economic and financial crises a fundamental analysis from islamic financial paradigms perspective

TRANSCRIPT

Economic & Financial Crises – A Fundamental Analysis from Islamic Financial Paradigms Perspective

PA Shameel Sajjad

Maqasid Al Shariah

• Protection of Life (Nafs)

• Protection of Religion (Deen)

• Protection of Intellect (Aql)

• Protection of Progeny (Nasl)

• Protection of Wealth (Maal)

The Definition of Financial Crisis

• A situation in which the value of financialinstitutions or assets drops rapidly. A financial crisisis often associated with a panic or a run on thebanks, in which investors sell off assets or withdrawmoney from savings accounts with the expectationthat the value of those assets will drop if theyremain at a financial institution.

• A situation in which the supply of money is outpacedby the demand for money. This means that liquidityis quickly evaporated because available money iswithdrawn from banks, forcing banks either to sellother investments to make up for the shortfall or tocollapse. See also recession.

Types of Crises

• Banking Crisis

• Currency Crisis

• Speculative Bubbles and Crashes

• International Financial Crises

• Wider Economic Crises

Banking Crisis

• When a bank suffers a sudden rush of withdrawals bydepositors, this is called a bank run.

• Since banks lend out most of the cash they receive, it isdifficult for them to quickly pay back all deposits if theseare suddenly demanded, so a run renders the bankinsolvent, causing customers to lose their deposits, tothe extent that they are not covered by depositinsurance.

• An event in which bank runs are widespread is called asystemic banking crisis or banking panic.

• Examples of bank runs include the run on the Bank ofthe United States in 1931 and the run on Northern Rockin 2007.

Currency Crisis

• There is no widely accepted definition of a currency crisis, whichis normally considered as part of a financial crisis.

• Kaminsky et al. (1998), for instance, define currency crises aswhen a weighted average of monthly percentage depreciationsin the exchange rate and monthly percentage declines inexchange reserves exceeds its mean by more than threestandard deviations.

• Frankel and Rose (1996) define a currency crisis as a nominaldepreciation of a currency of at least 25% but it is also definedat least 10% increase in the rate of depreciation.

• In general, a currency crisis can be defined as a situation whenthe participants in an exchange market come to recognize that apegged exchange rate is about to fail, causing speculation againstthe peg that hastens the failure and forces a devaluation orappreciation.

Speculative Bubbles and Crashes

• A speculative bubble exists in the event of large, sustained overpricing of someclass of assets.

• One factor that frequently contributes to a bubble is the presence of buyerswho purchase an asset based solely on the expectation that they can later resellit at a higher price, rather than calculating the income it will generate in thefuture.

• If there is a bubble, there is also a risk of a crash in asset prices: marketparticipants will go on buying only as long as they expect others to buy, andwhen many decide to sell the price will fall.

• However, it is difficult to predict whether an asset's price actually equals itsfundamental value, so it is hard to detect bubbles reliably.

• Some economists insist that bubbles never or almost never occur.• Well-known examples of bubbles (or purported bubbles) and crashes in stock

prices and other asset prices include the Dutch tulip mania, the Wall StreetCrash of 1929, the Japanese property bubble of the 1980s, the crash of the dot-com bubble in 2000–2001, and the now-deflating United States housingbubble. The 2000s sparked a real estate bubble where housing prices wereincreasing significantly as an asset good.

International Financial Crises

• When a country that maintains a fixed exchange rate is suddenly forced todevalue its currency due to accruing an unsustainable current account deficit,this is called a currency crisis or balance of payments crisis.

• When a country fails to pay back its sovereign debt, this is called a sovereigndefault.

• While devaluation and default could both be voluntary decisions of thegovernment, they are often perceived to be the involuntary results of a changein investor sentiment that leads to a sudden stop in capital inflows or a suddenincrease in capital flight.

• Several currencies that formed part of the European Exchange Rate Mechanismsuffered crises in 1992–93 and were forced to devalue or withdraw from themechanism.

• Another round of currency crises took place in Asia in 1997–98.• Many Latin American countries defaulted on their debt in the early 1980s.• The 1998 Russian financial crisis resulted in a devaluation of the ruble and

default on Russian government bonds.

Wider Economic Crises

• Negative GDP growth lasting two or more quarters is called a recession. An especiallyprolonged or severe recession may be called a depression, while a long period of slowbut not necessarily negative growth is sometimes called economic stagnation.

• Some economists argue that many recessions have been caused in large part by financialcrises.

• One important example is the Great Depression, which was preceded in many countriesby bank runs and stock market crashes.

• The subprime mortgage crisis and the bursting of other real estate bubbles around theworld also led to recession in the U.S. and a number of other countries in late 2008 and2009.

