d+w sector rotation model - naaimnaaim.org/wp-content/uploads/2015/11/presenters-1-thr… · ·...

TRANSCRIPT

OUTLOOK 2015

November 3

D+W Sector

Rotation

John

Worthington

Dauble+Worthington

Equity Portfolios

High Yield Plus Paul

Cunningham

Signal Research

Group, LLC

4csns2.0 Stanley

Linsenbardt

Four Seasons Capital

Growth

NDX Trading Mark Pankin MDP Associates, LLC

Dynamic Allocation Model

Andre Lister Signaline

Investments LLC

KKM Enhanced U.S.

Equity Fund

Jeff Kilburg KKM Financial

D+W Sector Rotation

John Worthington

Dauble+Worthington

Equity Portfolios

D+W Sector Rotation Model

Why Sector Rotation?

Causes of Price Movement

31%

20%

49%

Sector Company Market

Typical Resource Allocation

10%

80%

10%

Sector Company Market

Source: Investor's Business Daily, "Check Out Industry Rankings Before You Purchase a Stock" by Nancy Gondo

This University of Chicago study published in Investor's Business Daily suggests the true cause of stock movement.

Sector Rotation Goals• Identify outperforming sectors of the market

• Add diversification to existing portfolios and lower market correlation

• Avoid generational losses

*All data presented on this page reflect only completed (hypothetical and real) trades from 12/31/2001 through 6/30/15. Please see our complete tear sheet for more details and disclosures at www.dwequity.com.

Sector Rotation Rules• Investment universe: ProFunds 19 sector

funds, in addition to cash. • At any given time, the portfolio may invest in

up to 5 sectors.

• Relative strength measures are used to determine the strongest sectors on an intermediate term basis (average trade lasts about 5.57 months).

• All sectors to be included in the model must also be outperforming cash and the S&P 500.

• During periods of market decline, (money market favored over S&P 500 long term) model will move 100% to cash.

*The Sector Rotation has been back tested to 12/31/2001. The backtested portfolio began 12/31/2001. Actual money traded began 1/31/2010. Please see our complete tear sheet for more details and disclosures at www.dwequity.com.

Long or cash?Since 12/31/2001 our long-term market trend indicator has experienced two long periods and two cash periods:

Date Range S&P 500 performance

D+W Sector Rotation

12/31/2001-6/4/2003 downtrend (cash) -13.76% -4.42%

6/5/2003-7/2/2008 uptrend (long) 27.41% 166.01%

7/3/2008-3/26/2009 downtrend (cash) -34.05% -1.49%

3/27/2009-9/30/15 (long)130.53% 152.89%

D+W Sector Rotation performance vs. S&P 500 Total Return Index* through 9/30/15

*The D+W Sector Rotation has been backtested to 12/31/2001. The backtested portfolio began 12/31/2001. Actual money traded began 1/31/2010. Please see our complete tear

sheet for more details and disclosures at www.dwequity.com.

D+W Sector Rotation

S&P 500 TR

Growth of $1,000*

D+W Sector Rotation: Compound ROR: 14.37%

Annualized Standard Deviation: 21.05%

S&P 500 Total Return: Compound ROR: 5.92%

Annualized Standard Deviation: 14.60%

Benefits of D+W Sector Rotation• Proven 5+ year real track

record

• Independently verified performance (Theta Research)

• 100% mechanically driven following technical signals

• No shorting, infrequent trading, 1.5x leverage

• Efficient trading using ProFunds UltraSector Funds

• Transparent performance updated daily via our website

• Easy for clients to understand and believe

How to partner with Dauble+Worthington• Model traded at Trust Company of America (Money Managers X-Change

(MMX)) and ProFunds through solicitation agreement

• Custom branded tear sheets to match your firms’ look and feel

• Competitive payout to solicitor

• Signals also available through lease agreement

Contact info:

Jon A. Dauble - [email protected]

John A. Worthington - [email protected]

3116 E. Morgan Ave., Ste. A.

Evansville, IN 47711

812-401-8700 dwequity.com

Please visit our website for more information and important disclosures. https://www.dwequity.com

High Yield Plus

Paul Cunningham

Signal Research Group, LLC

HIGH YIELD BOND

PLUS

For professional use only. Not intended for

the public.

Live trading began in December of 2014.

