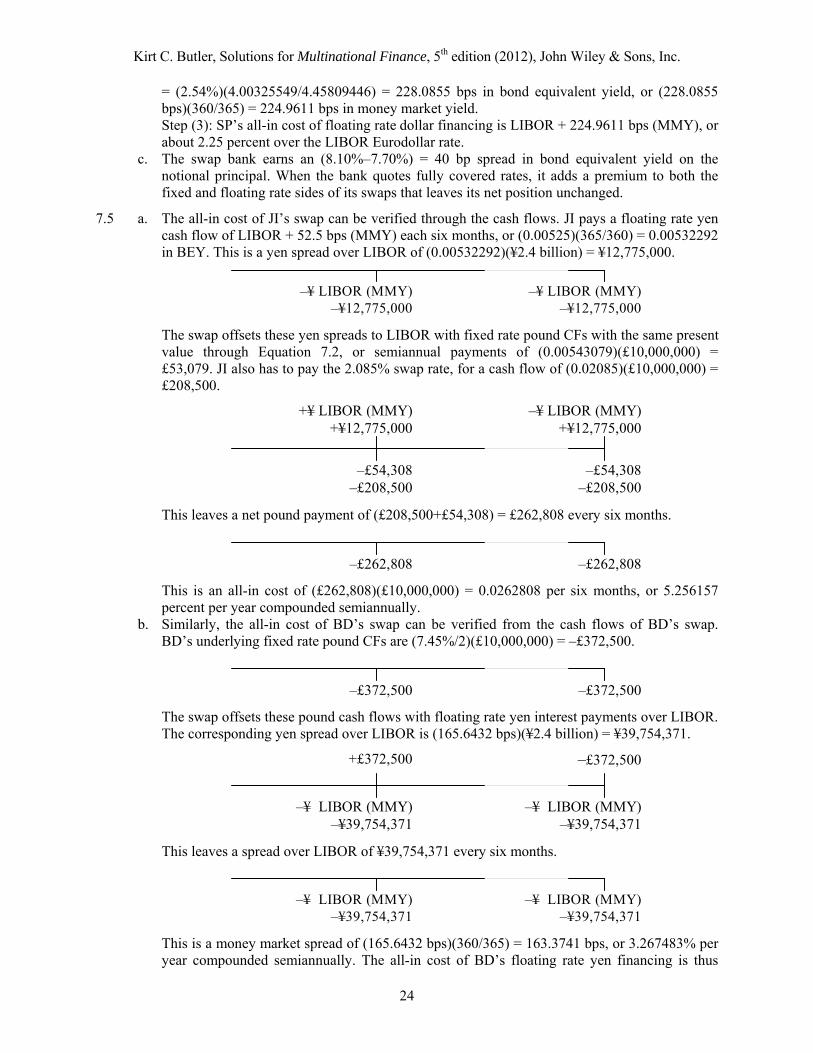

7.5 a. The all-in cost of JI’s swap can be verified through the cash flows. JI pays a floating rate yen cash flow of LIBOR + 52.5 bps (MMY) each six months, or (0.00525)(365/360) = 0.00532292 in BEY. This is a yen spread over LIBOR of (0.00532292)(¥2.4 billion) = ¥12,775,000.

–¥ LIBOR (MMY)

–¥12,775,000–¥ LIBOR (MMY)

–¥12,775,000

The swap offsets these yen spreads to LIBOR with fixed rate pound CFs with the same present value through Equation 7.2, or semiannual payments of (0.00543079)(£10,000,000) = £53,079. JI also has to pay the 2.085% swap rate, for a cash flow of (0.02085)(£10,000,000) = £208,500.

+¥ LIBOR (MMY)+¥12,775,000

–¥ LIBOR (MMY) +¥12,775,000

–£54,308–£208,500

–£54,308 –£208,500

This leaves a net pound payment of (£208,500+£54,308) = £262,808 every six months.

