ds burkenroad report_pq

TRANSCRIPT

PETROQUEST ENERGY INCORPORATED PQ/NYSE

Continuing Coverage: Chance of Thunder on the Bayou

Investment Rating: MARKET OUTPERFORM

Opportunity for production growth in Thunder Bayou

Woodford joint venture expiration could free capital for reallocation

Low commodity prices could negatively impact long‐term strategy

PetroQuest has increased leverage to finance growth

Hedging position insufficient in 2015

Our 12‐month target price is $7.00

Company Quick View:

PetroQuest Energy Inc. is an independent oil and gas, exploration and production company. The Company acquires, drills, and operates oil, natural gas, and natural gas liquids wells and currently operations in the Gulf Coast, East Texas, and Oklahoma. As of December 2013, the Company had proved reserves of 3.1 thousand barrels of oil (Mbbl), 29.1 billion cubic feet equivalent of natural gas liquids (bcfe), and 254.2 billion cubic feet of natural gas (bcf). Based out of Lafayette, Louisiana, PetroQuest Energy Inc. was founded in 1983 and has 126 full‐time employees.

Analysts: Investment Research Manager: Dylan Fox Matthew Guidry Andrew Grin Dan Smith Alex Berrick

November 7, 2014

PRICE: $ 4.01 S&P 500: 2,031.92 DJIA: 17,573.93 RUSSELL 2000: 4,632.53

Valuation

EPS

P/ECFPS

P/CFPS

2013 A$ 0.1428.6x $ 0.954.2x

2014 E$ 0.4010.0x $ 2.381.7x

2015 E$ (0.24)

NM$ 2.061.9x

Market Capitalization Stock DataEquity Market Cap (MM): $ 264.75 52‐Week Range: $3.70 ‐ $7.59

Enterprise Value (MM): $ 620.15 12‐Month Stock Performance: ‐4.75%

Shares Outstanding (MM): 66.02 Dividend Yield: Nil

Estimated Float (MM): 57.24 Book Value Per Share: $ 1.976‐Mo. Avg. Daily Volume: 658,583 Beta: 2.07

The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment.

Wall Street's Farm Team

BURK

ENRO

AD R

EPO

RTS

4/1/13 4:47 PM

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

2

Figure 1: 5‐year Stock Price Performance

INVESTMENT SUMMARY

We give PetroQuest Energy Inc. a rating of Market Outperform and a 12 month target price of $7.00. Our valuation represents a 74.56% appreciation from the stock price on November 7, 2014. We implemented the three year present value of future oil and gas reserves, net of estimated direct expenses, discounted at an annual rate of 10%, also known as the PV‐10 valuation method, to arrive at our target price.

PetroQuest is an independent oil and natural gas exploration and production company with production focused in the East Texas Cotton Valley, Oklahoma Woodford Shale, and Gulf Coast on‐shore, and Gulf Coast shallow offshore areas. The forecast for PetroQuest is largely dependent on production parameters, potential increases in future well production, exposure to commodity prices, and exposure to interest rate risk. The Company has been successful in recent years in implementing its strategy of diversifying its assets from purely offshore and shallow onshore oil and natural gas, into a mix of shorter life assets and long life, low risk oil and natural gas liquids assets. While PetroQuest has diversified, the Company continues to use its geologic and drilling expertise in developing shorter life assets of South Louisiana and the Gulf Coast.

PetroQuest’s ability to create cash flows will be significantly influenced by two upcoming events: the conclusion of the Company’s Woodford joint venture with NextEra in the second quarter of 2015, and the result of the Company’s drilling operations in the Thunder Bayou Prospect in the Gulf Coast. Future investment decisions hinge on whether the joint venture with NextEra is extended and the level of production realized by the Thunder Bayou Prospect.

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

11/7/2009 11/7/2010 11/7/2011 11/7/2012 11/7/2013 11/7/2014

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

3

In addition to these events, the Company is currently facing low commodity prices, which we believe will remain at current, depressed levels in the near future. The final component of our forecast highlights PetroQuest’s heightened interest rate exposure due to its increased debt level.

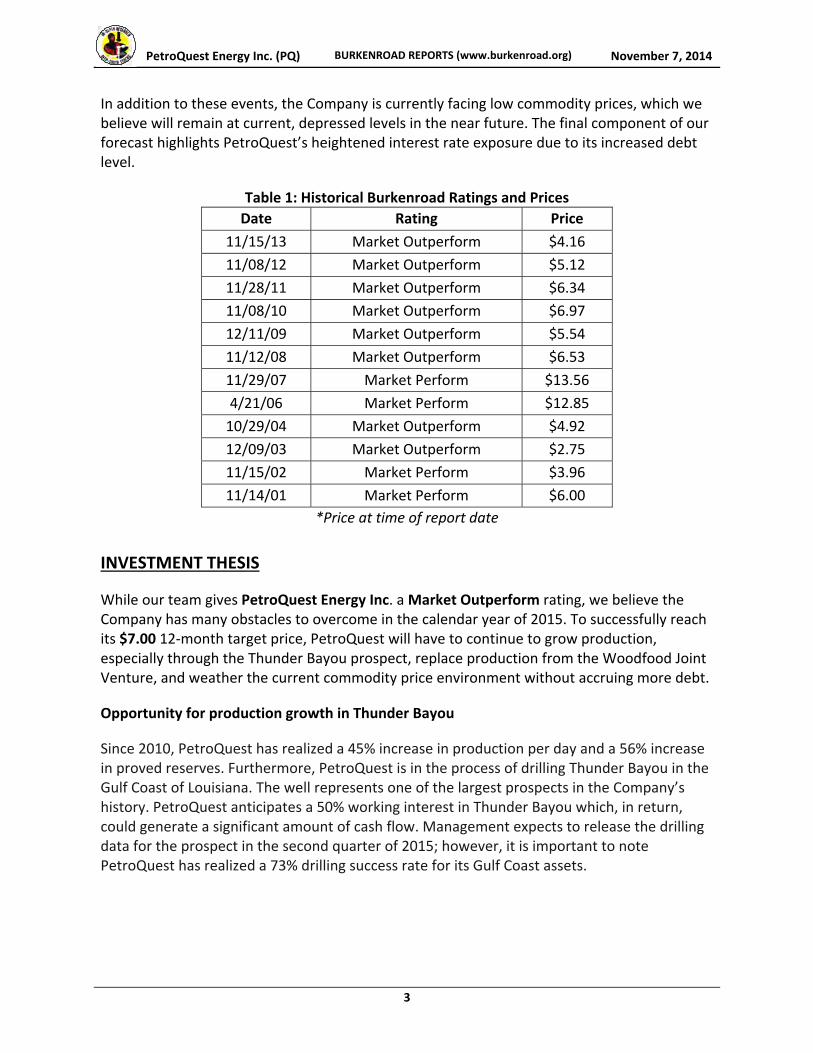

Table 1: Historical Burkenroad Ratings and Prices

Date Rating Price

11/15/13 Market Outperform $4.16

11/08/12 Market Outperform $5.12

11/28/11 Market Outperform $6.34

11/08/10 Market Outperform $6.97

12/11/09 Market Outperform $5.54

11/12/08 Market Outperform $6.53

11/29/07 Market Perform $13.56

4/21/06 Market Perform $12.85

10/29/04 Market Outperform $4.92

12/09/03 Market Outperform $2.75

11/15/02 Market Perform $3.96

11/14/01 Market Perform $6.00

*Price at time of report date

INVESTMENT THESIS

While our team gives PetroQuest Energy Inc. a Market Outperform rating, we believe the Company has many obstacles to overcome in the calendar year of 2015. To successfully reach its $7.00 12‐month target price, PetroQuest will have to continue to grow production, especially through the Thunder Bayou prospect, replace production from the Woodfood Joint Venture, and weather the current commodity price environment without accruing more debt.

Opportunity for production growth in Thunder Bayou

Since 2010, PetroQuest has realized a 45% increase in production per day and a 56% increase in proved reserves. Furthermore, PetroQuest is in the process of drilling Thunder Bayou in the Gulf Coast of Louisiana. The well represents one of the largest prospects in the Company’s history. PetroQuest anticipates a 50% working interest in Thunder Bayou which, in return, could generate a significant amount of cash flow. Management expects to release the drilling data for the prospect in the second quarter of 2015; however, it is important to note PetroQuest has realized a 73% drilling success rate for its Gulf Coast assets.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

4

Woodford joint venture expiration could free capital for reallocation

In 2010, PetroQuest formed a favorable joint venture with NextEra Energy Inc. in the Woodford Shale region. The joint venture (also referred to as a “drilling promote”) with NextEra distributes the cost of development of the property as well as the revenue that it produces. Since the operation began, PetroQuest has paid 25% of expenditures in exchange 50% of the revenue stream. The current joint venture is set to conclude in the second quarter of 2015 unless a new agreement is developed with NextEra. According to PetroQuest management, the conclusion of the joint venture would result in a reallocation of capital toward other basins. PetroQuest will likely invest in its Cotton Valley assets if the joint venture is not renewed.

Low commodity prices could negatively impact long‐term strategy

PetroQuest maintains a long‐term strategy of utilizing free cash flows from its shorter life Gulf Coast assets to develop its longer‐life assets such as Woodford and Cotton Valley. The $188.8 million shallow‐water Gulf of Mexico acquisition represents the Company’s commitment to the proceeding strategy and the importance of its shorter life free cash flows. Since 2007, PetroQuest has generated over $400 million in free cash flow from its Gulf Coast assets.

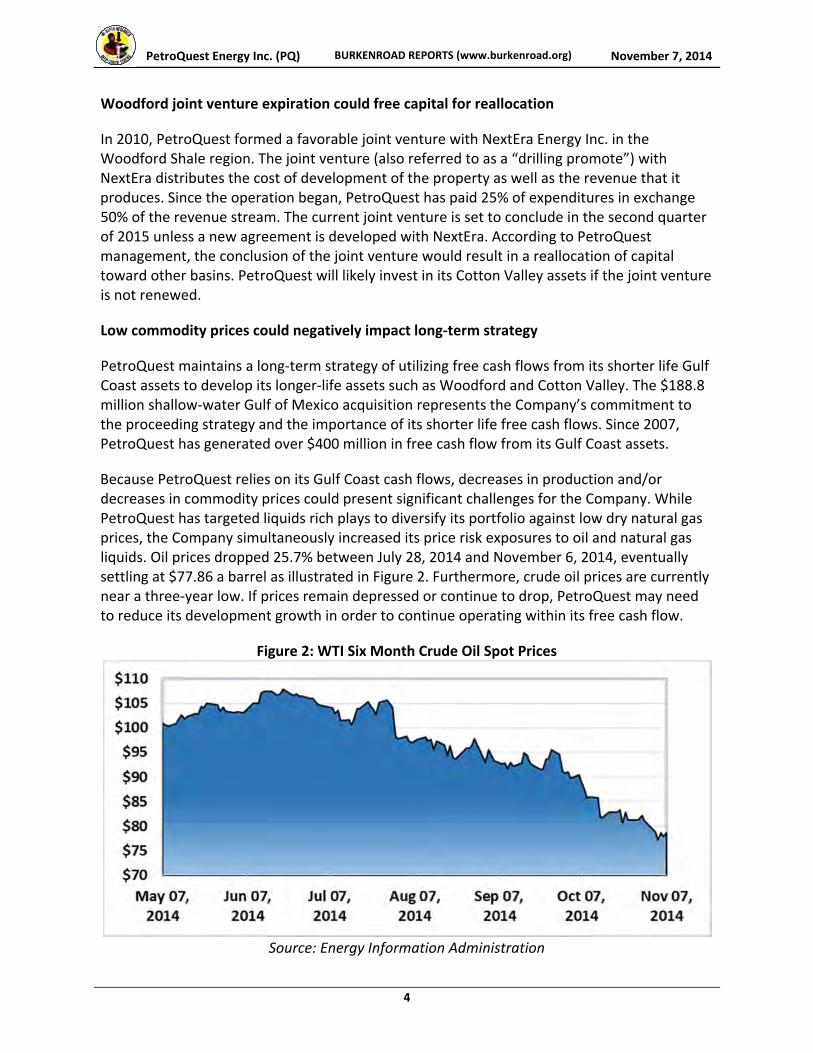

Because PetroQuest relies on its Gulf Coast cash flows, decreases in production and/or decreases in commodity prices could present significant challenges for the Company. While PetroQuest has targeted liquids rich plays to diversify its portfolio against low dry natural gas prices, the Company simultaneously increased its price risk exposures to oil and natural gas liquids. Oil prices dropped 25.7% between July 28, 2014 and November 6, 2014, eventually settling at $77.86 a barrel as illustrated in Figure 2. Furthermore, crude oil prices are currently near a three‐year low. If prices remain depressed or continue to drop, PetroQuest may need to reduce its development growth in order to continue operating within its free cash flow.