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

GROWTH OF $100,000

SRG HY PLUS

SRG HY

Lipper HY

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

Jan

-20

04

Jan

-20

05

Jan

-20

06

Jan

-20

07

Jan

-20

08

Jan

-20

09

Jan

-20

10

Jan

-20

11

Jan

-20

12

Jan

-20

13

Jan

-20

14

Jan

-20

15

UNDERWATER GRAPH – HY PLUS

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

Jan

-20

04

Jan

-20

05

Jan

-20

06

Jan

-20

07

Jan

-20

08

Jan

-20

09

Jan

-20

10

Jan

-20

11

Jan

-20

12

Jan

-20

13

Jan

-20

14

Jan

-20

15

UNDERWATER GRAPH - HY

1/2004 to

10/2015

Annualiz

ed Return

Standar

d

Deviatio

n

Max

Drawdow

n

# Up

Months

# Down

Months

Sharp

e Alpha Beta

SRG HY

PLUS 17.05% 7.68% -3.15% 115 26 2.09

15.98

% 0.18

SRG HY 9.23% 6.10% -6.73% 99 42 1.48

6.01

% 0.53

Lipper HY 6.06% 9.15% -33.16% 99 42 0.69

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

BREAKDOWN OF RETURNS

HY Bond

Long Gov't Bond

Inverse Gov't Bond

SRG HY PLUS

Lipper HY

S&P 500

SRG HY

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0% 5% 10% 15%

Re

turn

Volatility/Standard Deviation

SCATTERPLOT OF RISK/RETURN Jan-2004 to Oct-2015

About Back-Tested Returns. Hypothetical or simulated performance results have certain limitations. Unlike an actual performance

record, simulated results do not represent actual trading. Also, since the trades have not been executed, the results shown may

have under-or-over compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading

programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being

made that any account will or is likely to achieve profits or losses similar to those shown above. Live trading began in December of

2014.

Returns from the model are net of a 1.60% annual advisory fee. However, there could be additional transaction fees that have not

been included in the report. Performance results reflect all dividends, capital gains, and interest being reinvested. Performance

results were generated by applying the model's buy/sell signals to the Lipper High Yield Index, the Rydex Long Gov't Bond Fund

(RYADX), and the Rydex Inverse Long Gov't Bond Fund (RYJUX). Therefore, actual client account performance varied from this

report as investors cannot directly invest in an index. Model results are NOT BANK GUARANTEED, NOT FDIC INSUREDAND MAY

LOSE MONEY. Past performance is not an indication of future results.

The advisory fee paid is separate and distinct from the internal fees and expenses charged by mutual funds to their shareholders.

These fees and expenses are described in each fund's prospectus, and will generally include a management fee, internal

investment, custodial, and other expenses, and a possible distribution fee. Prospective clients should consider all of these fees and

charges when deciding whether to invest in the program. Performance results do not reflect the impact of taxes. Client accounts

may engage in a significant amount of trading. Gains and losses will generally be short-term in nature; consequently, this program

will likely not be suitable for clients seeking tax efficiency. A variable annuity can be used to provide a tax-deferred investment

vehicle.

This strategy may be offered within a variable annuity. Variable annuities and mutual funds are sold only by prospectus Please

carefully consider the product's features, risk, charges and expenses, and investment objectives, risks and policies of the underlying

portfolios, as well as other information about underlying fund options, before investing. The prospectus, which contains this and

other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus

carefully before deciding whether to invest.

The Standard & Poor's 500 Total Return Index (S&P 500TR) is a capitalization-weighted index of 500 stocks with dividends

reinvested. The index is designed to measure performance of the broad domestic economy through changes in the aggregate

market value of 500 stocks representing all major industries. The Lipper High Yield Bond Index provides a measure of the

performance of 30 of the largest high yield bond mutual funds. Securities are classified as high-yield if the middle rating of

Moody's, Fitch, and S&P is Ba1/BB+/BB+ or below. The historical performance results of the S&P 500TR Index and the Lipper High

Yield Bond Index do not reflect the deduction of transaction or custodial charges, nor the deduction of an advisory fee, which

would decrease historical performance results. Investors cannot invest directly in the S&P 500TR Index or the Lipper High Yield

Bond Index. Performance of the S&P 500TR Index and the Lipper High Yield Bond Index is provided solely for purposes of

comparison, to assist prospective clients in determining whether this strategy is generally suitable for their account. The use of the

S&P 500TR Index and the Lipper High Yield should not be construed as their endorsement of our management services.

DISCLOSURES

QUESTIONS?

