eastern india regional councileirc-icai.org/admin_panel/newsletter_files/_eirc_f677efac8b7fa... ·...

TRANSCRIPT

EIRC 1st June 2017 �

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

EIRC e-NEWSLETTERVOL 43 ISSUE : 4 1st JUNE 2017 ` 10/-

EASTERN INDIA REGIONAL COUNCIL

(Set up by an Act of Parliament)

��EIRC 1st June 2017

EIRC 1st June 2017 �

Dear Esteemed Colleagues,

Greetings !!!

I am in a way convinced that when we do

right things in the right way and at the right

time, success is bound to be achieved, but to

my mind, we need to stretch our thoughts,

look out for innovation, conceptualize

newer ideas and deliver the best. In the last

three months since taking over the office of

Chairman of EIRC, myself and my excellent

dedicated team have been trying to focus

our thoughts to provide the best of services to the members and students. I would,

now like to share that EIRC received excellent support and input from the members

for every programme of ours. I take this opportunity to thank every one of the

members, look forward to your continued co-operation, and support in our pursuit

to deliver the best to your satisfaction.

“Start by doing what’s necessary; then do what’s possible; and suddenly

you will see that you are doing the impossible .. !!”

GST the biggest challenge and opportunity for Chartered Accountants has been

the focus of our EIRC activities, apart from presenting quality programmes on all

possible professional topics to the members. It has been a constant endeavour of

this Regional Council to update our esteemed professionals and make them abreast

of all the quick updates, developments, be it Direct Taxes, Insolvency, ICDS, IFC,

Ind AS, Forensic Auditing to name a few amongst many programmes. We have

been successful in commencement of the 1st Certificate Course on GST at Kolkata

amongst all other Regions.

Another area that I wish to bring to notice to all my professionals that today, is the

need of more effective coordination & liasoning with the Government. Be it State

or Central. As we know that we are not in control of things and most of the times

only respond to situations. This has to change. We at the Regional Council wish to

appeal to my professional colleagues that anyone who are having dealings with

various ministries/government departments should have best of best co-ordination

and cordial relationship so as to ensure that our Region’s involvement is more in the

drafting of policies/bills/acts/laws rather than following up and representing later.

We as an institution referred as partners in Nation Building has greater role to play

other than just carrying out activities for our members. In this regard we have taken

the responsibility of organising GST Awareness events across the region so as to

disseminate the knowledge to all strata of the society. I am happy to share that

our members in general in their individual capacities are also making themselves

available as faculties in such events and portraying the image of ICAI as Knowledge

Partner. In this series many of our branches have held events with various trade

bodies and business association which is laudable. We at EIRC were able to join

hands with the Directorate of Commercial Taxes, West Bengal to organise such an

event at Kolkata, wherein the auditorium was overflowing with people from various

trade. I had the occasion to discuss about the Entry Tax in West Bengal with the

officials of the Directorate and they appreciated our suggestions to introduce a

Settlement of Dispute scheme in order to waive interest and penalty on demands

relating to Entry Taxes in West Bengal. Our members would be happy to know that

such a scheme has been passed by the West Bengal Legislative Assemble and has

gone for the assent of the Governor.

Its sizzling hot summer and the same way the EIRC activities have gained pace in

organising multifarious programmes for its members and students at the Region.

EIRC would like to make the season and its weather a pleasant one in terms of

updation of professional knowledge by organizing numerous programmes, which

includes the All Region Joint at cool elevated areas, like Darjeeling &Mirik in the

last week of June 2017, wherein we would be bestowed with the opportunity to

host representatives of all Regions and stay at different parts of the Country at the

Queen of Hills in our Region.

In the month of May we were able to organise two sub-regional conferences one

in Assam at Tinsukia, wherein Honourable M.P Sri Rameshwar . Teli was present as

the Chief Guest and other at Rourkela in Odissa. I am thankful to the members of

both the branches for hosting the same.

Our members have been good friends & guide to our article students. However, at

times certain malpractices & actions by some unethical professional bring a dent in

our reputation. Article ship Training based on age old concept of Guru- Shishya,

should be considered as a sacred and pious service to the future generation of our

country. The menace of improper article ship is engulfing our profession and for

the deeds of a handful the entire profession is taken to the task. I would urge my

respected members to refrain from any such kind of activities. Our HO is envisaging

some measures to check on this menace which would be announced in near future.

The EIRC website (www.eirc-icai.org) is a link to share information relating to

EIRC and activities relating to its branches & study circles. Members are requested to

kindly reap benefit of the same by visiting and also making a onetime registration

with their current details so that we can send you timely information through

various modes of communication.

We in our endeavour to provide support to the Skill India Program of the

Government are envisaging a plan to associate with various colleges in the region

wherein their graduates could join the offices as trainees. EIRC would just act as

facilitator and provide a platform to such students who want to join the CA firms

and members who could employ them. The students could enrich themselves

by learning the various tasks carried out by the firms. This will make them skilful

and employable. Especially at the time when GST is on the anvil there would be

huge requirement of GST Professionals, these students can take true benefit of this

opportunity. In turn our members who are feeling the dearth of article students

would be able to train and then employ them in their organisations.

Profession apart, one thing, which I would like to mention, is that our beloved

motherland is disturbed today, mainly by our own brethren. Terrorism is rampant,

precious lives are lost, national property is destroyed. Calmness is lacking. Our

country is getting engulfed in violence especially in the valleys, drenched with

human blood, destroyed civilization leading the whole nation in despair. We feel

desperate many times watching the situation and blaming somebody for the

situation. While many things are not in our sole control, I believe that we should

observe the ambience around us and just think, whether we can contribute for the

improvement of the same. Any little effort in this regard is its worth.

The monsoon is just set in and it will bring respite from the scorching heat. Its

also time to look towards our environment and plant trees to observe World

environment Day. The holy month of Ramzan has also begun and my sincere prayers

to the almighty to take our country to its golden era.

Looking forward to interact with you soon.

With Warm regards.

CA Manish Goyal

Chairman, EIRC of ICAI

��EIRC 1st June 2017

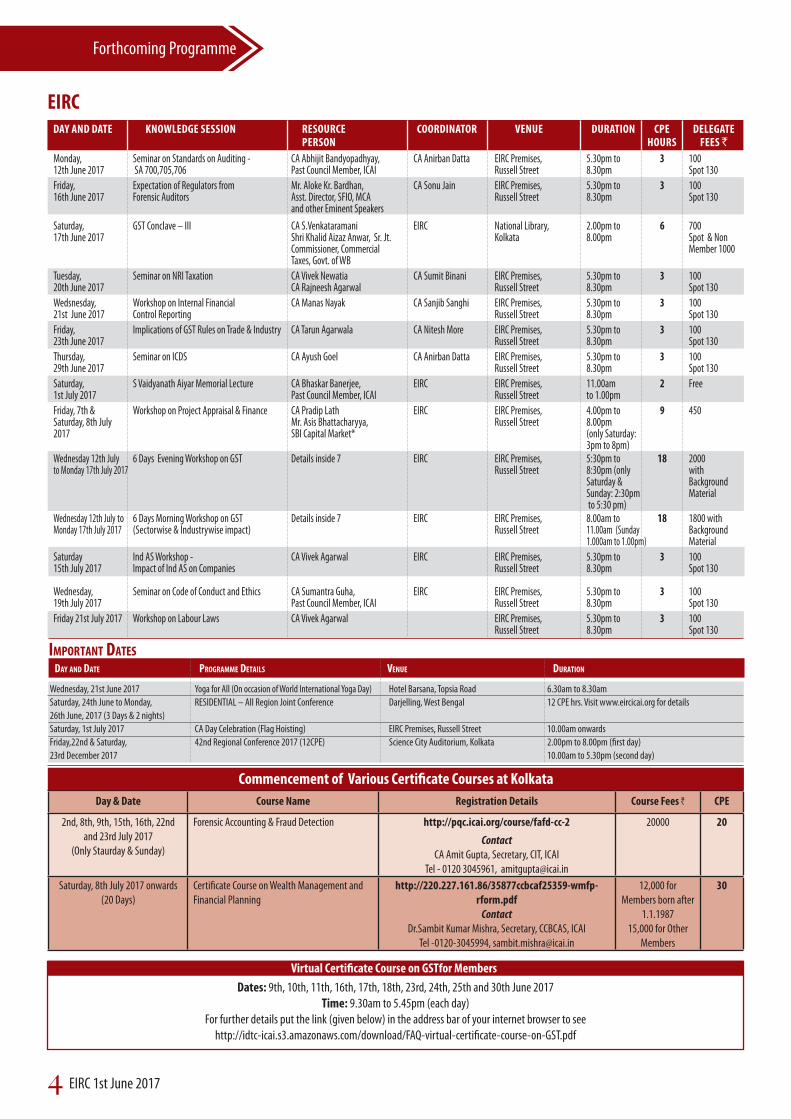

Forthcoming Programme

DAY AND DATE KNOWLEDGE SESSION RESOURCE COORDINATOR VENUE DURATION CPE DELEGATE PERSON HOURS FEES `

EIRC

Monday, Seminar on Standards on Auditing - CA Abhijit Bandyopadhyay, CA Anirban Datta EIRC Premises, 5.30pm to 3 10012th June 2017 SA 700,705,706 Past Council Member, ICAI Russell Street 8.30pm Spot 130