–£262,808 –£262,808

This is an all-in cost of (£262,808)(£10,000,000) = 0.0262808 per six months, or 5.256157 percent per year compounded semiannually.

b. Similarly, the all-in cost of BD’s swap can be verified from the cash flows of BD’s swap. BD’s underlying fixed rate pound CFs are (7.45%/2)(£10,000,000) = –£372,500.

–£372,500 –£372,500

The swap offsets these pound cash flows with floating rate yen interest payments over LIBOR. The corresponding yen spread over LIBOR is (165.6432 bps)(¥2.4 billion) = ¥39,754,371.

+£372,500 –£372,500

–¥ LIBOR (MMY)–¥39,754,371

–¥ LIBOR (MMY) –¥39,754,371

This leaves a spread over LIBOR of ¥39,754,371 every six months.

–¥ LIBOR (MMY)

–¥39,754,371–¥ LIBOR (MMY)

–¥39,754,371

This is a money market spread of (165.6432 bps)(360/365) = 163.3741 bps, or 3.267483% per year compounded semiannually. The all-in cost of BD’s floating rate yen financing is thus

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

25

LIBOR + about 3.27% compounded semiannually.

7.6 a. GE pays a floating rate dollar cash flow of LIBOR + 32.4444 bps (BEY) of the $7,111,087 notional principal on its existing debt, for an annual payment of (0.00324444)($7,111,087) = $23,072 over the 1-year LIBOR Eurodollar rate.

–$ LIBOR (MMY)

–$23,072–$ LIBOR (MMY)

–$23,072

The swap offsets the dollar spread to LIBOR with fixed rate zloty CFs of the same present value through Equation 7.2, or an annual spread of (0.00361307)(Z19,911,044) = Z71,940. GE also has to pay the 8.1% swap rate, for a fixed-rate zloty payment of (0.081)(Z19,911,044) = Z1,612,795.

+$ LIBOR (MMY)+$23,072

–$ LIBOR (MMY) +$23,072

–Z71,940–Z1,612,795

– Z71,940 – Z1,612,795

The total fixed-rate zloty payment is Z1,684,735 each year.

– Z1,684,735 – Z1,684,735

This is indeed an all-in cost (Z1,684,735)/(Z19,911,044) = 0.08461307 per year (or about 8.46 percent) on GE’s fixed-rate zloty debt.

b. SP’s underlying fixed rate zloty payments are (10.24%)(Z19,811,044) = Z2,038,891 per year.

–Z2,038,891 – Z2,038,891

The swap offsets these fixed-rate zloty CFs with floating rate dollar payments over LIBOR. The corresponding $ spread over LIBOR is (0.02280855)($7,111,087) = $162,194 as a BEY.

+Z2,038,891 +Z2,038,891

–$ LIBOR (MMY)–$162,194

–$ LIBOR (MMY) –$162,194

When combined with the underlying zloty obligation, this leaves net cash flows of

–$ LIBOR (MMY)

–$162,194–$ LIBOR (MMY)

–$162,194

This is a money market spread of (228.0855 bps)(360/365) = 224.8611 bps, or about 2.25% over the 1-year LIBOR Eurodollar rate.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

26

PART III Managing the Risks of Multinational Operations

Chapter 8 Multinational Treasury Management

Answers to Conceptual Questions

8.1 What is multinational treasury management?

Multinational treasury management involves five functions: 1) set overall financial goals, 2) manage the risks of international transactions, 3) arrange financing for international trade, 4) consolidate and manage the financial flows of the firm, and 5) identify, measure, and manage the firm’s risk exposures.

8.2 What function does a firm’s strategic business plan perform?

The strategic business plan performs the following functions: 1) identify the firm’s core competencies and potential growth opportunities, 2) evaluate the business environment within which the firm operates, 3) formulate a comprehensive strategic plan for turning the firm’s core competencies into sustainable competitive advantages, 4) develop robust processes for implementing the strategic business plan.

8.3 Why is international trade more difficult than domestic trade?

International trade is difficult largely because of information costs. Exporters must ensure timely payment from far-away customers. Importers must ensure timely delivery of quality goods or services. Also, dispute resolution is difficult across multiple jurisdictions.