• Some economists argue that financial crises are caused by recessions instead of the otherway around, and that even where a financial crisis is the initial shock that sets off arecession, other factors may be more important in prolonging the recession.

• In particular, Milton Friedman and Anna Schwartz argued that the initial economicdecline associated with the crash of 1929 and the bank panics of the 1930s would nothave turned into a prolonged depression if it had not been reinforced by monetary policymistakes on the part of the Federal Reserve, a position supported by Ben Bernanke.

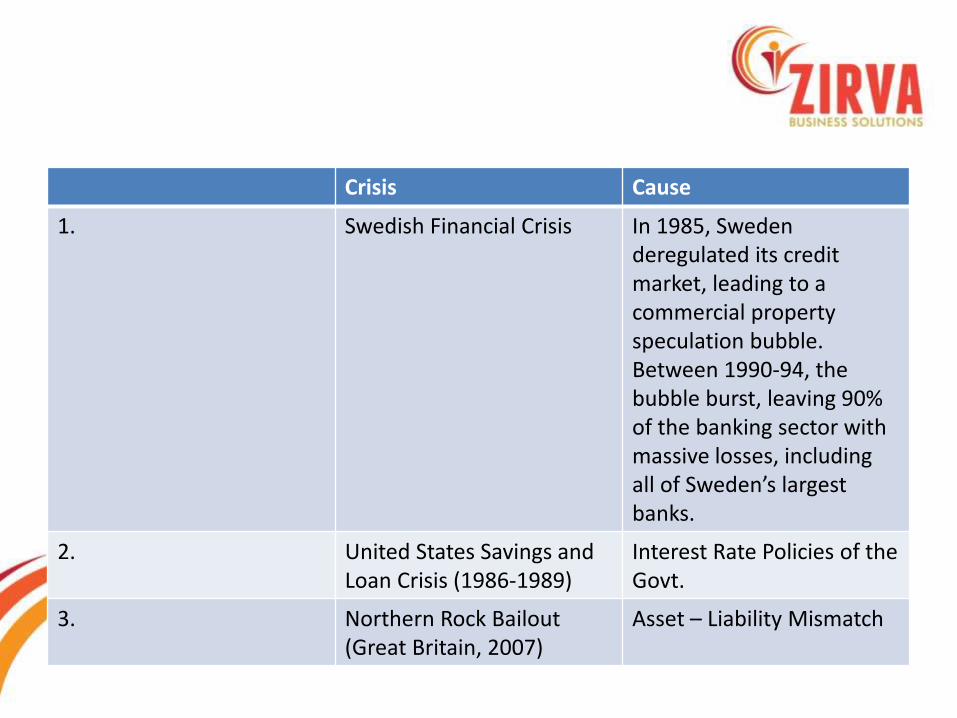

Crisis Cause

1. Swedish Financial Crisis In 1985, Sweden deregulated its credit market, leading to a commercial property speculation bubble. Between 1990-94, the bubble burst, leaving 90% of the banking sector with massive losses, including all of Sweden’s largest banks.

2. United States Savings and Loan Crisis (1986-1989)

Interest Rate Policies of the Govt.

3. Northern Rock Bailout (Great Britain, 2007)

Asset – Liability Mismatch

4. Tulip Mania (The Netherlands, 1637)

Futures trading in tulips. Short selling of futures contracts.

5. The Japanese asset price bubble (1986-1990)

Asset Liability Mismatch

Causes of Crises

Leverage

• Leverage refers to use of debt in capital.• Debt comes at a lower cost than equity and

thus reduces the weighted average cost ofcapital.

• Thus the use of debt in capital structuremagnifies profits for shareholders.

• The use of debt magnifies losses at a higherrate than it magnifies losses.

• This phenomenon is called the “LeverageEffect” which was first demonstrated by Black.

• When debt takes the form of security itassumes increased capacity to causedestruction in the financial system.

• Securitization of debt and trading in thosesecurities has been the basic cause of most ofthe crises including the 2008 sub prime crisis.

• The door to such massive destruction has beenclosed by Islam through the rule of bai al dayn.

Speculative Trades and Positions

• Speculative transactions are carried out mainly throughfinancial instruments known as derivatives.

• A derivative is a contract between two or more parties whosevalue is based on an agreed-upon underlying financial asset,index or security.

• In practice, while purchasing a derivative only a small portion ofthe price of the bundle of stocks as per the derivative contract ispaid by the buyer.

• That is, in effect, the major part of the price and the delivery ofthe whole of the subject matter of sale (equities in this case) isdeferred to a future date.

• This amounts to the sale of debt (price) for debt (shares) withunequal values as the price of shares keeps continuouslychanging in the market.

