economic and housing outlookmedia01.commpartners.com/nahb/042215_spring_forecast/... ·...

TRANSCRIPT

ECONOMIC AND HOUSING OUTLOOK

David Crowe

Chief Economist

Spring Construction Forecast Webinar

April 22, 2015

Macro Indicators

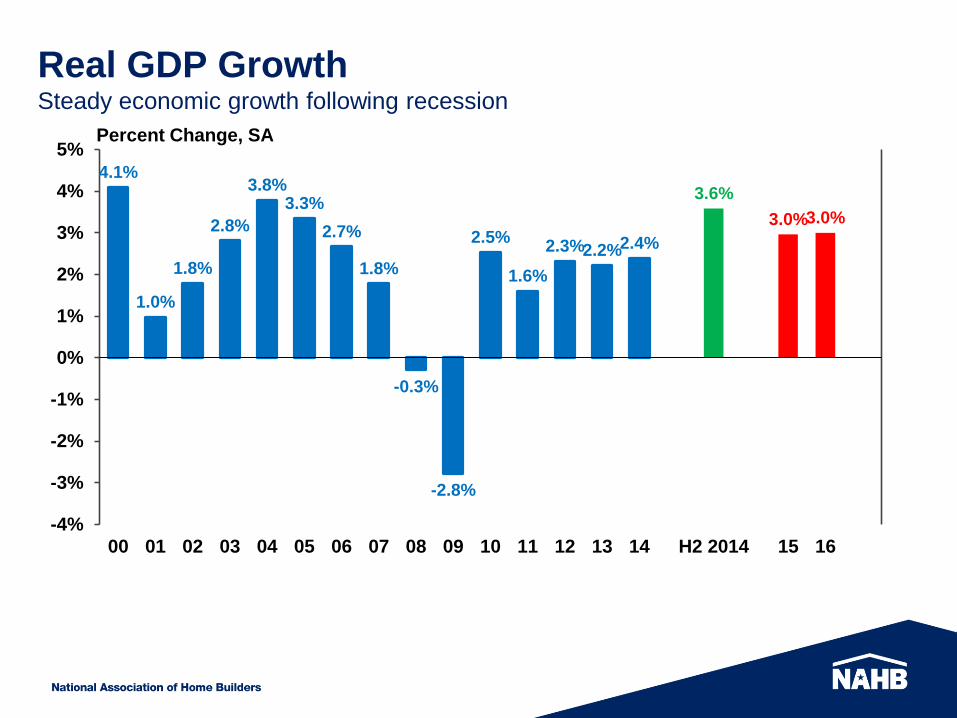

4.1%

1.0%

1.8%

2.8%

3.8% 3.3%

2.7%

1.8%

-0.3%

-2.8%

2.5%

1.6%

2.3% 2.2% 2.4%

3.6%

3.0% 3.0%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 H2 2014 15 16

Percent Change, SA

Real GDP Growth Steady economic growth following recession

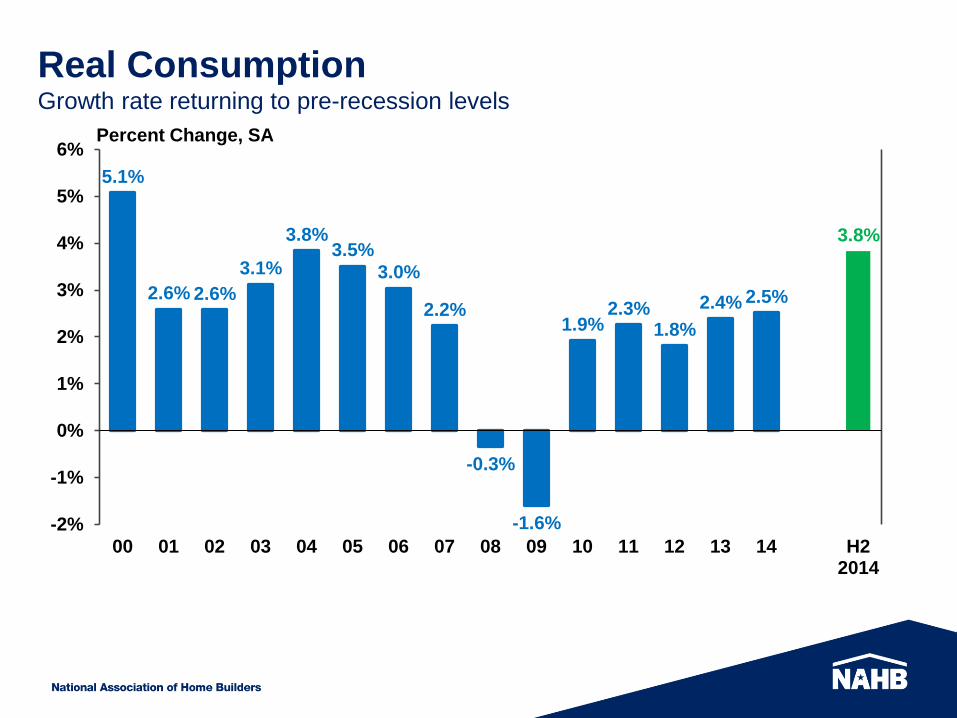

5.1%

2.6% 2.6%

3.1%

3.8% 3.5%

3.0%

2.2%

-0.3%

-1.6%

1.9% 2.3%

1.8%

2.4% 2.5%

3.8%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 H22014

Percent Change, SA

Real Consumption Growth rate returning to pre-recession levels

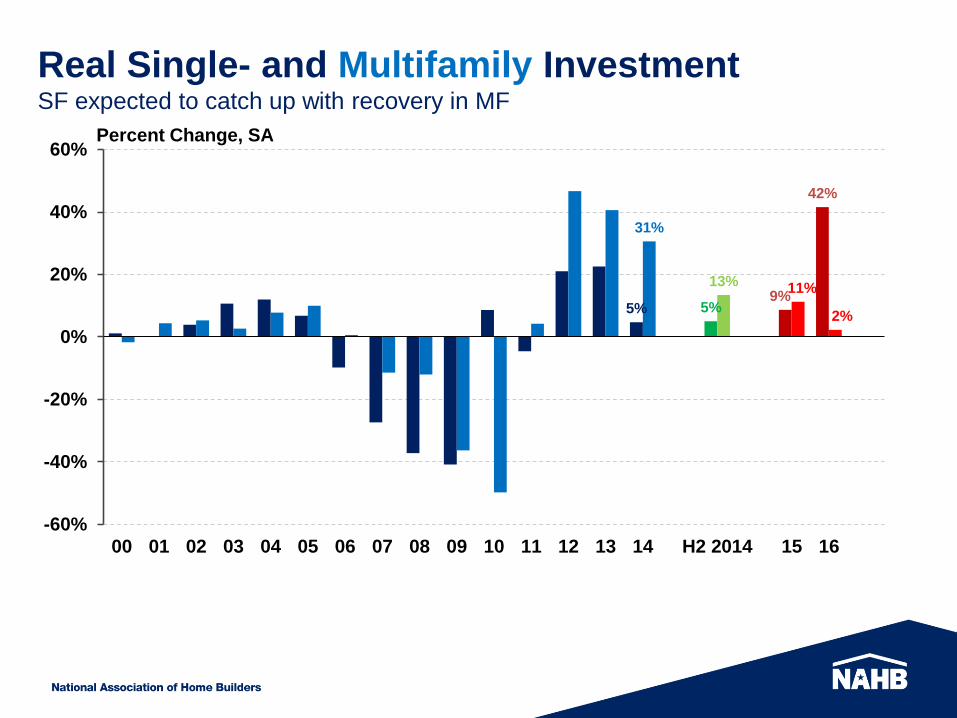

5% 5% 9%

42%

31%

13% 11%

2%

-60%

-40%

-20%

0%

20%

40%

60%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 H2 2014 15 16

Percent Change, SA

Real Single- and Multifamily Investment SF expected to catch up with recovery in MF

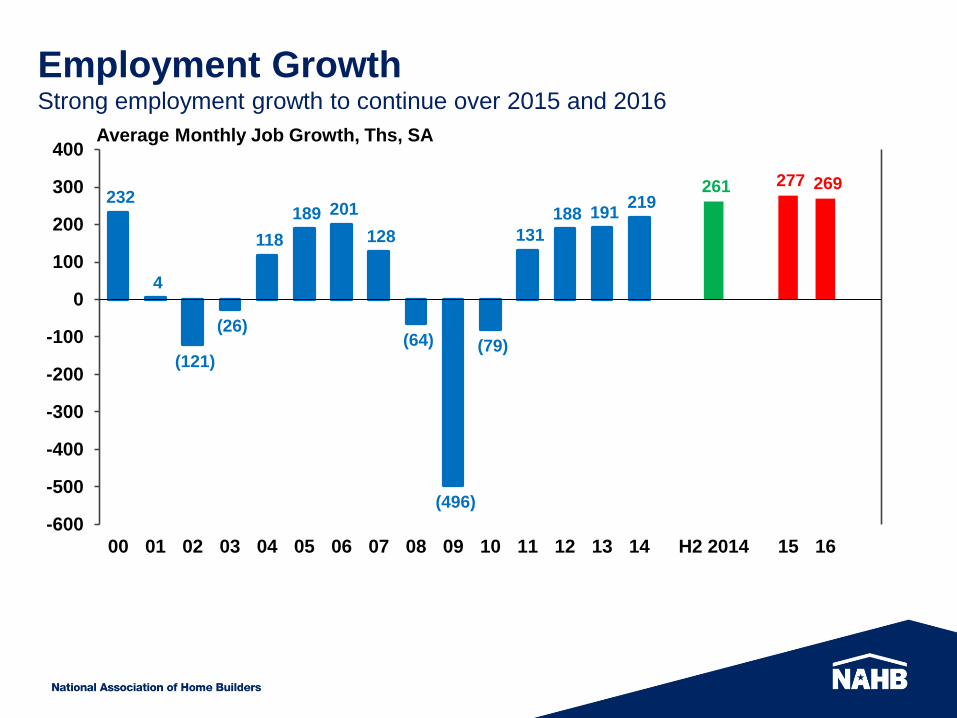

232

4

(121)

(26)

118

189 201

128

(64)

(496)

(79)