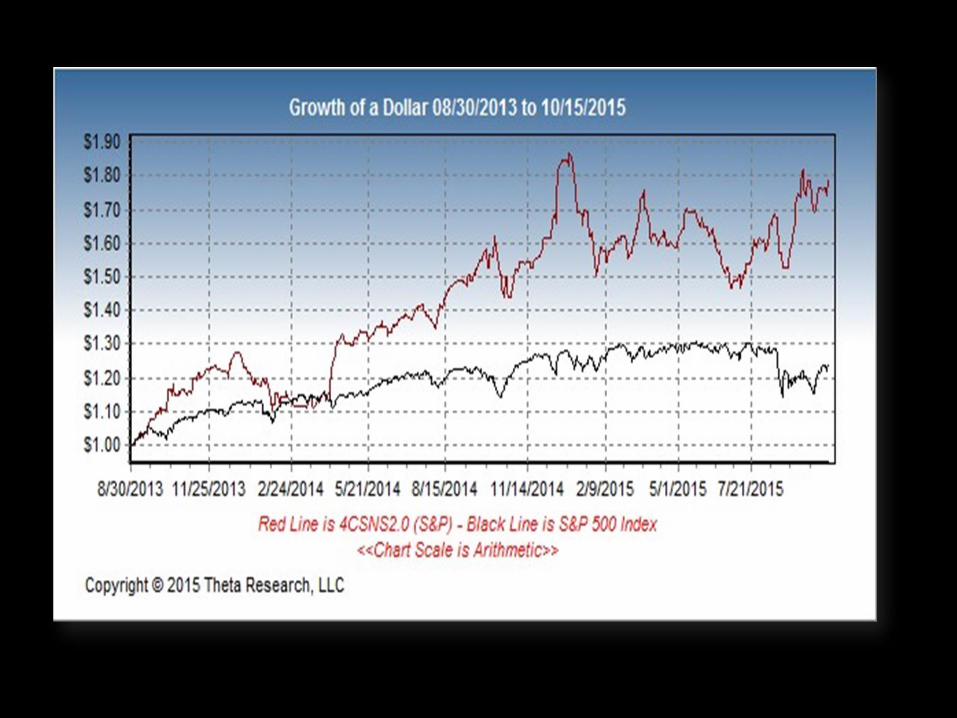

4csns2.0

Stanley Linsenbardt

Four Seasons Capital Growth

FOUR SEASONS CAPITAL GROWTH

Signal Provider

STAN LINSENBARDT

OWNER

NAAIM OUTLOOK 2015

4CSNS2.0 2X S&P LONG/ SHORT/ CASH

S&P 500 (BENCHMARK)

ANNUALIZED YIELD 30% 10%

MAX DRAW DOWN -23% -12%

SHARPE RATIO 1.4

TIME IN MARKET 70% 100%

MONTHS TRADED 25.5 25.5

AS OF 10/15/2015

4CSNS2.0 2X S&P 500 LONG/ SHORT/ CASH

4CSNS2.0 1X S&P 500 LONG/ CASH

ANNUALIZED YIELD 30% 14%

MAX DRAW DOWN -23% -9%

SHARPE RATIO 1.4 1.6

TIME IN MARKET 70% 45%

MONTHS TRADED 25.5 25.5

AS OF 10/15/2015

4CSNS2.0 1X S&P 500

LONG/ CASH

BOND FUND 1.2X

LONG/ CASH

50/50 COMBINATION

ANNUALIZED YIELD

14% 29% 21%

MAX DRAW DOWN

-9% -5% -4%

SHARPE RATIO 1.6 2.7 3.7

TIME IN MARKET

45% 39%

MONTHS TRADED

25.5 25.5 25.5

AS OF 10/15/2015

FOUR SEASONS CAPITAL GROWTH “Worth the Risk”

STAN LINSENBARDT

WWW.4CSNS.COM

NDX Trading

Mark Pankin

MDP Associates, LLC

NDX Trading

MDP Associates

NAAIM Shark Tank

November 3, 2015

Mark Pankin

Ph. D. in Math, U. of Illinois, Chicago

Marshall U., Huntington, WV – Math Prof.

Mathtech Inc., No. VA – Ops. Research

RIA since 1994 (Sector funds, TAA)