Figure 2: WTI Six Month Crude Oil Spot Prices

Source: Energy Information Administration

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

5

PetroQuest has increased leverage to finance growth

To fund recent reserve and production growth, PetroQuest significantly increased its leverage. PetroQuest’s debt to equity ratio has grown from .67 in December, 2012 to 4.29 by December 31, 2013—a 540% increase. While the ratio has since declined to 3.24 on November 6, 2014, PetroQuest still remains highly leveraged compared to its industry peers. In 2013, the Company took on an additional $200 million in 10% Senior notes in order to fund the Gulf of Mexico Acquisition. The proceeding notes, along with $150 million in outstanding notes, are due in 2017. As a consequence of the newest offering, management indicated that the Company plans to refinance the 10% Senior notes by the end of 2015.

Hedging position insufficient in 2015

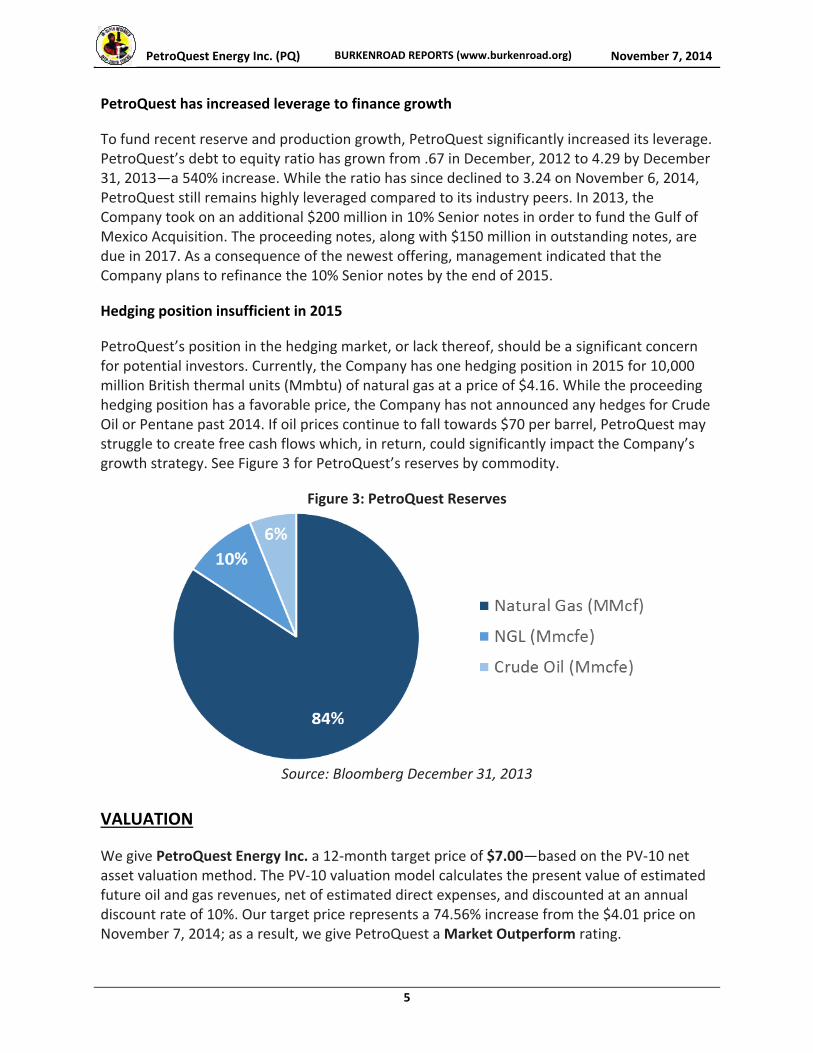

PetroQuest’s position in the hedging market, or lack thereof, should be a significant concern for potential investors. Currently, the Company has one hedging position in 2015 for 10,000 million British thermal units (Mmbtu) of natural gas at a price of $4.16. While the proceeding hedging position has a favorable price, the Company has not announced any hedges for Crude Oil or Pentane past 2014. If oil prices continue to fall towards $70 per barrel, PetroQuest may struggle to create free cash flows which, in return, could significantly impact the Company’s growth strategy. See Figure 3 for PetroQuest’s reserves by commodity.

Figure 3: PetroQuest Reserves

Source: Bloomberg December 31, 2013

VALUATION

We give PetroQuest Energy Inc. a 12‐month target price of $7.00—based on the PV‐10 net asset valuation method. The PV‐10 valuation model calculates the present value of estimated future oil and gas revenues, net of estimated direct expenses, and discounted at an annual discount rate of 10%. Our target price represents a 74.56% increase from the $4.01 price on November 7, 2014; as a result, we give PetroQuest a Market Outperform rating.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

6

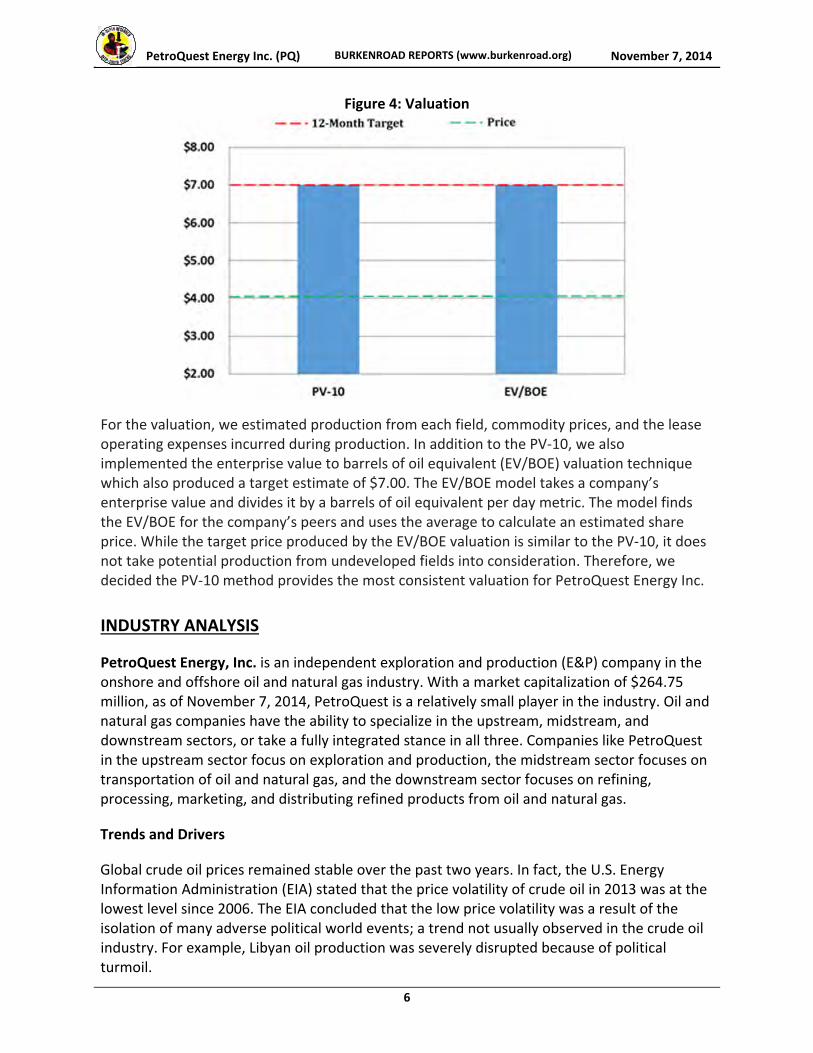

Figure 4: Valuation

For the valuation, we estimated production from each field, commodity prices, and the lease operating expenses incurred during production. In addition to the PV‐10, we also implemented the enterprise value to barrels of oil equivalent (EV/BOE) valuation technique which also produced a target estimate of $7.00. The EV/BOE model takes a company’s enterprise value and divides it by a barrels of oil equivalent per day metric. The model finds the EV/BOE for the company’s peers and uses the average to calculate an estimated share price. While the target price produced by the EV/BOE valuation is similar to the PV‐10, it does not take potential production from undeveloped fields into consideration. Therefore, we decided the PV‐10 method provides the most consistent valuation for PetroQuest Energy Inc.

INDUSTRY ANALYSIS

PetroQuest Energy, Inc. is an independent exploration and production (E&P) company in the onshore and offshore oil and natural gas industry. With a market capitalization of $264.75 million, as of November 7, 2014, PetroQuest is a relatively small player in the industry. Oil and natural gas companies have the ability to specialize in the upstream, midstream, and downstream sectors, or take a fully integrated stance in all three. Companies like PetroQuest in the upstream sector focus on exploration and production, the midstream sector focuses on transportation of oil and natural gas, and the downstream sector focuses on refining, processing, marketing, and distributing refined products from oil and natural gas.

Trends and Drivers

Global crude oil prices remained stable over the past two years. In fact, the U.S. Energy Information Administration (EIA) stated that the price volatility of crude oil in 2013 was at the lowest level since 2006. The EIA concluded that the low price volatility was a result of the isolation of many adverse political world events; a trend not usually observed in the crude oil industry. For example, Libyan oil production was severely disrupted because of political turmoil.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

7

However, other members of the Organization of the Petroleum Exporting Countries (OPEC), such as Saudi Arabia, consistently maintained oil output levels to support global oil demand. This helped create a relatively stable global oil supply.

The domestic development of shale oil has also been a large driver of stable crude oil prices. From 2012 to 2013, the U.S. increased crude oil production by 967,000 barrels per day to the highest level of production since 1989. According to the EIA, this production increase of 15% is the largest annual increase in the U.S. since 1940. As a result of this increase and a refusal of Organization of Petroleum Exporting Countries (OPEC) to reduce its production, oil price have dropped significantly during the fiscal year of 2014.

With the advances in onshore horizontal drilling and hydraulic fracturing, the U.S. has significantly increased its production of natural gas and is set to overtake Russia as the largest natural gas producer by 2015. Unlike crude oil prices, which are based on global demand, natural gas prices are based on local factors. In 2008, an increased supply of natural gas caused prices to decline roughly $8 per thousand cubic feet of natural gas to a price of $4, where prices have since remained. Low natural gas prices have forced natural gas producers, such as PetroQuest, to move away from dry gas exploration and production into the higher priced natural gas liquids or liquid rich shales. Other upstream companies have also been shifting out of natural gas and into oil in the near term.

Federal & State Regulations

PetroQuest is subject to federal and state laws regulating its drilling, operating, disposal, and abandonment of oil and gas wells in Texas, Oklahoma, Louisiana, and the Gulf of Mexico. At the state level, PetroQuest’s operations are regulated by the Louisiana Department of Natural Resources, the Texas Railroad Commission, and the Oklahoma Corporation Commission. These regulatory organizations have broad authority to regulate and oversee all aspects of exploration, production, and site restoration within Texas, Oklahoma, and Louisiana.

At the federal level, the Bureau of Ocean Energy Management (BOEM) and the Bureau of Safety and Environmental Enforcement (BSEE) regulate PetroQuest’s operations of federal oil and natural gas leases in the Gulf of Mexico. The BOEM oversees oil and gas resource potential, manages oil and gas lease sales in federal waters, and conducts environmental reviews. The BSEE ensures compliance with offshore regulatory requirements and coordination of oil spill cleanup, and holds operators accountable for commitments made when oil and gas leases are requested. Additionally, the Federal Energy and Regulatory Commission (FERC) regulates the transport and sale of oil and natural gas in interstate commerce to ensure no discrimination in accessing pipelines.

