ൣe rating procedures. -...

TRANSCRIPT

Jana Green, CFM 2013 NJAFM Annual Conference October 17, 2013 – Concurrent Session #3

Flood Insurance Rating: Facts and Factors

THIS PRESENTATION IS INTENDED TO PROVIDE:

• A clear and high-level explanation of how National Flood Insurance Program (NFIP) flood insurance premiums are calculated

THIS PRESENTATION IS NOT INTENDED TO PROVIDE:

• Answers to Biggert-Waters 2012 (BW12) mysteries

• NFIP coverage and claim information

• Policy cancellation/nullification/endorsement information

Purpose of Presentation

2 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Information Needed to Rate a NFIP Flood Insurance Policy

• Overview of Premium Calculation

• Breakdown of Premium Calculation • Preferred Risk Policies • Pre-FIRM • Post-FIRM

• NFIP Flood Insurance Rating References

Topics of Discussion

3 | Flood Insurance Rating: Facts and Factors October 17, 2013

• A program which makes flood insurance available within participating communities

NFIP

4 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Flexibility exists within the program so flood insurance is based on workable methods of pooling risks, minimizing costs, and distributing burdens equitably among those who would be protected by flood insurance

• NFIP participating community?

• Pre-FIRM construction or post-FIRM construction?

• Detailed building description and replacement cost

• Flood zone and building elevation data; CBRS area?

• Non-Principal/Non-Primary residence? Severe Repetitive Loss (SRL) property?

• Where are the building and contents located?

• New/lapsed policy? Loss history?

• CRS discount? Other deductible chosen?

