Download - Vedanta Zinc International: Home

Vedanta Resources plcCorporate Presentation

March 2011

1

Cautionary Statement and Disclaimer

The views expressed here may contain information derived from publicly available sources that have not been independently verified.

No representation or warranty is made as to the accuracy, completeness, reasonableness or reliability of this information. Any forward looking information in this presentation including without limitation any tables charts and/or graphs hasAny forward looking information in this presentation including, without limitation, any tables, charts and/or graphs, has been prepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendation or forecast by Vedanta Resources plc ("Vedanta"). Past performance of Vedanta cannot be relied upon as a guide to future performance.

This presentation contains 'forward looking statements' that is statements related to future not past events In thisThis presentation contains forward-looking statements – that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance, and often contain words such as 'expects,' 'anticipates,' 'intends,' 'plans,' 'believes,' 'seeks,' or 'will.' Forward–looking statements by their nature address matters that are, to different degrees, uncertain. For us, uncertainties arise from the behaviour of financial and metals markets including the London Metal Exchange, fluctuations in interest and or exchange rates and metal prices; from future integration of acquired businesses; and from numerous other matters of national, regional and p ; g q ; , gglobal scale, including those of a environmental, climatic, natural, political, economic, business, competitive or regulatorynature. These uncertainties may cause our actual future results to be materially different that those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements.

This presentation is not intended, and does not, constitute or form part of any offer, invitation or the solicitation of anThis presentation is not intended, and does not, constitute or form part of any offer, invitation or the solicitation of an offer to purchase, otherwise acquire, subscribe for, sell or otherwise dispose of, any securities in Vedanta or any of its subsidiary undertakings or any other invitation or inducement to engage in investment activities, nor shall this presentation (or any part of it) nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or investment decision.

2

Vedanta: A Diversified Natural Resources Group

FY 2009 - 10 FY 2010 -11E Pro Forma

Aluminium

FY 2011-12E Pro Forma

Aluminium

CopperIron Ore

Power

CopperOil & GasAluminiumPower

Iron Ore Copper

Power

Zinc-India

Zinc-India (HZL)

Zinc-India (HZL)

Zinc-Intl.

EBITDA: US$2.3bn Analyst EBITDA consensus: $8.4bn1&2

(including Oil and Gas)

Iron Ore

Zinc India (HZL)

Analyst EBITDA Consensus: US$3.5bn1

(HZL) (Anglo Zinc) Zinc-Intl. (Anglo Zinc)

Vedanta is one of the world’s leading diversified Natural Resources group

First Indian group to be listed on LSE; ranked 51 in FTSE 100

Over 34,000 employees globally, including 9,600 professionals, p y g y, g , p

Industry-leading organic growth programme – $19 billion capex, c. 2/3 already spent

31. Company estimate for Zinc-International 2. Vedanta: US$5.8bn; Cairn India:US$2.6bn

Strategy Focused On Value And Growth

Organic growth focused strategy

Leverage unique position in India

Asset optimisation

Structural low cost advantage

Exploration focus

Selective value accretive M&A optimisationSelective, value accretive M&A

Large brownfield assets

Embedded growth options

High quality long life assets

Unlocking value

Leverage core asset development & operational skills

g

World class assets

Opportunity to list vertical business lines (including the IPO of Sterlite

Energy and KCM)

Inherent value in Silver business

4

Cairn India: Compelling Growth Opportunity

260

RajasthanCambay BasinRavva

Entry into attractive Indian oil & gas sector

Cairn India Production Profile (kboepd, Gross)

200

Ravva

Gross 6.5 bn barrels of oil in place

125175

240+

159Significant exploration acreage, 35+ prospects identified

4

125

44Doubling production in short term to 240,000 bopd at Rajasthan

2009 2010 2011 Target

Source:Wood Mackenzie, Company data

5

Strong Metals and Energy Growth in India

1,000 5Zinc (kt) LHS Copper (kt) LHS

Aluminium (mt) RHS Oil (mbpd) RHS 1,500Demand Supply

Resource Consumption Growth in India Peak Power Capacity Deficit in India (bn units)

600

800

3

4

1,100

1,300FY06–10 CAGR:Demand : 7.1%Supply : 6.6%

200

400

1

2

700

900FY10–15 CAGR:Demand : 10%Supply : 11%

0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010E

2011E

2012E

2013E

2014E

2015E

0 500

FY06

FY07

FY08

FY09

FY10

FY11

E

FY12

E

FY13

E

FY14

E

FY15

E

S D t h B k W ld D l t I di t IIFL R h BMI I di Oil & G R t 2010

Infrastructure Spending

Increasing Urbanisation

Favourable Demographics

Metals and Energy

Demand

Source: Deutsche Bank, World Development Indicators, IIFL Research, BMI: India Oil & Gas Report 2010

