Utilities | Stock Recommendation

Nihar ShahMichael Song

03.09.2010

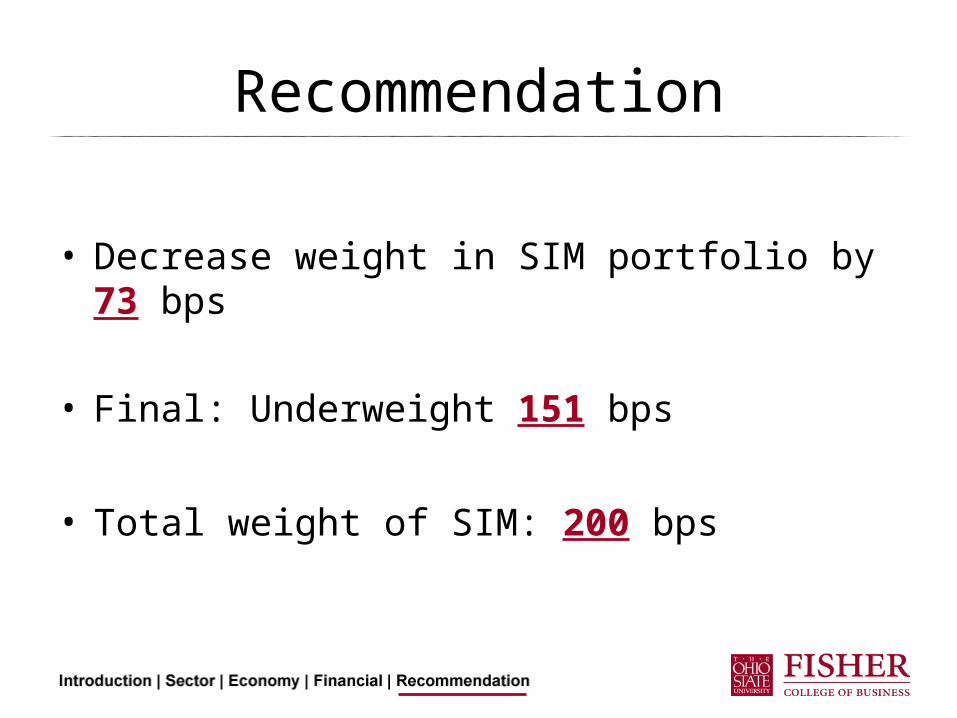

Recommendation

• Decrease weight in SIM portfolio by 73 bps

• Final: Underweight 151 bps

• Total weight of SIM: 200 bps

Introduction

• Utilities Sector– Size: 1721.2B– Industries

Industry Market Cap P/E ROE % Div. Yield % Price to Book

Diversified Utilities 135.0B 11.5 13.00% 4.69% 1.84

Electric Utilities 301.6B 15.1 10.00% 3.95% 1.81

Foreign Utilities 1170.9B 86.0 1.60% 1.58% 1.98

Gas Utilities 104.3B 15.7 13.80% 3.99% 3.31

Water Utilities 9.5B 0.0 -5.20% 3.47% 1.75

Source: Yahoo Finance as of 2/23/10

S&P/SIM Weight

(.78)%

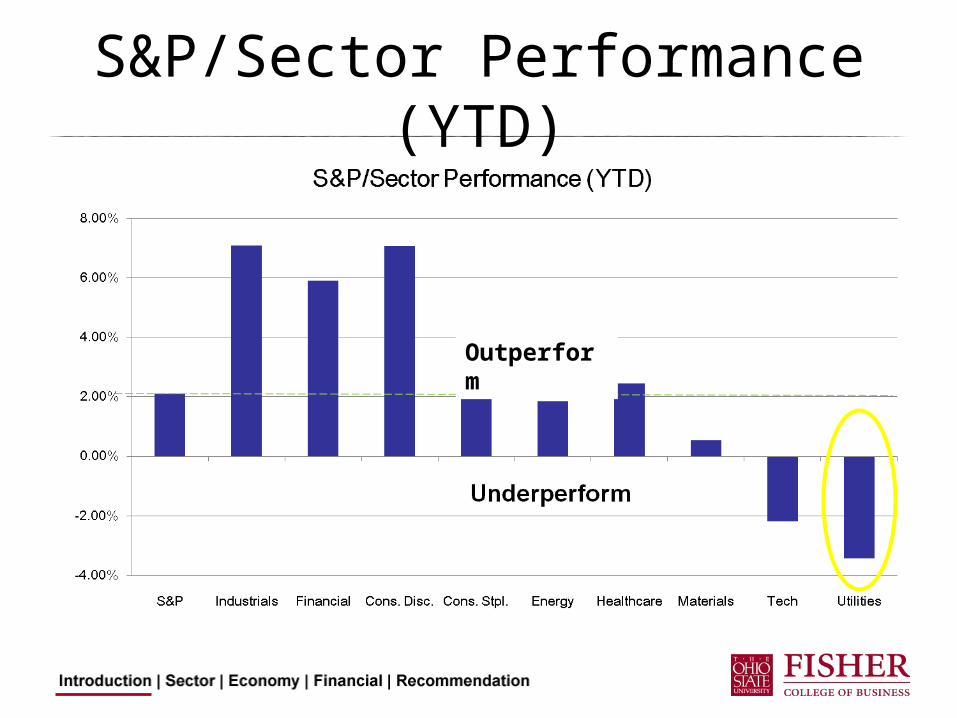

S&P/Sector Performance (YTD)

Outperform

Exelon Corp (EXC)

• Exelon is a diversified utility company which operates through three subsidiaries: Generation, PECO, and ComEd• Generation consists of owned and

contracted electric generating facilities with 24,850 MW of capacity, of which 17,009 MW (68.5%) is nuclear

• ComEd delivers energy to retail customers in northern Illinois

Exelon Corp (EXC)

Absolute Valuation High Low Median Current Target