Friday, Expectation of Regulators from Mr. Aloke Kr. Bardhan, CA Sonu Jain EIRC Premises, 5.30pm to 3 10016th June 2017 Forensic Auditors Asst. Director, SFIO, MCA Russell Street 8.30pm Spot 130 and other Eminent Speakers

Saturday, GST Conclave – III CA S.Venkataramani EIRC National Library, 2.00pm to 6 700 17th June 2017 Shri Khalid Aizaz Anwar, Sr. Jt. Kolkata 8.00pm Spot & Non Commissioner, Commercial Member 1000 Taxes, Govt. of WB

Tuesday, Seminar on NRI Taxation CA Vivek Newatia CA Sumit Binani EIRC Premises, 5.30pm to 3 10020th June 2017 CA Rajneesh Agarwal Russell Street 8.30pm Spot 130

Wedsnesday, Workshop on Internal Financial CA Manas Nayak CA Sanjib Sanghi EIRC Premises, 5.30pm to 3 10021st June 2017 Control Reporting Russell Street 8.30pm Spot 130

Friday, Implications of GST Rules on Trade & Industry CA Tarun Agarwala CA Nitesh More EIRC Premises, 5.30pm to 3 10023th June 2017 Russell Street 8.30pm Spot 130

Thursday, Seminar on ICDS CA Ayush Goel CA Anirban Datta EIRC Premises, 5.30pm to 3 10029th June 2017 Russell Street 8.30pm Spot 130

Saturday, S Vaidyanath Aiyar Memorial Lecture CA Bhaskar Banerjee, EIRC EIRC Premises, 11.00am 2 Free1st July 2017 Past Council Member, ICAI Russell Street to 1.00pm

Friday, 7th & Workshop on Project Appraisal & Finance CA Pradip Lath EIRC EIRC Premises, 4.00pm to 9 450Saturday, 8th July Mr. Asis Bhattacharyya, Russell Street 8.00pm2017 SBI Capital Market* (only Saturday: 3pm to 8pm)Wednesday 12th July 6 Days Evening Workshop on GST Details inside 7 EIRC EIRC Premises, 5:30pm to 18 2000to Monday 17th July 2017 Russell Street 8:30pm (only with Saturday & Background Sunday: 2:30pm Material to 5:30 pm) Wednesday 12th July to 6 Days Morning Workshop on GST Details inside 7 EIRC EIRC Premises, 8.00am to 18 1800 withMonday 17th July 2017 (Sectorwise & Industrywise impact) Russell Street 11.00am (Sunday Background 1.000am to 1.00pm) Material

Saturday Ind AS Workshop - CA Vivek Agarwal EIRC EIRC Premises, 5.30pm to 3 10015th July 2017 Impact of Ind AS on Companies Russell Street 8.30pm Spot 130

Wednesday, Seminar on Code of Conduct and Ethics CA Sumantra Guha, EIRC EIRC Premises, 5.30pm to 3 10019th July 2017 Past Council Member, ICAI Russell Street 8.30pm Spot 130

Friday 21st July 2017 Workshop on Labour Laws CA Vivek Agarwal EIRC Premises, 5.30pm to 3 100 Russell Street 8.30pm Spot 130

DAY AND DATE PROGRAMME DETAILS VENUE DURATION

IMPORTANT DATES

Wednesday, 21st June 2017 Yoga for All (On occasion of World International Yoga Day) Hotel Barsana, Topsia Road 6.30am to 8.30am

Saturday, 24th June to Monday, RESIDENTIAL – All Region Joint Conference Darjelling, West Bengal 12 CPE hrs. Visit www.eircicai.org for details

26th June, 2017 (3 Days & 2 nights)

Saturday, 1st July 2017 CA Day Celebration (Flag Hoisting) EIRC Premises, Russell Street 10.00am onwards

Friday,22nd & Saturday, 42nd Regional Conference 2017 (12CPE) Science City Auditorium, Kolkata 2.00pm to 8.00pm (first day)

23rd December 2017 10.00am to 5.30pm (second day)

Day & Date Course Name Registration Details Course Fees ` CPE

2nd, 8th, 9th, 15th, 16th, 22nd and 23rd July 2017

(Only Staurday & Sunday)

Forensic Accounting & Fraud Detection http://pqc.icai.org/course/fafd-cc-2

ContactCA Amit Gupta, Secretary, CIT, ICAI

Tel - 0120 3045961, [email protected]

20000 20

Saturday, 8th July 2017 onwards

(20 Days)

Certificate Course on Wealth Management and

Financial Planning

http://220.227.161.86/35877ccbcaf25359-wmfp-

rform.pdfContact

Dr.Sambit Kumar Mishra, Secretary, CCBCAS, ICAI

Tel -0120-3045994, [email protected]

12,000 for Members born after

1.1.198715,000 for Other

Members

30

Commencement of Various Certificate Courses at Kolkata

Dates: 9th, 10th, 11th, 16th, 17th, 18th, 23rd, 24th, 25th and 30th June 2017Time: 9.30am to 5.45pm (each day)

For further details put the link (given below) in the address bar of your internet browser to see http://idtc-icai.s3.amazonaws.com/download/FAQ-virtual-certificate-course-on-GST.pdf

Virtual Certificate Course on GSTfor Members

EIRC 1st June 2017 �

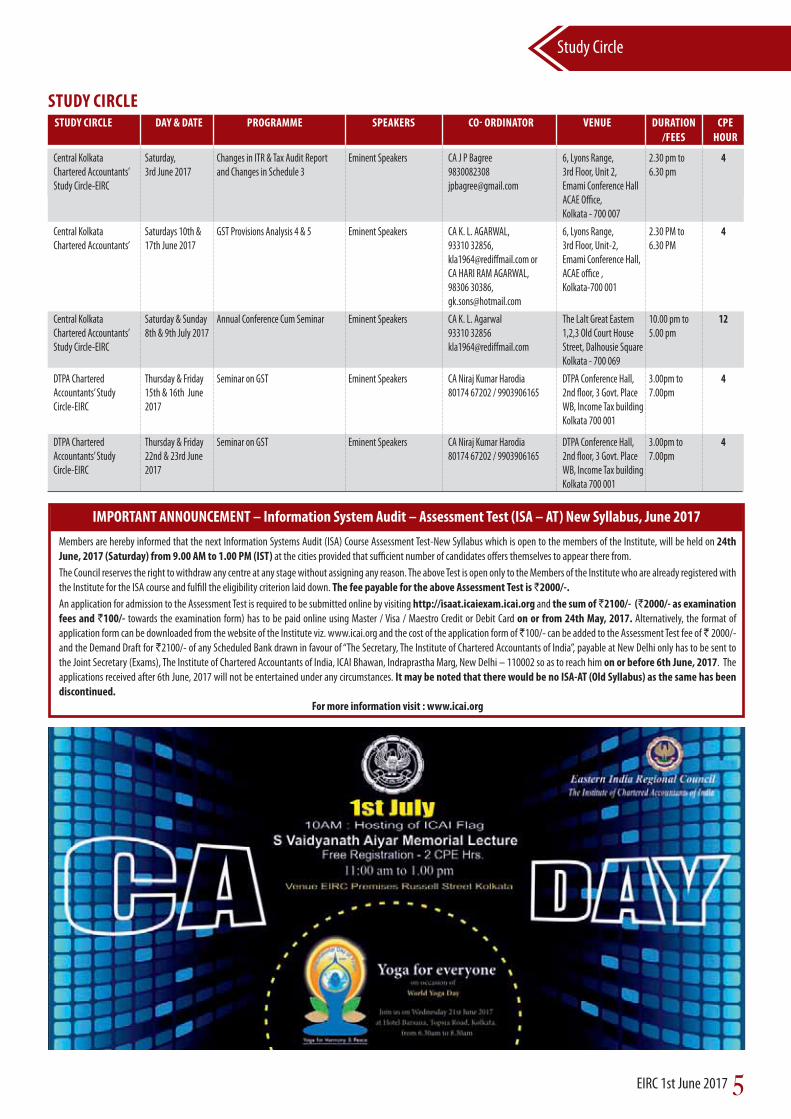

Study Circle

STUDY CIRCLESTUDY CIRCLE DAY & DATE PROGRAMME SPEAKERS CO- ORDINATOR VENUE DURATION CPE

/FEES HOUR

Central Kolkata Saturday, Changes in ITR & Tax Audit Report Eminent Speakers CA J P Bagree 6, Lyons Range, 2.30 pm to 4Chartered Accountants’ 3rd June 2017 and Changes in Schedule 3 9830082308 3rd Floor, Unit 2, 6.30 pmStudy Circle-EIRC [email protected] Emami Conference Hall ACAE Office, Kolkata - 700 007