SAAFTI/NAAIM member since 1996

Avid bicyclist

Webmaster of retrosheet.org

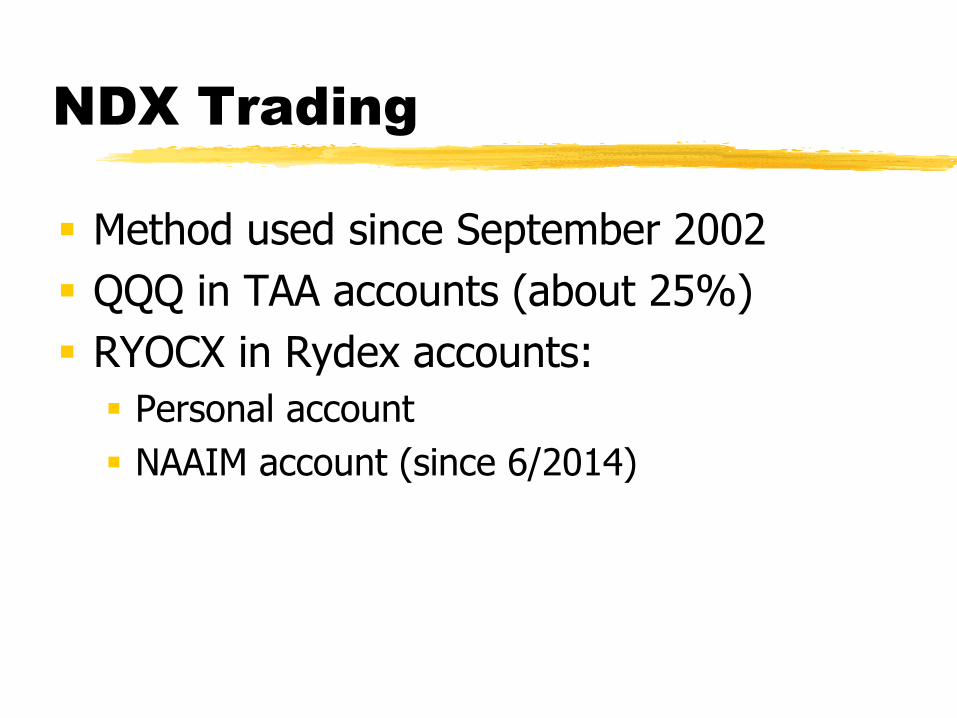

NDX Trading

Method used since September 2002

QQQ in TAA accounts (about 25%)

RYOCX in Rydex accounts:

Personal account

NAAIM account (since 6/2014)

Trading Method’s Logic

Small caps attract the most speculative and “nervous” money

Likely to trend up after larger caps

Trend likely to end sooner

Actions of Russell 2000 useful for trading Nasdaq 100

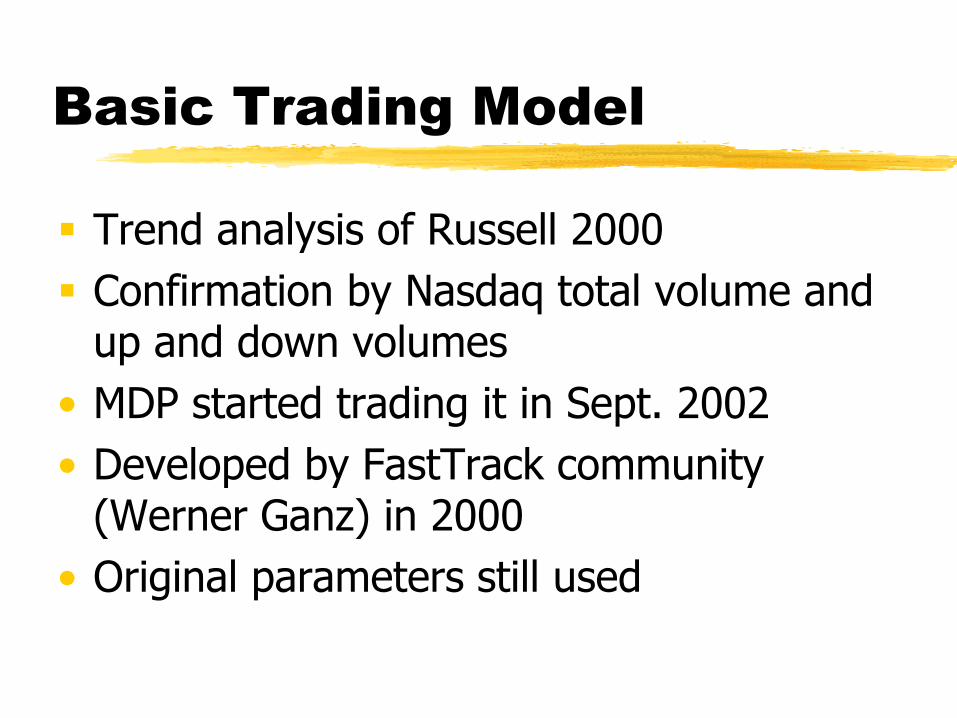

Basic Trading Model

Trend analysis of Russell 2000

Confirmation by Nasdaq total volume and up and down volumes

• MDP started trading it in Sept. 2002

• Developed by FastTrack community (Werner Ganz) in 2000

• Original parameters still used

Add “Spice” to Basic Model

Move partially or fully to 2-beta fund

After trade has moved up 8-10%

Take advantage of strong NDX gains

Get out for small profit if trend ends soon

Possible during basic model sell signal

Seasonal trades in a sector fund

Bounce from “oversold”

How well has it worked?