Before a Policy Can Be Rated

5 | Flood Insurance Rating: Facts and Factors October 17, 2013

6 | Flood Insurance Rating: Facts and Factors October 17, 2013

Click for Source

1. Determine rate and multiply by $100 of coverage

2. Subtract deductible discount, if applicable

3. Add Increased Cost of Compliance (ICC) premium

4. Subtract Community Rating System (CRS) discount

5. Add 5% Federal Reserve Fund Assessment

6. Add probation surcharge, if applicable

7. Add Federal Policy Fee

Premium Calculation

7 | Flood Insurance Rating: Facts and Factors October 17, 2013

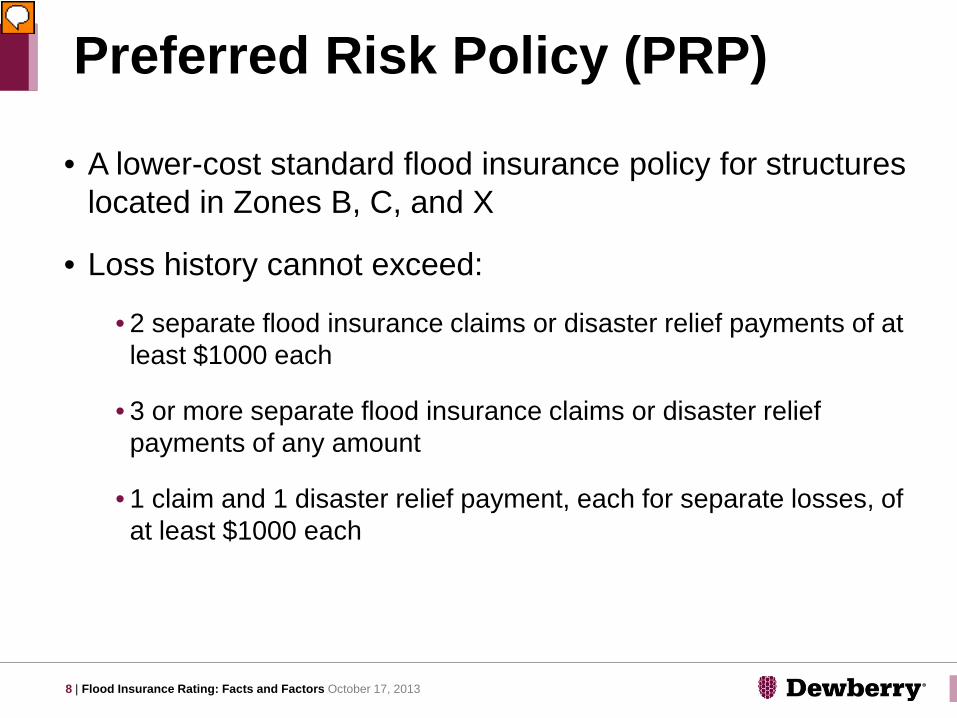

• A lower-cost standard flood insurance policy for structures located in Zones B, C, and X

• Loss history cannot exceed:

• 2 separate flood insurance claims or disaster relief payments of at least $1000 each

• 3 or more separate flood insurance claims or disaster relief payments of any amount

• 1 claim and 1 disaster relief payment, each for separate losses, of at least $1000 each

Preferred Risk Policy (PRP)

8 | Flood Insurance Rating: Facts and Factors October 17, 2013

Sample PRP Table

9 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Applies to buildings newly shown in Special Flood Hazard Areas on or after October 1, 2008

