dp eurasia n.v. · 11 65 24 20 50 47 domino's pizza pizza hut little caesar's burger king...

TRANSCRIPT

Interim Results for the Period

ended 30 June 2017

DP Eurasia N.V.

2

This Presentation is not an offer to buy or sell any securities. Save where otherwise indicated, the Company is the source of the

content of this Presentation and, accordingly, although care has been taken to ensure that the facts stated in this Presentation are

accurate and that the opinions expressed are fair and reasonable, no representation, warranty or undertaking, express or implied, is

made by any of the Company, any of its directors, officers, employees, affiliates, advisors, shareholders or representatives as to,

and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions

contained herein. Neither the Company nor any of its directors, officers, employees, affiliates, advisors or representatives shall have

any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this Presentation or its contents

or otherwise arising in connection with the Presentation.

Certain statements in this Presentation are not historical facts and are “forward looking” statements. These forward-looking

statements can be identified by the use of forward-looking terminology, including the terms “believes”, “estimates”, “anticipates”,

“expects”, “intends”, “plans”, “may”, “will” or “should” or, in each case, their negative or other variations or comparable terminology.

None of the Company, its directors, officers, employees, affiliates, advisors, shareholders or representatives intend or have any

duty or obligation to supplement, amend, update or revise any of the forward-looking statements contained in this Presentation or to

update or to keep current any other information contained in this Presentation. The information and opinions contained in this

Presentation are provided as at the date of this Presentation and are subject to change without notice. As a result, you are

cautioned not to place undue reliance on such forward looking statements.

Disclaimer

3

Aslan Saranga

Chief Executive Officer

Selim Kender

Chief Strategy Officer and Head of Investor Relations

Presentation Team

SECTION 1

Overview

5

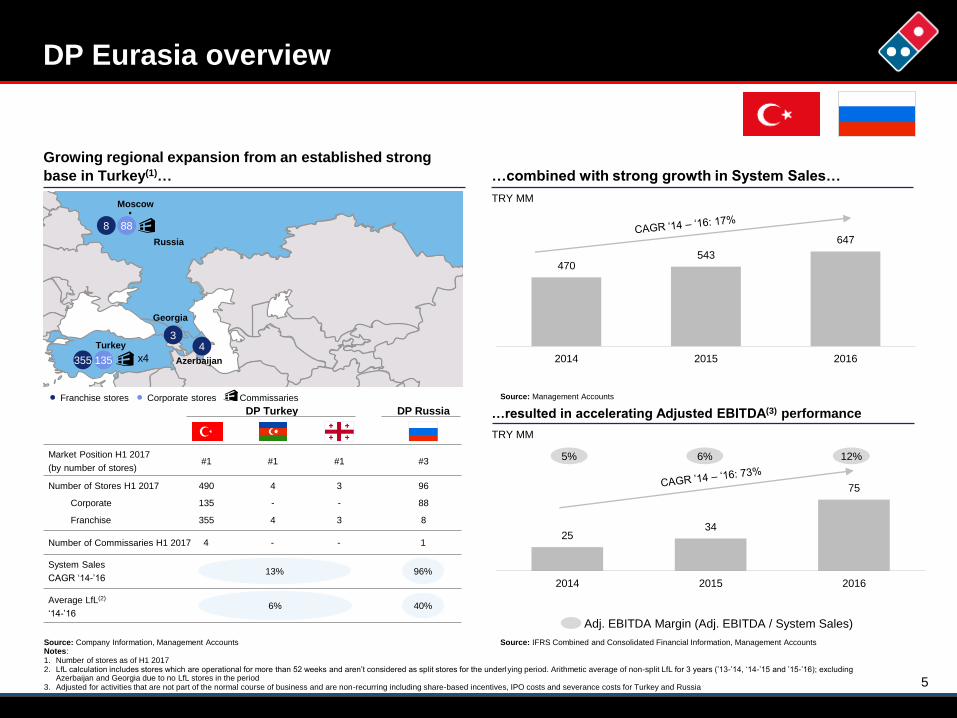

DP Eurasia overview

Growing regional expansion from an established strong

base in Turkey(1)…

DP Russia

Market Position H1 2017

(by number of stores)

