economic reforms aviation industry

TRANSCRIPT

ECONOMIC REFORM AVIATION SECTOR - INDIA

SOURCES• 2nd U.S.-India Aviation Partnership Summit(2009)• Research Study of the Civil Aviation Sector in India

SUBMITTED TO : The Ministry of Corporate Affairs, Govt. of India (2012)

• WIKIPEDIA• AIRLINE INDUSTRY- CHANGING TIMES (NMIMS PROJ;2002)

GUIDE : PROF N S SHETTY• NEWSPAPER UPDATES TILL 20 Nov 2013

– THE ECONOMIC TIMES– BUSINESS STANDARD– THE INDIAN EXPRESS– THE TIMES OF INDIA– LIVE MINT & THE WALL STREET JOURNAL.– WALL STREET JOURNAL

SUMMARY OF PRESENTATION

• Introduction

• India’s economy before 1991

• Aviation Industry before & after 1991

• Liberalisation policies/Government initiatives

• Impact of Liberalisation Policy

• Growth Story

• SWOT Analysis

• ROAD AHEAD

REGIONAL AIRLINES-29 JUL13• GoI has set target of building 50 new low cost small

airports by AAI across 11 states to cater for regional connectivity.

• Large airlines mandated to connect smaller cities

• scheduled regional airlines to induct smaller aircraft for deployment on regional routes

• Relaxation on number of aircrafts

• Cess and tax relaxation on regional routes

• Reduce VAT on ATF and Less Airport charges.

• Permission to fly international routes to regional airlines.

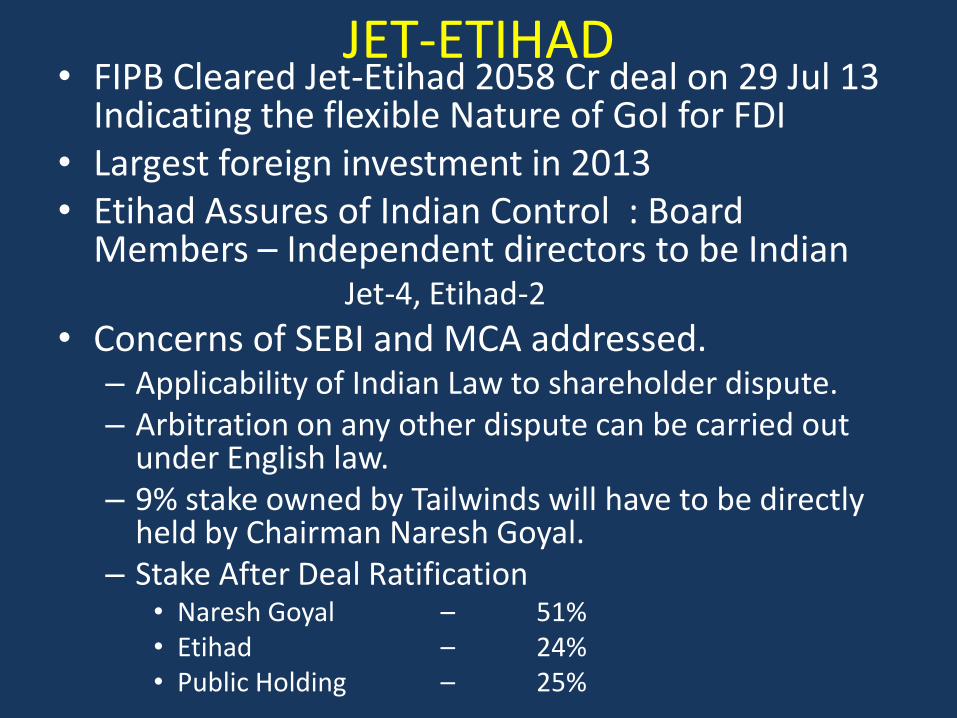

JET-ETIHAD• FIPB Cleared Jet-Etihad 2058 Cr deal on 29 Jul 13

Indicating the flexible Nature of GoI for FDI• Largest foreign investment in 2013• Etihad Assures of Indian Control : Board