MultipleTarget

E,S,B/ShareTarget Price

P/Forward E 20.8 9.3 13.0 12.1 12.1 3.77 45.6

P/S 3.3 1.0 1.8 1.7 1.8 26.26 47.3

P/B 6.8 1.8 3.1 2.4 2.5 18.96 47.4

P/EBITDA 9.5 2.8 5.8 3.9 5.8 11.76 68.1

P/CF 13.6 4.5 8.2 5.6 7.5 8.05 60.4

Multiples Valuation:

Exelon Corp (EXC)Year 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Revenue 17,664 18,548 19,475 20,449 21,471 22,545 23,672 24,856 26,098 27,403 28,773 % Growth 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

Operating Income 5,028 5,343 5,649 5,930 6,227 6,538 6,865 7,208 7,569 7,947 8,344 Operating Margin 28.5% 28.8% 29.0% 29.0% 29.0% 29.0% 29.0% 29.0% 29.0% 29.0% 29.0%

Interest Income (768) (807) (847) (890) (934) (981) (1,030) (1,081) (1,135) (1,192) (1,252) Interest % of Sales -4.4% -4.4% -4.4% -4.4% -4.4% -4.4% -4.4% -4.4% -4.4% -4.4% -4.4%

Taxes 1,651 1,758 1,861 1,953 2,051 2,153 2,261 2,374 2,493 2,618 2,748 Tax Rate 38.8% 38.8% 38.8% 38.8% 38.8% 38.8% 38.8% 38.8% 38.8% 38.8% 38.8%

Net Income 2,609 2,778 2,941 3,087 3,242 3,404 3,574 3,753 3,940 4,137 4,344 % Growth 6.5% 5.9% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