Environmental Regulations

The Environmental Protection Agency (EPA) has the primary federal authority to enforce federal environmental laws in the U.S. Other regulatory agencies that influence environmental regulations include the National Oceanic and Atmospheric Administration (NOAA), the U.S. Department of Energy (DOE), the Bureau of Land Management (BLM), and the BSEE.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

8

The primary federal laws influencing the oil and gas industry include: Energy Policy Act of 2005, Clean Air Act, Clean Water Act Federal Resource Conservation and Recovery Act, Oil Pollution Act, Coastal Zone Management Act, and Comprehensive Environmental Response Compensation and Liability Act.

State governments also have significant influence over environmental regulations that affect PetroQuest’s oil and gas drilling operations. The primary state authorities that carry out state oil and gas environmental laws are the Louisiana Department of Natural Resources, the Railroad Commission of Texas (RCT), and the Oklahoma Corporation Commission.

Barriers to Entry

PetroQuest operates in the upstream exploration and development sector of the oil and gas industry. As an upstream player, the Company experiences high upfront capital investments and strict regulation from federal and state agencies. By entering into the sector, companies are exposed to many different risks such as decreases in commodity prices, dry wells, increasing costs, labor shortages, political barriers, and subpar production. The industry also requires very experienced professional engineers, scientists, and geologists that have years of experience identifying and exploiting reserves. Consequently, companies interested in entering the upstream sector need a surplus of capital and a profound understanding of the industry’s technical challenges and regulatory requirements.

Bargaining Power of Suppliers

In the exploration and development sector, the bargaining power of suppliers is high. The power exists because oil and gas companies solicit specialized services to prospect, test, and drill the commodities. The proceeding services require not only state‐of‐the‐art equipment but also the expertise to operate efficiently. As a result, upstream oil and gas companies rely on a small group of suppliers and pay premium prices.

Bargaining Power of Buyers

The bargaining power of buyers in the oil and gas industry is low. There is very little elasticity of demand in the industry, which reduces the negotiation room for the buyers. The demand for oil, both at the intermediary and consumer level, is extremely high. As a whole, buyers may have some influence over pricing based on product quality but it is not nearly the influence suppliers’ yield.

Availability of Substitutes

The availability of substitutes to replace the oil and gas industry is very small. The upstream oil and gas industry provides crude products that are refined to be used for major everyday necessities. These necessities consist of powering utilities, heating houses and transportation. The main substitutes are renewable energy, carbon, and nuclear energy. Over the near future, none of these substitutes pose a major threat to the oil and gas industry. With renewable energy still being developed and nuclear energy posing major safety concerns, oil and gas will continue to be the main energy source across the globe.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

9

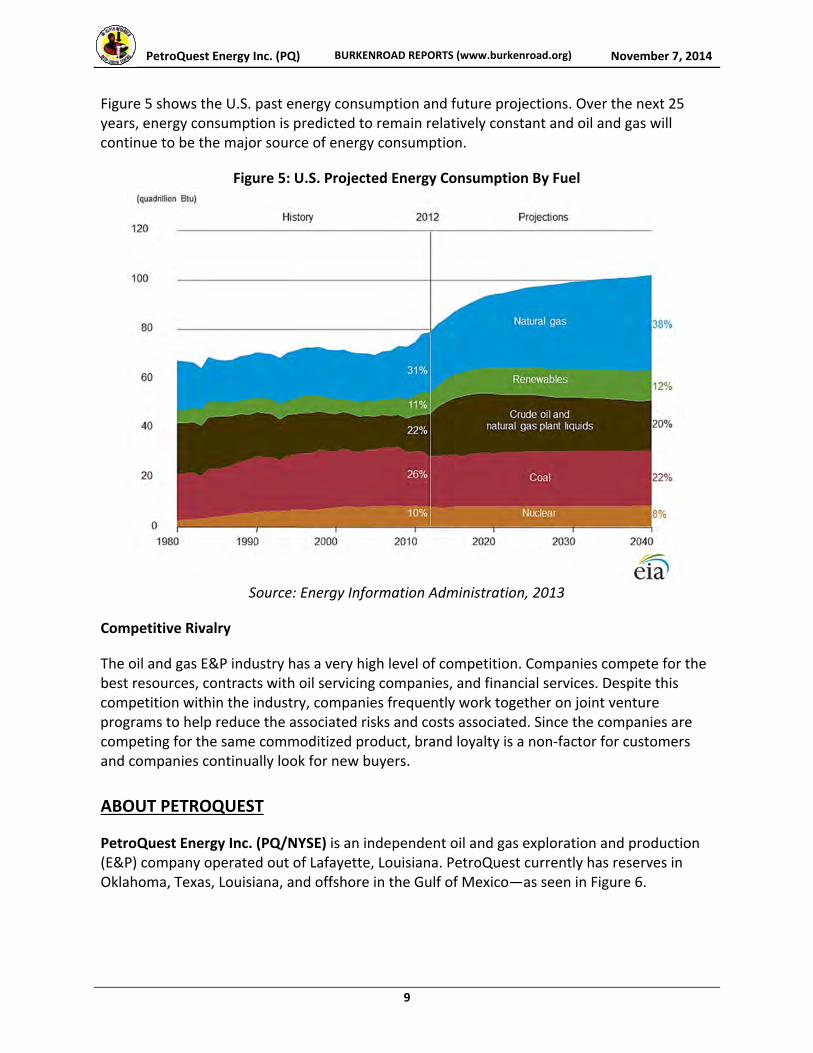

Figure 5 shows the U.S. past energy consumption and future projections. Over the next 25 years, energy consumption is predicted to remain relatively constant and oil and gas will continue to be the major source of energy consumption.

Figure 5: U.S. Projected Energy Consumption By Fuel

Source: Energy Information Administration, 2013

Competitive Rivalry

The oil and gas E&P industry has a very high level of competition. Companies compete for the best resources, contracts with oil servicing companies, and financial services. Despite this competition within the industry, companies frequently work together on joint venture programs to help reduce the associated risks and costs associated. Since the companies are competing for the same commoditized product, brand loyalty is a non‐factor for customers and companies continually look for new buyers.

ABOUT PETROQUEST

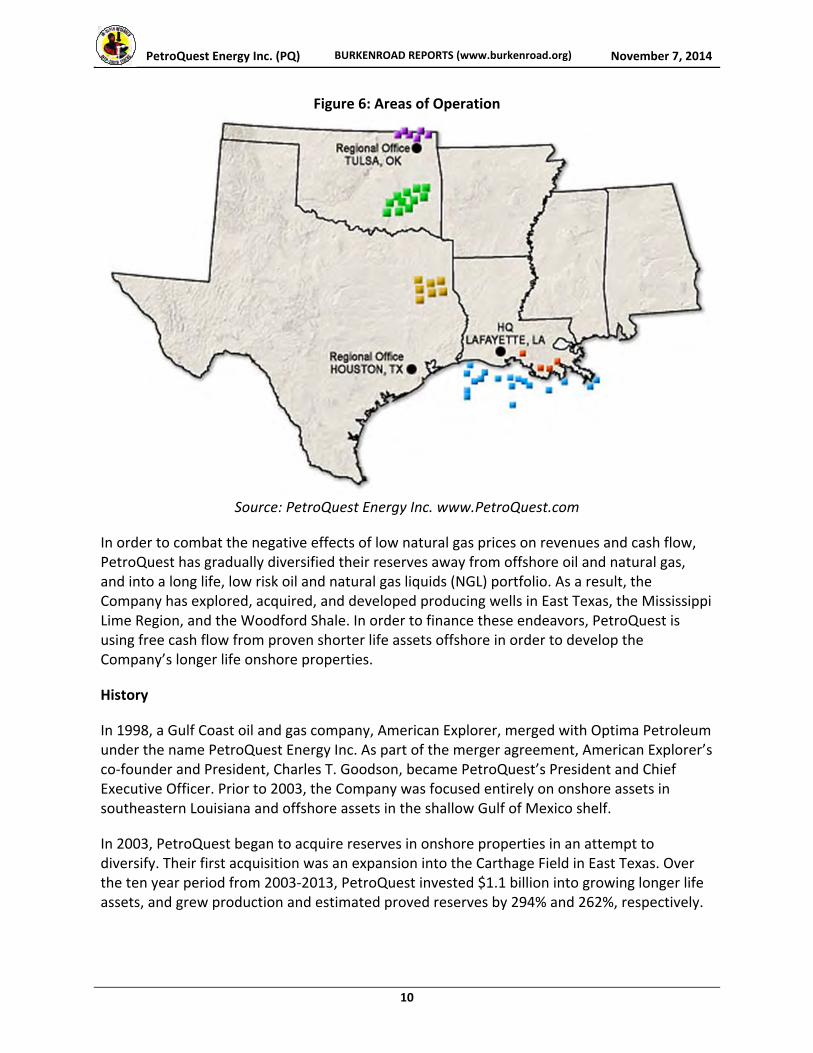

PetroQuest Energy Inc. (PQ/NYSE) is an independent oil and gas exploration and production (E&P) company operated out of Lafayette, Louisiana. PetroQuest currently has reserves in Oklahoma, Texas, Louisiana, and offshore in the Gulf of Mexico—as seen in Figure 6.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

10

Figure 6: Areas of Operation

Source: PetroQuest Energy Inc. www.PetroQuest.com

In order to combat the negative effects of low natural gas prices on revenues and cash flow, PetroQuest has gradually diversified their reserves away from offshore oil and natural gas, and into a long life, low risk oil and natural gas liquids (NGL) portfolio. As a result, the Company has explored, acquired, and developed producing wells in East Texas, the Mississippi Lime Region, and the Woodford Shale. In order to finance these endeavors, PetroQuest is using free cash flow from proven shorter life assets offshore in order to develop the Company’s longer life onshore properties.

History

In 1998, a Gulf Coast oil and gas company, American Explorer, merged with Optima Petroleum under the name PetroQuest Energy Inc. As part of the merger agreement, American Explorer’s co‐founder and President, Charles T. Goodson, became PetroQuest’s President and Chief Executive Officer. Prior to 2003, the Company was focused entirely on onshore assets in southeastern Louisiana and offshore assets in the shallow Gulf of Mexico shelf.

In 2003, PetroQuest began to acquire reserves in onshore properties in an attempt to diversify. Their first acquisition was an expansion into the Carthage Field in East Texas. Over the ten year period from 2003‐2013, PetroQuest invested $1.1 billion into growing longer life assets, and grew production and estimated proved reserves by 294% and 262%, respectively.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

11

Products

PetroQuest produces and sells natural gas, natural gas liquids (NGL), and crude oil under fixed and floating market contracts at current market prices. For the second quarter ending June 30, 2014, PetroQuest produced 230.2 million barrels of oil (Mboe), 7.696 billion of cubic feet equivalent (Bcfe) of gas, and 1.658 Bcfe of NGL. This represents a 99.0% increase in oil production, 14.3% increase in gas production, and 31.9% increase in NGL production, compared to the second quarter of 2013. The growth of PetroQuest’s crude oil and NGL production demonstrates the Company’s strategic focus on growing reserves and production of its higher priced commodities. While natural gas prices spiked in early 2014 because of harsh winter weather, prices decreased to nearly $4.50 per million British thermal units (mmBtu) by June 30, 2014. Analysts predict a slow, long‐term rise in natural gas prices, though short term prices will remain volatile and significantly lower than NGL and crude oil prices. PetroQuest’s 2013 reserves were 254.168 Bcf of natural gas, 29.140 Bcfe NGL, and 3.084 million barrels of oil equivalent (MMBoe) of crude oil. These reserves represent a 31.7%

increase in natural gas, 14.9% increase in NGL, and 86.3% increase in crude oil over 2012.

