economic contributions of the florida citrus industry in 2016-16

TRANSCRIPT

ECONOMIC CONTRIBUTIONS OF THE FLORIDA CITRUS INDUSTRY IN 2015-16

P R E S E N TAT I O N TO T H E F LO R I DA C I T R U S C O M M I S S I O NM AY 1 7 , 2 0 1 7

Christa D. Court, PhD | Assistant Scientist

Alan W. Hodges, PhD | Extension Scientist

Mohammad Rahmani, PhD | Economic Analyst

Thomas J. Spreen, PhD | Professor Emeritus FOOD AND RESOURCE ECONOMICS DEPARTMENT

Scope of the Florida Citrus Industry, 2015-16

Florida Commercial Citrus Production Areas

• Largest citrus producer in the U.S. 49% of total U.S. citrus production U.S. is 4th largest producer in the world

• 27 counties have citrus production 5 commercial citrus production areas

• 480,000+ acres of grove lands 435,000+ acres of bearing grove lands

• 32 packinghouses ship fresh fruit to global markets

• 19 processing facilities that process citrus juice and byproducts

Study Purpose• Estimate the economic contributions of

the citrus industry in Florida for 2015-16 season– Fruit production– Packinghouse operations– Citrus juice manufacturing

• Estimate impacts for five commercial citrus production areas– Northern– Western (peninsular)– Central– Indian River – Southern

• Compare results to previous studies – 2012-13 season– 2014-15 season

• Update estimates for the economic impacts of citrus greening disease (HLB)

Source: UF/IFAS

Data Sources and Methods• U.S. Department of Agriculture (USDA)

– National Agricultural Statistics Service (NASS)• Citrus acreage, fruit production by type, grower prices

– Foreign Agricultural Service (FAS)• World citrus production, consumption, and exports

• Florida Department of Agricultural and Consumer Services (FDACS)– Fruit shipments to packinghouses and processing

plants

• Florida Department of Citrus (FDOC)– Juice shipments, wholesale and retail prices

(Nielson), byproduct prices (industry survey)

– Byproduct volumes

• IMPLAN regional input-output software and data– Captures the direct, indirect, and induced

multiplier effects of industry activities in all economic sectors

Source: UF/IFAS

Source: UF/IFAS

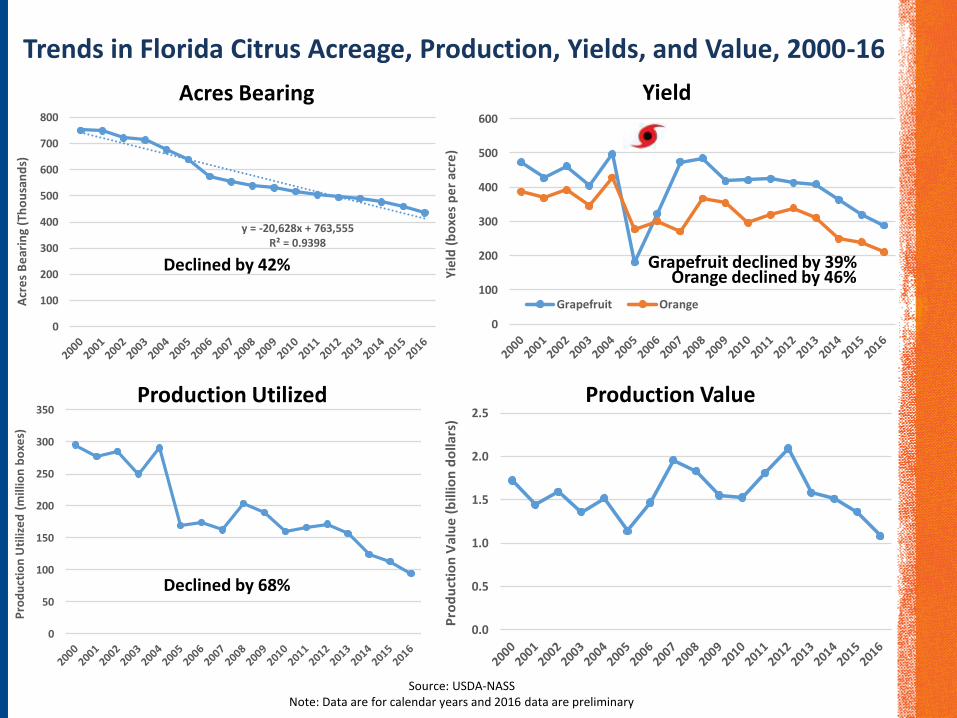

y = -20,628x + 763,555R² = 0.9398

0

100

200

300

400

500

600

700

800

Acr

es

Be

arin

g (T

ho

usa

nd

s)