Members – Independent directors to be IndianJet-4, Etihad-2

• Concerns of SEBI and MCA addressed. – Applicability of Indian Law to shareholder dispute.– Arbitration on any other dispute can be carried out

under English law.– 9% stake owned by Tailwinds will have to be directly

held by Chairman Naresh Goyal.– Stake After Deal Ratification

• Naresh Goyal – 51%• Etihad – 24%• Public Holding – 25%

AIR ASIA - JV

• AirAsia India is a proposed JV start-up and is the latest venture of the AirAsia Group. AirAsia Investment Ltd has applied to the Indian Foreign Investment Promotion Board (FIPB) to seek approval for AAIL to invest 49% into a proposed Indian JV together with Tata Sons Limited and Arun Bhatia of TelestraTradeplace Pvt Ltd. The JV plans to operate from Chennai, focused on providing domestic Tier II/Tier III city connectivity

AIRPORTS & AIRCRAFTS- INDIAAIRPORTS & AIRSTRIPS

ORG TOTAL OPERATIONALAAI 97 65DEFENCE 138 90*STATE GOV 161 67JV 06 06PVT 61 53* CIVIL ENCLAVE 25

AIRCRAFTSAIRLINE NOS OF A/CAIR INDIA 131JET 111INDIGO 62SPICEJET 48GO AIR 13BLUE DART 08DECCAN CARGO 02AIR MANTRA 02QUICKJET 01

INDUSTRY OVERVIEW

• India is World’s 9th largest market

• Comprises of Domestic Airline, Air Cargo and Airports

• Scheduled services available from to/fro 82 airports

• Bilateral with 104 countries

• Domestic air passenger - Worlds 4th

• Enhanced connectivity – 87 foreign airlines of 49 countries

• 07 scheduled airlines operating exclusively in passenger sector

• Presently it contributes 0.5 % of GDP and it is expected that by 2030 it will contribute 5 % of GDP

INDIA’S ECONOMY BEFORE 1991

• Influenced by Protectionism and Public ownership.

• Existence of License Raj (Red Tape).

• Average growth rate of India was 3.5% p.a with per capita 1.3%p.a.

• More focused on Heavy Industries and Agriculture.

• Less attention towards service sector.

• Downfall of USSR and Gulf War added fuel to the fire of crisis.

INDIA’S ECONOMY BEFORE 1991

• Major imbalance in payments of loans.

• International Monetary Fund (IMF) demanded for economic reforms in return of aid.

• Prime Minister Narasimha Rao and Finance Minister ManmohanSingh took initiative to bring Liberalization.

LICENCE RAJ

ECONOMIC REFORMS POST 1991

Policies

• Liberalisation - Private Players

• Open Sky

• Direct import of ATF - Regulation

• FDI – Domestic Services Sector

• Airports control - Airports Authority of India (AAI)

• Green Field Airport

IMPACT OF LIBERALISATION

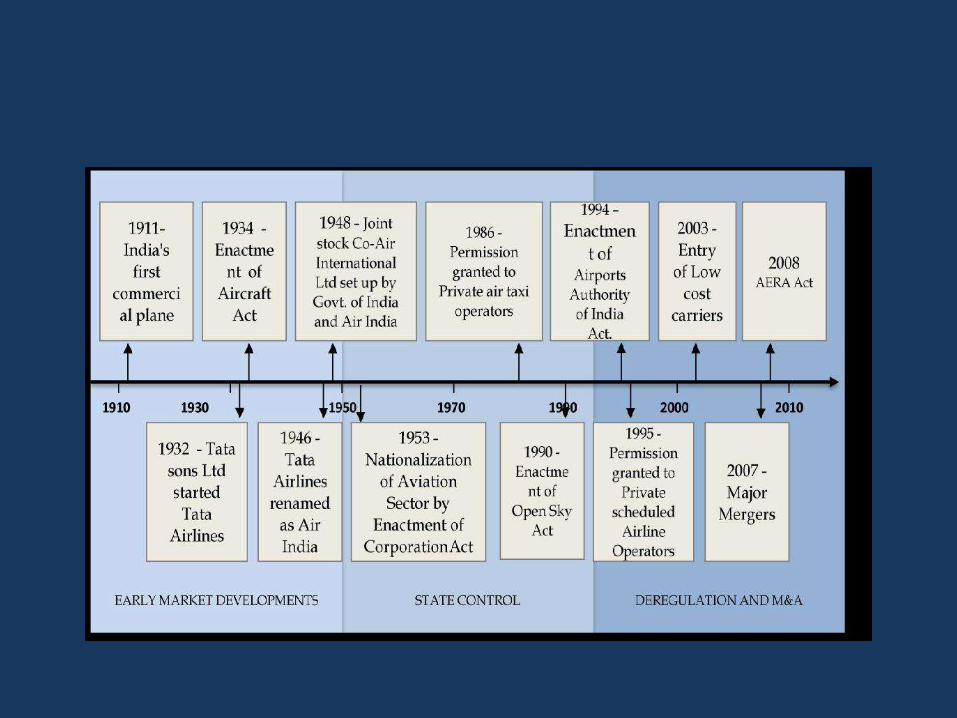

• The Air Corporation Act, 1953 repealed

Opening up of the domestic sectorDisinvestment of the two public sector airlinesNew privately owned domestic airlines

• Open Sky

Allow foreign airline of any country or ownership to land atany port on any number of occasions and with unlimited seatcapacity.

