1

Why further eurozone integration could hurt Europe’s competitiveness

2

Financial crisis

Debt crisis

Bank crisis

Competitiveness crisis

Political crisis

Europe’s four crises

3

The role of the euro

The crisis started in the US

but... ...the euro locked it in:

– One-size-fits-all interest rates– Perverse incentives – Exposed tremendous imbalances– Political stalemate

4

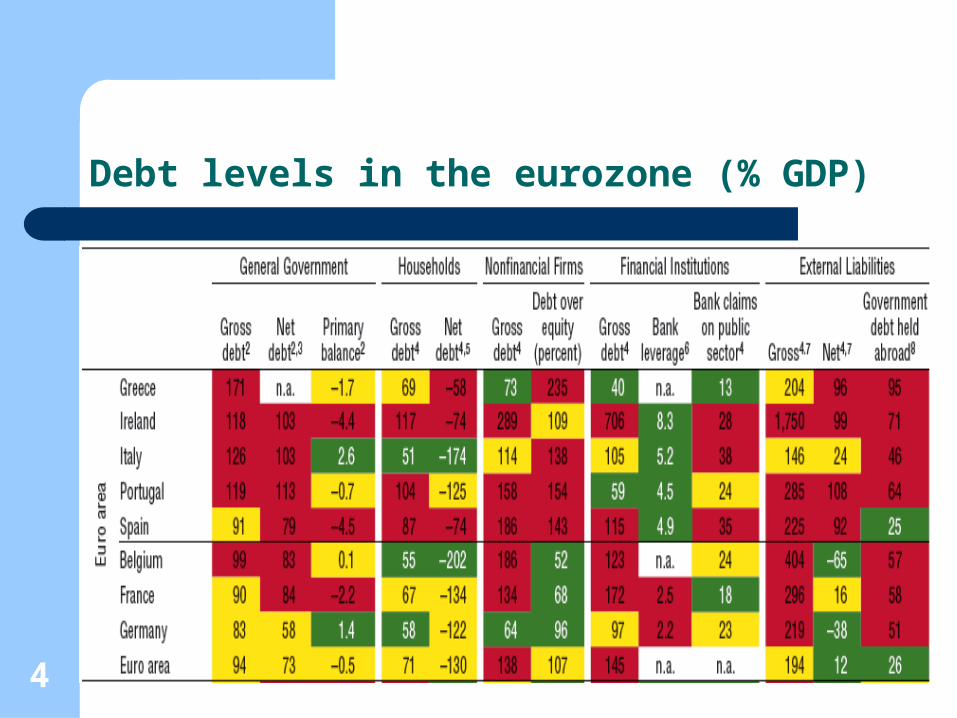

Debt levels in the eurozone (% GDP)

5

Debt crisis: Financing needs PIIGS 2013 - 2015 (€bn)

