e. martin davidoff & associates - cope seminars the irs.pdf · • seek penalty abatement types...

TRANSCRIPT

E. MARTIN DAVIDOFF & ASSOCIATES

ATTORNEY AT LAW

353 Georges Road - Suite K E. Martin Davidoff, CPA, ESQ. P.O. Box 835 Dayton, NJ 08810-0835

_____________

TEL: 732-274-1600 FAX: 732-274-1666

NAVIGATING THE IRS

Presented via

COPE Seminars

at

Mercer County Community CollegeEast Windsor, NJ - July 14, 2016

E. Martin Davidoff, CPA, Esq.

Page 1 of 169

Page 1 of 169

Navigating the IRS - TABLE OF CONTENTS Cover Page and Table of Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 -2

Steps in a Controversy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Tools in Dealing with the IRS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

The Rules of Engagement in Dealing with the IRS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Alternatives in a Collection Matter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-8

IRS Tools & Considerations; The Key is Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Sample Engagement Letters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 - 14

Ethical Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 - 18

Sample Forms 2848 & 8821 - Representative Authorizations . . . . . . . . . . . . . . . . . . . . . . . . 19 - 24

Sample Letters 1058 & Request for a Collection Due Process Hearing (Form 12153) . . . . . 25 - 38

IRS Appeals in Collection Matters - CPA Magazine Article . . . . . . . . . . . . . . . . . . . . . . . . 39 - 40

Tools in Dealing with IRS Liens, Before and After . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Sample Collection Appeal Request (Form 9423) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 - 46

Securing Discharges of IRS Liens for Property Matters - CPA Magazine Article . . . . . . . 47 - 50

Documents related to the Fresh Start Program and IRS Advisory . . . . . . . . . . . . . . . . . . . . . 51 - 58

Lien Withdrawals and Credit Repair . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59 - 81

Streamlined Installment Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 - 84

Samples of Form 9465 & Form 433-D & Online Installment Plan . . . . . . . . . . . . . . . . . . . . 85 - 94

Another Alternative: Offer In Compromise Statistics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95 - 96

Federal Tax Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

Transcripts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98 - 101

Quarterly Analysis of client Payroll tax returns filing and statements . . . . . . . . . . . . . . . . . . . . 102

Sample Cash Flow Analysis. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

Sample Penalty Abatement and Penalty Abatement Appeal Letters . . . . . . . . . . . . . . . . . 104 - 106

Sample Request for Taxpayer Advocate Service Assistance (Form 911) & NJ Form 911 107 - 112

SB/SE Fast Track Audit Program & Agreement to Mediate Information . . . . . . . . . . . . . 113 - 121

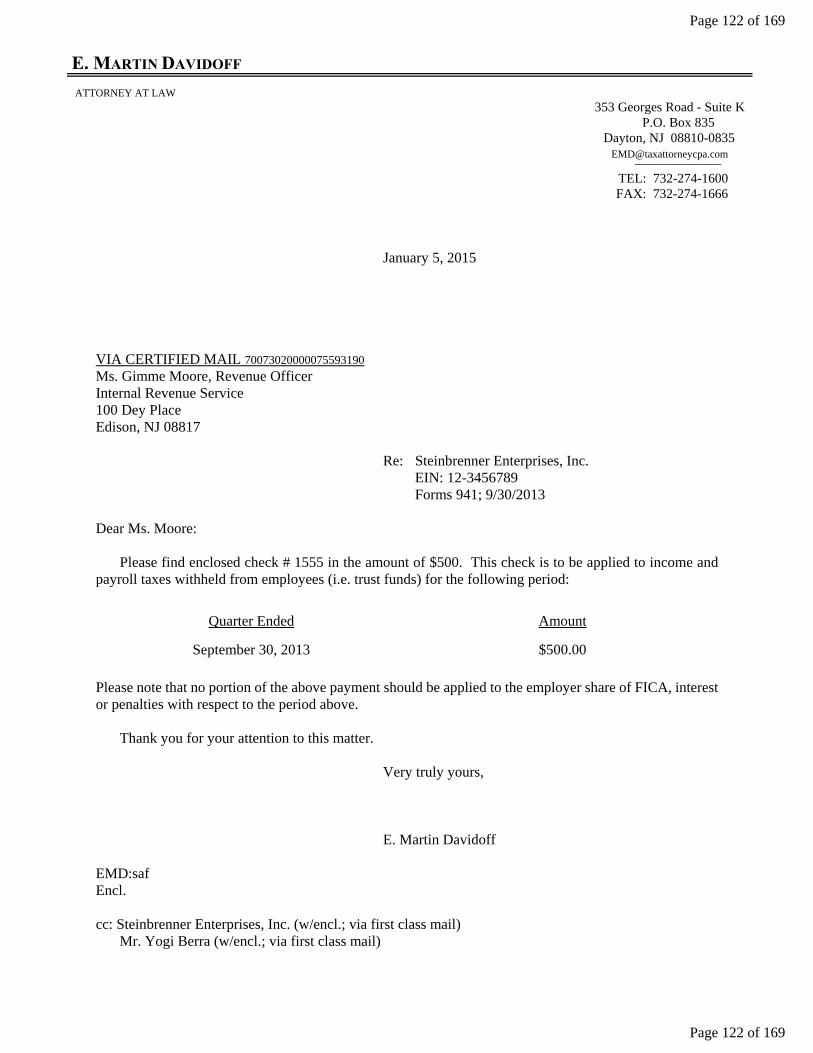

Sample Letter re Payment of Trust Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

Sample FOIA Request . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123 - 128

Sample Request for Third Party Contacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

Sample Cash Bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130 - 131

Sample Examination Appeal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132 - 133

Sample Status Sheets, Initial Meeting Notes and Plan of Action . . . . . . . . . . . . . . . . . . . 134 - 138

Sample letters to Clients regarding successful Installment Agreement (2 styles). . . . . . . . 139 - 143

Sample letters to Clients regarding successful Offer In Compromise. . . . . . . . . . . . . . . . 144 - 145

Identity Theft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146 - 153

Articles on Representation of Clients & Rules of Engagement & Audits. . . . . . . . . . . . . 154 - 169

1. Getting Started . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154 - 156

2. Being Authorized . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157 - 158

3. Rules of Engagement Part I (1-4) . . . . . . . . . . . . . . . . . . . . . . . . . . 159

4. Rules of Engagement Part II (5-6) . . . . . . . . . . . . . . . . . . . . . . . . . 160

5. Rules of Engagement Part III (7-8) . . . . . . . . . . . . . . . . . . . . . . . . . 161

6. Rules of Engagement Part IV (9-10) . . . . . . . . . . . . . . . . . . . . . . . . 162

7. Rules of Engagement Part V (11-13) . . . . . . . . . . . . . . . . . . 163 - 164

8. Rules of Engagement Part VI (14-19) . . . . . . . . . . . . . . . . . . 165 - 166

9. Steps of an Effective IRS Audit Resolution . . . . . . . . . . . . . 167 - 169

© Copyright 2016 E. Martin Davidoff (U.S.A.) All Rights Reserved

Page 2 of 169

Page 2 of 169

Steps in a Controversy

1. Initial contact by the Client and follow-up calls with prospective client to find out generalnature of their problem, “sell” the firm, and schedule a consultation.

2. Initial Consultation with client to understand his/her dilemma and outline a preliminary planof action.

3. Agree to what services you will provide and how you will get paid. Execute an engagementletter. (See pgs 12 through 14).

4. Get authorization to represent your client (Forms 2848, 8821, Oral TIAA, etc. See IRSpublication at http://www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Third-Party-Authorization-Purpose). (See pgs 19 through 24 and 157 through 158.)

5. Put forth a written Plan of Action with the client and your staff. (See pgs 134 through 137).

6. Put together a list of materials for your client to gather.

7. Transmit authorizations to CAF and to Revenue Officer, if applicable.

8. Get records of account/account transcripts and prepare a federal tax summary. (See pg 97)

9. Make certain client is staying current on all taxes going forward. Sometimes this mayrequire the client engaging a payroll tax service with a Tax-Pay service.

10. Follow Plan of Action and gather all materials.

Page 3 of 169

Page 3 of 169

Tools in Dealing with the IRS

1. Going up the chain of command:

North Atlantic (NA) & Central Area (NJ) Managers, SB/SE- Collections (NA Director) Tim Sherrill 414-231-2404- Collections (Central Director) Renee Mitchell 614-280-8611

(John Rice, Assistant)- Examination (NA Director) Joseph Tiberio 617-316-2539- Examination (Central Director) John Imhoff 267-941-6159

2. Form 12153, Collection Due Process Hearing (See pgs 32 through 37.)

3. Form 9423, Collection Appeal Request (See pgs 42 through 46.)

4. Appealing denials of Penalty Abatement requests & Examination Findings (See pgs 104through 106.)

5. Taxpayer Advocate's Office - (Form 911) - (See pgs 107 through 112)- Manhattan: Kevin Kelly 212-436-1010- Brooklyn, NY Mark Newman 718-834-2210- New Jersey Justin Axelford 973-921-4376- Philadelphia Lois Lombardo 215-861-1237

6. Fast Track Mediation/Settlement (See Publication 4167)

7. Designation of Trusts Fund (See pg 122)

8. Record of Third Party Contacts (See pg 129)

9. Freedom of Information Requests (“FOIA”) (See pg 123 through 128)

10. Deposit in the Nature of a Cash Bond (See pgs 130 through 131)

11. IRS Website & E-Services

12. Your Analysis of the Client’s Situation (see pages 102 & 103 regarding Quarterly Analysisand Cash Flow)

Page 4 of 169

Page 4 of 169

The Rules of Engagement in Dealing with the IRS

(See pages 159 through 166 )

1. Never volunteer information, unless it is part of a strategy.

2. Never give materials to the IRS that you have not reviewed carefully (e.g., bank statements, paycheckstubs, etc.).

3. Assert yourself as appropriate. Learn how to say:

“Please give me your full name and employee ID number.”

"Please give me the name and telephone number of your manager."

"Who is the Territory manager?"

"What is your authority for that position?"

"I want to take that issue to Fast Track Mediation"

"Are you refusing to provide that information to me?"

4. Always ask for the full name and employee ID of the IRS representative.

5. Never Lie. Period.

6. Do not accept unreasonable time-lines.

7. Do not agree to terms that your client cannot meet.

• Carefully review and understand your client's budget; and

• Build in additional time, anticipate client delays.