Number of Stores H1 2017

#1 #1 #3

Corporate

Franchise

System Sales

CAGR ‘14-’16

490 96

135 88

355 8

Average LfL(2)

‘14-’16

DP Turkey

#1

4

-

4

3

-

3

13%

6%

Number of Commissaries H1 2017 4 1- -

96%

40%

Turkey

Russia

Georgia

Azerbaijan

Moscow

88

355 135

34

x4

8

Commissaries Franchise stores Corporate stores

…combined with strong growth in System Sales…

Adj. EBITDA Margin (Adj. EBITDA / System Sales)

TRY MM

…resulted in accelerating Adjusted EBITDA(3) performance

TRY MM

Source: Company Information, Management AccountsNotes:1. Number of stores as of H1 20172. LfL calculation includes stores which are operational for more than 52 weeks and aren’t considered as split stores for the underlying period. Arithmetic average of non-split LfL for 3 years (’13-’14, ‘14-’15 and ’15-’16); excluding

Azerbaijan and Georgia due to no LfL stores in the period3. Adjusted for activities that are not part of the normal course of business and are non-recurring including share-based incentives, IPO costs and severance costs for Turkey and Russia

Source: IFRS Combined and Consolidated Financial Information, Management Accounts

Source: Management Accounts

470543

647

2014 2015 2016

2534

75

2014 2015 2016

5% 6% 12%

6

H1 2017 Highlights

- - -

AUG JUN

6.9% 31.3% 602 593

LIKE-FOR-LIKE GROWTH

38.5%

REVENUE

TRY 289.8 m

STORE COUNT

SYSTEM SALES Adjusted EBITDA

TRY 398.5 m TRY 39.4 m

26.4%

TRY 30.0 m

29.0%

CAPEX

SECTION 2

Operational Review

8

370 432 466 495 498

1319

4372 104

80103

130160

219289

383451

509567

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Aug 2017

DP RussiaDP Turkey

Store count growth

…with Russia surpassing 100 in less than 4 years

# of stores at period end

Source: Company Information

500th store in Turkey imminent...

# of stores at period end

# of stores at period end

Continuous and significant store rollout

Source: Company Information Source: Company Information

+23+27

+30+59

+70

+94+68

+58+58

462488

463490 490

400

500

600

2015 2016 H1 2016 H1 2017 Aug 2017

4372

45

96 104

0

50

100

150

2015 2016 H1 2016 H1 2017 Aug 2017

602

+35

+26 +27 +29

+51

9

Like-for-like performance

18%

7%

33%

7%

Online Total

H1 2016 H1 2017

225%

59%85%

31%

Online Total

H1 2016 H1 2017

Turkey Russia

System sales LfL growth, %

LfL performance in line with guidance

Source: Company Information

10

Online channel

48%

32%

63%

42%

Delivery Total

H1 2016 H1 2017

39%

25%

46%

30%

Delivery Total

H1 2016 H1 2017

Online system sales, %

Share of online ordering growing healthily

40%

25%

50%

33%

Delivery Total

H1 2016 H1 2017

Source: Company Information

Turkey Russia

Group

11

65

2420

50 47

Domino'sPizza

PizzaHut

LittleCaesar's

BurgerKing

McDonald's

85.6

H1 2017

93.2

H1 2017

Why do consumers choose DP Eurasia?

Attractive pricing vs competitors in Turkey

and Russia with high value for money

Value for money?

% of affirmative respondents

4033

28

Domino's Pizza Pizza Hut Papa John's

Value for money?(1)

% of affirmative respondents

Delivery on Time, % Delivery on Time, %

RussiaTurkey

Innovation – New Products

Quick delivery times all year round in Turkey and

Russia, despite the challenging weather conditions

Market positioning

I II

III

Source: Ipsos Connect Brand Health and Ad Tracking,Feb/Mar 2017

Source: Company Information

Source: Company Information

Notes:1. The figures are representing only Moscow

Source: "Russian OHD market and dining habits" consumer survey in 2016 conducted by Ipsos

