downloads 7 2698 3039 fraud the facts final 5

TRANSCRIPT

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 1/84

FRAUDTHE FACTS 2011THE DEFINITIVE OVERVIEW OF PAYMENT INDUSTRY FRAUDAND MEASURES TO PREVENT IT

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 2/84

Financial Fraud Action UK is the name under whichthe financial services industry co-ordinates itsactivity on fraud prevention, presenting a united frontagainst financial fraud and its effects. FinancialFraud Action UK works in partnership with The UKCards Association on industry initiatives to preventfraud on credit and debit cards, with the FraudControl Steering Group on non-card fraud mattersand the Cheque and Credit Clearing Company on

credit clearing and cheque fraud.

The UK Cards Association is the leading tradeassociation for the cards industry in the UK.With a membership that includes all major credit,debit and charge card issuers, and card acquiringbanks, the role of the Association is both to unifyand represent the UK card payments industry.It is responsible for formulating and implementingpolicy on non-competitive aspects of cardpayments including fraud prevention.

The Cheque and Credit Clearing Company is a

membership-based industry body which managesthe cheque clearing system in Great Britain. It alsocovers the management of the systems for clearingpaper bank giro credits, Euro-denominatedcheques and US Dollar cheques.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 3/84

“The cards industry is greatly encouraged by the major decrease in card fraudlosses for a second consecutive year, but we will not be easing off our efforts as aresult. It is essential to us that customers feel safe and secure when they use theircards and we will continue to invest in a wide range of fraud prevention initiativesto keep it this way.”

MELANIE JOHNSON, Chair of The UK Cards Association

“The year-on-year fall in online banking losses is testament to the efforts of allthose involved in combating this type of fraud. We remain committed to containingand reducing all areas of fraud and will continue to work with key partners toachieve this end.”

DAVID COOPER, Chairman of the Fraud Control Steering Group

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 4/84

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 5/84

P L A S T I C

C A R D S

PLASTIC CARDFRAUDOVERVIEW OF TYPES OF PLASTIC CARD FRAUD 08

INDUSTRY MEASURES TO PREVENT PLASTIC CARD FRAUD 35

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 6/84

06// PLASTIC CARD FRAUD

FRAUD LOSSES ON UK-ISSUED CARDS 2000-2010Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

100

200

300

400

500

3 1 7 . 0

+ 6 8 % 4

1 1 . 5

+ 3 0 %

4 2 4 . 6 + 3 %

4 2 0 . 4 - 1 % 5

0 4 . 8

+ 2 0 %

4 3 9 . 4

- 1 3 %

4 2 7 . 0 - 3 % 5

3 5 . 2

+ 2 5

%

6

0 9 . 9

+ 1 4 %

4 4 0 . 0

- 2 8 %

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

3 6 5 . 4

- 1 7 %

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 7/84

// 07

Due to the rounding of figures, the sum of separate items may differ from the totals shown.

P L A S T I C

C A R D S

ANNUAL FRAUD LOSSES ON UK-ISSUED CARDS 1999-2009All figures in £ millions

Fraud type 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Card-not-present 72.9 95.7 110.1 122.1 150.8 183.2 212.7 290.5 328.4 266.4 226.9 -15%

Counterfeit 107.1 160.4 148.5 110.6 129.7 96.8 98.6 144.3 169.8 80.9 47.6 -41%

Lost/stolen 101.9 114.0 108.3 112.4 114.4 89.0 68.5 56.2 54.1 47.7 44.4 -7%

Card ID theft 17.4 14.6 20.6 30.2 36.9 30.5 31.9 34.1 47.4 38.2 38.1 0%

Mail non-receipt 17.7 26.8 37.1 45.1 72.9 40.0 15.4 10.2 10.2 6.9 8.4 +22%

TOTAL 317.0 411.5 424.6 420.4 504.8 439.4 427.0 535.2 609.9 440.0 365.4 -17%

Contained within this total/breakdown by location

UK 213.4 273.0 294.4 316.3 412.3 356.6 309.9 327.6 379.7 317.4 271.5 -14%

Fraud abroad 103.5 138.4 130.2 104.1 92.5 82.8 117.1 207.6 230.1 122.6 93.9 -23%

+/-change09/10

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 8/84

08// PLASTIC CARD FRAUD

OVERVIEW

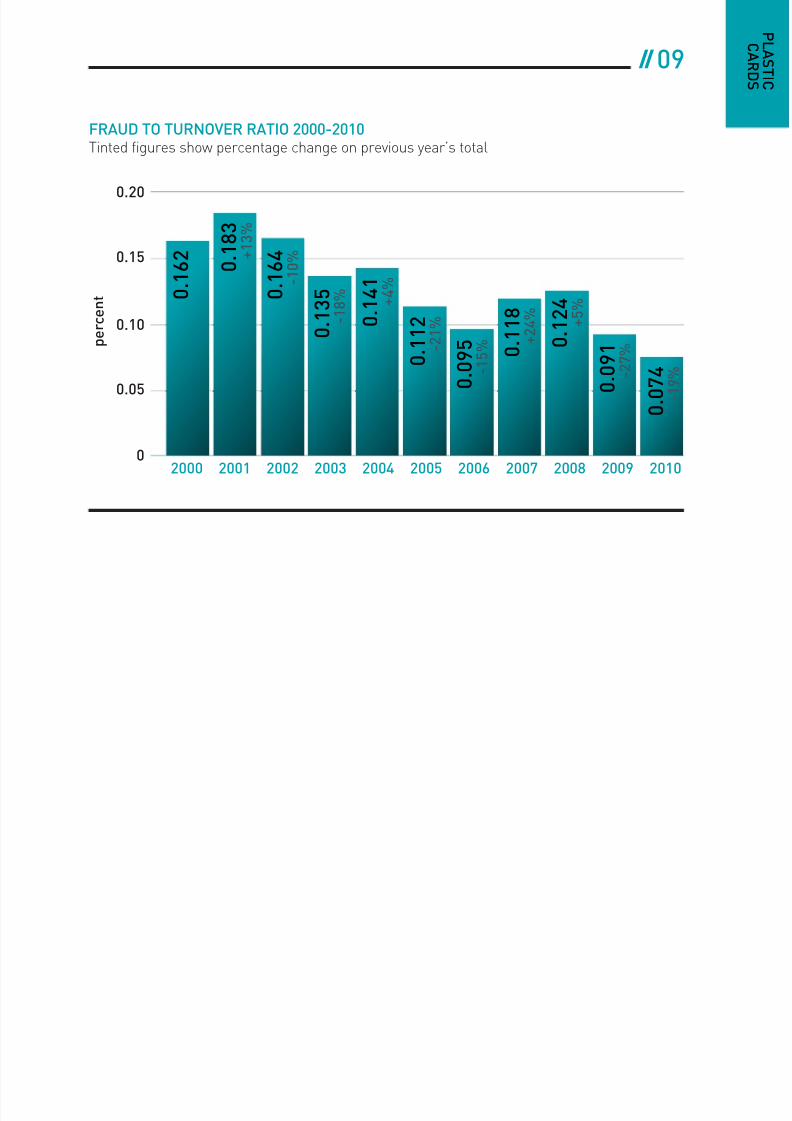

Total fraud losses on UK cards fell by 17%between 2009 and 2010 to £365.4 million.This is the lowest annual total since 2000and follows on from a fall of 28 per cent inthe previous year.

Whilst card usage and transaction volumescontinue to grow, card fraud losses against

total turnover – at 0.074% – continue todecrease and have now fallen by 40 per centin the past two years.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 9/84

// 09

P L A S T I C

C A R D S

FRAUD TO TURNOVER RATIO 2000-2010Tinted figures show percentage change on previous year’s total

p e r c e n t

0

0.05

0.10

0 . 1

6 2

0 . 1 8 3

+ 1 3 %

0 . 1

6 4

- 1 0 %

0 . 1 3 5

- 1 8 %

0 . 1 4 1

+ 4 %

0 . 1 1 2

- 2 1 %

0 . 0 9 5

- 1 5 % 0

. 1 1 8

+ 2 4 %

0 . 1 2 4

+ 5 %

0 . 0 9 1

- 2 7 %

0.15

0.20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

0 . 0 7 4

- 1 9 %

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 10/84

10// PLASTIC CARD FRAUD

CARD FRAUD LOSSES SPLIT BY TYPE (AS PERCENTAGE OF TOTAL LOSSES)

Lost/stolen

Mail non-receipt

Counterfeit

Card-not-present

Card ID theft

2000 2010

32%

10% 12%2%

13%

62%

6%

34%

23%

5%

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 11/84

// 11

P L A S T I C

C A R D S

FRAUD LOSSES ON UK-ISSUED CARDS SPLIT BY UK REGION 2006-2010All figures in £ millions

Region 2006 2007 2008 2009 2010

South East 176.6 179.0 204.6 167.8 156.6 -7%

North West 35.7 35.6 42.4 39.0 23.5 -40%

East Midlands 15.0 22.8 24.3 19.4 13.6 -30%

West Midlands 17.2 24.4 23.5 22.4 16.5 -26%

Yorkshire & Humberside 27.2 24.0 22.1 18.5 15.4 -17%

South West 9.7 11.8 19.2 13.0 13.4 3%

Scotland 9.9 11.5 17.9 11.4 10.6 -7%

North East 6.8 7.7 10.0 10.1 7.8 -23%

East Anglia 5.4 4.8 7.6 6.1 5.4 -11%

Wales 5.7 5.3 7.2 8.2 7.9 -4%

Northern Ireland 0.7 0.7 0.7 1.4 0.8 -39%

UK TOTAL 309.9 327.6 379.7 317.7 271.5 -14% Fraud abroad 117.1 207.6 230.1 122.7 93.9 -23%

TOTAL ALL UK CARDS 427.0 535.2 609.9 440.0 365.4 -17%

+/- change09/10

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 12/84

12// PLASTIC CARD FRAUD

PHONE, INTERNET ANDMAIL ORDER (CARD-NOT-PRESENTOR CNP) FRAUD£226.9 MILLION IN 2010 (DOWN 15%)

This crime most commonly involves the theftof genuine card details that are then used tomake a purchase over the internet, by phone,or by mail order.