8. Current Taxes Get Paid First!

9. Meet all commitments made to the IRS...or at least call.

10. Do not let Appeal Deadlines pass without preserving your client's rights.

11. Carefully read and fully understand all IRS communications.

12. Set ticklers and followup. Never just wait for the IRS to contact you. Know your case's status.

13. Confirm all examination computation through tax software.

14. Be realistic with your client. Promise less than you expect, deliver more than anticipated.

15. Confirm all oral agreements with the IRS in writing and request that they sign off.

16. When you win, say “thank you” and “goodbye!”

17. Pull transcripts and summarize them. (See page 98 through 102.)

18. Be fully prepared for all meetings....anticipate the unexpected.

19. Know your tools and rights (see previous page).

Page 5 of 169

Page 5 of 169

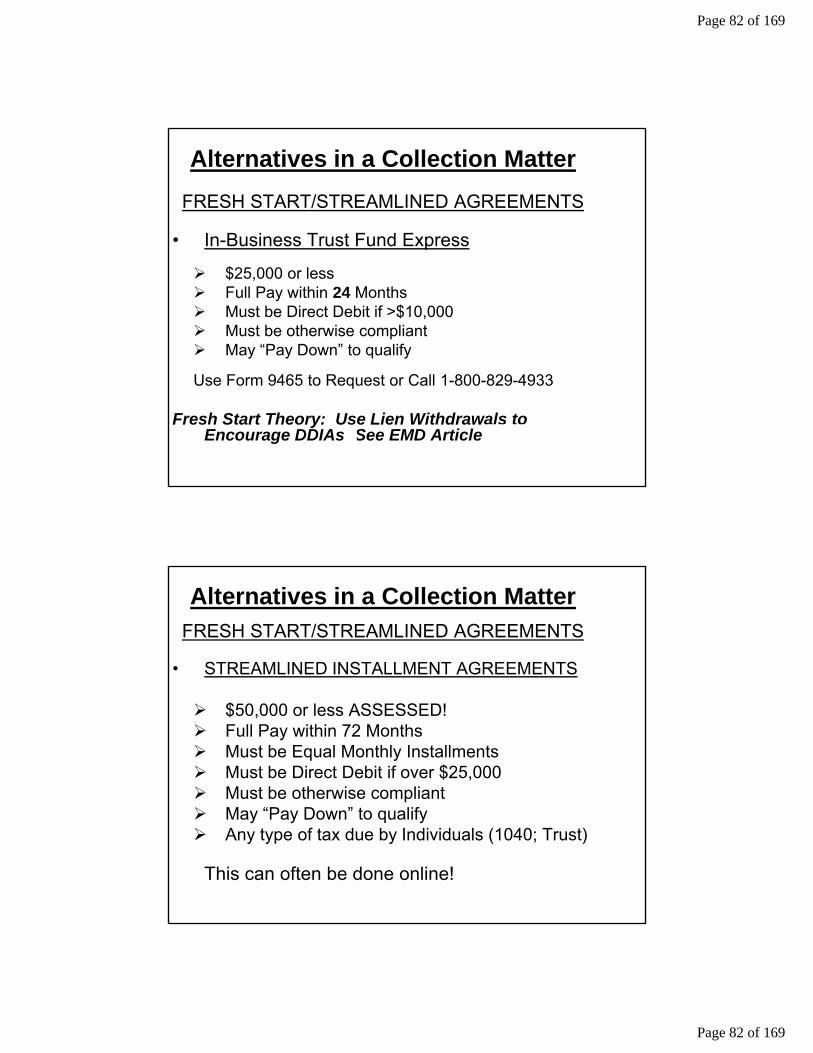

Alternatives in a Collection Matter

I. Pay all that is due• Refinance home• Loans from family [Can still seek penalty abatement]• Liquidate assets

II. Pay tax & interest only• Seek penalty abatement Types of Penalty Abatement

i Revenue Officer U First Time (IRM § 20.1.1.3.6.1)i Taxpayer Advocate U Reasonable Causei Service Centeri Telephone (note script)i Priority Practitioner Hotline

Note: IRS “rule” to pay all tax prior to considering late payment penalty abatements.

III. Uncollectible status• Reviewed periodically

IV. Partial pay installment agreement

V. Full-pay installment agreement• Streamlined: < $50,000 assessed

Pay within 6 years or less No financial documentation required

VI. Offer in Compromise

VII. Special Considerations

• Bankruptcy• Expiring Statutes• Innocent Spouse• Missing/Misapplied Payments• Transfer of assets for less than adequate consideration• Identity Theft

Common Threads to Installment Agreements

1. Up front consideration

2. Lien Filing or holding off thereon

3. Increasing payments with time

4. Date of Payment/Direct Debit

5. Communicate to client in writing (see samples - pgs 139 through 145)

6. The role of Reasonable Collection Potential

Page 6 of 169

Page 6 of 169

Alternatives in a Collection Matter����(�����1����0�� ���2���0� ��

� ����0�� ���� ����0� ��2���0� ��

'(��3�������4

� ��-�.�-5�"��,*���, ���$��$% ������67

� �% &����#��5��� �� ���,��#�����8 ���6�"��!�"��� �����&8���9:��5%����;9<=:::7

� � �5�����5��� �� ����&��$��$% ������6

Page 7 of 169

Page 7 of 169

1

Alternatives in a Collection MatterFRESH START/STREAMLINED AGREEMENTS

• STREAMLINED INSTALLMENT AGREEMENTS

REQUIRED FINANCIAL DISCLOSURES:

• Up to $25,000: None

• Over $25,000: None • 2nd Page of Form 9465 :

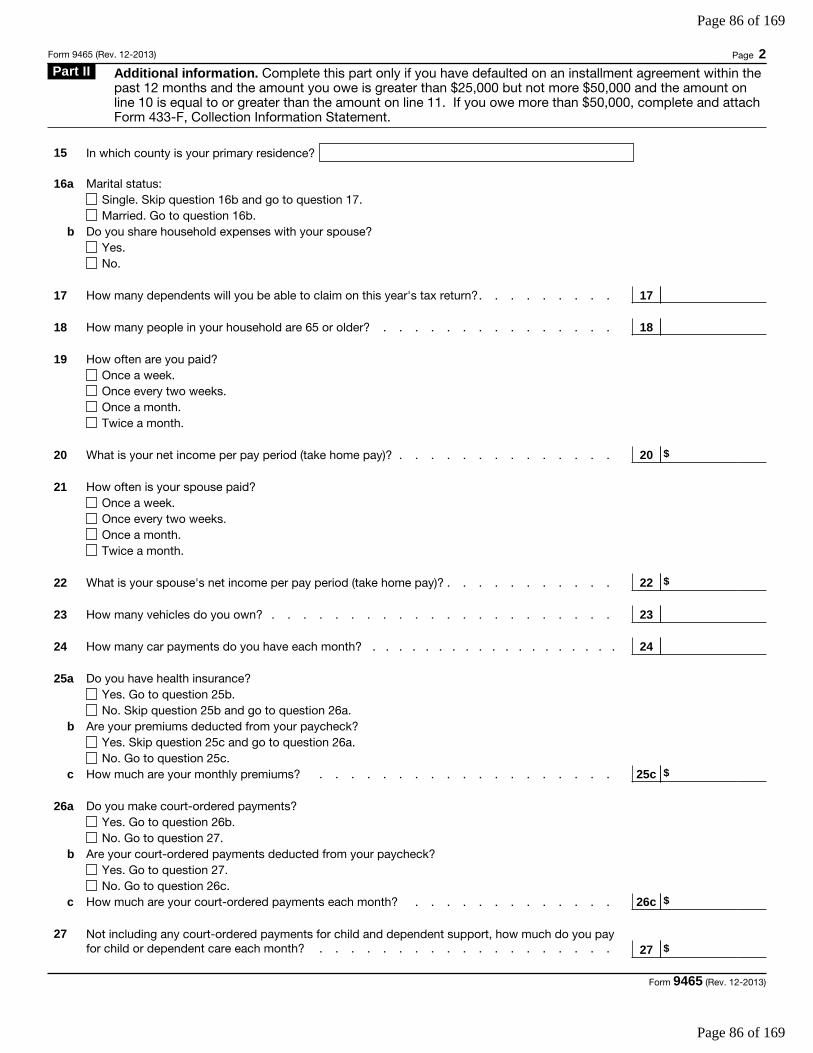

- Financial disclosure as of Jan 2014; required if one has defaulted on an installment agreement within the past 12 months.

-Provides essential financial information to assure to the IRS that the Taxpayer CAN make the monthly payments promised.

Alternatives in a Collection MatterFRESH START/STREAMLINED AGREEMENTS

• STREAMLINED INSTALLMENT AGREEMENTS

$50,000 or less ASSESSED! Full Pay within 72 Months Must be Equal Monthly Installments Must be Direct Debit if over $25,000 Must be otherwise compliant May “Pay Down” to qualify Any type of tax due by Individuals (1040; Trust)

IRS Claims can do this all online!

Page 8 of 169

Page 8 of 169

IRS Tools & Considerations

A. Financial Disclosure:• Form 433A Form 433A (OIC)• Form 433B Form 433B (OIC)• Form 433F Form 9465

B. Liens

C. Levy/Garnishment

D. Primary Considerations• Keep Current• Disclose Financial Information• Plan to deal with debt to the IRS

The Key is Time

Time as a Friend

A. Time to determine appropriate course of action

B. Time to get Client to take that action

• Payroll• Estimates• Filing of Returns• Verification of Financial Position• Documentation of all of the above

C. Time to get the IRS to come to “our” way of thinking on the case. Specifically, we need time to:

• Present financial information• Present facts regarding penalty abatement• Involvement of IRS management• Involvement of Appeals• Involvement of the Taxpayer Advocate Service• File Returns

D. Time for the Statute to Expire

Time as an Enemy

A. Appeal RightsB. Tax Court Petition DeadlinesC. IRS Arbitrary (non-statutory) DeadlinesD. The next payroll date during garnishmentE. Stress builds with time as matter remains unresolved

Page 9 of 169

Page 9 of 169

E. MARTIN DAVIDOFF

ATTORNEY AT LAW

353 Georges Road - Suite KP.O. Box 835

Dayton, NJ 08810-0835 [email protected] _____________

TEL: 732-274-1600 FAX: 732-274-1666

VIA E-MAIL January 2, 2016Mr. Ralph Terry41 ABC AvenueMetuchen, New Jersey 08840

RE: Consultation AdviceDear Mr. Terry:

I am writing this letter to confirm and specify the financial arrangements regarding the services which I willbe providing to you. I will be providing advice to you regarding federal and/or state taxation issues. I may alsoprovide other services which you request.