Central Kolkata Saturdays 10th & GST Provisions Analysis 4 & 5 Eminent Speakers CA K. L. AGARWAL, 6, Lyons Range, 2.30 PM to 4Chartered Accountants’ 17th June 2017 93310 32856, 3rd Floor, Unit-2, 6.30 PM [email protected] or Emami Conference Hall, CA HARI RAM AGARWAL, ACAE office , 98306 30386, Kolkata-700 001 [email protected]

Central Kolkata Saturday & Sunday Annual Conference Cum Seminar Eminent Speakers CA K. L. Agarwal The Lalt Great Eastern 10.00 pm to 12Chartered Accountants’ 8th & 9th July 2017 93310 32856 1,2,3 Old Court House 5.00 pmStudy Circle-EIRC [email protected] Street, Dalhousie Square Kolkata - 700 069

DTPA Chartered Thursday & Friday Seminar on GST Eminent Speakers CA Niraj Kumar Harodia DTPA Conference Hall, 3.00pm to 4Accountants’ Study 15th & 16th June 80174 67202 / 9903906165 2nd floor, 3 Govt. Place 7.00pmCircle-EIRC 2017 WB, Income Tax building Kolkata 700 001

DTPA Chartered Thursday & Friday Seminar on GST Eminent Speakers CA Niraj Kumar Harodia DTPA Conference Hall, 3.00pm to 4Accountants’ Study 22nd & 23rd June 80174 67202 / 9903906165 2nd floor, 3 Govt. Place 7.00pmCircle-EIRC 2017 WB, Income Tax building Kolkata 700 001

IMPORTANT ANNOUNCEMENT – Information System Audit – Assessment Test (ISA – AT) New Syllabus, June 2017

Members are hereby informed that the next Information Systems Audit (ISA) Course Assessment Test-New Syllabus which is open to the members of the Institute, will be held on 24th

June, 2017 (Saturday) from 9.00 AM to 1.00 PM (IST) at the cities provided that sufficient number of candidates offers themselves to appear there from.

The Council reserves the right to withdraw any centre at any stage without assigning any reason. The above Test is open only to the Members of the Institute who are already registered with

the Institute for the ISA course and fulfill the eligibility criterion laid down. The fee payable for the above Assessment Test is `2000/-.

An application for admission to the Assessment Test is required to be submitted online by visiting http://isaat.icaiexam.icai.org and the sum of `2100/- (`2000/- as examination

fees and `100/- towards the examination form) has to be paid online using Master / Visa / Maestro Credit or Debit Card on or from 24th May, 2017. Alternatively, the format of

application form can be downloaded from the website of the Institute viz. www.icai.org and the cost of the application form of `100/- can be added to the Assessment Test fee of ` 2000/-

and the Demand Draft for `2100/- of any Scheduled Bank drawn in favour of “The Secretary, The Institute of Chartered Accountants of India”, payable at New Delhi only has to be sent to

the Joint Secretary (Exams), The Institute of Chartered Accountants of India, ICAI Bhawan, Indraprastha Marg, New Delhi – 110002 so as to reach him on or before 6th June, 2017. The

applications received after 6th June, 2017 will not be entertained under any circumstances. It may be noted that there would be no ISA-AT (Old Syllabus) as the same has been

discontinued.

For more information visit : www.icai.org

��EIRC 1st June 2017

EICASA

EICASADAY AND DATE KNOWLEDGE SESSION RESOURCE PERSON VENUE DURATION DELEGATE FEES `

Thursday 15, 2017 Regional Level Elocution Contest EIRC & EICASA EIRC Premises, Russell Street – –

Friday 16, 2017 3-days Workshop ON GST CA Shubham Khaitan EIRC Premises, Russell Street 10.00am to 3.00pm 300

Saturday 17, 2017

Sunday 18, 2017

National Talent Hunt & Quiz Contest (Branch Level) on 24th May 2017

GST Refresher Course from 25th May 2017 to 27th May 2017

E-Fling of TDS Return by CA Ghanshyam Kalani on 22nd May 2017

My Dear Student Friends,

As Shraga Silverstein rightly observed, “We

are sometimes kept from doing good by a

too lofty impression of goodness.” We can

achieve everything if we touch the bottom of

his observation. Silverstein actually echoed

Napoleon’s famous feeling that impossibility

should be shelved into dictionary. Very

commonly “We the people” see and deem

and infer that “nobility” is not “my cup of tea”.

They consider it either impossible or tough ,

consciously or unconsciously being oblivious of the fact that “genius is three-fourth

perspiration and one-fourth inspiration.” Either with awe or with reverence we see

the “genius” and fear away from them. But we must realize that everything we

deem “tough” has been perceived and accomplished by creatures like us. Will creates

the difference.

Many a people consider Chartered Accountancy as a “tough” course. In actuality, it is

just a shape of mind , lacking of a positive outlook that makes it tough. Weak mind

people are also very strong in spreading rumours. This way “we” develop a notion

that it would not work and consequently failures followed by drop-outs come.

Traditionally speaking, May and June are the months of examinationwhile in reality

exam is a continuous process. Hence my dear students, keep it in mind that no

failure is greater than thinking and no thinking supersedes action.

In my tenure as the Chairperson of EICASA, I am working hard to convey this to all

my students that our TEAM is keen to clarify this particular message that not only

Chartered Accountancy but any impediment as a whole may be overcome if will

is there. With this end in view, we are structuring a diversified programmes apart

from initiatives being taken by the Institute. So please be vigilant with the eirc

website (www.eirc-icai.org) and do take initiative to participate in attending in and

organizing as maximum number of significant events as possible.

This month would be full with enthusiasm for CA Students’ National Conference to

be held at Kalamandir Auditorium, Shakespeare Sarani, Kolkata on 14.07.2017 and

15.07.2017 with a multitude of topics to be discussed upon by a host of prominent

personalities from the profession with prolific speakers deliberating on motivational

topic. It is going to be a great regret who will miss this opportunity. I hope that

everybody would take it seriously to join this grand event being organized by the

EICASA.

Please do register yourselves for workshops on GST for students which has already

been hoisted in the eirc site. In the days to follow the national conference would be

witnessing a procession of events like Educational Tour, Industrial Visits, Semianrs,

Workshops and many more.

Logging out by saying that enjoyment gives you pleasure but involvement leads you

to satisfaction which is success in disguise.

CA Sonu Jain

Chairperson EICASA and Vice Chairperson EIRC of ICAI

EIRC 1st June 2017

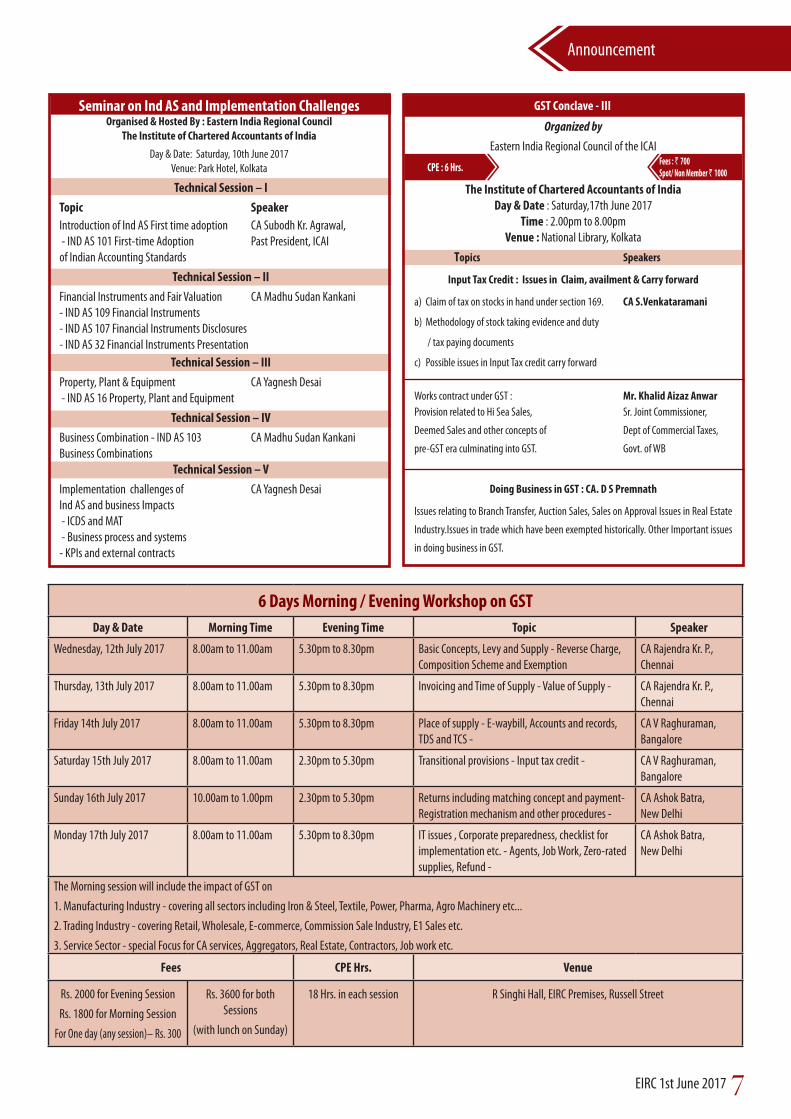

Announcement

Fees : ` 700Spot/ Non Member ` 1000

GST Conclave - III

CPE : 6 Hrs.