Notes: Metal and oil consumption are calendar year based

6

Industry Leading Organic Growth Programme

Vedanta Copper Equivalent Exit Capacity (kt)

2,500

1 500

2,000

1,000

1,500

500

0

FY2003-04 FY 2006-07 FY 2009-10 FY 2010-11 FY 2011-12 FY 2012-13

Oil and Gas Zinc-Intl Zinc-India Silver Aluminium Power Iron Ore Copper

Notes: 1. All metal and power capacities rebased using Copper LME and Commodity prices as on 3 February 2011

2. Copper custom smelting capacities rebased at TC/RC for H1 FY 2010-11

7

World’s Largest Zinc-Lead Producer

1,064

1,263

464Sterlite

Xstrata

Zinc-International Zinc-India (HZL)

Global Zinc and Lead Mine Production (kt) - 2010E1 Zinc - Lead R&R (Mt): 25+ Years Mine Life

5052

2 3 1,528

843

533

Teck

Glencore 206

655Rampura-Agucha

364Boliden

Top Zinc Mines MIC (kt) – 2010E(13.4%)

542505

375330

300224

Red Dog

Century

Antamina

Mount Isa Pb/Zn

San Cristobal

Brunswick144

299

(16.3%)

(11.3%)

(0.5%)

(7.0%)

(1.5%)

(8.2%)

194

177173170164

400

Lanping

Mc Arthur River

Lisheen

Tara

Skorpion

Gamsberg

FY 2002-03 FY 2009-10

(8.2%)

(9.3%)

(11.6%)

(7.2%)

(11.3%)

(6 7%)400Gamsberg

Data in bracket represents Zinc grade based on proved and probable reserves

Note: 1. Based on production of metal contained in concentrate.

2. Targeted production capacity on 100% basis

3. Actual Production of CY 2010 on 100% basis

Source: Brook Hunt, Company Data

Zinc International R&R as on 31 December 2009, Zinc India as on 31 March 2010(Potential)

(6.7%)

8

Zinc Mining Cost: Zinc-India competitively positioned on Global Cost Curve

($90

9)

tile

($1,

267)

2000

2300

s ($

668)

atio

ns(H

ZL)(

$300

)

Qua

rtile

($59

2)

Seco

ndQ

uart

ile(

Thir

dQ

uart

1100

1400

1700

1) natio

nal O

pera

tions

Indi

aO

pera

Firs

tQ

200

500

800

Min

ing

Cash

Cos

t (C

($/t

)

Inte

r

-700

-400

-100

M

0 10 20 30 40 50 60 70 80 90 100-1000

Cumulative Production

Source: Brook hunt, 9 months FY 2010-11 for cash cost of Sterlite: HZL costs excludes Silver credit

Note : Cost of International operations is weighted average mining cost of Lisheen and Black Mountain for CY2009

9

Zinc-International: Skorpion Mine, Namibia

Overview

SkorpionAcquisition completed on 3 December 2010Integrated zinc refining: Unique technology to

Zinc Production (kt)

Integrated zinc refining: Unique technology to extract zinc metal from zinc oxide oreReserves & Resources: 8.3 Mt11.3% Zinc

Gergarub145

150152

gZinc-lead sulphide depositDiscovered in 2008

CY 2008 CY 2009 CY 2010

10

Zinc-International: Black Mountain Mine, South Africa

Overview Production (kt)

Black MountainAcquisition completed on 4 February 2011

U d d i d i i d l d

Zinc Lead

Underground mine producing zinc and lead

New mining infrastructure related to deep shaft coming online mid-2010

Reserves & Resources: 51.7Mt28 28 36

47 49

51

Gamsberg Project

1.5% Zinc and 2.9% Lead

By Products: Copper and Silver

28 28

CY 2008 CY 2009 CY 2010

One of the world’s largest undeveloped zinc deposits, located near the Black Mountain mine

T l f 186 l d iTotal resources of 186mt, located in two ore bodies

Grade: 6.9% Zinc and 0.4% Lead

Potential to produce 400 ktpa of zincPotential to produce 400 ktpa of zinc

11

Zinc-International: Lisheen Mine, Ireland

Overview Production (kt)

