e i p m annual conference. the expectations of arcelor · e i p m annual conference. the...

TRANSCRIPT

E I P M Annual Conference.The expectations of ARCELOR

December 1rst, 2005

J. CHARDONSenior VP Industrial Services

ARCELOR PURCHASING

The ARCELOR Group

2004, a year of expansionInternationalisation is one of the main platforms supporting thedevelopment of Arcelor. In 2004, with the acquisition and consolidation of Acindar and CST, Arcelor became the number one steel group in Latin America.

Argentina

Arcelor holds 73% of Acindar capital.

Brazil

Arcelor holds 73% of capital and consolidates CST.

Operations begin at Vega Do Sul factory

India

Joint-venture with the Indian group Jindal to create a company that specialises in the production of precision laminates.

China

Joint venture with Baosteel and Nippon Steel for automotive products.

Joint venture with the Korean company Kiswireto construct a 2nd wire drawing plant.

Great Britain

Repurchase of sheet pile commercial activity at Corus

Belgium

Start of construction of Charleroi electric steel plant (€ 240 Minvestment)

Andean zone/Central AmericaLCS/ FCS acquisition

(downstream Brazil, etc.)

IndiaSlabs plant investigation

TurkeyComplete European

scheme with Erdemir

Russia/UkrainePartner or acquisition

in Flat Carbon andLong Carbon China

Several long and flat carbon contacts for stake

acquisition in existinggreenfield companies or

projects– with Chinese partners

Market opportunity

Semis competitiveness

The ARCELOR Group growth strategy

NaftaAutomotive presence

Downstream operations for CSTEntry of A3S

South America/BrazilInternal organic growth

of Arcelor companiesNew slabs capacity

Entry of A3S

Distribution of turnover 2004

Turnover by sector (in millions of euros) Total: 30.176 billion euros

Turnover by geographical zone

Flat carbon steel

A3S

Long carbon steel

Stainless steel

16 139

8 267

6 221

4 577

53.5%

27.4%

20.6%

15.2%

South America 7.1%

North America 7.6%Europe 77.5%

Rest of world 7.8%

Arcelor,leader of the worldwide steel industry transformation

Turnover

Production

Gross operational result

Net result (group)

Employees

: 30 billion euros

: 47 million tonnes of steel

: 4,341 million euros

: 2,314 million euros

: 95,000 people in more than 60 countries

Key figures 2004

ARCELOR's ambition

ImproveEBITDA

2,000 Million 2,000 Million €€

In 3 yearsIn 3 years

By focusing on greater efficiencyBy focusing on greater efficiency

Objective 2005: to pursue the strategy of a global player

The group will pursue external growth by targeting first and foremost those regions in the world offering the greatest development potential. Priority will be given to expansion in countries within the BRIC zone: Brazil-Russia-India-China

The stated objective is to increase the Group's presence in these countries to 50% of turnover, compared with the current 23%.

Factors supporting this growth will include Arcelor'sambitious commercial policy together with the offer of innovative steel solutions.