• The history of equity derivatives dates back to April26th, 1973 when Chicago Board Options Exchangelisted equity options for trading.

• 911 contracts traded in 16 different equities.

• Shortly after that Fischer Black and Myron Scholespublished their landmark article “The Pricing ofOptions and Corporate Liabilities” in the Journal ofPolitical Economy, Volume 81 (May / June 1973).

• Another landmark article in 1972 was “Theory ofRational Option Pricing” by Robert Merton in theBell Journal of Economics and Management Science.

• Since then Derivatives demonstrated a morbid capacity to effectand accelerate widespread financial crashes and take those tounimagined levels.

• Still, they are not undone with in spite of widespread criticism.• Mr. Warren Buffet; the world famous investor in equities and the

Chief of Berkshire Hathaway termed Derivatives as “weapons offinancial destruction” (Berkshire Hathaway Inc., 2002).

• Derivatives have been associated with a number of high profilecorporate events that roiled the global financial markets.

• Derivatives have played an important role in the near collapsesor bankruptcies of Barings Bank in 1995, Long Term CapitalManagement in 1998, Enron in 2001, Lehman Brothers andAmerican International Group (AIG) in 2008.

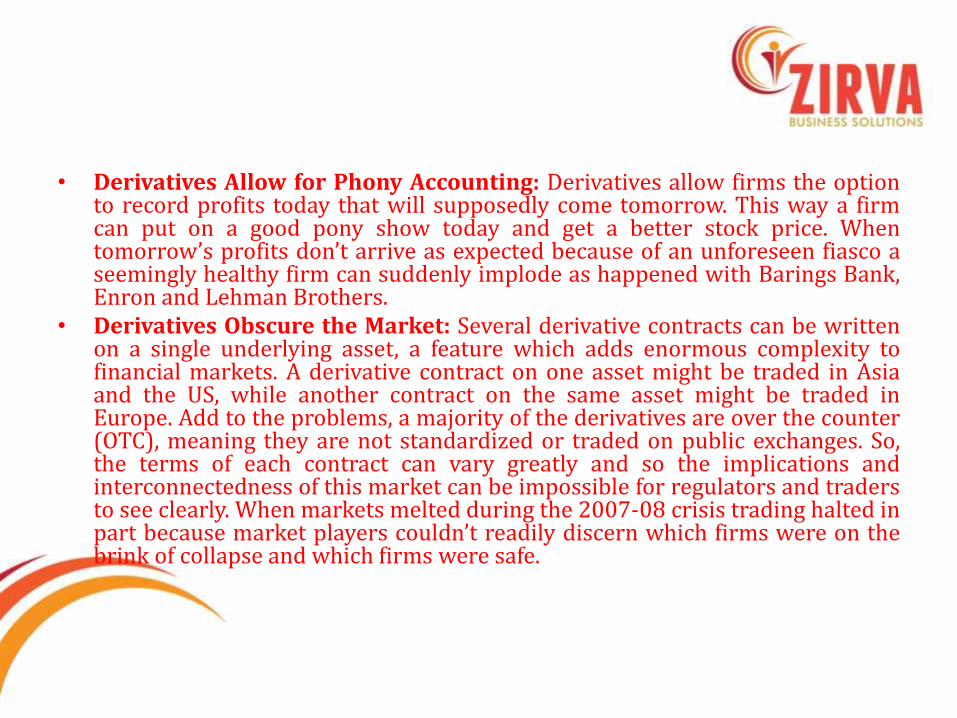

• Derivatives Allow for Phony Accounting: Derivatives allow firms the optionto record profits today that will supposedly come tomorrow. This way a firmcan put on a good pony show today and get a better stock price. Whentomorrow’s profits don’t arrive as expected because of an unforeseen fiasco aseemingly healthy firm can suddenly implode as happened with Barings Bank,Enron and Lehman Brothers.

• Derivatives Obscure the Market: Several derivative contracts can be writtenon a single underlying asset, a feature which adds enormous complexity tofinancial markets. A derivative contract on one asset might be traded in Asiaand the US, while another contract on the same asset might be traded inEurope. Add to the problems, a majority of the derivatives are over the counter(OTC), meaning they are not standardized or traded on public exchanges. So,the terms of each contract can vary greatly and so the implications andinterconnectedness of this market can be impossible for regulators and tradersto see clearly. When markets melted during the 2007-08 crisis trading halted inpart because market players couldn’t readily discern which firms were on thebrink of collapse and which firms were safe.

• Derivatives Concentrate Risk: Four US megabanks – JPMorgan, Bank of America, Citi and Goldman Sachs – have anotional amount of $214 trillion in derivatives exposure.That’s more than 30% of the worldwide amount just in fourUS banks. When firms have such concentrated derivativesexposure, they leave themselves to surprise losses like lastyear’s $6 billion London Whale loss at JPMorgan Chase.