Lisheen

Acquisition completed on 15 February 201121

Zinc Lead

Underground Mine

Reserves & Resources: 8.7 Mt

11.9% Zinc and 1.9% Lead 167172 175

16

1921

CY 2008 CY 2009 CY 2010

12

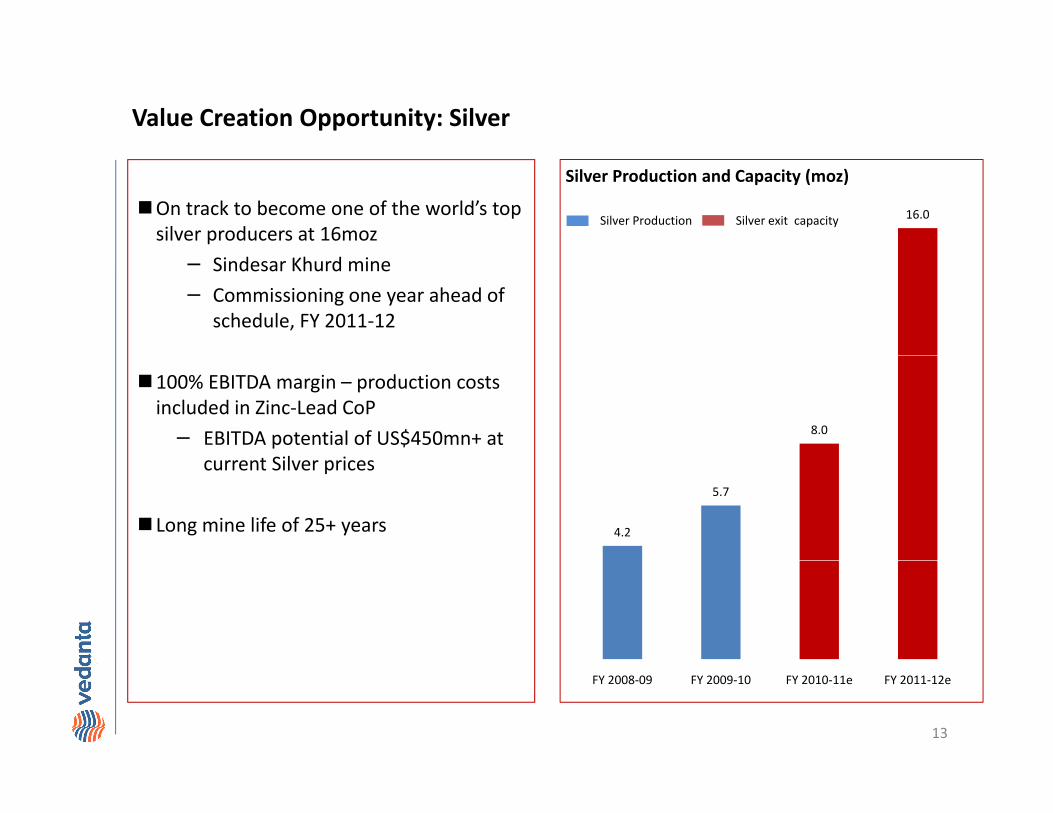

Value Creation Opportunity: Silver

16.0Silver Production Silver exit capacityOn track to become one of the world’s top silver producers at 16moz

Silver Production and Capacity (moz)

− Sindesar Khurd mine

− Commissioning one year ahead of schedule, FY 2011-12

8.0

100% EBITDA margin – production costs included in Zinc-Lead CoP

− EBITDA potential of US$450mn+ at t Sil i

4.2

5.7

current Silver prices

Long mine life of 25+ years

FY 2008-09 FY 2009-10 FY 2010-11e FY 2011-12e

13

/ 2

Silver : Unlocking Accumulated Value

F ill 17,806Fresnillo

EV of pure-play silver

producers ($mn)Zinc-India vs pure-play

silver producers (koz)1

EV/EBITDA2

13.5Fresnillox

41,388

28,745

Fresnillo

Silver Wheaton

17,806

13,730Silver Wheaton 22.8

Fresnillo

Silver Wheaton x

8,206Silver Standard 2,154Silver Standard 13.9Silver Standard x

4,433Silvercorp 2,475Silvercorp 20.9Silvercorp x

16,000

0 10,000 20,000 30,000 40,000

HZL (2012E)

0 5 000 10 000 15 000 20 0000 5,000 10,000 15,000 20,000

Source: Broker reports, Factset, Bloomberg as of February 21, 2011

1Peers production is as per 2011E

2 EBITDA based on CY 2011 estimates for peers

0 10 20 30

14

Aluminium: Optimising Returns

Power for sale (MW)