My fees are based upon the amount of time required to meet or speak with you and to review and analyzeinformation that you provide to me. In addition, you will be charged for my or my staff's time with respect tofollow-up calls, meetings and other services requested. My current hourly consultation rate is $600. The hourlyrates for my staff range from $60 to $400. All rates will increase from time to time consistent with the ratescharged generally to the firm’s tax controversy clients. Also, you will be charged for out-of-pocket expenses(photocopying, federal express, postage, etc.) As a courtesy for your referral through Mr. Bill Stafford, there willbe no charge for the first 15 minutes of this initial consultation. If the matter requires extended, involved work,a separate engagement letter will usually be required, as well as a retainer.

In the unlikely event that it becomes necessary for me to seek legal recourse to receive payment of my feesthrough litigation or arbitration, you hereby agree to reimburse me for all out-of-pocket expenses, as well as anyof the time expended by my staff and/or me at the hourly rates then in effect, to secure such payment. Forpurposes of our agreement, the term "out-of-pocket expenses" also includes any legal fees and all other expensesin connection with any attempt (including litigation) to collect my fees. By signing below, you hereby consentthat I may use any information which you provide me to collect any fees due to this firm. Such informationincludes income tax returns which we prepare for you or which you provide us.

If the terms outlined in this letter are in agreement with your understanding of our engagement, pleasesign this letter and complete the enclosed credit card authorization, if appropriate, to facilitate our phone or in-person conference, then fax or email these documents back to our office. Your card will be billed at the ratesspecified above for the appropriate increment of time for this and future consultation meetings.

I look forward to working with you.

EMD:jcencls.Agreed to by: ___________ Ralph Terry Date

Page 10 of 169

Page 10 of 169

E. MARTIN DAVIDOFF

ATTORNEY AT LAW

353 Georges Road - Suite KP.O. Box 835

Dayton, NJ 08810-0835 [email protected] _____________

TEL: 732-274-1600 FAX: 732-274-1666

January 2, 2016

Mr. Ralph Terry41 ABC AvenueMetuchen, New Jersey 08840

Dear Mr. Terry:

If applicable, please fill out the information below, including signature, and bring to the meeting sothat we may charge your credit card appropriately after the meeting. Feel free to call us should you haveany questions.

Thank you.

I hereby authorize E. Martin Davidoff, Attorney at Law to charge my account pursuant to the terms of theaccompanying engagement letter.

Name on Card : ___________________________________

Check one: MasterCard Visa American Express

*NOTE: If you are using an American Express card, an additional 1% of the charged amountwill be added to offset the American Express Merchant processing fee.

Credit Card Number__________________________________________

VIN Code (3 digit code on back)________________________________

Expiration Date_____________________________________________

_________________________________________ ______________________Ralph Terry Date

__________________________________________________________________________________Full Billing Address of Card

Page 11 of 169

Page 11 of 169

E. MARTIN DAVIDOFF

ATTORNEY AT LAW

353 Georges Road - Suite KAndrew G. Paradis, Esq. P.O. Box 835 Associate Dayton, NJ 08810-0835

[email protected] _____________

TEL: 732-274-1600 FAX: 732-274-1666

January 2, 2016

BY HAND IN OUR OFFICEMr. & Mrs. Mickey Mantle123 Main StreetAnywhere, New Jersey 08666

Dear Mr. & Mrs. Mantle:

We are writing this letter to confirm and specify the financial arrangements regarding the services whichI will be providing to you. We will be representing XYZ Corporation before the Internal Revenue Service("IRS") in connection with the assessment and collection of Payroll taxes for the years 2009 through 2011. We will be representing you, personally, before the IRS in connection with the assessment and collection ofincome taxes for the years 2009 through 2012, for trust fund recovery penalties proposed by the IRS and forother years and matters in the event that the IRS expands the scope of its investigation. I may also provideother services which you request.

As we have discussed, our representation is strictly limited to the government agency above. It is notour practice to investigate beyond this specific agency . However, should you require our representation onother matters at a later date, we would be glad to consider such requests provided to us in writing.

Our fees are based upon the amount of time required to review and analyze information provided to us,perform necessary research, carry out additional services in representing you, and complete additionalservices which you request. My current hourly rate is $600. The hourly rates for our staff range from $60to $400. The principal member of our staff who will be working on the case is Ms. Susan Smith, and herhourly rate is $275. All rates will increase from time to time consistent with the rates charged generally tothe firm’s tax controversy clients. In addition, you will be charged for out-of-pocket expenses (photocopying,federal express, postage, etc.)

I will require an initial retainer of $3,500 prior to commencing work. The $3,500 will be held in ourbusiness account and will be applied towards your final invoice. During the course of our engagement, youwill receive invoices periodically. Our invoices are due and payable immediately upon receipt. There willbe a late charge equal to 1.5% per month on any unpaid balances. Please note that, at our option, the workon your account will cease at anytime after any invoice of ours remains unpaid for a period of 10 days, unlessother mutually satisfactory arrangements have been made in writing.

We have also agreed to provide you with additional flexibility with respect to the payment of fees dueto this firm. So long as you make monthly payments of $350 on the first of each month, commencing withFebruary 1, 2016, we will continue to work on your account and we will waive any late charges. Please notethat, even if we have not yet issued our first invoice, the first payment of $350 is still expected to be madeon or before February 1, 2016 . Any balance due and payable as of February 1, 2018 shall become due andpayable immediately.

Page 12 of 169

Page 12 of 169

Mr. & Mrs. Mickey MantleJanuary 2, 2016Page 2

Although you may find it convenient and appropriate that we invoice XYZ Corporation for some or allof our services, you will be personally responsible for the payment of any of our invoices issued to thecorporation and/or you.

You have a role in assisting us in your representation. It is your obligation to respond timely andtruthfully to our inquiries. Often such inquiries will relate to answering financial related questions. Othertimes, our inquiries may relate to facts and circumstances which will assist us in securing an abatement oftaxes or penalties. We reserve the right to terminate this engagement if you fail to timely respond to ourinquiries and/or accurately portray your compliance history and communications with the taxing authority.

You have the right to terminate our engagement at any time. To do so, please send us your request toterminate the firm’s services in writing. Of course, we encourage you to speak directly to us as to the reasonsfor termination and to assist in the transition of the case to new counsel, if applicable. Upon receipt of yourwritten request, we will wrap-up services on your account to ensure that the current status of the case is fullydocumented and to provide you any documents in our file that you request. In a reasonable time thereafter,we will issue our final invoice and apply any remaining funds from the advance payment against thebalance. We will refund any unused portion of your advance payment and expect prompt payment of anybalance due after application of the advance payment.

In the unlikely event that it becomes necessary for us to seek legal recourse to receive payment of our feesthrough litigation or arbitration, you hereby agree to reimburse us for all out-of-pocket expenses, as well asany of the time expended by our staff at the hourly rates then in effect, to secure such payment. For purposesof our agreement, the term "out-of-pocket expenses" also includes any legal fees and all other expenses inconnection with any attempt (including litigation) to collect our fees. By signing below, you hereby consentthat we may use any information which you provide us to collect any fees due to this firm. Such informationincludes income tax returns which we prepare for you or which you provide us.

We are aware that you have been working with Tony Kubek, CPA, with respect to this case. You herebyacknowledge that we will be working with Mr. Kubek and you hereby give us permission to discuss your casewith and provide copies of documents, correspondence and invoices to Mr. Kubek.

If the terms outlined in this letter are in agreement with your understanding of our engagement, youshould sign the enclosed copy of this letter and return it to us as soon as possible along with the $3,500payment. By signing below you are each also agreeing to be jointly and individually responsible for theentire amount of our fees. Should you have any questions concerning this letter or the fees to be charged,please do not hesitate to contact us.

To facilitate our representation, you will find the following documents in your secure portal:

1. Form 2848 Power of Attorney which will enable us to represent you each (required separatelyby the IRS for each spouse) before the Internal Revenue Service

2. Form 8821 Tax Information Authorization for you each (required separately by the IRS for eachspouse) which will enable other members of our staff to discuss your case with the InternalRevenue Service

3. Form 2848 Power of Attorney which will enable us to represent XYZ Corporation before theInternal Revenue Service

4. Form 8821 Tax Information Authorization for you each which will enable other members of ourstaff to discuss XYZ Corporation's case with the Internal Revenue Service

Page 13 of 169

Page 13 of 169

Mr. & Mrs. Mickey MantleJanuary 2, 2016Page 3

Please sign two copies of each form and return them to us. You may retain the third copy for your files.

You have agreed to comply with all federal and state tax laws going forward on a timely basis. To thatend, you will be placing the payroll with Paychex and authorizing them to withdraw payroll taxes with eachpayroll (their "Tax Pay" service).

We look forward to working with you.

Very truly yours,

E. Martin Davidoff

EMD:

Agreed to by: U __________ Mickey Mantle Date

U Merlyn Mantle Date

Page 14 of 169

Page 14 of 169

Ethical ConsiderationsContext: Financial Disclosure:• Q: Do you own any property? A: Not in my name!

• Backstory:Client gives home to children. Agreement with family is parents get $$$s from sale. Whose property.

• How do you present on Form 433?

Ethical Considerations

• Alternate Scenario:Parents purchase home for adult son and retain in their name.

• How do you present on son’s Form 433?

Page 15 of 169

Page 15 of 169

Ethical ConsiderationsAdditional Facts:• Son makes all mortgage payments• Parents claim interest and real estate taxes• Son pays all expense on property, including

real estate taxes and insurance (through the mortgage).

• No Lease between the parties, no rental income claimed by parents.

• Family views the property as the son’s.

Ethical Considerations

Opinions on Options• Report as son’s asset on his Form 433-A?• Lease between parents and son?• Will to make clear that property will go to

son?• In reality, whose house is this?