• Buildings must meet Preferred Risk Policy loss history requirements

• Historic FIRM must be provided

Preferred Risk Policy Extension

10 | Flood Insurance Rating: Facts and Factors October 17, 2013

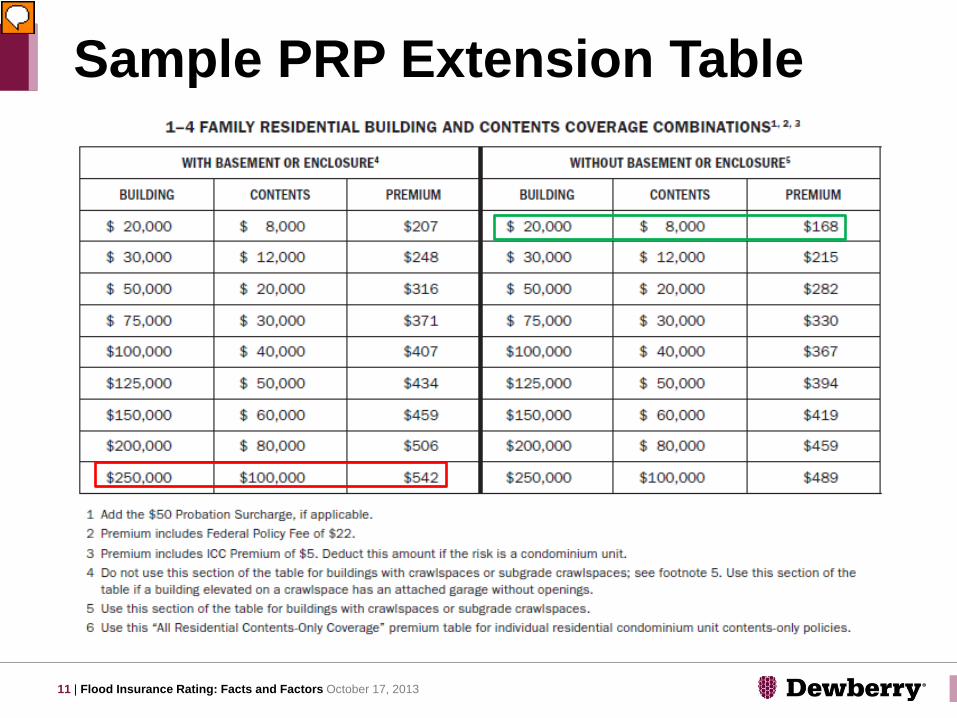

Sample PRP Extension Table

11 | Flood Insurance Rating: Facts and Factors October 17, 2013

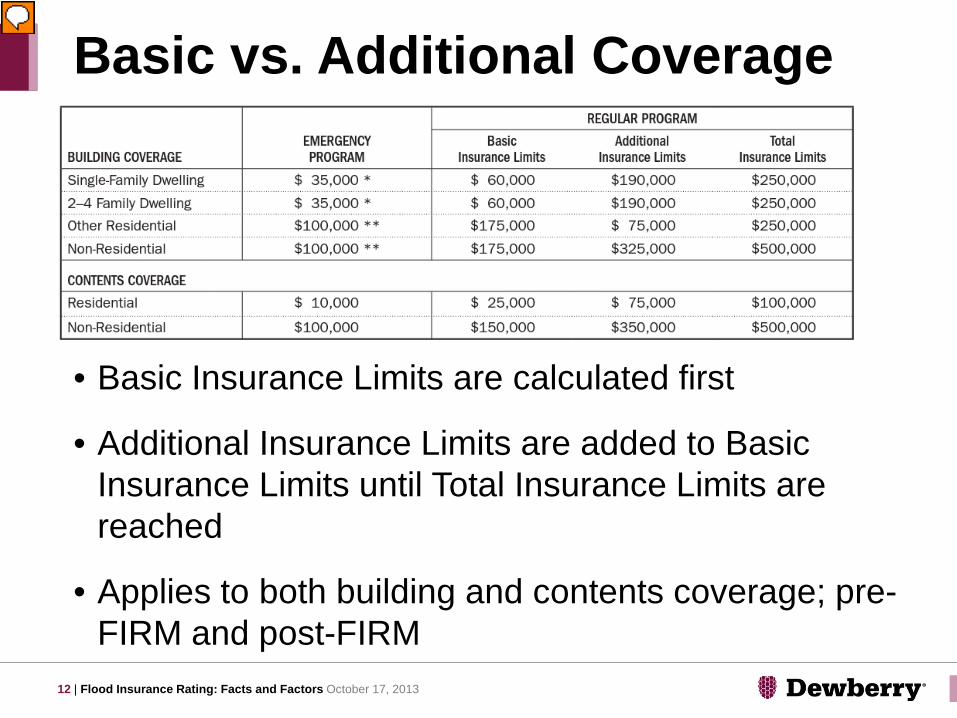

Basic vs. Additional Coverage

12 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Basic Insurance Limits are calculated first

• Additional Insurance Limits are added to Basic Insurance Limits until Total Insurance Limits are reached

