eastern maine healthcare systems maine healthcare systems ... •hiring of emhs executive team ......

TRANSCRIPT

Eastern Maine

Healthcare Systems Non-Profit Health Care Investor Conference

May 21, 2014

0

M. Michelle Hood, FACHE

President and Chief Executive Officer

Derrick O. Hollings, CPA

Senior Vice President, Treasurer/CFO

Together We’re Stronger 1

OUTLINE

System Overview Michelle Hood

Leadership Michelle Hood

Financials Derrick Hollings

Together We’re Stronger 2

Presented by Michelle Hood

SYSTEM OVERVIEW

Together We’re Stronger

‒ 10,301 employees

‒ 8 hospitals located across Maine

‒ 621 employed physicians

‒ 43 primary care practice locations

‒ 4 retail pharmacies

‒ 5 emergency transport units

‒ 9 nursing homes

‒ 5 home health locations

‒ integrated EMR

‒ freestanding cancer center

‒ 1.8 million outpatient visits annually

EMHS Provider Network

3

Together We’re Stronger

EMHS MARKET

SHARE

4

• EMHS exceeds 30% market share

across 2/3 of Maine’s geography

• 70% market share in Bangor

service area

• 25% market share in Portland

service area

Together We’re Stronger 5

Presented by Michelle Hood

LEADERSHIP

Together We’re Stronger

Leadership Engine

6

Passion Innovation Integrity Respect Partnership Accountability

EMHS partners with individuals and communities to improve health and

well-being by providing high quality, cost effective services.

EMHS will be a nationally recognized model of excellence in healthcare.

Mission

Vision

Values

Together We’re Stronger

Governance Structure

Committees of the Board of Directors

Clinical Coordinating

Governance Nomination Strategic Planning

Executive Management Performance

Finance Audit and

Compliance

Investment Function

Team

• Board Chair: Jim Nicholson, CPA

• Board Size: At least 15 and not more than 25 directors

• Board Committee: Representation from across market service area

• Board Term: 3 year term and maximum of 4 full consecutive terms

Council of Chairs

7

Together We’re Stronger 8

EMHS Board Exclusive

•System Level Budget

•Exercise rights as sole member or shareholder

Joint Board Initiatory Powers

•Member actions subjected to EMHS approval

•EMHS can act after consultation with Member

Member Board Exclusive

•Privileging and credentialing of medical staff

EMHS CEO

•Hiring of Member CEO

•Hiring of EMHS executive team

Member Organization CEO

•Hiring of Member Organization executive team

New Governance Model Joint & Exclusive Initiatory Powers

Integrated Member

Organizations subject to

EMHS, can initiate joint

strategic deliberation

and action

EMHS

President has

management

control of all

operations

EMHS, acting

independently,

can initiate

action at any

level

Together We’re Stronger

Triple Aim

9

Together We’re Stronger 10

State Wide ACO Network Beacon Health Leading Development of High Performing Provider Network

Together We’re Stronger

Beacon Health Pioneer ACP GPRO Benchmark Scores Compared to CMS 5 Star Cut Point

11

CMS 5 Star Cut Point

EMHS Beacon Health

• Medicare Advantage Plans

are graded on a 1-5 “star”

rating by CMS. The 5 star

quality rating system is

used to measure Medicare

beneficiaries experience

with their health plans and

the health care system.

• Beacon’s Pioneer ACO

GPRO Benchmark scores

when compared to the CMS

5 Star Cut Point, Beacon’s

scores were equal to or

higher in all but one

category

Together We’re Stronger

Brand Architecture Reinforce the strategy behind our statewide integrated care delivery system