131

188 191 219

261 277 269

-600

-500

-400

-300

-200

-100

0

100

200

300

400

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 H2 2014 15 16

Average Monthly Job Growth, Ths, SA

Employment Growth Strong employment growth to continue over 2015 and 2016

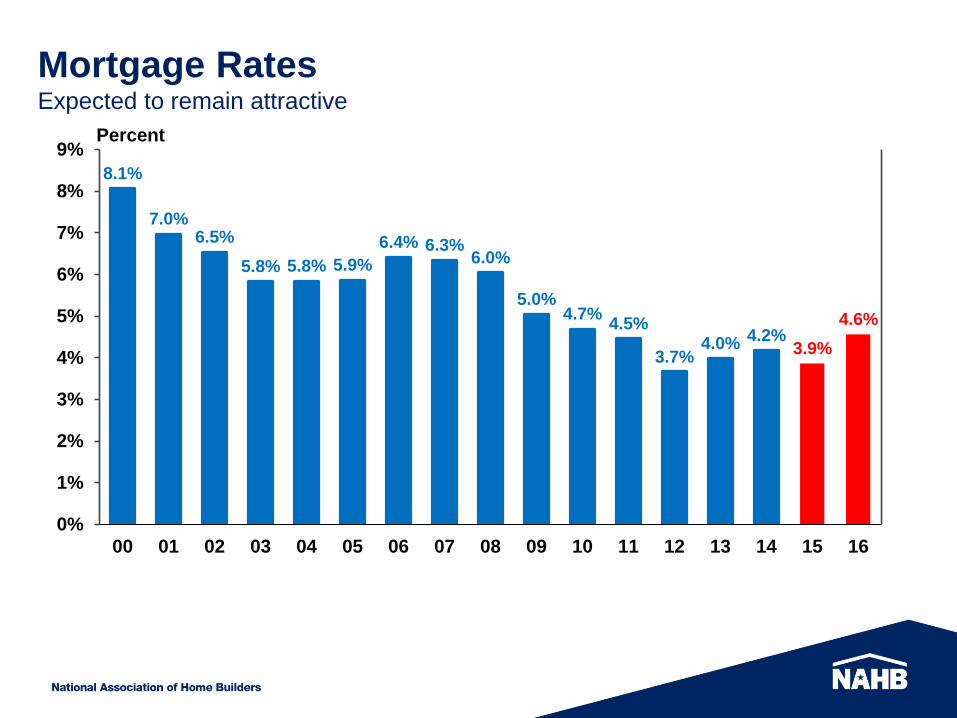

8.1%

7.0% 6.5%

5.8% 5.8% 5.9%

6.4% 6.3% 6.0%

5.0% 4.7%

4.5%

3.7% 4.0% 4.2%

3.9%

4.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Percent

Mortgage Rates Expected to remain attractive

20

40

60

80

100

120

140

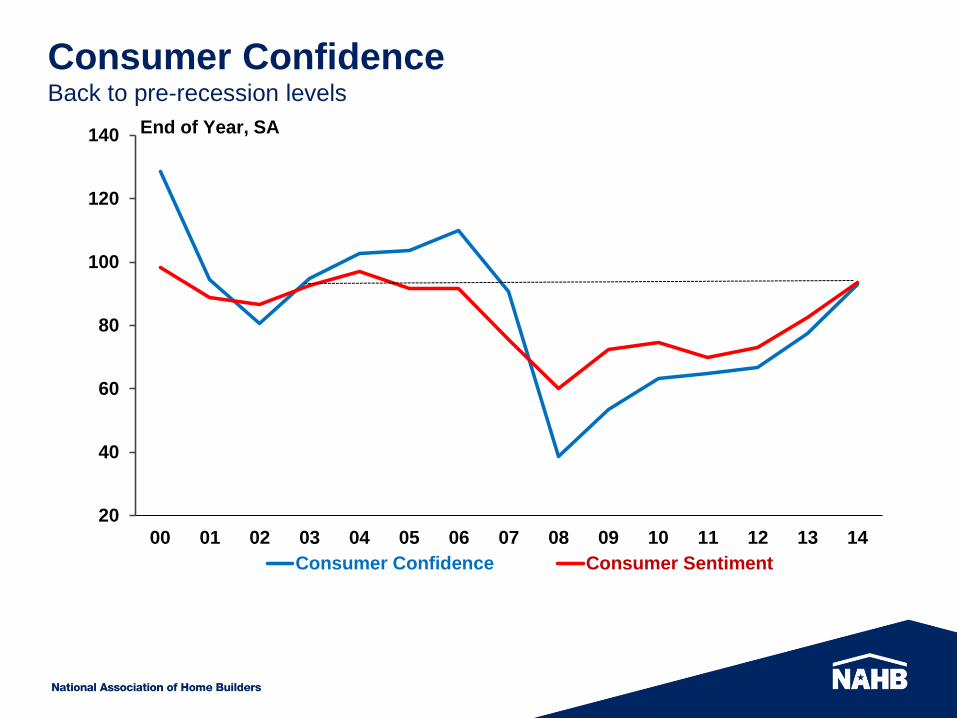

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Consumer Confidence Consumer Sentiment

End of Year, SA

Consumer Confidence Back to pre-recession levels

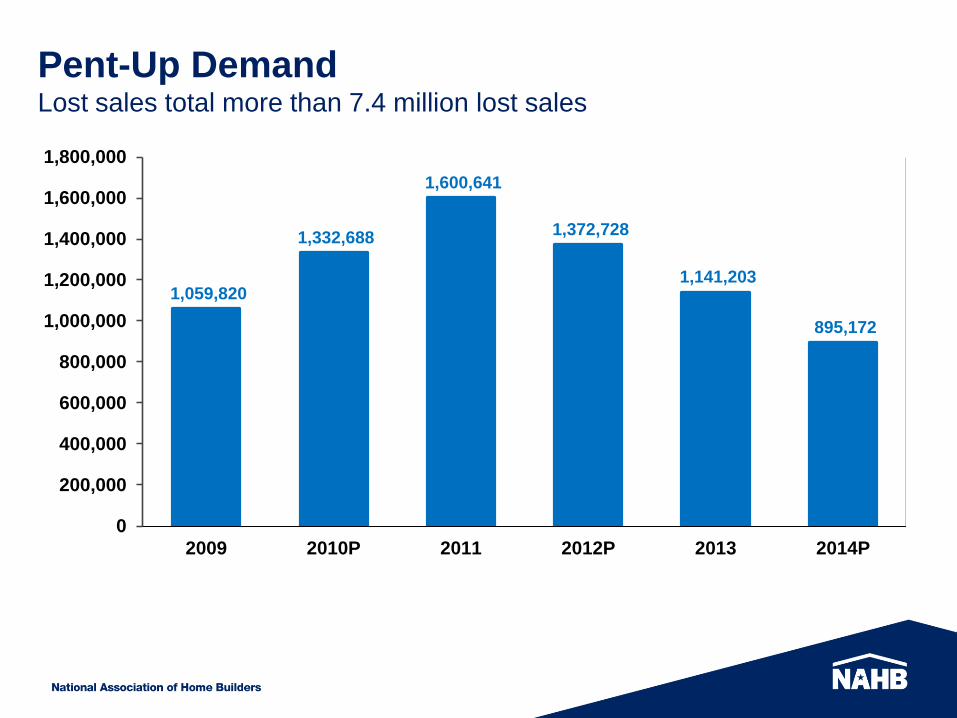

1,059,820

1,332,688

1,600,641

1,372,728

1,141,203

895,172

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2009 2010P 2011 2012P 2013 2014P

Pent-Up Demand Lost sales total more than 7.4 million lost sales

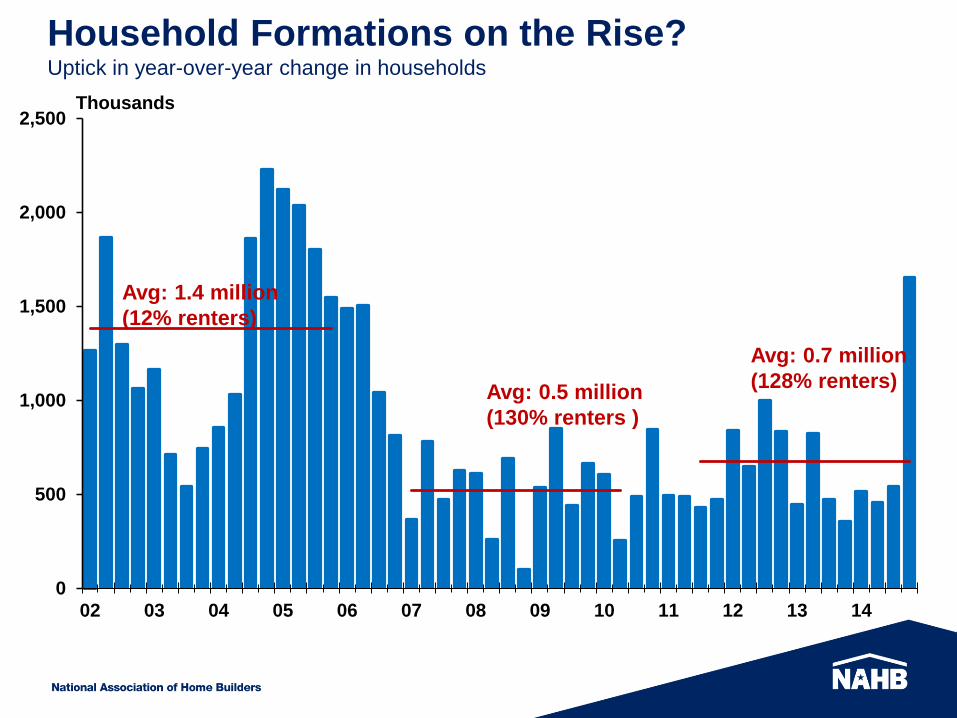

Household Formations on the Rise? Uptick in year-over-year change in households

0

500

1,000

1,500

2,000

2,500

02 03 04 05 06 07 08 09 10 11 12 13 14

Thousands

Avg: 1.4 million

(12% renters)

Avg: 0.5 million

(130% renters )

Avg: 0.7 million

(128% renters)

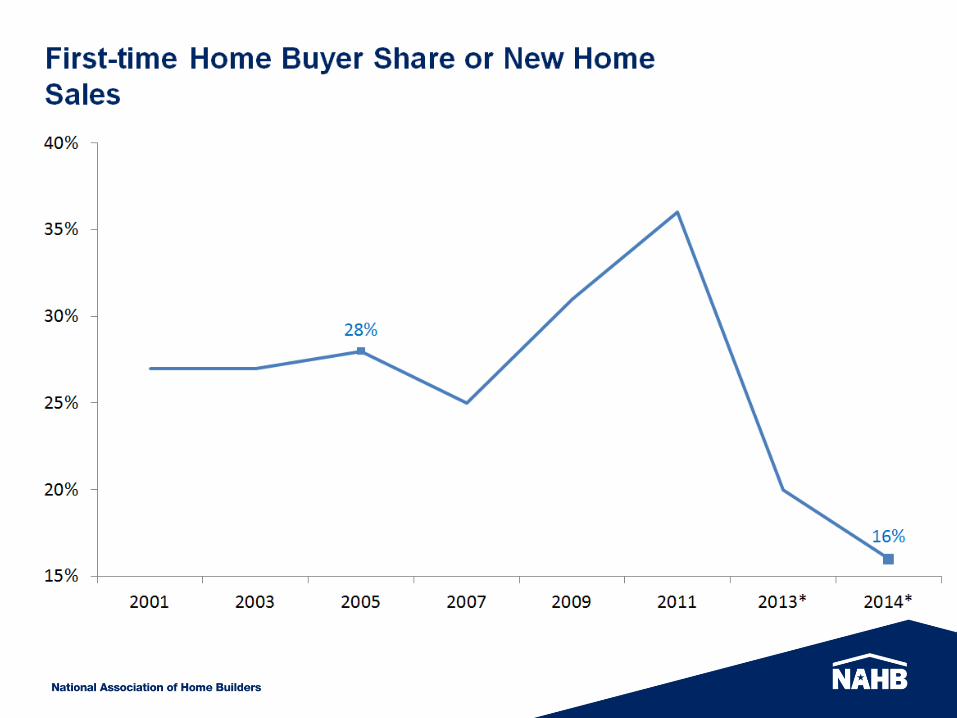

First-time Home Buyers

First-time Home Buyer Share of Existing

Home Sales

2/15: [VALUE]

42%

0%

10%

20%

30%

40%

50%

60%

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

13

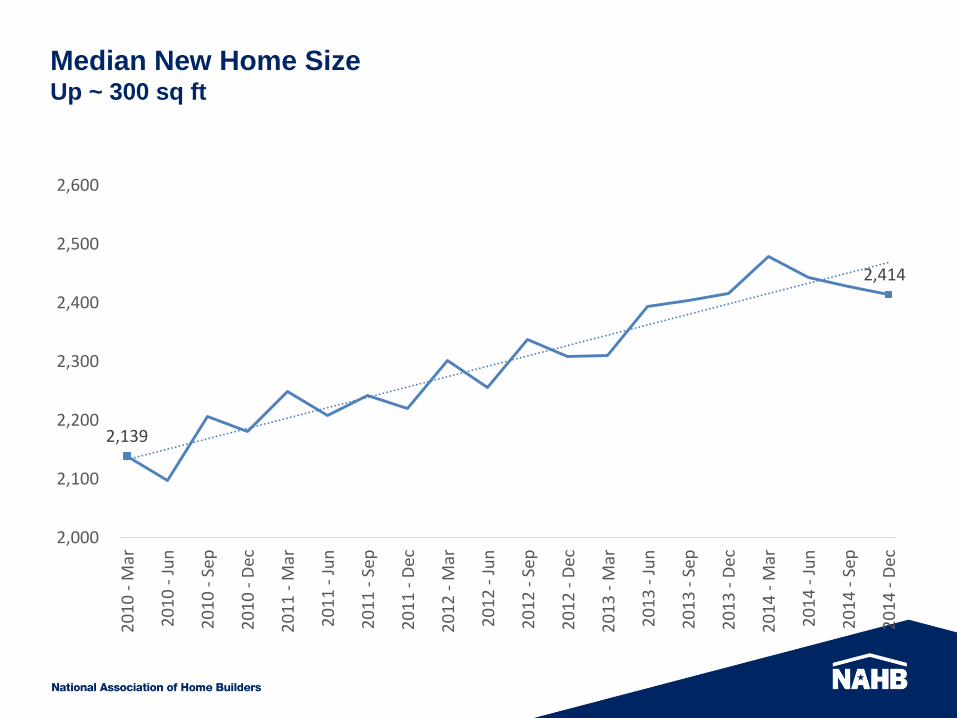

Median New Home Size Up ~ 300 sq ft

2,139

2,414

2,000

2,100

2,200

2,300

2,400

2,500

2,600

20

10

- M

ar

20

10

- J

un

20

10

- S

ep

20

10

- D

ec

20

11

- M

ar

20

11

- J

un

20

11

- S

ep

20

11

- D

ec

20

12

- M

ar

20

12

- J

un

20

12

- S

ep

20

12

- D

ec

20

13

- M

ar

20

13

- J

un

20

13

- S

ep

20

13

- D

ec

20

14

- M

ar

20

14

- J

un

20

14

- S

ep

20

14

- D

ec

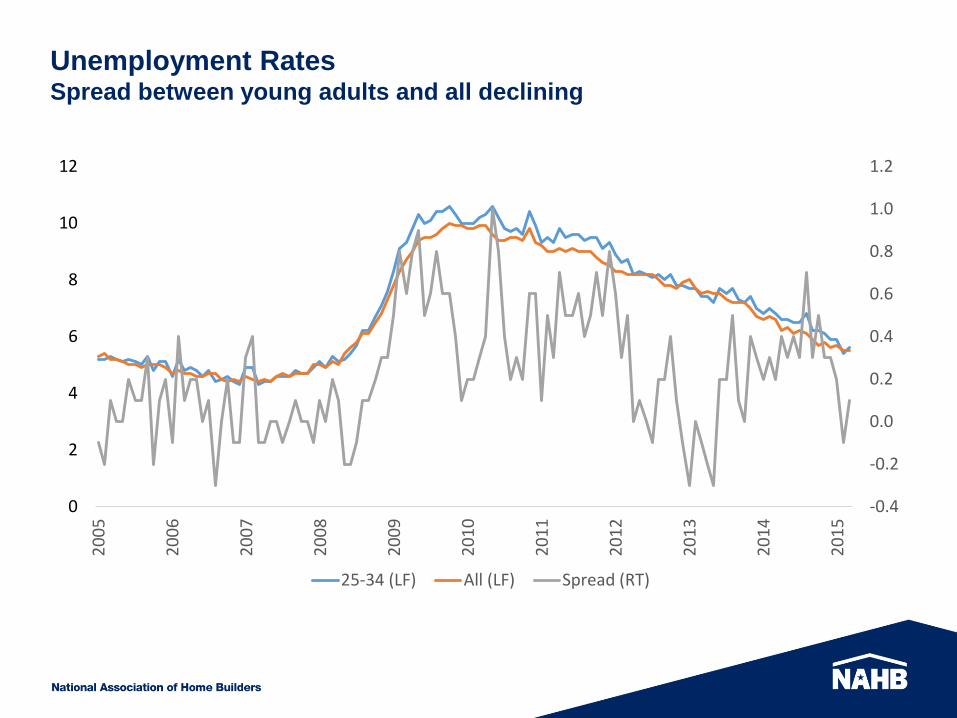

Unemployment Rates Spread between young adults and all declining

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0

2

4

6

8

10

12

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

25-34 (LF) All (LF) Spread (RT)