Page 16 of 169

Page 16 of 169

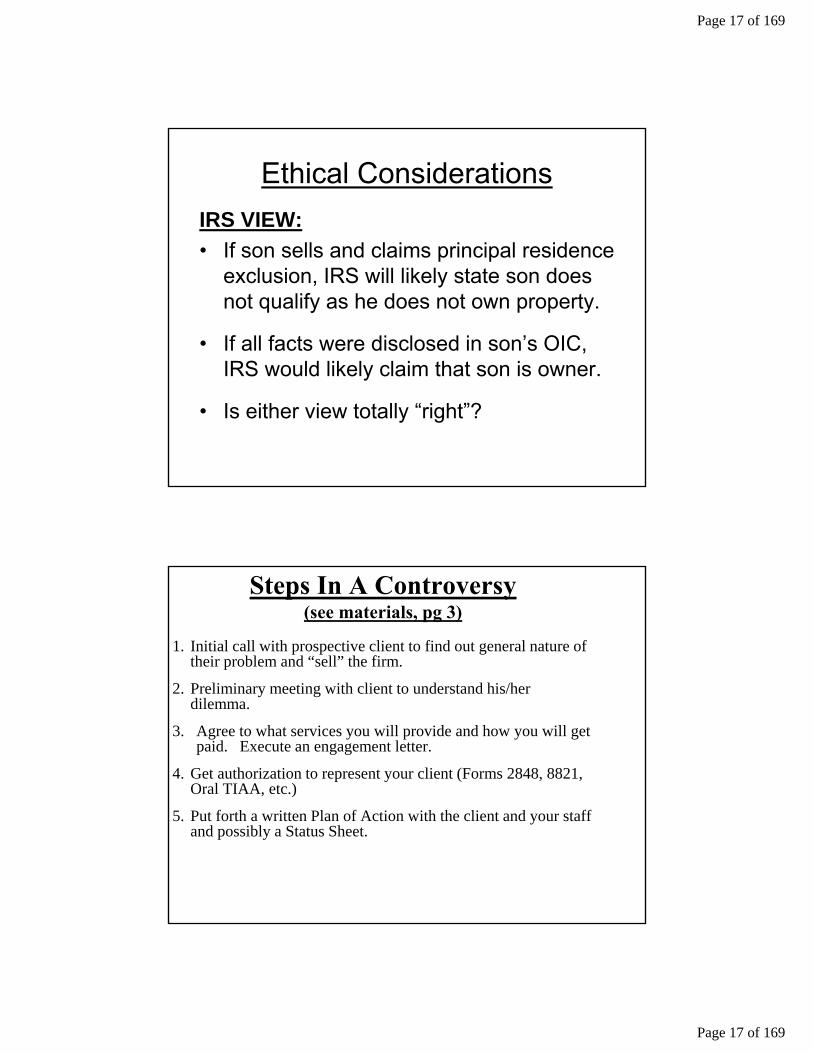

Ethical ConsiderationsIRS VIEW:

• If son sells and claims principal residence exclusion, IRS will likely state son does not qualify as he does not own property.

• If all facts were disclosed in son’s OIC, IRS would likely claim that son is owner.

• Is either view totally “right”?

Steps In A Controversy (see materials, pg 3)

1. Initial call with prospective client to find out general nature of their problem and “sell” the firm.

2. Preliminary meeting with client to understand his/her dilemma.

3. Agree to what services you will provide and how you will get paid. Execute an engagement letter.

4. Get authorization to represent your client (Forms 2848, 8821, Oral TIAA, etc.)

5. Put forth a written Plan of Action with the client and your staff and possibly a Status Sheet.

Page 17 of 169

Page 17 of 169

Form 8821• Allow Access to Account Information by

NON-CPAs!• Allows your secretary to get transcripts!• Future is for 8821 to Use E-Services

• Disclosure Authorization Still Closed Down! – Clients Get Transcripts?

• Clients – Getting Transcripts Online.

Page 18 of 169

Page 18 of 169

E. MARTIN DAVIDOFF & ASSOCIATES

CERTIFIED PUBLIC ACCOUNTANTS353 Georges Road - Suite K

E. Martin Davidoff, CPA, ESQ. P.O. Box 835 Robbin R. Weiner, CPA,CGMA Dayton, NJ 08810-0835

[email protected] _____________ TEL: 732-274-1600 FAX: 732-274-1666

FAX TRANSMITTAL SHEET

DATE: Feb 1, 2016 TIME:

PLEASE DELIVER THE FOLLOWING PAGES TO:NAME: IRS - CAF

TELEPHONE NUMBER: 901-546-4176

TELECOPIER NUMBER: 901-546-4115

TOTAL NUMBER OF PAGES INCLUDING COVER: 4

Following you will find Form 2848 (Power of Attorney and Declaration of Representative)and Form 8821 (Tax Information Authorization) for John J. Doe to be input into the CAF system.

Please do not hesitate to contact E. Martin Davidoff if you should ha ve any questions orcomments.

Sincerely,

Sarah A. FieldsEnrolled Agent

IF YOU DO NOT RECEIVE ALL THE PAGES OR THERE IS A PROBLEM, PLEASE CALL (732) 274-1600 ANDASK FOR SARAH.

G Confirmed by: _________

Page 19 of 169

Page 19 of 169

Form 2848Department of the Treasury Internal Revenue Service

(Rev. Dec. 2015)

Power of Attorney and Declaration of Representative

Information about Form 2848 and its instructions is at www.irs.gov/form2848.

OMB No. 1545-0150

For IRS Use Only

Received by:

Name

Telephone

Function

Date / /

Part I Power of Attorney Caution: A separate Form 2848 must be completed for each taxpayer. Form 2848 will not be honored for any purpose other than representation before the IRS.

1 Taxpayer information. Taxpayer must sign and date this form on page 2, line 7.

Taxpayer name and address Taxpayer identification number(s)

Daytime telephone number Plan number (if applicable)

hereby appoints the following representative(s) as attorney(s)-in-fact:

2 Representative(s) must sign and date this form on page 2, Part II.

Name and address

Check if to be sent copies of notices and communications

CAF No.

PTIN

Telephone No.

Fax No. Check if new: Address Telephone No. Fax No.

Name and address

Check if to be sent copies of notices and communications

CAF No.

PTIN

Telephone No.

Fax No. Check if new: Address Telephone No. Fax No.

Name and address

(Note: IRS sends notices and communications to only two representatives.)

CAF No.

PTIN

Telephone No.

Fax No. Check if new: Address Telephone No. Fax No.

Name and address

(Note: IRS sends notices and communications to only two representatives.)

CAF No.

PTIN

Telephone No.

Fax No. Check if new: Address Telephone No. Fax No.

to represent the taxpayer before the Internal Revenue Service and perform the following acts:

3 Acts authorized (you are required to complete this line 3). With the exception of the acts described in line 5b, I authorize my representative(s) to receive and inspect my confidential tax information and to perform acts that I can perform with respect to the tax matters described below. For example, my representative(s) shall have the authority to sign any agreements, consents, or similar documents (see instructions for line 5a for authorizing a representative to sign a return).

Description of Matter (Income, Employment, Payroll, Excise, Estate, Gift, Whistleblower, Practitioner Discipline, PLR, FOIA, Civil Penalty, Sec. 5000A Shared Responsibility

Payment, Sec. 4980H Shared Responsibility Payment, etc.) (see instructions)

Tax Form Number (1040, 941, 720, etc.) (if applicable)

Year(s) or Period(s) (if applicable) (see instructions)

4 Specific use not recorded on Centralized Authorization File (CAF). If the power of attorney is for a specific use not recorded on CAF, check this box. See the instructions for Line 4. Specific Use Not Recorded on CAF . . . . . . . . . . . . . . .

5a Additional acts authorized. In addition to the acts listed on line 3 above, I authorize my representative(s) to perform the following acts (see instructions for line 5a for more information):

Authorize disclosure to third parties; Substitute or add representative(s); Sign a return;

Other acts authorized:

For Privacy Act and Paperwork Reduction Act Notice, see the instructions. Form 2848 (Rev.12-2015)

ISA

John J. Doe123 Main StreetAnywhere, NJ 08666

123-45-6789

732-274-1600 (ATTY)

E. Martin Davidoff, CPA, Esq.P.O. Box 835Dayton, New Jersey 08810-0835

X

0000-00-000RP00000001

732-274-1600732-274-1666

Robbin R. Weiner, CPAP.O. Box 835Dayton, New Jersey 08810-0835

0000-00-000RP00000002

732-274-1600732-274-1666

Melanie Cobb, CPAP.O. Box 835Dayton, New Jersey 08810-0835

0000-00-000RP00000003

732-274-1600732-274-1666

Sarah A. Fields, EAP.O. Box 835Dayton, New Jersey 08810-0835

0000-00-000RP00000004

732-274-1600732-274-1666

Income 10402005 through 2019All Years Included

Civil Penalty N/A01/01/2006 through 12/31/2019All Quarters Included

See attached for additional representatives (total 6 representatives)

**Each Spouse Executes Separate Powers **

NEW FORM Dec 2015! Page 20 of 169

Page 20 of 169

Form 2848 (Rev. 12-2015) Page 2

b Specific acts not authorized. My representative(s) is (are) not authorized to endorse or otherwise negotiate any check (including directing or accepting payment by any means, electronic or otherwise, into an account owned or controlled by the representative(s) or any firm or other entity with whom the representative(s) is (are) associated) issued by the government in respect of a federal tax liability.

List any other specific deletions to the acts otherwise authorized in this power of attorney (see instructions for line 5b):

6 Retention/revocation of prior power(s) of attorney. The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Internal Revenue Service for the same matters and years or periods covered by this document. If you do not want to revoke a prior power of attorney, check here . . . . . . . . . . . . . . . . . . . . . . . . . . YOU MUST ATTACH A COPY OF ANY POWER OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

7 Signature of taxpayer. If a tax matter concerns a year in which a joint return was filed, each spouse must file a separate power of attorney even if they are appointing the same representative(s). If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the legal authority to execute this form on behalf of the taxpayer.

IF NOT COMPLETED, SIGNED, AND DATED, THE IRS WILL RETURN THIS POWER OF ATTORNEY TO THE TAXPAYER.

Signature

Print Name

Date Title (if applicable)

Print name of taxpayer from line 1 if other than individual

Part II Declaration of Representative Under penalties of perjury, by my signature below I declare that:

• I am not currently suspended or disbarred from practice, or ineligible for practice, before the Internal Revenue Service;

• I am subject to regulations contained in Circular 230 (31 CFR, Subtitle A, Part 10), as amended, governing practice before the Internal Revenue Service;

• I am authorized to represent the taxpayer identified in Part I for the matter(s) specified there; and

• I am one of the following:

a Attorney—a member in good standing of the bar of the highest court of the jurisdiction shown below.

b Certified Public Accountant—licensed to practice as a certified public accountant is active in the jurisdiction shown below.

c Enrolled Agent—enrolled as an agent by the Internal Revenue Service per the requirements of Circular 230.

d Officer—a bona fide officer of the taxpayer organization.

e Full-Time Employee—a full-time employee of the taxpayer.

f Family Member—a member of the taxpayer’s immediate family (spouse, parent, child, grandparent, grandchild, step-parent, step-child, brother, or sister).

g Enrolled Actuary—enrolled as an actuary by the Joint Board for the Enrollment of Actuaries under 29 U.S.C. 1242 (the authority to practice beforethe Internal Revenue Service is limited by section 10.3(d) of Circular 230).

h Unenrolled Return Preparer—Authority to practice before the IRS is limited. An unenrolled return preparer may represent, provided the preparer (1) prepared and signed the return or claim for refund (or prepared if there is no signature space on the form); (2) was eligible to sign the return or claim for refund; (3) has a valid PTIN; and (4) possesses the required Annual Filing Season Program Record of Completion(s). See Special Rules and Requirements for Unenrolled Return Preparers in the instructions for additional information.

k Student Attorney or CPA—receives permission to represent taxpayers before the IRS by virtue of his/her status as a law, business, or accounting student working in an LITC or STCP. See instructions for Part II for additional information and requirements.

r Enrolled Retirement Plan Agent—enrolled as a retirement plan agent under the requirements of Circular 230 (the authority to practice before the Internal Revenue Service is limited by section 10.3(e)).