Organized by

Eastern India Regional Council of the ICAI

The Institute of Chartered Accountants of IndiaDay & Date : Saturday,17th June 2017

Time : 2.00pm to 8.00pmVenue : National Library, Kolkata

Topics Speakers

Input Tax Credit : Issues in Claim, availment & Carry forward

a) Claim of tax on stocks in hand under section 169. CA S.Venkataramani

b) Methodology of stock taking evidence and duty

/ tax paying documents

c) Possible issues in Input Tax credit carry forward

Works contract under GST : Mr. Khalid Aizaz Anwar

Provision related to Hi Sea Sales, Sr. Joint Commissioner,

Deemed Sales and other concepts of Dept of Commercial Taxes,

pre-GST era culminating into GST. Govt. of WB

Doing Business in GST : CA. D S Premnath

Issues relating to Branch Transfer, Auction Sales, Sales on Approval Issues in Real Estate

Industry.Issues in trade which have been exempted historically. Other Important issues

in doing business in GST.

Seminar on Ind AS and Implementation Challenges Organised & Hosted By : Eastern India Regional Council

The Institute of Chartered Accountants of India

Day & Date: Saturday, 10th June 2017Venue: Park Hotel, Kolkata

Technical Session – I

Topic Speaker

Introduction of Ind AS First time adoption CA Subodh Kr. Agrawal, - IND AS 101 First-time Adoption Past President, ICAIof Indian Accounting Standards

Technical Session – II

Financial Instruments and Fair Valuation CA Madhu Sudan Kankani- IND AS 109 Financial Instruments- IND AS 107 Financial Instruments Disclosures- IND AS 32 Financial Instruments Presentation

Technical Session – III

Property, Plant & Equipment CA Yagnesh Desai - IND AS 16 Property, Plant and Equipment

Technical Session – IV

Business Combination - IND AS 103 CA Madhu Sudan KankaniBusiness Combinations

Technical Session – V

Implementation challenges of CA Yagnesh DesaiInd AS and business Impacts - ICDS and MAT - Business process and systems - KPIs and external contracts

6 Days Morning / Evening Workshop on GST

Day & Date Morning Time Evening Time Topic Speaker

Wednesday, 12th July 2017 8.00am to 11.00am 5.30pm to 8.30pm Basic Concepts, Levy and Supply - Reverse Charge, Composition Scheme and Exemption

CA Rajendra Kr. P., Chennai

Thursday, 13th July 2017 8.00am to 11.00am 5.30pm to 8.30pm Invoicing and Time of Supply - Value of Supply - CA Rajendra Kr. P., Chennai

Friday 14th July 2017 8.00am to 11.00am 5.30pm to 8.30pm Place of supply - E-waybill, Accounts and records, TDS and TCS -

CA V Raghuraman, Bangalore

Saturday 15th July 2017 8.00am to 11.00am 2.30pm to 5.30pm Transitional provisions - Input tax credit - CA V Raghuraman, Bangalore

Sunday 16th July 2017 10.00am to 1.00pm 2.30pm to 5.30pm Returns including matching concept and payment- Registration mechanism and other procedures -

CA Ashok Batra, New Delhi

Monday 17th July 2017 8.00am to 11.00am 5.30pm to 8.30pm IT issues , Corporate preparedness, checklist for implementation etc. - Agents, Job Work, Zero-rated supplies, Refund -

CA Ashok Batra, New Delhi

The Morning session will include the impact of GST on

1. Manufacturing Industry - covering all sectors including Iron & Steel, Textile, Power, Pharma, Agro Machinery etc...

2. Trading Industry - covering Retail, Wholesale, E-commerce, Commission Sale Industry, E1 Sales etc.

3. Service Sector - special Focus for CA services, Aggregators, Real Estate, Contractors, Job work etc.

Fees CPE Hrs. Venue

Rs. 2000 for Evening Session

Rs. 1800 for Morning Session

For One day (any session)– Rs. 300

Rs. 3600 for both Sessions

(with lunch on Sunday)

18 Hrs. in each session R Singhi Hall, EIRC Premises, Russell Street

�EIRC 1st June 2017

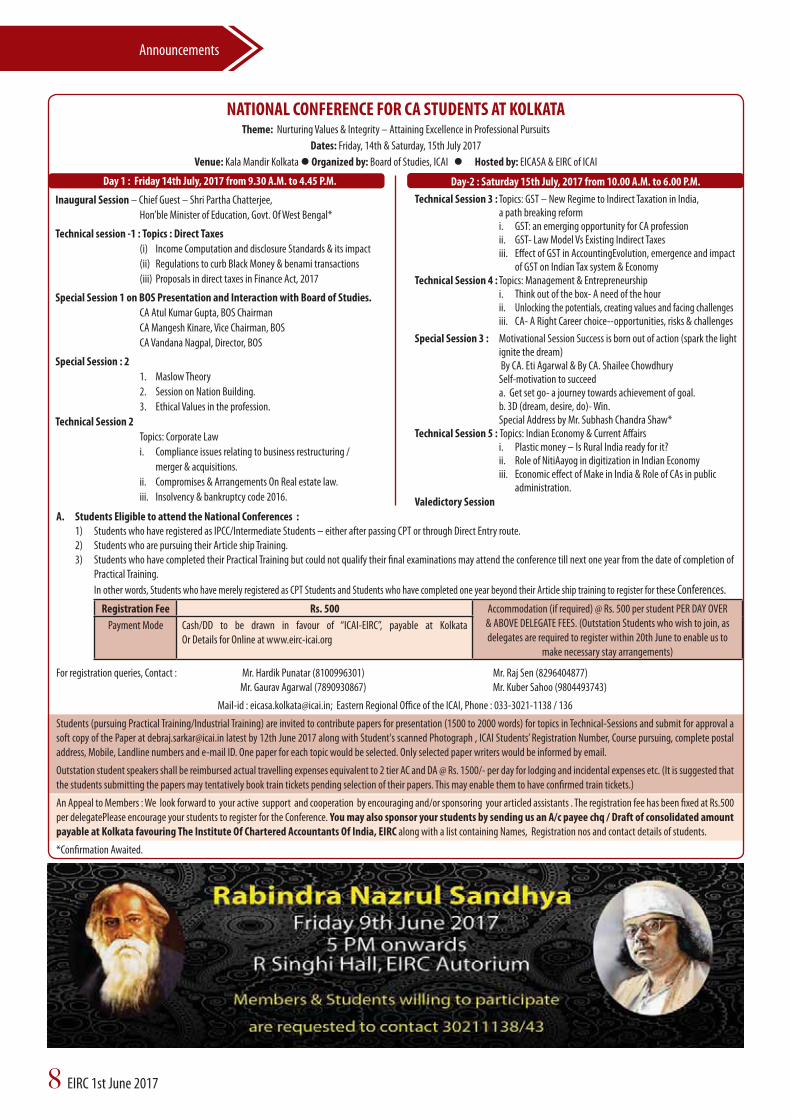

Announcements

NATIONAL CONFERENCE FOR CA STUDENTS AT KOLKATATheme: Nurturing Values & Integrity – Attaining Excellence in Professional Pursuits

Dates: Friday, 14th & Saturday, 15th July 2017

Venue: Kala Mandir Kolkata � Organized by: Board of Studies, ICAI ��Hosted by: EICASA & EIRC of ICAI

A. Students Eligible to attend the National Conferences : 1) Students who have registered as IPCC/Intermediate Students – either after passing CPT or through Direct Entry route. 2) Students who are pursuing their Article ship Training.3) Students who have completed their Practical Training but could not qualify their final examinations may attend the conference till next one year from the date of completion of

Practical Training.

In other words, Students who have merely registered as CPT Students and Students who have completed one year beyond their Article ship training to register for these Conferences.