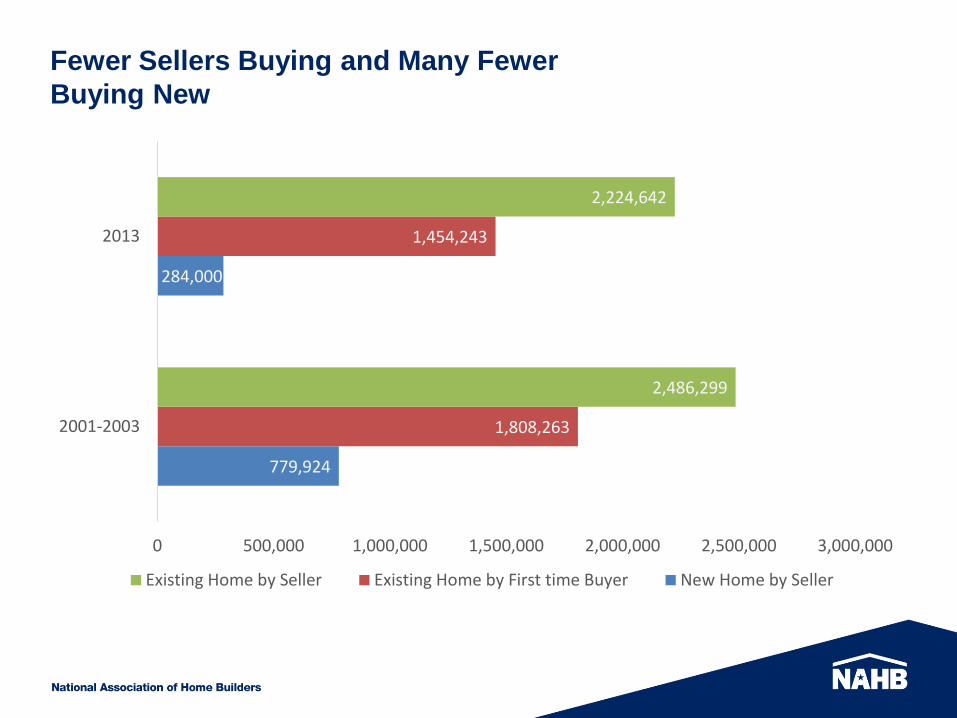

Fewer Sellers Buying and Many Fewer

Buying New

779,924

284,000

1,808,263

1,454,243

2,486,299

2,224,642

0 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000

2001-2003

2013

Existing Home by Seller Existing Home by First time Buyer New Home by Seller

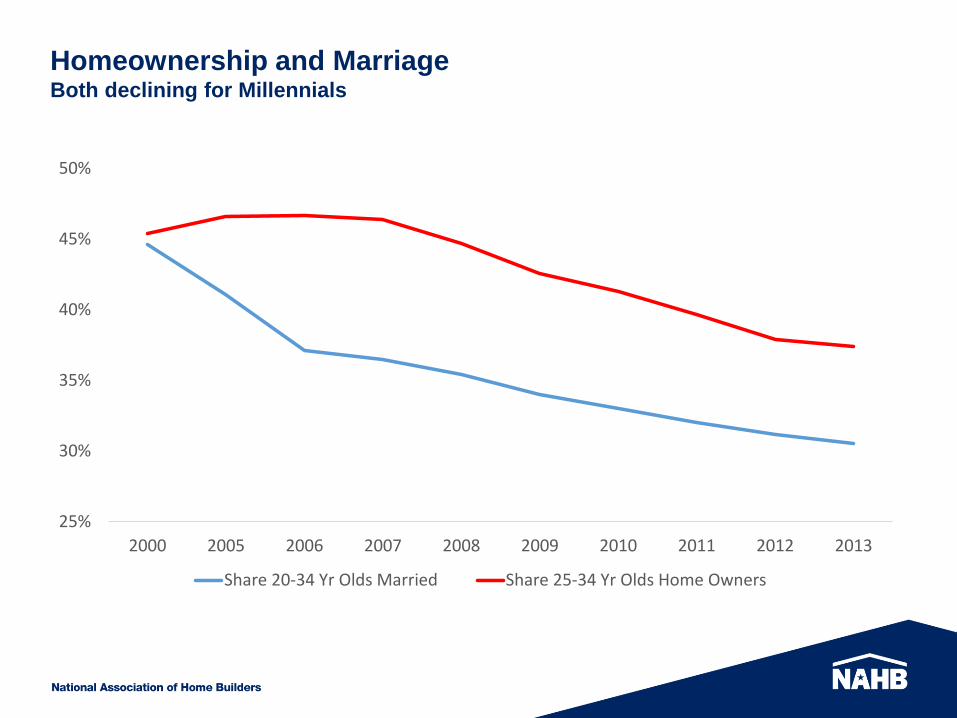

Homeownership and Marriage Both declining for Millennials

25%

30%

35%

40%

45%

50%

2000 2005 2006 2007 2008 2009 2010 2011 2012 2013

Share 20-34 Yr Olds Married Share 25-34 Yr Olds Home Owners

Forecasts

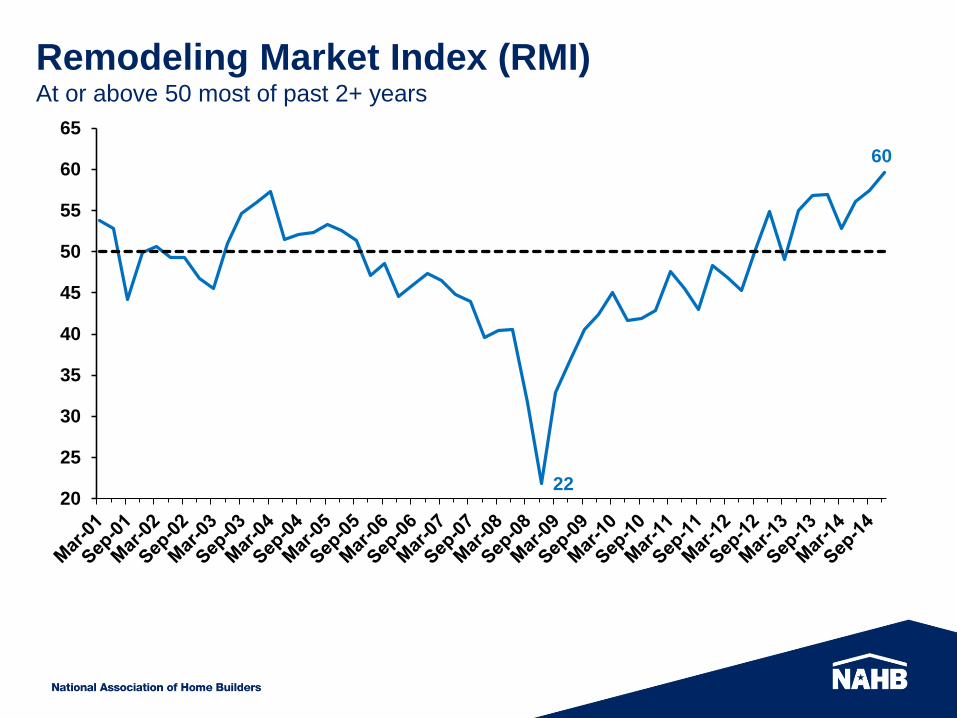

22

60

20

25

30

35

40

45

50

55

60

65

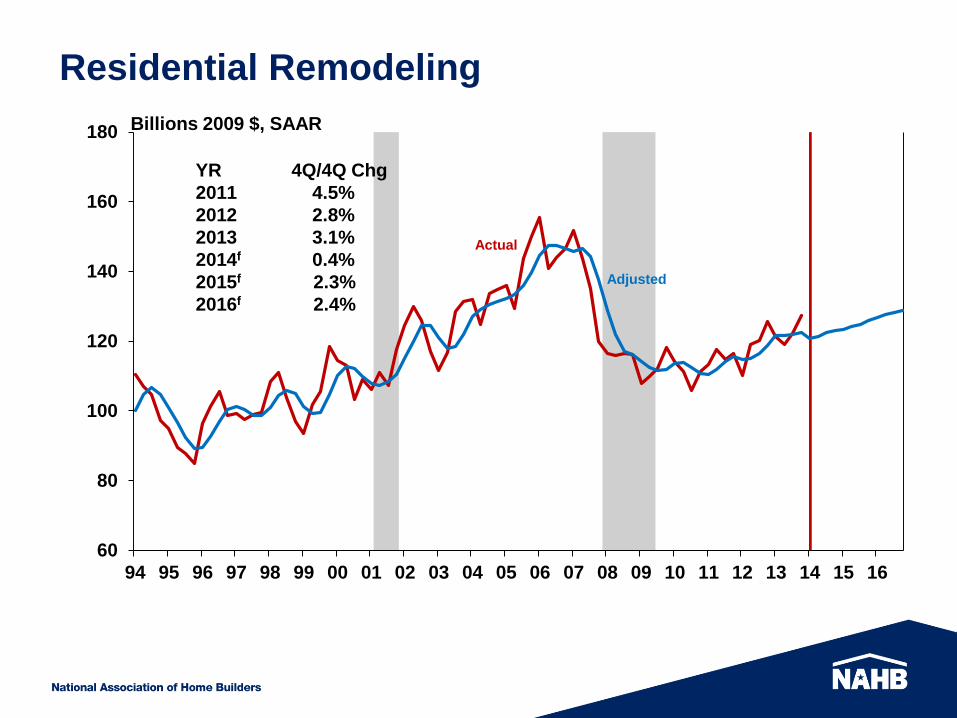

Remodeling Market Index (RMI) At or above 50 most of past 2+ years

60

80

100

120

140

160

180

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

YR 4Q/4Q Chg

2011 4.5%

2012 2.8%

2013 3.1%

2014f 0.4%

2015f 2.3%

2016f 2.4%

Residential Remodeling

Billions 2009 $, SAAR

Actual

Adjusted

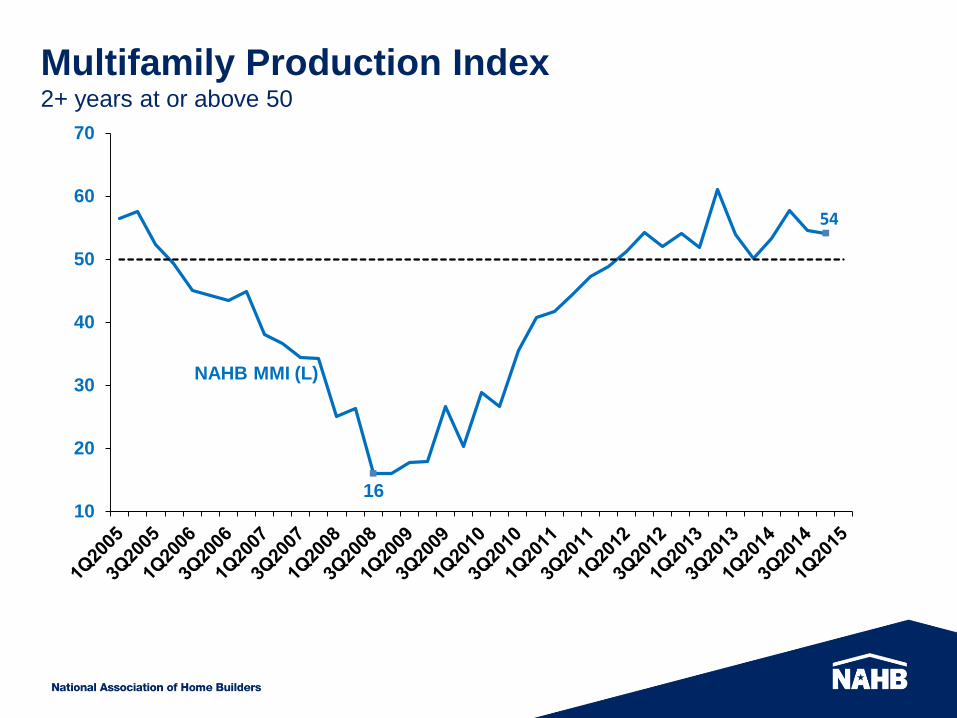

Multifamily Production Index 2+ years at or above 50

54

10

20

30

40

50

60

70

NAHB MMI (L)

