CA Mehul K. Shah

April 2015

Workshop on

conducting transfer

pricing study

What are the Documentation Requirements?

Entity related Price related Transaction related

• Transaction terms

• Economic analysis

(method selection,

comparable

benchmarking)

• Forecasts, budgets,

estimates

• Pricing related

correspondence (letters,

emails etc.)

• Functional analysis

(functions, assets and

risks)

• Agreements

• Invoices

• Profile of group

• Profile of Indian entity

• Profile of associated

enterprises

• Profile of industry

Contemporaneous documentation requirement

Documentation not required to be maintained if the aggregate value of all

international transactions does not exceed one crore rupees [Rule 10D(2)]

2

Documentation flow

Gather

background

information

Analyze data

and perform

functional

analysis

Identify risks

and assets

employed

Prepare

functional

analysis

Integrate

into

Transfer

Pricing

study

Tested party &

characterization

Identify

industry drivers

&

characteristics

Prepare

comparability

table &

benchmarking

Prepare

Industry

report/

analysis

3

What is BEPS?

Introduction to BEPS

• 19 July 2013: OECD released its Action Plan in regard to Base Erosion and

Profit Shifting (BEPS), to coincide with the G20 Finance Leaders meeting in

Moscow.

• Action Plan:

Is ambitious : it consists of 15 specific actions ―to prevent corporations from

paying little or no tax‖ (OECD press release)

Is consensus-based : it has been ―signed off‖ (at the political level) by all 34

OECD member countries and the 8 G20 countries which are not OECD

members

Has a relatively short timetable : all actions are to be completed by December

2015 (with many of the actions having earlier deadlines)

5

BEPS objectives: a new global tax environment

6

Action 13

Re-examine transfer pricing documentation

―Develop rules regarding transfer pricing documentation to enhance transparency

for tax administration, taking into consideration the compliance costs for

business. The rules to be developed will include a requirement that MNE‘s

provide all relevant governments with needed information on their global

allocation of the income, economic activity and taxes paid among countries

according to a common template.‖

7

Proposed Compliance DocumentationNew guidelines adopt 3-tiered approach

Country-by-CountryTemplate

• Key financial information on all group members on an aggregate country basis with an activity code for each member

Master File

• Key information about the group's global operations including a high-leveloverview of a company’s business operations along with important information on a company’s global TP policies with respect to intangibles and financing

Local File

• Information and support of the intercompany transactions that the local company engages in with related parties

Local law will determine the language in which the documentation must be submitted.

Countries are encouraged to permit filing in commonly used languages and request

translation after submission.

8

Case Study Discussion

9

Under which clause in Form 3CEB would each of the

transactions be disclosed

Purchase of finished goods - Form 3CEB clause -11B

Sale of manufactured goods - Form 3CEB clause -11B

Receipt of commission income - Form 3CEB clause - 13

Purchase of fixed assets - Form 3CEB clause - 11C

Payment of Management charges and software maintenance charges - Form

3CEB clause - 17

Payment of interest on External commercial borrowings - Form 3CEB clause - 14

Issue of equity shares - Form 3CEB clause – 16

Payment for corporate guarantee - Form 3CEB clause - 15

Payment of rent - Form 3CEB clause – 22

Recovery of expenses received - Form 3CEB clause – 19

10

Draw a Functions, Assets and Risk Analysis (FAR) for

BLUE India and its AEs?

FAR analysis would be prepared for the following segments:

I) Manufacturing segment;

II) Trading segment; and

III) Commission segment.

11

Which industry would you focus on for preparation of

industry analysis of BLUE India?