In general, the difficulty in countering this typeof fraud lies in the fact that neither the cardnor the cardholder is present when thetransaction happens.

Card-not-present fraud accounts formore than half of all card fraud, but theselosses have to be seen in the context of a

massive growth in CNP spending over the

past ten years, especially over the internet.

In light of this growth it is all the moreimpressive that CNP fraud has fallen for thesecond successive year.

The reasons behind the continued decreaseinclude the increasing use of sophisticatedfraud screening detection tools by retailersand banks, as well as the growth in the use

of MasterCard SecureCode and Verified byVisa by both online retailers and cardholders.

The industry’s Be Card Smart Onlinecampaign, launched at the end of 2008,provides consumers with straightforwardpractical tips to help them shop safelyon the internet.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 13/84

// 13

CARD-NOT-PRESENT FRAUD LOSSES ON UK-ISSUED CARDS IN 2000-2010Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

50

100

150

200

250

7 2 . 9

+ 1 4 9 %

9 5 . 7

+ 3 1 %

1 1 0 . 1

+ 1 5 %

1 2 2 . 1

+ 1 1 %

1 5 0 . 8

+ 2 4 %

1 8 3 . 2

+ 2 1 %

2 1 2 . 7

+ 1 6 %

2 9

0 . 5

+ 3 7 %

3 2 8 . 4

+ 1 3 %

2 6 6 . 4

- 1 9

%

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

2 2 6 . 9

- 1 5 %

P L A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 14/84

14// PLASTIC CARD FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 15/84

// 15

COUNTERFEIT CARD FRAUD£47.6 MILLION IN 2010 (DOWN 41%)

Counterfeit card fraud occurs when a fake cardis created by fraudsters using compromiseddetails from the magnetic stripe of agenuine card.

This type of fraud has fallen by 72 per cent inthe past two years. There are several factors

for this, including:- More and more countries have now

introduced chip and PIN technology,which makes it much harder to use fakeUK cards overseas.

- Increasing use by card companies ofsophisticated fraud prevention software.

- The banking industry working closely withthe retail community to raise awareness ofthe ways in which retailers can protect theirchip and PIN terminals from criminal

attack – minimising the opportunities for

card details to be electronically copied.- The continuing rollout of debit and credit

cards with enhanced security features.Cards with an updated integrated cardverification value (iCVV) have been rolledout since January 2008 and as of the endof December 2010 there were more than

134 million issued in the UK. In additionsome issuers are also rolling outDynamic Data Authentication (DDA)cards and at the end of December 2010there were more than 60 million of thesecards in circulation.

- The successful work of the bankingindustry-sponsored special police unit,

the Dedicated Cheque and PlasticCrime Unit (DCPCU), which has preventedapproximately £368 million in fraudlosses in the past nine years.

P L A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 16/84

16// PLASTIC CARD FRAUD

COUNTERFEIT CARD FRAUD LOSSES IN THE UK AND ABROAD 2006-2010All figures in £ millions

Region 2006 2007 2008 2009 2010

Domestic (in the UK) 45.8 31.0 36.2 24.5 16.8 -31%

Abroad 52.8 113.3 133.6 56.4 30.8 -45%

TOTAL 98.6 144.3 169.8 80.9 47.6 -41%

+/- change09/10

Counterfeit card fraud losses in the UK have

decreased by 63% since 2004 – this is due tothe fact that chip and PIN has made it much

harder for criminals to use fake cards in

cash machines and shops in the UK.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 17/84

// 17

COUNTERFEIT CARD FRAUD LOSSES ON UK-ISSUED CARDS IN 2000-2010

Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

50

100

150

4 7 . 6

- 4 1 %

1 0 7 . 1

+ 1 1 3 %

1 6 0 . 4

+ 5 0 %

1 4 8 . 5

- 7 %

1 1 0 . 6

- 2 6 %

1 2 9 . 7

+ 1 7 %

9 6 . 8

- 2 5 %

9 8 . 6 + 2 %

1 4 4 . 3

+ 4 6 % 1

6 9 . 8

+ 1 8 %

8 0 . 9

- 5 2 %

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

P L A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 18/84

18// PLASTIC CARD FRAUD

LOST AND STOLEN CARD FRAUD£44.4 MILLION IN 2010 (DOWN 7%)

This category covers fraud on cards that havebeen reported by the cardholder as lost orstolen. Lost and stolen cards could be usedin shops that do not have chip and PINequipment, or to commit fraud via atelephone, internet or mail order transaction.

Thanks to the introduction of chip and PINthis fraud type is now at its lowest levelsince the industry collation of fraud lossesbegan in 1991.

Other banking industry initiatives in place

to tackle this type of fraud include:- Intelligent computer systems that card

companies use to track customer accountsfor unusual spending patterns.

- An Industry Hot Card File (IHCF) thatenables retailers to checkelectronically whether a card has been

reported lost or stolen.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 19/84

// 19

LOST AND STOLEN FRAUD LOSSES ON UK-ISSUED CARDS 2000-2010

Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

20

40

60

80

100

4 4 . 4 - 7 %

1

0 1 . 9

+ 2 8 %

1 1 4 . 0

+ 1 2 %

1 0 8 . 3 - 5 %

1 1 2 . 4 + 4 %

1 1 4 . 4 + 2 %

8 9 . 0

- 2 2 %

6 8 . 5

- 2 3 %

5 6 . 2

- 1 8 %

5 4 . 1 - 4 %

4 7 . 7

- 1 1 %

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

P L A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 20/84

20// PLASTIC CARD FRAUD

CARD ID THEFT£38.1 MILLION IN 2010

Card ID theft occurs when a criminal usesa fraudulently obtained card or card details,along with stolen personal information, toopen or take over a card account held insomeone else’s name.

This type of fraud can be split into twocategories: third-party application fraudand account takeover fraud.

// APPLICATION FRAUD

£5.1 MILLION IN 2010 (DOWN 50%)

Application fraud occurs when criminals usestolen or fake documents to open an account

in someone else’s name. Criminals may tryto steal documents such as utility bills and

bank statements to build up useful personal

information. Alternatively, they may usecounterfeit documents for identificationpurposes.

// ACCOUNT TAKEOVER

£33.0 MILLION IN 2010 (UP 18%)

This involves a criminal fraudulently using

another person’s credit or debit cardaccount, first by gathering information aboutthe intended victim, then contacting theirbank or credit card issuer whilstmasquerading as the genuine cardholder.The criminal will then arrange for funds tobe transferred out of the account, or willchange the address on the account and ask

for new or replacement cards to be sent tothe new address.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 21/84

// 21

ID THEFT ON UK-ISSUED CARDS 2000-2010

Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

10

20

30

40

1 7 . 4

+ 2 1 %

1

4 . 6

- 1 6 % 2

0 . 6

+ 4 1 %

3 0 . 2

+ 4 7 %

3 6 . 9

+ 2 2

%

3 0 . 5

- 1 7 %

3 1 . 9 + 5 %

3 4 . 1 + 7 %

4 7 . 4

+ 3 9 %

3 8

. 2

- 1

9 %

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

3 8

. 1 0 %

P L A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 22/84

22// PLASTIC CARD FRAUD

Fraudsters are focusing on account

takeover, rather than application fraud,as the current economic climate hasgenerally made it much more difficult foranyone, including criminals, to establishnew lines of credit. Overall though, theincrease in account takeover is offset bythe decrease in application fraud.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 23/84

// 23

P L A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 24/84

24// PLASTIC CARD FRAUD

MAIL NON-RECEIPT FRAUD

£8.4 MILLION IN 2010 (UP 22%)

This type of fraud involves cards being stolenwhilst in transit – after card companies sendthem out and before the genuine cardholdersreceive them. Properties with communalletterboxes, such as flats and student hallsof residence and people who do not get their

mail redirected when they change addressare all vulnerable to this type of fraud.

Mail non-receipt fraud rose this year becausetwo major issuers replaced nearly 10 milliondebit cards, increasing the potential for thisfraud taking place. Another factor was that in2010 a large number of cards were upgradedto include contactless technology.