• Derivatives Create Notional Value which will never beRealized: The world derivatives market is worth some $700trillion. Some opine that it actually runs into quadrillions.Such unfathomable valuations never get realized in the realmarket. These valuations exist only in notions and papersand suddenly get eroded during crises.

Trading Cash for Cash (Dangerous Systemic Liquidity)

• Like leverage screening, liquidity screening is also an integral part ofthe Shariah screening of stocks. The application of this screening normrests in the command of the prohibition of Riba al fadl which is alsoknown as riba al hadith as the prohibition is found in the ahadith of theProphet (SAW).

• Abu Sa'id al-Khudri (r) reported Allah's Messenger (p) as saying: “Goldis to be paid for by gold, silver by silver, wheat by wheat, barley bybarley, dates by dates, salt by salt, like by like, payment being madehand to hand. He who made an addition to it, or asked for an addition,in fact dealt in riba. The receiver and the giver are equally guilty” (13).

• The consequence of this hukm (rule) is that cash or assets which aresynonymous to cash like trade debts receivable and money marketsecurities can be transacted only at par value and on spot. Equitiesrepresent assets of a company and assets include fixed assets andcurrent assets. Cash and cash equivalent assets represent currentassets.

Short Selling

• Short sellers bet against the stock. Instead of rooting for stockprices to go up, they seek an opportunity to make money byexpecting a decline. Short sellers borrow the stock from abroker, sell it, and wait for the prices to drop so they canpurchase the stock at a cheaper price.

• In 1610, the Dutch market crashed, and Isaac Le Maire, aprominent merchant, was blamed because he was actively shortselling stocks. He was a major shareholder in the Dutch EastIndia Company (also known as Vereenigde Oost-IndischeCompagnie or VOC). Le Maire, a former member of thecompany's board, and his associates were accused ofmanipulating VOC's stocks. They attempted to drive share pricesdown by selling large of quantities of shares on the market. TheDutch government took action and instituted a temporary banon short selling.

Ibadaat & Muamalaat

• Ibadaat

– The “principle” is everything except what isprescribed is “PROHIBITED”.

• Muamalaat

– The “principle” is everything except what isprohibited is “PERMITTED”.

The Fundamental Prohibitions in Muamalaat Riba (interest / usury)

Gharar (excessive uncertainty, deceit, misrepresentation,fraud)

Maysir (gambling, unearned income)

Rationale of Prohibition of Riba(Interest / Usury)

• The logic of the prohibition on theoretical ground.

• The evil effects of interest on production.

• The evil effects of interest on distribution.

Theoretical Explanation

• On pure theoretical ground, we would like to focus on two basic issues; firstly on the nature of money and secondly on the nature of a loan transaction.

Nature of Money

• One of the wrong presumptions on which all theories of interest are basedis that money has been treated as a commodity.

• It is, therefore, argued that just as a merchant can sell his commodity for ahigher price than his cost, he can also sell his money for a higher pricethan its face value, or just as he can lease his property and can charge arent against it, he can also lend his money and can claim interestthereupon.

• Islamic principles, however, do not subscribe to this presumption. Moneyand commodity have different characteristics and therefore they aretreated differently.

Points of Difference between Money & Commodity• Money has no intrinsic utility. A commodity, on the other

hand, has intrinsic utility.

• Commodities can be of different qualities while money has noquality except that it is a measure of value or a medium ofexchange.

• In commodities, the transactions of sale and purchase areeffected on an identified particular commodity. Money, on thecontrary, cannot be pin-pointed in a transaction of exchange.

• Based on these basic differences, Islamic Shar'iah has treatedmoney differently from commodities, especially on twoscores:

• Firstly, money (of the same denomination) is not held to bethe subject-matter of trade, like other commodities.

• Secondly, if for exceptional reasons, money has to beexchanged for money or it is borrowed the transactions mustbe at par.

• The commodities are classified into the commodities of firstorder which are normally termed as "consumption goods"and the commodities of the higher order which are called"productive goods."

• Since money, having no intrinsic utility, could not be includedin "consumption goods."

• Most of the economists had no option but to put it under thecategory of "production goods", but it was hardly proved bysound logical arguments that money is a "production good”.

The Nature of Loan

• Another major difference between the secular capitalist system and theIslamic principles is that under the former system, loans are purelycommercial transactions meant to yield a fixed income to the lenders.

• Islam, on the other hand, does not recognize loans as income-generatingtransactions.

