eco 6351 economics for managers chapter 5. supply decisions prof. vera adamchik

TRANSCRIPT

Eco 6351Economics for Managers

Chapter 5. Supply Decisions

Prof. Vera Adamchik

• The basic activity of a firm is to use inputs, such as workers, machines, and natural resources to produce outputs of goods and services.

• A firm’s technology is the process it uses to turn inputs into outputs of goods and services.

• We want to make predictions about the behavior of firms. We want to predict (a) the quantities of goods and services produced; and (b) the amounts of resources (i.e., labor and capital) employed.

• The usual assumption made in economic theory is that consumers maximize utility and firms maximize profit.

The Firm’s Objective:Profit Maximization

Two types of constraints limit the profit a firm can make. They are:

• market constraints,

• technology constraints.

Market Constraints• A firm’s market constraints are the

conditions under which it can buy its inputs and sell its output.

• On the output side, people have a limited demand and will buy additional quantities only at lower prices.

• On the input side, there is a limited supply of the productive resources and additional quantities will be supplied only at higher prices.

Technology Constraints

• A firm’s technology constraints are the limits to the quantity of output that can be produced by using given quantities of inputs – productive resources.

The Short Run and the Long Run in Economics• The possibilities that are open to a firm

depend on the length of the planning period over which it is making its decisions.

• When firms analyze the relationship between their level of production and their costs, they separate the time period involved into the short run and the long run.

The Short Run and the Long Run

• The short run is a period of time in which the quantity of at least one input is fixed and the quantities of the other inputs can be varied.

• The long run is a period of time in which the quantities of all inputs can be varied.

• The actual length of calendar time in the short run will be different from firm to firm. A pizza parlor may be able to increase its physical plant by adding another pizza oven and some tables and chairs in just a few weeks.

• BMW may take more than a year in increase the capacity of one of its automobile assembly plants by installing new equipment.

Production and Costsin the Short Run

• Product Concepts and Definitions

• Short-Run Product Curves

• Cost Concepts and Definitions

• Short-Run Cost Curves

Short-Run Product Curves

• Total Product curve = Production Function

• Marginal Product curve

Example (SHORT RUN)Capital is fixed = 1 knitting machine

Labor Total Product (workers per day) (sweaters per day)• A 0 0• B 1 4• C 2 10• D 3 13• E 4 15• F 5 16

Product Concepts and Definitions

• Total product (TP) is the number of units of output produced in a given time period using a given quantity of resources.

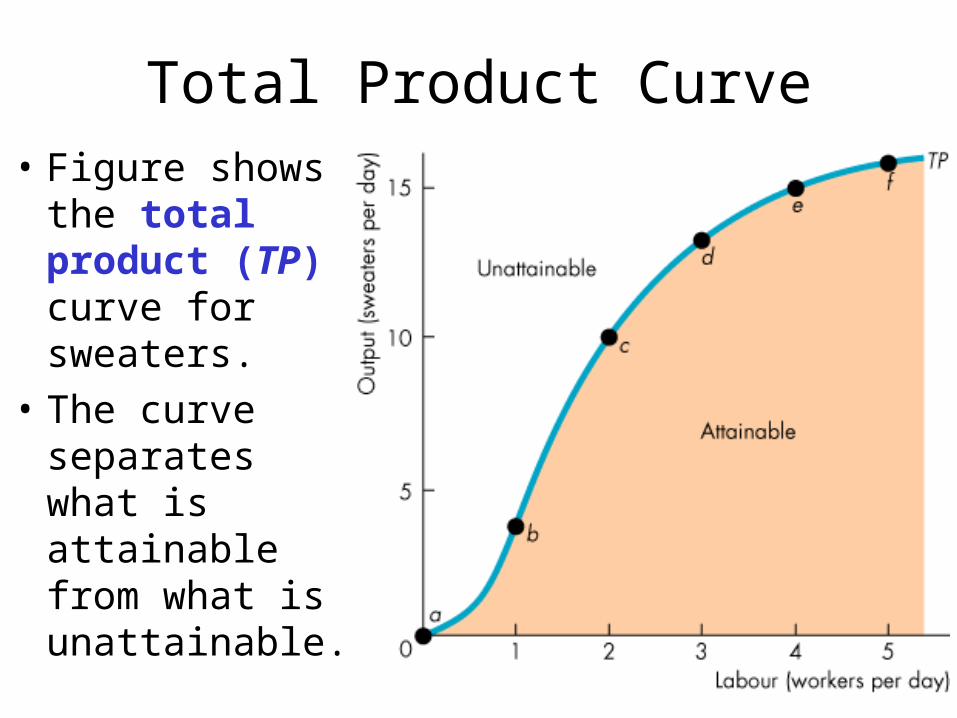

Total Product Curve• Figure shows

the total product (TP) curve for sweaters.

• The curve separates what is attainable from what is unattainable.

Example (conclusions)

• As the quantity of labor employed increases, output—total product—increases.