16

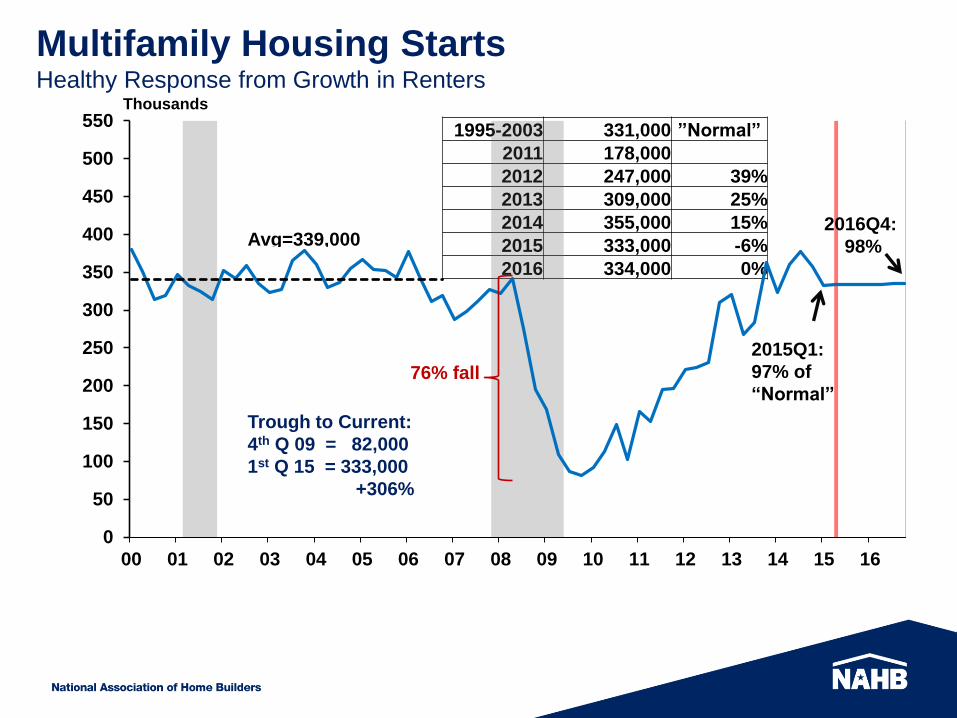

1995-2003 331,000 ”Normal”

2011 178,000

2012 247,000 39%

2013 309,000 25%

2014 355,000 15%

2015 333,000 -6%

2016 334,000 0%

Multifamily Housing Starts Healthy Response from Growth in Renters

Trough to Current:

4th Q 09 = 82,000

1st Q 15 = 333,000

+306%

2015Q1:

97% of

“Normal”

0

50

100

150

200

250

300

350

400

450

500

550

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Thousands

76% fall

2016Q4:

98% Avg=339,000

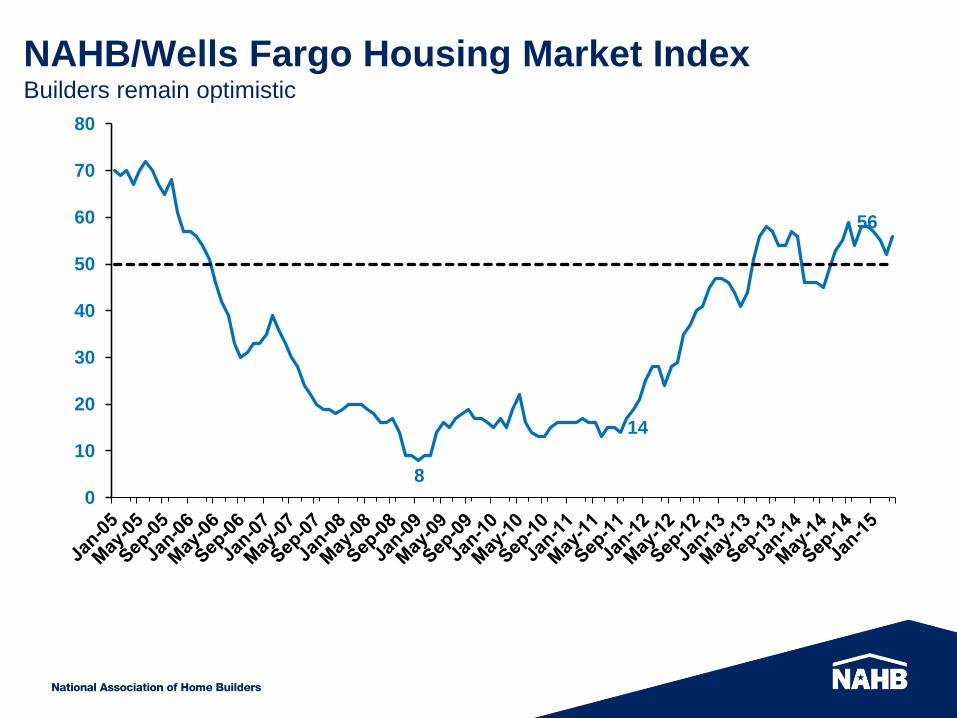

8

14

56

0

10

20

30

40

50

60

70

80

NAHB/Wells Fargo Housing Market Index Builders remain optimistic

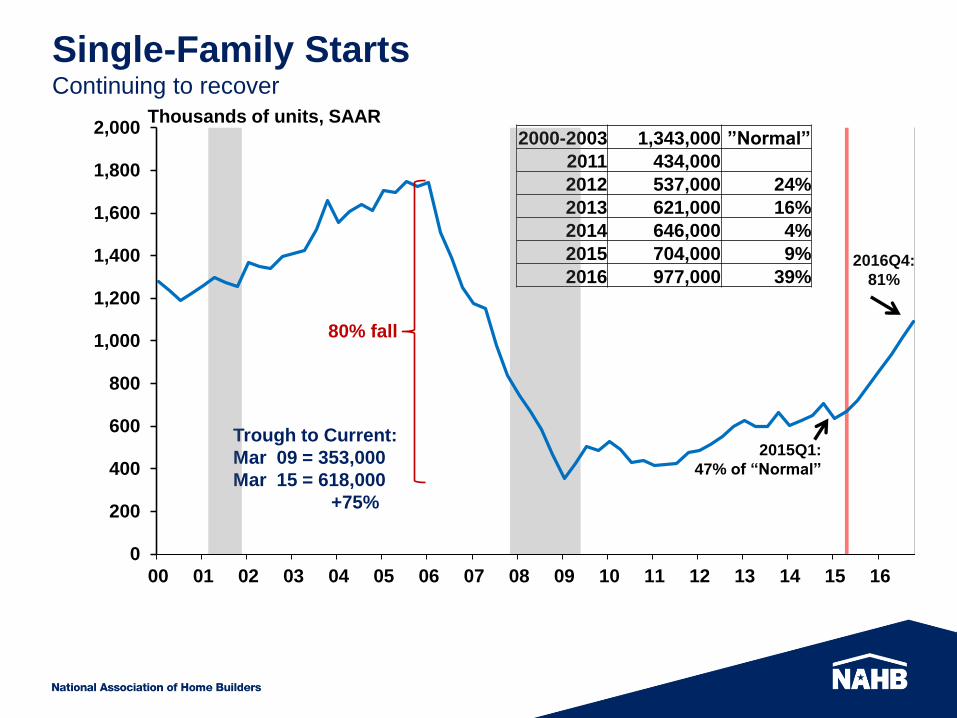

Single-Family Starts Continuing to recover

Trough to Current:

Mar 09 = 353,000

Mar 15 = 618,000

+75%

2015Q1:

47% of “Normal”

2016Q4:

81%

2000-2003 1,343,000 ”Normal”

2011 434,000

2012 537,000 24%

2013 621,000 16%

2014 646,000 4%

2015 704,000 9%

2016 977,000 39%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Thousands of units, SAAR

80% fall

New Home Market Update

Construction Forecast Conference

National Association of Home Builders

April, 2015

Outline

New home sale volumes weak, but pockets of strength exist

Eight of top 10 healthiest new sale markets in Carolinas and Texas

Waning supply of distressed sales will increase demand for lower-end new

homes

Relative to early 2000s, only 3 markets have higher new sales volumes

New home price growth fastest in coastal states and new price premium

approaching $100,000

Houston employment collapses in March. Is housing next?