Strategy

Maintain Financial Flexibility

PetroQuest counteracts the volatile energy sector by controlling the timing of its capital investments. As a result, the Company expects to manage changing commodity prices and unexpected movements in the global financial market. Furthermore, PetroQuest continues to operate a commodity hedging program that transforms non‐core assets into cash for new operations. The capital raised from this program is used for potential projects that are consistent with PetroQuest’s long‐term growth strategy.

Diversify for Balanced Growth

PetroQuest’s reserves portfolio is diversified between low and high‐risk projects. By concluding the 2013 calendar year with 81% of reserves in low‐risk basins, PetroQuest was able to confidently pursue the higher risk and higher potential flow basins along the Gulf Coast. Though Petroquest will maintain its reserves in liquefied natural gas, crude oil, and natural gas, the Company plans to allocate more resources to liquefied natural gas and crude oil production than natural gas due to current market prices.

Prospect Unexploited and High Potential Properties

PetroQuest focuses on prospective drill sites that are consistent with the Company’s existing operations. The Company seeks large acreage properties that permit the latest exploration, development, and operating techniques.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

12

Concentrate Production in Established Areas

PetroQuest plans to contain exploration and development activities to Oklahoma, Texas, and the Gulf Coast Basin. By concentrating its operational activities, the Company reduces operational expenses. Furthermore, PetroQuest believes its existing resources and relationships in Oklahoma, Texas, and the Gulf Coast Basin will offer new opportunity for expansion.

Competitors

PetroQuest competes in the independent oil and gas exploration and production industry. Its main competitors are independent oil and gas companies that operate in the same production areas. The Company’s major competitors include Abraxas Petroleum Corporation, EV Energy Partners Limited Partnership, PostRock Energy Corporation, Cimarex Energy Company, Newfield Exploration Company, and Quicksilver Resources Incorporated. These companies operate in the same areas and directly compete with PetroQuest for market share. The Company’s two major competitors are the Abraxas Petroleum Corporation and Newfield Exploration Company. These two companies, headquartered in Texas, operate under a similar market capitalization and conduct operations in the competitive gulf coast regions.

Latest Developments

Oklahoma ‐ Woodford

PetroQuest continues to participate in the drilling of natural gas liquids in the Woodford Shale Region. In 2013, the Company invested $36.2 million acquiring an additional 13,500 acres for prospective drill sites. Additionally, in 2013, the region realized an average daily production of 47 MMcfe—a 5% increase from 2012 daily production. PetroQuest’s increase in efficiency resulted in a reallocation of capital for the 2014 calendar year. The Company predicts the Woodford Shale region will consume 50% of its 2014 total capital expenditures.

East Texas

PetroQuest invested $11.3 million in East Texas properties in 2013. The Company drilled one gross well and plugged and abandoned other mature wells. The Company also added 2,000 new net acres to its existing 50,000 net acres in the East Texas region, increasing proved reserves by 3%. 2013 net production averaged 16.3 MMcfe per day, representing a 6% decrease from 2012. PetroQuest is currently drilling six gross wells and its #10 horizontal Cotton Valley Well achieved the highest initial production rate of any of PetroQuest’s East Texas horizontally drilled wells since entering the Cotton Valley in 2011.

Gulf of Mexico Acquisition

In the summer of 2013, PetroQuest purchased shallow water assets in the Gulf of Mexico for $188.8 million This acquisition included 16 wells located on seven platforms that effectively expanded the Company’s production by 235,000 gross barrels of oil as well as an additional gross 30.5 billion cubic feet of gas equivalent (bcfe) of estimated proved reserves.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

13

Using their expertise in offshore drilling, the Company plans to create free cash flow to develop longer life assets, specifically in the Woodford Shale and Cotton Valley plays.

PEER ANALYSIS

PetroQuest’s peer group was selected based on similarities in market capitalization, enterprise value, business drivers, and operational areas.

Callon Petroleum (CPE / NASDAQ)

Callon Petroleum is an oil and natural gas company focused on exploration and production. Callon is headquartered in Natchez, Mississippi and has assets in the Permian Basin region of Texas. In 2009, Callon repositioned its operations from offshore Gulf of Mexico drilling, to the onshore Permian Basin drilling. As of December 31, 2013, Callon had estimated proved reserves of 14.857 million barrels of oil equivalent (MMboe), with 11.898 million barrels of oil equivalent (MMboe) and 17.751 billion cubic feet of natural gas equivalent (Bcfe). The Company’s current market capitalization is $443.98 million.

Goodrich Petroleum (GDP / NASDAQ)

Goodrich Petroleum is an oil and natural gas company focused on exploration and production. Goodrich is headquartered in Houston, Texas and has assets in East Texas, South Texas, Northwest Louisiana, Southeast Louisiana, and Southwest Mississippi. In recent years, Goodrich has focused on increasing its oil production because of low current natural gas prices. As of December 31, 2013, Goodrich had estimated proved reserves of 14.078 MMBoe of oil, 6.353 MMBoe of natural gas liquids, and 329.615 Bcfe of natural gas. The Company’s current market capitalization is $443.98 million.

Swift Energy (SFY / NYSE)

Swift Energy Corp is an oil and gas company that acquires, explores, develops, and operates oil and gas properties. Similar to PetroQuest, the Company focuses on onshore and inland water areas of the Texas and Louisiana Gulf Coast. For the three months ending in June 2014, the company realized 3.449 MMBoe of Net Oil and Gas Production which was a 12% increase from the second quarter of 2013. As of December 31, 2013, Swift Energy had estimated proved reserves 219.227 MMBoe, with 815.125 Bcfe of natural gas, 52.994 MMboe of oil reserves, and 30.379 MMboe of natural gas liquids. The Company’s current market capitalization is $391 million.

Approach Resources (AREX / NASDAQ)

Approach Resources is an independent oil and gas company operated out of Fort Worth, Texas. Approach Resources operates primarily in the Permian Basin in West Texas where the Company has 163,000 gross acres of land. Using its experience and expertise in the region, the Company plans to develop the Wolfcamp shale in newly acquired acreage in the Southeast Permian Basin. By investing in field infrastructure systems as well as drilling multiple wells from a single pad, the Company plans to operate as a low cost producer. As of 2013, Approach Resources had 114.7 MMBoe of proved reserves, 69% of which was oil and natural gas liquids. The Company’s current market capitalization is $546.82 million.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

14

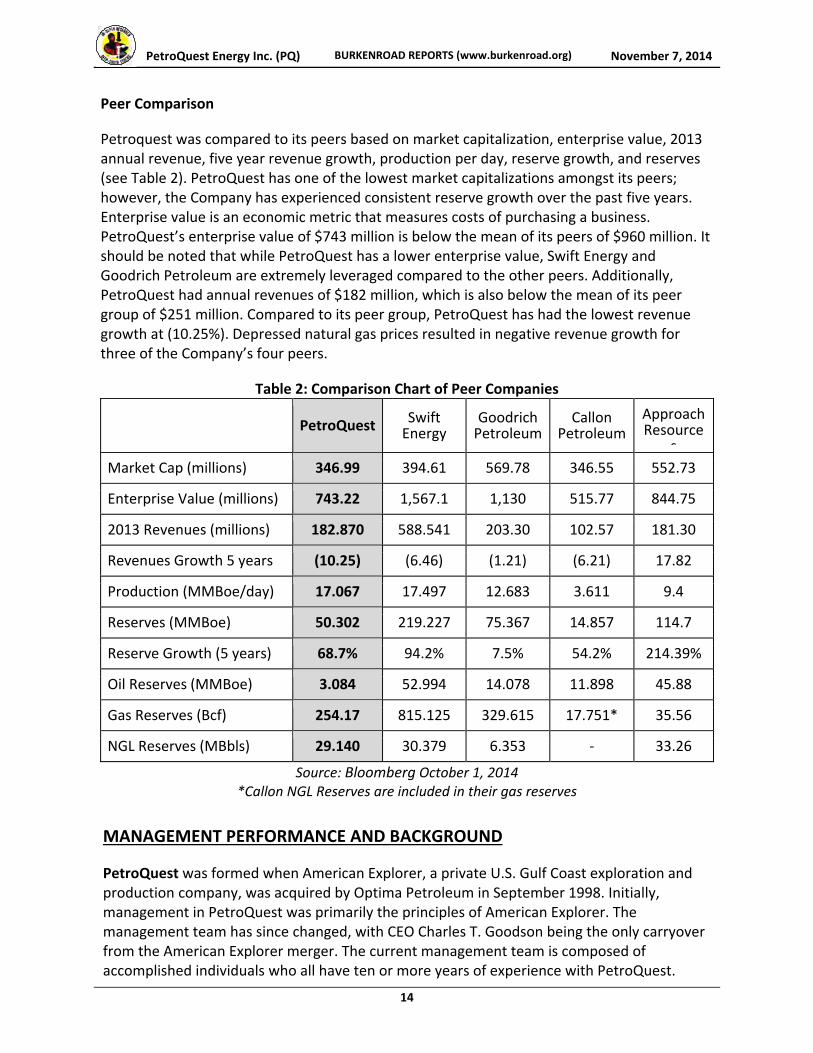

Peer Comparison

Petroquest was compared to its peers based on market capitalization, enterprise value, 2013 annual revenue, five year revenue growth, production per day, reserve growth, and reserves (see Table 2). PetroQuest has one of the lowest market capitalizations amongst its peers; however, the Company has experienced consistent reserve growth over the past five years. Enterprise value is an economic metric that measures costs of purchasing a business. PetroQuest’s enterprise value of $743 million is below the mean of its peers of $960 million. It should be noted that while PetroQuest has a lower enterprise value, Swift Energy and Goodrich Petroleum are extremely leveraged compared to the other peers. Additionally, PetroQuest had annual revenues of $182 million, which is also below the mean of its peer group of $251 million. Compared to its peer group, PetroQuest has had the lowest revenue growth at (10.25%). Depressed natural gas prices resulted in negative revenue growth for three of the Company’s four peers.

Table 2: Comparison Chart of Peer Companies

PetroQuest Swift Energy

Goodrich Petroleum

Callon Petroleum

Approach Resource

s

Market Cap (millions) 346.99 394.61 569.78 346.55 552.73

Enterprise Value (millions) 743.22 1,567.1 1,130 515.77 844.75

2013 Revenues (millions) 182.870 588.541 203.30 102.57 181.30

Revenues Growth 5 years (10.25) (6.46) (1.21) (6.21) 17.82

Production (MMBoe/day) 17.067 17.497 12.683 3.611 9.4

Reserves (MMBoe) 50.302 219.227 75.367 14.857 114.7

Reserve Growth (5 years) 68.7% 94.2% 7.5% 54.2% 214.39%

Oil Reserves (MMBoe) 3.084 52.994 14.078 11.898 45.88

Gas Reserves (Bcf) 254.17 815.125 329.615 17.751* 35.56

NGL Reserves (MBbls) 29.140 30.379 6.353 ‐ 33.26

Source: Bloomberg October 1, 2014 *Callon NGL Reserves are included in their gas reserves

MANAGEMENT PERFORMANCE AND BACKGROUND

PetroQuest was formed when American Explorer, a private U.S. Gulf Coast exploration and production company, was acquired by Optima Petroleum in September 1998. Initially, management in PetroQuest was primarily the principles of American Explorer. The management team has since changed, with CEO Charles T. Goodson being the only carryover from the American Explorer merger. The current management team is composed of accomplished individuals who all have ten or more years of experience with PetroQuest.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

15

Return on invested capital (ROIC) is an important method of measuring the performance of a company’s management. While many analysts use return on equity (ROE) in order to evaluate management, only ROIC compares company earnings to total capital investment by combining both equity and total debt. The ability to generate returns on invested capital provides insight into management’s effectiveness.

In 2011 and 2012, PetroQuest underperformed the average ROIC of its observed peers. Still, 2012 saw the only negative ROIC over the three year period from 2011‐2013. PetroQuest’s large variance in ROIC can be attributed to the issuance of a large amount of debt to finance the Gulf of Mexico Acquisition in 2013. Most companies have shown a decline in ROIC over the last three years, exhibiting a recent overall downtrend in the industry as shown in the average row in Table 3.