IF THIS DECLARATION OF REPRESENTATIVE IS NOT COMPLETED, SIGNED, AND DATED, THE IRS WILL RETURN THE POWER OF ATTORNEY. REPRESENTATIVES MUST SIGN IN THE ORDER LISTED IN PART I, LINE 2.

Note: For designations d-f, enter your title, position, or relationship to the taxpayer in the "Licensing jurisdiction" column.

Designation—Insert above letter (a–r).

Licensing jurisdiction (State) or other

licensing authority (if applicable).

Bar, license, certification, registration, or enrollment

number (if applicable). Signature Date

Form 2848 (Rev. 12-2015)

John J. Doe

a New Jersey 0101010101

b New Jersey 20CC00000000

b New Jersey 20CC00000001

c IRS 00100000-EA

T T Sign Here7**Note no PIN **

Page 21 of 169

Page 21 of 169

Form 8821(Rev. March 2015)

Department of the Treasury Internal Revenue Service

Tax Information AuthorizationInformation about Form 8821 and its instructions is at www.irs.gov/form8821.

Do not sign this form unless all applicable lines have been completed. Do not use Form 8821 to request copies of your tax returns

or to authorize someone to represent you.

OMB No. 1545-1165

For IRS Use Only

Received by:

Name

Telephone

Function

Date

1 Taxpayer information. Taxpayer must sign and date this form on line 7. Taxpayer name and address Taxpayer identification number(s)

Daytime telephone number Plan number (if applicable)

2 Appointee. If you wish to name more than one appointee, attach a list to this form. Check here if a list of additional appointees is attached

Name and address CAF No. PTIN Telephone No. Fax No.

Check if new: Address Telephone No. Fax No. 3 Tax Information. Appointee is authorized to inspect and/or receive confidential tax information for the type of tax, forms,

periods, and specific matters you list below. See the line 3 instructions. (a)

Type of Tax Information (Income, Employment, Payroll, Excise, Estate, Gift, Civil Penalty, Sec. 4980H Payments, etc.)

(b) Tax Form Number

(1040, 941, 720, etc.)

(c) Year(s) or Period(s)

(d) Specific Tax Matters

4 Specific use not recorded on Centralized Authorization File (CAF). If the tax information authorization is for a specific use not recorded on CAF, check this box. See the instructions. If you check this box, skip lines 5 and 6 . . . . . .

5 Disclosure of tax information (you must check a box on line 5a or 5b unless the box on line 4 is checked):

a If you want copies of tax information, notices, and other written communications sent to the appointee on an ongoing basis, check this box . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Note. Appointees will no longer receive forms, publications, and other related materials with the notices.b If you do not want any copies of notices or communications sent to your appointee, check this box . . . . . . .

6 Retention/revocation of prior tax information authorizations. If the line 4 box is checked, skip this line. If the line 4 box is not checked, the IRS will automatically revoke all prior Tax Information Authorizations on file unless you check the line 6 box and attach a copy of the Tax Information Authorization(s) that you want to retain. . . . . . . . . . . . .

To revoke a prior tax information authorization(s) without submitting a new authorization, see the line 6 instructions.

7 Signature of taxpayer. If signed by a corporate officer, partner, guardian, executor, receiver, administrator, trustee, or party other than the taxpayer, I certify that I have the authority to execute this form with respect to the tax matters and tax periods shown on line 3 above.

IF NOT COMPLETE, SIGNED, AND DATED, THIS TAX INFORMATION AUTHORIZATION WILL BE RETURNED.

DO NOT SIGN THIS FORM IF IT IS BLANK OR INCOMPLETE.

Signature Date

Print Name Title (if applicable)

For Privacy Act and Paperwork Reduction Act Notice, see instructions. Form 8821 (Rev. 3-2015)

ISA

John J. Doe123 Main StreetAnywhere, NJ 08666

123-45-6789

732-274-1600 (atty)

The Firm of E. Martin Davidoff, Attorney at LawP.O. Box 835Dayton, New Jersey 08810-0835

0300-00000R

732-274-1600732-274-1666

Income 1040 All Years Included N/A

Civil Penalty N/A All Quarters Included

X

John J. Doe

REFER TO IRM SECTION 21.3.7.5.1 (09-11-2015): "If a business entity is named as an appointee, this will include all employees of the named business entity and a list is not required.

Sign Here7T T

2005 through 2019

01/01/2006 hrough 12/31/2019

New Fom March 2015

**Each Spouse ExecutesSeparate Powers**

Page 22 of 169

Page 22 of 169

Excerpts from the Internal Revenue Manual at www.irs.gov

21.3.7.1 (09-11-2015) Third Party Authorization3. Different types of authorization authority are:

Representative - An individual that the taxpayer has authorized to represent them before theIRS. [EMD note: pertains to a valid Form 2848, Power of Attorney and Declaration ofRepresentative or Form 706, U.S. Estate Tax Return.]

Appointee - An individual person or business entity the taxpayer appoints to receive andinspect confidential tax return information. [EMD note: pertains to a valid Form 8821,Tax Information Authorization.]

Designee - An individual person that has been designated to receive and inspect confidentialtax return information via telephone or Check-box election on a tax return.

21.3.7.5 (09-11-2015)Form 2848, Power of Attorney and Declaration of Representative andForm 8821, Taxpayer Information Authorization Overview

1. Form 2848, Power of Attorney and Declaration of Representative can only be granted to anindividual eligible to practice before the Internal Revenue Service. For information onPowers of Attorney see IRS Publication 947, Practice Before the IRS and Power ofAttorney.

2. Form 8821, Tax Information Authorization, or equivalent, can appoint any third party toreceive and inspect account information for the tax matter(s) specified.

21.3.7.5.1 (09-11-2015) Essential Elements for Form 2848 and Form 8821 1. There are five essential elements needed to process the Form 2848 and/or Form 8821...4. Essential elements are:A. Essential element 1 The taxpayer's dated signature is required. An electronically signed,

printed or stamped signature is not acceptable..

EMD COMMENT: Form 8821,Tax Information Authorization, or equivalent, can designateany third party to receive and inspect account information for the tax matter(s) specified.

• Can be granted to an individual.• Can be granted to a business entity or firm (legal, accounting, tax preparation,

etc). When a business is the appointee, authority extends to the employees ofthe business.

Page 23 of 169

Page 23 of 169

Excerpts from the Internal Revenue Manual at www.irs.gov

(Continued)

When the taxpayer signs and dates the Form 2848 before the representative, the signaturedates of the taxpayer(s) and representative(s) must be within 45 days for domesticauthorizations...

B. Essential element 2 - Only applies to Form 2848. The representative's designationunder which he or she is authorized to practice before the IRS must be present. Inaddition, the representative must list the Licensing jurisdiction (state) or other licensingauthority and Bar, license, certification, registration or enrollment number, if applicable. The representative’s signature and date are also required. For multiple representativeslisted on the same form, only one signature date is required; however, all representativesmust sign the Form 2848.

C. Essential element 3 - Specific tax matter(s), i.e., type of tax or tax form number, isrequired.

D. Essential element 4 - Clear identification of the taxpayer, i.e., name, address, taxpayeridentification number is required. The presence of two of the three identifiers is sufficient.Research can be done to locate the third identifier.

E. Essential element 5 - Clear identification of the third party, i.e., name and address isrequired. A CAF number is not required.

Instructions for Form 2848 (Rev. December 2015)

& 8821 (Rev. March 2015)

Power of Attorney and Declaration of Representative (Form 2848)

Joint returns. Joint filers must now complete and submit separate individual to receiveand inspect your confidential tax information.

Tax Information Authorization (Form 8821)

Each individual and/or entity must now file and sign a separate Form 8821.

EMD COMMENT: Forms 8821, Tax Information Authorization, for the purpose of addressingtax matters, do not have to be received within 60 days of the taxpayer's dated signature. See IRM11.3.3.1.1(4), General Requirements for Disclosure to Designee . The taxpayer must sign anddate a TIA. The third party is not required to sign a TIA.

EMD COMMENT: Our firm’s practice for multiple years (on Forms 8821 or 2848) is to put,for example: “2003 through 2009

All Years Included”

Page 24 of 169

Page 24 of 169

Page 25 of 169

Page 25 of 169

Page 26 of 169

Page 26 of 169

Page 27 of 169

Page 27 of 169

Page 28 of 169

Page 28 of 169

Page 29 of 169

Page 29 of 169

Page 30 of 169

Page 30 of 169

Page 31 of 169

Page 31 of 169

E. MARTIN DAVIDOFF

ATTORNEY AT LAW353 Georges Road - Suite K

P.O. Box 835Dayton, NJ 08810-0835

[email protected]_____________TEL: 732-274-1600FAX: 732-274-1666

February 3, 2016

VIA CERTIFIED MAIL #7008281000011969999Internal Revenue ServiceACS SupportP.O. Box 57Bensalem, Pennsylvania 19020-0057

RE: Bob Turley SS#: 123-45-6789Forms 1040; 2012, 2013 and 2014 Forms 941: 3/31/13 through 9/30/14

To Whom It May Concern:

We represent the above-named Taxpayer and are in receipt of your Final Notice of Intent to Levy (Letter 1058) dated January 29, 2016 for the above-referenced Taxpayer for the above-referenced tax periods. To that end, please find enclosed Form 12153, Request for a Collection Due Process Hearing along with Form 2848 empowering me to act on behalf of the Taxpayer.

We respectfully request that our Collection Due Process Hearing be held in person with an Appeals Officerat the Newark, New Jersey, Philadelphia, Pennsylvania or New York City, New York Appeals Office of theInternal Revenue Service.

Thank you very much for your attention to this matter.