2013

2014

2015

0 50 100 150 200 250 300 350 400 450 500

GreeceIrelandItalyPortugalSpain

6

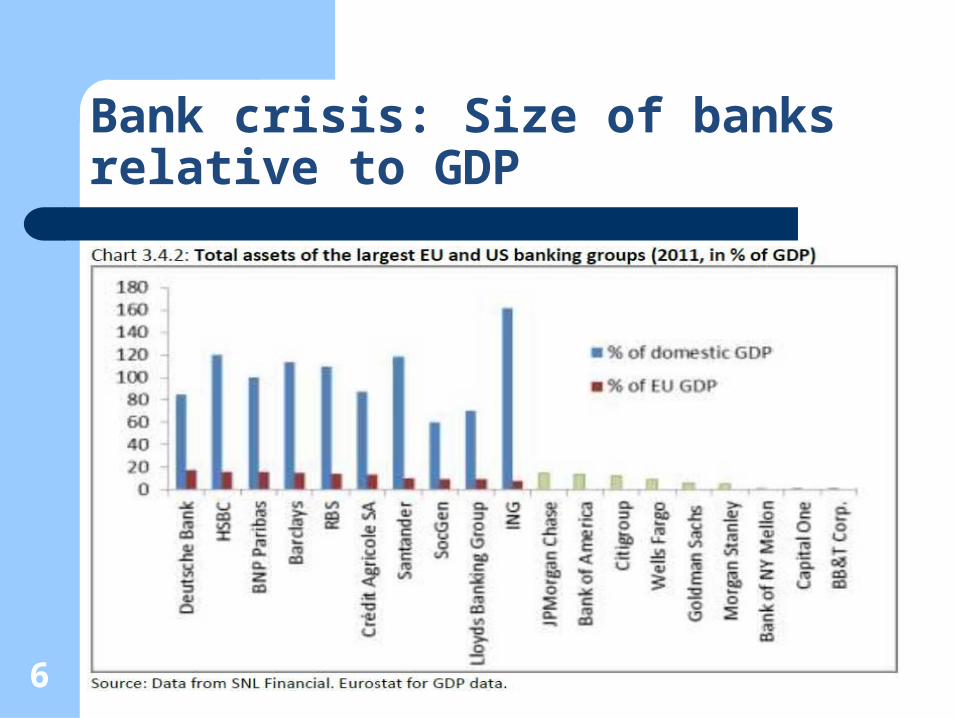

Bank crisis: Size of banks relative to GDP

7

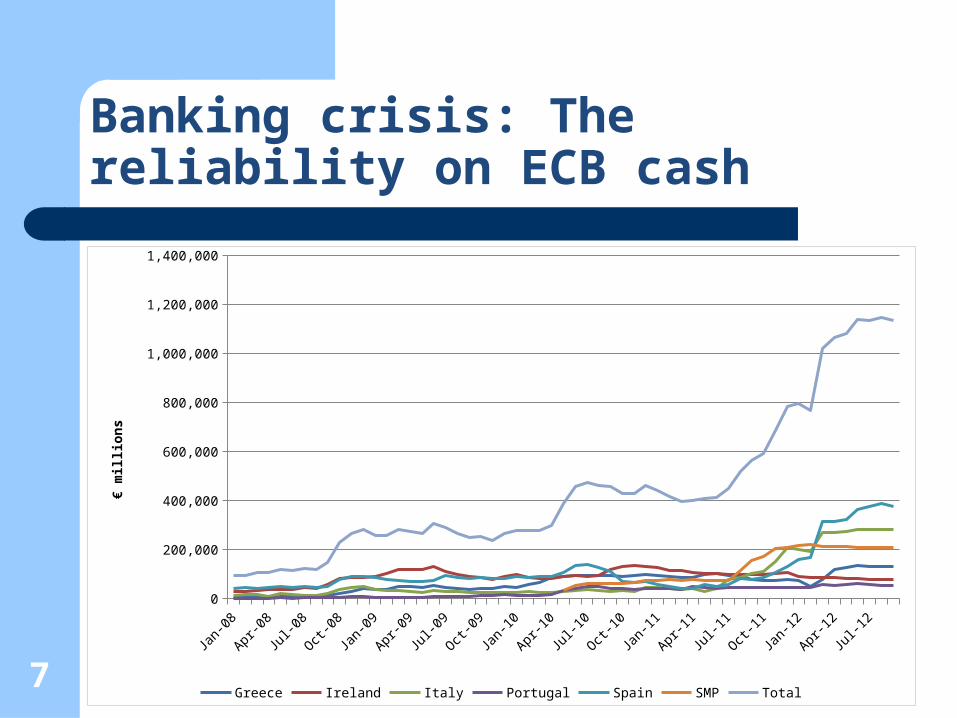

Banking crisis: The reliability on ECB cash

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08Jan

-09

Mar-09

May-09

Jul-09

Sep-09

Nov-09Jan

-10

Mar-10

May-10

Jul-10

Sep-10

Nov-10Jan

-11

Mar-11

May-11

Jul-11

Sep-11

Nov-11Jan

-12

Mar-12

May-12

Jul-12

Sep-12

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Greece Ireland Italy Portugal Spain SMP Total

€ m

illio

ns

8

Bank crisis / debt crisis: Net Balance within Eurosystem / Target [€bn]

Jan-07

May-07

Sep-07

Jan-08

May-08

Sep-08

Jan-09

May-09

Sep-09

Jan-10

May-10

Sep-10

Jan-11

May-11

Sep-11

Jan-12

May-12

-1,250,000

-750,000

-250,000

250,000

750,000

1,250,000

GIIPS

DNLF

DNLF = Germany, Netherlands, Luxembourg, FinlandGIIPS = Greece, Italy, Ireland, Portugal, Spain

