e xploring v alue c reation through i ntangibles : managers ' decisions vs investors '...

TRANSCRIPT

EXPLORING VALUE CREATION THROUGH INTANGIBLES: MANAGERS' DECISIONS VS

INVESTORS' EXPECTATIONS

Outlines of the Problems in Corporate Governance

• Lazonick W & O'Sullivan M. (2000) Maximizing shareholder value: a new ideology forcorporate governance. Economy and Society

• Charreaux G, Desbrières Ph. (2001) Corporate Governance: Stakeholder Value Versus Shareholder Value. Journal of Management and Governance

• Porter M. & Kramer M. (2011) How to reinvent capitalism—and unleash a wave of innovation and growth. Harvard Business Review

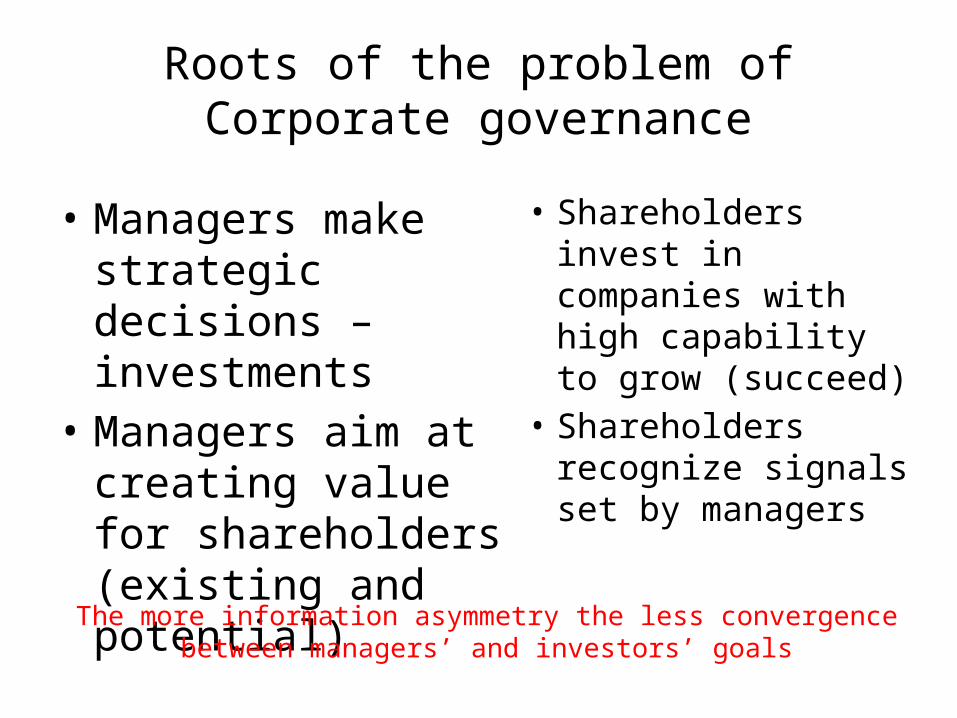

Roots of the problem of Corporate governance

• Managers make strategic decisions – investments

• Managers aim at creating value for shareholders (existing and potential)

• Shareholders invest in companies with high capability to grow (succeed)

• Shareholders recognize signals set by managers

The more information asymmetry the less convergence between managers’ and investors’ goals

Intangibles’ disclosure

• Investments associated with the intangibles are exacerbated by the traditional reporting of companies’ performance (JE Grojer, U Johanson, 1999; Orens et al.,2009 and Vergauwen et al., 2007)