0

100

200

300

400

500

600

Yie

ld (

bo

xes

pe

r ac

re)

Grapefruit Orange

0

50

100

150

200

250

300

350

Pro

du

ctio

n U

tiliz

ed

(m

illio

n b

oxe

s)

Trends in Florida Citrus Acreage, Production, Yields, and Value, 2000-16

Declined by 42% Grapefruit declined by 39%Orange declined by 46%

Declined by 68%

Source: USDA-NASSNote: Data are for calendar years and 2016 data are preliminary

0.0

0.5

1.0

1.5

2.0

2.5

Pro

du

ctio

n V

alu

e (

bill

ion

do

llars

)

Acres Bearing Yield

Production Utilized Production Value

Trends in World Citrus Production, Consumption, Exports, and Orange Juice Consumption, 2011-12 – 2015-16

Source: USDA-FAS

8.818.42

8.90 8.92 9.36

0

1

2

3

4

5

6

7

8

9

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2011-12 2012-13 2013-14 2014-15 2015-16

Wo

rld

Exp

ort

s(t

ho

usa

nd

me

tric

to

ns)

Co

un

try/

Re

gio

n E

xpo

rts

(th

ou

san

d m

etr

ic t

on

s)

World China South Africa Turkey United States Egypt

88.93 86.2989.91 90.14 88.49

0

10

20

30

40

50

60

70

80

90

0

5

10

15

20

25

30

35

2011-12 2012-13 2013-14 2014-15 2015-16

Wo

rld

Co

nsu

mp

tio

n(m

illio

n m

etr

ic t

on

s)

Co

un

try/

Re

gio

n C

on

sum

pti

on

(m

illio

n m

etr

ic t

on

s)

World China Brazil European Union United States Mexico

89.6386.69

90.84 90.89 89.21

0

10

20

30

40

50

60

70

80

90

0

5

10

15

20

25

30

35

2011-12 2012-13 2013-14 2014-15 2015-16

Wo

rld

Pro

du

ctio

n(m

illio

n m

etr

ic t

on

s)

Co

un

try

/Re

gio

n P

rod

uct

ion

(mill

ion

me

tric

to

ns)

World China Brazil European Union United States Mexico

Production Consumption

Exports Orange Juice Consumption2,058 2,070

1,9592,055

1,892

0

500

1000

1500

2000

0

100

200

300

400

500

600

700

800

900

1000

2011-12 2012-13 2013-14 2014-15 2015-16

Wo

rld

Ora

nge

Ju

ice

Co

nsu

mp

tio

n

(t

ho

usa

nd

me

tric

to

ns)

Co

un

try/

Re

gio

n O

ran

ge J

uic

e C

on

sum

pti

on

(t

ho

usa

nd

me

tric

to

ns)