Although this type of fraud increased, it is

still 88% lower than in 2004, which was thepeak year for mail non-receipt fraud. Thebanking industry continues to work with theRoyal Mail, and other organisations it uses todeliver its cards, to monitor card losses,identify fraud hot spots and take preventativeaction. Card companies use secure couriersto deliver to high-risk postcodes, or cards

may be sent to a customer’s branch forpersonal collection. Customers may also berequired to phone their card companies toactivate their cards before they can be used.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 25/84

// 25

PL A S T I C

C A R D S

MAIL NON-RECEIPT FRAUD LOSSES ON UK-ISSUED CARDS 2000-2010

Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

10

20

30

40

50

8 . 4 + 2 2 % 1

7 . 7

+ 2 1 %

2 6 . 8

+ 5 1 %

3 7 . 1

+ 3 9 % 4

5 . 1

+ 2 2 %

7 2 . 9

+ 6 2 %

4 0 . 0

- 4 5 %

1 5 . 4

- 6 1 %

1 0 . 2

- 3 4 %

1 0 . 2

0 %

6

. 9

-

3 2 %

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 26/84

26// PLASTIC CARD FRAUD

WHERE DOES CARD FRAUD

TAKE PLACE?The card fraud landscape has changedover the past ten years mainly due to thecontinuing success of chip and PIN inthe UK. Fraudsters are now targetingthose environments that do not yet use chipand PIN, such as the internet. Overseas

fraud losses have also gone down fromtheir peak in 2008, due in part to thecontinuing rollout of chip and PIN in othercountries around the world.

UK RETAILER

(FACE-TO-FACE) FRAUD£67.4 MILLION IN 2010 (DOWN 6%)

Card fraud losses in the UK high street havedeclined by 69% since peaking at £218.8million in 2004.

This decrease is thanks to the success ofchip and PIN. However, card fraud can still

happen in shops in the UK through lost andstolen cards if a criminal has access to thePIN, for example, if a cardholder has writtentheir PIN down and stored it in their purse orwallet, which is stolen.

A much smaller proportion of this fraudinvolves cards being used fraudulently as a

result of mail non-receipt fraud, where thefraudster has been able to intercept both thecard and its PIN on the way to the cardholder.

P

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 27/84

// 27

CARD FRAUD LOSSES AT UK RETAILERS (FACE-TO-FACE TRANSACTIONS) 2000-2010

Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

50

100

150

200

6

7 . 4 - 6 %

1 3 9 . 1

+ 5 0 %

1 8 8

. 9

+ 3 6 %

1 8 6

. 9

- 1 %

1 7 7 . 9

- 5 %

2 1 8 . 8

+ 2 3 %

1 3 5 . 9

- 3 8 %

7 2 . 1

- 4 7 %

7 3 . 0 + 1 % 9

8 . 5

+ 3 5 %

7

1 . 8

- 2 7 %

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

PL A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 28/84

28// PLASTIC CARD FRAUD

UK CASH MACHINE FRAUD

£33.2. MILLION IN 2010 (DOWN 9%)

The amount of money withdrawnfraudulently last year at UK cash machines,on UK-issued cards accounted for 9% of totalcard fraud losses.

A lot of cash machine fraud is still theresult of cardholders keeping their PIN

written down in their purse or wallet,which is then stolen.

Fraudsters also use cash machines tocompromise or steal cards or card details.The three main ways in which cards and carddetails are stolen at cash machines are:

- Card-trapping devices – a device is inserted

into a cash machine’s card slot, whichretains the card inside the cash machine.The criminal tricks the victim into

re-entering their PIN while the criminal

watches. After the cardholder gives up andleaves, the criminal removes the device,with the card, and withdraws cash.

- Skimming – a device is attached to the cashmachine to record the electronic detailsfrom the magnetic stripe of genuine cardsas they are inserted. A miniature camera ishidden overlooking the PIN pad to capturethe PIN being entered. A fake magneticstripe card is then produced and used withthe genuine PIN to withdraw cash at cashmachines overseas, where they have yet toupgrade to chip and PIN.

- Shoulder surfing – criminals watch thecardholder entering their PIN, then steal

the card using distraction techniques orpickpocketing, before using the stolen cardand genuine PIN.

P

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 29/84

// 29

FRAUD LOSSES AT UK CASH MACHINES 2000-2010

Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

10

20

30

40

50

1 8

. 3

+ 5

0 %

2

1 . 2

+

1 6 % 2

9 . 1

+ 3 7 %

4 1 . 1

+ 4 1 %

7 4 . 6

+ 8 1 %

6 5 . 8

- 1 2 %

6 2 . 0 - 6 %

3 5 . 0

- 4 4 %

4 5 . 7

+ 3 1 %

3 6 . 7

- 2 0 %

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

3 3 . 2 - 9 %

PL A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 30/84

30// PLASTIC CARD FRAUD

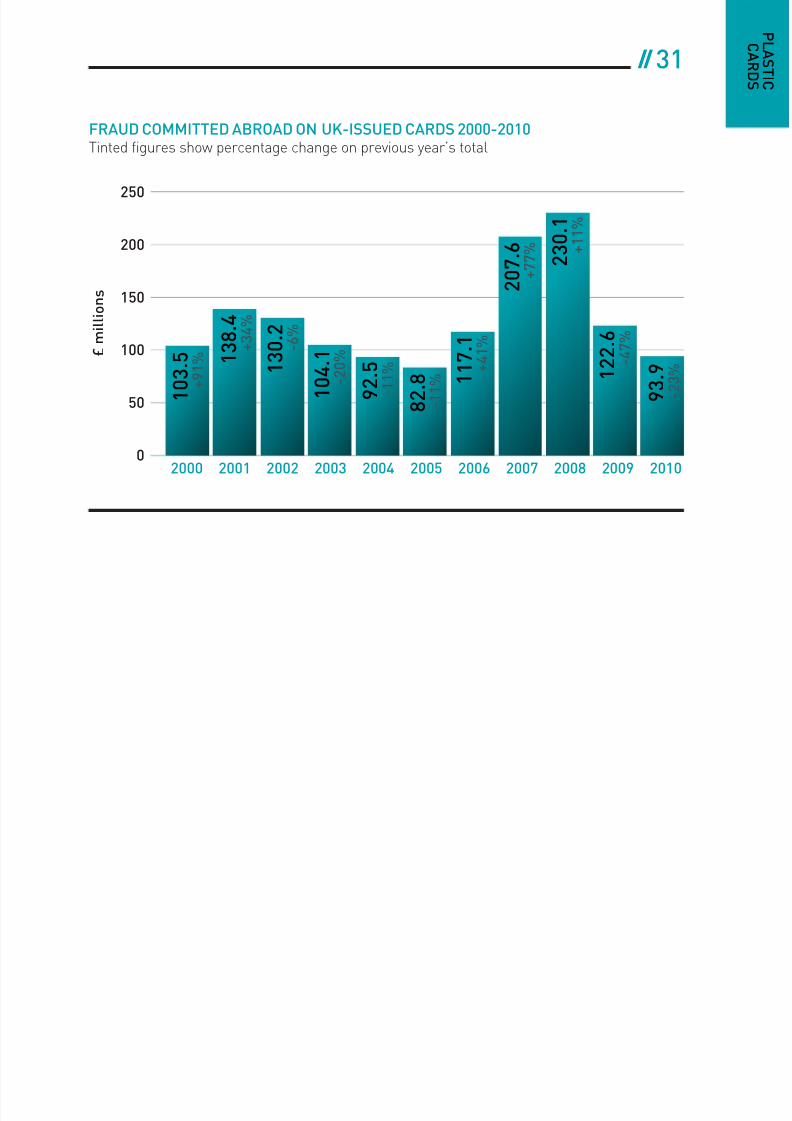

FRAUD ABROAD

£93.9 MILLION IN 2010 (DOWN 23%)

This type of fraud typically occurs as aresult of criminals stealing magnetic stripedetails from UK cards to make fakemagnetic stripe cards for use overseasin countries yet to upgrade to chip and PIN.At £93.9 million, fraud abroad accounts for

just over one quarter (26%) of total cardfraud losses. However, this type of fraudhas dropped significantly in the past twoyears, partly due to banks’ fraud detectionsystems, which monitor for unusualspending patterns and stop potentialfraud before it happens.

The countries where fraud is occurring on

UK-issued cards have also changed markedlyover the past five years. As chip and PIN isrolled out in more and more locations aroundthe world, the traditional fraud hotspots suchas France and Spain have been replaced bymore faraway places. This is becausefraudsters are targeting countries withoutchip and PIN, where they can still use fake

magnetic stripe cards. This includes the USA,which has been a constant in the top five forthe past five years – occupying the top spotevery year. This situation is unlikely to changein the near future as the USA has no firmplans to introduce chip and PIN.

P

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 31/84

// 31

FRAUD COMMITTED ABROAD ON UK-ISSUED CARDS 2000-2010

Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

50

100

150

200

1 0 3 . 5

+ 9 1 % 1

3 8 . 4

+ 3 4 %

1 3 0 . 2 - 6 %

1 0 4 . 1

- 2 0 %

9 2 . 5

- 1 1 %

8 2 . 8

- 1 1 % 1

1 7 . 1

+ 4 1 %

2

0 7 . 6

+ 7 7 %

2 3 0 . 1

+ 1 1 %

1 2 2 . 6

- 4 7 %

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

9 3 . 9

- 2 3 %

L A S T I C

C A R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 32/84

32// PLASTIC CARD FRAUD

TOP 5 COUNTRIES FOR FRAUD ABROAD 2007-2010

UK-issued cards or card details used fraudulently overseas

£ m i l l i o n s

0

5

10

15

20

25

2 1 . 5 U

S A

B r a z i l

S o u t h A f r i c a

C a n a d a

I n d o n e s i a

U S A

I t a l y

F r a n c e

A u s t r a l i a

C a n a d a

A u s t r a l i a

S p a i n

I t a l y

U S A

U

S A

C a n a d a

A u s t r a l i a

S p a i n

I t a l y

C a n a d a

2 4 .