Registration Fee Rs. 500 Accommodation (if required) @ Rs. 500 per student PER DAY OVER & ABOVE DELEGATE FEES. (Outstation Students who wish to join, as delegates are required to register within 20th June to enable us to

make necessary stay arrangements)

Payment Mode Cash/DD to be drawn in favour of “ICAI-EIRC”, payable at Kolkata Or Details for Online at www.eirc-icai.org

For registration queries, Contact : Mr. Hardik Punatar (8100996301) Mr. Raj Sen (8296404877) Mr. Gaurav Agarwal (7890930867) Mr. Kuber Sahoo (9804493743)

Mail-id : [email protected]; Eastern Regional Office of the ICAI, Phone : 033-3021-1138 / 136

Students (pursuing Practical Training/Industrial Training) are invited to contribute papers for presentation (1500 to 2000 words) for topics in Technical-Sessions and submit for approval a

soft copy of the Paper at [email protected] latest by 12th June 2017 along with Student's scanned Photograph , ICAI Students’ Registration Number, Course pursuing, complete postal address, Mobile, Landline numbers and e-mail ID. One paper for each topic would be selected. Only selected paper writers would be informed by email.

Outstation student speakers shall be reimbursed actual travelling expenses equivalent to 2 tier AC and DA @ Rs. 1500/- per day for lodging and incidental expenses etc. (It is suggested that

the students submitting the papers may tentatively book train tickets pending selection of their papers. This may enable them to have confirmed train tickets.)

An Appeal to Members : We look forward to your active support and cooperation by encouraging and/or sponsoring your articled assistants . The registration fee has been fixed at Rs.500 per delegatePlease encourage your students to register for the Conference. You may also sponsor your students by sending us an A/c payee chq / Draft of consolidated amount payable at Kolkata favouring The Institute Of Chartered Accountants Of India, EIRC along with a list containing Names, Registration nos and contact details of students.

*Confirmation Awaited.

Day 1 : Friday 14th July, 2017 from 9.30 A.M. to 4.45 P.M.

Inaugural Session – Chief Guest – Shri Partha Chatterjee,

Hon’ble Minister of Education, Govt. Of West Bengal*

Technical session -1 : Topics : Direct Taxes

(i) Income Computation and disclosure Standards & its impact

(ii) Regulations to curb Black Money & benami transactions

(iii) Proposals in direct taxes in Finance Act, 2017

Special Session 1 on BOS Presentation and Interaction with Board of Studies.

CA Atul Kumar Gupta, BOS Chairman

CA Mangesh Kinare, Vice Chairman, BOS

CA Vandana Nagpal, Director, BOS

Special Session : 2

1. Maslow Theory

2. Session on Nation Building.

3. Ethical Values in the profession.

Technical Session 2

Topics: Corporate Law

i. Compliance issues relating to business restructuring /

merger & acquisitions.

ii. Compromises & Arrangements On Real estate law.

iii. Insolvency & bankruptcy code 2016.

Day-2 : Saturday 15th July, 2017 from 10.00 A.M. to 6.00 P.M.

Technical Session 3 : Topics: GST – New Regime to Indirect Taxation in India, a path breaking reform i. GST: an emerging opportunity for CA profession ii. GST- Law Model Vs Existing Indirect Taxes iii. Effect of GST in AccountingEvolution, emergence and impact of GST on Indian Tax system & EconomyTechnical Session 4 : Topics: Management & Entrepreneurship i. Think out of the box- A need of the hour ii. Unlocking the potentials, creating values and facing challenges iii. CA- A Right Career choice--opportunities, risks & challenges

Special Session 3 : Motivational Session Success is born out of action (spark the light ignite the dream) By CA. Eti Agarwal & By CA. Shailee Chowdhury Self-motivation to succeed a. Get set go- a journey towards achievement of goal. b. 3D (dream, desire, do)- Win. Special Address by Mr. Subhash Chandra Shaw*Technical Session 5 : Topics: Indian Economy & Current Affairs i. Plastic money – Is Rural India ready for it? ii. Role of NitiAayog in digitization in Indian Economy

iii. Economic effect of Make in India & Role of CAs in public administration.

Valedictory Session

EIRC 1st June 2017 �

Compiled and Edited By CA. Raginee GoyalEmail: [email protected]

A. CENTRAL EXCISE

1. Seeks to amend notification no. 12/2012-Central Excise dated 17.03.2012 extending the time period for furnishing the final Mega power project certificate from 60 months to 120 months and extending the period of validity of security in the form of Fixed Deposit Receipt or Bank Guarantee from 66 months to 126 months, in case of provisional mega power projects. (Notification No. 08/2017- Central Excise, Dated 16-05-2017)

2. Notification under Section 11C of the Central Excise Act on Heena Powder and Paste falling under Chapter 33. (Notification No 11/2017- Central Excise NT Dated 24-04-2017)

B. SERVICE TAX

1. Extension of the date of submission of the Form ST-3 for the period 1st October 2016 to 31st March 2017 from 25th April 2017 to 30th April 2017. (Order No. 01/2017-Service Tax Dated 25-04-2017 corrigendum Dated 27.04.2017)

2. Seeks to amend notification No. 25/2012-ST dated 20.06.2012 so as to exempt life insurance services under ‘Pradhan Mantri Vaya Vandana Yojana’. (Notification No 17/2017-Service Tax Dated 04-05-2017)

HELD: The undisputed facts are that during the material period, the appellant

was the rightful owner of ‘IDEAL’ brand for applying it on its product “plastic

storage tanks”. In terms of the Circular issued by the Board dated 30-12-88

(supra), SSI exemption cannot be denied to an assessee on the sole ground that

a brand name as used on the products of the assessee is also used by another

assessee on a different category of goods. The Department has no case that

above Circular issued by the Board has since been modified or withdrawn. The

admissibility of SSI exemption in the circumstance of two manufacturers of

different goods using the same brand has been laid down by the Apex Court, as

pointed out by the ld. Counsel for the appellants.

In the “Megharaj Biscuits” case (supra) relied on by the Commissioner in support

of his decision, two manufacturers had used the same brand name on the same

specified goods. One of the manufacturers was allotted the ownership of the

brand name with retrospective effect. Apex Court held that the assessee who

was allotted the brand name long after it applied for the same could not enjoy

the benefit of the brand as an SSI retrospectively. In the circumstances, the

impugned order is based on an incorrect interpretation of the provisions and

that the same is not sustainable.

3. 2012 (283) E.L.T. 92 (Tri. - Chennai) - RITZBURY INDIA (P) LTD. Versus

COMMISSIONER OF CENTRAL EXCISE, CHENNAI:

SSI Exemption - Brand name - Owned by foreign holding companies -

Assigned exclusive right of using thereof to assessee-Indian subsidiary

company, who had applied for its registration after Department

started its enquiries - HELD : In view of assignment, assessee was

entitled to use brand name, and benefit of SSI exemption.

HELD: There are two streams of precedent decisions which are applicable to a

case of this kind. In the case of CCE, Mumbai v. Capital Controls (I) Pvt. Ltd. -

2008 (232) E.L.T. 357, it was held by the Tribunal that in the case of assignment

of brand name by a foreign collaborator, the right to use brand name is

different from ownership and mere right to use by the assignment does not

confer ownership and accordingly small scale exemption is not available. In the

case of CCE, Jaipur v. Dugar Tetenal India Ltd. - 2008 (224) E.L.T. 180 (S.C.), the

Hon’ble Supreme Court held that small scale exemption was not available when

the brand name “Tetenal” belonging to the foreign collaborator was used. In

Meghraj Biscuits (supra) and in Meyer Health Care (supra), the Hon’ble Supreme

Court held that retrospective date of registration as applicable under trade mark

law cannot be extended to excise law for the purpose of small scale exemption

and the assessee was not entitled to take benefit of an assignment deed for the

said purpose.

However, in the case of CCE, Goa v. Primella Sanitary Products - 2005 (184)

E.L.T. 125 (S.C.), the Hon’ble Supreme Court upheld the order of the Tribunal

that in view of the assignment, the assessee in that case was entitled to use the

mark “Comfit always” and that as long as the assignment stood the assessee

was entitled to the benefit of small scale exemption. In the case of Convertech

Equipment (supra), the Hon’ble Supreme Court has also upheld the decision of

the Tribunal that affixation of a brand name of a foreign company otherwise

registered in the name of the Indian company would not be a bar to availing

small scale exemption.

The Hon’ble Supreme Court’s decisions in the cases of Primella Sanitary

Products (supra) and Convertech Equipment (supra) have been rendered by

the Benches comprising of three Hon’ble Judges. Hence, following the ratio

of these decisions, the appellant-assessee herein is entitled to the small scale

exemption. Hence, we set aside the impugned Order-in-Appeal and restore

the Order-in-Original. Consequently, the assessee’s appeal is allowed and the

Department’s appeal for enhancement of penalty is dismissed.