• The basic philosophy underlying this scheme is that the one who isoffering his money to another person has to decide whether:

(a) He is lending money to him as a sympathetic act or.

(b) He is lending money to the borrower, so that his principal may be saved or

(c) He is advancing his money to share the profits of the borrower.

• In the former two cases (a) and (b) he is not entitled to claim anyadditional amount over and above the principal.

• However, if his intention is to share the profits of the borrower,as in case (c), he shall have to share his loss also, if he suffers aloss. In this case, his objective cannot be served by a transactionof loan.

• Once the interest is banned, the role of "loans" in commercialactivities becomes very limited, and the whole financingstructure turns out to be equity-based and backed by real assets.

• In order to limit the use of loans, the Shar'iah has permitted toborrow money only in cases of dire need, and has discouragedthe practice of incurring debts for living beyond one's means.

• Conversely, once the interest is allowed; advancing loans, in itself,becomes a form of profitable trade.

• The whole economy turns out to be debt-oriented which not onlydominates over the real economic activities and disturbs its naturalfunctions by creating frequent shocks, but also puts the wholemankind under the slavery of debt.

• It is no secret that all the nations of the world, including thedeveloped countries, are drowned in national and foreign debts tothe extent that the amount of payable debts in a large number ofcountries exceeds their total income.

• Just to take one example of UK, the household debt in 1963 wasless than 30% of total annual income. In 1997, however, thepercentage of household debt rose up to more than 100% of thetotal income.

Overall Effects of Interest

Evil Effects on Allocation of Resources• Loans in the present banking system are advanced mainly to

those who, on the strength of their wealth, can offersatisfactory collateral.

• The veracity of this statement can be confirmed by the factthat according to the statistics issued by the State Bank ofPakistan in September 1999, 9269 account holders out of2,184,417 (only 0.4243% of total account holders) haveutilized Rs.438.67 billion which is 64.5% of total advances byDecember 1998.

• Since in an interest-based system funds are provided on the basis of strongcollateral and the end-use of the funds does not constitute the main criterionfor financing, it encourages people to live beyond their means.

• The rich people do not borrow for productive projects only, but also forconspicuous consumption.

• Governments borrow money not only for genuine development programs, butalso for their lavish expenditure and for projects motivated by their politicalambitions rather than being based on sound economic assessment.

• Non-project-related borrowings, which were possible only in an interest-basedsystem have thus helped in nothing but increasing the size of our debts to ahorrible extent.

• According to the budget of 1998/99 in our country 46 percent of the totalgovernment spending is devoted to debt-servicing, while only 18% is allocatedfor development which includes education, health and infrastructure.

Evil Effects on Distribution

• In the context of modern capitalist system, it is the bankswhich advance depositors' money to the industrialists andtraders.

• Almost all the giant business ventures are mostly financed bythe banks and financial institutions.

• If the entrepreneurs having only ten million of their own,acquire 90 million from the banks and embark on a hugeprofitable enterprise, it means that 90% of the projects iscreated by the money of the depositors while only 10% wasgenerated by their own capital.

• If these huge projects bring enormous profits, only a small proportion (ofinterest which normally ranges between 2% to 10% in different countries)will go to the depositors whose input in the projects was 90% while all therest will be secured by the big entrepreneurs whose real contribution tothe projects was not more than 10%. Even this small proportion given tothe depositors is taken back by these big entrepreneurs, because all theinterest paid by them is included in the cost of their production and comesback to them through the increased prices. The net result in this case isthat all the profits of the big enterprises is earned by the persons whoseown financial input does not exceed 10% of the total investment, whilethe people whose financial contribution was as high as 90% get nothing inreal terms, because the amount of interest given to them is often repaidby them through the increased prices of the products, and therefore, in anumber of cases the return received by them becomes negative in realterms.