Biscuits and Confectioneries

12

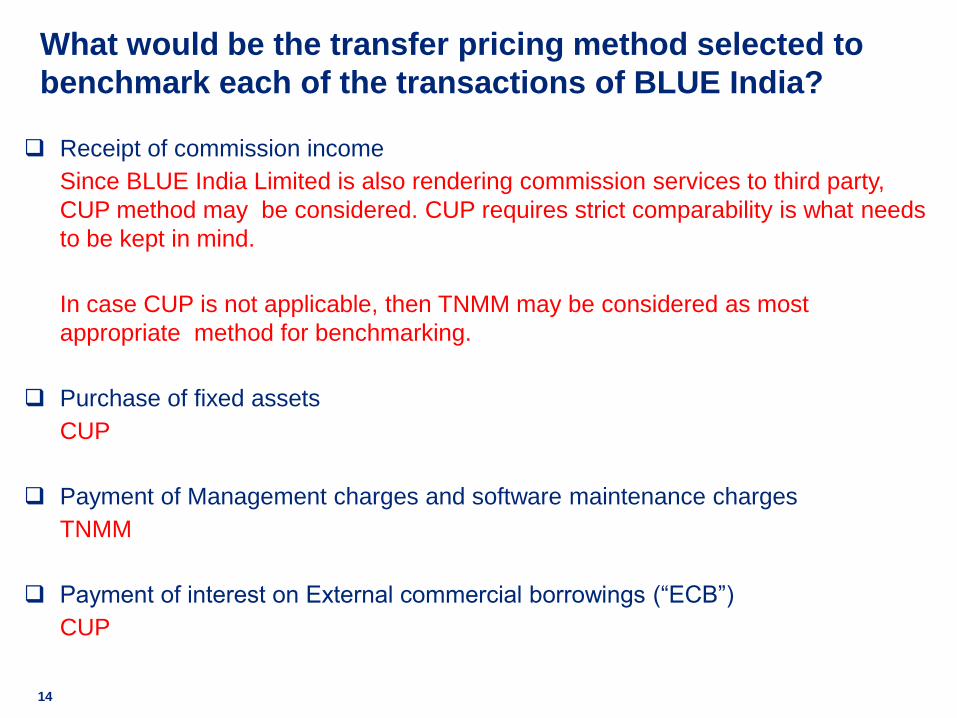

What would be the transfer pricing method selected to

benchmark each of the transactions of BLUE India?

Purchase of finished goods

Resale Price Method (―RPM‖) can would be the preferred method. However,

RPM is unlikely to lead to accurate results if there are differences level of

market, functions performed, products sold etc.

Hence, in case RPM is not applicable, then TNMM may be considered as most

appropriate method.

Sale of Manufactured goods

Comparable Uncontrolled Price Method ("CUP") would be the preferred

method, however the application of CUP needs comparability on specific

characteristics of the property transferred or services provided in either

transaction, FAR, the contractual terms, conditions prevailing in the markets in

which the respective parties etc.

In case CUP is not applicable, then TNMM may be considered as most

appropriate method

13

Receipt of commission income

Since BLUE India Limited is also rendering commission services to third party,

CUP method may be considered. CUP requires strict comparability is what needs

to be kept in mind.

In case CUP is not applicable, then TNMM may be considered as most

appropriate method for benchmarking.

Purchase of fixed assets

CUP

Payment of Management charges and software maintenance charges

TNMM

Payment of interest on External commercial borrowings (―ECB‖)

CUP

What would be the transfer pricing method selected to

benchmark each of the transactions of BLUE India?

14

What would be the transfer pricing method selected to

benchmark each of the transactions of BLUE India?

Issue of equity shares

Other Method (Refer slide 28)

Payment for corporate guarantee

CUP

Payment of Rent

Other method can be preferred in case there are quotations. In case there are

no back to back supporting than TNMM can be considered for the purpose of

benchmarking the transaction.

Reimbursement of expenses (paid)

CUP method can be preferred in case there are back to back third party

supporting for of expenses. In case there are no back to back supporting than

TNMM can be considered for the purpose of benchmarking the transaction.

15

Whether a segmental benchmarking analysis is possible

in the case of benchmarking of transactions of BLUE

India?

Segment International transactions

Manufacturing segment Purchase of raw materials, sale of

manufactured goods

Trading segment Purchase of finished goods

Commission segment Receipt of commission income

The international transactions of BLUE India could be segregated under the

following segments:

Note:

Payment of Management charges and software maintenance charges and

reimbursement of expenses would be segregated among all the three segments.

16

Would it be appropriate to conduct a AE v/s Non AE

segmental analysis for BLUE India?

Yes, segmental profitability statement can be drawn of BLUE India considering

manufacturing, trading and commission segments for benchmarking purposes.

AE v/s Non AE sub segments analysis is the ideal way of benchmarking the

international transactions under TNMM method.

Assuming BLUE India has suffered losses in AE segment how do we then

benchmark?

If BLUE India in its initial years of operation having under-utilized capacity, then

how do we benchmark?

Some judicial decisions are:

• Mando India Steering Systems Private Limited v. ACIT;

• Fuchs Lubricants (India) Pvt. Ltd. v. DCIT;

• Global Turbine Services Inc. V. ADIT; etc

17

Name of the case Observations

Mando India Steering

Systems Private

Limited

it is a well known fact that in the initial years of production, the over head

fixed costs are more due to under-utilization of resources.