5

3 2 . 6

2 1 . 4

5 . 7

1 3 . 4

1 2 . 0

9 . 5

9 . 0 1

1 . 6

1 1 . 0

1 0 . 5

8 . 6

6 . 3

5 . 2 4 . 4 4 . 3 4

. 8

30

35

2007 2008 2009 2010

3 . 9 3

. 3

P L

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 33/84

// 33LA S T I C

CA R D S

INTERNET/E-COMMERCE FRAUD

ON CARDSESTIMATED AT £135.1 MILLION IN 2010(DOWN 12%)

An estimated £135.1 million of card fraud tookplace over the internet in 2010, a decrease of12% from 2009 when e-commerce fraudlosses were £153.2 million. Internet fraud now

accounts for 59% of card-not-present losses– slightly up from 58% in 2008.

The decrease in the value of internet fraudlosses has been aided by the increasing use

of sophisticated fraud screening detection

tools by retailers and banks to detectpotential internet fraud as well as thecontinued growth in use of Verified byVisa and MasterCard SecureCode.

The vast majority of this type of fraudinvolves the use of card details that havebeen fraudulently obtained through methodssuch as skimming, data hacking, or throughunsolicited emails or telephone calls. Thecard details are then used to undertakefraudulent card-not-present transactions.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 34/84

34// PLASTIC CARD FRAUD

INTERNET/E-COMMERCE FRAUD LOSSES ON UK-ISSUED CARDS 2000 TO 2010

Tinted figures show percentage change on previous year’s total. All figures estimated.

£ m i l l i o n s

0

50

100

150

3 . 8 0 % 1 5 . 0

+ 2

9 5 %

2 8 . 0

+ 8 7 % 4

5 . 0

+ 6 1 % 1

1 7 . 0

+ 1 6 0 %

1 1 7 . 1 0 %

1 5 4

. 5

+ 3

2 % 1

7 8 . 3

+ 1 5 %

1 8 1 . 7 + 2 %

1 5 3

. 2

- 1 6 %

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

1 3 5 . 1 - 1 2 %

P L C

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 35/84

// 35

INDUSTRY MEASURES TO PREVENT

PLASTIC CARD FRAUD

CHIP AND PINMAKING CARD TRANSACTIONS SAFER

Chip and PIN is part of a global programmeto tackle plastic card fraud and has proven tobe an undoubted success, resulting insignificant reductions in specific types offraud on UK cards:

- Lost and stolen card fraud is at its lowestlevel since the 1990s.

- Counterfeit card fraud is at its lowest levelsince 1998.

- Fraud losses in the UK high street havefallen by 69% since 2004.

LA S T I C

CA R D S

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 36/84

36// PLASTIC CARD FRAUD

DEDICATED CHEQUE AND

PLASTIC CRIME UNIT (DCPCU)A SPECIALIST POLICE UNIT TARGETINGORGANISED CRIMINAL GANGS

The DCPCU is a special police unit,sponsored by the banking industry, withan ongoing brief to help stamp outorganised payment fraud across the UK.

It is a unique body that comprises officersfrom the Metropolitan and City of Londonpolice forces who work along side bankingindustry fraud investigators.

The Unit has been responsible for savingsof approximately £368 million in estimatedfraud since its launch in 2002.

FINANCIAL FRAUD

BUREAU (FFB)The FFB is responsible for managing thepayment industry’s co-ordinated initiativeson data sharing to reduce financial fraud.The Bureau is recognised as a centre ofexcellence and enables its customer groupsto share data through a secure and trustedprocess. It provides data directly to lawenforcement, including the DCPCU andthe National Fraud Intelligence Bureau.

It is responsible for supporting andco-ordinating the Payments Industry ThreatManagement Process and maintaining theFraud Intelligence Sharing System (FISS)database. It also issues and receives

intelligence alerts from the paymentsindustry and a range of other stakeholders.

P L C

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 37/84

// 37

FRAUD INTELLIGENCE

SHARING SYSTEMSHARING INTELLIGENCE TO TACKLE FRAUD

A Fraud Intelligence Sharing System (FISS)was established in 2008, which enablesthe banking industry to share informationon all confirmed, attempted and suspectedfraud in a central, shared database.

Established specifically to combat all typesof banking-related fraud in the UK, thesystem provides the industry with a secureand robust reporting mechanism,supporting the industry’s long-term fraudprevention strategy.

NATIONAL FRAUD

INTELLIGENCE BUREAUThe payments industry has worked closelywith the City of London Police to establish theNational Fraud Intelligence Bureau (NFIB)and now provides a regular data feed from itsFraud Intelligence Sharing System.

The NFIB is one of the most advanced police

intelligence systems in the world, usingmillions of reports of fraud from a wide rangeof public and private sector organisations tohelp catch serial fraudsters and provide abetter picture of the nature of fraud.

The Bureau is government-funded andrun by the City of London Police, which is theNational Lead Force for fraud, in partnership

with police forces and the public andprivate sector.

LA S T I C

CA R D S

38//PLASTIC CARD FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 38/84

38// PLASTIC CARD FRAUD

INDUSTRY HOT CARD FILE (IHCF)

CHECKING TRANSACTIONS FOR CARDSBEING USED FRAUDULENTLY

The IHCF contains information on more than6 million cards reported lost or stolen. In2010, 424,669 (434,756 in 2009) cases ofattempted fraud were prevented by thissystem. The IHCF is also used successfully

at French motorway tollbooths to combat theuse of stolen UK cards.

More than 60,000 UK retailers subscribe to

this electronic file. When a participatingretailer accepts a card payment as part of anormal transaction, it is automaticallychecked against the file, and the retailer isalerted if the card’s details match any ofthose on the system.

The IHCF is increasingly being used byretailers in the card-not-present environment,and has provided a mechanism for checkingcard details prior to the goods beingdispatched.

//39

P L A

C

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 39/84

// 39A S T I C

A R D S

REDUCING PHONE, INTERNET

AND MAIL ORDER (CARD-NOT-PRESENT) FRAUDHELPING BUSINESSES FIGHT CNP FRAUD

Phone, internet and mail order fraud fell forthe second successive year in 2010 but theselosses still account for more than half of allcard fraud. However, the fall in this type offraud is all the more notable given thecontinuing popularity of shopping over thephone and the internet. Indeed, theestimated total value of internet spending in2010 was £53.6 billion – an increase of 14%on the previous year. (£47.2 billion in 2009.)

A number of initiatives are in place to tackle

phone, internet and mail order fraud:- Verified by Visa and MasterCard

SecureCode are online fraud preventionsolutions that make cards more securewhen shopping online. Cardholderssimply need to register a private passwordwith their card company for use whenshopping online at participating retailers.

More than 70 million cards had beenregistered by March 2011 (up from64 million in March 2010).

- More information can be found atwww.becardsmart.org.uk.

40//PLASTIC CARD FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 40/84

40// PLASTIC CARD FRAUD

- An automated cardholder address

verification (AVS) and card security code(CSC) system is available for businessesthat accept phone, internet or mail ordertransactions. The system allows themto verify the billing address of a cardholderand cross-check the security code onthe signature strip of the card. These datachecks provide additional information to

help businesses assess fraud risks anddecide whether to proceed withthe transaction.

- The industry encourages retailers to makeuse of various card-not-present fraudprevention tools, such as intelligent frauddetection software, available from third-party providers.

//41

P L A

C A

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 41/84

// 41A S T I C

AR D S

BANKS’ USE OF INTELLIGENT

FRAUD-DETECTION SYSTEMSCHECKING FOR UNUSUAL SPENDINGPATTERNS TO SPOT FRAUD BEFORE IT ISREPORTED BY THE CARDHOLDER

Card companies continue to increasethe effectiveness and sophistication ofcustomer-profiling neural networks that

can identify unusual spending patternsand potentially fraudulent transactions.The card company will then contact thecardholder to check whether the suspecttransaction is genuine. If not, an immediateblock can be put on the card.

INDUSTRY MEASURES TO

PREVENT CARD ID THEFTCROSS-INDUSTRY CO-OPERATION

Although card ID fraud remained stable andcontinues to be a relatively small proportionof total card fraud losses – just over 10% –the industry remains committed to enhancingexisting prevention measures and developing

new ways of combating this type of fraud.The banking industry is represented onthe Identity Fraud Communications andAwareness Group (IFCAG) which includesrepresentatives from the British Bankers’Association and CIFAS, amongst manyothers. It has created a website for identityfraud prevention at www.identitytheft.org.uk,

which provides best practice guidelinesfor businesses that could be targeted byidentity fraudsters. There is also an

42//PLASTIC CARD FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 42/84

42// PLASTIC CARD FRAUD

interactive e-learning section to improve

the understanding of employees who needto check and verify the identity of customerson a day-to-day basis. The site also advisesthe public how best to protect themselvesfrom becoming a victim of identity theft andwhat to do if they have. This is complementedwith a range of leaflets and posters for usein public areas such as libraries, citizens

advice bureaux and bank counters.For more information visitwww.identitytheft.org.uk.