RECENT JUDICIAL PRONOUNCEMENT - INDIRECT TAXES

NOTIFICATIONS & CIRCULAR ON CENTRAL EXCISE & SERVICE TAX

INDIRECT TAX

Compiled and Edited By: CA. Raginee Goyal

Email: [email protected]

1. 2016 (338) E.L.T. 134 (Tri. - Chennai) - ELAC MARKETING PVT. LTD. Versus

COMMISSIONER OF C. EX., CHENNAI-II:

SSI Exemption - Brandname - Similar and akin brandnames of two

manufacturers - Exemption sought to be denied on ground that

assessee manufacturing water heater bearing brandnamesimilar and

akin to another manufacturer. When it is clear that brand name not of

another person, assessee entitled to SSI exemption.

HELD : Water heater made of plastic body cleared by assessee under brandname

“Elac Excel” not same as water heater made of stainless steel body cleared by

another manufacturer under brandname “Elac”, notwithstanding that both

are similar and akin - Assessee had applied for and obtained registration of

brandname “Elac Excel” - Notification apply only to goods bearing brandname

or trade name of another person - Assessee not using brandname of another

but its own brandname - Assessee’s name itself having word “Elac” and could

not be disentitled to use it - Assessee and other manufacturer independent and

their brandnames distinctly different - “Elac Excel” not a brandname or trade

name of any other person and not hit by Para (4) of notification - Assessee

entitled to exemption - Demand of duty and penalty set aside

2. 2009 (233) E.L.T. 379 (Tri. - Chennai) - IDEAL INDUSTRIES

VersusCOMMISSIONER OF C. EX., COIMBATORE :

SSI Exemption - Brandname - Use of samebrandname by two

manufacturers of different goods - Appellant rightful owner of ‘IDEAL’

brand for applying it on its product plastic storage tanks, not disputed

- SSI exemption available in terms of C.B.E & C Circular No. 88/88-CX.6,

dated 30-12-1988 and Department has no case that such Circular, since

been modified or withdrawn - Moreover, Apex Court decision in case

of Rukmani Pakkwell Traders [2004 (165) E.L.T. 481 (S.C.)] applicable -

Impugned order denying SSI exemption set aside

Notifications & CircularsIndirect Taxes

���EIRC 1st June 2017

Notifications & CircularsIndirect Taxes

Compiled by CA MOHIT BHUTERIA

Email : [email protected]

COMPANY LAW

1. SPC & Associates vs. DVAK & Co. and NISC Export Services Private Limited

(2017 (4) TMI 674)

The Petitioner had filed a petition for its reinstatement as an auditoron the ground that

non-ratification of its appointment / removal by NISC Export Services Private Limited

(Respondent 2) was done without passing a special resolution and seeking approval

of the Central Government as per provisions of section 140 of Companies Act, 2013.

Also, the Petitioner was not provided with reasonable opportunity of being heard.

The Petitioner alleged that the reason for the subsequent appointment of DVAK &

Co. (Respondent 1) as the auditor of Respondent 2 was because the Petitioner had

requested for a hike by 10% of its current audit fee, which was supposedly contrary

to the terms of appointment of the Petitioner as per a formal communication by

Respondent 2. It is worthy to mention that DVAK & Co. was a newly formed audit firm

whose partners had formerlybeen partners of the Petitioner with one such partner

having also been a signing partner of the financial statements of Respondent 2.

Held: The NCLT held that a 10% increase in audit fee is reasonable and cannot be a

justifiable ground for non-ratification of appointment of auditor. If such an increase

was not acceptable, then any subsequent auditor can also not be guaranteed of

continuing for the entire tenure of 5 years.The NCLT clearly stated that frequent change

of auditor is not advisable for effective auditing, preparation of financial statement,

transparency in audit policies / procedures.The NCLT also observed that Respondent 2

had not substantiated its claim that the request for increase in audit fee was contrary

to the terms of appointment of Petitioner. Further, where an auditor is proposed to

be removed / his appointment is not ratified, such an auditor has to be provided with

sufficient opportunity seeking their comments in the light of Natural Justice.Lastly,

NCLT also held that DVAK & Co. was ineligible to be appointed as auditor of Respondent

2 as per Explanation II(b) to Rule 6 to the Companies (Audit and Auditors) Rules, 2014.

2. Nirmal Overseas Limited, In re. (Order of New Delhi Bench of NCLT dated May

8, 2017)

The Petition was filed praying for permission to rectify the Register of Members

which had been damaged extensively by termites and had to be reconstructed. Some

defects were also noted in respect of the number of shares held and/or names of the

shareholders, distinctive numbers, multiple certificates with the same name after the

original certificate was split. The Petitioner sought to rectify all these defects.

Held: The NCLT stated that the petition was filed under section 59 of the Act, 2013,

which granted relied to an aggrieved person by directing the company to make

suitable amendments to the Register of Members. In this case since the anomalies

were discovered by the Petitioner, it is well within the right of the Petitioner to make

suitable corrections or to reconstruct its Register of Members without any directions

from NCLT. Since the Register of Members is maintained by the Company as per

statutory obligations, no prior permission is needed to prepare them.

3. Reebok India Co., In re ([2017] 137 CLA 279 (NCLT))

The NCLT held that prayers for compounding in cases where defaults are incurable

and cannot be rectified cannot be permitted since these were not due to any bonafide

omission or a delayed rectification of a statutory requirement. Compounding of such

offences would demolish and prejudice the prosecution under penal provisions.

The offences in this case were under Companies Act and Penal Code, which were

intrinsically linked. Hence, compounding of offences under Companies Act would

hamper the criminal prosecutions and no accused should be allowed to get away with

deliberate large scale bungling and fabrication of documents carried out with criminal

intention.

4. Diana Buildwell Limited, In re ([2017] 137 CLA 303 (NCLT))

The NCLT allowed the conversion of the Petitioner company from a public limited

company to a private limited company on the grounds that it had complied with all the

provisions of the Companies Act, 2013. The NCLT also stated that the conversion was

in the interest of the Petitioner with a view to comply efficiently with the provisions

of the Companies Act, 2013 causing no prejudice either to the members or to the

creditors of the Petitioner company.

JUDICIAL PRONOUNCEMENTS ON COMPANY LAW 5. M/s Repro India Ltd, In re (Order of Mumbai Bench of NCLT dated

May 6, 2017)

The NCLT compoundeda violation of section 217(4) of Companies Act, 1956 after

payment of compounding fee of Rs. 60,000. Under the erstwhile Act, section 217(4)

required the Chairman to sign the Board’s Report if authorised by the Board and where

he is not so authorised, the Board’s Report hadd to be signed in the same manner

as financial statements. In this case, although the Chairman had chaired the board

meeting in which the Directors’ Reports were approved, the Board had authorised the

managing director to sign the Director’s Report instead of the Chairman in violation of

section 217(4).

6. M/s Repro India Ltd, In re (Order of Mumbai Bench of NCLT dated

May 6, 2017)

The NCLT compoundeda violation of section 224(8) of Companies Act, 1956 on

payment of compounding fee of Rs. 10,00,000/- in total by the managing director,

four directors and company secretary. The violation pertained to failure to fix the

remuneration of auditors by the board of directors even after authorisation by the

shareholders. This was despite the fact that the auditors’ fee was raised every year

during the period under consideration and the board minutes during this period did

not bear any resolution passed by the board for fixing and authorising payment of

auditors’ fees.

RECENT CASE LAW - INCOME TAX

Compiled by CA RAJ SINGHANIA

Email : [email protected].

Recent Case laws ( Income Tax):

DIT vs. Rolls Royce Industrial Power India Ltd (Delhi High Court)

S. 147/148 reassessment has to be based on “fresh material”. A reopening based on reappraisal of existing material is invalid. The assessee’s duty is only to disclose facts and not to make inferences. Consolidated Photo 281 ITR 394 (Del) is not good law.