Under-utilization of production capacity in the initial years is a vital factor

which has been ignored by the authorities below while determining the

ALP cost. The TPO should have made allowance for the higher overhead

expenditure during the initial period of production.

Global Turbine

Services Inc.

Relied the ruling in the case Amdocs Business Services Pvt. Ltd where it

was observed that “The plea set-up by the assessee for economic

adjustments on account of under capacity utilization and being in start up

phase, is not something which is unreasonable and neither it is otiose to

the mechanism of transfer pricing assessments.”

18

In case of purchase of machinery, how would you

benchmark the following purchases from AE:

Purchase of machinery by AE from third party and then sold to BLUE India

CUP method – Based on third party back to back supporting's.

Machinery purchased by AE from third party which was also subsequently used

by AE before selling it to BLUE India.

CUP method – Based on third party valuation certificate.

What are the supporting documents you would require to substantiate that the

transaction of purchase of machinery is at arm‘s length in the above scenarios?

Third party back to back supporting's and third party valuation certificate would

be the corroborative evidences.

19

Whether interest should be charged to related parties on

the outstanding balance receivable as on 31 March?

Finance Act 2012 has amended definition of term 'international transaction u/s

92B w.e.f. April 1, 2002 to include payments or deferred payment or receivable

or any other debt arising during the course of business. (Clause 14 of Form

3CEB)

Check the credit period generally extended to Non-AE's

Review the agreement

Assess the industry in which the assessee operates and the general trend.

In the case of Nimbus Communications Ltd (Mumbai ITAT), since no interest

was charged to Non-AE's, the ITAT deleted the addition of interest on the

outstanding balances from AEs. However, in case of Dania Oro Jewellery Pvt.

Ltd. (Mumbai ITAT), the Tribunal held that since credit period extended to Non-

AEs is around 200 days, interest should be charged on the credit period

extended beyond the credit granted to Non-AE's.

20

Whether interest should be charged to related parties on

the outstanding balance receivable as on 31 March?

In case of Kusum Healthcare Pvt Ltd vs ACIT (TS-129-ITAT-2015 (DEL)-TP),

ITAT held that notional interest adjustment on receivables outstanding from AE

beyond stipulated credit period is unwarranted when the assessee had earned

significantly higher margin than the comparable companies which compensates

for the credit period extended to the AEs.

21

Whether transaction between BLUE India and ORANGE

India Pvt. Ltd. needs to be disclosed in Form 3CEB?

As per section 92B(2) of the Income-tax Act, 1961, ―a transaction entered into

by an enterprise with a person other than an associated enterprise shall, be

deemed to be a transaction entered into between two associated enterprises, if

there exists a prior agreement in relation to the relevant transaction between

such other person and the associated enterprise, or the terms of the relevant

transaction are determined in substance between such other person and the

associated enterprise.”

Disclosed in Form 3CEB clause – 20

22

How would you benchmark the payment made to BLACK

and GREEN. Would the analysis change if the payment of

rent to BLACK amounts to Rs 100,000,000.

As per section 92BA of the Act, the transaction would be covered under the

specified domestic transactions where the aggregate of such transactions

entered into by the assessee in the previous year exceeds a sum of five crore

rupees

However, Green would not be considered as an AE of BLUE India.

Transactions outside the ambit of SDT as the value of transaction does not

exceed five crore rupees.

Where payment of rent exceeds five crore rupees, the transaction would be

covered under the ambit of SDT. (Clause 22)

23

The threshold limit for SDT has now been proposed to be

increased from 5 crore to 20 crore with effect from FY 2015-16

Whether AMP expenditure incurred by BLUE India is an

international transactions? Whether the same needs to be

benchmarked separately?

Whether AMP expense constitutes an international transaction?

Yes

Whether AMP expenditure incurred needs to separately benchmarked?

The Delhi High Court has recently held that AMP function can be aggregated

with the distribution activity if the transaction are closely linked and meet

specified common portfolio or packaged parameter.

24

Whether BLUE India needs to benchmark payment of Management

charges separately? Is there any additional documentation that

would be required to be maintained by the client to support the

payment of management charges?

BLUE India can benchmark payment of management charges considering

TNMM method.

However, given the aggressive TP audit experience, BLUE India would be

required to maintain robust documentation containing details when the

intragroup services were requested for, whether the same is backed by an

agreement, how intragroup services were received, the cost allocation workings

and the benefits derived to BLUE India Limited.