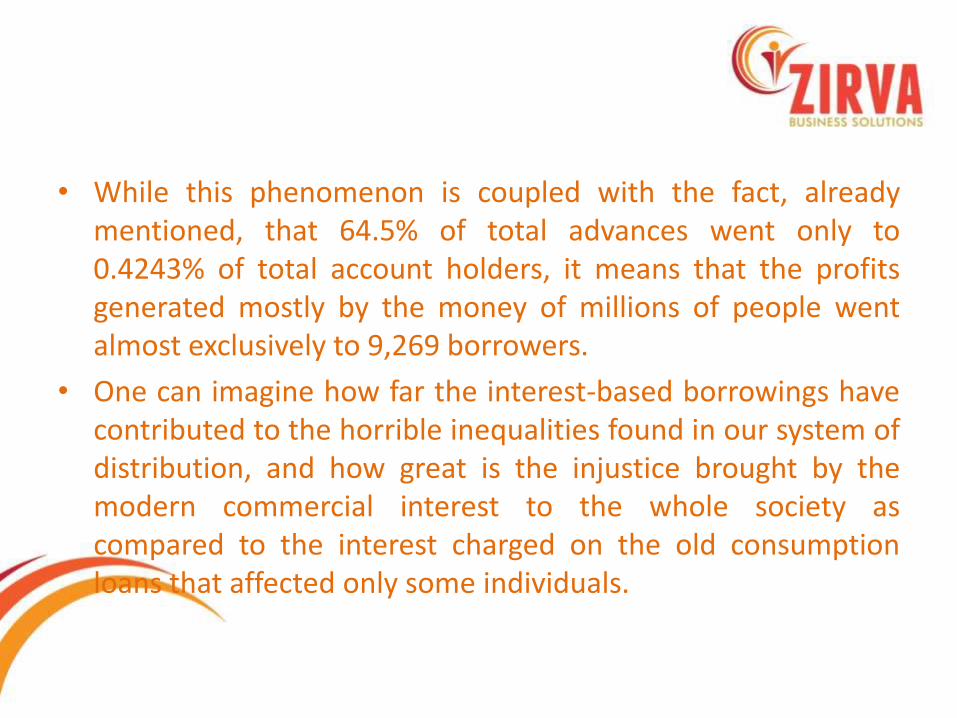

• While this phenomenon is coupled with the fact, alreadymentioned, that 64.5% of total advances went only to0.4243% of total account holders, it means that the profitsgenerated mostly by the money of millions of people wentalmost exclusively to 9,269 borrowers.

• One can imagine how far the interest-based borrowings havecontributed to the horrible inequalities found in our system ofdistribution, and how great is the injustice brought by themodern commercial interest to the whole society ascompared to the interest charged on the old consumptionloans that affected only some individuals.

Expansion of Artificial Money and Inflation

• Since interest-bearing loans have no specific relation withactual production, and the financier, after securing a strongcollateral, normally has no concern how the funds are used bythe borrower, the money supply effected through banks andfinancial institutions has no nexus with the goods and servicesactually produced on the ground.

• It creates a serious mismatch between the supply of moneyand the production of goods and services.

• This is obviously one of the basic factors that create or fuelinflation.

• This phenomenon is aggravated to a horrible extent by thewell-know characteristic of the modern banks normallytermed as "money creation.

• " Even the introductory books of economics usually explain,often with complacence, how the banks create money.

• This apparently miraculous function of the banks issometimes taken to be one of the factors that boostproduction and bring prosperity. But the illusion underlyingthis concept, is seldom unveiled by the champions of modernbanking.

Year Total Coins & Notes Issued by the Govt. (Pound Sterling bn)

Total Money Stock (Pound Sterling bn)

% of Real Debt Free Money to the Money Supply)

1977 8.1 65 12%

1979 10.5 87 12%

1981 12.1 116 10.5%

1983 12.8 7.9%

1985 14.1 205 6.8%

1987 15.5 269 5.8%

1989 17.2 372 4.6%

1991 18.6 485 3.8%

1993 20.0 525 3.8%

1995 22.4 585 3.8%

1997 25.0 680 3.6%

• This table shows that the money created by the banks had beengrowing at a galloping speed throughout the two decades until itreached 680 billion pounds in 1997.

• The last column of the table shows the yearly declining percentageof the real money to the total money supply which fell from 12% in1977 to 3.6% in 1997.

• This phenomenon unveils two realities.

• Firstly, it shows that 96.4% of the total money supply is debt-riddenmoney and only 3.6% is debt-free.

• One can imagine how the whole economy is drowned under debt.

• Secondly, it means that 96.4% of the aggregate money circulated inthe country is nothing but numbers created by computers, havingno real thing behind them.

Profit & Loss Sharing

• The basic and foremost characteristic of Islamicfinancing is that, instead of a fixed rate of interest, itis based on profit and loss sharing.

• Realizing the evils brought by this system, manyeconomists, even of the Western world are nowadvocating in favour of an equity-based financialarrangement.

• In equity-based banking the depositors are expectedto gain much more than they are receiving today inthe form of interest which often becomes negative inreal terms by the inflation caused mainly by theexpansion of the debt-based money.

• It will divert the flow of wealth towards the commonpeople and in turn will encourage savings and bring agradual and balanced prosperity.

Islamic Finance in the World

Currently Islamic finance practices have spread to about 75countries of the world.

Shariah-compliant assets reached about $400 billionthroughout the world in 2009, according to Standard &Poor’s Ratings Services, and the potential market is $4trillion. Iran, Saudi Arabia and Malaysia have the biggestSharia-compliant assets

By 2020, a major part of the economy in the Middle Eastwill become Shariah-compliant.