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 26

New Home Sales Market

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 27

Very Slow Improvement

Note: CoreLogic data lagged by two months

Source: CoreLogic and Census

0

10,000

20,000

30,000

40,000

50,000

60,000

Ja

n-0

8

Apr-

08

Ju

l-0

8

Oct-

08

Ja

n-0

9

Apr-

09

Ju

l-0

9

Oct-

09

Ja

n-1

0

Apr-

10

Ju

l-1

0

Oct-

10

Ja

n-1

1

Apr-

11

Ju

l-1

1

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-1

2

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-1

3

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-1

4

Oct-

14

CoreLogic

Census

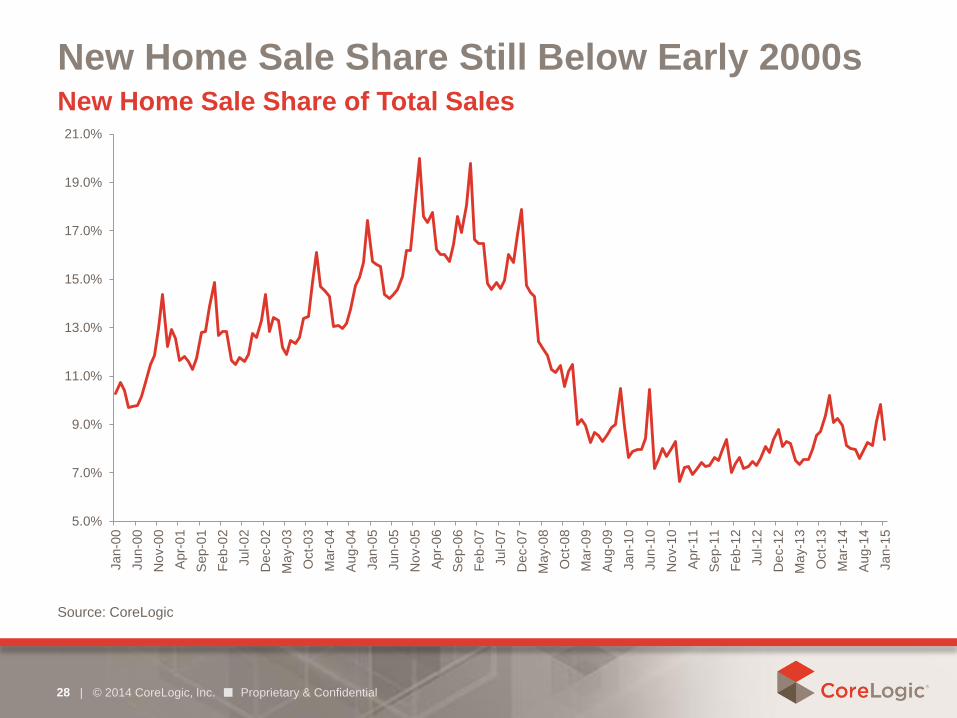

New Home Sale Share Still Below Early 2000s

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 28

New Home Sale Share of Total Sales

Source: CoreLogic

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

Jan-0

0

Jun-0

0

No

v-0

0

Apr-

01

Sep-0

1

Feb

-02

Jul-0

2

De

c-0

2

Ma

y-0

3

Oct-

03

Ma

r-0

4

Aug-0

4

Jan-0

5

Jun-0

5

No

v-0

5

Apr-

06

Sep-0

6

Feb

-07

Jul-0

7

De

c-0

7

Ma

y-0

8

Oct-

08

Ma

r-0

9

Aug-0

9

Jan-1

0

Jun-1

0

No

v-1

0

Apr-

11

Sep-1

1

Feb

-12

Jul-1

2

De

c-1

2

Ma

y-1

3

Oct-

13

Ma

r-1

4

Aug-1

4

Jan-1

5

Healthiest New Sale Markets in Texas and Carolina’s

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 29

Avg Monthly Number of New Sales Last 12 Months

Source: CoreLogic

0% 5% 10% 15% 20% 25%

El Paso, TX

Raleigh, NC

Charleston-North Charleston, SC

Houston-The Woodlands-Sugar…

San Antonio-New Braunfels, TX

Columbia, SC

Austin-Round Rock, TX

Charlotte-Concord-Gastonia, NC-SC

Jacksonville, FL

Baton Rouge, LA

Colorado Springs, CO

Orlando-Kissimmee-Sanford, FL

Dallas-Plano-Irving, TX

Fresno, CA

Oklahoma City, OK

Washington-Arlington-Alexandria,…

Boise City, ID

Greenville-Anderson-Mauldin, SC

Las Vegas-Henderson-Paradise, NV

Nashville-Davidson--…

- 500 1,000 1,500 2,000 2,500

Houston-The Woodlands-Sugar…

Dallas-Plano-Irving, TX

Atlanta-Sandy Springs-Roswell, GA

Phoenix-Mesa-Scottsdale, AZ

Washington-Arlington-Alexandria,…

San Antonio-New Braunfels, TX

Austin-Round Rock, TX

Orlando-Kissimmee-Sanford, FL

Charlotte-Concord-Gastonia, NC-SC

New York-Jersey City-White…

Las Vegas-Henderson-Paradise, NV

Tampa-St Petersburg-Clearwater,…

Denver-Aurora-Lakewood, CO

Fort Worth-Arlington, TX

Nashville-Davidson--…

Jacksonville, FL

Seattle-Bellevue-Everett, WA

Riverside-San Bernardino-…

Raleigh, NC

Portland-Vancouver-Hillsboro,…

New Home Sale Share

The Top 100 Markets

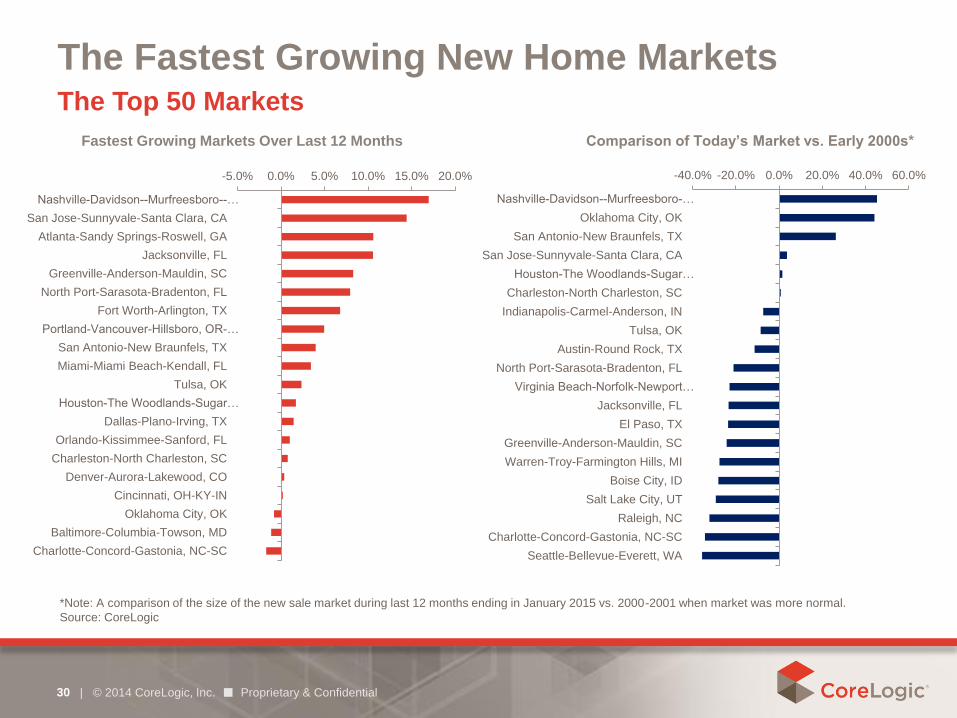

The Fastest Growing New Home Markets

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 30

The Top 50 Markets

*Note: A comparison of the size of the new sale market during last 12 months ending in January 2015 vs. 2000-2001 when market was more normal.

Source: CoreLogic

-5.0% 0.0% 5.0% 10.0% 15.0% 20.0%

Nashville-Davidson--Murfreesboro--…

San Jose-Sunnyvale-Santa Clara, CA

Atlanta-Sandy Springs-Roswell, GA

Jacksonville, FL

Greenville-Anderson-Mauldin, SC

North Port-Sarasota-Bradenton, FL

Fort Worth-Arlington, TX

Portland-Vancouver-Hillsboro, OR-…

San Antonio-New Braunfels, TX

Miami-Miami Beach-Kendall, FL

Tulsa, OK

Houston-The Woodlands-Sugar…

Dallas-Plano-Irving, TX

Orlando-Kissimmee-Sanford, FL

Charleston-North Charleston, SC

Denver-Aurora-Lakewood, CO

Cincinnati, OH-KY-IN

Oklahoma City, OK

Baltimore-Columbia-Towson, MD

Charlotte-Concord-Gastonia, NC-SC

-40.0% -20.0% 0.0% 20.0% 40.0% 60.0%

Nashville-Davidson--Murfreesboro-…

Oklahoma City, OK

San Antonio-New Braunfels, TX

San Jose-Sunnyvale-Santa Clara, CA

Houston-The Woodlands-Sugar…

Charleston-North Charleston, SC

Indianapolis-Carmel-Anderson, IN

Tulsa, OK

Austin-Round Rock, TX

North Port-Sarasota-Bradenton, FL

Virginia Beach-Norfolk-Newport…

Jacksonville, FL

El Paso, TX

Greenville-Anderson-Mauldin, SC

Warren-Troy-Farmington Hills, MI

Boise City, ID

Salt Lake City, UT

Raleigh, NC

Charlotte-Concord-Gastonia, NC-SC

Seattle-Bellevue-Everett, WA

Fastest Growing Markets Over Last 12 Months Comparison of Today’s Market vs. Early 2000s*

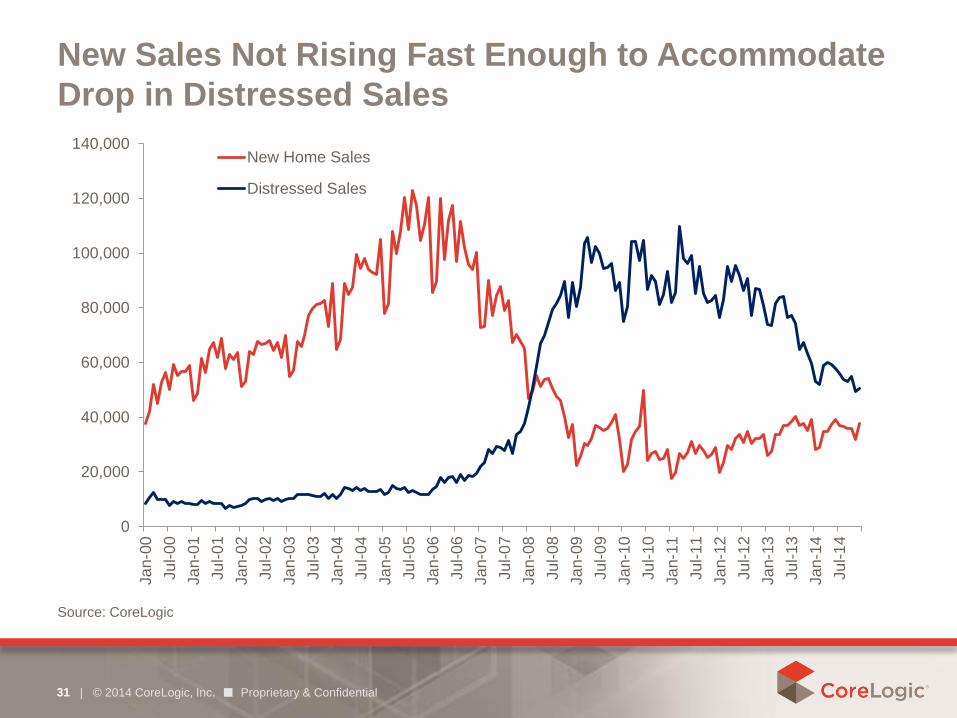

New Sales Not Rising Fast Enough to Accommodate

Drop in Distressed Sales

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 31

Source: CoreLogic

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000Ja

n-0

0

Ju

l-0

0

Ja

n-0

1

Ju

l-0

1

Ja

n-0

2

Ju

l-0

2

Ja

n-0

3

Ju

l-0

3

Ja

n-0

4

Ju

l-0

4

Ja

n-0

5

Ju

l-0

5

Ja

n-0

6

Ju

l-0

6

Ja

n-0

7

Ju

l-0

7

Ja

n-0

8

Ju

l-0

8

Ja

n-0

9

Ju

l-0

9

Ja

n-1

0

Ju

l-1

0

Ja

n-1

1

Ju

l-1

1

Ja

n-1

2

Ju

l-1

2

Ja

n-1

3

Ju

l-1

3

Ja

n-1

4

Ju

l-1

4

New Home Sales

Distressed Sales

Market Snapshots

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 32

Atlanta, GA

Austin, TX

Cape Coral, FL Chicago, IL

Nashville, TN Phoenix, AZ

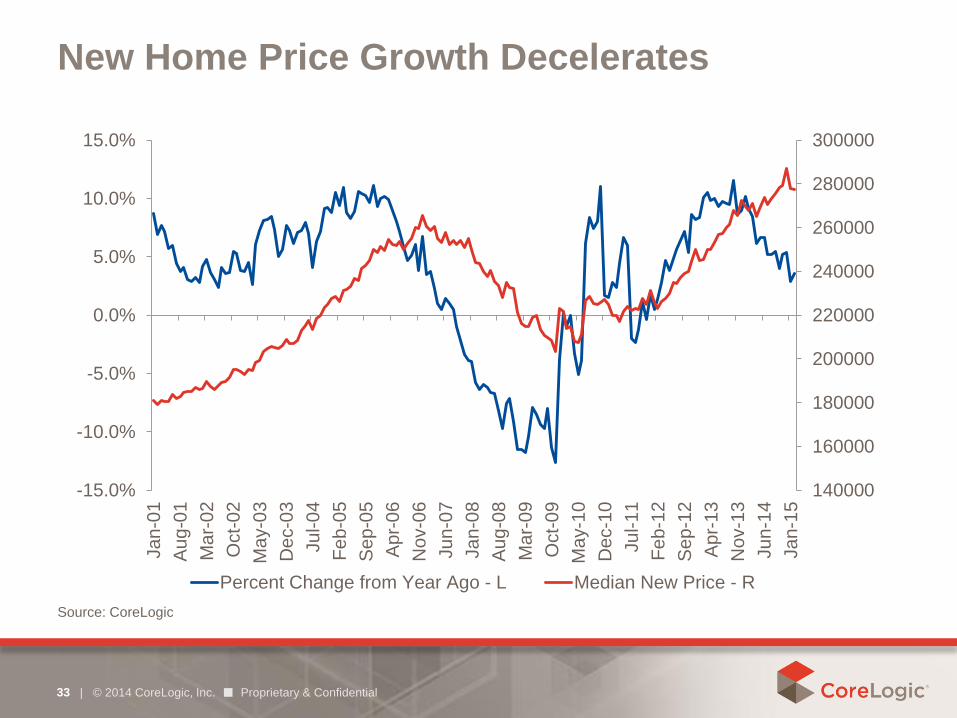

New Home Price Growth Decelerates

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 33

Source: CoreLogic

140000

160000

180000

200000

220000

240000

260000

280000

300000

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%Ja

n-0

1

Au

g-0

1

Mar-

02

Oct-

02

Ma

y-0

3

De

c-0

3

Ju

l-0

4

Fe

b-0

5

Se

p-0

5

Ap

r-0

6

No

v-0

6

Ju

n-0

7

Ja

n-0

8

Au

g-0

8

Ma

r-0

9

Oct-

09

Ma

y-1

0

De

c-1

0

Ju

l-1

1

Fe

b-1

2

Se

p-1

2

Ap

r-1

3

No

v-1

3

Ju

n-1

4

Ja

n-1

5

Percent Change from Year Ago - L Median New Price - R

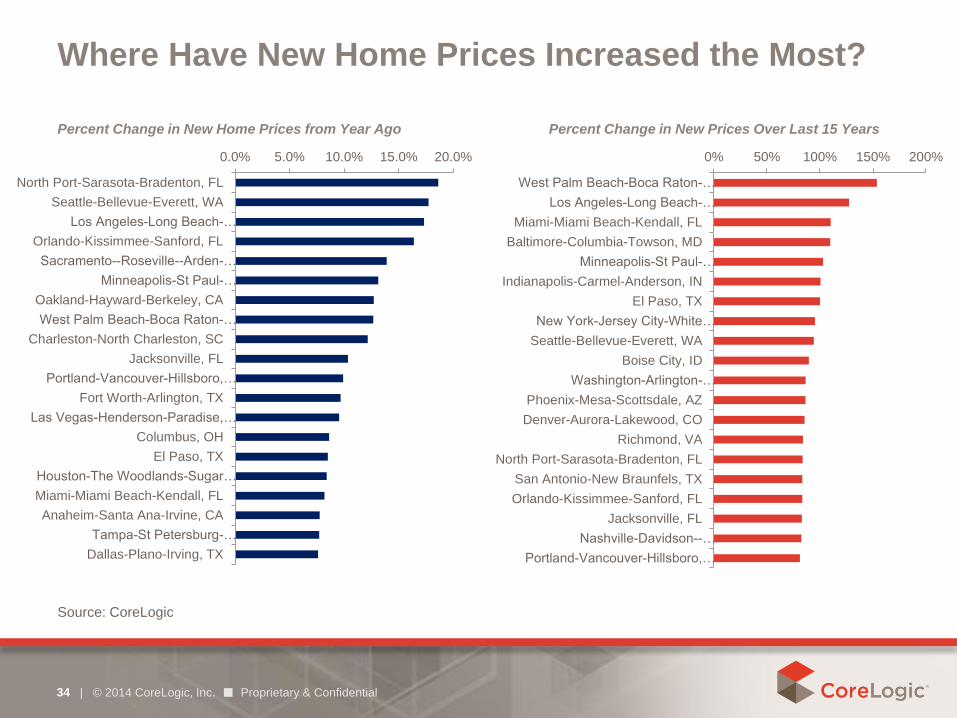

Where Have New Home Prices Increased the Most?