In case of Safran Aerospace India Pvt. Ltd., Quintiles Research (India) Pvt. Ltd.,

TNS India Pvt. Ltd., Dresser Rand India Private Limited, AWB India Private

Limited, McCann Erickson India Pvt. Ltd, the tribunals have accepted payment

of management charges on reproduction of substantial documentary evidences.

Contrary case laws Gemplus India Private Limited and Knorr-Bremse India

Private Limited.

25

Whether the management and software maintenance services

availed by BLUE India from its AE is in the nature of shareholder

activities/duplicative services? If yes provide reasons for the

same.

. Since BLUE India has its own HR, finance departments, legal team and IT team

comprising of two personnel one may take a view that the nature of

management services and IT support services are duplicative in nature.

However, appropriate documentation needs to be maintained by BLUE India

limited to differentiate the services/support provided by AE and services

performed by in-house local team and how the intragroup services availed has

benefited BLUE India limited.

The management services availed by BLUE India Limited are not in the nature

of shareholders activities. In this regard, reliance can be placed on OECD

guidelines which define shareholders activities as follows:

• Costs of activities relating to the juridical structure of the parent company

itself, such as meetings of shareholders of the parent, issuing of shares in the

parent company and costs of the supervisory board;

• Costs relating to reporting requirements of the parent company including the

consolidation of reports; and

• Costs of raising funds for the acquisition of its participation.26

In case of a transfer pricing audit, if the pricing

mechanism of sales of manufactured goods by BLUE

India at a cost plus 15% for AE and 20-25% for NON AE is

questioned, what would be the reasonable line of

defense?

BLUE India Limited would have to defend its pricing mechanism in case of AE

(15%) and Non AE (20%-25%) by documenting the reasons such as differences

arising from differences in contractual terms and conditions, product quality

differences, geographical differences, differences in credit terms, marketing

spend etc. BLUE India Limited may also contend that it has global transfer

pricing policy of cost plus 15% across AEs.

27

Whether shares issued by BLUE India needs to be

reported as an international transaction in Form 3CEB?

What are the documents you would require to

substantiate that the transaction of issue of shares is at

arm’s length?

Issue of shares

Based on the judicial precedent of Hon‘ble Mumbai High Court in case of

Vodafone India Services Pvt. Ltd, no income arises from the transaction of

issue of shares and accordingly the transfer pricing provisions do not apply.

However, out of abundant caution, the same may be reported in the Form

3CEB.

What are the supporting documents you would require to substantiate that the

transaction of issue of shares is at arm‘s length?

Third party valuation report, Board resolution could be some of the evidences

28Back

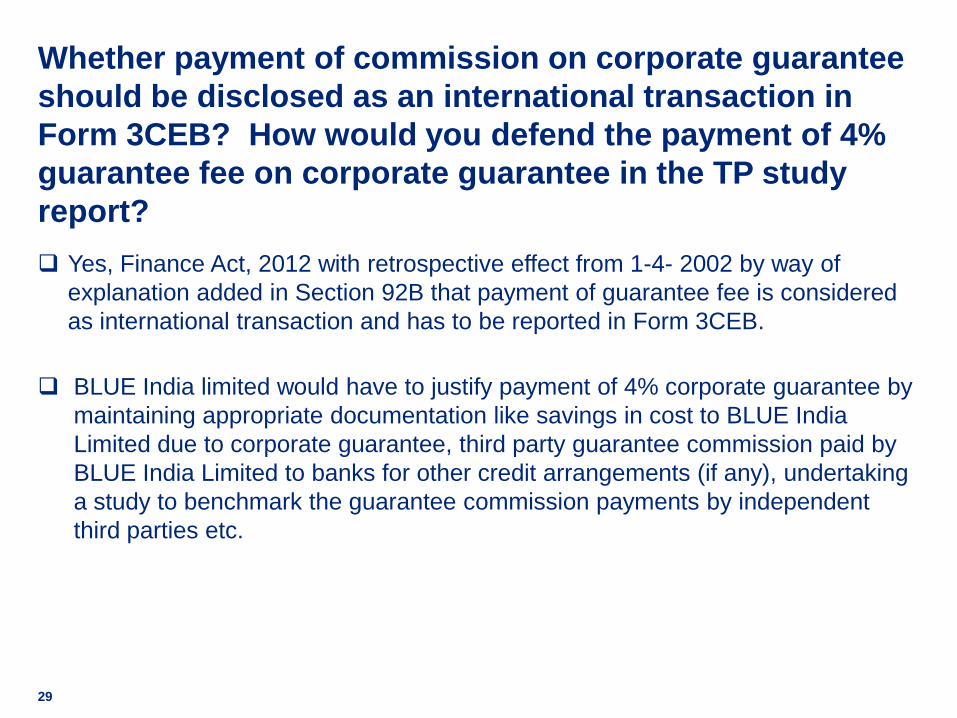

Whether payment of commission on corporate guarantee

should be disclosed as an international transaction in

Form 3CEB? How would you defend the payment of 4%

guarantee fee on corporate guarantee in the TP study

report?