• Applies to both building and contents coverage; pre-FIRM and post-FIRM

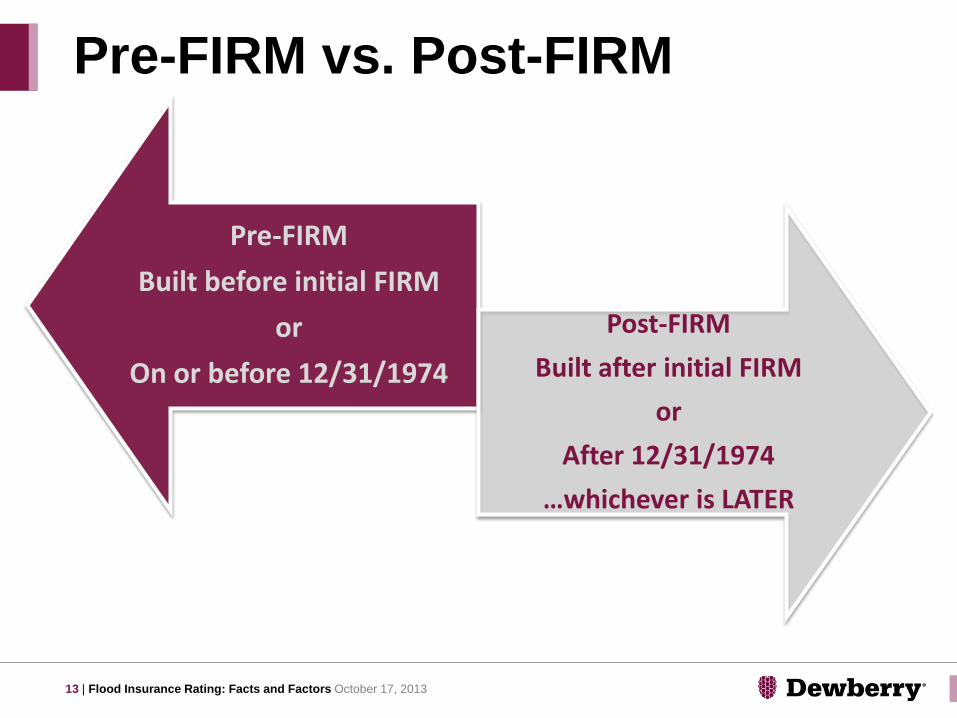

Pre-FIRM vs. Post-FIRM

13 | Flood Insurance Rating: Facts and Factors October 17, 2013

Pre-FIRM Built before initial FIRM

or On or before 12/31/1974

Post-FIRM Built after initial FIRM

or After 12/31/1974

…whichever is LATER

Pre-FIRM Policy Rating

14 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Rate for a single family home; $250,000 building and $100,000 contents; with basement

• Building Basic = $0.97 x 600 = $582 • Building Additional = $1.14 x 1900 = $2166 • Contents Basic = $1.15 x 250 = $288 • Contents Additional $1.16 x 750 = $870 Subtotal = $3906

• Provides building elevations and other building specifications

• Required for all post-FIRM and full-risk rated pre-FIRM structures located in SFHAs

• Can be completed by property owner or community official for Zone A structures if no BFE is available

• Can be completed by property owner or community official for Zone AO structures

Elevation Certificate

15 | Flood Insurance Rating: Facts and Factors October 17, 2013

Lowest Floor Guide

16 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Uses information from the Elevation Certificate to determine the elevation used for rating a flood insurance policy

17 | Flood Insurance Rating: Facts and Factors October 17, 2013

FOR MOST FLOOD HAZARD ZONES:

• Lowest Floor Elevation (LFE) - Base Flood Elevation (BFE) = Elevation Difference

• LFE determined using Lowest Floor Guide; BFE determined using the Flood Insurance Rate Map and Flood Insurance Study

Elevation Difference

18 | Flood Insurance Rating: Facts and Factors October 17, 2013

FOR ZONE A AND ZONE AO:

• Top of Bottom Floor (TOBF) - Highest Adjacent Grade (HAG) = Elevation Difference

• TOBF and HAG found on the Elevation Certificate

Elevation Difference

19 | Flood Insurance Rating: Facts and Factors October 17, 2013

Post-FIRM Rating: Zone AE, A1-30

20 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Rate for a single family home; $250k building; 3 floors with basement; elevation difference = -1

• Building Basic = $2.28 x 600 = $1368 • Building Additional = $0.41 x 1900 = $779

Subtotal = $2147

• Additional information may be used to evaluate the coastal risk when it is believed that the design, placement, and/or construction of a building is such that the usual criteria used to establish actuarially appropriate rates do not reflect the lessened risk to the structure

• The V-Zone Risk Factor Rating Form is used in conjunction with the V-Zone Risk Rating Relativities Table to reflect premium adjustments

• Factors range from 0.4 to 1.0

V-Zone Considerations

21 | Flood Insurance Rating: Facts and Factors October 17, 2013

Questions?