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 34

Percent Change in New Home Prices from Year Ago

Source: CoreLogic

0.0% 5.0% 10.0% 15.0% 20.0%

North Port-Sarasota-Bradenton, FL

Seattle-Bellevue-Everett, WA

Los Angeles-Long Beach-…

Orlando-Kissimmee-Sanford, FL

Sacramento--Roseville--Arden-…

Minneapolis-St Paul-…

Oakland-Hayward-Berkeley, CA

West Palm Beach-Boca Raton-…

Charleston-North Charleston, SC

Jacksonville, FL

Portland-Vancouver-Hillsboro,…

Fort Worth-Arlington, TX

Las Vegas-Henderson-Paradise,…

Columbus, OH

El Paso, TX

Houston-The Woodlands-Sugar…

Miami-Miami Beach-Kendall, FL

Anaheim-Santa Ana-Irvine, CA

Tampa-St Petersburg-…

Dallas-Plano-Irving, TX

0% 50% 100% 150% 200%

West Palm Beach-Boca Raton-…

Los Angeles-Long Beach-…

Miami-Miami Beach-Kendall, FL

Baltimore-Columbia-Towson, MD

Minneapolis-St Paul-…

Indianapolis-Carmel-Anderson, IN

El Paso, TX

New York-Jersey City-White…

Seattle-Bellevue-Everett, WA

Boise City, ID

Washington-Arlington-…

Phoenix-Mesa-Scottsdale, AZ

Denver-Aurora-Lakewood, CO

Richmond, VA

North Port-Sarasota-Bradenton, FL

San Antonio-New Braunfels, TX

Orlando-Kissimmee-Sanford, FL

Jacksonville, FL

Nashville-Davidson--…

Portland-Vancouver-Hillsboro,…

Percent Change in New Prices Over Last 15 Years

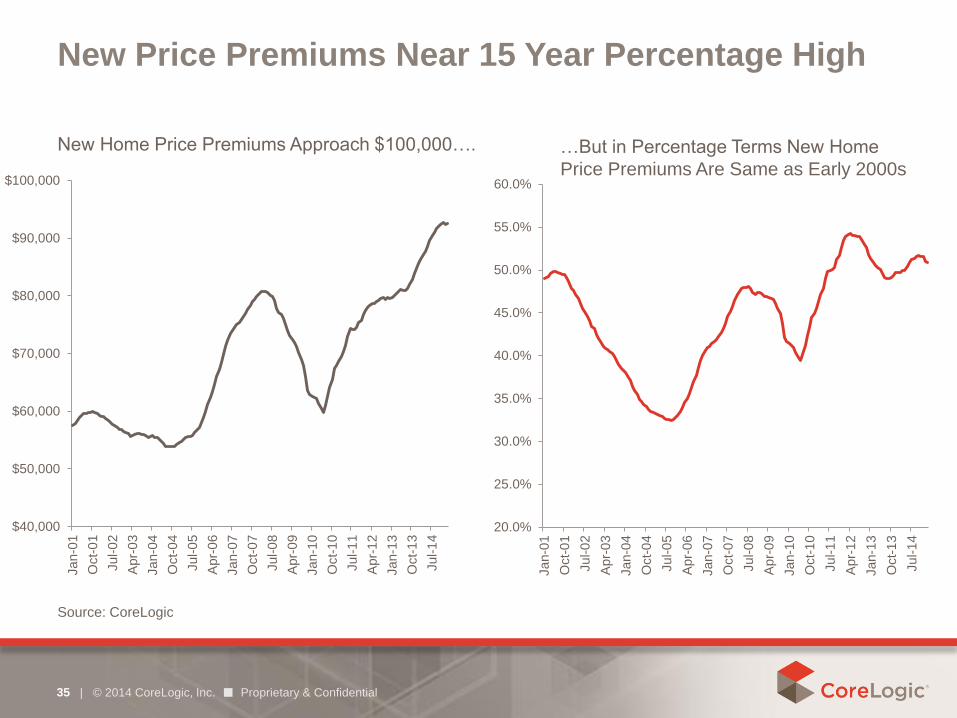

New Price Premiums Near 15 Year Percentage High

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 35

Source: CoreLogic

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

Jan-0

1

Oct-

01

Jul-0

2

Apr-

03

Jan-0

4

Oct-

04

Jul-0

5

Apr-

06

Jan-0

7

Oct-

07

Jul-0

8

Apr-

09

Jan-1

0

Oct-

10

Jul-1

1

Apr-

12

Jan-1

3

Oct-

13

Jul-1

4

New Home Price Premiums Approach $100,000….

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

Jan-0

1

Oct-

01

Jul-0

2

Apr-

03

Jan-0

4

Oct-

04

Jul-0

5

Apr-

06

Jan-0

7

Oct-

07

Jul-0

8

Apr-

09

Jan-1

0

Oct-

10

Jul-1

1

Apr-

12

Jan-1

3

Oct-

13

Jul-1

4

…But in Percentage Terms New Home

Price Premiums Are Same as Early 2000s

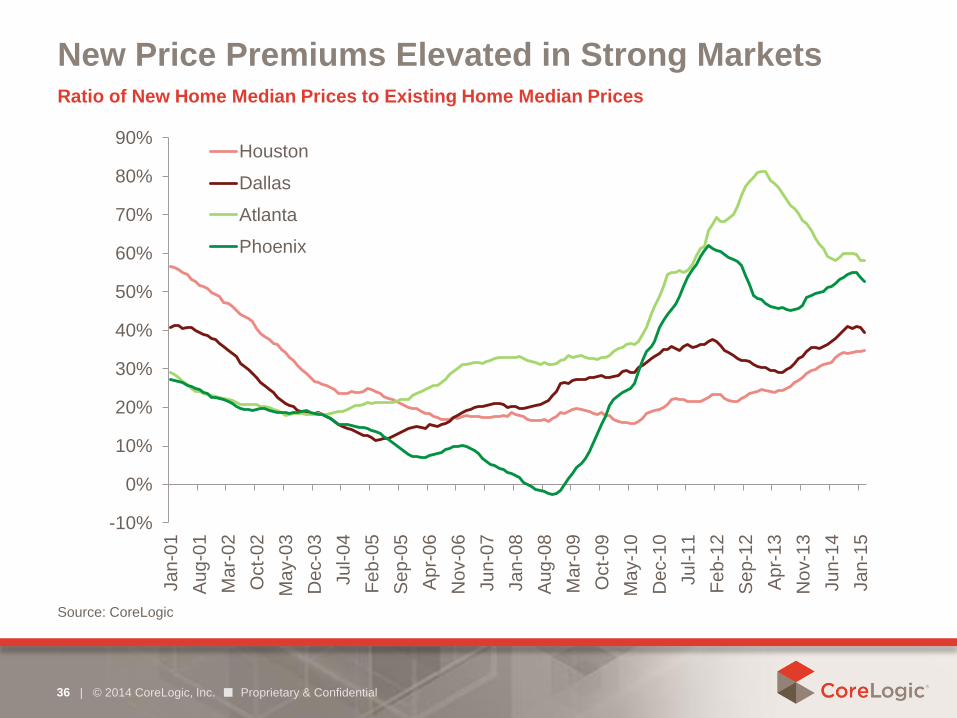

New Price Premiums Elevated in Strong Markets

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 36

Source: CoreLogic

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Jan-0

1

Au

g-0

1

Ma

r-0

2

Oct-

02

Ma

y-0

3

De

c-0

3

Ju

l-0

4

Fe

b-0

5

Se

p-0

5

Ap

r-0

6

No

v-0

6

Ju

n-0

7

Ja

n-0

8

Au

g-0

8

Ma

r-0

9

Oct-

09

Ma

y-1

0

De

c-1

0

Ju

l-1

1

Fe

b-1

2

Sep-1

2

Ap

r-1

3

No

v-1

3

Ju

n-1

4

Ja

n-1

5

Houston

Dallas

Atlanta

Phoenix

Ratio of New Home Median Prices to Existing Home Median Prices

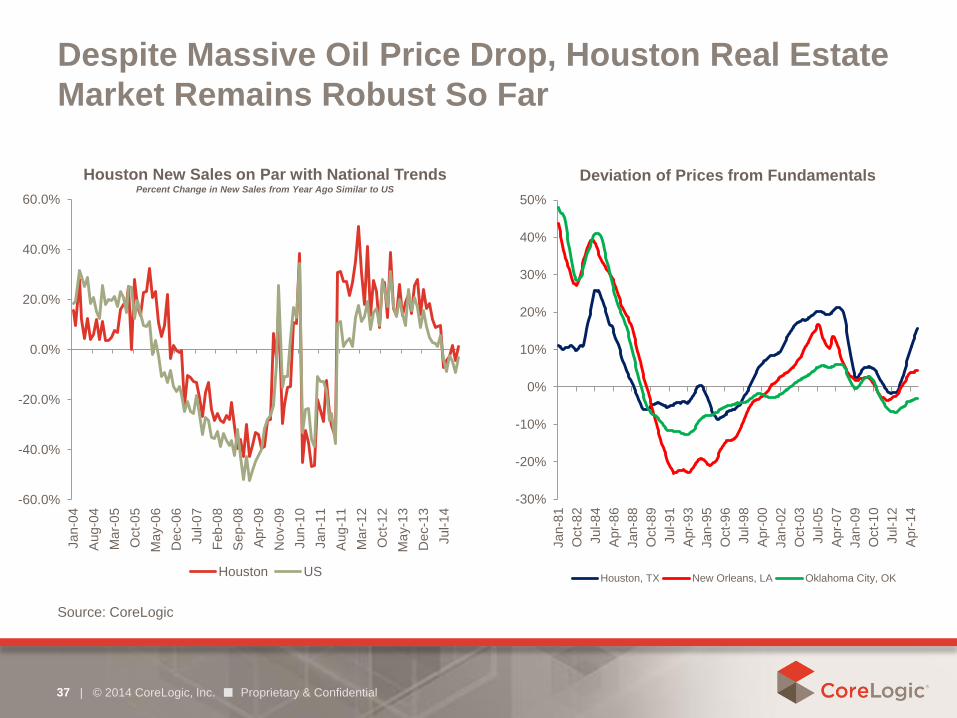

Despite Massive Oil Price Drop, Houston Real Estate

Market Remains Robust So Far

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 37

Source: CoreLogic

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Jan-8

1

Oct-

82

Jul-8

4

Apr-

86

Jan-8

8

Oct-

89

Jul-9

1

Apr-

93

Jan-9

5

Oct-

96

Jul-9

8

Apr-

00

Jan-0

2

Oct-

03

Jul-0

5

Apr-

07

Jan-0

9

Oct-

10

Jul-1

2

Apr-

14

Deviation of Prices from Fundamentals

Houston, TX New Orleans, LA Oklahoma City, OK

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

Jan-0

4

Aug-0

4

Ma

r-0

5

Oct-

05

Ma

y-0

6

De

c-0

6

Jul-0

7

Feb

-08

Sep-0

8

Apr-

09

No

v-0

9

Jun-1

0

Jan-1

1

Aug-1

1

Ma

r-1

2

Oct-

12

Ma

y-1

3

De

c-1

3

Jul-1

4

Houston US

Houston New Sales on Par with National Trends Percent Change in New Sales from Year Ago Similar to US

Thank You!

