VAT – value added taxChapter 6

Cost Price

Mark-up Selling

Price

Profit

Farmer R5 R5 R10 R5

Manufacturer R10 R5 R15 R5

Wholesaler R15 R5 R20 R5

Retailer R20 R5 R25 R5

Consumer R25

Cost Price

VATInput

Mark-up

Selling

Price

VAT Out put

Pay to

SARS

Profit

Farmer R5.70 R0.70 R5 R11.40

R1.40 R0.70 R5

Manufacturer R11.40 R1.40 R5 R17.10

R2.10 R0.70 R5

Wholesaler R17.10 R2.10 R5 R22.80

R2.80 R0.70 R5

Retailer R22.80 R2.80 R5 R28.50

R3.50 R0.70 R5

Consumer R28.50

VAT Indirect tax Charged on the supply of:

Goods or Services

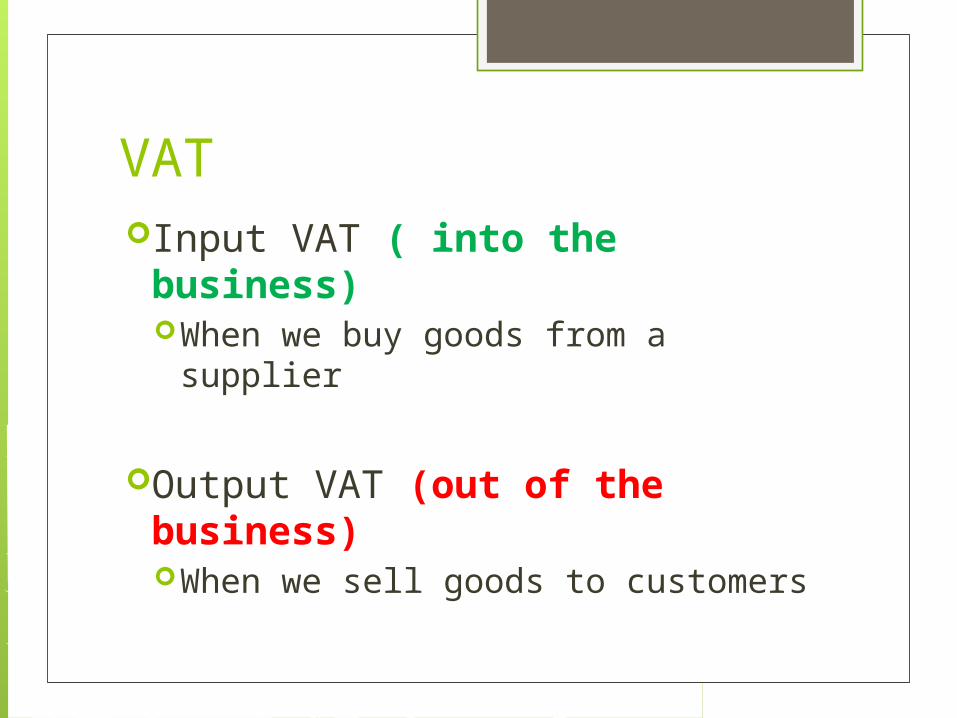

2 types of VAT Input VAT - purchases Output VAT - sales

VATInput VAT ( into the business)

When we buy goods from a supplier

Output VAT (out of the business)When we sell goods to customers

VATStandard

Rated Supplies

Exempt Supplie

s

Zero-Rated

Supplies

VAT

VAT – standard-rated Standard-Rated Supplies

All goods and services are standard rated unless specifically Exempt Zero-rated

Standard-rated supplies are taxed at a rate of 14%

VAT - exempt supplies Exempt Supplies

No VAT is paid or chargedNo VAT is or can be claimed back

VAT is not charged on these goods or services

No VAT, not at standard rate (14%) zero-rate (0%)

VAT - exempt supplies

No VAT is charged on the following Financial services – interest received & interest paid

medical aids, provident, pension or retirement funds Life assurance Donated goods or services sold by non-profit bodies Rent – for use as a private home (not holiday homes) Passenger transport in South Africa – bus, taxi or train Educational services – schools, universities

Vat - zero-rated supplies

Taxable supplies where 0% can be claimed back 0% charged to customers

Fuel – petrol, diesel and illuminating paraffin Services provided to foreign residents

(certified by customs) Direct exports – supply to a customer in

another country Sale of a going concern Any service rendered by a welfare society

VAT – zero rated supplies Brown bread Brown flour Eggs Dried beans Maize meal Pilchards in cans Milk or milk

powder Mielie rice

Dried mielies Samp Fresh/frozen fruit &

vegetables Lentils Rice Oil – only vegetable

Non-allowable items

Does the item paid for

constitute an essential input to our business to

create outputs on which VAT output will be charged?

Non-allowable items

A business cannot run properly without water & electricity, telephone, advertising and equipment.

SARS will therefore allow a business to claim VAT input on such items.

Non-allowable itemsA business can operate without gym membership, refreshments and entertainment. SARS will therefore not allow any VAT claims on these items.