Euro Crisis MonitorInstitute of Empirical Economic Research

Osnabrück University

9

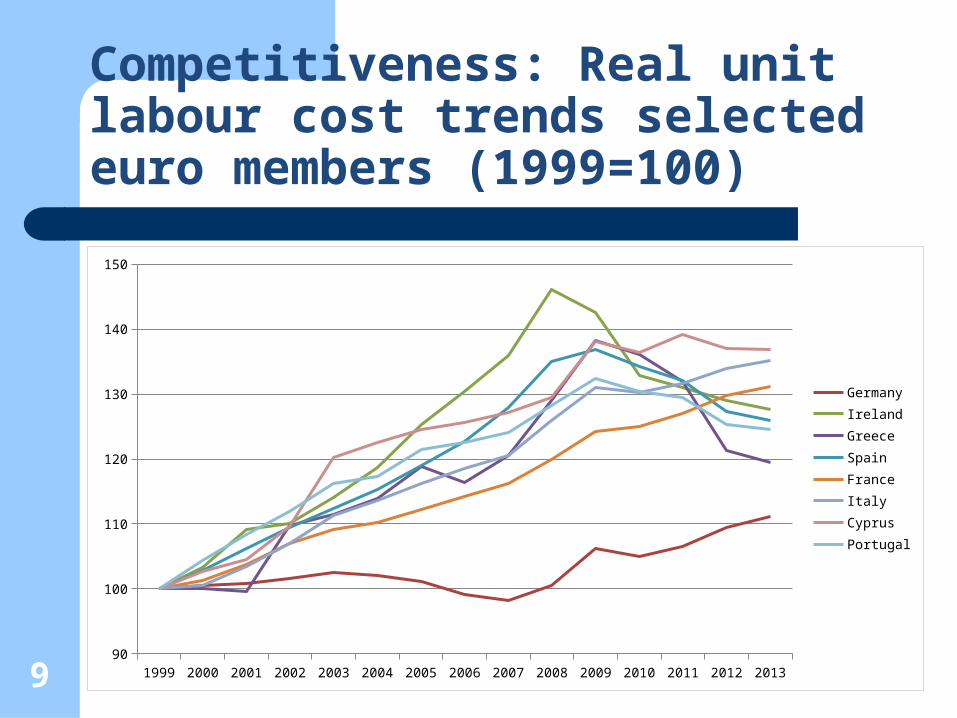

Competitiveness: Real unit labour cost trends selected euro members (1999=100)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 201390

100

110

120

130

140

150

GermanyIrelandGreeceSpainFranceItalyCyprusPortugal

10

Competitiveness: Internal devaluation

Greece Ireland Italy Portugal Spain0

5

10

15

20

25

30

35

40

45

50

Peak20112012

Diffe

renc

e to

Ger

man

labo

ur co

sts (

%)

112000Q1

2000Q3

2001Q1

2001Q3

2002Q1

2002Q3

2003Q1

2003Q3

2004Q1

2004Q3

2005Q1

2005Q3

2006Q1

2006Q3

2007Q1

2007Q3

2008Q1

2008Q3

2009Q1

2009Q3

2010Q1

2010Q3

2011Q1

2011Q3

2012Q10

5

10

15

20

25

30

35

40

45

EU (Total) PIIGS (Total) EU (Youth) PIIGS (Youth)

Competitiveness: Unemployment levels (%)