In 2009 Iranian banks accounted for about 40 percent oftotal assets of the world's top 100 Islamic banks.

Bank Melli Iran, with assets of $45.5 billion came first,followed by Saudi Arabia's Al Rajhi Bank, Bank Mellat with$39.7 billion and Bank Saderat Iran with $39.3 billion.

Iran holds the world's largest level of Islamic financeassets valued at $235.3bn which is more than double thenext country in the ranking with $92bn.

Six out of ten top Islamic banks in the world are Iranian.

In November 2010, The Banker published its latestauthoritative list of the Top 500 Islamic FinanceInstitutions with Iran topping the list. Seven out of ten topIslamic banks in the world are Iranian according to the list.

Conventional banks in the region have either startedIslamic Finance subsidiaries or converted their entireoperations into the shariah-compliant mode.

Even foreign financial institutions in the region are noexceptions to this trend.

Similarly, in many western countries such as UK, USA,Switzerland, France and Germany etc. many IslamicFinance institutions have come up to tap the nicheopportunities.

Islamic Finance in Secular Economies

Islamic Finance Institutions in the West

UK25

US20

Switzerland5

France4

Luxembourg4

Ireland3

Germany3

Cayman Islands2

Canada1

Italy1

The Size of Islamic Finance Sector

Islamic Finance Institutions

Size(USD billion)

Number

Islamic Banks 750 292

Islamic Bonds 173 732

Islamic Financing for Projects and Infrastructure

464 194

Islamic Real Estate Funds 56 102

Phases of Islamic Finance in India

Academic (1930-1970)

• Writings started during independence struggle

• Books, researches, models, first generation Islamic economists.

Non-Profit Model (1930-1980)

• Efforts during Nizam’s rule in South India

• Jamiet-e- Ulemae Hind’s poverty alleviation program

• Jamat-e- Islami’s cooperative model

• Entry of professionals

Profit Model (1980-2000)