Compare MDP = Trading in Rydex personal account

RYOCX = Rydex fund tracks Nasdaq 100

VFINX = Vanguard Index 500 fund

We will see Equity curves

Comparison of annual returns

Comparison of annual drawdowns

Summary data for 2002-Q4 to 2015-Q3

Performance of NAAIM account

Percent Changes since 9/02

Sep-

02

Mar-

03

Sep-

03

Mar-

04

Sep-

04

Mar-

05

Sep-

05

Mar-

06

Sep-

06

Mar-

07

Sep-

07

Mar-

08

Sep-

08

Mar-

09

Sep-

09

Mar-

10

Sep-

10

Mar-

11

Sep-

11

Mar-

12

Sep-

12

Mar-

13

Sep-

13

Mar-

14

Sep-

14

Mar-

15

Sep-

15

400%

300%

200%

100%

RYOCX

VFINX

MDP

Maximum

Drawdowns:

MDP -- 16.6%

RYOCX -- 53.7%

VFINX -- 55.3%

Annual Returns

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

MDP

RYOCX

VFINX

Annual Drawdowns

-60%

-50%

-40%

-30%

-20%

-10%

0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

MDP

RYOCX

VFINX

Summary Data (13 years)

MDP RYOCX VFINX

CAGR (2002-Q4 to 2015-Q3): 8.63% 12.71% 8.88%

Exposure: 40.8% 100.0% 100.0%

Maximum Drawdown: -16.6% -53.7% -55.3%

Date of Max DD: 3/30/09 11/20/08 3/9/09

Standard Deviation*: 11.02% 18.46% 14.11%

Negative Deviation*: 5.85% 11.62% 9.51%

Ulcer Index (daily returns): 4.48% 9.28% 8.86%

Sharpe Ratio: 0.66 0.61 0.53

Calmar Ratio: 0.52 0.24 0.16

* based on monthly returns and annualized

Past performance is no guarantee of future returns

NAAIM Account Returns

MDP* RYOCX RYSPX

2014-Q3 -0.29% 5.20% 0.71%

2014-Q4 3.77% 4.48% 4.35%

2015-Q1 -1.29% 2.42% 0.66%

2015-Q2 7.99% 1.46% -0.07%

2015-Q3 2.76% -4.85% -6.86%

Total 13.34% 8.67% -1.56%

Annualized 10.54% 6.88% -1.25%

* includes MDP management fee, 50% of normal

Past performance is no guarantee of future returns

Contact Information

Mark Pankin

MDP Associates LLC

1018 N. Cleveland St.

Arlington, VA 22201

www.pankin.com

Dynamic Allocation Model

Andre Lister and John M. Davis

Signaline Investments LLC

Signaline

Investments The Dynamic Allocation Model Presented by Andre N. Lister and John M. Davis

For Financial Professional or Institutional Use Only. Not For Public Distribution.

In search of low

correlation and strong

diversification….

Holistic / Diversified Portfolio

Gold

Fixed Income

Equities

The strategy consists of three components: Equities; Fixed Income; and Gold.

Each component is managed individually and combined to create a holistic portfolio.

Strategy can be used as a core or satellite.

Momentum strategy that seeks to identify the strengths and weaknesses of 6 different ETFs.

Primarily a long strategy, inverse ETFs are used to increase returns in down markets.

No leverage used.

For Financial Professional or Institutional Use Only. Not For Public Distribution.

Low Expenses to

Maximize Value Investment Universe and Expense Ratios

VTI – Vanguard Total Stock Market Index ETF (.05%)

SH – ProShares Short S&P500 ETF (.89%)

JNK – SPDR Barclays High Yield Bond ETF (.40%)

TLT – iShares 20+ Year Treasury Bond ETF (.15%)

GLD – SPDR Gold Shares ETF (.40%)

DGZ – DB Gold Short ETN (.75%)

Low cost structure to benefit both investors and financial professionals.

Signaline Investments Management Fee: 45bps

Maximum Expense*: 134bps

Minimum Expense*: 50bps

For Financial Professional or Institutional Use Only. Not For Public Distribution.

* Not Including Trading

Costs

Opportunities In Every

Direction Equities

VTI

SH

Fixed Income

JNK

TLT

Gold

GLD

DGZ

Maximum of three securities held at one time; one from each of the three asset classes.

Equities and Gold can be long, short, or cash.

Fixed Income uses a unique set of indicators to trade between JNK, TLT, or CASH.

Momentum strategy using a defined set of rules to control buys and sells.

Non-emotional trades.

Moving averages and envelopes used to determine entry and exit points for each trade.

Core Value: Winning by not losing.

For Financial Professional or Institutional Use Only. Not For Public Distribution.

Two Factors: Micro and Macro

The Micro Indicators

• Micro Indicators control the basic buy and sell of each security.

• Micro Indicators trump Macro Indicators.

• Each security is measured by its own distinct set of indicators and buy/sell rules.

• Long-security indicators trump short-security indicators.

The Macro Indicators

o Macro Indicators control the allocation between held securities.

o Increased Allocation is controlled by the “Golden Cross”.

o Decreased Allocation is controlled by the “Death Cross”.

o Where an Increased Allocation is relative, a Decreased Allocation is a set 10%.