ARCELOR PURCHASING

ARCELOR PURCHASING

ENERGY TRANSPORT & LOGISTICS

J.L. SANCHEZ

INDUSTRIAL PRODUCTS

J.M. DECRUYENAEREPh. CARON

RAW MAT.O. DUBREUIL

A. GARCIA

SCRAPY. SCHRAUBF. BARONE

HUMAN RESOURCESD. de ROTALIER

QUALITY AND INFORMATION SYSTEMS

S. DELFANNE

INVEST and ITD. VACHER

LOGISTICS AND INTERNATIONAL DEVELOPMENT SUBSIDIARIES

D. FRANCON

GLOBAL ALLIANCEJ. LLERA

MANAGERARCELOR PURCHASING

A. BOUCHARD

MANAGEMENT CONTROLPh. BIQUILLON

INDUSTRIAL SERVICES

J. CHARDONG. BECKERS

STRATEGYY. KOEBERLE

J.P. REBOUL

AP: 200Of which AP PARIS : 60

LOCAL : 600TOTAL : 800

TURN

GUARANTEED TURNOVER: 16 billion €/year

MANAGEMENT MONITORING

Ph. BIQUILLON

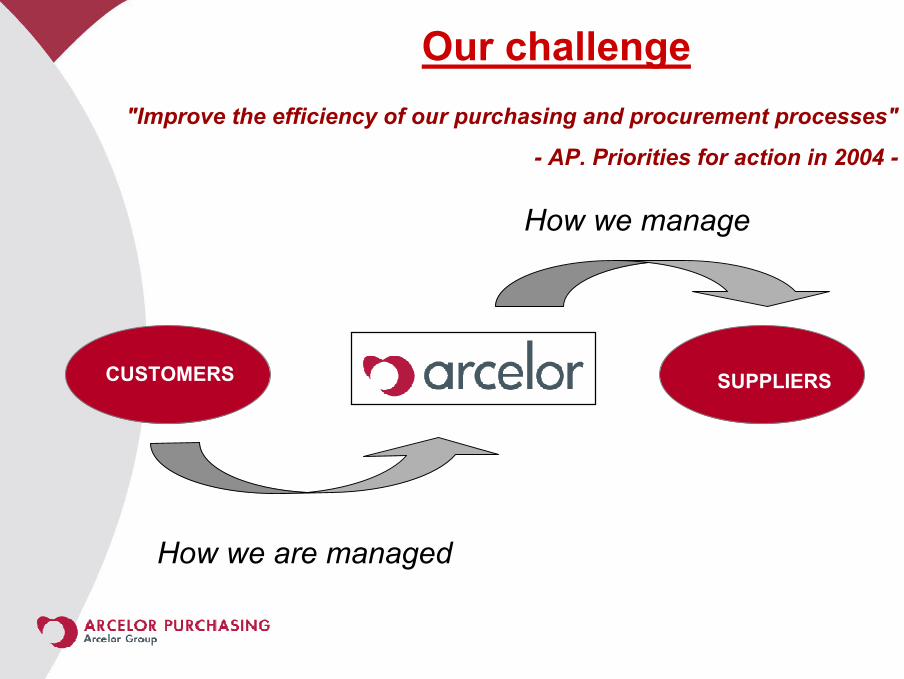

How we are managed

Our challenge"Improve the efficiency of our purchasing and procurement processes"

- AP. Priorities for action in 2004 -

CUSTOMERS

How we manage

SUPPLIERS

Supplier Management

HOW WE CAN IMPROVE THE WAY WE MANAGE RELATIONSHIPS WITH OUR SUPPLIERS

T/O, ARCELOR market share

Safety, environment, technical, commercial

and financial expertise, service-orientated,

continuous progress Availability, quality, dependence in relation to ARCELOR, financial well-being

Supplier Management

Information sharing in ARCELOR

Added value

OP2Supplier

Management

OP2Supplier

Management

OP2Measure of value created/destroyed

Market participation by

supplier in ARCELOR

Supplier performance Risk

analysis

OP4

OP4

SupplierMonitoring

OP2

OP2

Market, strategy, products, cost structure, sustainable

development, etc.

SupplierKnowledge

Technical, economic, geographical

Supplier competence

OP2

OP2

The Industrial Services Category

INDUSTRIAL SERVICES

Category Manager (CM)

Reporting, Statistics and Administration

0.9 E. Malis G.Dey1

J. Chardon1

G. Beckers

Category Mgr Asst. (CMa)

1

Admin Assistant (AS)

0,2 M. Wouters

Fleet managementTravel

1 Ph. BergerA. Ruffin

Industrial operations (LB)

Industrial servicesMaintenance (LB)

G. Amann

Financial/legal support (AN)

1 S. Villard

Marketing Suppliers

D. Butgen0,5

Operations Vega

J. Chardon

P. Vidal

Trans activities(LB)

1 1

Multiservice projects (LB)

S. Laleu0,7

CM

LBGBANFSAS

Category Manager/DeputyLead BuyerGlobal Buyer/BuyerAnalyst/Buying Ass.Functional SupportAdministr. Assist

Maintenance services (LBa)

Ph. Pilière1

Benchmark

(GB)

L.O. Coudeyre0,2

1

€ 0.15 B € 0.4 B€ 1.2 B

€ 0.2 B

€ 0.6 B

€ 2.55 billion/year

INDUSTRIAL SERVICES

One of the 7 departments within ARCELOR PURCHASING

18 buyers + 3 support positions

6 nationalities

6 different geographical locations

Annual GOM: € 35 million/year2 million €/year and per FTE€ 40 K/week

Coaching and involvement in local management

100 projects currently being researched

INDUSTRIAL SERVICES

Breakdown into sub-categories:Acid regenerationWater treatmentDomestic transportHarbour operationsUtilities managementScrap yard operationsTreatment of slag from blast furnace and steel worksRefractory servicesPackingChromium plating and cylinder grindingTreatment of slabs: repairing cracks, oxygen cutting, etc.Treatment of waste: ordinary and technicalDust and fumesSocial building and industrial cleaningGlobal contracts: caretaking, industrial lifts, transformers, etc.MaintenanceTemp.Etc…..

