econ 101 introduction to economics1 · pdf fileand average total cost) –represent the...

TRANSCRIPT

College of Education

School of Continuing and Distance Education 2014/2015 – 2016/2017

ECON 101

Introduction to Economics1

Session 10 – Cost Concept

Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: [email protected]

Session Overview

• There is a difference between economist’s measure of profit and accountant’s measure of profit. Profit is the difference between total revenue and total cost. For economists, total cost includes the opportunity cost of owner’s capital. This session seeks to explain the concept of cost in economics.

Dr. RicMrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 2

Session Objectives

• At the end of the session, the student should be able to:

– Differentiate between implicit cost and explicit cost.

– Determine economic cost.

– Understand accounting profit and economic profit.

– Understand costs in the short run with mathematical calculations.

– Calculate Total, Fixed and Variable costs as well as Per unit Fixed and Variable costs (Average Variable Cost, Average Fixed cost and Average Total Cost)

– Represent the various measures of costs with curves.

– Demonstrate the relationship between the cost curves.

– Understand costs in the long run.

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 3

Session Outline

The key topics to be covered in the session are as follows:

• Cost Concept

• Economic Costs

• Costs in the Short run

• Short and Long run cost curves

• Economies and Diseconomies of Scale

Slide 4 Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Reading List

• Lipsey R. G. and K. A. Chrystal. (2007). Economics. 11th Edition. Oxford University Press.

• Bade R. and M. Parkin. (2009). Foundations of Microeconomics. 4th Edition. Boston: Pearson Education Inc.,

• Begg. D. Fischer S. and R. Dornbusch. (2003). Economics. 7th Edition. McGraw-Hill

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 5

• Accounting cost refers to the monetary outlay on inputs. Thus, the explicit cost of inputs.

• Economic cost refers to the opportunity cost of use of resources. This involves both the explicit and implicit costs of resources

The Cost Concept

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 6

The Cost Concept

Economic cost

Explicit Costs

Plant and equipment

Raw materials Wages and salaries (cost of resources acquired from outside the firm and paid for)

Implicit Costs

forgone wages forgone rent (forgone benefits as a result of use

of owner resources)

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 7

• Explicit costs arise from transactions in which the firm purchases inputs or the services of other parties. E.g. wages and salaries of workers, cost of raw materials, insurance, electricity

• Implicit costs are those associated with the use of the firm’s own resources and reflect the fact that these resources could have been employed elsewhere. These costs are sometimes difficult to measure.

Examples: • A firm in the owner’s own building, where he does not pay rent.

This cost is implicit • Being a manager of his own production firm, he does not pay

himself a salary.

Economic Costs

Slide 8 Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

• Economists thus count the opportunity cost of the owner’s capital as part of a firm’s costs.

• It includes an estimate of what the capital, and any other advantages owned by the firm, could have earned in their best alternative uses.

• Thus economic cost is the opportunity cost of resources used • explicit costs

– paid in money – wages, rent, material, etc.

• implicit costs – opportunity cost of resources used

Economic Costs

Slide 9 Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Accounting Profit and Economic profit

• Accounting profit = total revenue(TR) – explicit costs

– TR = (price)(quantity)

• It ignores opportunity cost

• Economic profit includes opportunity costs.

Economic profit = total revenue - total costs

= (price)(quantity) - (explicit + implicit costs)

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 10

Economic View vs.. Accounting View

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 11

Normal Profit

• Amount of accounting profit = opportunity costs of resources

• It is the same as zero economic profit

• That is, TR – opportunity costs = 0

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana Slide 12

Costs in the Short Run

• Costs are measured in 3 ways:

– total cost

– marginal cost

– average cost

Total cost of production varies with the rate of output.