Add Depreciation/Amort 1,811 1,855 1,947 2,045 2,147 2,254 2,367 2,486 2,610 2,740 2,877 % of Sales 10.3% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%Plus/(minus) Changes WC 65 211 221 225 236 248 260 273 287 301 317 % of Sales 0.4% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1%Subtract Cap Ex 3,356 3,431 3,505 3,579 3,650 3,720 3,788 3,853 3,915 3,973 4,028 Capex % of sales 19.0% 18.5% 18.0% 17.5% 17.0% 16.5% 16.0% 15.5% 15.0% 14.5% 14.0% Free Cash Flow 998 991 1,162 1,329 1,503 1,690 1,893 2,112 2,348 2,603 2,877 % Growth -0.7% 17.2% 14.4% 13.1% 12.5% 12.0% 11.6% 11.2% 10.8% 10.5%

NPV of Cash Flows 10,952 34%

NPV of terminal value 20,861 66%

Terminal EV/EBIT

DA 5.4 Terminal

Value 49,385 Projected Equity Value 31,813 100%

Free Cash Flow Yield 3.31%Terminal

P/E 11.4

Free Cash Yield 5.83%

Shares Outstanding 662

Current Price $ 45.50 Implied equity value/share $ 48.06 Upside/(Downside) to DCF 5.6%

Terminal Discount Rate: 9.0%

Terminal FCF Growth: 3.0%

Exelon Corp (EXC)

• Valuation• Current Price:

$45.50• Target Price: $48.06• Upside: 5.6%• Dividend Yield:

$2.10 / 4.6%• $30.1 Billion• Recommendation:

Sell 100%

Sensitivity Analysis:

Public Service Enterprise Group (PEG)

• PEG is a diversified utility company with operations primarily in the Northeastern and Mid-Atlantic United States

• 3 Primary Businesses (% of total revenue):• Power (74.7%) - Selling electricity, natural gas,

capacity, and emissions credits under contract or on spot market

• PSE&G (20.4%) - Provides electric transmission and electric and gas distribution to residential, commercial and industrial customers in New Jersey. Currently increasing level of renewable generation

• Energy Holdings (4.5%) - Manages leveraged lease investments and operates domestic generation projects. Also pursuing solar and other renewable generation projects.

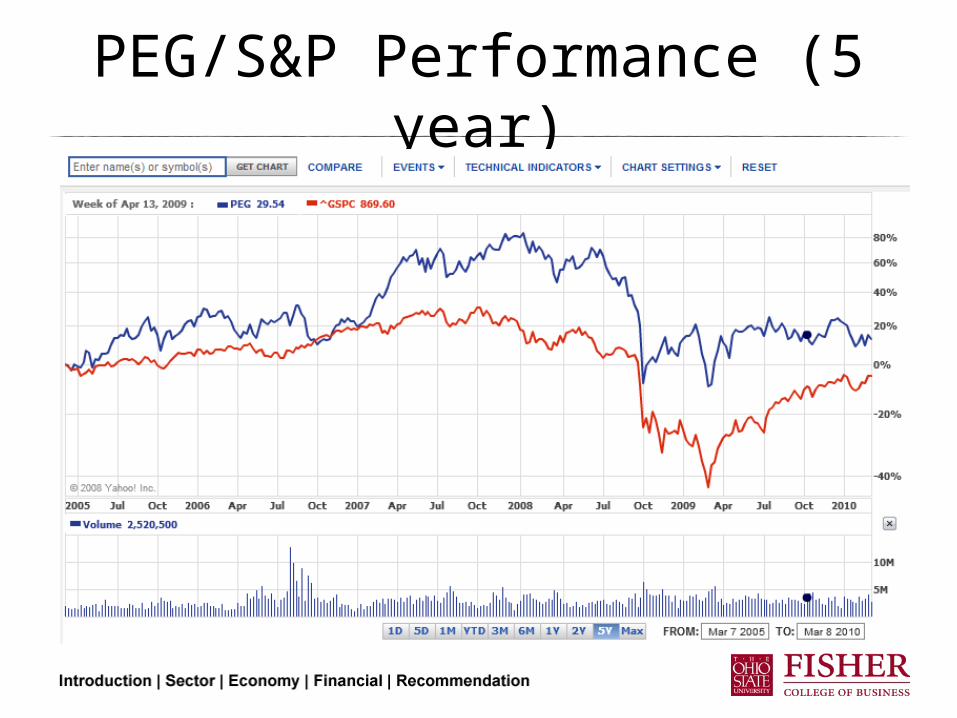

PEG/S&P Performance (5 year)