Chicken popcorn Cold chocolate bites Greek salad Caesar salad

SECTION 3

Financial Results

13

31

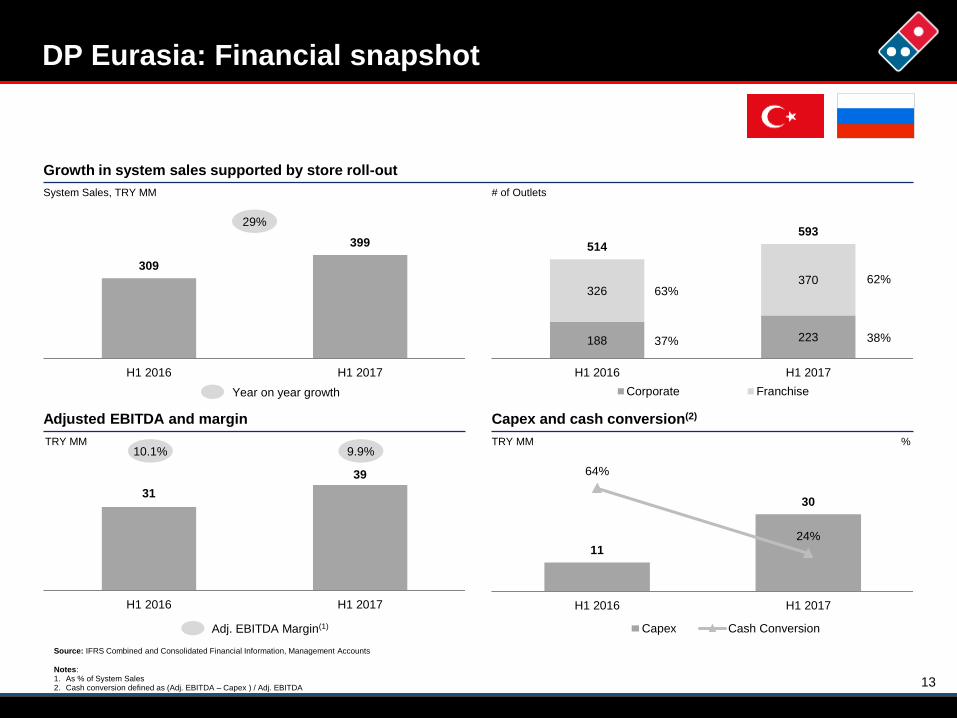

39

H1 2016 H1 2017

309

399

H1 2016 H1 2017

Year on year growth

188 223

326370

514

593

H1 2016 H1 2017

Corporate Franchise

DP Eurasia: Financial snapshot

System Sales, TRY MM

11

30

64%

24%

H1 2016 H1 2017

Capex Cash Conversion

TRY MM %

63%

37%

# of Outlets

29%

TRY MM

Growth in system sales supported by store roll-out

Adjusted EBITDA and margin Capex and cash conversion(2)

Source: IFRS Combined and Consolidated Financial Information, Management Accounts

Notes:1. As % of System Sales2. Cash conversion defined as (Adj. EBITDA – Capex ) / Adj. EBITDA

10.1%

Adj. EBITDA Margin(1)

9.9%

62%

38%

14

DP Turkey: Financial snapshot(1)

29

34

H1 2016 H1 2017

279 308

H1 2016 H1 2017

Year on year growth

143 135

320 355

463 490

H1 2016 H1 2017

Corporate Franchise

System Sales, TRY MM

TRY MM %

69%

31%

# of Outlets

11%

TRY MM

System Sales

Adjusted EBITDA and margin Capex and cash conversion(4)

Source: IFRS Combined and Consolidated Financial Information, Management Accounts

Notes:1. Including contributions from Azerbaijan and Georgia2. Turkey only

10.5%

Adj. EBITDA Margin(3)

11.1%

72%

28%

Store count(2)

3. As % of System Sales4. Cash conversion defined as (Adj. EBITDA – Capex ) / Adj. EBITDA

611

78%68%

H1 2016 H1 2017

Capex Cash Conversion

15

DP Russia: Financial snapshot

25

H1 2016 H1 2017

30

91

H1 2016 H1 2017

Year on year growth

88

8

45

96

H1 2016 H1 2017

Corporate Franchise

System Sales, TRY MM

TRY MM

# of Outlets

200%

TRY MM

System Sales

Adjusted EBITDA Capex

Source: IFRS Combined and Consolidated Financial Information, Management Accounts

Notes:1. As % of System Sales

5.9%

Adj. EBITDA Margin(1)