Yes, Finance Act, 2012 with retrospective effect from 1-4- 2002 by way of

explanation added in Section 92B that payment of guarantee fee is considered

as international transaction and has to be reported in Form 3CEB.

BLUE India limited would have to justify payment of 4% corporate guarantee by

maintaining appropriate documentation like savings in cost to BLUE India

Limited due to corporate guarantee, third party guarantee commission paid by

BLUE India Limited to banks for other credit arrangements (if any), undertaking

a study to benchmark the guarantee commission payments by independent

third parties etc.

29

However, the Delhi ITAT in the case of Bharti Airtel Limited held that corporate

guarantees did not constitute ‗international transaction‘ under section 92B of the

Income-tax Act, 1961. The Delhi ITAT analysed clause (c) of Explanation, and

held that, the scope of these transactions is restricted to such capital financing

transactions, including inter alia any guarantee, deferred payment or receivable

or any other debt during the course of business, as will have “a bearing on the

profits, income, losses or assets of such enterprise”.

Further, the ITAT observed, "This pre-condition about impact on profits, income,

losses or assets of such enterprises is a pre-condition embedded in Section

92B(1) and the only relaxation from this condition precedent is set out in clause

(e) of the Explanation which provides that the bearing on profits, income, losses

or assets could be immediate or on a future date." The Delhi ITAT held that the

guarantee did not involve any cost to the enterprise issuing it and accordingly do

not have impact of income, profits, losses or assets of an enterprise. A

"contingent" impact that may or may not materialise would not be considered to

be an "international transaction" under the Indian law.

Some rulings on the subject matter are mentioned below:

30

Name of the case Observations

Pre amendment to the definition of international transaction

Four Soft Limited – Hyderabad The TP legislation does not stipulate any guidelines in respect to guarantee

transactions.

The corporate guarantee is very much incidental to the business of the assessee and

hence, the same cannot be compared to a bank guarantee transaction of the Bank or

financial institution.

In the absence of any charging provision, the corporate guarantee provided by the

assesse company does not fall within the definition of international transaction

Mahindra & Mahindra Limited – Mumbai The ITAT held that if the Finance Bill of 2012 is passed by the Parliament amending

the provisions of section 92B, with effect from 1st April 2002, (the AO) will have to

ignore the decision of the ITAT Hyderabad (ie Four Soft Limited), else the assessee

should be granted relief.

Post amendment to the definition of international transaction

Everest Kanto Cylinder Limited Payment of guarantee fee is included in the expression ‗international transaction‘ in

view of the Explanation i(c) of Section 92B of the Act.

There would be cost or charge of guarantee fee by providing corporate guarantee to

its subsidiary because there is an always element of benefit or cost while providing

such kind of guarantee to AE.

Manugraph India Ltd. ITAT upholds LIBOR for benchmarking loans denominated in foreign currency, directs

AO/TPO to adopt LIBOR + 2% as arm‘s length interest in respect to loan provided by

assessee to US subsidiary.

Adjustment on account of guarantee commission charges has to be only in respect of

the amount of actual loan availed by the AE during the year.

31

Name of the case Observations

Reliance Industries

Limited

The ITAT rejected the contention of the assessee, particularly in view of the

amendment made by Finance Act, 2012 with retrospective effect from 1.4.2002 by

way of Explanation –(i) (c) of section 92B to include guarantee in the Expression

―international transaction‖, that providing of guarantee by the assessee to the bank on

behalf of its AE does not constitute an ―international transaction‖ as the said

transaction is between the assessee company and the bank, who are unrelated

parties and not between the two associated enterprises.

The ITAT clarified that there is a benefit to assessee‘ s AE by providing of guarantee

by the assessee for the loan taken from bank.

The ITAT held that the assessee has undertaken a risk on behalf of its AE, which in

any case, of third party consideration, the same would not have been undertaken or

would have charged a consideration for it by the assessee.

Four Soft Limited –

Hyderabad

• It is not disputed that section 92B of the Act has been amended by the Finance Act,

2012 with the insertion of Explanation I (c) with retrospective effect from 01/04/2002.