Unit Pre Deferral1 Post Deferral1

Aluminium capacity (kt)

2,500

1,200MWCPP at BALCO

600 1,200

2,400MWIPP t Jh d

600 2,400

260

500

IPP at Jharsuguda ,

BALCO-1 CPP 270 270

T t lBALCO

Jharsuguda

Present TargetTotal 1,470 3,870

FY10 Production FY12 Capacity Post Captive BauxiteFY10 Production FY12 Capacity Post Captive Bauxite

2,500kt Aluminium

760kt Aluminium and 3,570MW Surplus Power

533kt Aluminium

1: The first metal tapping from the 325 ktpa smelter at BALCO and 1.25 mtpa Smelter at Jharsuguda has been deferred

15

Aluminium : Positioning on Global Cost Curve

$1,9

74)

)($1,

840)

rtile

($2,

064)

2500

3000

96)Target costs of

$1 800 1 900/tTarget cost of $1 100 1 200/t

uart

ile($

1,56

5)

Jhar

sugu

da(

Korb

a($

1,78

5)

Seco

ndQ

uart

ile(

Thir

dQ

ua

2000

ost (

C1)

/t)

Veda

nta

($1,

8$1,800-1,900/t with bought-out bauxite and alumina

$1,100-1,200/t with captive bauxite

Firs

tQ1500

Cash

Co

($/

1000

0 10 20 30 40 50 60 70 80 90 100

500

Cumulative Production

16

Source: Brook hunt, 9 months FY 2010-11 for cash cost of Sterlite/ Vedanta

Commercial Energy - IPPs

Jharsuguda 2,400 MW

Talwandi Sabo 2,640 MW

SEL capacity (MW)Jharsuguda 2,400 MW (4 x 600 MW)

Synchronisation−Unit 1: Q2 FY 2010-11−Unit 2: Q3 FY 2010-11−Unit 3: Q2 FY 2011-12

5,040

Unit 3: Q2 FY 2011 12−Unit 4: Q3 FY2011-12

Fuel arrangements−65% Coal linkage−25-30% E-Auction/ Forward E-Auction−5-10% Imported Coal

2,640

3,060

Off Take arrangements−First unit to Grid−Balance in Merchant Market - 60% under Short term sales

agreement, 40% spot

T l di S b 2 640 MW (4 660 MW) 6602,400

Talwandi Sabo 2,640 MW (4 x 660 MW)

Synchronisation−Unit 1: Q4 FY 2012-13−Unit 2: Q1 FY 2013-14−Unit 3: Q2 FY 2013-14