For Financial Professional or Institutional Use Only. Not For Public Distribution.

Macro Indicator: The “Death Cross” and the “Golden Cross”

The purpose of using a decreased allocation is to help reduce unwanted volatility in the portfolio, even when the Micro Indicator has a BUY on the security.

For Financial Professional or Institutional Use Only. Not For Public Distribution.

Allocation Controlled By The

Macro Indicators

There are 27 possible portfolio allocations, including ALL CASH.

When all positions have an Increased Allocation Indicator, allocation is split evenly. A Decreased Allocation Indicator sets the given security at 10% and all other securities are allocated to evenly.

The model operates a “low-cash” system. When a position is reduced, cash generated is re-allocated evenly to positions with an Increased Allocation.

Example: An Increased Allocation on VTI, Decreased Allocation on TLT, and Increased Allocation on DGZ would result in a portfolio mix of VTI (44%), TLT (10%), DGZ (44%), and CASH (2%).

The portfolio generally holds about 2% in CASH.

For Financial Professional or Institutional Use Only. Not For Public Distribution.

Back-Tested Results Used As A

Confidence Indicator

For Financial Professional or Institutional Use Only. Not For Public Distribution.

Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the

performance of any investment.

Back-Tested Portfolio Metrics

For Financial Professional or Institutional Use Only. Not For Public Distribution.

2015 Model Performance Through 3rd Qtr: -3.75% (Net of

2% Annual Fee) 2015 S&P500 TR Performance Through 3rd

Qtr: -5.29%

Contact Information and

Disclaimers

Signaline Investments

Portfolio Managers:

André N. Lister – [email protected]

John M. Davis – [email protected]

Phone: 844-654-6365

Available through the Envestnet/Placemark and UMA

Marketplace Platforms.

Available on the broader Envestnet Platform in 2016.

Investment advice and financial planning offered through Financial Advocates Investment

Management, DBA Signaline Investments, a registered investment advisor.

For Financial Professional or Institutional Use Only. Not For Public Distribution.

This presentation has been prepared to provide you with general information only. Information provided does not constitute any investment recommendation. Before making an investment decision, you need to consider whether this information is appropriate to

your objectives, financial situation, and needs.

For back-tested results, an annual wrap fee of 2% was included to simulate potential fees, expenses, sales

charges, and trading costs. Actual fees and expenses could be higher or lower than the 2%. Prices used in calculating back-tested returns in the model may be

different from actual executed trade prices. Back-tested trades were generally priced using the published

VWAP for that security on that day. Actual trade data is used in the model from 06/18/2014 forward.

The performance of, or any particular repayment of capital on any investment is not guaranteed. Past investment performance is not indicative of future

results. The value of investments and the income from them can fall as well as rise and are not guaranteed. You may not get back the amount of your original

investment.

We reserve the right at any time to change, amend, or cease this investment program.

KKM Enhanced U.S. Equity Fund

Jeff Kilburg

KKM Financial

KKM Enhanced U.S. Equity Fund

2015 Q4

kkmfinancial.com | 312.448.7230 | 141 W. Jackson Blvd. Suite 1711, Chicago, IL 60604

KKMAX KKMIX

Research provided by

53 kkmfinancial.com | 312.448.7230 | 141 W. Jackson Blvd. Suite 1711, Chicago, IL 60604

CONFIDENTIAL USE This Presentation and any other information provided to the recipient by KKM Financial, LLC (“KKM”) is confidential and is intended for use only by the persons or entity to which it was furnished. This Presentation may not be distributed, reproduced or used without the express consent of KKM. This material has been prepared by KKM for informational purposes only. DISCLAIMER This document does not constitute an offer to sell or the solicitation of an offer to buy any security or investment product and should not be construed as such. The investment strategies presented may not be suitable for all types of clients. All investing involves risk including the possible loss of all amounts invested. Prospective clients should not rely solely on this Presentation in making a decision as to whether to retain KKM and should make an independent review of all available facts and information regarding KKM, including the economic benefits and risks of pursuing the strategies mentioned.

Research provided by

54

KKM Enhanced U.S. Equity Fund

kkmfinancial.com | 312.448.7230 | 141 W. Jackson Blvd. Suite 1711, Chicago, IL 60604

In today's market environment, downside protection continues to be a primary focus for investors. The challenge, however, is to both generate positive returns and reduce downside risk. The KKM Enhanced U.S. Equity Fund seeks to be a solution to this challenge. The KKM Enhanced U.S. Equity Fund offers investors the ability to strategically invest in a broadly diversified portfolio of U.S. stocks through ETFs (Exchange Traded Funds) with the enhanced diversification of an optimized volatility hedge (“The Umbrella”) that includes embedded daily tail-risk protection. Our approach is simple – quantitatively select superior sectors inside of the 10 sectors that comprise the U.S. stock market and then dynamically allocate to volatility based upon methodology that utilizes historical and forward-looking market volatility trends.