Table 3: Return Over Invested Capital for PetroQuest and its Peers

ROIC 2011 2012 2013

PetroQuest 3.58% (38.65)% 7.48%

Callon Petroleum 45.88% 2.80% 1.10%

Goodrich Petroleum 2.16% (5.67)% (8.26)%

Swift Energy 7.89% 3.17% 1.56%

Approach Resources 2.26% 1.52% 9.54%

Average 12.35% (7.37)% 2.28%

Source: Morningstar October 12, 2014

Charles T. Goodson Chief Executive Officer (58)

Charles T. Goodson began working in the oil and gas industry with Mobil Oil from 1977 to 1980 and with Callon Petroleum from 1980 to 1985. After leaving Callon, he co‐founded American Explorer, an exploration and production company focused on the Gulf of Mexico and the Gulf Coast. Mr. Goodson owned American Explorer and served as President until 1998 when the company merged with PetroQuest Energy. Since 1998, Goodson has served as PetroQuest’s President and Chief Executive Officer.

W. Todd Zehnder Chief Operating Officer (38)

W. Todd Zehnder began working in the oil and gas industry with KPMG from 1997 to 2001. Mr. Zehnder joined PetroQuest in 2001 and has served the Company as Executive Vice President, Chief Financial Officer and Treasurer, Vice President of Corporate Development, Vice President of Oil and Gas Marketing, and Controller. He is a Certified Public Accountant and has served as PetroQuest’s Chief Operating Officer since October 2009.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

16

J. Bond Clement Chief Financial Officer (42)

J. Bond Clement is a Certified Public Accountant who began working for various energy clients at Arthur Anderson from 1993 to 1996. From 1996 until 2004, Mr. Clement worked in several finance and accounting positions at Stone Energy and Freeport‐McMoRan. He joined Petroquest in October 2004 and has served as Chief Financial Officer since October 2009.

Art M. Mixon Executive Vice President Operations and Production (58)

Art M. Mixon joined Petroquest in January 2001 after working for over 20 years in the oil and gas industry with Amoco, British Petroleum Amoco, and British Petroleum. Mr. Mixon is currently a Registered Professional Engineer and currently serves as PetroQuest’s Executive Vice President of Operations and Production.

Management Incentives

PetroQuest uses a Compensation Committee to establish and monitor the Company’s compensation system. The Committee develops an executive compensation system that encourages both short and long term performance. Furthermore the Committee determines management incentives, the CEO’s bonus, and reviews, evaluates, and approves the compensation of all directors and executive officers. They also must approve all benefits including salary adjustments, bonuses, and stock options. Financial and strategic performances are the main criteria for establishing the compensation system.

SHAREHOLDER ANALYSIS

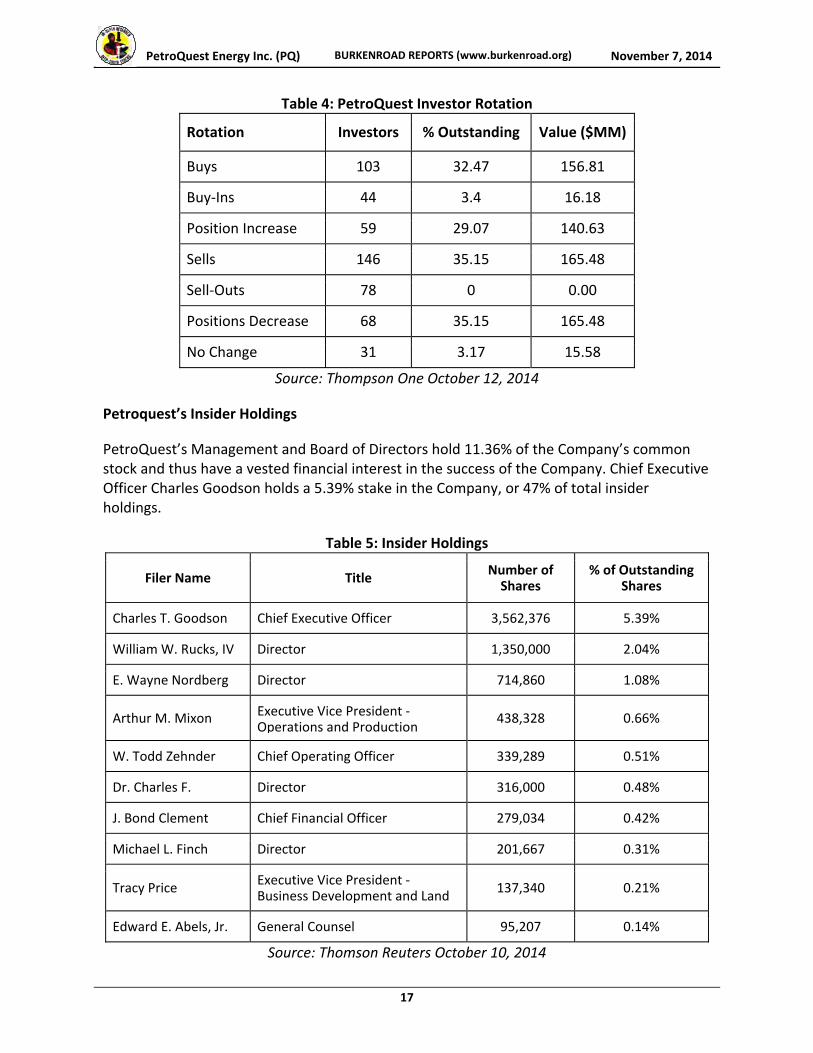

PetroQuest’s shares attract niche investors that operate growth and blend portfolios. The majority of the Company’s outstanding shares are distributed between Investment Advisors and individuals, with holdings of 67.33% and 17.18%, respectively.

Table 4 displays the buy and sell movement for PetroQueset during the fiscal year 2013. The data reveals that, in 2013, the Company experienced a heightened trend of sale in its common stock. In comparison with its peers—Callon Petroleum, Goodrich Petroleum, Swift Energy, and Approach Resources—PetroQuest had the most sells and position decreases with the exception of Goodrich Petroleum.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

17

Table 4: PetroQuest Investor Rotation

Rotation Investors % Outstanding Value ($MM)

Buys 103 32.47 156.81

Buy‐Ins 44 3.4 16.18

Position Increase 59 29.07 140.63

Sells 146 35.15 165.48

Sell‐Outs 78 0 0.00

Positions Decrease 68 35.15 165.48

No Change 31 3.17 15.58

Source: Thompson One October 12, 2014

Petroquest’s Insider Holdings

PetroQuest’s Management and Board of Directors hold 11.36% of the Company’s common stock and thus have a vested financial interest in the success of the Company. Chief Executive Officer Charles Goodson holds a 5.39% stake in the Company, or 47% of total insider holdings.

Table 5: Insider Holdings

Filer Name Title Number of Shares

% of Outstanding Shares

Charles T. Goodson Chief Executive Officer 3,562,376 5.39%

William W. Rucks, IV Director 1,350,000 2.04%

E. Wayne Nordberg Director 714,860 1.08%

Arthur M. Mixon Executive Vice President ‐Operations and Production

438,328 0.66%

W. Todd Zehnder Chief Operating Officer 339,289 0.51%

Dr. Charles F. Director 316,000 0.48%

J. Bond Clement Chief Financial Officer 279,034 0.42%

Michael L. Finch Director 201,667 0.31%

Tracy Price Executive Vice President ‐Business Development and Land

137,340 0.21%

Edward E. Abels, Jr. General Counsel 95,207 0.14%

Source: Thomson Reuters October 10, 2014

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

18

PetroQuest Institutional Holders

PetroQuest’s top ten institutional holders own 31.13% of the Company and the top three institutions hold 17.43% of the Company. The concentration of Company holdings among a small group of investors decreases the stocks liquidity. Index and growth funds make up the majority of these institutional investors as the Company is held in many small capitalization growth funds. It should also be noted that, as of October 2014, institutional investors held approximately 65% of PetroQuest shares, which is a decline from a high of 86.29% held by institutions in March of 2013.

Table 6: Institutional Holders

Source: Bloomberg October 7, 2014 *N/A Indicates holding PetroQuest in multiple portfolios

Holder Investor Style Number of Shares

% of Outstanding

Shares

Blackrock Index 5,741,237 8.69%

Vanguard Group Inc Index 3,692,194 5.59%

Voya Investment Management LLC N/A 2,081,500 3.15%

Dimensional Fund Advisors LP Core Growth 1,931,813 2.92%

Segall Bryant & Hamill Core Growth 1,416,616 2.14%

Kennedy Capital Management Growth At Reasonable Price 1,257,196 1.90%

Driehaus Capital Management LLC

Aggressive Growth 1,120,280 1.69%

Frank Russell Trust Company N/A 1,119,262 1.69%

Allianz Se Core Growth 1,112,180 1.68%

State Street Corp Index 1,108,614 1.68%

RISK ANALYSIS AND INVESTMENT CAVEATS

PetroQuest is exposed to a variety of risks standard to the oil and gas exploration and production industry that can impact the company in the short and long term. These risks factors fall into three main categories: operational, regulatory, and financial.

Operational Risks

Environmental Risks

Severe weather—especially in the Gulf Coast region—can impose catastrophic damage to exploration and production companies. Approximately 40% of PetroQuest’s production is exposed to the risk of severe weather in the Gulf Coast region including hurricanes, tropical storms, flooding, and coastal erosion.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

19

Such events can halt operations, damage facilities and equipment, and restrict production through third party pipelines. While PetroQuest’s offshore properties are exposed to severe weather risks, the Company also possesses safer onshore oil and gas properties.

Reserve Replacement Risk

PetroQuest’s ability to find, develop, and acquire additional oil and gas reserves is critical in determining its future financial condition. Exploration and production companies can experience severe decline curves in production and, in turn, are required to invest heavily in exploration opportunities. To maintain adequate reserves, PetroQuest relies on its ability to drill commodity rich sites while simultaneously avoiding low‐yielding or dry wells.

Commodity Price Risk

The price received for PetroQuest’s oil and gas influences revenues, profitability, future growth, and the carrying value of oil and natural gas properties. As a consequence, commodity prices drive the current and future financial condition of the Company. Oil and gas prices are affected by changes in supply and demand, market uncertainty, weather conditions, and the level of consumer product demand. The increase of natural gas production in the U.S. has resulted in less price volatility. However, as a consequence of heightened production, prices of oil and natural gas have dropped significantly. To combat commodity price risk, PetroQuest developed a diversified portfolio with oil natural gas, and natural gas liquids in on and off‐shore locations. Therefore, the Company has the ability adjust production as a response to volatile commodity prices.

Regulatory Risks

PetroQuest’s ability to continue exploration and production of its offshore and onshore assets is significantly influenced by federal and state regulations. Both oil and gas drilling activity and the health and safety of workers are regulated in the U.S. Future regulations could change the areas where drilling is allowed or the types of drilling activities allowed, and could lead to increased costs for environmental cleanup. Additionally, the increased attention on hydraulic fracturing and its environmental impact could result in increased federal and state oversight of onshore activities.

The impact regulatory risk can have on exploration and production companies is illustrated by the 2010 Deepwater Horizon oil spill that resulted in a six month moratorium on deep‐water drilling by the U.S. Department of the Interior. While this specific regulation did not affect PetroQuest because it does not operate in deep waters, future oil spills or environmental events could lead to new regulations that adversely impact Petroquest.

Financial, Liquidity, and Business Risks

Compared to its peers, PetroQuest exhibits a slightly above average liquidity risk. Liquidity risk refers to a company’s ability to pay off its short term financial obligations so as to mitigate large losses.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

20

As shown in Table 7, PetroQuest has a low cash ratio which is common in the exploration and production industry. At the end of fiscal year 2013, PetroQuest had a cash ratio of 0.09. This table implies that PetroQuest has less cash on hand than current liabilities and thus could struggle to pay short term debt obligations. In addition, it might be difficult to acquire additional debt because a low cash ratio is usually a red flag for creditors.

PetroQuest’s current ratio of 0.73 and quick ratio of 0.37 are comparable to its peers. The current ratio and the quick ratio measure a company's ability to pay off its liabilities with all of its assets or its most liquid assets, respectively. Generally speaking, ratios under 1 are a sign that a company might not be able to pay off its obligations, if necessary. However, these ratios appear to be on par with industry averages and peer averages.