1,200

2,400 2,400 2,4001,200−Unit 4: Q3 FY 2013-14

Fuel arrangements− Coal linkage in place for 1,980 MW

Off Take arrangements− 1 980 MW to Grid

FY 2010-11e FY 2011-12e FY 2012-13e FY 2013-14e

17

− 1,980 MW to Grid− 85% of balance 660 MW in Merchant Market and 15% to Grid

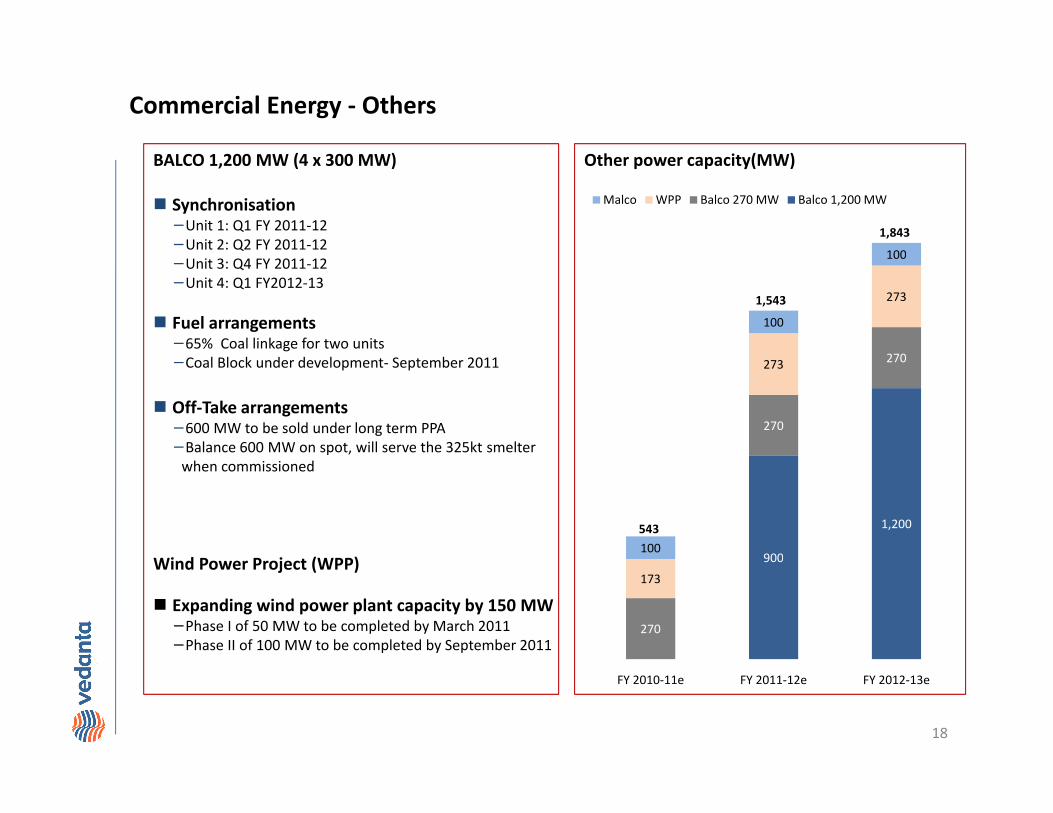

Commercial Energy - Others

100

Malco WPP Balco 270 MW Balco 1,200 MW

Other power capacity(MW)BALCO 1,200 MW (4 x 300 MW)

Synchronisation−Unit 1: Q1 FY 2011-12−Unit 2: Q2 FY 2011-12

1,843

270

273

100

100−Unit 3: Q4 FY 2011-12−Unit 4: Q1 FY2012-13

Fuel arrangements−65% Coal linkage for two units

1,543

270

270273−Coal Block under development- September 2011

Off-Take arrangements−600 MW to be sold under long term PPA−Balance 600 MW on spot, will serve the 325kt smelter

900

1,200

100

when commissioned

Wi d P P j t (WPP)

543

900

270

173Wind Power Project (WPP)

Expanding wind power plant capacity by 150 MW−Phase I of 50 MW to be completed by March 2011−Phase II of 100 MW to be completed by September 2011

FY 2010-11e FY 2011-12e FY 2012-13e

18

Copper - Creating Value at KCM

275

350

400+Pre Vedanta ownership

– Long operating history with quality asset base, but limited mine life

– Significantly underinvested

Increasing copper production

173

– Significantly underinvested

$1.8bn capital investment

– Significant reserves and resources added

– New smelter utilising latest technology

FY 2009-10A FY 2009-10e FY 2010-11e FY 2011-12e

1. Exit capacity

1 1 1

g gy

– Konkola Deeps Mining Project

– Asset optimisation

Delivering future value$/

1.80

1.39

– Substantial high grade R&R

– Integrated, well invested assets

– Production growth

– Improved cost performance

Integrated cash costs (US$/lb)

1.00– Valued local partner

FY 2009-10A Sep 10 Target

19

Copper – India/Australia

Production (kt) Exit capacity (kt)

Overview

One of the world’s largest single location copper custom

smelter

Production and Capacity (kt)

800

LME registered Cathodes and value added rods capacity of

240,000 tpa

Efficient by-product management

Captive power plant under construction

313 334 400

FY 2008-09 FY 2009-10 FY 2010-11e FY 2012-13e

Captive power plant under construction

Doubling capacity to 800 ktpa to further improve the market

share

Stable operations at CMT copper mines Australia – 30,000 tpa

20

Copper Smelting : Lowest Decile

40

USc

11.3

)

arti

le (U

Sc16

.4)

25

30

35

h Co

stb)

rin

(Usc

5.0)

Qua

rtile

(USc

5.6)

Seco

nd Q

uart

ile (

Thir

d Q

u a

10

15

20

Net

Cas

h(c

/lb

Tutic

o

Firs

t Q

0

5

10

0 10 20 30 40 50 60 70 80 90 100-5

Cumulative Production

Source: Brook hunt, 9 months FY 2010-11 for cash cost of Sterlite

21

Iron Ore Expansion

40 0

Production (mt) Exit capacity (mt)