Product Concepts and Definitions

• Marginal product (MP) is the increase in total product, TP, resulting from a one-unit increase in the amount of the variable factor (labor) employed.

• Marginal product is calculated as the change in total product divided by the change in the quantity of the variable input.

Marginal Product Curve• Figure shows

the total product (TP) curve for sweaters again.

• But now, it emphasizes the idea of marginal product.

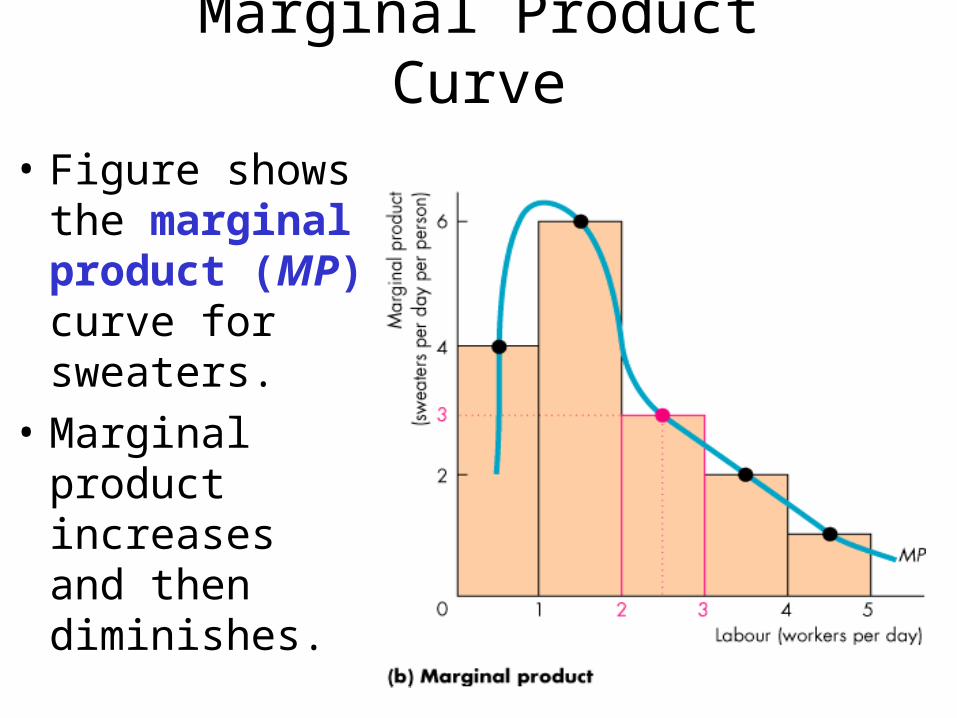

Marginal Product Curve• Figure shows

the marginal product (MP) curve for sweaters.

• Marginal product increases and then diminishes.

Example (conclusions): Initial Increasing Returns

• As a firm uses more of a variable input, with the quantity of fixed inputs held constant, the marginal product of the variable input at first increases.

Example (conclusions): The Law of Diminishing Returns

• As a firm uses more of a variable input, with the quantity of fixed inputs held constant, the marginal product of the variable input eventually diminishes.

Intuition on product curves

• Marginal product at first increases because of specialization and the division of labor.

• Marginal product eventually diminishes because the gains from specialization and the division of labor are limited and the plant eventually becomes congested.

Short-Run Cost Curves

• Total cost curves

• Average cost curves

• Marginal cost curve

Cost Concepts and Definitions

• Total fixed cost (TFC) is cost of all fixed inputs. Total fixed cost is independent of the level of output.

• Total variable cost (TVC) is cost of all variable inputs. Total variable cost varies with the level of output.