22 | Flood Insurance Rating: Facts and Factors October 17, 2013

Click for Source

Post-FIRM Rating: Zone A

23 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Rate for a single family home; $250k building/$100k contents; no basement; no BFE; elevation difference = +1

• Building Basic = $2.68 x 600 = $1608 • Building Additional = $0.42 x 1900 = $798 • Contents Basic = $1.54 x 250 = $385 • Contents Additional $0.16 x 750 = $120

Subtotal = $2911

Post-FIRM Rating: Zone AO

24 | Flood Insurance Rating: Facts and Factors October 17, 2013

• No BFE; TOBF – HAG = Elevation Difference

• If Elevation Difference is equal to or greater than the flood depth shown on the FIRM, use “compliant” rates

• Rate for a single family home; $250k building/$100k contents; no basement; no BFE; compliant

• Building Basic = $0.28 x 600 = $168 • Building Additional = $0.08 x 1900 = $152 • Contents Basic = $0.38 x 250 = $95 • Contents Additional $0.23 x 750 = $98

Subtotal = $513

• All non-residential floodproofed structures are submitted for rating directly from the NFIP

• Building must be floodproofed to the BFE +1

• Floodproofing credit is not available in V zones

Floodproofing Certificate

25 | Flood Insurance Rating: Facts and Factors October 17, 2013

Certain structures in high-risk zones have characteristics which require an in-depth underwriting analysis before a premium can be provided.

• FEMA Underwriting Branch receives:

• NFIP Application and Submit-for-Rate Worksheet

• Elevation Certificate and Building Photographs

• Elevated Building Determination Form

• Miscellaneous Items • Variance statement • List of machinery and equipment • Breakaway wall certification • V-Zone Risk Factor Rating Form

Submit-for-Rate

26 | Flood Insurance Rating: Facts and Factors October 17, 2013

Click for Source

• Section 1 – Pre-FIRM and Post-FIRM Non-Elevated Buildings and Pre-FIRM Elevated Buildings

• Section 2 – Post-FIRM Elevated Buildings

• Section 3 – Unnumbered A Zone

• Section 4 – Unnumbered V Zone

• Section 5 – Miscellaneous (buildings over water; floodproofed non-residential buildings; ICC coverage)