• Foreign Direct Investment

Up To 49% Of Foreign Equity & 100% Of NRI investment isallowed Pertaining to the Domestic Air Transport Services

IMPACT OF LIBERALISATION

• Private Carriers permitted to operate scheduled services – 75% share in domestic aviation

• Entry of low cost carriers

• City side development of non-metro airports

• Allowing Indian carriers to compete on international routes

• Reduction in Landing charges.

• Fleet expansion plans of Air India

IMPACT OF LIBERALISATION

• Restructuring of Delhi and Mumbai airport and development

of Greenfield airports at Bangalore and Hyderabad

undertaken.

• Up gradation/ expansion/ development of airports

undertaken depending upon traffic potential, requirement of

airline operators and need of air passengers.

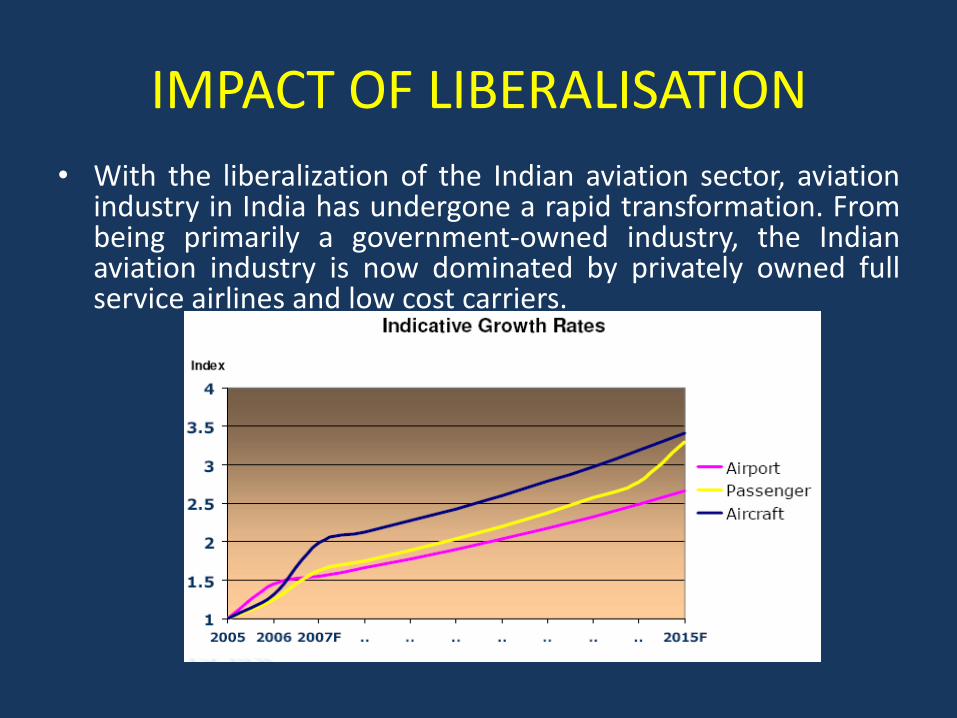

IMPACT OF LIBERALISATION

• With the liberalization of the Indian aviation sector, aviationindustry in India has undergone a rapid transformation. Frombeing primarily a government-owned industry, the Indianaviation industry is now dominated by privately owned fullservice airlines and low cost carriers.