Doubled iron ore production since acquisition in 2007 by Vedanta

Lowest quartile producer*

Iron ore Production and proposed capacities

KA 10

40.0Lowest quartile producer

– Goa continues to be in lowest decile

Logistics and infrastructure key to unlocking 40mtpa

15 9

21.4

40mtpa

– Goa & Karnataka expansions on track subject to environmental clearances

Expanding Pig iron capacity from 250 ktpa toGoa3011.3

15.9Expanding Pig iron capacity from 250 ktpa to 625 ktpa and Met coke capacity from 280 ktpa to 560 ktpa

FY 2007-08 FY 2008-09 FY 2009-10 FY 2012-13e

Notes: Capacities in FY 2012-13e refer to exit rates* - Excluding export duty and royalty p f

All capacities in WMT

22

Corporate Social Responsibility

Case Study: Health Update

General Health Outreach

55,419 people benefited through 28 company run

Impact

552 villages, 2.7 million people positively impacted

145 villages under the Integrated Village Development hospitals

47,828 people reached by mobile health units

293,197 people benefited through 1883 health

awareness camps

Program

Health care services outreach to over 308,000 people

20,000 children enrolled for computer education in 200

government schoolsp

1,236 patients screened and benefited by Vedanta

Cancer Hospital outreach

N i i

government schools

770 Self Help Groups, 27,100 members earnings

supplemented

6,652 farmers, 1470 acres covered under the agriculture

and watershed programNutrition

230,000 children at 2,232 government schools

benefited through 8 mid-day meal kitchens

136,707 children covered through 2,546 pre-school

and watershed program

81 NGO partners, 77 CSR personnel and 199 extension

workers

centres under the Vedanta Bal Chetna Anganwadi

programme

23

Summary

Vedanta Copper Equivalent Capacity (kt)

2 000

2,500

1,500

2,000

500

1,000

0

FY2003-04 FY 2006-07 FY 2009-10 FY 2010-11 FY 2011-12 FY 2012-13

Oil and Gas Zinc-Intl Zinc-India Silver Aluminium Power Iron Ore Copper

Significant near term production growth across attractive commodity portfolio

Diversified Earnings

24

Strong cash flow growth

A diAppendix

25

Zinc-International: Financial Highlights

Skorpion CY 2009 CY 2010

EBITDA ($mn) 100 165

CoP (c/lb) 41 46

Black Mountain

Depreciation ($mn) 57 62

Tax rate (%) 1-5% 1-5%

Black MountainCY 2009 CY 2010

EBITDA ($ mn) 55 73

CoP (c/lb) 56 69

Depreciation ($mn) 1 1

LisheenCY 2009 CY 2010

Tax rate (%) 28% 27%

EBITDA ($mn) 72 115

CoP (c/lb) 58 58

Depreciation ($mn) 1 4

Tax rate (%) 7% 13%

26

Zinc-International: Consideration Paid

Particulars Skorpion

($mn)Black Mountain

($mn) Lisheen ($mn)

Total ($mn)

Debt-Cash free acquisition price announced on 10 May 2010 698 332 308 1,338

Add: Opening Net Cash / (Net Debt) 46 (100) 209 155

Share Value 744 232 517 1,493

Add: Accrued Interest on Share Value from the period of announcement of acquisition up to completion

51 29 29 109

Less: Dividend and Others (88) (1) - (89)

Share Value as at acquisition completion 707 260 546 1,513

Add: Settlement of loans as at closing of acquisition - 88 - 88

Cash paid on closing 707 348 546 1,601

Note: Economic ownership, including profits and cash flows passing to Sterlite with effect from of 1 January 2010.

27

Vedanta Group Structure

Vedanta Resources(Listed on LSE)

Konkola Copper Mines (KCM)

54.6%

Madras Aluminium (MALCO)

94.5%70.5%

29.5%Sterlite Industries

(Listed on BSE and NSE and NYSE)

VedantaAluminium (VAL)

79.4%

Sesa Goa (Listed on BSE

and NSE)

55.7%

3.1%

51 0%100%

64 9%100%

VS Dempo and Company Private Limited

100%

51.0% 64.9%

Zinc-India(HZL)(Listed on BSE

and NSE)

AustralianCopper Mines

Bharat Aluminium (BALCO)

Sterlite Energy(DRHP filed)

100% 74%

CopperAluminium

KEY

Skorpion and

Lisheen

Black Mountain

100% 74%

Zinc-International

Zinc-India (HZL)

PowerIron ore

Structure as at 30 September 2010. Zinc-International acquisition completed – February 2011

Zinc-International

28