12

Together We’re Stronger

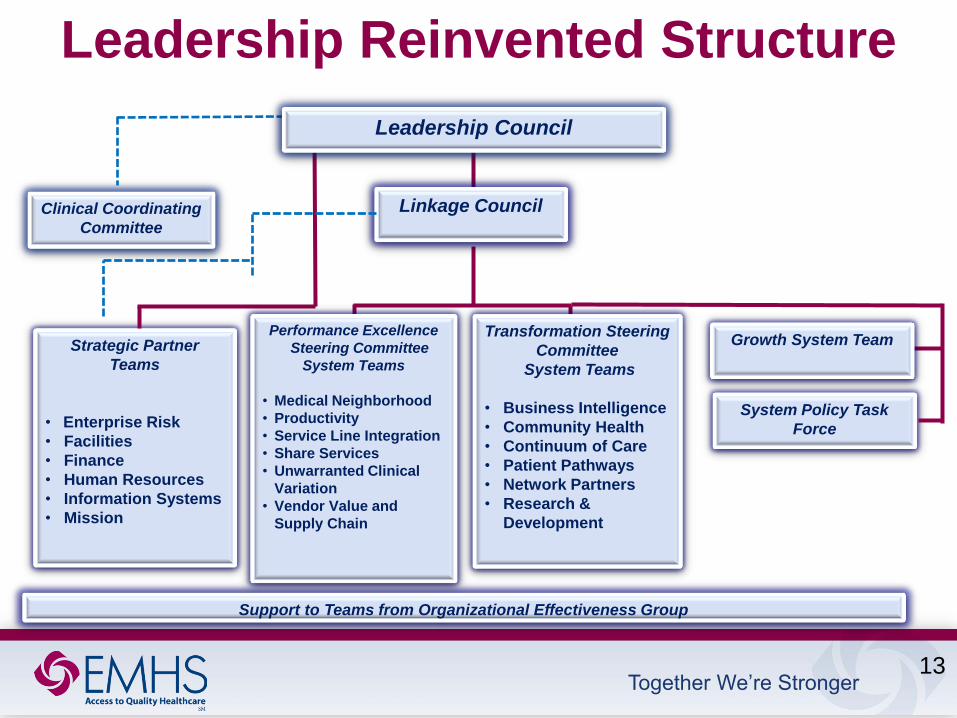

Leadership Reinvented Structure

Transformation Steering

Committee

System Teams

• Business Intelligence

• Community Health

• Continuum of Care

• Patient Pathways

• Network Partners

• Research &

Development

Strategic Partner

Teams

• Enterprise Risk

• Facilities

• Finance

• Human Resources

• Information Systems

• Mission

Leadership Council

Linkage Council Clinical Coordinating

Committee

Performance Excellence

Steering Committee

System Teams

• Medical Neighborhood

• Productivity

• Service Line Integration

• Share Services

• Unwarranted Clinical

Variation

• Vendor Value and

Supply Chain

Support to Teams from Organizational Effectiveness Group

Growth System Team

System Policy Task

Force

13

Together We’re Stronger

Leadership Reinvented

Strategy Teams Initiatives

Linkage Council

Leadership

Council

14

Together We’re Stronger 15

Human Resources Transformation Future Delivery Model

Together We’re Stronger

Nursing doc.

Doc. imaging CPOE/orders

Financial

Reporting

Medical Records

ED

Pharmacy

Surgery

EMPI

Device Integration

(from home)

OB Cardiology

Secure Messaging to Physician

(referrals, consults, notes)

ICU Oncology

Registration

Eligibility

ePrescribing

Patient

Education

Results

Review

Document Image Scanning CPOE/Orders

Protocols

Documentation Templates

Automated Faxing

Scanning

Patient

Messaging

EMPI

Chronic

Disease Registries PACS

P4P Reporting

PQRI / MU

Health

Maintenance

Office Device

Integration

Workflow

Task Queue

Appointment

Scheduling

Billing

AR

Charge

Capture

Bi Directional

Orders

Physician

Portal

Secure Messaging to Physician

(referrals, consults, notes)

Data Exchange

Community Viewer

NHIN

Personal Health

Record (PHR)

State Immunization

Registry

Patient Portal

eVisits

State

HIE

Enterprise Supply Chain & HRIS Enterprise Revenue

Foundation and

pathways

Enhanced data

capture and workflow

Interoperability/

Connectivity

Building The IT Foundation The Last Ten Years

Integration & Interoperability Platform

16

Together We’re Stronger

Future IT Architecture Delivery Model

Future Source Data Source Data

PHR Referral Patient

Satisfaction Lab PBM (Rx)