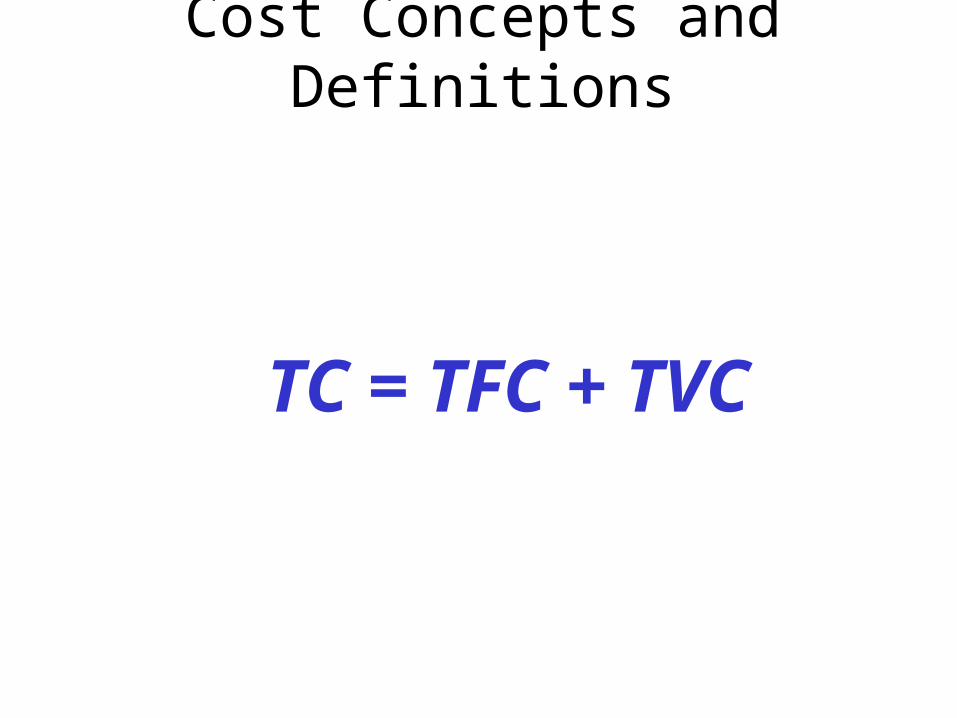

• Total cost (TC) is the sum of the costs of all the inputs used in production. Total cost is divided into two parts:

TC = TFC + TVC

Cost Concepts and Definitions

Example

• Our firm rents its knitting machine for $30 a day.

• It hires workers at a wage rate of $25 a day.

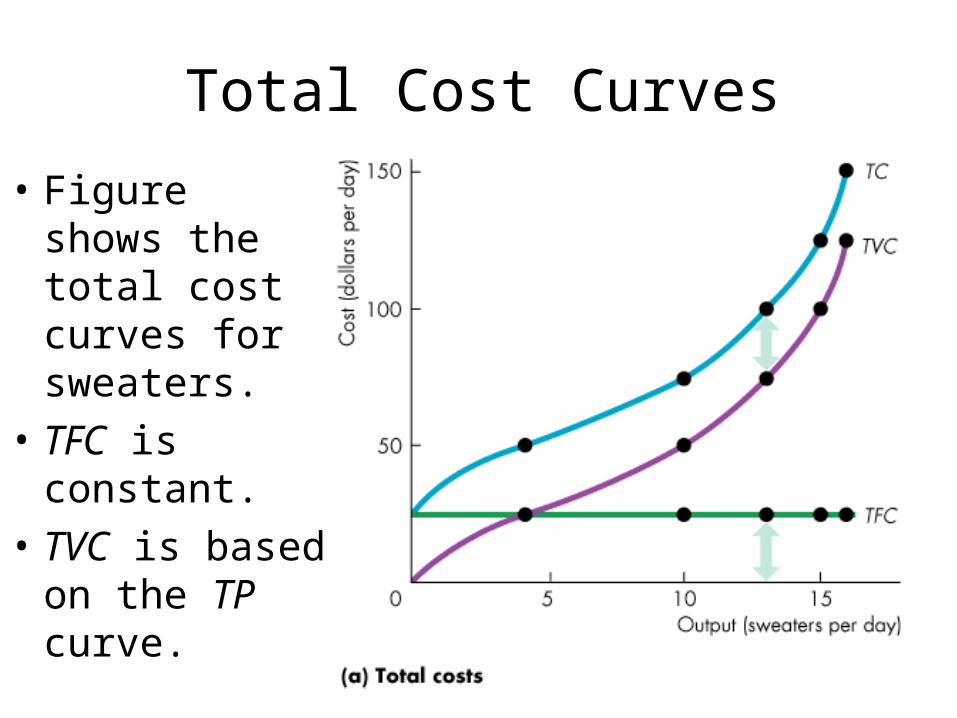

Total Cost Curves

• Figure shows the total cost curves for sweaters.

• TFC is constant.

• TVC is based on the TP curve.

Total Cost Curves

• TC is the sum of TFC and TVC.

• Average cost is cost per unit of output.

• Average total cost (ATC) is total cost per unit of output.

• Marginal cost (MC) is the increase in TC resulting from a one-unit increase in output. It is calculated as the change in total cost divided by the change in total output.

Cost Concepts and Definitions

ATC and MC

• Both ATC and MC are U-shaped.

• MC intersects ATC at its minimum point.

Accounting vs Economic Profit

• Accounting Profit =

TR – Total accounting cost

• Economic profit =

TR – Opportunity cost

Opportunity Cost

• Firms must consider the opportunity cost of their actions when they make production decisions.

• The opportunity cost of producing a unit of good x is quantity of good y that could have been produced in place of x, where good y is the highest value alternative to good x.

Opportunity Cost

• For convenience, we express opportunity cost in money units.

• A firm’s opportunity cost has two components:

– explicit costs,

– implicit costs.

Opportunity Cost

• Explicit costs are paid directly in money at the time that a resource is used in production.

Opportunity Cost

• Implicit costs are measured in units of money, but they are not paid for directly in money. A firm incurs implicit costs when it uses the following productive resources:

– capital equipment and buildings,

– inventories,

– owner’s capital (money) and owner’s human resources (time and entrepreneurial ability).