Explanation (i)(c) to section 92B, reads as under:

“ capital financing, including any type of long-term or short-term borrowing, lending or

guarantee, purchase or sale of marketable securities or any type of advance,

payments or deferred payment or receivable or any other debt arising during the

course of business.”

• A reading of the aforesaid clause from the Explanation would make it clear that the

corporate guarantee provided by the assessee comes within the scope and ambit of

‗international transaction‘ as per the aforesaid clause.

32

What should be the ideal benchmarking rate of interest in

case of foreign currency loans - PLR rate or Libor/Euribor

rate?

Generally Libor can be considered as a start point for benchmarking interest in

case of foreign currency loans.

Source: RBI/2014-15/3 Master Circular No. 12/2014-15

Some judicial decisions in this regard are as under:

TTK Prestige Ltd. v. ACIT;

Mylan Laboratories Ltd. v. ACIT (Euribor);

Apollo Tyres Ltd. v. ACIT;

Aurobindo Pharma Ltd. v. ACIT;

Cotton Naturals (I) Pvt. Ltd., v. DCIT;

MahinSiva Industries & Holdings Ltd. v. ACIT;

DCIT vs. Tech dra Limited; etc.

Average Maturity Period All-in-cost Ceilings over 6 month LIBOR

Three years and up to five years 350 basis points

More than five years 500 basis points

33

What should be the ideal benchmarking rate of interest in

case of foreign currency loans - PLR rate or Libor/Euribor

rate?

However, in the TP audits the TPO‘s are taking aggressive approach and

considering PLR as a starting point for benchmarking interest rate.

34

What are the supporting documents BLUE India should

maintain to defend the payment made to AE for

reimbursement of expenses?

35

In case of M/s Cushman & Wakefield India Private Limited, the Delhi High Court

has held that:

“the costs incurred, the activities for which they were incurred, and the benefit

accruing to the assessee from those activities must all be proved to determine

first, whether, and how much, of such expenditure was for the purpose of

benefit of the assessee (deductible under Section 37 of the Act), and secondly,

whether that amount passed muster under a transfer pricing analysis”

(emphasis supplied)‖

Based on the above ruling, BLUE India needs to maintain documentary

evidence to demonstrate receipt of services, the basis of costs incurred,

activities for which they were incurred, benefits directly related to such activities,

etc. for proving the validity of the claim and determination of ALP.

QUERIES

36

Miscellaneous Questions:

1) Is the assessee required to maintain information in respect of other associated

enterprises i.e. enterprises that are not its group entities but are deemed to be

associated enterprises by virtue of provisions of clauses (c) to (m) of section

92A(2)?

2) Whether an assessee is required to maintain transfer pricing documentation in

case the value of international transaction has never crossed amount of rupees

one crore, however, in FY 2014-15, the value of international transaction (e.g.

rendering marketing support service) exceeded rupee one crore on account of

foreign exchange fluctuation?

3) Whether the ceiling limit of one crore for maintaining of transfer pricing

documentation is with reference to an assessee or with reference to any

undertaking or unit?

4) Whether an assessee who is given relief from maintenance of specific records

and documents prescribed in rule 10D also exempted from obtaining and

furnishing audit report under section 92E of the Act?

37

5) Is the assessee required to obtain Form 3CEB even though the books of

accounts are not liable to be audited as per the provision of section 44AB of the

Income Tax Act, 1961?

6) Does Income tax Act provide for revision of Form 3CEB in case any error is

found?

7) Whether two separate set of documentations and audit reports need to be

maintained/obtained viz. one for International TP and another for Domestic TP?

Whether a taxpayer can appoint separate auditors for International TP and

Domestic TP?

8) An Indian company becomes associate of a non -resident in the last quarter of

the previous year. Do the transfer pricing rules apply for the year? If it does,

does it apply for the quarter or whole of the year?

9) Whether an assessee who has agreed an APA with the revenue authorities

needs to undertake transfer pricing compliance?

38

Miscellaneous Questions:

Nature of transaction To be

reported

Has the assessee entered into any international transaction(s) in respect

of purchase/sale of traded/finished goods?

If ‗yes‘ provide the following details in respect of each associated

enterprise and each transaction or class of transaction :

(a) Name and address of the associated enterprise with whom the

international transaction has been entered into.

(b) Description of transaction and quantity purchased/sold.

(c) Total amount paid/ received or payable/receivable in the transaction

(i) as per books of accounts;

(ii) as computed by the assessee having regard to the arm‘s length price.