INDUSTRY MEASURES TO PREVENT

CASH MACHINE CRIMEMULTI-LAYERED APPROACH TOTACKLING FRAUD

Although UK cash machine fraud losses havedecreased by 56% since 2004 – the peak yearfor this type of fraud – the UK banking industrycontinues to work with cash machine suppliersto enhance technical solutions to prevent cashmachine tampering. The industry also workswith the police to target the organisedcriminals behind these types of crime.

A number of generic initiatives are in place tocounter cash machine crime. These include:

- Technology upgrades to make cashmachines tamper-proof, such as redesigned

card reader surrounds in order to make itdifficult for fraudsters to attach a skimmingdevice to a machine.

//43

P L A

C A

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 43/84

// 43A S T I C

AR D S

- Encouraging regular inspections of cash

machines by cash machine owners forevidence of tampering and unusualattachments.

- Use of CCTV to deter criminal activity.

- Consumer advice on best practice whenusing a cash machine. This includesco-ordinating use of screen messagesdesigned to raise security awareness.

- LINK, the UK’s cash machine network,

also works in partnership with independentcharity Crimestoppers, to offer rewards ofup to £25,000 for information on cashmachine crime. Anyone with details aboutthose responsible for cash machinecrime – such as card skimming or evenphysical attacks on the machine itself –can call Crimestoppers on 0800 555 111,

where they can leave their informationcompletely anonymously.

44//PLASTIC CARD FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 44/84

44// PLASTIC CARD FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 45/84

C H E Q U E

F R A U D

TYPES OF CHEQUE FRAUD 46COMMON CHEQUE SCAMS 48

INDUSTRY MEASURES TO PREVENT CHEQUE FRAUD 50

LIABILITY FOR CHEQUE FRAUD 52

CHEQUEFRAUD

46//CHEQUE FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 46/84

46// CHEQUE FRAUD

CHEQUE FRAUD

£28.9 MILLION IN 2010 (DOWN 3%)Following year-on-year increases since2007, last year saw a 3% drop in chequefraud losses.

There are three types of cheque fraud:counterfeit, forged, and fraudulently alteredcheques.

TYPES OF CHEQUE FRAUD// COUNTERFEIT CHEQUE FRAUD£3.8 MILLION IN 2010 (DOWN 19%)

Counterfeit cheques are printed on non-bankpaper to look exactly like genuine chequesand are drawn by a fraudster on genuineaccounts.

// FORGED CHEQUE FRAUD

£13.1 MILLION IN 2010 (DOWN 16%) A forged cheque is a genuine cheque that hasbeen stolen from an innocent customer andused by a fraudster with a forged signature.

// FRAUDULENTLY ALTERED CHEQUES£12.0 MILLION IN 2010 (UP 29%)A fraudulently altered cheque is a genuinecheque that has been made out by the

genuine customer, but a fraudster hasaltered the cheque in some way before it ispaid in, e.g. by altering the beneficiary’sname or the amount of the cheque.

//47

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 47/84

// 47

CHEQUE FRAUD LOSSES 2002-2010

Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

10

20

30

40

3 6

. 0 4 5 . 0

+ 2 5 %

4 6 . 2 + 3 %

4 0 . 3

- 1 3 %

3 0 . 6

- 2 4 %

3 3 . 5

+ 1 0 %

4 1 . 9

+ 2 5 %

2 9 . 8

- 2 9 %

50

2002 2003 2004 2005 2006 2007 2008 2009 2010

2 8 . 9 - 3 %

C H E Q U E

F R A U D

48//CHEQUE FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 48/84

48// CHEQUE FRAUD

COMMON CHEQUE SCAMS

There are a number of cheque scams. Theymay involve not only stolen or fraudulentcheques and bankers’ drafts, but alsogenuine cheques owned by the fraudster,which subsequently bounce due to lack ofsufficient funds.

Over recent years organised gangs haveparticularly targeted consumers sellinghigh-value goods such as cars, by offeringto pay using stolen or counterfeit chequesand bankers’ drafts. Anyone wanting toaccept a cheque or banker’s draft is advisednot to hand over the goods until they havecertainty that the cheque funds will not bereclaimed (this happens at the end of the

sixth working day after they have paid thecheque into their account).

Frequently this scam will also involve the

fraudster offering a cheque or banker’s draftfor significantly more than the price of thegoods. As ever, anything that sounds too goodto be true should set alarm bells ringing, butthe fraudster’s excuse may sound plausible.

In this type of scam the seller is asked totransfer the amount of the overpaymenteither to the fraudster, or to a third party

after three days when, it is claimed, thecheque will be cleared. It is likely that thecheque or banker’s draft is fraudulent. Thebanks do all they can to spot and stop suchcheques and drafts in the clearing system.However, with this scam, the cheque mightbe genuine, but the fraudster does not havesufficient funds in their account. The payingbank will therefore return the cheque unpaid.

//49

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 49/84

// 49

If the customer has already made the

overpayment to a third party, they will losethe funds. With the 2-4-6 clearing timescalesit is not until the end of the sixth workingday after the cheque has been paid in thatthe customer can be sure that the fundsare theirs, and will not bounce (see 2-4-6clearing timescales on next page).

There have been a number of cases reported

which involve the addition of an extra name tothe payee line – without any of the originaldetail being removed. Fraudsters targetcheques where there is an unused space inthe payee line, by adding ‘re’, ‘or’, ‘T/As’ or‘c/o’ followed by a new name in the space leftblank. This type of fraud means there are nosigns of obvious alteration, reinforcing theimportance of drawing a line through allunused spaces when writing out a cheque.

C H E Q U E

F R A U D

50// CHEQUE FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 50/84

50//CHEQUE FRAUD

WHAT IS THE BANKING INDUSTRY

DOING TO PROTECT CUSTOMERSFROM CHEQUE FRAUD?

The banking industry introduced the 2-4-6cheque clearing timescales to help protectcustomers who inadvertently accept chequesfrom fraudsters. It means that customerscan be sure that at the end of six workingdays (after paying in a cheque) the money is

theirs. Subsequently they are protected fromany loss should the cheque turn out to be

fraudulent – the funds cannot be reclaimed

without the customer’s consent unless thecustomer is a knowing party to fraud.

Despite this positive change, the industrycontinues to recommend that customersshould be wary of accepting cheques orbankers’ drafts if they don’t know or trust theperson offering them – particularly if they areof high value.

// 51

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 51/84

WHAT IS THE BANKING

INDUSTRY DOING TO PREVENTCHEQUE FRAUD?

There is a range of prevention measuresemployed at both bank and industry level. Atan industry level, banks continue to focus onidentifying lost, stolen or fraudulent chequesas they pass through the clearing system,before there is a victim. This approach is very

successful and in the past year the bankingindustry successfully identified over 90% ofall fraudulent cheques as they went throughthe cheque clearing process.

Another way in which the industry iscombating cheque fraud is through theCheque Printer Accreditation Scheme(CPAS), which was set up in 1995 and ismanaged by the Cheque and Credit ClearingCompany. All printers of cheques arerequired to be accredited to the Scheme,and to comply with the regulations forensuring that cheques are printed to the

highest security standards. Customers’chequebooks are printed by CPAS members.

C H E Q U E

F R A U D

52// CHEQUE FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 52/84

LIABILITY FOR CHEQUE FRAUD

Any innocent customer whose chequebookis used by a fraudster will continue to enjoyfull protection from any financial loss,provided they haven’t breached their termsand conditions.

Following the introduction of the 2-4-6cheque changes, a customer can be surethat at the end of six working days (afterpaying a cheque or banker’s draft into theirbank account) the money is theirs. They are

protected from any loss, should the chequeturn out to be fraudulent – the funds cannotbe reclaimed without the customer’sconsent unless the customer is a knowingparty to fraud. However, any customers whodo not wait until the end of the sixth workingday, and decide to withdraw and spendfunds before that, do so at their own risk.If the cheque subsequently bounces, they

may have to return funds to their bank orbuilding society.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 53/84

ONLINE BANKING FRAUD 54

INDUSTRY MEASURES TO PREVENT ONLINE BANKING FRAUD 59

PHONE BANKING FRAUD 61

ONLINE ANDPHONE BANKING

FRAUD

O NL I N

E &

P H

O NE

54// ONLINE AND PHONE BANKING FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 54/84

ONLINE BANKING FRAUD

£46.7 MILLION IN 2010 (DOWN 22%)In 2010 online banking fraud losses totalled£46.7 million – a decrease of 22% from theprevious year (£59.7 million in 2009).

The reduction in online banking fraud is due toa number factors. Although more and morecustomers are now banking online, users have

become more aware of security and havebecome better at securing their PCs, following

campaigns from the industry. Another factor isthe banks’ increasing use of sophisticatedfraud detection software to monitor and spotsuspected fraudulent transactions.

In addition to this the Police Central e-CrimeUnit (PCeU), which launched in the spring of2009, is helping to tackle these losses byproviding specialist police officer training andco-ordinating cross-force initiatives to crack

down on online offenders.