EPM Practice

Demographics

Payer

Non-Affiliate

EHR

Public

Health

Single

EHR

Population Health

Data Warehouse

Network

Practice

HIEs

Quality

Mgmt Physician

Profiling Payer/Contract

Analytics Network

Mgmt

Analytics

Physician

Portal

Patient

Portal

Registry

Integration & Interoperability Platform

HIEs Medical

Devices Data

Other Data

TBD

Care Management

Medical

Economics Patient/Physician

Engagement

<Internal Data

Research

External Data>

17

Together We’re Stronger

Real Estate Development

Corporation • Business Overview

• Developer services • Planning

• Design

• Construction Management

• Regulatory

• Landlord and tenant leasing

• Ongoing property management

• Acquisition and divestiture •Business Overview

• Healthcare Properties

• Hospitals

• Medical office buildings

• Ambulatory surgery centers

• Health plexes

• Free standing urgent cares

CORPORATE STRATEGY EMHS

The Client

Steering Committee

CLINICAL

STRATEGY The Client

Programming

Committee

FACILITIES

SUPPORT The Company

Developer

CPM

SUCCESSFUL

REAL ESTATE

DEVELOPMENTS

18

Together We’re Stronger

Transforming Payment Models Declining Dollars Entering Healthcare Will Trigger Reallocation of Existing Payments

• Episodic treatments and reactive approach

• Employed physicians with very little incentive for population health management

Patient Experience

Hospital Role

Health Plan

• Economics largely inpatient based

• Disjointed approach to cost reductions

• Infancy state of reducing variation in clinical care

• EMHS negotiating individual contracts for hospitals and physicians

• Reimbursements are based on number of transactions and gross charges

• Proactive wellness management , and care coordination for all illnesses

• Culture of personal accountability with incentives for care management

• Most care delivery in ambulatory settings

• Bed utilization management across health system to achieve maximum efficiency

• Care coordination strategies across patient care continuum

• Joint ventures with health plans

• EMHS at greater risk for managing costs in fixed budget arrangements

• Data collaborations with payers, patients and employers

Physician Alignment

• Low productivity in physician practices

• Fragmented medical groups across EMHS

• Lots of closed physician panels

• Real time tools tracking and measuring productivity

• Reduced clinical variations

• System wide product/service lines

EMHS Today EMHS Tomorrow

19

Together We’re Stronger

Treasury Transformation Future Delivery Model

Centralized Platform

Capital Allocation

Invested Asset

Cash Management

Cash

Investments • Assets are managed and

controlled at System level

• Allocation of cash resources

occurs across System

• Invested asset purpose and

policies and risk tolerance

set and then maintained at

System level

Financial Management

• Centralized Balance

Sheet

• Decentralized Income

Statements

• Business Unit

Model

• Performance

Centric Design

20

Cash Management • Pooling cash into single account at

System level

• Endowment remain aligned with Member

• Disbursements for payroll and vendors

occur at System level

Debt Management • All debt issued under single Obligated

Group

• System-wide capital structure that relates

to a System-wide risk point of view

• Allows capital market access for all

Members

Together We’re Stronger

Integrated Planning The whole is greater than sum of its parts

21

Demand • Trends rates /1000 populations • Clinical capacity • Competitive landscape • Service offering • Environmental impact Fiscal Year 15