(d) Method used for determining the arm‘s length price

[See section 92C(1)]

Yes/No

Clause 11B

Back40

Nature of transaction To be

reported

Particulars in respect of providing of services :

Has the assessee entered into any international transaction(s) in respect

of Services including transactions as specified in Explanation (i)(d) below

section 92B(2)?

If ‗yes‘ provide the following details in respect of each associated

enterprise and each category of service :

(a) Name and address of the associated enterprise with whom the

international transaction has been entered into.

(b) Description of services provided/availed to/from the associated

enterprise.

(c) Amount paid/received or payable/receivable for the services

provided/taken—

(i) as per books of account;

(ii) as computed by the assessee having regard to the arm‘s length price.

(d) Method used for determining the arm‘s length price

[See section 92C(1)]

Yes/No

Clause 13

Back41

Nature of transaction To be

reported

Has the assessee entered into any international transaction(s) in respect of

purchase, sale, transfer, lease or use of any other tangible property

including transactions specified in Explanation (i)(a) below section 92B(2)?

If ‗yes‘ provide the following details in respect of each associated enterprise

and each transaction or class of transaction:

(a) Name and address of the associate enterprise with whom the

international transaction has been entered into.

(b) Description of the property and nature of transaction.

(c) Number of units of each category of tangible property involved in the

transaction.

(d) Amount paid/received or payable/receivable in each transaction of

purchase/sale/transfer /use, or lease rent paid/received or

payable/receivable in respect of each lease provided/entered into —

(i) as per books of account;

(ii) as computed by the assessee having regard to the arm‘s length price.

(e) Method used for determining the arm‘s length price [See section 92C(1)]

Yes/No

Clause 11C

Back42

Nature of transaction To be

reported

Particulars in respect of mutual agreement or arrangement :

Has the assessee entered into any international transaction with an

associated enterprise or enterprises by way of a mutual agreement or

arrangement for the allocation or apportionment of, or any contribution

to, any cost or expense incurred or to be incurred in connection with a

benefit, service or facility provided or to be provided to any one or more

of such enterprises?

If ‗yes‘ provide the following details in respect of each

agreement/arrangement:

(a) Name and address of the associated enterprise with whom the

international transaction has been entered into.

(b) Description of such mutual agreement or arrangement.

(c) Amount paid/received or payable/receivable in each such

transaction—

(i) as per books of account;

(ii) as computed by the assessee having regard to the arm‘s length

price.

(d) Method used for determining the arm‘s length price

[See section 92C(1)].

Yes/No

Clause 17

Back43

Nature of transaction To be

reported

Particulars in respect of lending or borrowing of money :

Has the assessee entered into any international transaction(s) in respect of

lending or borrowing of money including any type of advance, payments,

deferred payments, receivable, non-convertible preference shares/

debentures or any other debt arising during the course of

business as specified in Explanation (i)(c ) below section 92B (2)?

(a) Name and address of the associated enterprise with whom the

international transaction has been entered into.

(b) Nature of financing agreement.

(c) Currency in which transaction has taken place

(d) Interest rate charged/paid in respect of each lending/borrowing.

(e) Amount paid/received or payable/receivable in the transaction—

(i) as per books of account;

(ii) as computed by the assessee having regard to the arm‘s length price.

(f) Method used for determining the arm‘s length price

[See section 92C(1)]

Yes/No

Clause 14

Back44

Nature of transaction To be

reported

Particulars in respect of international transactions of purchase or sale of

marketable securities, issue and buyback of equity shares, optionally

convertible/ partially convertible/ compulsorily convertible debentures/

preference shares:

Has the assessee entered into any international transaction(s) in respect

of purchase or sale of marketable securities or issue of equity shares

including transactions specified in Explanation (i)(c ) below section 92B

(2)?

If yes, provide the following details:

(a) Name and address of the associated enterprise with whom the

international transaction has been entered into.

(b) Nature of transaction

(c) Currency in which the transaction was undertaken

(d) Consideration charged/ paid in respect of the transaction.