Relative Multiple ValuationRelative to Industry

High Low Median Current

P/Trailing E 2.6 .12 .95 .81P/Forward E 1.5 .44 .91 .83P/B 3.4 .3 1.4 1.2P/S 19.4 .6 1.6 1.2P/CF 1.7 .2 1.2 1.0P/EBITDA 1.58 .92 1.32 .94

Relative to S&P 500

High Low Median Current

P/Trailing E 1.4 .31 .66 .57P/Forward E 1.3 .32 .67 .67P/B 1.5 .3 .8 .8P/S 1.6 .4 .9 1.1P/CF 1.2 .3 .7 .6P/EBITDA 1.24 .54 .93 .59

Absolute ValuationAbsolute Valuation

High Low Median

Current #Your Target Multiple

*Your Target E, S, B, etc/Share

Your Target Price (F x G)

A. B. C. D. E. F. G. H.

P/Forward E 19.0 6.8 11.5 9.9 11.5 3.16 36.34

P/S 2.0 .6 1.2 1.3 1.3 30.09 39.12

P/B 3.6 1.4 2.3 1.8 2.2 17.33 38.13

P/EBITDA 8.13 2.41 4.40 3.85 4.5 8.10 36.45

P/CF 12.9 4.3 7.1 6.2 7.0 5.03 35.23

Public Service Enterprise Group Inc. (PEG)

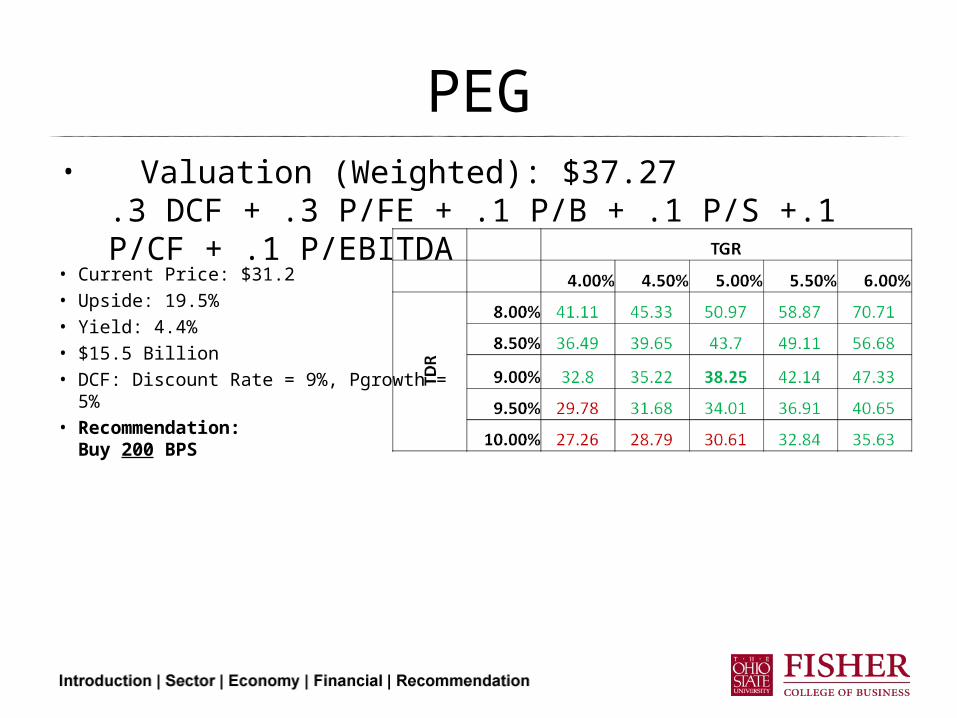

Analyst: Nihar Shah Terminal Discount Rate = 9.0%

3/6/2010 Terminal FCF Growth = 5.0%

(Millions)