Very truly yours,

E. Martin Davidoff

EMD:rb

encls.

cc: Mr. Bob Turley (via first class mail and e-mail w/encls.)

Page 32 of 169

Page 32 of 169

Form 12153(Rev. 12-2013)

Request for a Collection Due Process or Equivalent Hearing

Form 12153 (Rev. 12-2013) www.irs.gov Department of the Treasury - Internal Revenue Service

Use this form to request a Collection Due Process (CDP) or equivalent hearing with the IRS Office of Appeals if you have been issued one of the following lien or levy notices:

• Notice of Federal Tax Lien Filing and Your Right to a Hearing under IRC 6320,• Notice of Intent to Levy and Notice of Your Right to a Hearing,• Notice of Jeopardy Levy and Right of Appeal,• Notice of Levy on Your State Tax Refund,• Notice of Levy and Notice of Your Right to a Hearing.

Complete this form and send it to the address shown on your lien or levy notice. Include a copyof your lien or levy notice to ensure proper handling of your request.

Call the phone number on the notice or 1-800-829-1040 if you are not sure about the correct address or if you want to fax your request.

You can find a section explaining the deadline for requesting a Collection Due Process hearing in this form's instructions. If you've missed the deadline for requesting a CDP hearing, you must check line 7 (Equivalent Hearing) to request an equivalent hearing.

1. Taxpayer Name: (Taxpayer 1)

Taxpayer Identification Number

Current Address

City State Zip Code

2. Telephone Number and Best Timeto Call During Normal BusinessHours

Home am. pm.

Work am. pm.

Cell am. pm.

3. Taxpayer Name: (Taxpayer 2)

Taxpayer Identification Number

Current Address(If Different from Address Above) City State Zip Code

4. Telephone Number and Best Timeto Call During Normal BusinessHours

Home am. pm.

Work am. pm.

Cell am. pm.

5. Tax Information as Shown on the Lien or Levy Notice (If possible, attach a copy of the notice)

Type of Tax (Income,Employment, Excise,etc. or Civil Penalty)

Tax Form Number(1040, 941, 720, etc)

Tax Period or Periods

ISA

Bob Turley

123-45-6789

123 Main Street

Anywhere NJ 08666

732-274-1600 6:00 X

Jane Turley

987-65-4321

732-274-1600 6:00 X

Income 1040 2012, 2013 & 2014

Employment 9413/31/13 through 9/30/14 ALL QUARTERS INCLUDED

(Attorney phone)

(Attorney phone)

Page 33 of 169

Page 33 of 169

Form 12153(Rev. 12-2013)

Request for a Collection Due Process or Equivalent Hearing

Form 12153 (Rev. 12-2013) www.irs.gov Department of the Treasury - Internal Revenue Service

6. Basis for Hearing Request (Both boxes can be checked if you have received both a lienand levy notice)

Filed Notice of Federal Tax Lien Proposed Levy or Actual Levy

7. Equivalent Hearing (See the instructions for more information on Equivalent Hearings)

I would like an Equivalent Hearing - I would like a hearing equivalent to a CDP Hearing if my request for a CDP hearing does not meet the requirements for a timely CDP Hearing.

8. Check the most appropriate box for the reason you disagree with the filing of the lien or the levy. See page 4 of this form for examples. You can add more pages if you don't have enough space.

If, during your CDP Hearing, you think you would like to discuss a Collection Alternative to the action proposed by the Collection function it is recommended you submit a completed Form 433A (Individual) and/or Form 433B (Business), as appropriate, with this form. See www.irs.govfor copies of the forms. Generally, the Office of Appeals will ask the Collection Function to review, verify and provide their opinion on any new information you submit. We will share their comments with you and give you the opportunity to respond.

Collection Alternative Installment Agreement Offer in Compromise I Cannot Pay Balance

Lien Subordination WithdrawalDischargePlease explain:

My Spouse Is Responsible Innocent Spouse Relief (Please attach Form 8857,Request for Innocent Spouse Relief, to your request.)

Other (For examples, see page 4)Reason (You must provide a reason for the dispute or your request for a CDP hearing will not be honored. Use asmuch space as you need to explain the reason for your request. Attach extra pages if necessary.):

9. Signatures I understand the CDP hearing and any subsequent judicial review will suspend the statutory period of limitations for collection action. I also understand my representative or I must sign and date this request before the IRS Office of Appeals can accept it. If you are signing as an officer of a company add your title (president, secretary, etc.) behind your signature.

SIGN HERE Taxpayer 1's Signature Date

Taxpayer 2's Signature (if a joint request, both must sign) Date

I request my CDP hearing be held with my authorized representative (attach a copy of Form2848)

Authorized Representative's Signature Authorized Representative's Name Telephone Number

IRS Use Only

IRS Employee (Print) Employee Telephone Number IRS Received Date

X

X

X

X

See Detailed Explanation Attached.

X

E. Martin Davidoff, CPA, Esq. 732-274-1600

Page 34 of 169

Page 34 of 169

Form 12153Request for a Collection Due Process Hearing

Bob & Janet Turley

Mr. & Mrs. Bob Turley (hereinafter the "Taxpayers") ha�� made several attempts to discussthis case with Mr. Pepitone. Mr. Pepitone has never provided the Taxpayers with a convenient timefor either of them to call Mr. Pepitone.

We believe this case can be easily handled through an installment agreement. Please note that we are aware that there are unfiled Form 941s for the first three quarters of 2014. All of these forms will be filed with Mr. Pepitone on or before March 1, 2016. At that time, we will make appropriate arrangements to enter into an installment agreement on behalf of the Taxpayer�. Please also be advised that it is the intent of the Taxpayer� to engage the services of a payroll tax service. Such a tax service would then impound the funds for payroll taxes upon the issuance of each paycheck.

Please note that the Taxpayers have been using the services of Mr. Tony Kubek for over 20 years. In the middle of 2013, Mr. Kubek retired. Although the Taxpayers have engaged the services of the successor company to Mr. Kubek, things have not quite been the same. The Taxpayers have now figured out how to handle all of these problems, with some assistance from our firm.

We respectfully request that our Collection Due Process Hearing be held in person with anAppeals Officer at the Newark, New Jersey��Philadelphia, Pennsylvania��or New York City, NewYork Appeals Office of the Internal Revenue Service.

Additional Notes Regarding forms 12153

1. Equivalent Hearings are no longer automatically provided if you do not qualify for astatutory CDP hearing. This is as a result of regulatory changes in the fall of 2006. If aCDP request is made more then one year beyond the original due date, then there will beno CDP hearing or equivalent thereto.

2. On May 25, 2007, President Bush signed The Small Business and Work Opportunity TaxAct (P.L. 110-28). Under new Section 6330(h) added by that legislation, a CDP hearingis no longer an entitlement if the particular taxpayer had previously requested a CDPhearing with respect to unpaid employment taxes arising in the two-year period beforethe beginning of the taxable period to which the employment tax levy is served.

Page 35 of 169

Page 35 of 169

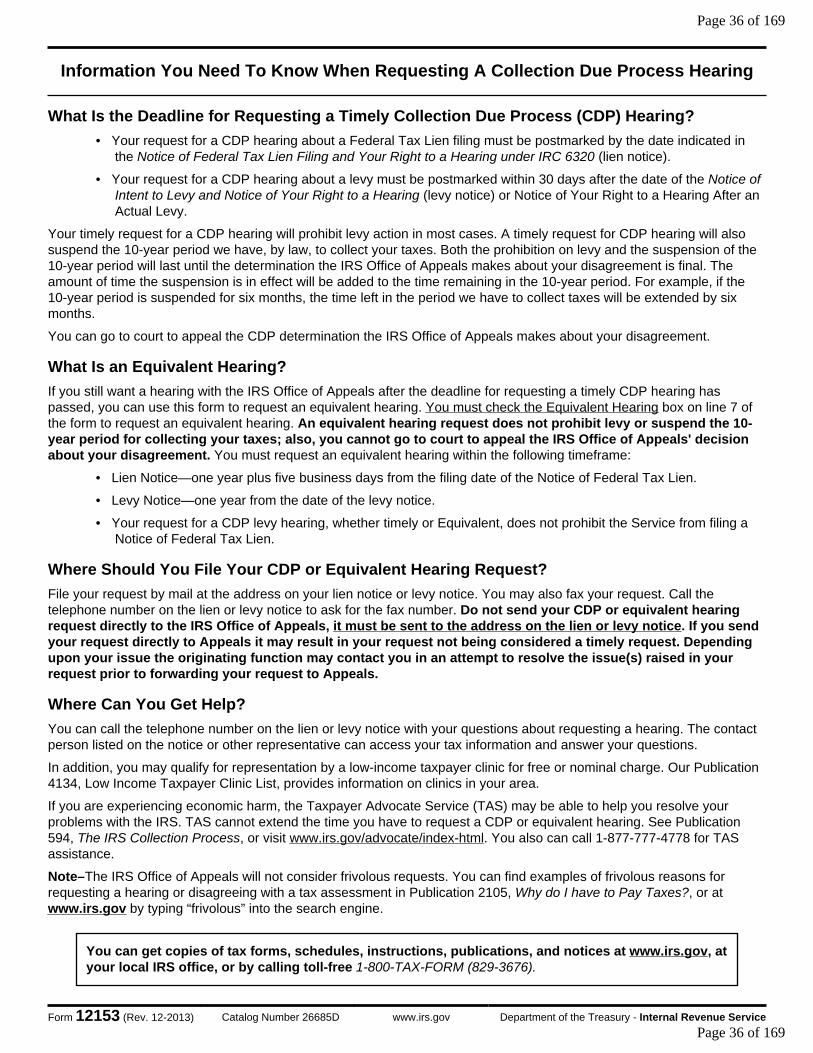

Information You Need To Know When Requesting A Collection Due Process Hearing

Form 12153 (Rev. 12-2013) Catalog Number 26685D www.irs.gov Department of the Treasury - Internal Revenue Service

What Is the Deadline for Requesting a Timely Collection Due Process (CDP) Hearing?

• Your request for a CDP hearing about a Federal Tax Lien filing must be postmarked by the date indicated in the Notice of Federal Tax Lien Filing and Your Right to a Hearing under IRC 6320 (lien notice).

• Your request for a CDP hearing about a levy must be postmarked within 30 days after the date of the Notice of Intent to Levy and Notice of Your Right to a Hearing (levy notice) or Notice of Your Right to a Hearing After an Actual Levy.