(e) Method used for determining the arm‘s length price

[See section 92C(1)]

Yes/No

Clause 16

Back45

Nature of transaction To be

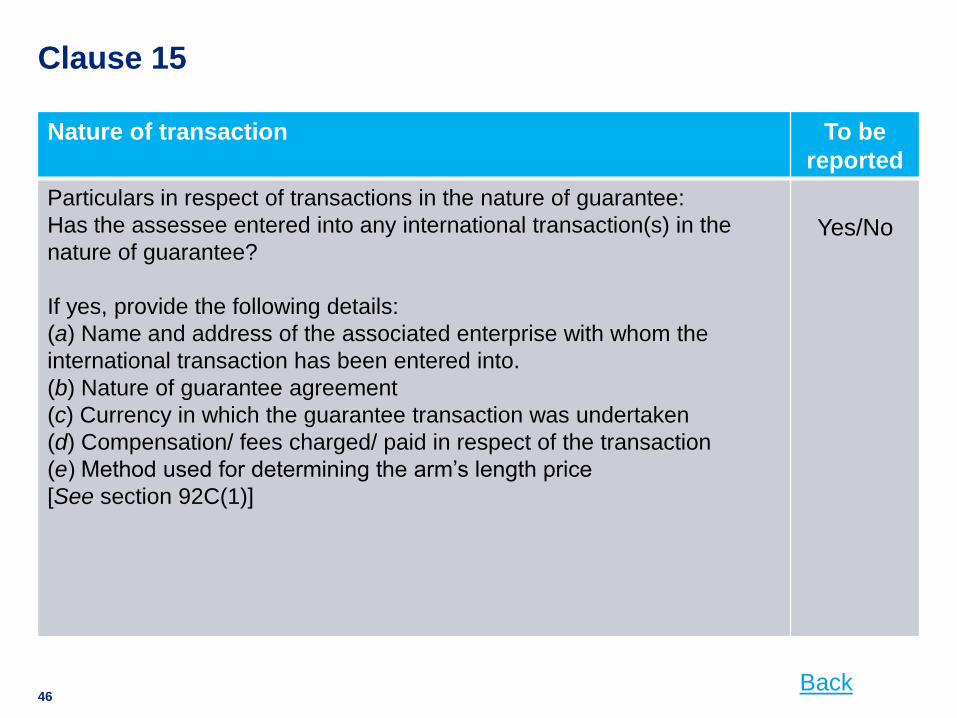

reported

Particulars in respect of transactions in the nature of guarantee:

Has the assessee entered into any international transaction(s) in the

nature of guarantee?

If yes, provide the following details:

(a) Name and address of the associated enterprise with whom the

international transaction has been entered into.

(b) Nature of guarantee agreement

(c) Currency in which the guarantee transaction was undertaken

(d) Compensation/ fees charged/ paid in respect of the transaction

(e) Method used for determining the arm‘s length price

[See section 92C(1)]

Yes/No

Clause 15

Back46

Nature of transaction To be

reported

Particulars in respect of transactions in the nature of any expenditure:

Has the assessee entered into any specified domestic transaction (s)

being any expenditure in respect of which payment has been made or is

to be made to any person referred to in section 40A(2)(b)?

If ―yes‖, provide the following details in respect of each of such person

and each transaction or class of transaction:

(a) Name of person with whom the specified domestic transaction has

been entered into.

(b) Description of transaction along with quantitative details, if any

(c) Total amount paid or payable in the transaction—

(i) as per books of account;

(ii) as computed by the assessee having regard to the arm‘s length price.

(d) Method used for determining the arm‘s length price

[See section 92C(1)]

Yes/No

Clause 22

Back47

Nature of transaction To be

reported

Particulars in respect of any other transaction including the transaction

having a bearing on the profits, income, losses or assets of the assessee:

Has the assessee entered into any other international transaction(s)

including a transaction having a bearing on the profits, income, losses or

asset , but not specifically referred to above, with associated enterprise?

If ‗yes‘ provide the following details in respect of each associated enterprise

and each transaction :

(a) Name and address of the associated enterprise with whom the

international transaction has been entered into.

(b) Description of the transaction.

(c) Amount paid/received or payable/receivable in the transaction—

(i) as per books of account;

(ii) as computed by the assessee having regard to the arm‘s length price.

(d) Method used for determining the arm‘s length price

[See section 92C(1)].

Yes/No

Clause 19

Back48

Nature of transaction To be

reported

Particulars of deemed international transactions:

Has the assessee entered into any transaction with a person other than an

AE in pursuance of a prior agreement in relation to the relevant transaction

between such other person and the associated enterprise?

If yes, provide the following details in respect of each of such agreement

(a) Name and address of the person other than the associated enterprise

with whom the deemed international transaction has been entered into.

(b) Description of the transaction.

(c) Amount paid/received or payable/receivable in the transaction—

(i) as per books of account;

(ii) as computed by the assessee having regard to the arm‘s length price.

(d) Method used for determining the arm‘s length price

[See section 92C(1)].

Yes/No

Clause 20

Back49