Year 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Revenue 15,259 15,717 16,346 17,000 17,680 18,387 19,122 19,887 20,683 21,510 22,370

% Growth 3.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0%

Operating Income 3,392 3,285 3,463 3,655 3,819 3,990 4,169 4,355 4,530 4,711 4,899

Operating Margin 22.2% 20.9% 21.2% 21.5% 21.6% 21.7% 21.8% 21.9% 21.9% 21.9% 21.9%

Interest Income (641) (644) (654) (680) (707) (735) (765) (795) (827) (860) (895)

Interest % of Sales -4.2% -4.1% -4.0% -4.0% -4.0% -4.0% -4.0% -4.0% -4.0% -4.0% -4.0%

Taxes 1,149 1,103 1,173 1,242 1,299 1,359 1,421 1,486 1,546 1,607 1,672

Tax Rate 41.8% 41.8% 41.8% 41.8% 41.8% 41.8% 41.8% 41.8% 41.8% 41.8% 41.8%

Net Income 1,602 1,538 1,636 1,733 1,813 1,896 1,983 2,074 2,157 2,243 2,333

% Growth -4.0% 6.4% 5.9% 4.6% 4.6% 4.6% 4.6% 4.0% 4.0% 4.0%

Add Depreciation/Amort 992 982 981 1,020 1,061 1,103 1,147 1,193 1,241 1,291 1,342

% of Sales 6.5% 6.3% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0%

Plus/(minus) Changes WC 737 116 159 170 177 184 191 199 207 215 224

% of Sales 4.8% 0.7% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

Subtract Cap Ex 1,940 1,680 1,645 1,711 1,779 1,850 1,924 2,001 2,081 2,164 2,251

Capex % of sales 12.7% 10.7% 10.1% 10.1% 10.1% 10.1% 10.1% 10.1% 10.1% 10.1% 10.1%

Free Cash Flow (83) 725 814 872 918 965 1,015 1,067 1,110 1,154 1,200

% Growth -977.1% 12.2% 7.2% 5.2% 5.2% 5.2% 5.1% 4.0% 4.0% 4.0%

NPV of Cash Flows 6,085 31%

NPV of terminal value 13,307 69% Terminal Value 31,503

Projected Equity Value 19,392 100%

Free Cash Flow Yield -0.52% Free Cash Yield 3.81%

Current P/E 9.9 10.3 9.7 Terminal P/E 13.5

Projected P/E 12.1 12.6 11.9

Current EV/EBITDA 5.3 5.5 5.2 Terminal EV/EBITDA 6.2

Projected EV/EBITDA 6.1 6.3 6.0

Shares Outstanding 507

Current Price $ 31.20

Implied equity value/share $ 38.25

Upside/(Downside) to DCF 22.6%

PEG

• Current Price: $31.2• Upside: 19.5%• Yield: 4.4%• $15.5 Billion• DCF: Discount Rate = 9%, Pgrowth = 5%• Recommendation:

Buy 200 BPS

• Valuation (Weighted): $37.27.3 DCF + .3 P/FE + .1 P/B + .1 P/S +.1 P/CF + .1 P/EBITDA

AEP

• Current Price: $34.21• Valuation (Weighted): $36.17

– .3 DCF + .3 P/FE + .1 P/B + .1 P/S +.1 P/CF + .1 P/EBITDA

• Upside: 7.1%• Yield: 4.9%

Questions?

Old Slides

Utilities – Catalysts/Risks

• Catalysts– Rate Regulation Increase– Weather Patterns– Improvement in Economy– Green Policy (Nuclear/Water)

• Risks– Rate Regulation Neutral/Decrease– Inconsistent or over-demand– Commodity Prices– Green Policy (Electric/Diversified/Gas)

Largest Companies in (SPUT)