5.6%

8%

92%

Store count

5

19

H1 2016 H1 2017

16

65%

35%

TRY EUR

Cash flow generation and debt profile

Notes:1. Adjusted for activities that are not part of the normal course of business and are non-recurring including share-based incentives, IPO costs and severance costs for Turkey and Russia2. Adjusted net debt is calculated as sum of short-term borrowings and long-term borrowings, less cash and cash equivalents and adjusted for non-recurring items including long term deposit for loan guarantee and delay in

collection/payment day coinciding on a weekend

31 39

(11)(30)

20 9

H1 2016 H1 2017

Adj. EBITDA Capex Adj. EBITDA - Capex Cash Conversion

146 171

53 47

200217

1.9x 2.0x

2016 H1 2017

Adj. Net Debt Gross Debt

TRY MM TRY MM

Cash flow generation

DP Eurasia’s debt profile by currency DP Eurasia’s debt profile by segment

Source: IFRS Combined and Consolidated Financial Information

Debt profile of DP Eurasia

64% 24%

(1) Adj. Net Debt / Adj. EBITDA LTM(2) (1)(2)

28%

68%

5%

TRY EUR RUB

8%

92%

RUB EUR

H1 2017 Russian Gross Debt

TRY 124 MM

H1 2017 Turkish Gross Debt

TRY 93 MM

H1 2017 Gross Debt

TRY 217 MM

75% Hedged

via EUR

deposit

17

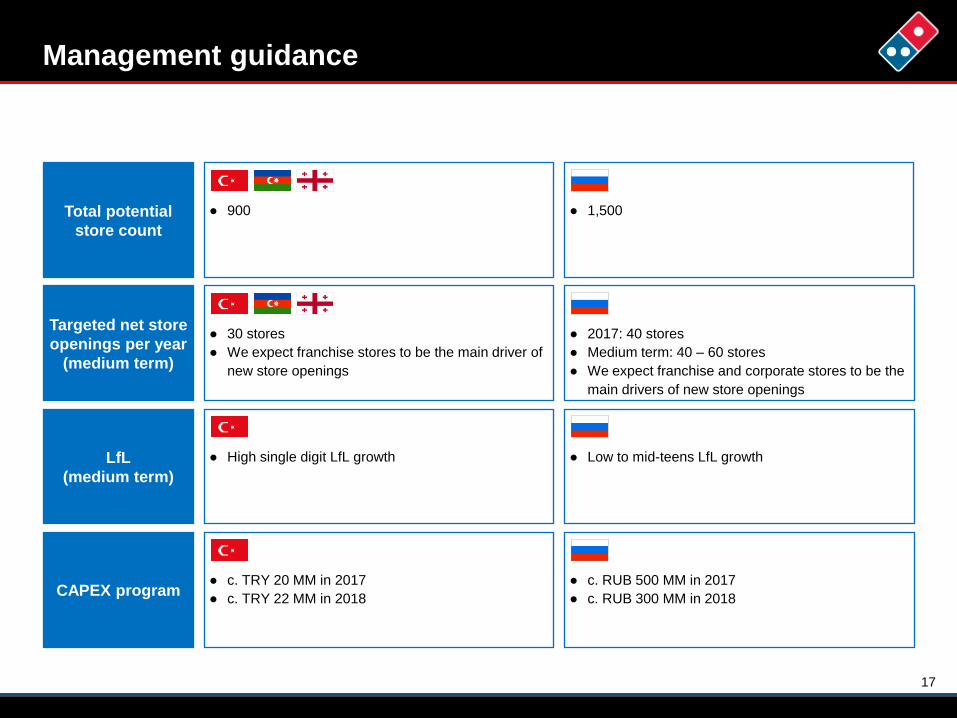

Management guidance

Total potential

store count

Targeted net store

openings per year

(medium term)

LfL

(medium term)