PASSENGER FLOW2006 - 2011

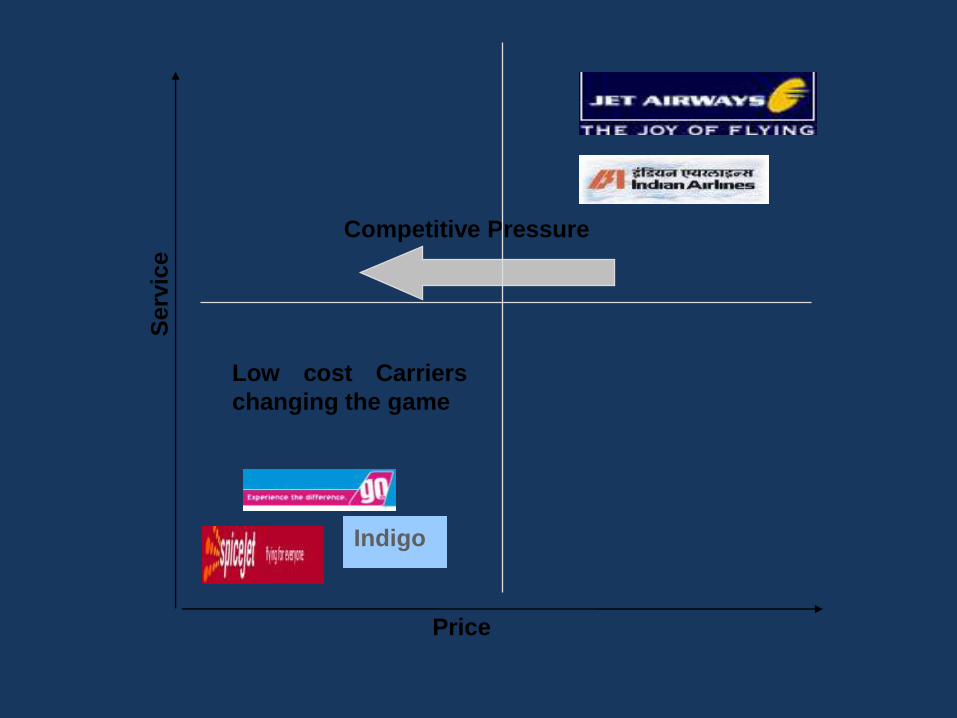

Competitive Pressure

Serv

ice

Price

Low cost Carriers

changing the game

Indigo

Market Size

Domestic Air Traffic quadrupled from 13 million to 52 billion in last decade

International Traffic more than tripled to 38 million

87 foreign airlines fly to and from India and 5 Indian airlines fly to and from 40 countries

45 million tons of cargo through 920 airlines, using 4200 airports and deploying 27000 aircrafts

Projections for traffic during the Eleventh Five Year Plan, which shows increase in passenger traffic (i.e. 18.8%) as compared to cargo (i.e. 11.4%). The figure is as follows:

Market Size Contd…….

Projection of Traffics upto 2016-17

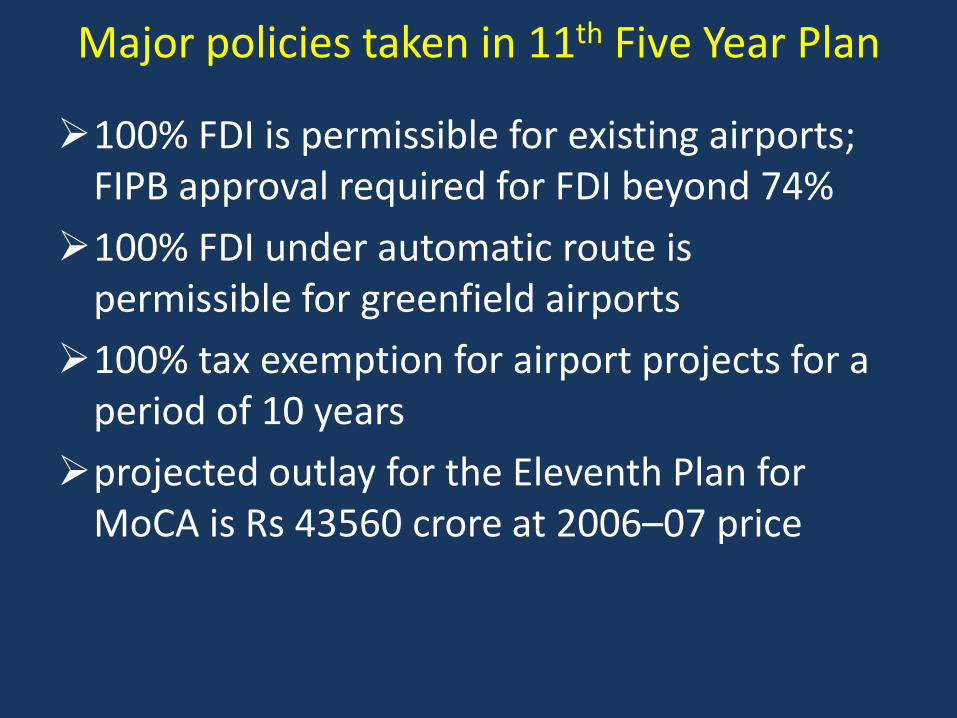

Major policies taken in 11th Five Year Plan

Reduction of high Aviation Turbine Fuel(ATF) cost and review of its Tax structure