Ameeta Mehra vs. ADIT (Delhi High Court)

S. 132/153A: Important law explained on the preconditions necessary for the department to initiate valid search and seizure action u/s 132 and whether the assessee is entitled to challenge the same. Consequences of the search being declared void on the s. 153A assessment also explained

Pr CIT vs. Meetu Gutgutia (Delhi High Court)

S. 153A: Entire law explained on whether concluded assessments can be reopened u/s 153A even in the absence of incriminating material found during the search in the light of the apparently conflicting verdicts in CIT vs. Kabul Chawla 380 ITR 573 (Del) and Dayawanti Gupta v. CIT 390 ITR 496 (Del)

Balgopal Trust vs. ACIT (ITAT Mumbai)

S. 54F: U/s 161, a trust which is for the sole benefit of an individual, has to be assessed as an “individual” and not as an “AOP”. Consequently, a trust is eligible for s. 54F deduction

CIT vs. Krishan K. Aggarwal (Supreme Court)

Supreme Court issues strictures against the income-tax department stating that it is “extremely unhappy” with the delay of 3381 days in refiling the SLP and demands that “The concerned authorities need to wake up”

Raj Dadarkar & Associates vs. ACIT (Supreme Court)

Law on tests to be applied to determine whether income from property is chargeable as “Income from house property” or as “Profits and gains of business” explained. The objects clause is not determinative. Income earned from a shopping center is required to be taxed under the head “Income from House Property” (Chennai Properties 373 ITR 673 (SC) and Rayala Corporation distinguished)

State Of Jharkhand vs. Lalu Prasad Yadav (Supreme Court)

Severe strictures passed against the High Court for “inconsistent decision-making” and passing orders which are “palpably illegal, faulty and contrary to the basic principles of law” and by ignoring “large number of binding decisions of the Supreme Court” and giving “impermissible benefit to accused”. Law on condonation of delay explained. CBI directed to implement mechanism to ensure that all appeals are filed in time

CIT vs. M/s Carpet Mahal (Rajasthan High Court)

Bogus purchases: In view of the Supreme Court’s order in Vijay Proteins Ltd vs. CIT whereby the verdicts of the Gujarat High Court in Sanjay Oilcake Industries vs. CIT 316 ITR 274 (Guj) and N.K. Industries Ltd vs. Dy. CIT were confirmed, the AO has to accept the law and verify whether the transaction is genuine or not on the basis of the aforesaid three judgments

EIRC 1st June 2017 ��

Notifications Income Tax

CIT vs. Laxman Industrial Resources Pvt.Ltd (Delhi High Court)

Bogus share capital: Fact that the investigation wing’s report alleged that the assessee was beneficiary to bogus transactions and that the identity of shareholders, genuineness etc was suspect is not sufficient. The AO is bound to conduct scrutiny of documents produced by the assessee and cannot rest content by placing reliance on the report of the investigation wing

CIT vs. Pashupati Nath Agro Food Products Pvt. Ltd (Allahabad High Court)

S. 145: If the AO has not rejected the books of account, it means that the assessee has maintained the books of accounts in accordance with the prescribed standards as per s. 145 of the Act. If so, the AO is not entitled to make any addition on account of sale of goods out of

books or for investment in stock out of undisclosed sources.

Director of Income-tax specified in column (4) of the Schedule to issue orders in writing for

the exercise of the concurrent powers and performs the functions of an Assessing Officer to

an Assistant Director of Income-tax or Deputy Director of Income-tax who are subordinate to

them, in respect of cases or class of cases falling within the territorial areas specified in column

(6) of the Schedule for the purpose of the said Act.

[Notification No. 40/2017/F. No.173/429/2016-ITA-I ]

S.O. 1621(E).—In exercise of the powers conferred under sub-section (2) of section 28 read

with section 59 of the Prohibition of Benami Property Transactions Act, 1988 (45 of 1988),

and in supersession of the Ministry of Finance, Department of Revenue, Central Board of

Direct Taxes, notification number S.O. 3290(E), dated the 25th October, 2016, published in

the Gazette of India, Extraordinary, Part-II, Section 3, Sub-section (ii), dated the 25th October,

2016, except as respects things done or omitted to be done before such supersession, the

Central Government hereby directs that the Income-tax authorities under section 116 of

the Income-tax Act, 1961 (43 of 1961) specified in column (2) of the Schedule, having

headquarters at the places specified in the corresponding entry in column (3), to exercise the

powers and perform the functions of the ‘Authority’ under the Prohibition of Benami Property

Transactions Act, 45 of 1988 specified in the corresponding entries in column (4) in respect

of the territorial areas specified in the corresponding entries in column (5) of the Schedule

[Notification No. 05/2017/F. No. DGll(S)/CPC(TDS/2017-18 ]

Subject: - lOS and filing of ITR in case both the parents are dead of minor - reg.-

It has been brought to the notice of CBDT that in cases of minors whose both the parents

have deceased, lOS deductors/Banks are clubbing the interest income accrued to the minor

in the hand of grandparents and issuing lOS certificates to the grandparents, which is not in

accordance with the law as the Income-tax Act envisages clubbing of minor’s income with

that of the parents only and not any other relative. Ideally in such type of situations, the

income should be assessed in the hands of the minor and the income-tax returns be filed by

the minor through his/ her guardian.

CIRCULAR No. 18 /2017( F. No. 385/01l2015-IT (B))

Subject: Requirement of tax deduction at source in case of entities whose income is exempted

under Section 10 of the Income-tax Act, 1961 - Exemption thereof.

The Central Board of Direct Taxes (the Board) had earlier issued Circular No. 4/2002 dated

16.07.2002 and Circular No. 7/2015 dated 23 .04.2015 which laid down that in case of such

entities, whose income is unconditionally exempt under Section 10 of the Income-tax Act

(the Act) and who are also statutorily not required to file return of income as per Section

139 of the Act, there would be no requirement for tax deduction at source (TDS) from the

payments made to them since their income is anyway exempted from tax under the Act. The

issue of whether exemption from TDS can be extended to more entities on these principles

and whether the exemption is needed to be withdrawn in respect of some of the exempted

entities was examined by the Board.

Examination of the eligibility of entities for exemption from TDS on the principle of

unconditional exemption and no requirement to file return revealed that Circulars No. 4/2002

both the above mentioned conditions but are not mentioned in the aforesaid Circulars need

4/2002 but their exemption from income tax has since been withdrawn need to be removed

because of subsequent amendment they are now required to mandatorily file their returns of

income U/S 139 need to be removed from the list of exempted entities.

In view of the above, a revised list of entities exempted from TDS has been drawn by adding

entities in the first category listed above to the entities mentioned in Circular No. 4/2002

and Circular No. 7/2015 and removing entities in second and third categories from the list of

existing entities eligible for exemption from TDS.

Accordingly, it has been decided that in case of certain mentioned funds or authorities or

Boards or bodies, by whatever name called, referred to in section 10 of the Income-tax Act,

whose income is unconditionally exempt under that section and who are also statutorily not

required to file return of income as per section 139 of the Income-tax Act, there would be no

0.385/01120 I 5-lTfB) Circular No. 18/2017 -2- requirement for tax deduction at source, since

their income is anyway exempt under the Income-tax Act.

CIRCULARS- INCOME TAX

[Notification No. 33/2017/F.No. 196/15/2015-ITA-I]

S.O. 1361(E).—In exercise of the powers conferred by clause (46) of section 10 of the Income-

tax Act, 1961 (43 of 1961) the Central Government hereby notifies for the purposes of the said

clause, the National Skill Development Agency, a body constituted by the Central Government

in respect of the following specified income arising to that body, as follows:- i) grant-in-aid

from Government of India; and ii) interest earned on grant-in-aid from Government of India.

2. This notification shall be effective subject to the conditions that National Skill Development

Agency, - (a) shall not engage in any commercial activity; (b) activities and the nature of the

specified income remain unchanged throughout the financial years; and (c) shall file returns

of income in accordance with the provision of clause (g) of sub-section (4C) section 139 of the

Income-tax Act, 1961. 3. This notification shall deemed to have been applied for the financial

years 2014-2015, 2015-2016, 2016-2017 and shall be applicable for the financial years 2017-

2018 and 2018-2019

[Notification No. 36/2017/F.No. 370142/7/2017-TPL]

S.O. 1381(E).—In exercise of the powers conferred by section 295 read with section 115BA

of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes

the following rules further to amend the Income-tax Rules, 1962, namely: - 1. (1) These

rules may be called the Income-tax (9th Amendment) Rules, 2017. (2) They shall come

into force on the date of their publication in the Official Gazette. 2. In the Income-tax Rules,

1962 (hereafter referred to as the principal rules), after rule 21AC, the following rule shall be

inserted, namely:- “21AD. Exercise of option under sub-section (4) of section 115BA. (1) The

option to be exercised in accordance with the provisions of sub-section (4) of section 115BA

by a person, being a domestic company, for any previous year relevant to the assessment year

beginning on or after the 1st day of April, 2017, shall be in Form No. 10-IB. (2) The option in

Form No. 10-IB referred to in sub-rule (1) shall be furnished electronically either under digital

signature or electronic verification code.

(3) The Principal Director General of Income-tax (Systems) or the Director General of Income-

tax (Systems), as the case may be, shall- (i) specify the procedure for filing of Form referred

to in sub-rule (2); (ii) specify the data structure, standards and manner of generation of

electronic verification code, referred to in sub-rule(2), for purpose of verification of the person

furnishing the form referred to in the said sub- rule; and (iii) be responsible for formulating

and implementing appropriate security, archival and retrieval policies in relation to Form so

furnished.”; 3. In the principal rules, after Form No. 10-IA, Form 10-IB shall be inserted.