In the short run, there are two types of costs;

– Fixed costs

– Variable costs

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana Slide 13

workers TP TFC TVC TC

0 0 10 0 10

1 1 10 6 16

1.6 2 10 9.6 19.6

2 3 10 12 22

4 5

8 9

10 10

24 30

34 40

Assume the costs of producing chairs as: Labour = ¢6/ hour TFC = ¢10/ hour (the cost of the workshop)

Costs in the Short Run

Slide 14 Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Q = output

TC

TFC 10

TC

TVC

TC, TVC and TFC

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 15

Short Run Total Cost Curves

Output

TFC

TVC

TC Cost

Output

TFC

TVC

TC Cost

Dr. Richard Boateng, UGBS

Slide 16

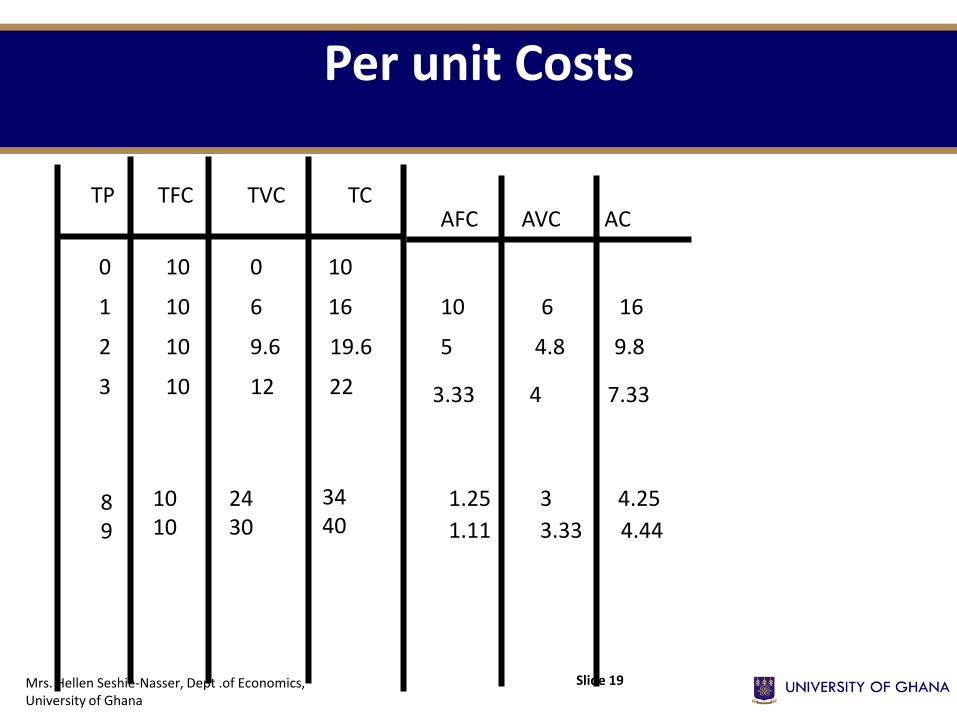

• Average Fixed Cost (AFC) is the total fixed cost divided by the quantity of output. It is the fixed cost per unit of output.

• It declines with output level. Since fixed cost is constant, the greater the output, the lower the AFC

• Average Variable Cost (AVC) is the variable cost per unit of output.