Your timely request for a CDP hearing will prohibit levy action in most cases. A timely request for CDP hearing will also suspend the 10-year period we have, by law, to collect your taxes. Both the prohibition on levy and the suspension of the 10-year period will last until the determination the IRS Office of Appeals makes about your disagreement is final. The amount of time the suspension is in effect will be added to the time remaining in the 10-year period. For example, if the 10-year period is suspended for six months, the time left in the period we have to collect taxes will be extended by six months.

You can go to court to appeal the CDP determination the IRS Office of Appeals makes about your disagreement.

What Is an Equivalent Hearing?

If you still want a hearing with the IRS Office of Appeals after the deadline for requesting a timely CDP hearing has passed, you can use this form to request an equivalent hearing. You must check the Equivalent Hearing box on line 7 of the form to request an equivalent hearing. An equivalent hearing request does not prohibit levy or suspend the 10-year period for collecting your taxes; also, you cannot go to court to appeal the IRS Office of Appeals' decision about your disagreement. You must request an equivalent hearing within the following timeframe:

• Lien Notice—one year plus five business days from the filing date of the Notice of Federal Tax Lien.

• Levy Notice—one year from the date of the levy notice.

• Your request for a CDP levy hearing, whether timely or Equivalent, does not prohibit the Service from filing a Notice of Federal Tax Lien.

Where Should You File Your CDP or Equivalent Hearing Request?

File your request by mail at the address on your lien notice or levy notice. You may also fax your request. Call the telephone number on the lien or levy notice to ask for the fax number. Do not send your CDP or equivalent hearing request directly to the IRS Office of Appeals, it must be sent to the address on the lien or levy notice. If you send your request directly to Appeals it may result in your request not being considered a timely request. Depending upon your issue the originating function may contact you in an attempt to resolve the issue(s) raised in your request prior to forwarding your request to Appeals.

Where Can You Get Help?

You can call the telephone number on the lien or levy notice with your questions about requesting a hearing. The contact person listed on the notice or other representative can access your tax information and answer your questions.

In addition, you may qualify for representation by a low-income taxpayer clinic for free or nominal charge. Our Publication 4134, Low Income Taxpayer Clinic List, provides information on clinics in your area.

If you are experiencing economic harm, the Taxpayer Advocate Service (TAS) may be able to help you resolve your problems with the IRS. TAS cannot extend the time you have to request a CDP or equivalent hearing. See Publication 594, The IRS Collection Process, or visit www.irs.gov/advocate/index-html. You also can call 1-877-777-4778 for TAS assistance.

Note–The IRS Office of Appeals will not consider frivolous requests. You can find examples of frivolous reasons for requesting a hearing or disagreeing with a tax assessment in Publication 2105, Why do I have to Pay Taxes?, or at www.irs.gov by typing “frivolous” into the search engine.

You can get copies of tax forms, schedules, instructions, publications, and notices at www.irs.gov, at your local IRS office, or by calling toll-free 1-800-TAX-FORM (829-3676).

Page 36 of 169

Page 36 of 169

Information You Need To Know When Requesting A Collection Due Process Hearing

Form 12153 (Rev. 12-2013) Catalog Number 26685D www.irs.gov Department of the Treasury - Internal Revenue Service

What Are Examples of Reasons for Requesting a Hearing?

You will have to explain your reason for requesting a hearing when you make your request. Below are examples of reasons for requesting a hearing.

You want a collection alternative— “I would like to propose a different way to pay the money I owe.” Common collection alternatives include:

• Full payment—you pay your taxes by personal check, cashier's check, money order, or credit card.

• Installment Agreement—you pay your taxes fully or partially by making monthly payments.

• Offer in Compromise—you offer to make a payment or payments to settle your tax liability for less than the full amount you owe.

“I cannot pay my taxes.” Some possible reasons why you cannot pay your taxes are: (1) you have a terminal illness or excessive medical bills; (2) your only source of income is Social Security payments, welfare payments, or unemployment benefit payments; (3) you are unemployed with little or no income; (4) you have reasonable expenses exceeding your income; or (5) you have some other hardship condition. The IRS Office of Appeals may consider freezing collection action until your circumstances improve. Penalty and interest will continue to accrue on the unpaid balance.

You want action taken about the filing of the tax lien against your property—You can get a Federal Tax Lien released if you pay your taxes in full. You also may request a lien subordination, discharge, or withdrawal. See www.irs.gov for more information.

When you request lien subordination, you are asking the IRS to make a Federal Tax Lien secondary to a non-IRS lien. For example, you may ask for a subordination of the Federal Tax Lien to get a refinancing mortgage on your house or other real property you own. You would ask to make the Federal Tax Lien secondary to the mortgage, even though the mortgage came after the tax lien filing. The IRS Office of Appeals would consider lien subordination, in this example, if you used the mortgage proceeds to pay your taxes.

When you request a lien discharge, you are asking the IRS to remove a Federal Tax Lien from a specific property. For example, you may ask for a discharge of the Federal Tax Lien in order to sell your house if you use all of the sale proceeds to pay your taxes even though the sale proceeds will not fully pay all of the tax you owe.

When you request a lien withdrawal, you are asking the IRS to remove the Notice of Federal Tax Lien (NFTL) information from public records because you believe the NFTL should not have been filed. For example, you may ask for a withdrawal of the filing of the NFTL if you believe the IRS filed the NFTL prematurely or did not follow procedures, or you have entered into an installment agreement and the installment agreement does not provide for the filing of the NFTL. A withdrawal does not remove the lien from your IRS records.

Your spouse is responsible—“My spouse (or former spouse) is responsible for all or part of the tax liability.” You may believe that your spouse or former spouse is the only one responsible for all or a part of the tax liability. If this is the case, you are requesting a hearing so you can receive relief as an innocent spouse. You should complete and attach Form 8857, Request for Innocent Spouse Relief, to your hearing request.

Other Reasons—“I am not liable for (I don't owe) all or part of the taxes.” You can raise a disagreement about the amount you owe only if you did not receive a deficiency notice for the liability (a notice explaining why you owe taxes—it gives you the right to challenge in court, within a specific timeframe, the additional tax the IRS says you owe), or if you have not had another prior opportunity to disagree with the amount you owe.

“I do not believe I should be responsible for penalties.” The IRS Office of Appeals may remove all or part of the penalties if you have a reasonable cause for not paying or not filing on time. See Notice 746, Information About Your Notice, Penalty and Interest for what is reasonable cause for removing penalties.

“I have already paid all or part of my taxes.” You disagree with the amount the IRS says you haven't paid if you think you have not received credit for payments you have already made.

See Publication 594, The IRS Collection Process, for more information on the following topics: Installment Agreements and Offers in Compromise; Lien Subordination, Discharge, and Withdrawal; Innocent Spouse Relief; Temporarily Delay Collection; and belief that tax bill is wrong.

Page 37 of 169

Page 37 of 169

Additional Notes Regarding CDP Request

1. Need Draft of form 433- A to Transfer Cases from Service Center Appeals Offices BEFORE transfer will take place to allow in-person appeals

2. Knee-Jerk reaction to issuing form 1058 in the field…this is what the IRS managers want.

3. Reversing premature 1058 issuances from the Service Center…for cause (i.e. We Sent in the 433 package!)

Page 38 of 169

Page 38 of 169

`

E. Martin Davidoff, CPA, Esq. Chapter 4

IRS Appeals in Collection Matters

I R S

R E PRESENTATIoN

AdvISoR

T he most underutilized arm of the Internal Revenue Service with respect to Taxpayer collection

issues is the IRS Office of Appeals (“Appeals”). This office can be used to appeal threatened levies and liens, denials of installment agreements, and denied offers to compromise one’s tax. Understanding the processes and tools available is critical to a practitioner’s success in this specialty.

Generally, Appeals functions are divided into two categories: i) assessment issues and ii) collection issues. Appeals’ officers have become specialized and most officers deal with either assessment issues or collection issues, but not both. Appeals of examination findings, trust fund assessments, and denials of claims for refund all fall within the area of assessment issues. Appeals’ officers working on collection issues are often referred to as Settlement Officers.

Other than appeals of Offers in Compromise (“OICs”), there are two primary procedures to appeal a Tax Collection matter:

■■ Collection Due Process (“CDP”) Appeals (form 12153)■■ The Collection Appeals Program

(“CAP”; form 9423)

CAP is the only methodology that can be used to head off the filing of a Notice of Federal Tax Lien (“NFTL”). The CDP Appeal can only be filed in response to the filing of the NFTL or when a Levy is threatened by the IRS. That threat of levy often comes in the form of the Letter 1058 which states prominently, “NOTICE OF INTENT TO LEVY AND NOTICE OF YOUR RIGHT TO A HEARING.” Providing advance notice of levy is required by Internal Revenue Code (“IRC”) §6330. Such notices are

always sent via Certified Mail. OICs are appealed through a process clearly delineated on OIC rejection letters and will not be discussed in this article.

CDP Hearings The biggest mistake made by taxpay-ers and practitioners alike is not respond-ing to the IRC §6330 notice within the 30 days required to fully protect the tax-payer’s rights. In such hearings, Appeals is empowered to consider ALL collection alternatives. Responding to the §6330 notice is relatively simple. One need only complete the form 12153. The most re-cent revision (March of 2011) provides comprehensive guidance. Considerations when dealing with a §6330 notice and submitting form 12153 are set forth be-low, some of which will be more fully dis-cussed in the next edition of this column.

1 . Determine whether or not to respond within 30 days. The IRS has developed a process to consider untimely-filed requests for CDP hearings. Such hearings are administrative, not stat-utory. Therefore:

a.) The statute of limitations for the IRS to collect the tax con-tinues to run; and

b.) The Taxpayer does not have the right to pursue the matter in the U.S. Tax Court.

IRS policies are that such adminis-trative hearings should be equiva-lent to the CDP hearing and, as do CDP hearings, should consider all collection alternatives. Accordingly, such administrative hearings have been named “Equivalent Hearings,” which can be requested at item #7 of

form 12153 up to 1 year after the tax-payer is provided the §6330 Notice.

So, if a client is not willing to take the matter to Tax Court, would there be any reason to file within 30 days and suspend the running of the statute of limita-tions? One could argue (correctly, I believe), that the possibility of a U.S. Tax Court appeal from the CDP hearing puts added pressure on Appeals to resolve the matter.

Often, the 30-day period is gone before the practitioner gets in-volved. So, it is important for a prac-titioner to obtain IRS account tran-scripts to see when the §6330 notice was issued so that the time to file an Equivalent Hearing does not pass by without consideration of action.

When one is deep into the 10-year IRS limitations period to col-lect the tax, filing for a CDP hearing may be considered risky as the stat-ute may expire without the hearing request. This has become rare, as the IRS has become more consistent about issuing notices of intent to levy early in the collection process.