[Notification No. 37/2017, F. No. 370133/6/2017-TPL]

S.O. 1513 (E).—In exercise of the powers conferred by sub-section (3) of section 139AA

of the Income-tax Act, 1961 (43 of 1961), the Central Government hereby notifies that

the provisions of section 139AA shall not apply to an individual who does not possess the

Aadhaar number or the Enrolment ID and is:- (i) residing in the States of Assam, Jammu and

Kashmir and Meghalaya; (ii) a non-resident as per the Income-tax Act, 1961; (iii) of the age

of eighty years or more at any time during the previous year; (iv) not a citizen of India. 2. This

notification shall come into force with effect from the 1st day of July, 2017.

[Notification No. 39/2017/F. No. 187/13/2015-ITA-I]

S.O. 1590(E).—In exercise of the powers conferred by sub sections (1) and (2) of section 120

of the Income-tax Act, 1961 (43 of 1961), read with section 6 of the Black Money (Undisclosed

Foreign Income and Assets) and Imposition of Tax Act, 2015 (22 of 2015) (hereinafter referred

to as ‘the Act’), the Central Board of Direct Taxes hereby authorises the Director General of

Income-tax specified in column (2) of Schedule annexed hereto, or the Principal Director or

���EIRC 1st June 2017

EIRC Events

Workshop on GST from 4th to 6th May 2017

CA Rohit Surana

CA Ravi Kumar Patwa

CA Abhishek Tibrewal

CA K KChhaparia

CA Pramod Dayal Rungta, Past Chairman, EIRC

CA Rajeev Agarwal L – R: CA Abhishek Agarwal, CA Aditya Maheshwari

L – R: CA Vivek Agarwal, CA Nitesh Kumar More, CA Krishanu Bhattacharyya, Past Chairman, EIRC

L – R: CA Subham Khaitan, CA Manish Goyal, Chairman, EIRC, CA Sonu Jain, Vice Chairperson, EIRC

L – R: CA Sandeep More, CA Manish Goyal, Chairman, EIRC, Mr. Sanjeev Zarbade, VP, Kotak Securities, CA Sonu Jain, Vice Chairperson, EIRC

L – R: CA Mohit Bhuteria, Mrs. Monisha Chakraborty, GM, RBI, CA Nitesh Kumar More, Member, EIRC, Mr. Amitava Ghosh, AGM, RBI, Mrs. Subha Modi, AGM, RBI

CA Manish Goyal, Chairman, EIRC, CA Nitesh Kumar More, Member, EIRC along with Mr. Priyabrata Pramanik, Addl. Director, IT along with others

(L to R): CA. Raja Narayan Tripathy, Vice Chairman & Chairman, EICASA, Bhubaneswar, CA. R.R Modi, Kolkata, CA. Rashmi Ranjan Mishra, Chairman, Bhubaneswar Branch, CA. Ranjeet Kumar Agarwal, Central Council member, ICAI and CA. Vishnu Dutt, New Delhi.

Awareness Programme on IND AS on 15th May 2017

Analysis of Filing Requirement of SFTs by Assesses liable to Tax Audit on 22nd May 2017

Workshop on Insolvency and Bankruptcy Code, 2016 by Bhubaneswar Branch of EIRC

Investor awareness Programme – “Lets Talk Market”on 19th May 2017

Role of Auditors of NBFC’s and Expectation of Regulators on 26th May 2017

Breakfast Meeting on GST for Industry & Women Members on 12th May 2017

Demystifying LLP Conversion on 9th May

2017

Seminar on Benami Transaction on 10th

May 2017

EIRC 1st June 2017 ��

EIRC Events

Seminar on Insolvency and Bankruptcy Law Summit on 13th May 2017

L – R: CA Manish Goyal, Chairman, EIRC, CA Sonu Jain, Vice Chairperson, EIRC, CA Ranjeet Kumar Agarwal, Council Member, ICAI, Advocate Nalin Kohli, Lawyer, Supreme Court of India, CA (Dr.) Debashis Mitra, Council Member, ICAI, CA Sushil Kumar Goyal, Council Member, ICAI

CA Jayesh Gupta

Smt. Smaraki Mohapatra, Commissioner, Commercial Taxes, Govt. of WB

L - R: Ms. Manorama Kumari, Member Judicial, NCLT, Mr. A N Dhar, General Manager, SBI, CA Sumit Binani, Secretary, EIRC, CA Manish Goyal, Chairman, EIRC, CA Arun Kumar Jagatramka, CMD, Gujrat NRE Coke Ltd., CA Subodh Kumar Agrawal, Past President, ICAI

Advocate Nalin Kohli, Lawyer, Supreme Court of India

CA Arun Agarwal

CA G Sekhar, Council Member, ICAI CA Kapil Goel CA Nihar N Jambusaria, Council Member, ICAI

CA Ramesh Patodia CA S S Gupta Mr Dharam Vir, Income Tax Official

Mr. Khalid Aizaz Anwar, Sr. Jt. Commissioner, Dept. of Commercial Taxes, Govt. of WB

CA Puneet AgarwalL – R: CA Manish Goyal, Chairman, EIRC, CA Sonu Jain, Vice Chairperson, EIRC, CA Sushil Kumar Goyal, Vice Chairman, IDTC, ICAI, CA Puneet Agarwal, CA Sumit Binani,

L – R: Smt. Smaraki Mohapatra, Commissioner, Dept. of Commercial Taxes, Govt. of WB, CA Arun Agarwal, CA Manish Goyal, Chairman, EIRC, Mr. Khalid Aizaz Anwar, Dy. Commissioner, Dept. of Commercial Taxes, Govt. of WB, Mr. Narayan Gurian, Sr. Dept. of Commercial Taxes, Govt. of WB

GST Conclave II on 20th May 2017

Outreach Programme on GST on 26th May 2017

Seminar on Direct Taxes on 27th May 2017

���EIRC 1st June 2017

EIRC Events

Durgapur Branch Seminar on GST on 7th May 2017

Durgapur Branch - National Talent Hunt on 28th May 2017

GUWAHATI BRANCH

Concurrent Audit- Panel Discussion

Group Photo at NAGAON CPE CHAPTER

CPE Prog at Jorhat

Seminar on GST by Jorhat CPE Chapter of EIRC of ICAI on 14.05.2017

CPE Prog at Naogaon

Seminar on GST by Nagaon CPE Study Group of EIRC of ICAI on 15.05.2017

EIRC 1st June 2017 ��

ROURKELA BRANCH

SILIGURI BRANCH

TINSUKIA BRANCH

EIRC

EIRC Events

L - R CA Aishraya Agarwal, Secretary, Rourkela Branch, CA (Dr.) Debasish Mitra, CCM, ICAI, CA Yogesh Banka, Chairman, Rourkela Branch, CA Manish Goyal, Chairman, EIRC, CA Nitesh More, Member, EIRC

Certificate Course on Concurrent Audit of Banks

Refresher Course on GST

CABF Contribution on the occasion of Sub Regional Conference on 9th May 2017

Lighting the Inauguration Lamp

Programme at the Branch

L - R CA Sanjay Das, Chairman, Siliguri Branch, Shri Priyabrata Pramanik, Addl. Director, IT

Dais at the Sub Regional Conference on 9th May 2017

Lighting the Inauration Lamp

Refresher Course on GST

Seminar on Benami Transaction on 10th may 2017 (L - R) CA Sanjib Sanghi, Treasurer, EIRC, CA K K Chhaparia

Lighting of Lamp at the Sub Regional Conference on 9th May 2017

Registered RN 27144/75 Registration No. KOL RMS / 227 / 2016-18

If undelivered please return to : Eastern India Regional Council, The Institute of Chartered Accountants of India, 7, Anandilal Poddar Sarani (Russell Street), Kolkata - 700 071

BOOK POST

���

CA Manish Goyal, Editor

CA Sonu Jain, Jt. Editor

CA Sumit Binani, Member

CA Sanjib Sanghi, Member

CA Debashis Mitra, Member

CA Sushil Kr. Goyal, Member

Owner: The Institute of Chartered Accountants of India, Eastern India Regional Council Printer: Shri Alok Ray, Joint Secretary, The Institute

of Chartered Accountants of India, Publisher: Shri Alok Ray, Joint Secretary, The Institute of Chartered Accountants of India Published from : The Institute of Chartered Accountants of India, Eastern India Regional Council, 7, Anandilal Poddar Sarani, P.S.: Shakespeare Sarani,

Kolkata - 700 071 Printed from: CDC Printers Pvt. Ltd., Tangra Industrial Estate - II, (Bengal Pottery), 45, Radhanath Chowdhury Road, P.S. :Tangra

Kolkata - 700 015 Editor: CA Manish Goyal, Chairman, Eastern India Regional Council, The Institute of Chartered Accountants of India.

The Institute does not accept any responsibility for the view expressed in the contributions of advertisements published in the

newsletter. Phone: 91-33-30211140/41, Fax: 033-22272317, Website: www.eirc-icai.org, Email : [email protected]