CAPEX program

● 900 ● 1,500

● High single digit LfL growth ● Low to mid-teens LfL growth

● 30 stores

● We expect franchise stores to be the main driver of

new store openings

● 2017: 40 stores

● Medium term: 40 – 60 stores

● We expect franchise and corporate stores to be the

main drivers of new store openings

● c. TRY 20 MM in 2017

● c. TRY 22 MM in 2018

● c. RUB 500 MM in 2017

● c. RUB 300 MM in 2018

SECTION 4

Conclusion

19

Conclusion

Source: Company Information

• Solid topline and profitability growth

o System Sales: 29.0%

o Adjusted EBITDA: 26.4%

• LfL growth in line with guidance

• Online share increasing: ~ 50% of delivery

• Milestone store openings achieved in August

o Group: exceeded 600

o Russia: exceeded 100

APPENDIX

21

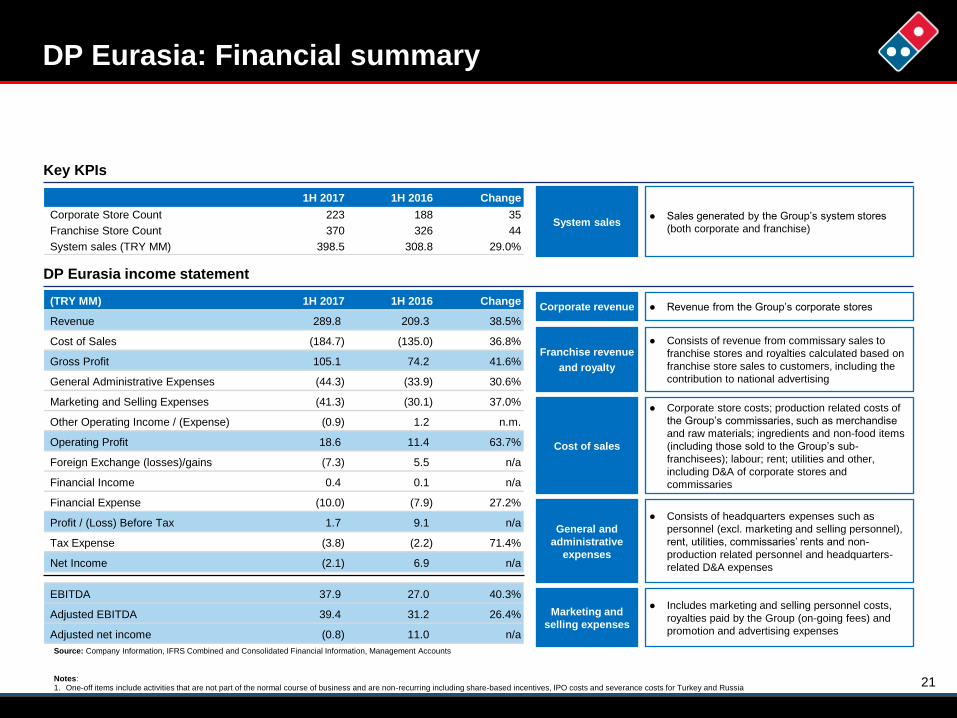

DP Eurasia: Financial summary

Key KPIs

DP Eurasia income statement

System sales● Sales generated by the Group’s system stores

(both corporate and franchise)

Corporate revenue ● Revenue from the Group’s corporate stores

Franchise revenue

and royalty

● Consists of revenue from commissary sales to

franchise stores and royalties calculated based on

franchise store sales to customers, including the

contribution to national advertising

Cost of sales

● Corporate store costs; production related costs of

the Group’s commissaries, such as merchandise

and raw materials; ingredients and non-food items

(including those sold to the Group’s sub-

franchisees); labour; rent; utilities and other,

including D&A of corporate stores and

commissaries

General and

administrative

expenses

● Consists of headquarters expenses such as

personnel (excl. marketing and selling personnel),

rent, utilities, commissaries’ rents and non-

production related personnel and headquarters-

related D&A expenses

Marketing and

selling expenses

● Includes marketing and selling personnel costs,

royalties paid by the Group (on-going fees) and

promotion and advertising expenses

Source: Company Information, IFRS Combined and Consolidated Financial Information, Management Accounts

Notes:1. One-off items include activities that are not part of the normal course of business and are non-recurring including share-based incentives, IPO costs and severance costs for Turkey and Russia

1H 2017 1H 2016 Change

Corporate Store Count 223 188 35

Franchise Store Count 370 326 44

System sales (TRY MM) 398.5 308.8 29.0%

(TRY MM) 1H 2017 1H 2016 Change

Revenue 289.8 209.3 38.5%

Cost of Sales (184.7) (135.0) 36.8%

Gross Profit 105.1 74.2 41.6%

General Administrative Expenses (44.3) (33.9) 30.6%

Marketing and Selling Expenses (41.3) (30.1) 37.0%

Other Operating Income / (Expense) (0.9) 1.2 n.m.