Annual Budget

Fiscal Years 16-19 Financial Plan

Strategic Plan Capital Expenditures

Annual Budget Financial Plan

Planning

Business

Plans

Centralized

Budgeting

Process

5 Year Plan

Driven By

Performance

Metrics

Combination

of System &

Member

Prioritization

Together We’re Stronger

Population Health Migration

Physician Engagement

Clinical Transformation Clinically Integrated

Network Service

Distribution Network

• Breakeven on Medicare

• 3%-4% Operating Margin

• 10% - 12% EBIDA Margin

• “A “ Credit Ratings

• State Wide Network

• Hospitalized Care

• Ambulatory Care

• Skilled Nursing Facilities

• Home Health

• Hospice

• Long Term Acute Care

• Rehabilitation

• Healthplexes

• Care Redesign

• Beacon Health

• Health Exchanges

• Clinical Variations

• High Access Care

• Value Based Purchasing

• Productivity Standards

• Reduced Cost of Care

Financial Sustainability

• Primary Care Capabilities

• Specialist Care

• Re-align Incentives

• Practice Management Capability

• Physician Organization

Population Health

• Covered Lives

• Postal Code Attribution

• Community-Provider Partnerships

• Health Plan Partnerships

• Data Collaborative Agreements

• Risk-Bearing Models

• Shared Infrastructures

Supply Chain

Information Technology Advocacy

Business Intelligence

Revenue Management Grants/Fundraising Human Resources Medical Quality

Finance Insurance/Risk

Decision Support Mission Integration

Branding/Marketing Public Relations

Legal Strategic Planning

SHARED SERVICES INFRASTRUCTURE

22

Together We’re Stronger 23

Presented by Derrick Hollings

FINANCIALS

Together We’re Stronger

Debt Structure

1- As of June 1, 2014

1

24

* - Private Placement Debt

Debt

Par

Outstanding 1

Final

Maturity Coupon Enhancement Call Status

2014 Mercy* 8,450,000 2024 4.53% N/A 7/1/2014 @ 3%

2014 Mercy* 61,055,000 2036 3.07% N/A 7/1/2014 @ 3%

2013 EMMC $143,900,000 2043 3%-5% N/A 7/1/2023 @ par

2013 SVH* 9,924,999 2029 2.87%-3.41% N/A 1/1/2014 @ 5%

2012A TAMC 5,365,000 2022 2.5%-5.05 N/A 7/1/2022 @ par

2010B BHMH 2,130,000 2028 3.0%-5.25% N/A 7/1/2020 @ par

2010B TAMC 5,065,000 2019 3.0%-5.25% N/A Non-Callable

2010A Acadia 9,855,000 2021 3.0%-5.0% N/A 7/1/2020 @ par

2010A EMMC 64,730,000 2040 3.0%-5.25% N/A 7/1/2020 @ par

2007B Inland 2,845,000 2037 4.0%-5.0% FGIC 7/1/2018 @ par

2007B Lakewood 6,255,000 2037 4.0%-5.0% FGIC 7/1/2018 @ par

2006A Inland 1,135,000 2030 4.0%-5.0% MBIA 7/1/2015 @ par

2004B SVH 185,000 2015 3.625%-3.75% Ambac 7/1/2015 @ par

$320,894,999

Together We’re Stronger

Debt Dashboard

Bond Interest Mix

As of June 1, 2014

25

Maximum Annual Debt Service

Bond Debt Mix

Bond Debt Security

EMMC 67%

Acadia 2%

BHMH 1%

TAMC 2%

SVH 2%

Inland 4%

CA Dean 0%

Home Office

7%

Mercy 15%

Obligated Group,

64%

Non-Obligated

Group, 21%

Private 25%

Public 75%

Private Fixed, 28%

Public Fixed, 62%

Variable , 2%

Synthetic Fixed, 8%

Together We’re Stronger

Obligated Groups

Potential Obligated Group Member

EMHS

(Parent)

Acadia Hospital Corp.

Affiliated Healthcare Systems

Beacon Health, LLC

Blue Hill Memorial Hospital

C.A. Dean Memorial Hospital

EMH Real Estate

EM HomeCare

EMMC EMHS Foundation

Inland Hospital

ME Institute for Human Genetics

and Health

ME Network for Health

Mercy HS of ME

Rosscare

SVH

TAMC

Obligated Group Member

26

Exclude From Obligated Group

Together We’re Stronger

Revenue Growth

27

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2008 2009 2010 2011 2012 2013 2014

Total Revenue

(1)

Note 1: Forecast

Together We’re Stronger

Outpatient Visits Growth

28

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2011 2012 2013 2014

Outpatient Visits

(1)

Note 1: Forecast

Together We’re Stronger

Primary Care Visits Growth

29

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2011 2012 2013 2014

Primary Care Visits

Note 1: Forecast

(1)

Together We’re Stronger

Assets Growth

30

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

2009 2010 2011 2012 2013 2014

Total Assets

Note 1: as of March 31, 2014

(1)

Together We’re Stronger

Key Performance Indicators

Description 2011 2012 2013 2014 (1)

Debt Position:

Debt Service Coverage 4.4 6.0 6.5 2.8

LTD to Capitalization 29.6% 25.1% 36.8% 36.4%

Debt Service as % of Revenue 1.9% 1.8% 1.7% 2.2%

Cushion Ratio 15.1 16.6 21.9 15.4

Liquidity:

Cash to Long Term Debt 167% 200% 122% 120%

Days Cash on Hand 113 124 146 134

Days in A/R, net 38.4 33.4 38.4 41

Performance:

Operating Margin 2.2% 5.9% 3.7% -1.6%

EBIDA Margin 7.6% 10.7% 8.6% 2.9%

Total Margin 3.1% 6.1% 6.2% -1.3%

Note 1: as of March 31, 2014

31

Together We’re Stronger

Thank You

32