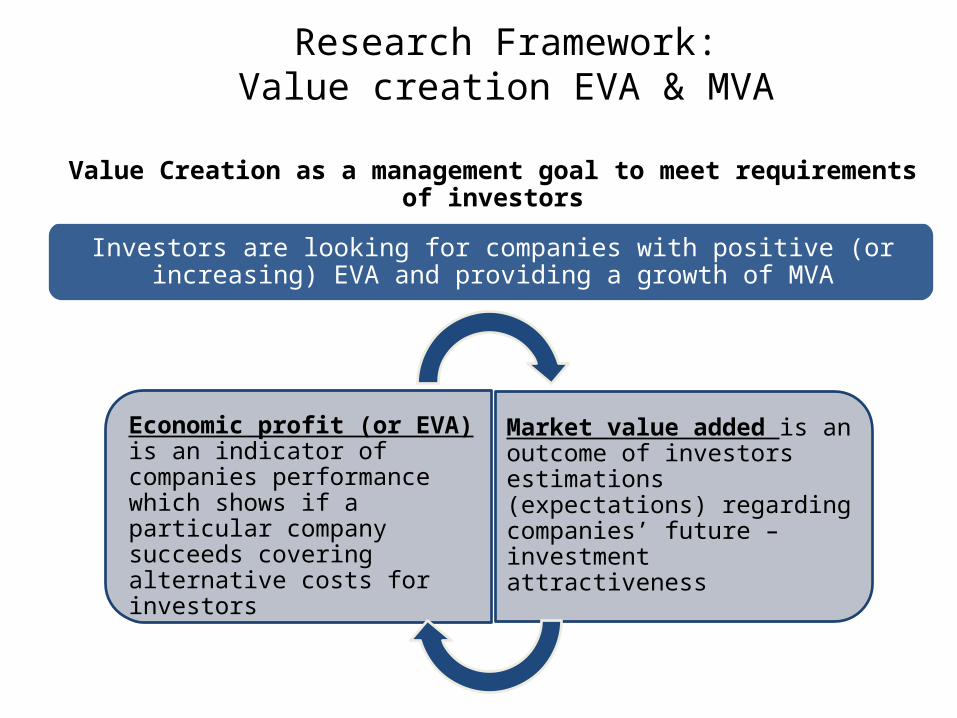

Research Framework:Value creation EVA & MVA

Economic profit (or EVA) is an indicator of companies performance which shows if a particular company succeeds covering alternative costs for investors

Market value added is an outcome of investors estimations (expectations) regarding companies’ future – investment attractiveness

Value Creation as a management goal to meet requirements of investors

Investors are looking for companies with positive (or increasing) EVA and providing a growth of MVA

Research Framework: Specifying value creation process

Investment decisions made by companies’

managers:• to invest in resources

which provide competitive advantages

• to disclose intangibles to make a company

attractive for investors

input

• Companies resources

output

• EVA

outcome

• MVA

Positive and increasing EVA

• is a goal of managers• is a signal for investors

to buy

Shows that companies value drivers were

recognized by investors

The idea of the research

• Discover intangibles’ factors that drive EVA and MVA• EVA is directly influenced by managers’

decisions; • MVA is strongly associated with the

expectations of the investors

Assuming that if managers would voluntary disclose intangibles in a proper way:

• Managers and investors goals would be aligned

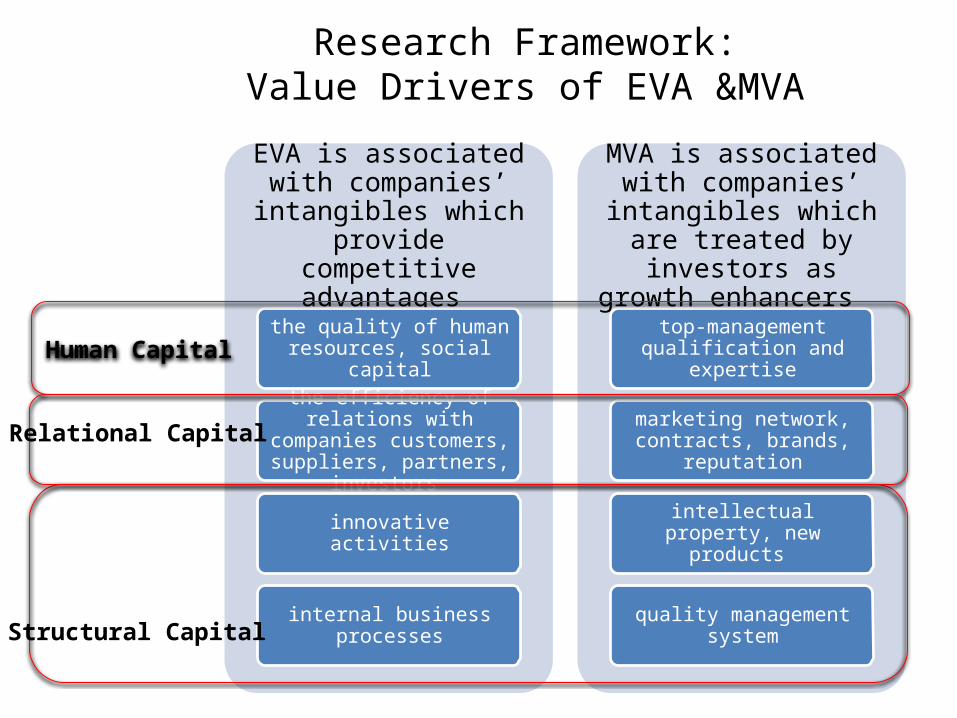

Research Framework:Value Drivers of EVA &MVA

EVA is associated with companies’ intangibles

which provide competitive advantages

the quality of human resources, social capital

the efficiency of relations with companies customers,

suppliers, partners, investors

innovative activities

internal business processes

MVA is associated with companies’ intangibles which are treated by investors as growth