corelogic.com/blog | NYSE: CLGX

| © 2014 CoreLogic, Inc. ■ Proprietary & Confidential 38

Robert Denk

Assistant Vice President

Forecasting and Analysis

April 22, 2015

Spring 2015 Construction Forecast Webinar

Progress of Housing Market Recovery

A. Housing Market Conditions

Production

Prices

Foreclosures

Employment

B. The Forecast

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

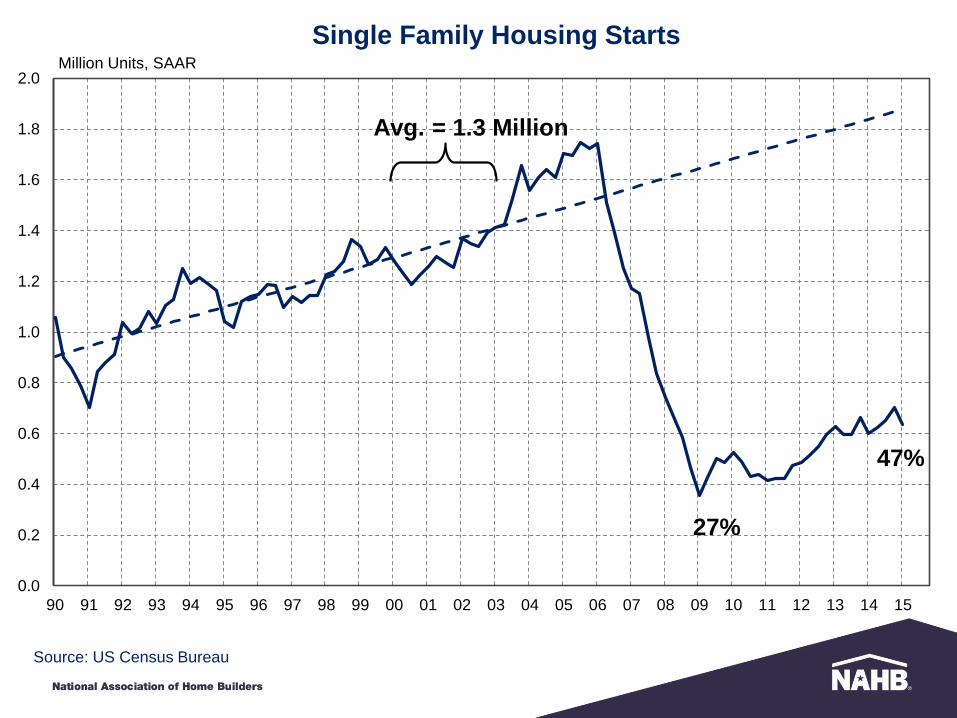

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Million Units, SAAR

Avg. = 1.3 Million

27%

47%

Single Family Housing Starts

Source: US Census Bureau

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

M

I

N

V

I

L

A

Z

M

N

C

O

C

A

F

L

G

A

O

H

M

O

I

N

W

I

N

H

C

T

R

I

N

J

O

R

K

Y

M

D

I

D

U

T

V

T

A

K

K

S

M

A

N

C

W

V

N

M

V

A

P

A

N

Y

H

I

I

A

T

N

M

S

M

E

N

E

W

A

D

E

D

C

N

D

S

D

S

C

A

R

A

L

T

X

O

K

L

A

M

T

W

Y

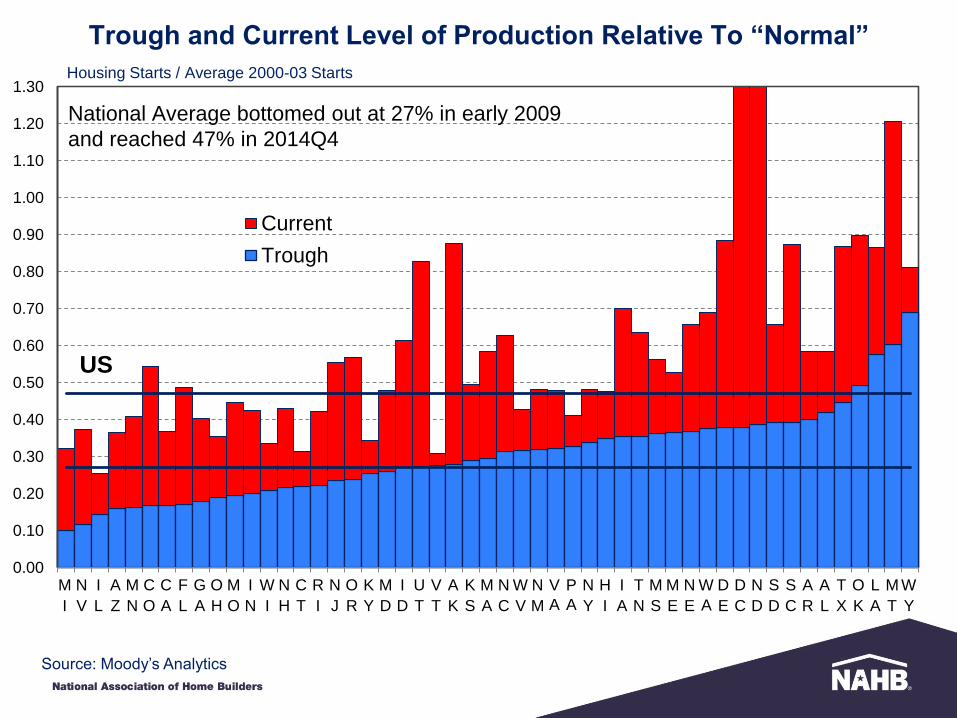

Current

Trough

Housing Starts / Average 2000-03 Starts

National Average bottomed out at 27% in early 2009

and reached 47% in 2014Q4

US

Trough and Current Level of Production Relative To “Normal”

Source: Moody’s Analytics

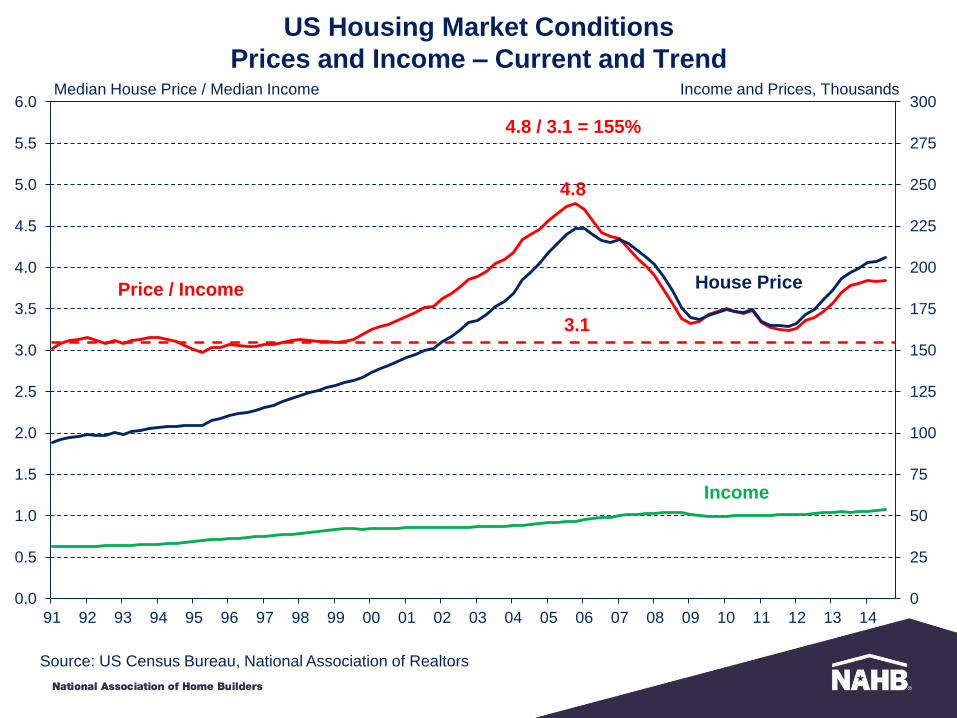

US Housing Market Conditions

Prices and Income – Current and Trend

0

25

50

75

100

125

150

175

200

225

250

275

300

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0Median House Price / Median Income Income and Prices, Thousands

House Price Price / Income

Income

3.1

4.8

4.8 / 3.1 = 155%

Source: US Census Bureau, National Association of Realtors

US Housing Market Conditions

Prices and Income – Current and Trend

0

25

50

75

100

125

150

175

200

225

250

275

300

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0Median House Price / Median Income Income and Prices, Thousands