• Jamat-e-Islami encouraged group

• Professionals entry

• Unscrupulous elements entry

• Crisis of late 1990s

Phase 1

Phase 2

Phase 3

Non-Profit Oriented Institutions

Year Institution Type Place

1923 Anjuman Imdad-e-BahmiQardh Bila Sud

Baitul Maal Hyderabad

1934 Patni Co-operative Credit Society

Cooperative Society Gujarat

1939 Muslim Fund, Tanda Baoli Baitul Maal Rampur, UP

Partition Effect

1966 Toor Baitul Maal Baitul Maal Hyderabad

1969 Muslim Fund Deoband Baitul Maal Saharan Pur

1973 Baitun Nasr Cooperative Society Mumbai

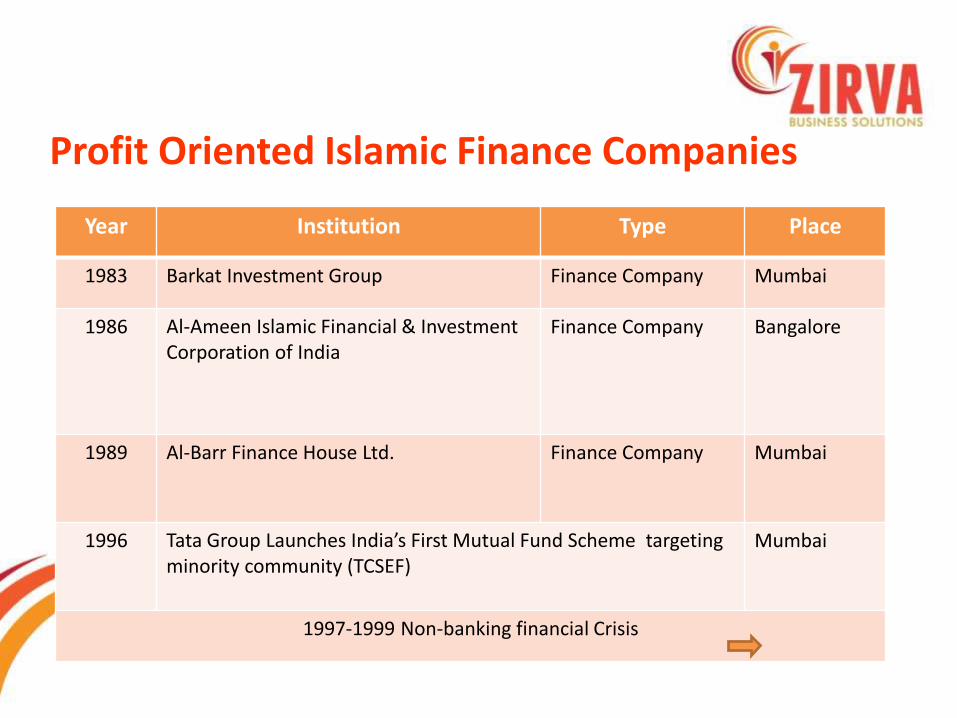

Profit Oriented Islamic Finance Companies

Year Institution Type Place

1983 Barkat Investment Group Finance Company Mumbai

1986 Al-Ameen Islamic Financial & Investment Corporation of India

Finance Company Bangalore

1989 Al-Barr Finance House Ltd. Finance Company Mumbai

1996 Tata Group Launches India’s First Mutual Fund Scheme targeting minority community (TCSEF)

Mumbai

1997-1999 Non-banking financial Crisis

Current Phase of Islamic Finance in India

• 2000-2009

– Since NBFC crisis only one Islamic NBFC could be establish i.e. Alternative Investments and Credits Ltd (AICL, 2000)

– Riding high on stock market rebounding shariah screening started in India (2005)

– “India provides maximum number of shariah compliant options”, Research presented at Harvard forum on Islamic finance 2006.

– Overseas offices of India based institutions started marketing India’s shariah compliant options.

– Market started turning for positive, India started attracting funds from overseas

– Establishment of Shariah Advisory Firm TASIS, 2007

India’s Official Response to Islamic FinanceAction Year

Establishment of Anand Sinha Committee (RBI) for studying Islamic Financial Products 2005

Raghuramrajan Committee recommends Islamic banking for financial inclusion of

Muslims in India

2008

Ministry of Minority Affairs asking bid for reconstruction of National Minority

Development Finance Corporation (NMDFC) on Shariah Lines

2008

SEBI permitting India’s first shariah compliant Mutual Fund 2009

SEBI permitting India’s first shariah compliant Venture Capital Fund 2009

GIC (Re), a government of India owned company, appoints TASIS for shariah advisory 2009

State Government of Kerala appoints E&Y as consult to recommend appropriate

structure for starting an Islamic finance business in the state

2009

Indian Financial System

Banking Sector

Non-banking

RBICapital Market

Collective Investments

Venture Capital

SEBILife Insurance

General Insurance

IRDA

Islamic Finance in India: Options

• Legal Issues

• Practical issuesBanks

• Legal Issues

• Practical issues

• Viability ProblemNBFC

• Most Flexible

• Most Liquid

• More Options

• Government Permission

Capital Market

• Legal Issues

• Practical Issues

• Ray of HopeInsurance

The Great Crisis Among Finance Companies

Finance Companies in India

15358

24009

55995

7855

13873

0

10000

20000

30000

40000

50000

60000

1985 1990 1995 1999 2007

Year

Nu

mb

ers

June 30, 2009: NBFCs No Deposit 834 & 336 (allowed to accept deposit)

Shariah Compliant Stocks in India

116132 138

123 125

297

329 331312

265

0

50

100

150

200

250

300

350

2004 2005 2006 2007 2008

Nu

mb

er

of C

om

pa

nie

s

Year

BSE 500 Shariah Compliant NSE Shariah Compliant

Islamic Finance Deals in Recent Years

Date Projects PartnerUSD

MillionLead Arranger

December 2007Economic Development

Zone (EDZ)Maharashtra State 10,000 Gulf Finance House

November 2007 SREI ProjectsSREI Infrastructure

Finance Ltd.50

HSBC Amananh / KFH

August 2007Bearys Global Research

Triangle Bearys Groups 20 SEDCO

July 2007 Velcan Hydro Electric Dam Velcan Energy Holdings 275National Bank of

Dubai

October 2006 Energy City of India Maharashtra State 2,000 Gulf Finance House

TASIS’ Recent works

Company Product Name Remark

Taurus Asset Management Company

Taurus Ethical Fund India’s First actively Managed Shariah Fund

Bajaj Allianz Insurance Co. Ltd

Pure Stock Pension Fund

India’s First shariah compliant scheme in insurance sector

Secura Investment Management Company

Secura India Real Estate Fund

India’s first Shariah Compliant Venture Capital Fund in real estate sector

GIC Re (Government of India owned)

ReTakaful Scheme This is also going to be India’s first scheme of its kind

Raghuramrajan Committee Report

Chapter 3: Broadening Access to finance Page 35

• “While interest-free banking is provided in a limited manner through

NBFCs and cooperatives, the Committee recommends that measures be

taken to permit the delivery of interest-free finance on a larger scale,

including through the banking system. This is in consonance with the

objectives of inclusion and growth through innovation. The Committee

believes that it would be possible, through appropriate measures, to

create a framework for such products without any adverse systemic risk

impact.”