Multi Modal Connectivity by building expressways to facilitate advantage of air transportation by reducing the total travel time

foreign equity participation up to 49% and investment by non-resident Indians (NRIs) up to 100% in the domestic air transport services

Promotion of Regional Airlines by the way of liberal policy and provision of better infrastructure facilities

Development of MRO hub Review of RDG to bring them in line with developments Merger of AI and Indian Airlines to optimize fleet

acquisition & to leverage the asset base

Major policies taken in 11th Five Year Plan

100% FDI is permissible for existing airports; FIPB approval required for FDI beyond 74%

100% FDI under automatic route is permissible for greenfield airports

100% tax exemption for airport projects for a period of 10 years

projected outlay for the Eleventh Plan for MoCA is Rs 43560 crore at 2006–07 price

FDI Policy

The Reserve Bank of India (RBI) announced that foreign institutional investors might have shareholdings more than the limited 49% in the domestic sector.

• Airports – Foreign equity up to 100% is allowed by the means of automatic approvals

pertaining to establishment of Greenfield airports – Foreign equity up to 74% is allowed by the means of automatic approvals

pertaining to the existing airports – Foreign equity up to 100% is allowed by the means of special permission from

Foreign Investment Promotion Board, Ministry of Finance, pertaining to the existing airports

– 100 per cent tax exemption for airport projects for a period of 10 years.

• Air Transport Services– Up to 49% of foreign equity is allowed by the means of automatic approvals

pertaining to the domestic air transport services – Up to 100% of NRI investment is allowed by the means of automatic approvals

pertaining to the domestic air transport services – 74 per cent FDI is permissible in cargo and non-scheduled airlines.

Foreign companies can explore various

modes of entry into the Indian market

AVIATION SECTOR

GROWTH OF THE INDUSTRY

• The growth of airlines traffic in Aviation Industry in India is almostfour times above international average.

• Domestic airlines passengers traffic in increasing at the rate of 25%.

• India ranks fourth after US, China and Japan in terms of domesticpassengers volume.

The domestic aviation sector is expected to grow at a rate of 9-10per cent to reach a level of 150-180 million passengers by 2020.

• The industry witnessed an annual growth of 12.8 per cent duringthe last 5 years in the international cargo handled at all Indianairports.

GROWTH OF THE INDUSTRY

• Further, there has been an increase in tourist charter flights to Indiawith around 686 flights bringing 150,000 tourists.

• It is predicted that international passengers will grow upto 50million by 2015

• Aviation is now affordable with check fares and discount schemes.

• Various Operators with different business model.

• Regional connectivity – Tier II & Tier III cities

Contribution to GDP

Present Contribution < 1%.

Poised to grow at 5% contribution to GDP by 2030

OPPORTUNITIES

Airport development and modernisation

• The government is promoting private participation for thedevelopment of greenfield airports and modernisation of existingairports.

Airport connectivity

• The Ministry of Civil Aviation is focussing on improving connectivity

to major airports.

City-side development

• The government is focussing on the city-side development of airports,including real estate and commercial development. The city-sidedevelopment of 24 non-major airports is being taken up.

SWOT ANALYSIS

Road Ahead

• The Indian aviation sector is likely to see clear skies ahead in the years tocome.

• Passenger traffic is projected to grow at a CAGR of over 15 per cent in thenext 5 years.

• The Vision 2020 statement announced by the Ministry of Civil Aviation,envisages creating infrastructure to handle 280 million passengers by 2020.

• Investment opportunities of US$ 110 billion envisaged up to 2020 withUS$ 80 billion in new aircraft and US$ 30 billion in development of airportinfrastructure.

• Associated areas such as maintenance, repair and overhaul (MRO) andtraining offer high investment potential. A report by Ernst & Young says theMRO category in the aviation sector can absorb up to US$ 120 billionworth of investments by 2020.

• Aerospace major Boeing forecasts that the Indian market will require 1,000commercial jets in the next 20 years, which will represent over 3 per centof Boeing Commercial Airplanes’ forecasted market worldwide. Thismakes India a US$ 100 billion market in 20 years.

THANK YOU