World European Union United States Japan China Canada

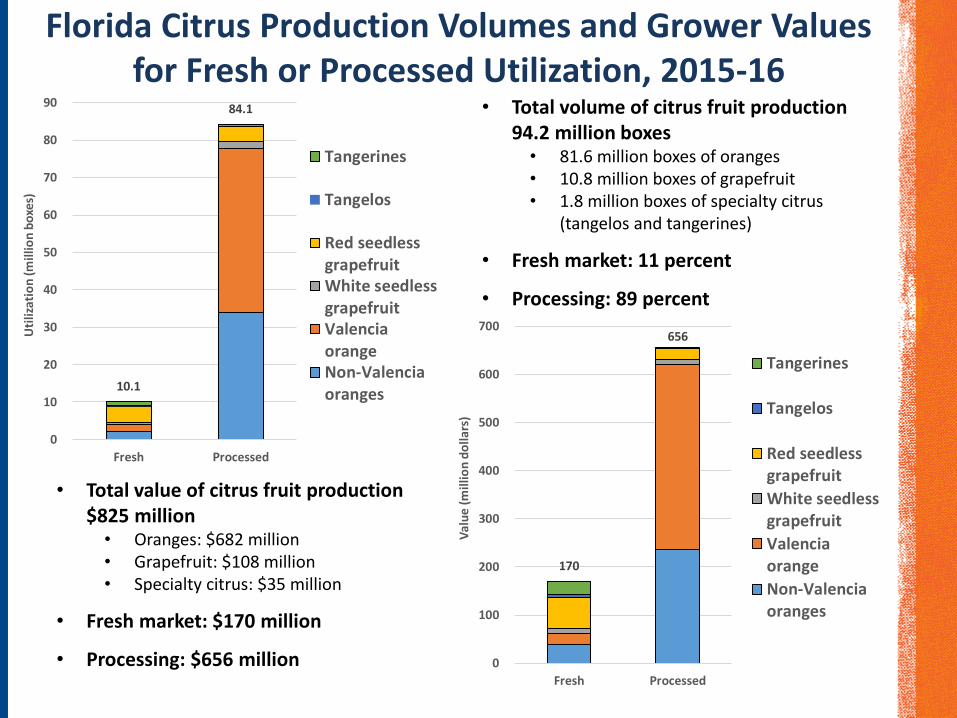

10.1

84.1

0

10

20

30

40

50

60

70

80

90

Fresh Processed

Uti

liza

tio

n (

mill

ion

bo

xes)

Tangerines

Tangelos

Red seedlessgrapefruitWhite seedlessgrapefruitValenciaorangeNon-Valenciaoranges

Florida Citrus Production Volumes and Grower Values for Fresh or Processed Utilization, 2015-16

• Total volume of citrus fruit production 94.2 million boxes• 81.6 million boxes of oranges• 10.8 million boxes of grapefruit • 1.8 million boxes of specialty citrus

(tangelos and tangerines)

• Fresh market: 11 percent

• Processing: 89 percent

• Total value of citrus fruit production $825 million• Oranges: $682 million• Grapefruit: $108 million • Specialty citrus: $35 million

• Fresh market: $170 million

• Processing: $656 million

170

656

0

100

200

300

400

500

600

700

Fresh Processed

Va

lue

(m

illio

n d

olla

rs)

Tangerines

Tangelos

Red seedlessgrapefruit

White seedlessgrapefruit

Valenciaorange

Non-Valenciaoranges

Florida Fresh Citrus Shipment Values and Packinghouse Margins, 2015-16

The wholesale margin on fresh packed fruit is the difference between the value of shipped fruit and the value paid to growers.

Volume of certified fresh shipments: 17,458 thousand 4/5 bushel cartons

Non-Valencia oranges: 3,153 Valencia oranges: 2,862 White seedless grapefruit: 980 Red seedless grapefruit: 8,091 Tangelos: 414 Tangerines: 1,959

53 40

19

128

6

48

0

20

40

60

80

100

120

140

Non-Valenciaoranges

Valenciaorange

Whiteseedless

grapefruit

Redseedless

grapefruit

Tangelos Tangerines

Oranges fill Grapefruit fill Specialty Citrus

Va

lue

(m

illio

n d

olla

rs)

Value paid to growers

Packinghouse margin

Wholesale Value of Florida Citrus Juice, 2015-16

• Total volume: 810 million gallons Orange juice: 771 million gallons Grapefruit juice: 38 million gallons

• Total producer value: $2.8 billion Orange juice: $2.7 billion Grapefruit juice: $115 million

• Total in-state sales: $157 million Frozen concentrate: $42 million Single strength: $116 million

• Total out-of-state sales: $2.6 billion Frozen concentrate: $692 million Single strength: $1.9 billion

• 94% of the value of citrus juice sales is shipped out-of-state

733

2,057

0

500

1,000

1,500

2,000

2,500

Frozen Concentrate Single Strength

Val

ue

(mill

ion

do

llars

) Out-of-state In-state

697

36

1,978

79

0

400

800

1,200

1,600

2,000

Orange Grapefruit Orange Grapefruit

Frozen Concentrate fill Single Strength

Va

lue

(m

illio

n d

olla

rs) Packaged Bulk

Volume and Value of Processed Citrus Byproducts, 2015-16

Sources: www.svfeeds.com; www.gardeningknowhow.com; www.primafleurbotanicals.blogspot.com

Economic Contributions of Florida Citrus Industry Activities, 2015-16

15,563

27,872

1,987

0

5,000

10,000

15,000

20,000

25,000

30,000

Growers Processors Packinghouses

Em

plo

yme

nt

(fu

lltim

e a

nd

pa

rt-t

ime

job

s)

Direct Indirect Induced

2,559

4,230

8,632

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Labor Income Value Added Industry Output

(mill

ion

do

llars

)

Growers Processors Packinghouses

Total contributions by citrus industry sector

Total employment contributions by type and citrus sector

State and local tax contributions:

$271 million

Tax Contributions of Florida Citrus Activities, 2015-16

Tax on Production and Imports:

Sales Tax46%Tax on

Production and Imports:

Property Tax36%

Personal Tax: NonTaxes

(Fines- Fees)5%

Tax on Production and Imports: Other Taxes

4%

Corporate Profits Tax

4%Other

5%

Federal tax contributions:

$547 million

Personal Tax: Income Tax

34%

Social Ins Tax-Employer

Contribution23%

Social Ins Tax-Employee

Contribution21%

Corporate Profits Tax

16%

Tax on Production and Imports: Excise

Taxes4%

Other2%

Total Employment Contributions by Industry (Jobs), 2015-16

Agriculture, forestry, fishing & hunting,

8065, 18%

Manufacturing, 6425, 14%

Health & social services, 4088, 9%

Retail trade, 3861, 8%

Government & non-NAICs, 3746, 8%

Accommodation & food services, 2439,

5%

Professional, scientific & technical

services, 2314, 5%

Wholesale trade, 2119, 5%

Other services, 2110, 5%

Construction, 1704, 4%

Other, 8552, 19%

Florida Citrus Production by County, 2015-16

Source: FDACS

• Top five producing counties1. Hendry2. DeSoto3. Polk4. Highlands5. Hardee

• County and area level estimates of economic contributions were allocated based on the proportional distribution of production volume

Citrus production by county, 2015-16

Economic Contributions of the Florida Citrus Industry by Production Area, 2015-16

Economic Contributions of the Florida Citrus Industry by Production Area, 2015-16

• Central, share of 2015 economy Employment contributions: 2.7 percent Value added contributions: 3.5 percent

• Southern, share of 2015 economy Employment contributions: 2.1 percent Value added contributions: 2.7 percent

• Western (peninsular), share of 2015 economy Employment contributions: 0.9 percent Value added contributions: 1.0 percent

Direct Employment and Value Added Contributions as a Share of 2015 Employment and Value Added by County

Employment Shares

6.01% - 13.00%

4.01% - 6.00%

1.01% - 4.00%

0.51% - 1.00%

0.01% - 0.50%

Value Added Shares

10.01% - 25.00%

4.01% - 10.00%

2.01% - 4.00%

0.51% - 2.00%

0.001% - 0.50%

Comparisons with Past Studies

29,448

19,942

15,563

34,037

27,877 27,872

2,960 2,149 1,987

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2012-13 2014-15 2015-16

Emp

loym

en

t (F

ull

tim

e a

nd

Par

t-ti

me

Jo

bs)

Growers Processors Packinghouses

4,007

2,7132,118

8,043

6,303 6,206

465 334 3080

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2012-13 2014-15 2015-16

Ind

ust

ry O

utp

ut

(Mil

lio

n D

oll

ars,

20

16

)

Growers Processors Packinghouses

Declines in total employment contributions by sector: Growers: 47% Processors: 18% Packinghouses: 33%

Declines in total output contributions by sector: Growers: 47% Processors: 23% Packinghouses: 34%

Overall employment, labor income, value added, and industry output contributions have all decreased by 31 percent in constant dollar terms between 2012-13 and 2015-16 and

by 8-9 percent between 2014-15 and 2015-16.

Economic Impacts of Citrus Greening (HLB)

Cumulative total losses attributable to HLB from 2006-07 – 2015-16 were estimated at: $4.643 billion in industry output (annual average of $464 million) $2.768 billion in value added (annual average of $277 million) $1.760 billion in labor income (annual average of $176 million) 34,124 job-years (annual average of 3,412 ongoing full- and part-time jobs)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Tota

l gr

ow

er

reve

nu

es

rece

ive

d (

mill

ion

$)

Without HLB With HLB

Economic Impacts of Citrus Greening (HLB)

Cumulative total losses attributable to HLB from 2012-13 – 2015-16 were estimated at: $4.393 billion in industry output (annual average of $1.098 billion) $2.631 billion in value added (annual average of $658 million) $1.673 billion in labor income (annual average of $418 million) 31,778 job-years (annual average of 7,945 ongoing full- and part-time jobs)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Tota

l gr

ow

er

reve

nu

es

rece

ive

d (

mill

ion

$)

Without HLB With HLB

Corresponding Author Contact Information:

Christa D. Court

(352) 294-7675

Alan W. Hodges

(352) 294-7674

Connect. Explore. Engage.

/fred.ifas.ufl

@UF_IFAS_FRED