Denied Input Tax Entertainment – goods or services

obtained for entertainment purposes

Any fees – sporting, social or recreational

Buying a motor car

Goods or services acquired by Medical schemes or

Denied Input Tax Entertainment

Refreshments, Christmas parties, customer entertainment & equipment to provide staff refreshments

Allowable entertainment While away on business Seminars Entertainment is what the business does Welfare organisations events for fund-

raising

Denied Input Tax Motor cars

The Act specifies what a motor car is Cannot claim VAT even if the vehicle is

strictly being used by the business Motor cars as per the Act includes:

Double cab bakkies Sedan type passenger vehicles Station wagons Minibuses Sport utility vehicles

Denied Input Tax(allowed vehicles – per the ACT) Goods transportation trucks. Single cab delivery vehicles. Motor cycles. Caravans. Ambulances, game viewing vehicles and hearses. Vehicles capable of accommodating more than

16 persons (for example, a bus). Vehicles with an unladen mass of 3500 kg or

more. Special purpose vehicles constructed for

purposes other than the carrying of passengers. Equipment such as bulldozers, graders, hysters,

harvesters and tractors.

VAT - deemed suppliesRequired to pay output tax

Goods or services taken for own use Certain fringe benefits to staff Assets retained when deregistering as a

vendor Insurance claims Subsidies or grants received from state Goods acquired under an instalment credit

agreement that’s been repossessed from you

VAT - Notional VAT A VAT vendor can claim input tax when

purchasing second-hand goods Even if no VAT was paid E.g if you buy a second-hand car If you paid R20 000 then you can claim

the input tax. Can claim R20 000/1.14 x 14% = R 2

456 Calculate the VAT assuming the

purchase price includes VAT

VAT vendorsTurnover = > R1000 000

compulsory to register for VAT

Pay VAT over to SARS every 2 months Group A - Jan, Mar, May, July, Sep,

Nov Group B - Feb, Apr, June, Aug, Oct,

Dec

VATVAT is not charged on:

Money received from or paid to the owner

Salaries and wages

Interest income

Payment vs Invoice Basis Payment Basis

Only record VAT input once cash is paid Only record VAT output once cash is

received

Invoice Basis Record VAT input once the sale is made,

invoice is created. Record VAT output once a purchase is

made, invoice is received.

Payments Basis Vendor only accounts for VAT on actual

payments made and actual payments received

A vendor must apply in writing to SARS to apply the payments basis.

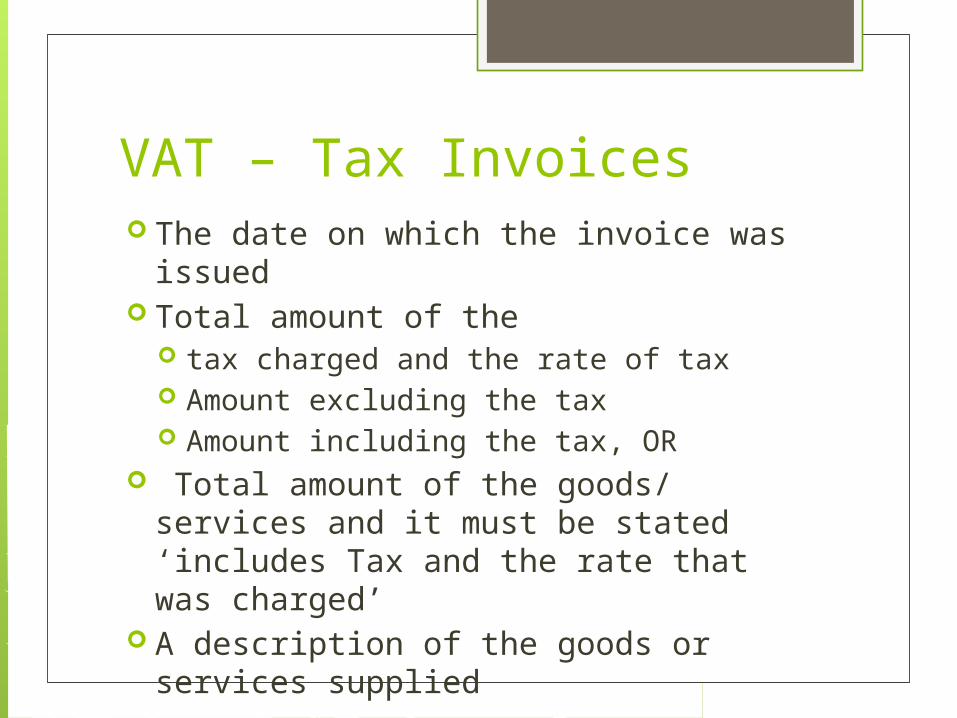

VAT – Tax InvoicesTax Invoices must contain the following information The words “Tax Invoice” Name, address and registration number

of the supplier Name and address of the customer The VAT registration number of the

customer An individual unique number for each

tax invoice

VAT – Tax Invoices The date on which the invoice was

issued Total amount of the

tax charged and the rate of tax Amount excluding the tax Amount including the tax, OR

Total amount of the goods/ services and it must be stated ‘includes Tax and the rate that was charged’

A description of the goods or services supplied

Approved methods for reflecting the consideration and VAT