The fund seeks to deliver comparable returns, before fees and expenses, of the CBOE VIX Tail Hedge IndexSM (VXTHSM)

80% U.S. Sector Selection + 20% “The Umbrella”

Research provided by

55

Portfolio Overview

kkmfinancial.com | 312.448.7230 | 141 W. Jackson Blvd. Suite 1711, Chicago, IL 60604

Objective – To outperform the S&P 500 Index with smaller draw downs by investing in a diversified basket of sector and volatility ETFs.

”The Umbrella” 20%

U.S. Sectors, 80%

U.S. Sectors

1. Identify Sectors Analyze 3 month, 6 month and 12 month trends in job

creation, GDP and profitability Determine the 5 sectors or sub-sectors showing

growth opportunities Concentration strives to generate best opportunity for

alpha

2. Select ETFs Current opportunity set includes 10 sectors and more

than 20 sub-sector ETFs Allocation based on ETF fundamentals

“The Umbrella”

1. Determine market behavior Is this a growth environment or contraction? Is the market moving sideways? Do we need protection from exogenous events, or tail

risk?

2. Select ETFs Aim to capture alpha in bull markets and protect

principle in bear markets Current opportunity set of 10 ETFs is available

3. Hedge Tail Risk

A defined allocation to VIX call options ensures the portfolio is always net long volatility and hedged against tail risk events.

Research provided by

56

Sector Selection

kkmfinancial.com | 312.448.7230 | 141 W. Jackson Blvd. Suite 1711, Chicago, IL 60604

Optimization

Price/earnings, price/book value, price/sales, yield, ROE, concentration

Allocation

Diversification by sector, security and geography, market capitalization

Product Selection

Expense ratio, AUM, trading volume, premium/discount, ETP structure, tax optimization

ETF Ownership Influence

Compare ETF penetration to overall market weighting

Output from Leading Indicators

Job creation, GDP impact, and profit realization in each sector

Objective: Identify 5 U.S. sectors or sub-sectors that have the opportunity to grow faster than the S&P 500 index.

Research provided by

57

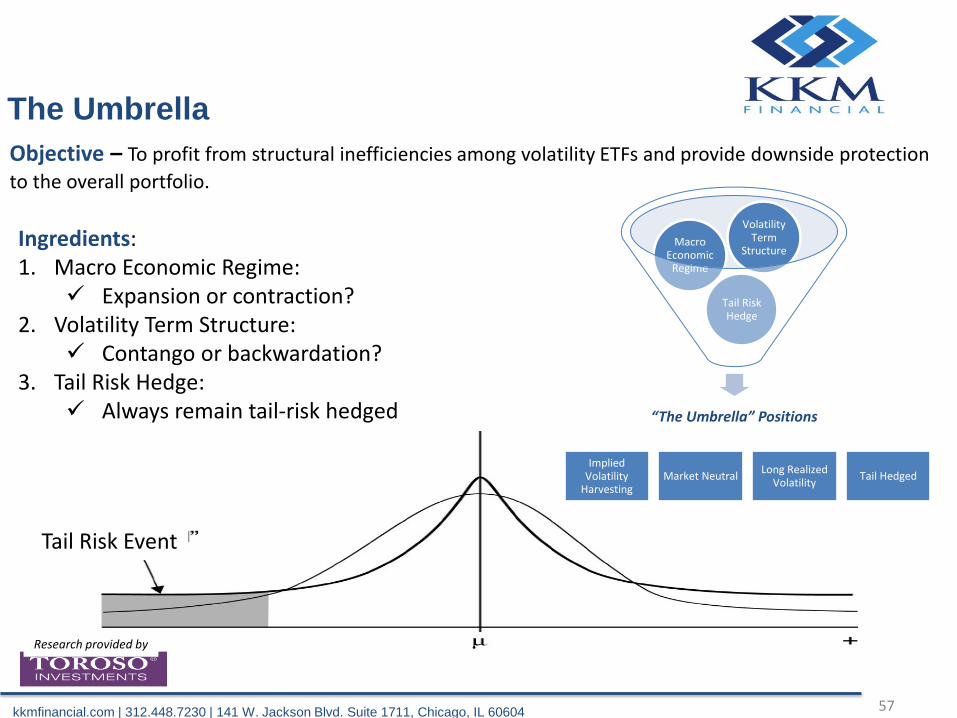

The Umbrella

kkmfinancial.com | 312.448.7230 | 141 W. Jackson Blvd. Suite 1711, Chicago, IL 60604

Objective – To profit from structural inefficiencies among volatility ETFs and provide downside protection

to the overall portfolio.