8.4 Why use a freight forwarder?

A freight shipper coordinates the logistics of transportation and documentation, which can be formidable on international shipments.

8.5 Describe four methods of payment on international sales.

The methods are open account, cash in advance, drafts, and letters of credit. In an open account, the seller bills the buyer upon delivery of the goods. In cash in advance, the buyer pays prior to receiving shipment. A draft is used to pay upon delivery and is like a check or money order. A bank letter of credit guarantees payment upon presentation of the specified trade documents.

8.6 What is a banker’s acceptance, and how is it used in international trade?

A banker’s acceptance is a time draft drawn on a commercial bank in which the bank promises to pay the holder of the draft a stated amount on a specified future date. Banker’s acceptances are negotiable and so may be sold by the exporter to finance working capital.

8.7 What is discounting, and how is it used in international trade?

Discounting is the purchase of a promised payment at a discount from face value.

8.8 How is factoring different from forfaiting?

Factoring is the sale of accounts receivable. Forfaiting is a form of factoring involving medium- to long-term receivables with maturities of six months or more.

8.9 What is countertrade? When is it most likely to be used?

Countertrade involves an exchange of goods or services without the use of cash. It is commonly used in countries with inconvertible currencies, currency controls, or limited reserves of hard currency. Large exporters with significant international experience are more likely to use countertrade as a means of entry into new and developing markets.

8.10 What is multinational netting?

In multinational netting, transactions that offset one another are identified within the corporation.

Kirt C. Butler, Solutions for Multinational Finance, 5th edition (2012), John Wiley & Sons, Inc.

27

Once offsetting transactions are identified, only the net amount of funds need be exchanged.

8.11 How can treasury assist in managing relations among the operating units of the MNC?

Treasury can serve as a “corporate bank” satisfying the financing requirements of the operating units. This central role allows Treasury to net transactions within the corporation and thereby minimize the number and size of external market transactions. Treasury can also direct operating units on transfer pricing issues and identify hurdle rates on new investments.

8.12 What are the five steps in a currency risk management program?

1) Identify those currencies to which the firm is exposed and the distribution of future exchange rates for each of these currencies. 2) Estimate the firm’s sensitivity to changes in these currency values. 3) Determine the desirability of hedging, given the firm’s estimated risk exposures and risk management policy. 4) Evaluate the cost/benefit performance of each hedging alternative, given the forecasted exchange rate distributions. Select and implement the hedging instrument or strategy. 5) Monitor the firm’s evolving exposures and revisit these steps as necessary.

8.13 What is the difference between passive and active currency risk management?

Active management selectively hedges FX exposures depending on the manager’s market view. Passive management does not take a view, but applys the same hedging rule to each exposure.

8.14 What is the difference between technical and fundamental analysis?

Technical analysis uses exchange rate history to predict short-term exchange rate movements. Fundamental analysis uses macroeconomic data to forecast long-term exchange rate movements.

8.15 Are small, medium, or large firms most likely to use derivatives to hedge currency risk? How do firms benchmark their hedges?

Derivatives users tend to be large firms, and typically use the forward rate for benchmarking.

Problem Solutions

8.1 a. A 6% interest rate compounded quarterly is the same as a 1.5% quarterly rate. The net amount payable at maturity is $9,990,000 after subtracting Paribas’ acceptance fee. Fruit of the Loom will receive ($9,990,000)/(1.015) = $9,842,365 if it sells the acceptance to its bank.

b. The all-in cost of the acceptance is ($10,000,000)/($9,842,365)–1 = 1.60% per quarter or an effective annual rate of (1.0160)4–1= 0.0656, or 6.56% per year.

8.2 a. The 2%/month factoring fee of ($10 million)(0.02/month)(3 months) = $600,000 is due at the time the receivables are factored. Fruit of the Loom is giving up accounts receivable with a face amount of $10 million due in three months in exchange for a net amount of $9,400,000.