Operating Profit 18.6 11.4 63.7%

Foreign Exchange (losses)/gains (7.3) 5.5 n/a

Financial Income 0.4 0.1 n/a

Financial Expense (10.0) (7.9) 27.2%

Profit / (Loss) Before Tax 1.7 9.1 n/a

Tax Expense (3.8) (2.2) 71.4%

Net Income (2.1) 6.9 n/a

EBITDA 37.9 27.0 40.3%

Adjusted EBITDA 39.4 31.2 26.4%

Adjusted net income (0.8) 11.0 n/a

22

DP Eurasia: Revenue & Expense Breakdown

Notes:1. One-off items include activities that are not part of the normal course of business and are non-recurring including share-based incentives, IPO costs and severance costs for Turkey and Russia

(TRY MM) 1H 2017 1H 2016 Change 1H 2017 1H 2016

System sales 398.5 308.8 29%

Corporate 173.8 117.9 48% as a % of system sales 43.6% 38.2%

Franchise 224.7 190.9 18% as a % of system sales 56.4% 61.8%

1H 2017 1H 2016 Change 1H 2017 1H 2016

Revenue 289.8 209.3 38%

Corporate 173.8 117.9 48% as a % of revenue 60.0% 56.3%

Franchise 103.4 85.2 21% as a % of revenue 35.7% 40.7%

Other revenue 12.5 6.2 102% as a % of revenue 4.3% 3.0%

Cost of Sales (184.7) (135.0) 37%

Cost of Food/Non-Food/Transportation (100.5) (76.4) 32% as a % of system sales 25.2% 24.7%

Corporate Store Expenses (70.5) (46.8) 51% as a % of corporate system sales 40.5% 39.7%

Depreciation and Amortization (13.7) (11.8) 16%

Gross Profit 105.1 74.2 42% as a % of system sales 26.4% 24.0%

General Administrative Expenses (44.3) (33.9) 31%

Overhead (Including Commisary) (38.6) (26.1) 48%

of w hich one-off (1.4) (0.2)

Overhead (excluding one-offs) (37.2) (25.9) 44% as a % of system sales 9.3% 8.4%

Share based incentives (0.1) (4.0) n/a

Depreciation and Amortization (5.6) (3.8) 46%

Marketing and Selling Expenses (41.3) (30.1) 37%

Marketing and Advertising (23.0) (16.3) 41% as a % of system sales 5.8% 5.3%

Corporate Store Local Marketing (2.5) (1.9) 31% as a % of corporate system sales 1.5% 1.6%

Royalty (15.8) (11.9) 32% as a % of system sales 4.0% 3.9%

Other Operating Income / (Expense) (0.9) 1.2 n/a

Operating Profit 18.6 11.4 64%

23

(TRY MM) 1H 2017 1H 2016

System Sales 308.0 278.7

Operating profit 19.4 11.8

D&A 13.5 13.6

EBITDA 32.8 25.4

Non-recurring (income)/expenses 1.5 4.0

Adjusted EBITDA 34.3 29.4

% of system sales 11.1% 10.5%

Adjusted EBIT 20.8 15.8

% of system sales 6.8% 5.7%

Capital expenditures 11.0 6.5

Cash conversion 67.9% 78.0%

(TRY MM) 1H 2017 1H 2016

System Sales 398.5 308.8

Operating profit 18.6 11.4

D&A 19.3 15.6

EBITDA 37.9 27.0

Non-recurring (income)/expenses 1.5 4.2

Adjusted EBITDA 39.4 31.2

% of system sales 9.9% 10.1%

Adjusted EBIT 20.1 15.5

% of system sales 5.0% 5.0%

Capital expenditures 30.0 11.2

Cash conversion 23.7% 64.2%

(TRY MM) 1H 2017 1H 2016

System Sales 90.5 30.1

Operating profit (0.8) (0.4)

D&A 5.8 2.0

EBITDA 5.0 1.6

Non-recurring (income)/expenses 0.0 0.2

Adjusted EBITDA 5.1 1.8

% of system sales 5.6% 5.9%

Adjusted EBIT (0.7) (0.2)

% of system sales -0.8% -0.8%

Capital expenditures 19.0 4.7

Cash conversion n.m. n.m.