Company Market Cap Sales (in M) EPS 5 Yr Growth LT Growth ROE Yield ROE + Yield

SPUT 355.0 B N/A N/A 8.00% 5.00% 12.30% 4.60% 16.90%

EXC 29.5 B 17.32 B 4.09 10.00% 0.00% 22.90% 4.70% 27.60%

SO 25.9 B 15.74 B 2.07 3.00% 4.00% 13.00% 5.40% 18.40%

NGG 24.7 B 24.13 B 3.85 2.00% 7.00% 25.20% 4.60% 32.90%

DUK 21.40 B 12.73 B .83 -8.00% 4.00% 7.40% 5.80% 13.20%

FPL 19.40 B 15.65 B 3.97 12.00% 7.00% 13.60% 4.30% 17.90%

AEP 16.10 B 13.44 B 2.88 5.00% 4.00% 12.00% 4.90% 16.90%

FE 12.10 B 12.97 B 3.29 11.00% 3.00% 13.60% 5.50% 19.10%

EIX 11.00 B 12.54 B 2.59 10.00% 3.00% 11.30% 3.70% 15.00%

OKE 4.60 B 10.23 B 2.65 3.00% 10.00% 14.40% 4.00% 18.40%

Business Analysis

Electric

Water GasForeignDiversified

Industry vs Sector Performance

Sector vs S&P Performance

Historical Prices

0

50

100

150

200

250

Jan-00

May-00

Sep-00

Jan-01

May-01

Sep-01

Jan-02

May-02

Sep-02

Jan-03

May-03

Sep-03

Jan-04

May-04

Sep-04

Jan-05

May-05

Sep-05

Jan-06

May-06

Sep-06

Jan-07

May-07

Sep-07

Jan-08

May-08

Sep-08

Jan-09

May-09

Sep-09

Jan-10

Sector S&P

Correlation: 80.93%

Outperform Outperform

Economic Analysis

Economic AnalysisUnemployment vs GDP

12,200

12,400

12,600

12,800

13,000

13,200

13,400

13,600

Jan-04 May-05 Oct-06 Feb-08 Jul-09 Nov-10

GD

P

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Une

mpl

oym

ent

Real Gross Domestic Product Unemployment Rate

Economic Analysis

Change in GDP vs Sector Price

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

Aug-87 May-90 Jan-93 Oct-95 Jul-98 Apr-01 Jan-04 Oct-06 Jul-09 Apr-12

% C

hang

e in

GD

P

-30

-20

-10

0

10

20

30

40

% C

hang

e in

Sec

tor

Real Gross Domestic Product EXC.S

Forecast: GDP will very slowly increase over the short term

Economic AnalysisRelative Strength of Utility Sector vs S&P 500

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Aug-87 May-90 Jan-93 Oct-95 Jul-98 Apr-01 Jan-04 Oct-06 Jul-09 Apr-12