Per unit Costs

Slide 17 Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

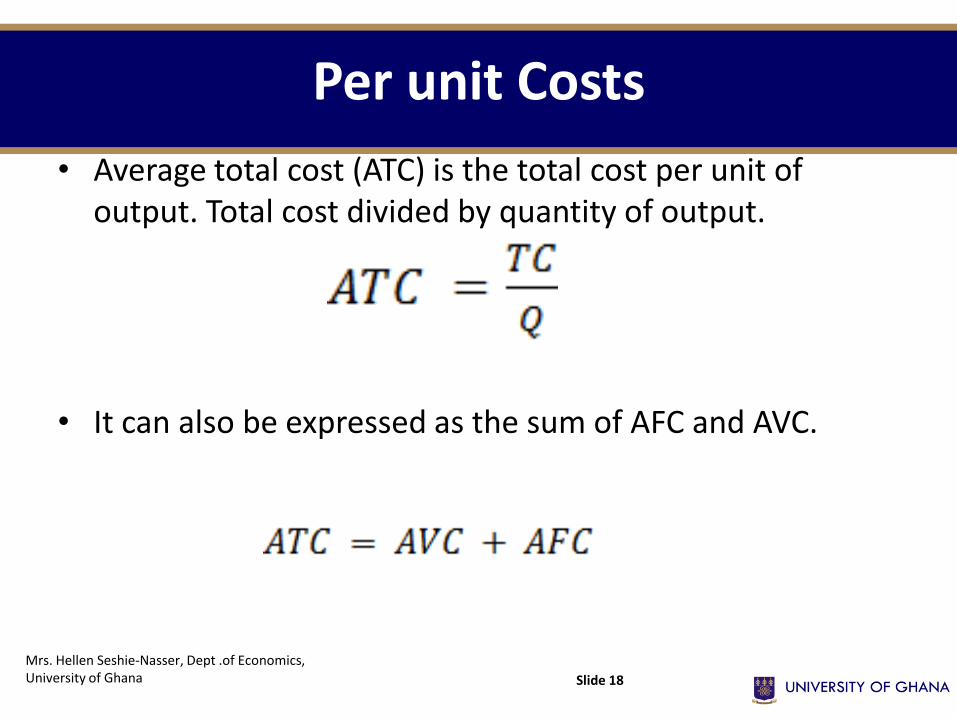

• Average total cost (ATC) is the total cost per unit of output. Total cost divided by quantity of output.

• It can also be expressed as the sum of AFC and AVC.

Per unit Costs

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana Slide 18

TP TFC TVC TC

0 10 0 10

1 10 6 16

2 10 9.6 19.6

3 10 12 22

8 9

10 10

24 30

34 40

AFC AVC AC

10 6 16

5 4.8 9.8

3.33 4 7.33

1.25 3 4.25

1.11 3.33 4.44

Per unit Costs

Slide 19 Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Marginal Cost

• Marginal cost (MC) is the change in total cost resulting from changing the rate of production by one unit.

• Change in TC due to one-unit increase in output (Q)

= change in TC

change in Q MC

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana Slide 20

TP TFC TVC TC

0 10 0 10

1 10 6 16

2 10 9.6 19.6

3 10 12 22

8 9

10 10

24 30

34 40

MC

6

3.6

2.4

6

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

TP, TFC, TVC, TC and MC

Slide 21

Q = output

AC, MC

AFC

ATC

AVC

MC

MC, ATC, AVC & AFC

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 22

Relationship between Short Run per unit Cost Curves

AFC

Output

AVC ATC

MC

Cost

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 23

MC and AC

• MC intersects AC at the minimum of AC

• When MC < AC, AC is falling

• When MC > AC, AC is rising

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana Slide 24

What shifts cost curves?

• Technology – make more with same inputs – shifts TP, MP, AP up – changes ATC curve

• Changes in factor prices (e.g. increase in input prices) – increase fixed costs -- TFC, AFC shift up -- TC shifts up – increase wages (variable) -- TVC, AVC, MC shift up -- TC shift up

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana Slide 25

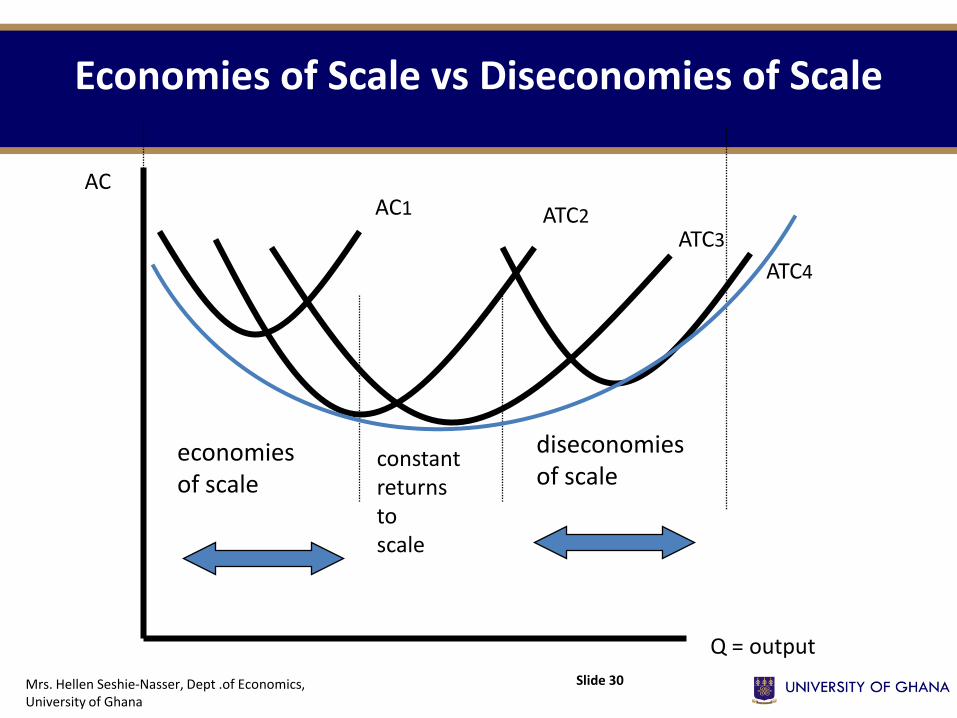

Long Run Costs: Average Cost (LRAC)

• In the LR, all inputs (and costs) are variable.