Each buyer is responsible for at least 2 sub-categories

Essential technical training

INDUSTRIAL SERVICES

CORPORATE thinking on ARCELOR core business

Our thinking is cross-sector within an "industrial basin" logic

As regards the nature of the steel industry, we constantly have to strike a balance between being competitive in the short term whilst maintaining relationships for the long term

Sub-contracting/outsourcing policy required to create value and not just to sustain it (training, recruitment, supply of investment)

Highly specific purchasing process aimed at greater professionalism:Project method: KO meeting, BP, Make or Buy analysis, Risk analysis, Award contract

Technical and financial training essential for buyers with strictly commercial competence being less important

Active involvement in the Group's transformation

INDUSTRIAL SERVICES - OBJECTIVES

Generalisation of PROJECT method: But with the obligation to achieve an initial result within 3 monthsPromote joint projects with Investment Purchasing and IndustrialProducts departments: outsourcing, MRO, items made to measure, etc.Duplication of “Best practices”Development of benchmarks with industries outside the steel industryPragmatic sourcing in countries with lower costsEUROPE will remain as our action zone for some time to comeBuyer involvement in drawing up specifications through to awarding contractsParamount importance of safety

INDUSTRIAL SERVICES - TOOLSTotal involvement regarding scope definitionBusiness Plan"Make or Buy" analysisRisk analysisContract monitoring performance chartSummary contract for signatureKey Performance Indicators (KPI)

OP1 : STRATEGYOP2 : SUPPLIER MANAGEMENTOP3 : NEGOTIATIONOP4 : AWARD

Development of ratios

NEGOTIATION BECOMES SECONDARY

ACTION BY THE BUYER DOES NOT CEASE UNTIL THE CONTRACT IS AWARDED

INDUSTRIAL SERVICES -CHARACTERISTICS

We are working for the long term: from 3 to 15 yearsWe are seeking added value for the long termThe jobs we have are similar to those of our suppliers: because of cultural differences between the different companies within the Group, we often find it difficult to "sell" a contract, even if we bring all competencies into one project teamWe do not always precisely determine production data

IN CONCLUSION, FOR THE LONG TERM WE ARE LOOKING TO:CREATE VALUEBE FLEXIBILEBE COMPETITIVE

All this is in return for a long-term contract and a suitable saving

AND THISAND THIS

In a fully developing context of:In a fully developing context of:

Restructuring the 4 ARCELOR sectorsRestructuring the 4 ARCELOR sectors

Group growth:Group growth: 100 million tonnes of 100 million tonnes of steelsteel

EXPECTATIONS VIS-A-VIS SUPPLIERSSupplier's right to interfere outside the strict scope of the service with profit-sharing system Development of progress contract against a balanced mechanism for profit sharingA flexibility that extends to the notion of modularity for a given periodAn irreproachable policy in matters of hygiene and safetyManagement by objectives shared by HRTransparencyActive contribution towards simplifying processesAdherence to a method of negotiation resulting in permanent agreements:Coverage of costs + margin linked to risks taken by partner + management of progressConsultancy role when drawing up the specifications for an activityWe analyse supplier performance at a number of levels: contract, site, industrial scope, ARCELOR scope. You have a duty of global performance

In return:Ethical charter signed by the buyer:

Undertaking not to use the ideas provided by the supplier throughout the purchasing process

Duty of informationRespect for economic conditions: WCR, indexationDuty of explanation in the event of an invitation to tender

being lostEquitable profit sharing to maintain high motivationPre-negotiated clauses for immediate application for all

contractsResponsibility assumed by ARCELOR in the event of

unilateral breach of contractStricter verification of project basicsGuarantee by ARCELOR in the event of prolonged mobilisation of supplier teams or particular research

ARCELOR PLATFORMS for 2006Profits

OWCR particularly supplier lead time

Suppliers: management and evaluation

Establishment of a strategic Purchasing plan for the next three years

Transformation of the Group and improved efficiency

Development of human resources and smarter management of competencies