Adjusted EBITDA and Net Debt calculation

DP Turkey DP Russia

DP Eurasia

Notes:1. Excludes income and expenses which are not part of normal course of business and are non-recurring items

(TRY MM) 1H 2017 2016

Short term bank borrowings 113.4 115.9

Short-term portions of long-term financial lease borrowings 3.9 3.0

Long-term bank borrowings 91.6 73.3

Long-term financial lease borrowings 8.5 7.3

Total borrowings 217.5 199.5

Cash and cash equivalents 21.6 19.5

Net debt 195.9 180.0

Non-recurring items

Long term deposit for loan guarantee (25.0) (23.2)

Adjusting delay in collection/payment day coinciding on a

weekend- (10.4)

Adjusted net debt 170.9 146.4

24

Exchange Rates

Source: Company Information

Currency Period End Period Average Period End Period Average

EUR/TRY 4.003 3.931 3.204 3.256

RUB/TRY 0.059 0.062 0.045 0.041

EUR/RUB 67.499 62.719 71.210 78.367

Currency Period End Period Average Period End Period Average

EUR/TRY 3.710 3.338 3.178 3.019

RUB/TRY 0.057 0.045 0.040 0.045

EUR/RUB 63.811 74.231 79.697 67.777

Period ended 30 June

2017 2016

Year ended 31 December

2016 2015

25

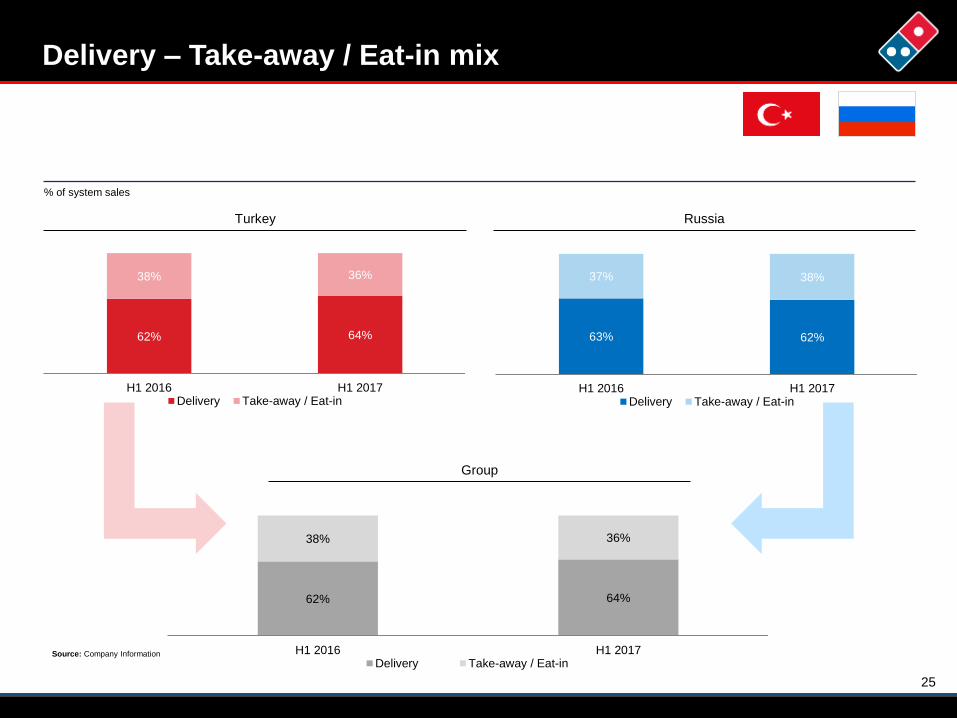

Delivery – Take-away / Eat-in mix

% of system sales

Source: Company Information

Turkey Russia

Group

62% 64%

38% 36%

H1 2016 H1 2017Delivery Take-away / Eat-in

62% 64%

38% 36%

H1 2016 H1 2017Delivery Take-away / Eat-in

63% 62%

37% 38%

H1 2016 H1 2017Delivery Take-away / Eat-in