• Appendix – Forms for Use in Specific Rating

Specific Rating Guidelines

27 | Flood Insurance Rating: Facts and Factors October 17, 2013

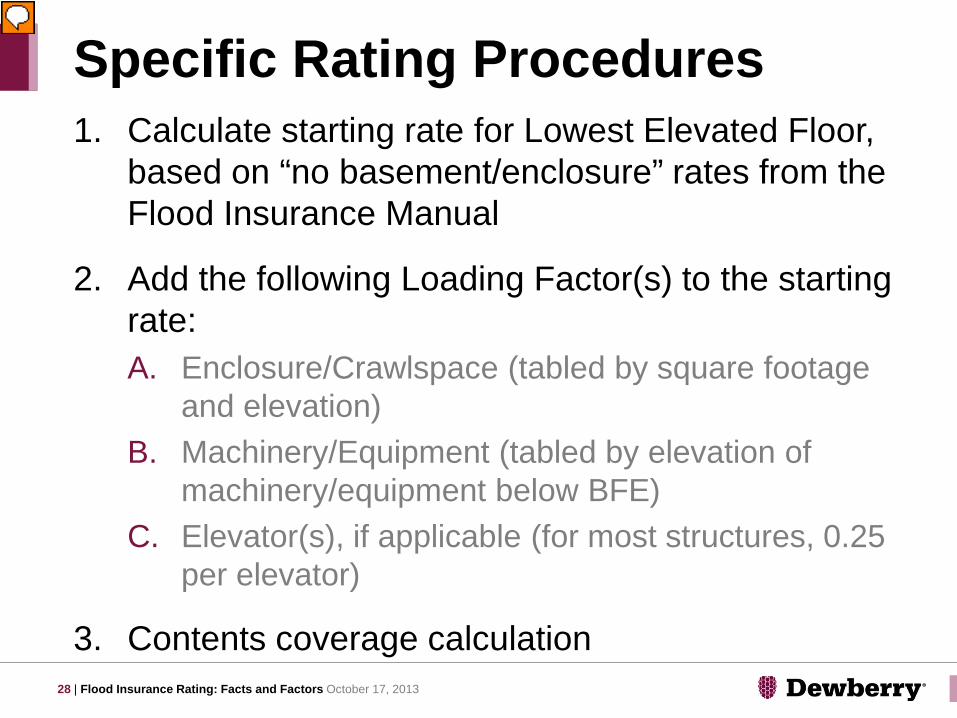

1. Calculate starting rate for Lowest Elevated Floor, based on “no basement/enclosure” rates from the Flood Insurance Manual

2. Add the following Loading Factor(s) to the starting rate: A. Enclosure/Crawlspace (tabled by square footage

and elevation) B. Machinery/Equipment (tabled by elevation of

machinery/equipment below BFE) C. Elevator(s), if applicable (for most structures, 0.25

per elevator)

3. Contents coverage calculation

Specific Rating Procedures

28 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Enables rating of new policies before an Elevation Certificate has been received

• Building/contents rates range from $3.00/$2.00 to $6.00/$4.00 per $100 of coverage

• All of the following must apply • Post-FIRM • 1-4 family residential • Building located in Zones AE, A1-A30, AO, AH, or in Zone

A areas where the community provides BFEs

• Policies cannot be renewed or rewritten with provisional rates

Provisional Rating

29 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Used to issue policies when agents fail to provide the full-risk rating information

• Range from $3 to $12 per $100 of coverage

• Notice of Tentative Rating provided to the policyholder, agent, and mortgagee, if any

• When necessary documentation has been received, policy is rerated and rewritten

• Coverage amounts adjusted in the event of a loss

Tentative Rates

30 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Written consent from any mortgagee listed on the policy should be obtained before requesting a deductible higher than the standards

Deductible Factors

31 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Serves to fund Increased Cost of Compliance Coverage

• Not eligible for deductible discounts

ICC Premium

32 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Ranges from 5% to 45%, depending on the community’s class

• Preferred Risk Policies and Mortgage Portfolio Protection Program Policies are not eligible

• Most Submit-for-Rate policies are also ineligible

• Discount table located in Flood Insurance Manual

CRS Discount

33 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Required by Biggert-Waters 2012

• 5% of premium; applied after CRS discount

• Assessed to most premiums to build a catastrophic reserve fund

• Does not apply to Preferred Risk Policies and Group Flood Insurance Policies

Federal Reserve Fund Assessment

34 | Flood Insurance Rating: Facts and Factors October 17, 2013

• A non-compliant NFIP community may face a one-year probationary period

• $50 surcharge applied to all policies within the community

Probation Surcharge

35 | Flood Insurance Rating: Facts and Factors October 17, 2013

• Required by Biggert-Waters 2012

• $44 for standard NFIP policies; $22 for Preferred Risk Policies

• Assessed to defray administrative expenses incurred in carrying out the NFIP

Federal Policy Fee

36 | Flood Insurance Rating: Facts and Factors October 17, 2013

1. Determine rate and multiply by $100 of coverage

2. Subtract deductible discount, if applicable

3. Add Increased Cost of Compliance (ICC) premium

4. Subtract Community Rating System (CRS) discount

5. Add 5% Federal Reserve Fund Assessment

6. Add probation surcharge, if applicable

7. Add Federal Policy Fee

Overview Revisited

37 | Flood Insurance Rating: Facts and Factors October 17, 2013

• NFIP Flood Insurance Manual

• NFIP Specific Rating Guidelines

• FloodSmart

• Map Service Center

• FEMA GeoPortal – National Flood Hazard Layer

• BW-12

• FEMA Elevation Certificate

• NFIP Lowest Floor Guide

• NFIP Write Your Own (WYO) Bulletins

References

38 | Flood Insurance Rating: Facts and Factors October 17, 2013

Questions?