// 55

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 55/84

ONLINE BANKING FRAUD LOSSES 2004-2010Tinted figures show percentage change on previous year’s total

£ m i l l i o n s

0

10

20

30

40

50

1 2

. 2 2 3 . 2

+ 9 0 %

3 3 . 5

+ 4 4 %

2 2 . 6

- 3 3 %

5 2 . 5

+ 1 3 2 % 5

9 . 7

+ 1 4 %

60

2004 2005 2006 2007 2008 2009 2010

4

6 . 7

- 2 2 %

O NL I N

E &

P H O NE

56// ONLINE AND PHONE BANKING FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 56/84

COMMON SCAMS

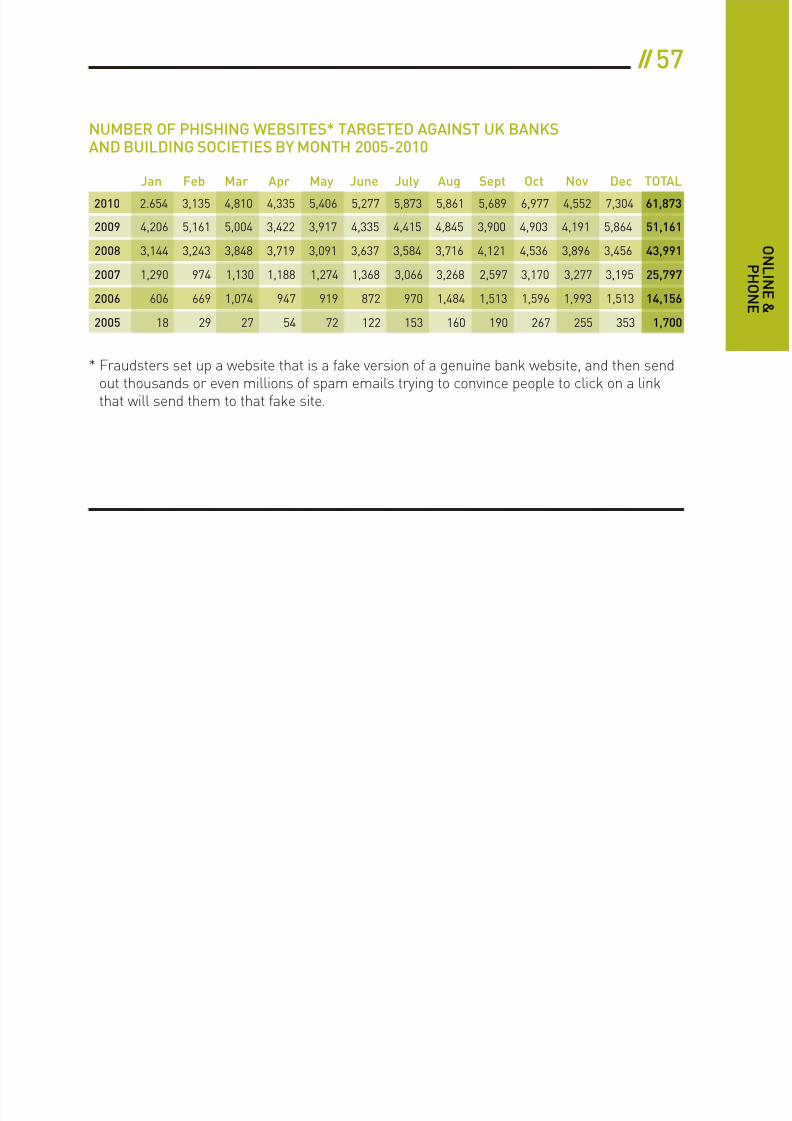

// PHISHINGPhishing is the name given to the practice ofsending emails at random, purporting to comefrom a genuine company such as a bank, inan attempt to trick customers of that companyinto disclosing information at a bogus companywebsite operated by fraudsters.

These emails usually claim that it isnecessary to ‘update’ or ‘verify’ your password,and they urge you to click on a link from theemail that takes you to the bogus bank website.Any information entered on the bogus websitewill be captured by the criminals for theirown fraudulent purposes.

Criminals use phishing because the banks’

own systems have proven difficult to attack.Criminals have turned their attention to

phishing attacks, targeting individual internetusers in order to gain personal or secretinformation that can be used online forfraudulent purposes.

// MALWARE (MALICIOUS SOFTWARE)

Malware remains a popular method usedby fraudsters to obtain customers’ details,and is increasingly used in combinationwith phishing emails.

Malware includes computer viruses thatcan be installed on a computer without theuser’s knowledge, typically by users clickingon a link in an unsolicited email, or bydownloading suspicious software. Malwareis capable of logging keystrokes therebycapturing passwords and other personal

details or financial information.

// 57

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 57/84

NUMBER OF PHISHING WEBSITES* TARGETED AGAINST UK BANKSAND BUILDING SOCIETIES BY MONTH 2005-2010

2009 4,206 5,161 5,004 3,422 3,917 4,335 4,415 4,845 3,900 4,903 4,191 5,864 51,161

2008 3,144 3,243 3,848 3,719 3,091 3,637 3,584 3,716 4,121 4,536 3,896 3,456 43,991

2007 1,290 974 1,130 1,188 1,274 1,368 3,066 3,268 2,597 3,170 3,277 3,195 25,797

2006 606 669 1,074 947 919 872 970 1,484 1,513 1,596 1,993 1,513 14,156

2005 18 29 27 54 72 122 153 160 190 267 255 353 1,700

Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec TOTAL

2010 2.654 3,135 4,810 4,335 5,406 5,277 5,873 5,861 5,689 6,977 4,552 7,304 61,873

* Fraudsters set up a website that is a fake version of a genuine bank website, and then sendout thousands or even millions of spam emails trying to convince people to click on a linkthat will send them to that fake site.

O NL I N

E &

P H O NE

58// ONLINE AND PHONE BANKING FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 58/84

// MONEY MULES

Most of the fraudsters behind online bankingscams are located overseas, so they need anaccomplice with a UK bank account to act asa ‘money mule’ or money transfer agent, tolaunder the funds obtained as a result ofonline scams. Some mules are recruitedunder false pretences, in the belief that theywill be working for a legitimate company.

After being recruited by the fraudsters, moneymules receive funds into their accounts andthey then withdraw the money and send itoverseas using a wire transfer service,minus a percentage commission payment.

Money mules are recruited by a variety ofmethods, including spam emails, adverts ongenuine recruitment websites or newspapers,and approaches to people with their CVsdisplayed online.

Although the prospect of making someeasy money may appear attractive, anycommission payments will be recovered asthey are the proceeds of fraud, and money

mules may become embroiled in a policeinvestigation. Money mules are the easiestpart of the chain to track down.

// 59

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 59/84

O NL I N

E &

P H O NE

INDUSTRY MEASURES TO PREVENTONLINE AND TELEPHONEBANKING FRAUDThe banking industry works alongside anumber of partners to tackle this type of fraud,such as the Serious Organised Crime Agency,the Police Central e-Crime Unit (PCeU),overseas law enforcement agencies,technology companies, anti-virus firms and

Internet Service Providers.A number of initiatives are already in place:

- Monitoring of the internet at industry andbank level to detect and close downphishing-related websites.

- Two-way communication with onlinepartners so security intelligence can be

shared and used effectively.- Development and use of clear and

consistent advice for consumers.

- Banks continually monitor for potentiallyfraudulent online and phone bankingtransactions and will contact a customerto check if a suspect transaction isgenuine or not.

One of the initiatives introduced by somebanks to provide a higher level of onlinebanking security is the use of hand-held chipand PIN card reading devices. These devices

work via a customer inserting their chip andPIN card into a hand-held card reader andentering their PIN. On entering the PIN, thecard reader generates a unique, one-time onlypasscode, which the cardholder provides,when prompted during a transaction, forauthentication with their online bank. Thissolution helps to ensure that the person

conducting business online is the genuinecustomer and makes these types oftransaction even safer.

60// ONLINE AND PHONE BANKING FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 60/84

The industry has createdwww.banksafeonline.org.uk to helpcustomers to stay safe while banking online.The site details types of online bankingscams, how to spot them, and how to protectyourself from falling victim.