Be careful about missing dead-lines. Sometimes practitioners will call the Revenue Officer and/or their manager upon the receipt of a Let-ter 1058 or other notice of intent to levy. While negotiating or playing telephone tag, the deadline to appeal could go by and weaken your nego-tiating position significantly.

2. Consider requesting a face-to-face/in-person conference at a local Appeals of-fice. Generally, our office requests a face-to-face hearing on all form 12153 filings (also referred to as “CDP requests”). Why not? Our

E. Martin Davidoff, CPA, Esq. is a sole proprietor in Dayton, NJ, with more than 30 years experience practicing as a CPA and tax attorney. He founded the IRS Tax Liaison Committee of the American Association of Attorney-CPAs, and is a past president of the AAA-CPA.

10 I N O V E M B E R / D E C E M B E R 2 0 11 www.taxcpecourse.com

CPA_NovemberDecember_11.indd 10 11/10/11 1:24 PM

Page 39 of 169

Page 39 of 169

experience is that we secure bet-ter results when meeting in person. Our office is located in central New Jersey. Accordingly, we find any of three offices (Newark, New York City, or Philadelphia) relatively convenient. I believe our flexibil-ity regarding location makes it easier for the IRS to grant our requests.

More information on face-to-face conferences for CDP hearing requests, and the IRS reluctance to grant re-quests for such hearings, will be found in the next edition of this column.

3. Seek Penalty Abatements. Whenever there is money due to the IRS, the abatement of penalties should be a consideration. Even if you cannot elaborate on the detail of reasonable cause within the form 12153 attach-ment, you should request abatement and provide an overview of the rea-sonable causes and state clearly that you are willing to provide additional substantiation.

4. Clearly State the Desired ResultsYou want to make clear what you want the Appeals Officer to do. Accord-ingly, your attachment should state the desired results. That attachment should also indicate why you were not able to resolve the problem (i.e. The Revenue Officer sent the threat to levy without ever calling the taxpayer or his/her representative), provide all pertinent facts, and identify the po-tential issues for consideration.

5. Consider requesting that the hearing be recorded. To preserve a record for the Tax Court, you may wish to consid-er requesting that the hearing be re corded. You have the right to do so. By making this request, you will be as-sured that the Appeals manager will be in attendance. I have not used this tool personally, but I do know it is being used regularly by practitioners, partic-ularly in larger, more complex cases.

6. Other technicalities. Include state-ments in your attachment that make it clear that:■■ You reserve the right to amend

the request;

■■ You reserve the right to supplement the CDP request■■ There shall be no ex-parte

communications (communication to influence a decision-making official off the record) between Appeals and other IRS employees working on the case, without your express written permission■■ Don’t forget to include your

power of attorney for the client, form 2848

7. Who attends? As with nearly all of my representation before the IRS, I will attend alone or with a member of my staff. In the rare instances that my cli-ent attends an IRS conference/hear-ing, I make the decision. I have had situations wherein my clients insisted on attending. In such instances, con-sideration should be given to whether or not to retain the client. My pur-pose in bringing staff is to either pro-vide training, have someone along with me who is more knowledgeable of the factual nuances and intricacies of the case, and/or someone whose personality will assist in the resolu-tion of the matter.

CAP AppealsCAP Appeals enable a taxpayer/

practitioner to Appeal a specific action or proposed action of the IRS. Some considerations with respect to CAP Appeals:

1. Only the specific action or proposed action is evaluated by the Settlement Officer. The Settlement Officer will not consider all collection alternatives. However, some Settlement Officers will tell you that they are only doing an “administrative review” to determine whether the IRS followed the requisite procedures in deciding to take or threaten the action being appealed. Under the Internal Revenue Manual (“IRM”), this is simply not true in my opinion. The Settlement Officer is to put himself/herself in the position of the IRS employee and determine whether the action is the appropriate action to be taken considering all facts and circumstances.

2. CAP is an expedited procedure in which the Settlement Officer is required to have the hearing within five days of his/her receipt. However, one never knows when the officer will actually “receive” the case. The five-day rule brings on unfair and extraordinary results, often under the pretense of doing the Taxpayer a ‘favor’ by expediting the case. For example, you could receive a call from a Settlement Officer, have what you believe is a preliminary conversation to the hearing, and then be told that the Settlement Officer is finding in favor of the IRS action. Effectively, you may not have realized that you had the hearing during that conversation! Accordingly, you need to clarify from the beginning in all conversations whether you are having the hearing or just trying to set up a mutually convenient time for one. Also, if you are planning to be away from the office for an extended period, you may want to contact Appeals to make sure that the hearing is not sched-uled while you are unavailable. The IRS will consider your unavail-ability for more than five days, effectively, a forfeiture of your hearing rights.

3. Normally, face-to-face hearings will be permitted in local IRS offices. However, it is very rare that a Service Center CAP will be transferred for a face-to-face hearing.

4. The CAP Program is used to appeal rejections of installment agreements (IRC §7122(e)) and proposed terminations of installment agreements (IRC 6159(e)).

The details of IRS procedures and practices relating to Appeals change frequently. For that reason, you should regularly refer to Section 8 of the IRM, which covers the Appeals function of the IRS and can be found online at: http://www.irs.gov/irm/part8/index.html. See also IRS Publications 594 and 1660.

Contact E. Martin Davidoff, CPA, Esq. at [email protected] and his firm’s Web site can be found at www.taxattorneycpa.com.

By Tax Practitioners ... For Tax Practitioners N O V E M B E R / D E C E M B E R 2 0 11 I 11

CPA_NovemberDecember_11.indd 11 11/10/11 1:24 PM

Page 40 of 169

Page 40 of 169

IRS Liens 1. CDP’s available only AFTER Lien Filings

2. Only CAP Appeals can avoid Liens *

3. IR Release 2011-20 (2/24/2011)• See Letter to Commissioner/EMD Article

• Encourages DDIAs

• Allows withdrawal of liens <$25,000 individuals

4. Current Policy is not to file Liens for those entering into DDIAs of $50,000 or less assessed

5. Recent Rules on Withdrawals of Liens

*See IRM 5.12.6.2 ¶2 “CAP is the only appeal available before the NFTL filing. Taxpayers who dispute the proposed filing of the NFTL should be advised of appeal rights under CAP.”

Tools in Dealing with the IRS (see materials, page 4)

Office of Appeals2. Form 12153, Collection Due Process Hearing (Pgs 25 through 32 in materials.)

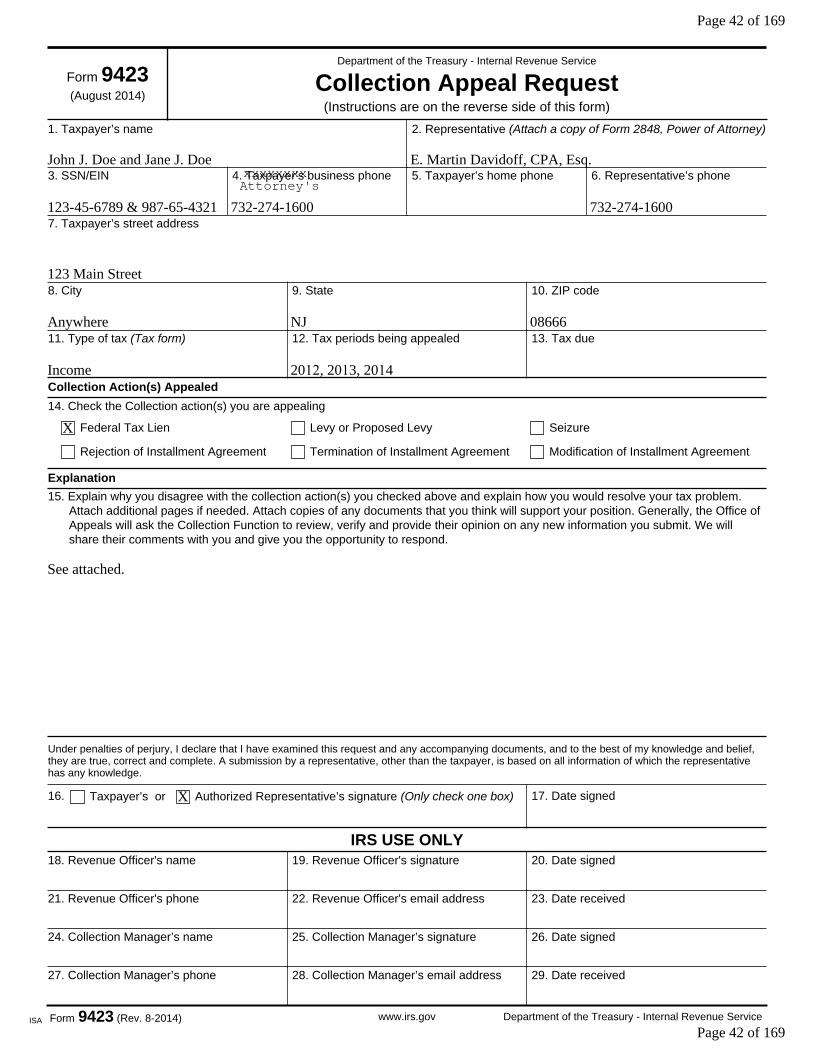

3. Form 9423, Collection Appeal Request (See pages 36 through 40. New Form as of August 2014)

4. Appealing denials of Penalty Abatement requests & Examination Findings

In-Person Conferences – Developing Relationships

Page 41 of 169

Page 41 of 169

Form 9423 (Rev. 8-2014) Department of the Treasury - Internal Revenue Servicewww.irs.gov

1. Taxpayer’s name 2. Representative (Attach a copy of Form 2848, Power of Attorney)

3. SSN/EIN 4. Taxpayer’s business phone 5. Taxpayer’s home phone 6. Representative’s phone

7. Taxpayer’s street address

8. City 9. State 10. ZIP code

11. Type of tax (Tax form) 12. Tax periods being appealed 13. Tax due

Collection Action(s) Appealed

14. Check the Collection action(s) you are appealing

Federal Tax Lien Levy or Proposed Levy Seizure

Rejection of Installment Agreement Termination of Installment Agreement Modification of Installment Agreement

Explanation

15. Explain why you disagree with the collection action(s) you checked above and explain how you would resolve your tax problem.Attach additional pages if needed. Attach copies of any documents that you think will support your position. Generally, the Office ofAppeals will ask the Collection Function to review, verify and provide their opinion on any new information you submit. We willshare their comments with you and give you the opportunity to respond.