As shown in the last column of Table 7, PetroQuest demonstrates a low ratio of cash flow from operations over average current liabilities as compared to its peers. The ratio of 0.55 is well below the peer average of 1.28 and is only greater than Goodrich Petroleum’s ratio of 0.54. This could be attributed to the Company’s recent acquisition of property in the Gulf of Mexico that was financed predominantly with debt. In addition, the Company is in a transition, shifting its portfolio onshore and has taken on debt to complete this shift.

Table 7: Liquidity Ratios at the End of 2013

Company Cash Ratio

Current Ratio

Quick Ratio

Cash Flow from Operations/ Avg. Current Liabilities

PetroQuest 0.09 0.73 0.37 0.55

Callon Petroleum 0.05 0.47 0.38 1.07

Goodrich Petroleum 0.32 0.87 0.34 0.54

Swift Energy 0.02 0.49 0.42 1.76

Approach Resources 0.7 1.07 0.97 1.74

Peer Average 0.27 0.73 0.53 1.28

Source: Bloomberg October 1, 2014

Credit Risk

Credit risk refers to the probability a company will default on its debt payments. PetroQuest has continued to increase its debt liability over the past year in order to retain capital. The Company has a higher total debt‐to‐equity ratio than its peers. This higher debt‐to‐equity ratio is a result of an acquisition in the Gulf of Mexico that was financed entirely with $188.8 million of debt. The financing for this acquisition nearly doubled the total debt‐to‐equity and total debt to assets ratio from the previous year. with the increase in debt, PetroQuest is able to maintain an interest coverage ratio higher than the peer average and the ratio is relatively unchanged from the previous year of 1.64 (see Table 8).

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

21

Table 8: Credit Ratios at End of 2013

Company Total Debt/ Equity (%)

Interest Coverage

(x)

Total Debt/ Total Asset

(%)

Market Capitalization (Millions)

Reserves (MMBOE)

PetroQuest 428.88 1.62 63.70 275 50.3

Callon Petroleum

27.14 2.26 17.87 263.5 14.9

Goodrich Petroleum 136.18 (.79) 49.84 753.3 75.4

Swift Energy 110.56 1.64 43.21 585.9 219.2

Approach Resources 35.19 3.02 21.82 753.6 114.7

Peer Average 77.27 1.53 33.19 589.08 106.05

Source: Bloomberg October 1, 2014

FINANCIAL PERFORMANCE AND PROJECTIONS

PetroQuest’s financial performance and projections are based on its ability to produce cash flows in the Gulf Coast to continue growth in the Cotton Valley fields. Because of significant uncertainty in the Company’s future (i.e. the continuation of the Woodford Joint Agreement and the success of the Bayou Thunder prospect) we were forced to make numerous assumptions in our revenue model. Despite PetroQuest’s recent effort to diversify its portfolio across oil, natural gas, and natural gas liquids, the Company is subject to significant commodity price risk. While oil prices remain depressed, our model does not reflect the extent of the drop below $85.

Production

Our revenue model relies on the estimated reserves and production for each of the following fields: Woodford, Mississippi Lime, Cotton Valley, and the Gulf Coast. After speaking with management regarding the estimated CAPEX for 2015, we came to the conclusion that PetroQuest would cease its operations in the Mississippi Lime region. Additionally, we made the assumption that the Company would not renew its joint venture with Nextera in the Woodfood region. As a consequence, we projected no new wells in the Woodford region starting in the second quarter of 2015. Lastly, during our meeting with management, Mr. Quantz referenced a significant reallocation of CAPEX from the Woodford region to Cotton Valley if the joint venture were to end. Therefore, our estimated reserves and production reflect 20 new net wells per annum in the Cotton Valley region.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

22

Commodity Prices

Commodity prices significantly impact our revenue model because PetroQuest’s revenues from production are determined by the price of oil, natural gas, and natural gas liquids. Exploration and production companies can mitigate the impact of changing commodity prices by hedging their production; however PetroQuest has currently announced only one hedging position for natural gas in 2015 and none for crude oil or Pentane. Taking into account the hedged and unhedged portions of production, we forecasted revenues using commodity prices compiled by the Burkenroad Reports program. These commodity prices were the result of a compilation of publicly available data from the Energy Information Administration’s (EIA) Short‐Term Outlook, the EIA’s Annual Energy Outlook, and Louisiana Light Sweet Crude New York Mercantile Exchange Futures. While these forecasts were updated October 13, 2014 to account for the significant drop in oil prices to $85 per barrel, the continued drop in oil prices below $75 per barrel has not been accounted for in our model

Financing

Currently, PetroQuest has $350 million of 10% senior notes outstanding expiring in 2017. The Company plans to refinance the notes next year as indicated by management. We were unable to forecast any significant changes in interest expenses because the terms of the refinancing agreement are uncertain.

SITE VISIT

On Friday, October 24, our team of analysts traveled to Lafayette, Louisiana to visit PetroQuest’s headquarters. The team met with Matt Quantz, the Company’s Manager of Investor Relations and Corporate Communications. Mr. Quantz walked us through PetroQuest’s October 2014 investor presentation, detailing PetroQuest’s current and future operations. First, he explained the Company's growth over the past four years citing its 45% growth in production, 56% growth in proved reserves, 87% growth in present value with a 10 percent discount rate (PV10), and 44 percent growth in earnings before interest, taxes, depreciation, and amortization (EBITDA). Despite growth and promising performance indicators, Mr. Quantz acknowledged that the stock price has suffered, dropping 37% since 2010. While he appeared optimistic about PetroQuest’s financial standing, he acknowledged the importance of its Thunder Bayou prospect and the Woodford Joint Venture.

Currently, PetroQuest has a joint agreement (also referred to as a “drilling promote”) with NextEra to drill multiple wells in the Woodford shale region. This agreement shares the cost of developing the property as well as the revenue that it produces. Under this agreement, PetroQuest pays 25% of the expenditures and receives 50% of the revenue stream. NextEra offered these terms in return for PetroQuest’s experience in the exploration and production industry. Mr. Quantz explained to us that the joint agreement is set to expire in the second quarter of 2015.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

23

Mr. Quantz then discussed PetroQuest’s current operations and future prospects in the Gulf Coast. He noted one large factor that could affect PetroQuest’s future production is the Thunder Bayou Prospect, which is one of the largest drilling prospects PetroQuest has ever undertaken. PetroQuest is in the process of drilling the onshore Thunder Bayou prospect in South Louisiana and has a 50% working interest. The prospect represents a significant opportunity for the Company as it is believed to hold 162 billion cubic feet equivalent (Bcfe) of unrisked reserves. Mr. Quantz indicated that the Company is currently evaluating the progress internally and will likely release more data on the progress of this well by Q1 of 2015.

Site Visit Photo

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

24

INDEPENDENT OUTSIDE RESEARCH

To adequately evaluate PetroQuest Energy Inc., research was compiled from a variety of primary and secondary sources. Primary sources included information from PetroQuest’s historical Annual Reports, Securities and Exchange Commission filings, press releases, earnings calls, investor presentations, and management guidance. Additionally, the Burkenroad Reports PetroQuest analyst team gained valuable secondary information from equity analysts’ reports, oil and gas industry reports, and from a meeting on November 9, 2014, with Hank Corder. Mr. Corder has years of invaluable experience in the E&P industry with companies such as Global Hunter Securities, Sterne Agee & Leach, and Southcoast Capital L.L.C.. Mr. Corder was well acquainted with PetroQuest and provided insight on many of the team’s unanswered questions.

Mr. Corder shared his experiences with PetroQuest and was able to highlight different trends in industry and Company operations. The most revealing insight regarded PetroQuest’s current hedging position in the futures exchange. The fact that PetroQuest is only hedged for the next six months baffled Mr. Corder. He stated a company of PetroQuest’s size, especially during periods of extreme commodity price uncertainty, should be significantly hedged to reduce any price risks. Because of the Company’s lack of hedging, Mr. Corder recommended that we conduct a sensitivity analysis for future commodity price changes to value the Company going forward.

Per Mr. Corder’s advice, we conducted a sensitivity analysis between crude oil prices and our PV‐10 valuation. By decreasing oil prices to a level of $75 a barrel, our valuation for PetroQuest fell by 10%. Furthermore, the PV‐10 model does not consider all expenses incurred throughout production. Additionally, depressed oil prices could have an even more significant impact on the actual share price.

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

25

ANOTHER WAY TO LOOK AT IT

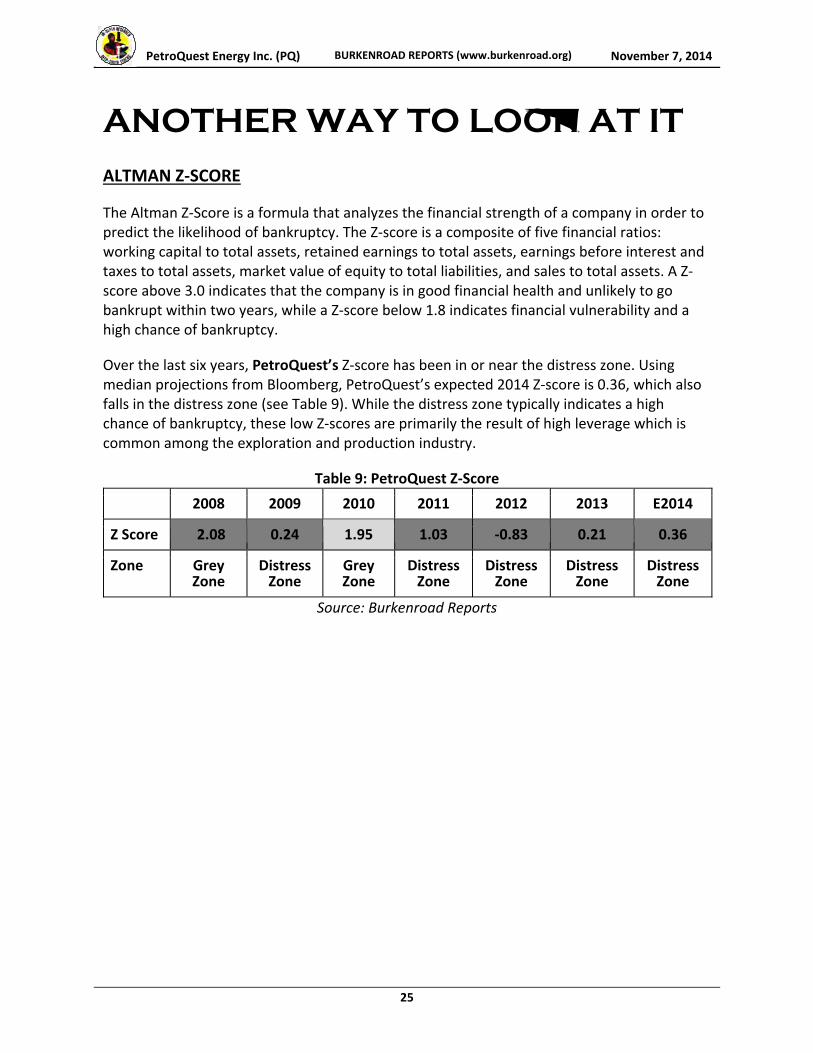

ALTMAN Z‐SCORE

The Altman Z‐Score is a formula that analyzes the financial strength of a company in order to predict the likelihood of bankruptcy. The Z‐score is a composite of five financial ratios: working capital to total assets, retained earnings to total assets, earnings before interest and taxes to total assets, market value of equity to total liabilities, and sales to total assets. A Z‐score above 3.0 indicates that the company is in good financial health and unlikely to go bankrupt within two years, while a Z‐score below 1.8 indicates financial vulnerability and a high chance of bankruptcy.

Over the last six years, PetroQuest’s Z‐score has been in or near the distress zone. Using median projections from Bloomberg, PetroQuest’s expected 2014 Z‐score is 0.36, which also falls in the distress zone (see Table 9). While the distress zone typically indicates a high chance of bankruptcy, these low Z‐scores are primarily the result of high leverage which is common among the exploration and production industry.