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 61/84

62// ONLINE AND PHONE BANKING FRAUD

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 62/84

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 63/84

FACTSAND FIGURES2010

F A C T S &

F I G U R E S

PLASTIC CARDS 64

CASH MACHINES 64

CHEQUES 65

ONLINE BANKING 65

64// FACTS AND FIGURES 2010

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 64/84

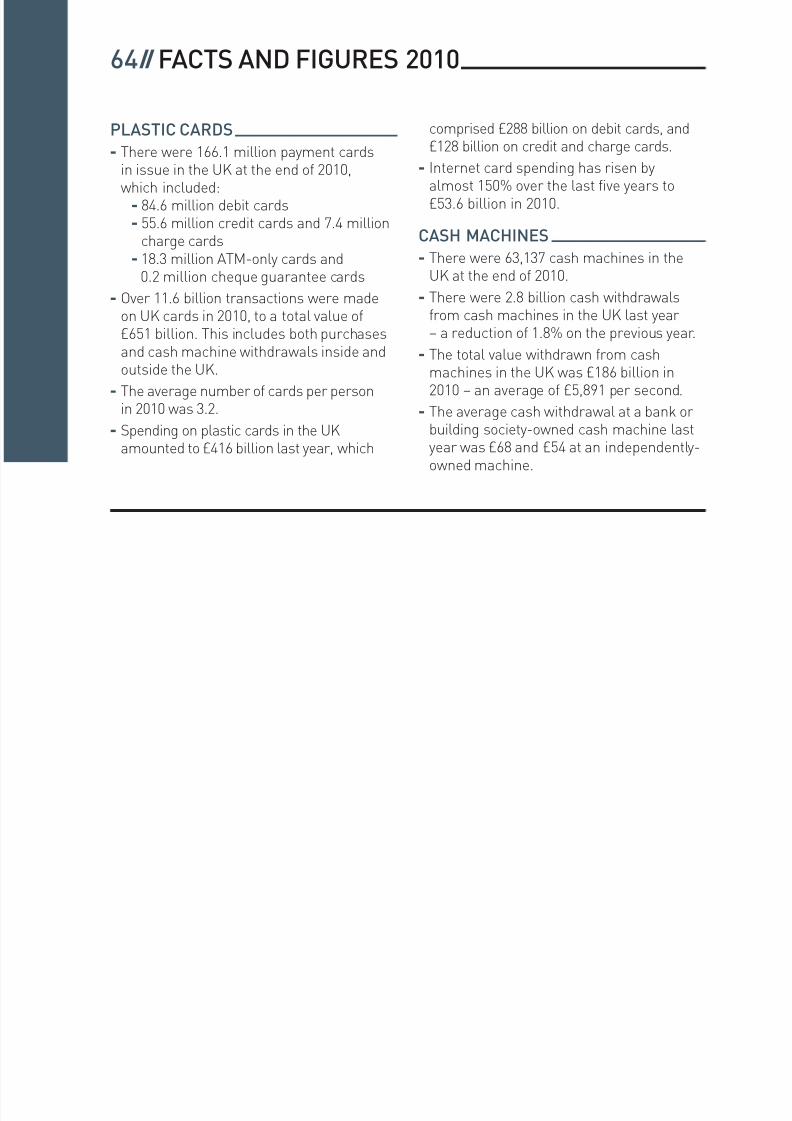

PLASTIC CARDS

-There were 166.1 million payment cardsin issue in the UK at the end of 2010,which included:- 84.6 million debit cards- 55.6 million credit cards and 7.4 million

charge cards- 18.3 million ATM-only cards and

0.2 million cheque guarantee cards

- Over 11.6 billion transactions were madeon UK cards in 2010, to a total value of£651 billion. This includes both purchasesand cash machine withdrawals inside andoutside the UK.

- The average number of cards per personin 2010 was 3.2.

- Spending on plastic cards in the UKamounted to £416 billion last year, which

comprised £288 billion on debit cards, and£128 billion on credit and charge cards.

- Internet card spending has risen byalmost 150% over the last five years to£53.6 billion in 2010.

CASH MACHINES

- There were 63,137 cash machines in theUK at the end of 2010.

- There were 2.8 billion cash withdrawalsfrom cash machines in the UK last year– a reduction of 1.8% on the previous year.

- The total value withdrawn from cashmachines in the UK was £186 billion in2010 – an average of £5,891 per second.

- The average cash withdrawal at a bank or

building society-owned cash machine lastyear was £68 and £54 at an independently-owned machine.

// 65

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 65/84

CHEQUES

-There were 3.1 million business and personalcheques issued each day in 2010, comparedwith 11 million in the peak year for chequevolumes, 1990.

- The average consumer writes 1 cheque permonth, and receives only one every 3 months.

- The average value of a personal chequetransaction in 2010 was £392.

- Only 2% of retail spending is still paid bycheque, compared with over 60% by debitor credit card.

ONLINE BANKING

-Over 26.9 million adults banked onlinein 2010.

- 61% of adults have regular access to aninternet bank online.

- Use is highest among 25 to 34 year olds.

- 95% of internet banking users use theservice to check the balance of their account.

F A C T S &

F I G U R E S

66// FACTS AND FIGURES 2010

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 66/84

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 67/84

ADVICEAND CONTACTS

A D V I C E &

C O NT A C T S

WEB LINKS 68

PUBLICATIONS 78

USEFUL CONTACTS 80

68// ADVICE AND CONTACTS

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 68/84

FRAUD PREVENTION ADVICE

//

AVOIDING CARD FRAUDCards remain a very safe way to pay for goodsand services in the UK and overseas. If youare unlucky enough to become a victim offraud the good news is that you are protectedby legislation and should not suffer anyfinancial loss as a consequence - providedyou have not acted fraudulently or without

reasonable care.To minimise the chances of becominga victim of card fraud:

- Look after your cards and card detailsat all times.

- Try not to let your card out of your sightwhen making a transaction, and don’t leave

your cards unattended in public places.

- Check receipts against statementsregularly and contact your card company

as soon as possible if you find an unfamiliartransaction.

- Store your statements, receipts anddocuments that contain informationrelating to your financial affairs safely anddestroy or preferably shred them when youdispose of them.

- Sign any new cards as soon as they arrive.Keep it secret, keep it safe –protect your PIN

- Ensure you are the only person thatknows your PIN. Your bank or the policewill never phone you and ask you todisclose it; anyone who does ask you for

your PIN is a fraudster.

// 69

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 69/84

A D V I C E &

C O NT A C T S

- When entering your PIN, use your freehand and your body to shield the number,

in case fraudsters have installed a hiddencamera or are watching you over yourshoulder. If you think someone has seenyour PIN you can change it at a cashmachine or by contacting your bank.

// USING YOUR CARDS OVERSEAS

Before you go overseas:- Only take cards that you intend to use;

leave others in a secure place at home.

- It’s a good idea to take another card oralternative payment method with you sothat you are not reliant on just one card.

- Make sure you have your card company’s

24-hour contact telephone number.

- Make sure your card company has up-to-date contact details for you, including a

mobile telephone number.- If your cards are registered with a Card

Protection Agency, ensure you have theircontact telephone number and your policynumber with you.

When you are overseas:

- Don’t let your card out of your sight,

especially in restaurants and bars.- Don’t give your PIN to anyone – even if

they claim to be from the police or yourcard company.

- Shield your PIN with your free hand whentyping it into a keypad in a shop or at acash machine.

70// ADVICE AND CONTACTS

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 70/84

- Consider wearing a concealed moneybelt to keep your cards, cash and traveller’s

cheques safe.When you get back:

- Check your card statements carefully forunfamiliar transactions.

- If there are any, report them to your cardcompany as soon as possible.

// CASH MACHINE FRAUD PREVENTION

Cash machines are generally very safe,however they do sometimes attract criminalattention so you still need to follow commonsense precautions when withdrawing cash.

To minimise the chances of having your cardor card details stolen at a cash machine:

- If you spot anything unusual about the cashmachine, or there are signs of tampering, donot use it. Report it to the police immediately.

- Be alert and put your personal safety first.If someone is crowding or watching you,

cancel the transaction and go to anothermachine. Do not accept help fromseemingly well-meaning strangers andnever allow yourself to be distracted.

- Stand close to the cash machine. Alwaysshield the keypad with your free hand andyour body to avoid anyone seeing you enter

your PIN.- Once you have completed a transaction put

your money and card away before leavingthe cash machine. If the cash machinedoes not return your card, report its lossimmediately to your card company, ideallyusing your mobile phone while you are stillin front of the machine. Destroy or

preferably shred your cash machinereceipts, mini-statements or balanceenquiries when you dispose of them.

// 71

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 71/84

A D V I C E &

C O NT A C T S

// AVOIDING CHEQUE FRAUD

- Never accept a cheque, or banker’s draftfrom someone, unless you know and trustthem. Be especially wary when accepting ahigh–value cheque; for instance if you areselling a car.

- Be aware that, until a cheque has beencleared at the end of the sixth working dayafter you have paid it in to your account,

there is a risk that the money could bereclaimed if the cheque turns out to bestolen, fraudulently altered or counterfeit.

- It is safer to ask for payment for high–valueitems to be made by other means (aninternet or phone banking payment or aCHAPS payment). There is a charge for aCHAPS payment but it is a guaranteed

same-day value payment. If the “buyer” isunwilling to pay the relatively small cost

involved – or to split it with you – then youreally do need to be on your guard.

- Be aware that a banker’s draft or buildingsociety cheque is not necessarily safe fromfraud. They can be stolen or altered like anyother cheque, and if altered, stolen orcounterfeit they will not be honoured. If youreceive a banker’s draft in payment forgoods, you should wait until you have

certainty at the end of the sixth working dayafter you’ve paid the cheque in to youraccount before releasing the goods.

- Keep your chequebook in a safe place,report any missing cheques to your bankimmediately and always check your bankstatement thoroughly.

- Ensure every ‘space’ which is left blank on

your cheque is crossed through i.e. after theamount in words and after the payee name.

72// ADVICE AND CONTACTS

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 72/84

- If you are making a cheque payable to abank or credit card company to pay off your

credit card bill, you must ensure that youprovide sufficient details about the payee.Enter the full details for the account holderin the payee line, for example XYZ bank,re J Jones, account number 123456.