S&P 500 Rel Str

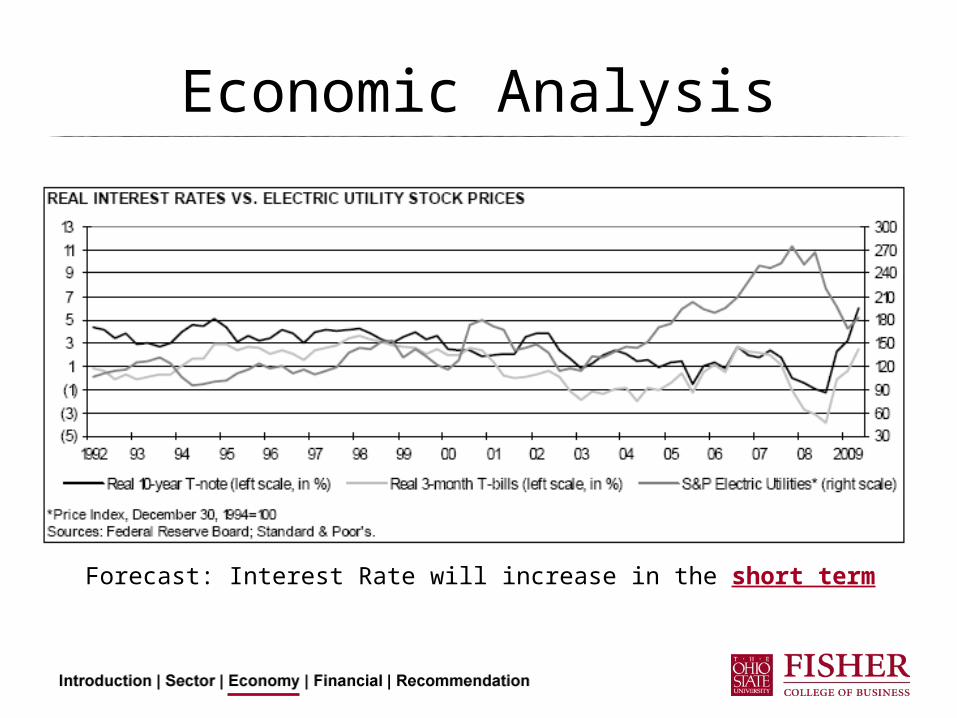

Economic Analysis

Forecast: Interest Rate will increase in the short term

Economic Analysis

EXC.S vs OIL (USO)

R2 = 0.4733

0

20

40

60

80

100

120

100 120 140 160 180 200 220 240

Utility Sector Price (EXC.S)

Oil

ETF

Pric

e (U

SO)

Economic Analysis

Economic Analysis

EXC.S vs Natural Gas (UNG)

R2 = 0.7701

010203040506070

100 120 140 160 180 200 220 240

Utility Sector Price (EXC.S)

Nat

ural

Gas

ETF

Pri

ce

(UN

G)

Forecast: Natural Gas Price will stay relatively constant in the short term

Economic Analysis

EXC.S vs Coal (KOL)

R2 = 0.7565

010203040506070

100 120 140 160 180 200 220

Utility Sector Price (EXC.S)

Coal

EFT

Pri

ce (K

OL)

Economic Analysis

Forecast: Potential for long term growth

Regulation• State commissions are responsible for determining utilities’ proper rate bases and allowable

operating expenses. Individual states’ rulings often differ with regard to these determinations. They also differ in allowed accounting treatments for depreciation accruals and investment tax credits. Although rulings are often presumed to be based solely on the public interest, commissions actually seek to provide a balance between investor and consumer interests.

Green Policy (Update)• On June 26, 2009, the House of Representatives passed, by a

narrow 217–205 margin, its version of a new energy bill, H.R. 2454. Included in the bill, called the American Clean Energy and Security Act, 2005–2050, were provisions for a cap-and-trade system that would incrementally reduce GHG emissions, beginning with a cap on 2012 emissions that is 3% below 2005 levels. The bill, whose principal sponsor was Henry Waxman (D.–California), also included a requirement that utilities get 15% of their electricity from renewable energy sources and, through increasing their energy efficiencies, reduce their electricity use 5% by 2020. Individual states, however, would be allowed to vary these two percentages as long as the total came to 20%.