Table 9: PetroQuest Z‐Score

2008 2009 2010 2011 2012 2013 E2014

Z Score 2.08 0.24 1.95 1.03 ‐0.83 0.21 0.36

Zone Grey Zone

Distress Zone

Grey Zone

Distress Zone

Distress Zone

Distress Zone

Distress Zone

Source: Burkenroad Reports

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

26

PETER LYNCH EARNINGS MULTIPLE VALUATION

Peter Lynch is regarded as the most successful mutual fund manager of all time, having posted an average annual return of 29.2% in his portfolios over 13 years. In his book One Up On Wall Street, Lynch explains the charting tool he used (later deemed the “Peter Lynch Chart”) in order to determine whether a stock was undervalued and thus should be bought.

The chart overlaps a stock’s price with its “earnings line,” a value equal to 15 times the earnings per share. If a stock trades below its earnings line, Lynch would buy the equity because he believed it to be undervalued. Likewise, if the price rose above the earnings line, Lynch would sell.

Figure 7 shows the price of PetroQuest compared with its earnings line. At the current level, the price of the stock is well below the earnings line, and thus Peter Lynch would consider buying into the Company.

Figure 7: Earnings Line Versus Stock Price

Source: Bloomberg

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

27

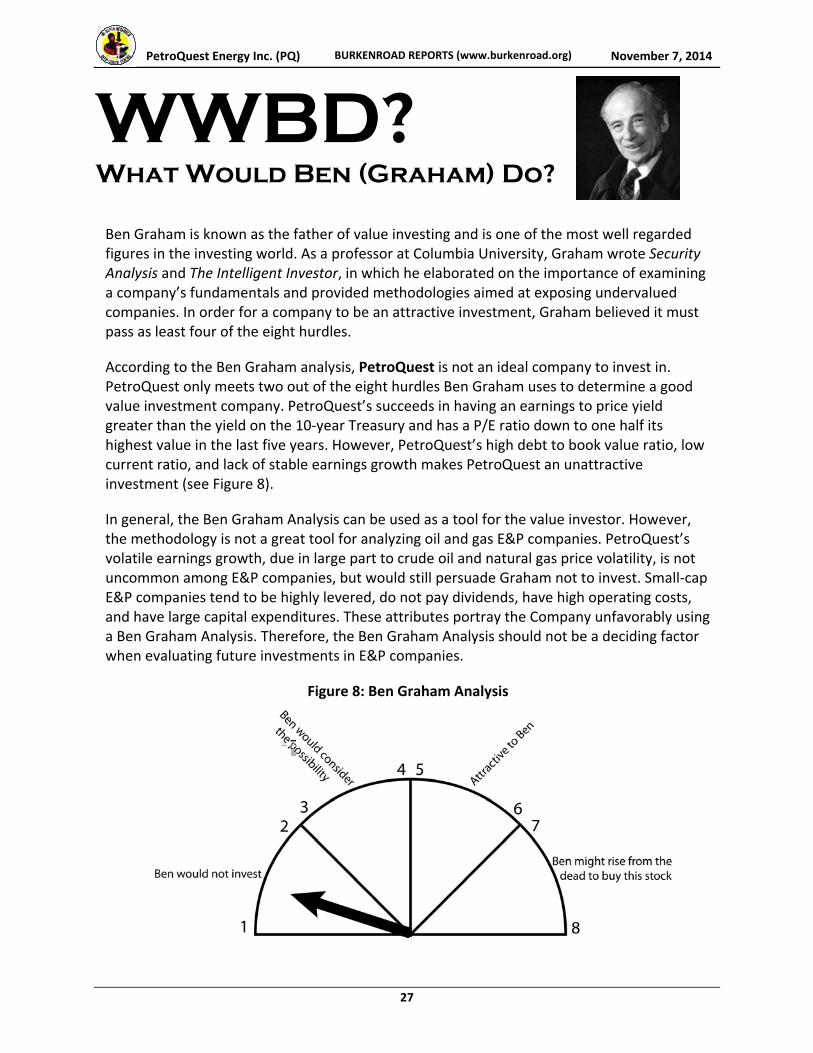

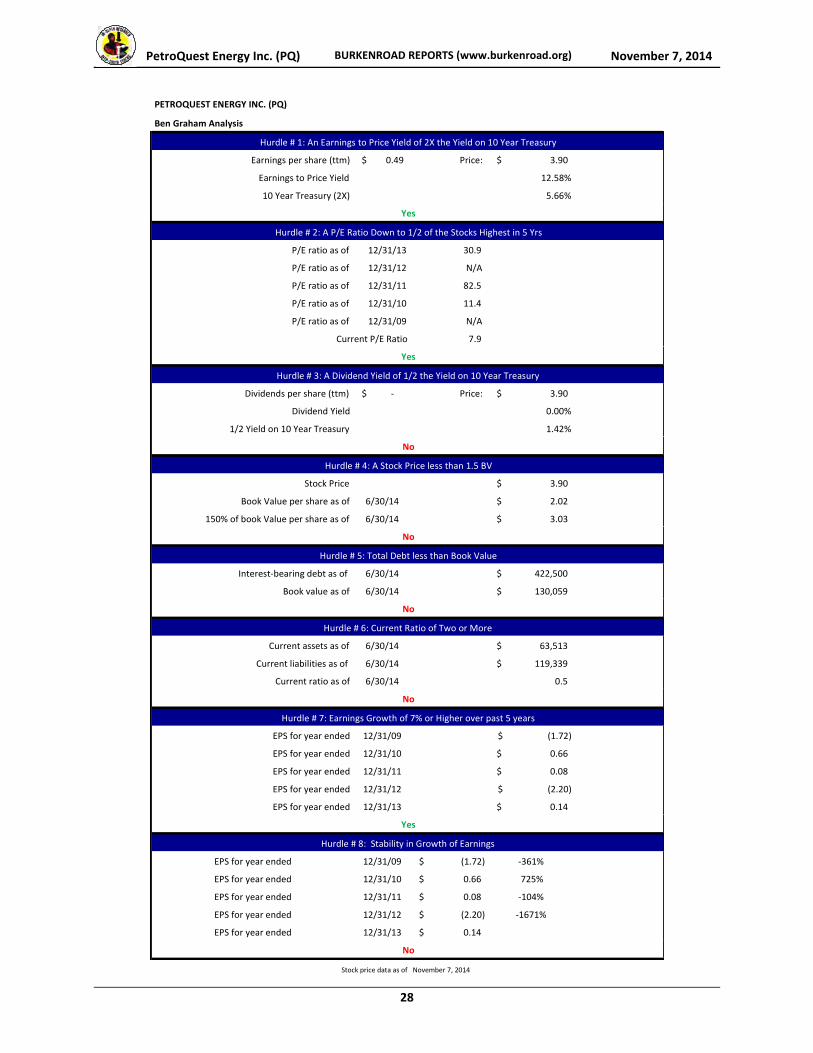

WWBD? What Would Ben (Graham) Do?

Ben Graham is known as the father of value investing and is one of the most well regarded figures in the investing world. As a professor at Columbia University, Graham wrote Security Analysis and The Intelligent Investor, in which he elaborated on the importance of examining a company’s fundamentals and provided methodologies aimed at exposing undervalued companies. In order for a company to be an attractive investment, Graham believed it must pass as least four of the eight hurdles.

According to the Ben Graham analysis, PetroQuest is not an ideal company to invest in. PetroQuest only meets two out of the eight hurdles Ben Graham uses to determine a good value investment company. PetroQuest’s succeeds in having an earnings to price yield greater than the yield on the 10‐year Treasury and has a P/E ratio down to one half its highest value in the last five years. However, PetroQuest’s high debt to book value ratio, low current ratio, and lack of stable earnings growth makes PetroQuest an unattractive investment (see Figure 8).

In general, the Ben Graham Analysis can be used as a tool for the value investor. However, the methodology is not a great tool for analyzing oil and gas E&P companies. PetroQuest’s volatile earnings growth, due in large part to crude oil and natural gas price volatility, is not uncommon among E&P companies, but would still persuade Graham not to invest. Small‐cap E&P companies tend to be highly levered, do not pay dividends, have high operating costs, and have large capital expenditures. These attributes portray the Company unfavorably using a Ben Graham Analysis. Therefore, the Ben Graham Analysis should not be a deciding factor when evaluating future investments in E&P companies.

Figure 8: Ben Graham Analysis

PetroQuest Energy Inc. (PQ) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014

28

Earnings per share (ttm) 0.49$ Price: 3.90$

Earnings to Price Yield 12.58%

10 Year Treasury (2X) 5.66%

P/E ratio as of 12/31/13 30.9

P/E ratio as of 12/31/12 N/A

P/E ratio as of 12/31/11 82.5

P/E ratio as of 12/31/10 11.4

P/E ratio as of 12/31/09 N/A

Current P/E Ratio 7.9

Dividends per share (ttm) ‐$ Price: 3.90$

Dividend Yield 0.00%

1/2 Yield on 10 Year Treasury 1.42%

Stock Price 3.90$

Book Value per share as of 6/30/14 2.02$

150% of book Value per share as of 6/30/14 3.03$

Interest‐bearing debt as of 6/30/14 422,500$

Book value as of 6/30/14 130,059$

Current assets as of 6/30/14 63,513$

Current liabilities as of 6/30/14 119,339$

Current ratio as of 6/30/14 0.5

EPS for year ended 12/31/09 (1.72)$

EPS for year ended 12/31/10 0.66$

EPS for year ended 12/31/11 0.08$

EPS for year ended 12/31/12 (2.20)$

EPS for year ended 12/31/13 0.14$

EPS for year ended 12/31/09 (1.72)$ ‐361%

EPS for year ended 12/31/10 0.66$ 725%

EPS for year ended 12/31/11 0.08$ ‐104%

EPS for year ended 12/31/12 (2.20)$ ‐1671%

EPS for year ended 12/31/13 0.14$

Stock price data as of November 7, 2014

Yes

PETROQUEST ENERGY INC. (PQ)

Ben Graham Analysis

Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury

Yes

Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs

Yes

Hurdle # 8: Stability in Growth of Earnings

No

Hurdle # 3: A Dividend Yield of 1/2 the Yield on 10 Year Treasury

No

Hurdle # 4: A Stock Price less than 1.5 BV

No

Hurdle # 5: Total Debt less than Book Value

No

Hurdle # 6: Current Ratio of Two or More

No

Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years

PetroQuest En

ergy Inc. (PQ)

BURKEN

ROAD REP

ORTS (www.burken

road

.org)

November 7, 2014

29

PETROQUEST EN

ERGY INC. (PQ)

Annual

and Quarterly Earnings

In th

ousands

For the period ended

Revenues:

Oil and gas

sales

Gas

gathering revenue and other

income

Total revenues

Expen

ses:

Lease operating expen

ses

Production ta

xes

Dep

reciation, dep

letion and amortization

Ceiling test

write

down

2011 A

160,486

$

214

160,700

38,57

1

3,100

58,24

3

18,90

7

2012 A

141,433

$

158

141,591

38,890

885

60,689

137,100

2013 A

31‐M

ar A

30‐Jun A

30‐Sep A

31‐Dec

E2014 E

31‐M

ar E

30‐Jun E

30‐Sep

E31‐Dec

E2015 E

182,804

$

59,966

$

60

,581

$

56,486

$

50,475

$

227,508

$

55,635

$

57,755

$

65,740

$

71,791

$

250,921

$

66

182,870

59,966

60,581

56,486

50,475

227,508

55,635

57,755

65,740

71,791

250,921

43,743

12,258

12,168

13,019

11,653

49,098

12,950

14,277

16,047

26,337

69,612

3,950

1,477

1,492

1,709

1,589

6,267

1,766

1,947

2,188

3,591

9,493

71,445

20,428

21,702

22,294

21,187

85,611

23,546

25,958

29,177

47,886

126,567

2015

E2014 E

Gen

eral and administrative expen

ses

Accretion of a

sset retiremen

t obligation

Interest

expen

se

Total expen

ses

20,43

6

2,049

9,648

150,954

22,957

2,07

8

9,80

8

272,407

26,512

6,242

6,467

6,319

6,156

25,184

6,785

7,044

8,018

8,756

30,602

1,753

791

708

724

739

2,962

732

725

718

712

2,887

21,886

7,636

7,380

7,050

7,140

29,206

7,182

7,182

7,182

7,182

28,728

169,289

48,832

49,917

51,115

48,463

198,327

52,962

57,133

63,331

94,464

267,889

Other

income (e

xpen

se)