ONLINE FRAUD PREVENTION

// ONLINE SHOPPING

- Sign up to Verified by Visa or MasterCardSecureCode whenever you are given theoption whilst shopping online. This involvesyou registering a password with your cardcompany. By signing up, your card will havean additional level of security that willminimize the chances of you becoming

a victim of online fraud.- Only shop on secure sites. Before entering

card details ensure that the locked padlock

or unbroken key symbol is showing in yourbrowser. Additionally, the beginning of the

online retailer’s internet address willchange from ‘http’ to ‘https’ to indicate theconnection is secure.

- Never send your PIN over the internet.

- Keep a copy of the retailer’s terms andconditions, returns policy, deliveryconditions, postal address (not a post

office box) and phone number (not amobile number).

- Always log out properly after shoppingonline – if the website you have used hasa ‘sign out’ or ‘log off’ button, click it whenyou have finished, especially if you havebeen using a shared or public computer.

More detailed advice on how to stay safewhen shopping online is available atwww.becardsmart.org.uk

// 73

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 73/84

A D V I C E &

C O NT A C T S

// PHONE AND ONLINE BANKING

To help avoid scams you should:

- Always be suspicious of emails that aresupposedly from your bank or from anotherbank that you do not deal with.

- Make sure your home computer has asecurity programme and virus protection.

- Make sure your computer has up-to-dateanti-virus software and a firewall installed;

consider using anti-spyware software.- Download the latest security updates,

known as patches, for your browser and foryour operating system (e.g. Windows).

- Be wary of unsolicited requests forpersonal financial information.

- Keep passwords and PINs safe; always be

wary of unsolicited emails or calls askingyou to disclose any personal details or card

numbers. Your bank, building society or thepolice would never contact you to ask you

to disclose your PIN.As additional preventative measures whenbanking online, you are encouraged to:

- Ensure your browser is set to the highestlevel of security notification andmonitoring. The safety options are notalways activated by default when you install

your computer.- Be particularly security-conscious if you

are using a public computer or public Wi-Fiinternet connection.

- Know who you are dealing with – alwaysaccess internet banking sites by typing thebank’s address into your web browser.Never go to a website from a link in anemail and then enter personal details, asthe email could be fraudulent.

74// ADVICE AND CONTACTS

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 74/84

// IDENTITY THEFT

The following tips will help you protect

your identity and prevent criminals fromcommitting fraud in your name.

- Always keep important personal documents,plastic cards and chequebooks in a safeand secure place.

- Don’t share personal information unlessyou are confident you know who you are

dealing with.- When disposing of any statements, receipts

and documents that contain informationrelating to your financial affairs do sosafely, preferably by shredding them.

- Thoroughly check bank and cardstatements as soon as they arrive. If you

find an unfamiliar transaction contact yourcard company or bank immediately.

- Be aware that your post is valuableinformation in the wrong hands. If you fail to

receive a bank statement, card statement,utility bill or any other financial informationcontact the supplier as soon as possible.

- Get your post immediately redirected toyour new address if you move house.

- More tips and advice are available fromwww.identitytheft.org.uk

// IF YOU BECOME A VICTIM OF FRAUD

Steps to take if you find you have become avictim of fraud:

- If the fraud involves credit or debit cards,phone/online banking or cheques, youshould report it to the financial institution

concerned. They will then be responsiblefor undertaking further investigation and,

// 75

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 75/84

A D V I C E &

C O NT A C T S

as appropriate, reporting cases of criminalactivity to the police.

- Any fraud that doesn’t involve your bank orcard company should be reported to thebusiness or organisations concerned in thefirst instance, and, dependent on theiradvice, then to your local police station.

- When an additional crime has beencommitted with the fraud, for example, you

have had your wallet or purse stolen or thecard used fraudulently was taken as aresult of a burglary, then this should still bereported to the police.

- Ensure you keep a record of allcommunications.

- Get a copy of your personal credit reportfrom one of the credit reference agencies –Experian, Equifax and Call Credit. A paperversion of your report is available for a

nominal fee. If applications for credit havebeen made in your name you can ask to

have any incorrect information removed.- Consider contacting CIFAS – the UK’s Fraud

Prevention Service, to apply for protectiveregistration. Once you have registered,CIFAS members will carry out extra checkswhenever anyone applies for a financialservice using your address. www.cifas.org.uk

- If you suspect mail theft, contact theRoyal Mail Customer Enquiry Number on08456 740740 or visit www.royalmail.com

- If you are a victim of card fraud or onlinebanking fraud you have protection throughlegislation, which states that you will not beliable for any losses unless you have actedfraudulently or without reasonable care.

Emergency contacts and advice is available atwww.financialfraudaction.org.uk .

76// ADVICE AND CONTACTS

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 76/84

INDUSTRY CONTACTS

www.financialfraudaction.org.ukFinancial Fraud Action UK is the nameunder which the financial services industry

co-ordinates its activity on fraud, presentinga united front against financial fraud andits effects.

www.identitytheft.org.uk

How to help protect yourself or your businessfrom identity theft, what to do if it happens to youand suggestions on where to get further help.

www.theukcardsassociation.org.ukThe UK Cards Association is the leadingtrade association for the card paymentsindustry in the UK.

www.paymentscouncil.org.ukThe strategic payments body set up to

ensure that UK payments’ plans andservices meet the needs of users, paymentservice providers and the wider economy.

// 77

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 77/84

A D V I C E &

C O NT A C T S

www.chequeandcredit.co.ukThe Cheque and Credit Clearing Company isa membership-based industry body which

manages the cheque clearing system inGreat Britain.

www.link.co.uk

LINK is the UK's cash machine (ATM)network and the busiest ATM transactionswitch in the world.

www.banksafeonline.org.ukBank Safe Online is the UK bankingindustry's initiative to help online bankingcustomers stay safe online.

78// ADVICE AND CONTACTS

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 78/84

PUBLICATIONS

//

UK PAYMENT STATISTICS 2011Provides a comprehensivesource of UK payment statisticsand historical data from 2000 to2010, with additional forecastdata up to and including 2018.£750.

// UK CASH AND CASHMACHINES 2011Covers the main trends in cashpayments, the deployment andusage of cash machines, andother forms of cash acquisition.£250.

//

UK PLASTIC CARDS 2011Plastic card trends in theUK by businesses andindividuals. £250.

// UK AUTOMATED PAYMENTS

2011Covers the main trends in theuse of direct credits, DirectDebits, Faster Payments,standing orders and CHAPSpayments. £250.(Publication date: August 2011)

// 79

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 79/84

A D V I C E &

C O NT A C T S

// UK CHEQUES 2011Covers the main trends in the use

of cheques for payment and cashacquisition. £250.(Publication date: September 2011)

// UK CONSUMER PAYMENTS 2011Looks in detail at consumerholdings and use of different

payment methods. £1,500.(Publication date: October 2011)

For more information or to order any of these publications please [email protected].

80// ADVICE AND CONTACTS

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 80/84

USEFUL CONTACTS

// PAYMENTS INDUSTRY PRESS OFFICE(CHAPS, Cheque & Credit Clearing Company,DCPCU, Faster Payments, FFA UK, LINK,Payments Council, The UK Cards Associationand SWIFT)020 3217 [email protected]

Sandra Quinn, Director of communications

020 3217 8234M: 07768 [email protected]

Jemma Smith, Head of PR020 3217 8340M: 07811 113075

Mark Bowerman, PR manager020 3217 8251

M: 07799 [email protected]

Neil Aitken, Press officer020 3217 [email protected]

Doriena Koldenhof, PR assistant020 3217 8368

[email protected] Beaumont, Public affairs manager020 3217 [email protected]

// 81

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 81/84

A D V I C E &

C O NT A C T S

// BACS0845 680 1368

// BRITISH BANKERS’ ASSOCIATION020 7216 8800

// BUILDING SOCIETIES ASSOCIATION020 7520 5900

// CIFAS – THE UK’S FRAUD PREVENTIONSERVICE033 0100 0180

// CREDIT REFERENCE AGENCIESCall Credit: 0870 060 1414Equifax: 0870 010 0583Experian: 0870 241 6212

// CRIMESTOPPERSwww.crimestoppers-uk.org

// FINANCIAL OMBUDSMAN SERVICE

0845 080 1800

// FSAConsumer helpline: 0300 500 5000

Press office: 020 7066 [email protected]

// LENDING STANDARDS BOARD020 7012 0085

// ROYAL MAIL CUSTOMER ENQUIRIES0845 7740 740

82// ADVICE AND CONTACTS

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 82/84

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5

http://slidepdf.com/reader/full/downloads-7-2698-3039-fraud-the-facts-final-5 83/84

This document is provided for information purposes only. While every effort is made to ensure the accuracy of any information

or other material contained in this document, it is provided on the basis that UK Payments Administration Ltd (and its members,either individually or collectively) accept no responsibility for any loss, damage, cost or expense of whatsoever kind arising

directly or indirectly from, or in connection with, the use by any person of any information or other material contained therein.

Any use of the information or other material contained in this document shall signify agreement to this provision.

© UK Payments Administration Ltd 2011 Published by the UK Payments Administration

84// Printed on paper made from well managed

sources containing 100% recycled chlorine free

material. Cover laminated with Cellogreen which

is sustainable, compostable and recyclable.

B W C

3 0 3 9 0 6 /

8/3/2019 Downloads 7 2698 3039 Fraud the Facts Final 5