enhancers

top-management qualification and expertise

marketing network, contracts, brands, reputation

intellectual property, new products

quality management system

Human Capital

Relational Capital

Structural Capital

Few empirical evidences

• On database of 5 European countries during 2004-2011

• Structural equation model

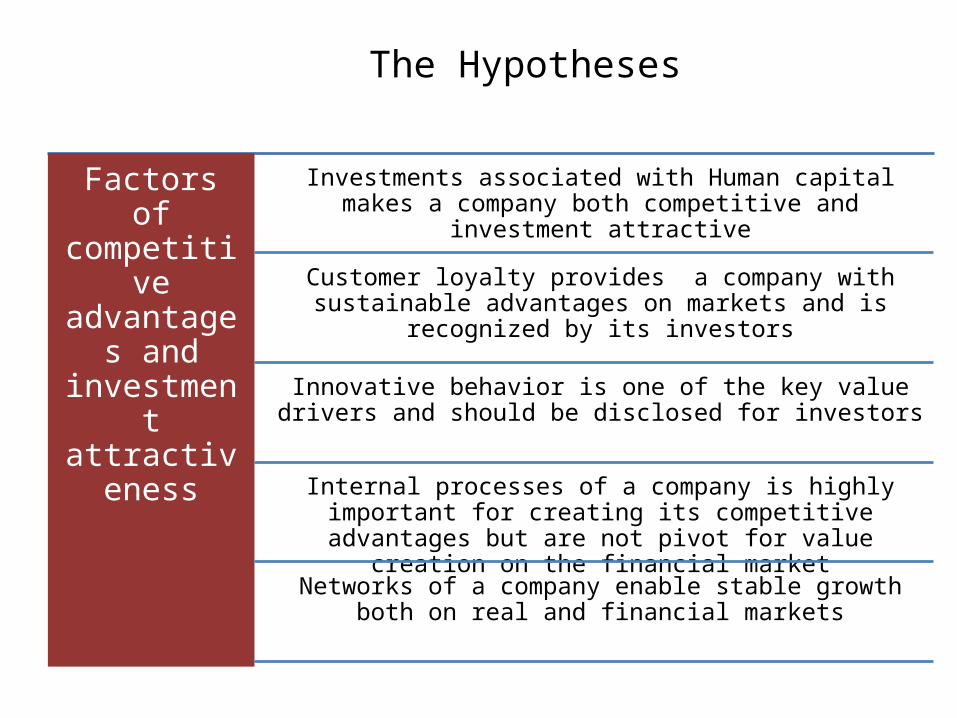

The Hypotheses

Factors of competitive advantages

and investment

attractiveness

Investments associated with Human capital makes a company both competitive and investment attractive

Customer loyalty provides a company with sustainable advantages on markets and is recognized by its investors

Innovative behavior is one of the key value drivers and should be disclosed for investors

Internal processes of a company is highly important for creating its competitive advantages but are not pivot for value creation on the

financial market

Networks of a company enable stable growth both on real and financial markets

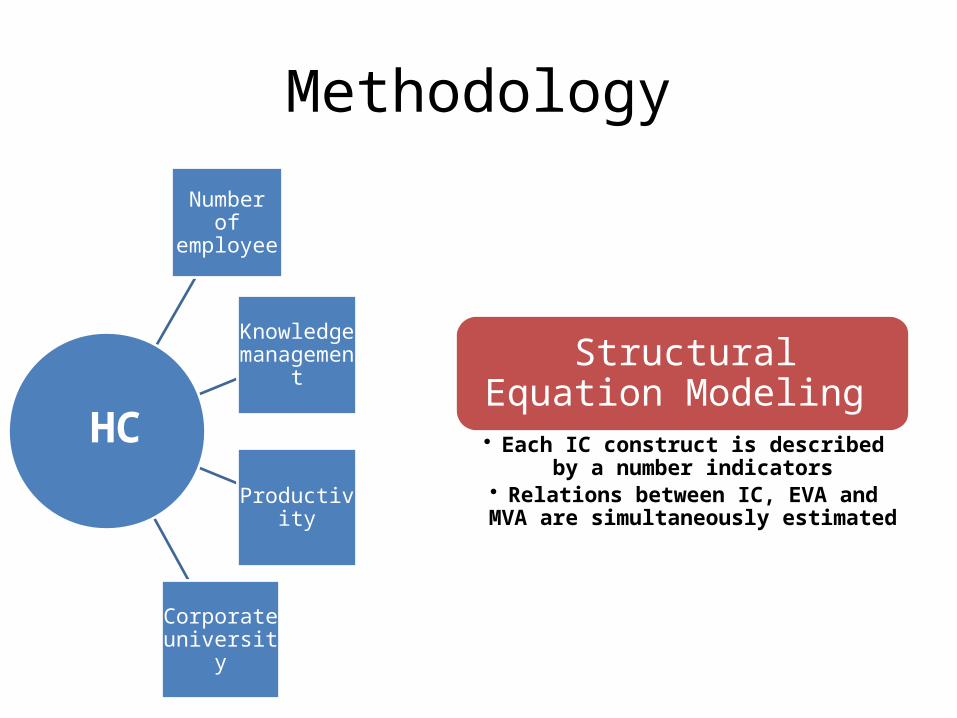

Methodology

Number of employee

Knowledge management

Productivity

Corporate university

HC

Structural Equation Modeling

• Each IC construct is described by a number indicators

• Relations between IC, EVA and MVA are simultaneously estimated

Results

Sig. positive

Sig. negative

Not sig