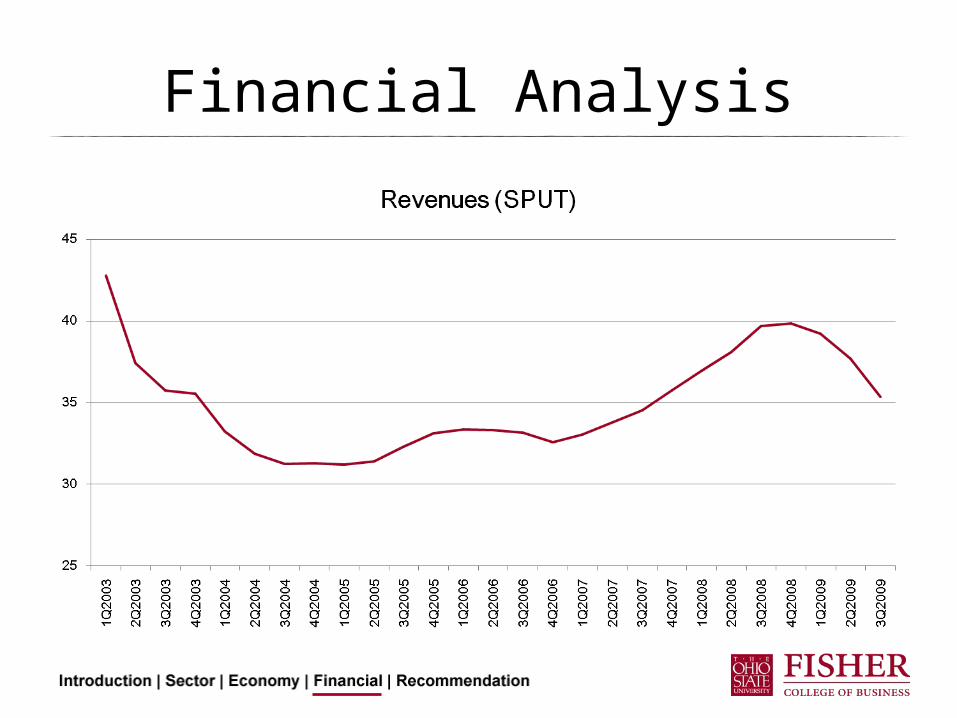

Financial Analysis

Sector

Financial Analysis

Margins

Net ProfitN/A

Summary

Analysis Conclusions View

Business Mature industry, cyclical in nature Neutral

Economic Expect slow growth Slightly Negative

Financial Declining Revenue, stable profit margin stable ROE, and declining Net Profit Margin.

Negative

Valuation Sector seems to be trading at a slight discount.

Slightly positive

Overall: Slightly negative for short term

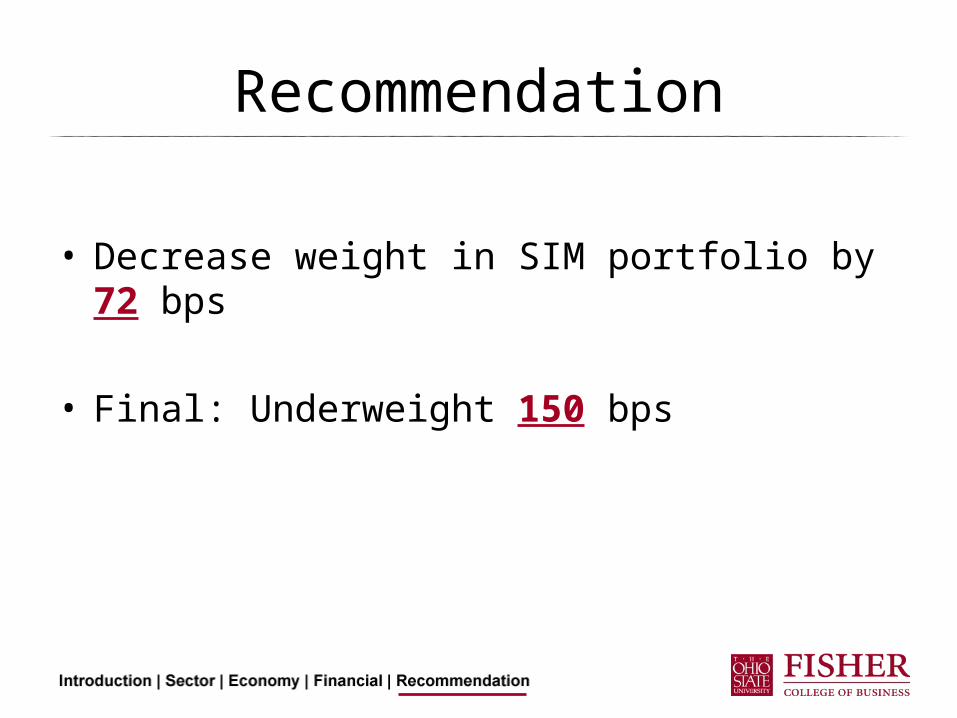

Recommendation

• Decrease weight in SIM portfolio by 72 bps

• Final: Underweight 150 bps

Questions