• TC = TVC

• AC = AVC

• Short Run AC curves are from different plant sizes

• The long run AC gives the lowest average cost when all inputs are variable. It is the envelop of all short run ACs

Slide 26 Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

LRAC

Q = output

AC

AC1 AC2 AC3

AC4

Long Run Costs: Average Cost (LRAC)

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 27

Economies of Scale

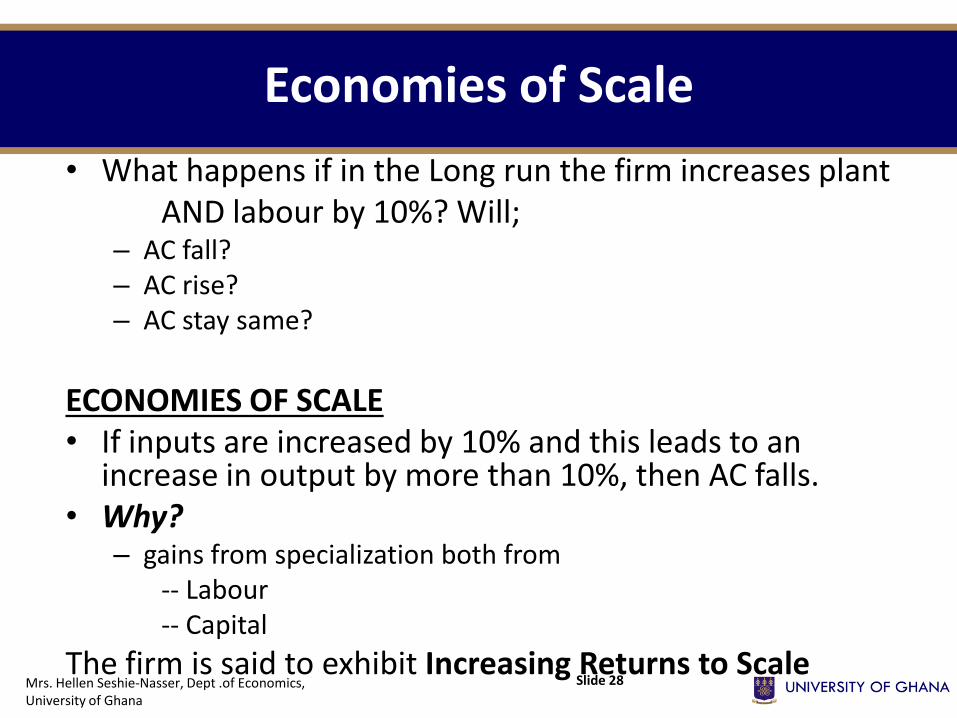

• What happens if in the Long run the firm increases plant AND labour by 10%? Will;

– AC fall? – AC rise? – AC stay same?

ECONOMIES OF SCALE • If inputs are increased by 10% and this leads to an

increase in output by more than 10%, then AC falls. • Why?

– gains from specialization both from -- Labour -- Capital

The firm is said to exhibit Increasing Returns to Scale Slide 28 Mrs. Hellen Seshie-Nasser, Dept .of Economics,

University of Ghana

Diseconomies of Scale

• On the other hand, if inputs are increased by 10%, and output increases by less than 10%, then AC rises.

• Why? – The firm has grown large such that, it has become too hard to control.

• The firm is said to be exhibiting Decreasing Returns to Scale

• CONSTANT RETURNS TO SCALE

• It occurs if for example, the firm increases inputs by 10%, and output also increases by same 10%. AC remains same

Dr. Richard Boateng, UGBSMrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 29

Q = output

AC AC1 ATC2

ATC3

ATC4

economies of scale

constant returns to scale

diseconomies of scale

Economies of Scale vs Diseconomies of Scale

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 30