Long Volatility Tail Risk Hedge

“The Umbrella” Positions

Tail Risk Hedge

Macro Economic

Regime

Volatility Term

Structure Ingredients: 1. Macro Economic Regime:

Expansion or contraction? 2. Volatility Term Structure:

Contango or backwardation? 3. Tail Risk Hedge:

Always remain tail-risk hedged

Implied Volatility

Harvesting Market Neutral

Long Realized Volatility

Tail Hedged

Tail Risk Event

Research provided by

58

Portfolio Manager

kkmfinancial.com | 312.448.7230 | 141 W. Jackson Blvd. Suite 1711, Chicago, IL 60604

Research Providers

Michael J. Venuto is Co-Founder and Chief Investment Officer of Toroso Investments, LLC. He has over 16 years experience in the asset management business. Michael oversees asset allocation and security selection for both Toroso’s 401k and SMA business. He is also the lead portfolio manager for the the Toroso Newfound Tactical Allocation Fund. His most recent position was Head of Investments at Global X Funds where Michael provided portfolio optimization services to institutional clients. Previously he was Senior Vice President at Horizon Kinetics where his responsibilities included new business development, investment strategy, client and strategic initiatives. As Director of the Private Client Group, Michael managed the financial advisory team, client service group and marketing strategy for $1.6 billion in client accounts. Michael also served on Horizon’s Investment Committee where he helped implement the firm’s “Core Value” portfolio, as well as portfolio customization strategies on behalf of high net worth individuals. Additionally, he developed and implemented a fixed income portfolio utilizing exchange traded products. Michael was also instrumental in the establishment of multiple strategic investments and partnerships related to ETFs, Exchanges and Indexation. In 2014, Michael was chosen as one the ETF.COM All Stars for his research and is often quoted as an ETF expert in publications such as Reuters and Barron's.

Scott D. Martin is Chief Market Strategist of United Advisors, a diversified financial services company and CEO of Accent Asset Management. He is frequently featured on radio and television; and he is a contributor to and commentator on Fox Business Network. Prior to joining United Advisors, Mr. Martin was Managing Director at Astor Asset Management where he supervised new advisory relationships for the company and oversaw significant growth in the firm’s assets under management during his tenure. Mr. Martin also served on Astor’s portfolio management team beginning in 2004 and was co-portfolio manager on all of Astor’s ETF-based separate account programs as well as Astor’s mutual fund, which was launched in 2009. At the company, he authored the weekly “Astor Long/Short Balanced Update” newsletter, which received the NAAIM President’s Award for excellence in financial newsletter writing. A recognized graduate from Denison University, Mr. Martin completed a double major in Economics and French, and spent months abroad studying the introduction of the Euro currency and its impact on European markets. Mr. Martin began his career in the financial industry with TD Waterhouse Investment Services Corporation, concentrating on portfolio services for high net worth clients at the firm. A frequent speaker and lecturer, Mr. Martin has been featured in print and broadcast media such as The Wall Street Journal, Investor’s Business Daily, Bloomberg, and CNBC. He is currently a contributor to Fox Business Network and is a former columnist with TheStreet.com.

Jeff Kilburg started his career at the Chicago Board Options Exchange (CBOE). After learning equity options from Mercury Founders Jon and Pete Najarian, Mr. Kilburg was offered an opportunity in the Chicago Board of Trade (CBOT) bond option pit. He had the opportunity to learn from a team of veteran traders with one of the premier firms, Ritchie Capital Markets Group at the CBOT. There he was first introduced to volatility. After gaining a footing in the fixed income option, Mr. Kilburg gravitated to the bond futures pits. Subsequently, he joined a specialist group in the thirty-year pit, JLS Group. The thirty-year pit in the 1990s was a riveting opportunity and became his starting point in futures. Mr. Kilburg is regarded as one of the industry’s premier futures traders and is a member of the Futures Now team on CNBC. In early 1999, he decided to launch a floor operation of his own. He went on to become one of the larger market makers in the ten-year note pit. With the ability to trade the entire Treasury curve, Mr. Kilburg obtained vast experience in understanding risk management. His deep understanding of the Treasury curve has proven applicable for various futures markets and truly helps separate Mr. Kilburg from his peers. Risk management was imperative as he transitioned his floor operations into a registered investment advisory firm in 2012. KKM Financial is a liquid alternative investment firm. Mr. Kilburg gained national recognition in 2012 when he called, on CNBC, for the ten-year to fall to historic lows (under 1.5%). Since then, Mr. Kilburg has had an exclusive contract as a CNBC contributor and is on air regularly. He is also the recipient of a four-year football scholarship (under Lou Holtz) and a graduate of the University of Notre Dame.