Derivative expense

Net income (loss) b

efore

income taxes

Income tax expense

(ben

efit)

Net income (loss)

Preferred

dividen

ds

Net income (loss) available

to common shareholders

Earnings

(loss) p

er common share

Basic

Adjustmen

t for w

ritedown

Adjustmen

t for legal

settlemen

t

Adjustmen

t for e

arly

extinguishment o

f deb

t

Adjusted

basic

Diluted

Adjustmen

t for w

ritedown

Adjustmen

t for legal

settlemen

t

Adjustmen

t for e

arly

extinguishment o

f deb

t

Adjusted

diluted

Average

shares

outstanding

Average

shares

outstanding assuming dilution

PRODUCTION

SUMMARY

Gas

revenues

Oil revenues

1,008

8,738

(1,810)

10,548

$

5,139

5,409

$

0.08

$

0.31

$

0.39

$

0.08

$

0.30

$

0.38

$

61,93

7

62,32

5

100,420

60,06

4

606

(233)

(130,443)

1,63

6

(132,079)

$

5,13

9

(137,218)

$

(2.20)

$

2.20

$

(0.00)

$

(2.20)

$

(2.20)

$

62,459

62,459

84,797

56,636

588

189

215

198

198

800

198

198

198

198

792

233

1,982

1,982

127

127

14,402

11,323

10,879

5,569

4,192

31,963

2,999

820

2,607

(22,475)

(16,049)

320

‐

‐

(389)

1,551

1,162

1,110

303

965

(8,316)

(5,938)

14,082

$

11,323

$

10

,879

$

5,958

$

2,64

1$

30,801

$

1,889

$

517

$

1,642

$

(14,159

)$

(10,111)

$

5,139

1,280

1,287

1,287

1,287

5,141

1,287

1,287

1,287

1,287

5,148

8,943

$

10,043

$

9,592

$

4,671

$

1,35

4$

25,660

$

602

$

(770)

$

355

$

(15,446

)$

(15,259)

$

0.14

$

0.15

$

0.15

$

0.07

$

0.02

$

0.40

$

0.01

$

(0.01)

$

0.01

$

(0.24)

$

(0.24)

$

0.14

$

0.15

$

0.15

$

0.07

$

0.02

$

0.40

$

0.01

$

(0.01)

$

0.01

$

(0.24)

$

(0.24)

$

0.14

$

0.15

$

0.15

$

0.07

$

0.02

$

0.40

$

0.01

$

(0.01)

$

0.01

$

(0.24)

$

(0.24)

$

0.14

$

0.15

$

0.15

$

0.07

$

0.02

$

0.40

$

0.01

$

(0.01)

$

0.01

$

(0.24)

$

(0.24)

$

63,054

63,846

64,103

64,265

64,267

64,150

64,211

64,185

64,203

64,200

64,206

63,208

63,902

64,167

64,352

64,331

64,214

64,275

64,249

64,267

64,264

64,270

112,328

35,826

37,113

29,110

36,787

138,836

43,549

46,564

52,901

57,780

200,793

70,476

24,141

23,468

27,376

13,687

88,672

12,086

11,191

12,839

14,010

50,127

Production: gas

(MMcf)

Produciton: N

GL (M

boe)

Production: o

il (M

Bbls)

Production in

equivalent u

nits (M

Mcfe)

Production per

day

in equivalen

t units (m

mcfe)

chan

ges

YY changes

% of o

il production

% of gas

production

26,74

9

572

30,18

1

83

‐2

.48%

11.37%

88.63%

30,833

521

33,957

93

12.51%

9.20%

90.80%

33,980

8,315

9,354

10,550

7,573

35,793

8,177

9,028

10,257

11,037

38,499

320

320

457

529

575

1,991

3,552

681

242

230

170

184

826

142

130

147

160

578

38,066

9,769

10,736

11,570

10,593

40,749

11,773

12,979

14,589

23,943

41,969

104

109

117.97

125.77

115.15

112

131

144

162

266

115

‐4.42%

9.89%

7.78%

‐8.44%

11.14%

10.24%

12.40%

64.12%

12.10%

18.33%

23.64%

6.11%

3.64%

7.05%

20.51%

20.90%

26.08%

126.02%

2.99%

10.73%

14.88%

12.87%

8.82%

28.52%

12.16%

30.54%

30.44%

29.69%

53.91%

8.27%

89.27%

85.12%

87.13%

91.18%

71.48%

87.84%

69.46%

69.56%

70.31%

46.09%

91.73%

Average

price

of o

il (M

Bbl)

Average

price

of gas

(Mcfe)

Dep

letion ra

te

Lease operating cost

per

equivalen

t unit

Production ta

x/revenues

105.01

$

3.75

$

1.93

$

1.28

$

1.93%

108.79

$

2.75

$

1.79

$

1.15

$

0.63%

103.49

$

99.64

$

10

1.94

$

161.02

$

74.59

$

107.35

$

85.21

$

86

.08

$

87.57

$

87.64

$

86

.68

$

3.31

$

4.31

$

3.97

$

2.76

$

4.86

$

3.88

$

5.33

$

5.16

$

5.16

$

5.24

$

5.22

$

0.57

$

2.09

$

2.02

$

1.93

$

2.00

$

2.10

$

2.00

$

2.00

$

2.00

$

2.00

$

3.02

$

0.33

$

1.25

$

1.13

$

1.13

$

1.10

$

1.20

$

1.10

$

1.10

$

1.10

$

1.10

$

1.66

$

0.11%

2.46%

2.46%

2.82%

3.15%

2.75%

3.17%

3.37%

3.33%

5.00%

3.78%

PetroQuest En

ergy Inc. (PQ)

BURKEN

ROAD REP

ORTS (www.burken

road

.org)

November 7, 2014

30

PETROQUEST EN

ERGY INC. (PQ)

Annual

and Quarterly Earnings

For the period ended

SELECTED

COMMON‐SIZE AMOUNTS

2011 A

2012 A

2013 A

31‐M

ar A

30‐Jun A

30‐Sep A

31‐Dec

E2014 E

31‐M

ar E

30‐Jun E

30‐Sep

E31‐Dec

E2015 E

2015

E2014 E

Expen

ses:

Lease operating expen

ses

Production ta

xes

Dep

reciation, dep

letion and amortization

Gen

eral and administrative expen

ses

Net income (loss) b

efore

income taxes

Income tax expense

Net income (loss)

YEAR TO

YEA

R CHANGE

Oil and gas

sales

Lease operating expen

ses

Production ta

xes

Dep

reciation, dep

letion and amortization

Gen

eral and administrative expen

ses

24.03%

1.93%

36.29%

12.73%

5.44%

‐20.71%

6.57%

‐10.36%

‐1.13%

‐36.95%

‐1.83%

‐4.24%

27.50%

0.63%

42.91%

16.23%

‐92.23%

‐1.25%

‐93.39%

‐11.87%

0.83%

‐71.45%

4.20%

12.34%

6.86%

20.44%

20.09%

21.49%

23.09%

21.58%

23.28%

24.72%

24.41%

36.69%

27.74%

0.11%

2.46%

2.46%

2.82%

3.15%

2.75%

3.17%

3.37%

3.33%

5.00%

3.78%

11.80%

34.07%

35.82%

36.80%

41.97%

37.63%

42.32%

44.95%

44.38%

66.70%

50.44%

14.50%

10.41%

10.67%

10.43%

12.20%

11.07%

12.20%

12.20%

12.20%

12.20%

12.20%

7.88%

18.88%

17.96%

9.19%

8.31%

14.05%

5.39%

1.42%

3.97%

‐31.31%

‐6.40%

2.22%

0.00%

0.00%

‐6.99%

37.00%

3.64%

37.00%

37.00%

37.00%

37.00%

37.00%

7.70%

18.88%

17.96%

9.83%

5.23%

13.54%

3.40%

0.89%

2.50%

‐19.72%

‐4.03%

29.25%

66.68%

59.11%

9.00%

6.23%

24.45%

‐7.22%

‐4.66%

8.52%

42.23%

10.29%

‐67.77%

26.12%

37.69%

2.90%

‐7.04%

291.69%

5.65%

17.33%

23.26%

126.02%

41.78%

‐78.19%

43.68%

0.74%

36.94%

723.32%

3147.15%

19.56%

30.49%

28.04%

126.02%

51.47%

‐64.47%

58.71%

49.30%

‐0.81%

‐1.74%

297.03%

15.26%

19.61%

30.87%

126.02%

47.84%

15.49%

32.36%

1.83%

‐30.80%

‐2.49%

‐5.01%

8.70%

8.92%

26.88%

42.23%

21.52%

PetroQuest En

ergy Inc. (PQ)

BURKEN

ROAD REP

ORTS (www.burken

road

.org)

November 7, 2014

31

PETROQUEST EN

ERGY INC. (PQ)

Annual

and Quarterly Balance

Sheets

In th

ousands

As of

Current A

ssets:

Cash and cash equivalents

Revenue receivable

Joint Interest

billing receivable

Other

receivable

Hed

ge asset

Prepaid drilling costs

Drilling pipe inventory

Other

current a

ssets

Total current a

ssets

Oil and gas

properties

Oil and gas

properties,

full cost

method

Unevaluated

oil and gas

properties

Accumulated dep

reciation, dep

letion and amortization

Oil and gas

properties,

net

31‐Dec

A

22,263

$

15,86

0

47,44

5

6,418

2,900

4,070

2,965

101,921

1,600,546

70,40

8

(1,265,603)

405,351

31‐Dec‐12 A

14,904

$

17,742

42,595

9,208

830

1,

698

707

1,

900

89,584

1,734,477

71,713

(1,472,244)

333,946

31‐Dec‐13 A

31‐M

ar A

30‐Jun A

30‐Sep A

31‐Dec

E31‐Dec‐14 E

31‐M

ar E

30‐Jun E

30‐Sep

E31‐Dec

E31‐Dec‐15 E

9,153

$

11,991

$

30

,901

$

5,403

$

17,653

$

17,653

$

15,427

$

14,317

$

17,503

$

31,791

$

31,791

$

26,568

24,104

26,113

24,215

20,987

20,987

23,647

24,278

27,334

29,850

29,850

26,556

23,872

17,967

25,163

18,476

18,476

20,818

21,374

24,064

26,279

26,279

521

27

22

1,387

1,387

1,387

1,387

1,387

1,387

1,387

1,387

477

520

343

522

522

522

522

522

522

522

522

8,132

8,176

7,532

6,823

6,823

6,823

6,823

6,823

6,823

6,823

6,823

71,407

68,690

82,878

63,513

65,849

65,849

68,624

68,701

77,633

96,653

96,653

2,035,899

2,068,266

2,111,889

2,151,119

2,169,639

2,169,639

2,197,859

2,226,079

2,254,299

2,282,519

2,282,519

98,387

102

,707

126,571

128,217

128

,217

128,217

128,217

128,217

128,217

128,217

128,217

(1,553

,044)

(1,573,147)

(1,594,875)

(1,624

,980)

(1,646,167)

(1,646,167)

(1,669,713)

(1,695,671)

(1,724,848)

(1,772,734)

(1,772,734)

581,242

597

,826

643,585

654,356

651

,689

651,689

656,363

658,625

657,668

638,002

638,002

2015

E2014 E

Gas

gathering assets

Accumulated dep

reciation and amortization

Total property and equipmen

t

4,177

(1,794)

407,734

12,370

(7,607)

338,709

13,993

14,251

14,511

14,887

14,887

14,887

14,887

14,887

14,887

14,887

14,887