12

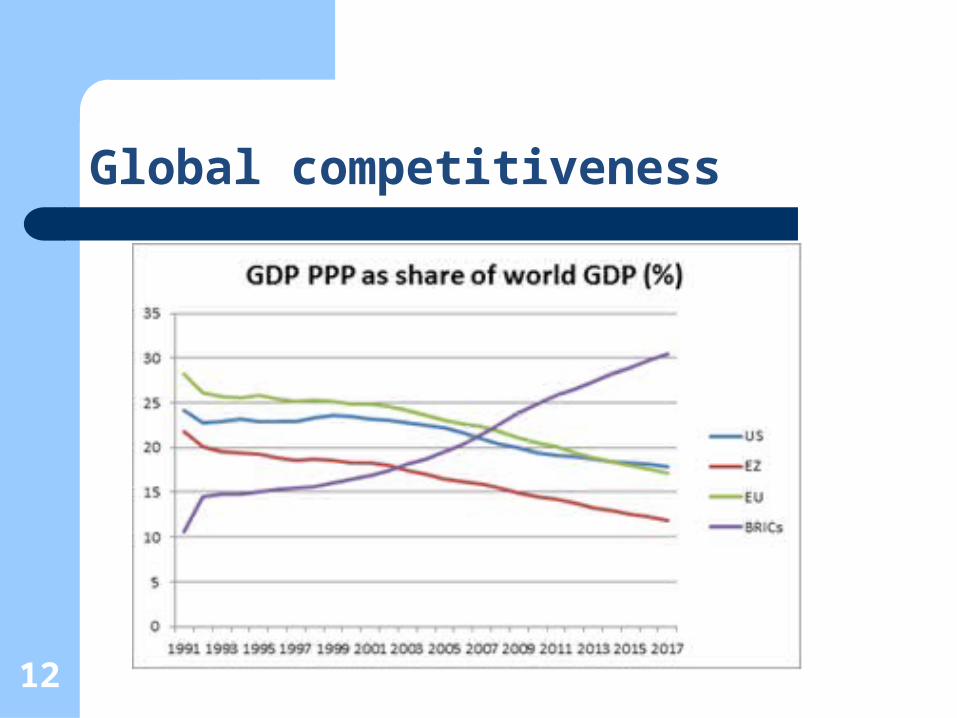

Global competitiveness

13

Global competitiveness

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Labour productivity growth (%)

Euro area Total OECD

14

Is fiscal / banking union the answer?

“Inexorable logic” of the euro? Joint back stop for banks (deposit guarantee

scheme / resolution fund) Fiscal distribution (eurobonds / transfers)

15

1. Can Germany afford it?

Superman: "Easy, Miss, I've got you."

Lois Lane: "You...you've got me, who's got you?"

16

Germany’s demographic trends

2010 2020 2030 2050 20600.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Figure: Eurozone population projections selected member states 2010 - 2060 (millions)

DE

FR

IT

ES

17

2. How to avoid moral hazard in a fiscal / banking union?

Will it be possible to incentivise reforms in a fully fledged fiscal / banking union?

How to avoid déjà vu? Berlin’s answer: strict central controls

18

Political crisis: 17 national democracies

17 national parliaments Electoral cycles Constitutional limitations Public opinion No demos

= Massive risk of political backlash

19

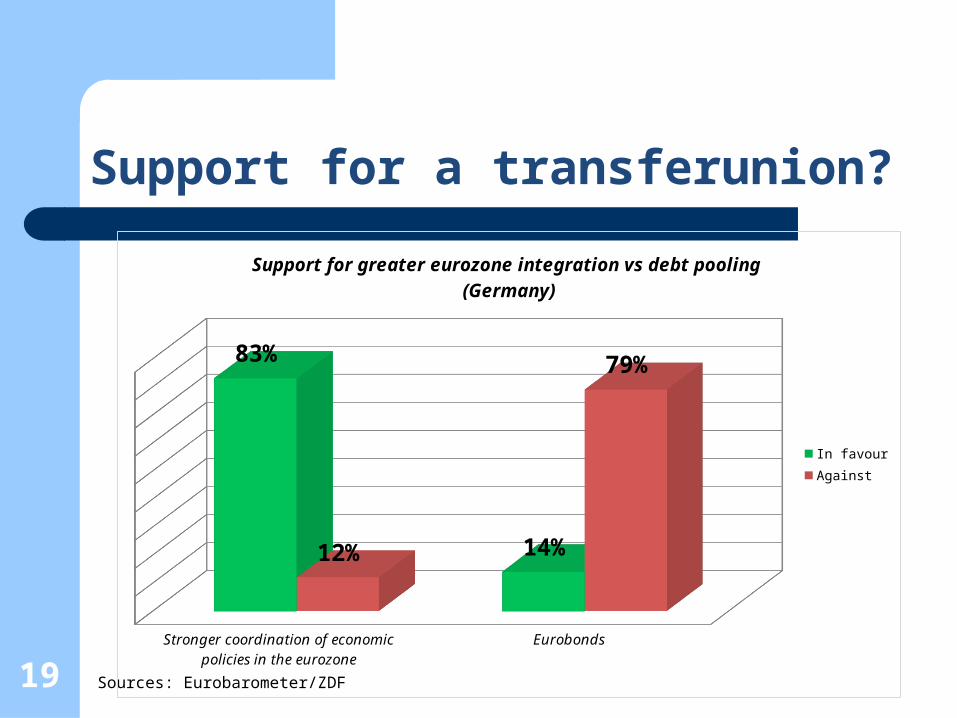

Support for a transferunion?

Sources: Eurobarometer/ZDFStronger coordination of economic policies

in the eurozone Eurobonds

83%

14%12%

79%

Support for greater eurozone integration vs debt pooling (Germany)

In favour

Against

20

Support for central fiscal controls?

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20120

10

20

30

40

50

60

70

80

Do you trust the EU (Portugal, Ireland, Italy, Greece, Spain)?

Trust Do not Trust

21

What alternatives?

Muddle through: Cash for austerity Transfer-union / bank-union: Who’ll be lender

of last resort? Political and economic price? Euro break-up: Greece or more countries?