House Price Price / Income

Income

3.1

4.8

4.8 / 3.1 = 155%

Percentage of 3.1

124%

Source: US Census Bureau, National Association of Realtors

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

150%

160%

170%

180%

190%

200%

210%

220%

U

S

I

N

W

Y

O

H

S

D

M

O

T

N

A

L

C

T

V

T

N

M

A

R

I

A

K

S

K

Y

M

I

O

K

G

A

U

T

T

X

N

E

N

C

M

S

P

A

M

T

L

A

N

D

W

I

N

H

M

E

I

L

H

I

A

K

S

C

D

E

W

V

C

O

M

N

I

D

R

I

M

A

W

A

N

Y

O

R

V

A

N

J

M

D

D

C

A

Z

C

A

N

V

F

L

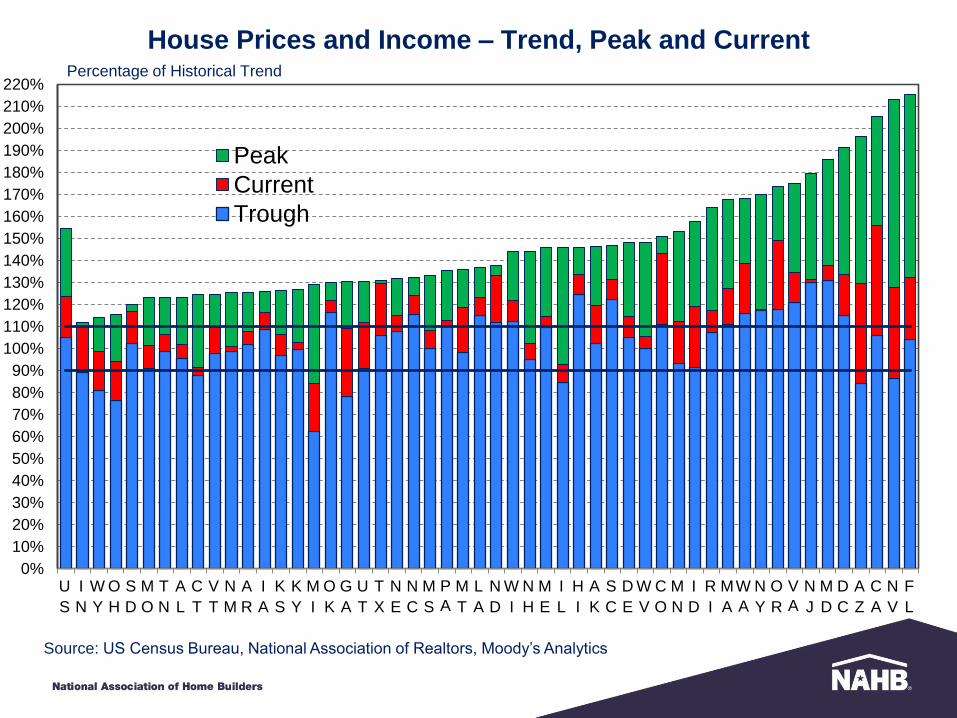

Peak

Current

Trough

Percentage of Historical Trend

House Prices and Income – Trend, Peak and Current

Source: US Census Bureau, National Association of Realtors, Moody’s Analytics

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Percent

Delinquent 90+ Days

Started

Inventory

Foreclosures: Started, Inventory and Delinquent Loans

Source: Mortgage Bankers Association, National Delinquency Survey

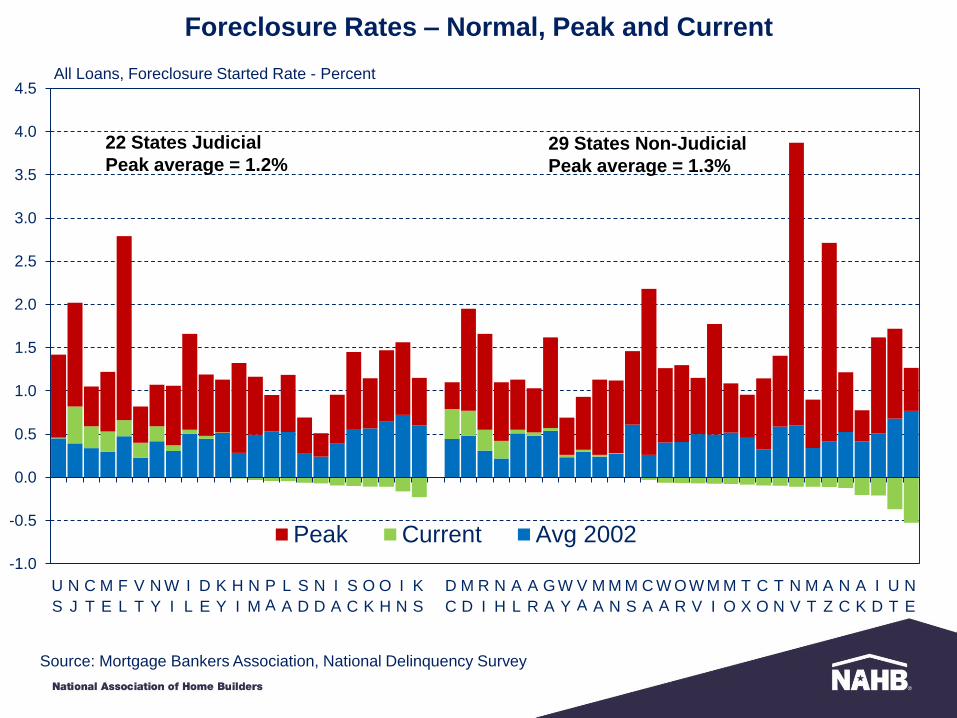

Foreclosure Rates – Normal, Peak and Current

U

S

N

J

C

T

M

E

F

L

V

T

N

Y

W

I

I

L

D

E

K

Y

H

I

N

M

P

A

L

A

S

D

N

D

I

A

S

C

O

K

O

H

I

N

K

S

D

C

M

D

R

I

N

H

A

L

A

R

G

A

W

Y

V

A

M

A

M

N

M

S

C

A

W

A

O

R

W

V

M

I

M

O

T

X

C

O

T

N

N

V

M

T

A

Z

N

C

A

K

I

D

U

T

N

E

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Peak Current Avg 2002

All Loans, Foreclosure Started Rate - Percent

22 States Judicial

Peak average = 1.2% 29 States Non-Judicial

Peak average = 1.3%

Source: Mortgage Bankers Association, National Delinquency Survey

U

S

N

J

F

L

N

Y

M

E

C

T

H

I

V

T

I

L

D

E

N

M

O

K

W

I

P

A

I

A

S

C

L

A

K

Y

S

D

K

S

O

H

N

D

I

N

R

I

N

V

M

D

D

C

O

R

M

A

N

H

W

A

C

A

A

R

A

L

M

N

V

A

C

O

G

A

W

Y

N

C

A

Z

T

X

M

T

W

V

M

O

M

S

I

D

M

I

T

N

A

K

N

E

U

T

-2

0

2

4

6

8

10

12

14

16

Peak Current Avg 2002

All Loans, In Foreclosure - Percent

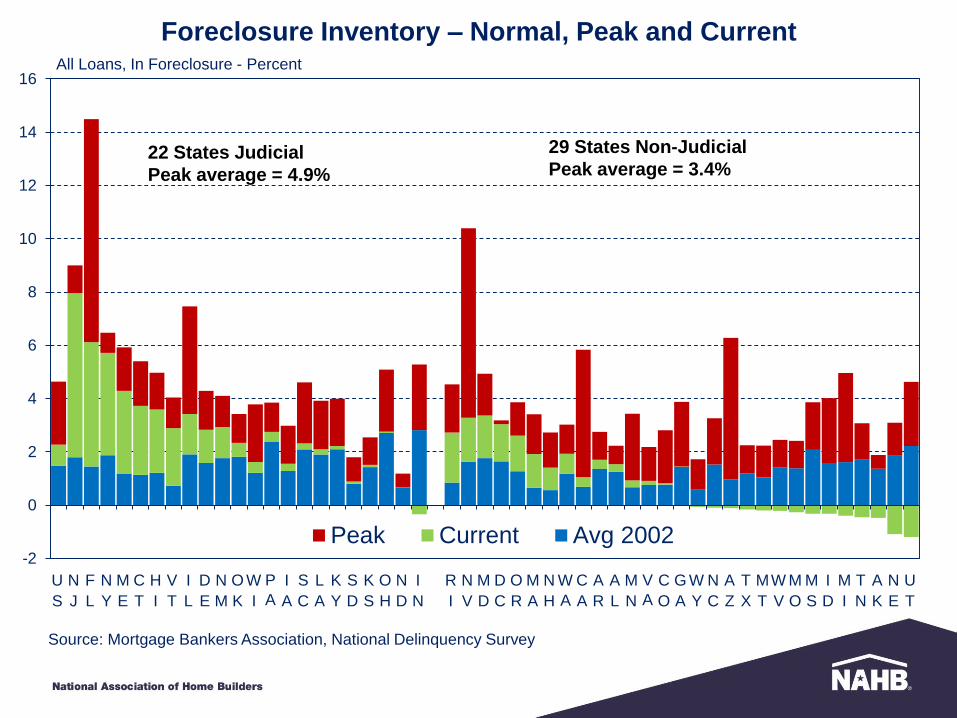

22 States Judicial

Peak average = 4.9%

29 States Non-Judicial

Peak average = 3.4%

Foreclosure Inventory – Normal, Peak and Current

Source: Mortgage Bankers Association, National Delinquency Survey

80%

90%

100%

110%

120%

130%

140%

N

D

T

X

U

T

D

C

C

O

A

K

W

A

N

Y

S

D

M

A

C

A

O

K

N

E

I

D

I

A

M

N

M

T

L

A

S

C

G

A

T

N

K

Y

M

D

N

C

V

T

O

R

K

S

I

N

H

I

V

A

D

E

W

I

A

R

P

A

N

H

F

L

W

V

W

Y

O

H

I

L

M

O

C

T

N

M

A

Z

N

J

M

E

M

S

R

I

A

L

M

I

N

V

Current

Trough

Percent

US

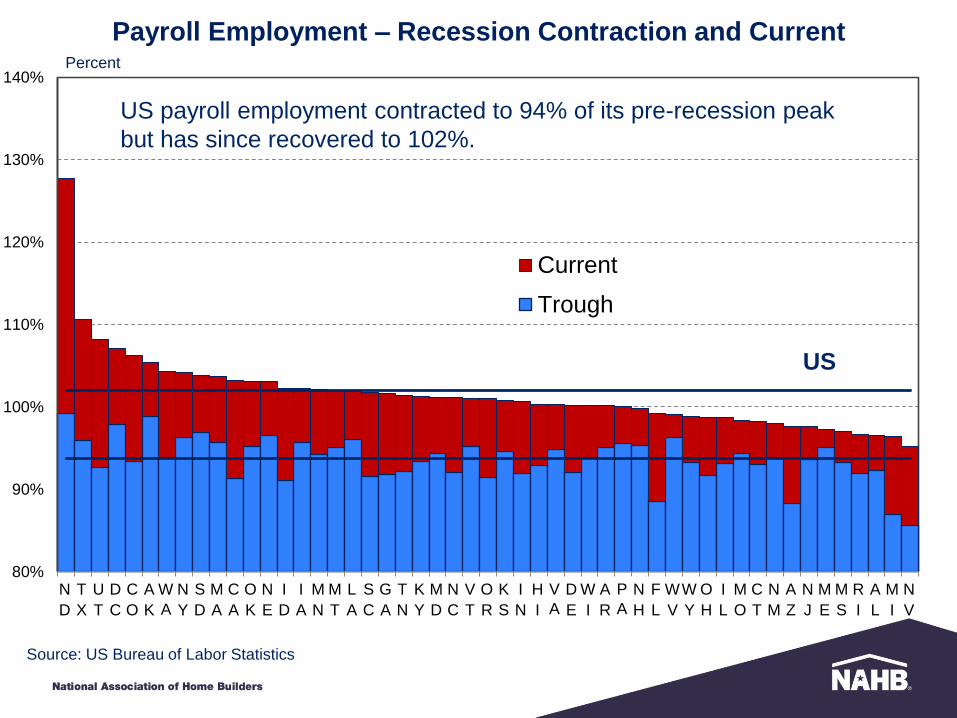

US payroll employment contracted to 94% of its pre-recession peak

but has since recovered to 102%.

Payroll Employment – Recession Contraction and Current

Source: US Bureau of Labor Statistics

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

90% 95% 100% 105% 110% 115%

Percent of “Normal” Housing Starts

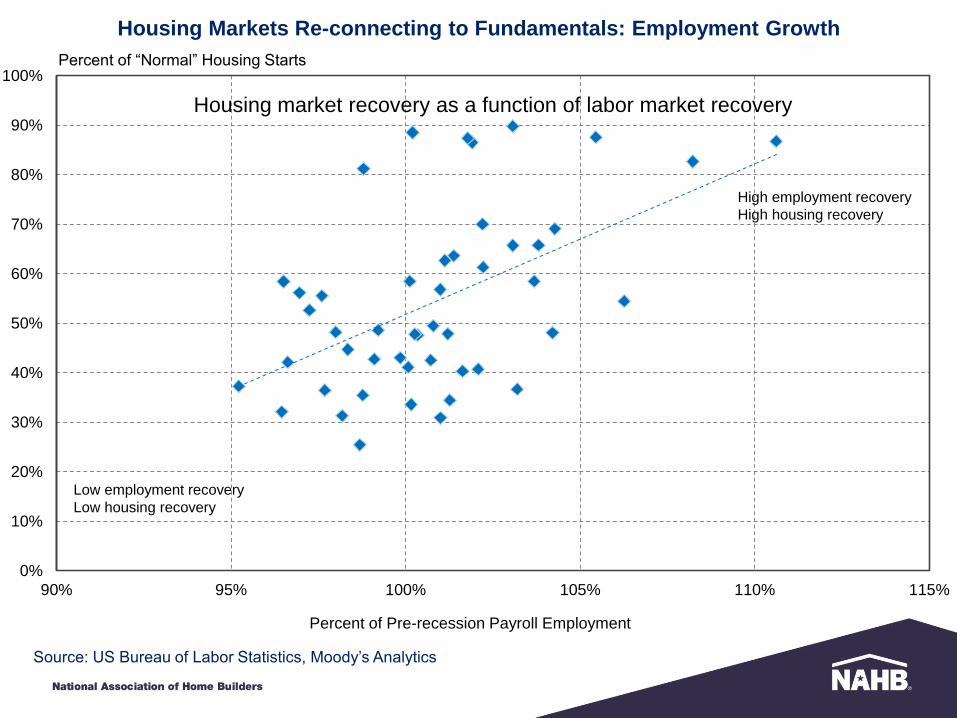

Housing Markets Re-connecting to Fundamentals: Employment Growth

Percent of Pre-recession Payroll Employment

Housing market recovery as a function of labor market recovery

High employment recovery

High housing recovery

Low employment recovery

Low housing recovery

Source: US Bureau of Labor Statistics, Moody’s Analytics

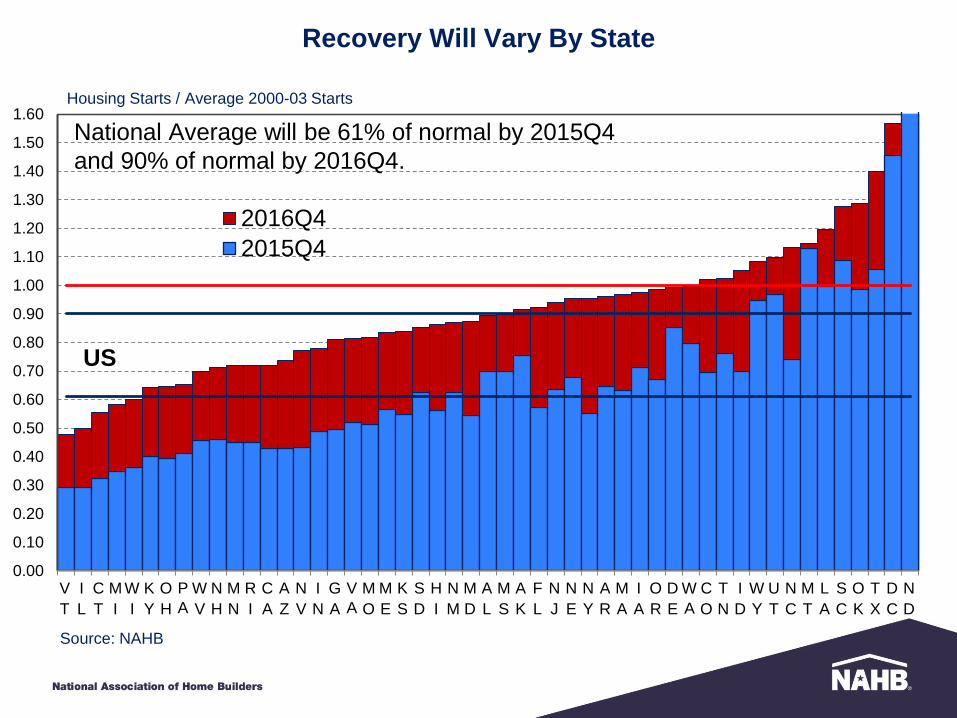

Progress of Housing Market Recovery

B. The Forecast

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Million Units, SAAR

47%

90%

61%

27%

Single Family Housing Starts

Sources: US Census Bureau, NAHB

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

V

T

I

L

C

T

M

I

W

I

K

Y

O

H

P

A

W

V

N

H

M

N

R

I

C

A

A

Z

N

V

I

N

G

A

V

A

M

O

M

E

K

S

S

D

H

I

N

M

M

D

A

L

M

S

A

K

F

L

N

J

N

E

N

Y

A

R

M

A

I

A

O

R

D

E

W

A

C

O

T

N

I

D

W

Y

U

T

N

C

M

T

L

A

S

C

O

K

T

X

D

C

N

D

2016Q4

2015Q4

Housing Starts / Average 2000-03 Starts

National Average will be 61% of normal by 2015Q4

and 90% of normal by 2016Q4.

US

Recovery Will Vary By State

Source: NAHB

Rank Q4 2016

Bottom 20%

20% to 40%

40% to 60%

60% to 80%

Top 20%

The Long Road Back to Normal

< 72%

72% - 84%

85% - 95%

96% - 105%

105% <

Relative

to Normal

This map shows how the states rank in the return to more normal levels of housing production.

By the end of 2016, the top 40% will be back to near normal production levels.

The bottom 20% will be below 72% of normal production.