UNDERSTANDING AND

USING FINANCIAL

STATEMENTS

Presented by

SCORE®

Indianapolis Chapter 1

THE BUSINESS

“REPORT CARDS”

Financial Statements are the report cards

of a business. They portray the activities of a

business to third parties, such as investors,

banks and creditors.

Most important of all, however, these

Report Cards are the most significant tools

that a business owner has available to

successfully manage his or her business. 2

Why Learn About Financials?

Two very good reasons:

1. To help you better understand and

manage your business activities, and

2. To provide those who have a financial

stake in your business (partners, other

owners or banks) vital information about

your business problems or achievements

3

WHAT ARE

FINANCIAL STATEMENTS?

There are four major financial

statements:

• Income Statement (or Profit & Loss)

• Balance Sheet

• Statement of Cash Flow

● Statement of Funds Flow

4

INCOME STATEMENT

A statement, prepared for a specific period of time (month/year),

that lists:

• Your company’s SALES or REVENUE

• The COST OF SALES (cost of the products you sell or the

cost of materials, labor, and overhead if your business is

contracting or a service organization)

• The EXPENSES incurred to generate the sales and pay for

administrative costs

• The NET INCOME (or loss), for the period, which equals

sales less cost of sales and expenses)

5

A SAMPLE

INCOME STATEMENT (each item on this statement is the balance in an account or a

group of accounts or a total)

Sales $500

Cost of sales:

Materials 50

Labor 75

Overhead 25

Total Cost of Sales 150

Gross Profit 350

Operating Expenses 150

Depreciation expense 50

Total expenses 200

Earnings before tax $150 6

BALANCE SHEET

A statement, prepared as of a specific date, that lists:

• Your company’s ASSETS (these are things that your

company OWNS),

• Your company’s LIABILITIES (these are amounts that your

company OWES),

• Your company’s NET WORTH or Owners’ Equity, (this is the

EXCESS of the value of the company’s assets over the

company’s liabilities)

7

THE FINANCIAL EQUATION

ASSETS = LIABILITIES + EQUITY

What your business OWNS =

What your business OWES + Equity

STATED ANOTHER WAY –

ASSETS - LIABILITIES = EQUITY

What your business OWNS minus

what your business OWES = Equity

8

EXAMPLES OF BALANCE

SHEET ACCOUNTS

ASSETS - those things your Company OWNS:

(Cash, Accounts Receivable, Inventory and Equipment)

LIABILITIES - the amounts your Company OWES:

(Accounts Payable, Credit Card Balances and Bank Loans)

EQUITY - the amount the Company OWES the owners:

(including YOU, for their investment and their share of the

earnings of the business)

9

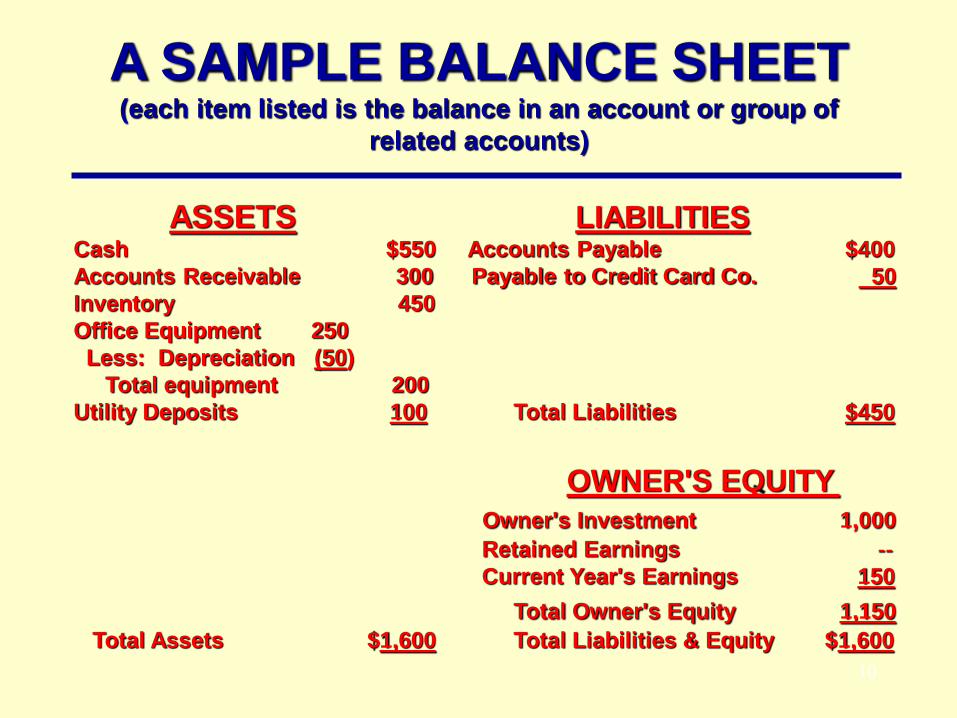

A SAMPLE BALANCE SHEET (each item listed is the balance in an account or group of

related accounts)

ASSETS LIABILITIES Cash $550 Accounts Payable $400

Accounts Receivable 300 Payable to Credit Card Co. 50

Inventory 450

Office Equipment 250

Less: Depreciation (50)

Total equipment 200

Utility Deposits 100 Total Liabilities $450

OWNER'S EQUITY

Owner's Investment 1,000

Retained Earnings --

Current Year's Earnings 150

Total Owner's Equity 1,150

Total Assets $1,600 Total Liabilities & Equity $1,600

10

CASH FLOW STATEMENT

A statement, prepared for a specific period of time

(month/year), that lists:

• Your company’s CASH RECEIPTS, such as cash sales,

payments from customers, loan proceeds and others

• CASH PAYMENTS by your company to pay for inventory,

expenses, wages and more

• The CASH BALANCES at the beginning and ending of

the period involved

11

A SAMPLE CASH FLOW

STATEMENT

Beginning Cash $ 0

Receipts:

Owner Investment 1,000

Cash Sales 200

Total Receipts 1200

Payments:

Make Utility Deposit 100

Payment of Expenses 150

Payment on Payables 400

Total Payments 650

Cash Flow for the Period 550

Ending Cash $ 550

(Each item listed is a type of transaction, not an account) 12

STATEMENT OF FUNDS FLOW

A statement, prepared for a specific period of time (month/year),

that lists:

• Funds your company generates from operations (net income

with non-cash items, like depreciation, added back)

• Other sources of funds generated by the company through

(increases in bank loans, payables, added owner

investment, or decreases in receivables, inventory or

other assets)

• Uses of funds (to increase inventory, receivables or other

assets and to decrease payables, loans or other liabilities)

13

A SAMPLE STATEMENT OF

FUNDS FLOW

Beginning Cash $ 0

Funds From:

Operations $150

Add back: non-cash items (depr) 50 200

Owner’s investment 1,000

Increase in accounts payable 400

Increase in credit card payables 50

Total funds generated 1,650

Funds Applied to:

Increase in accounts receivable 300

Increase in inventory 450

Purchase of office equipment 250

Make Utility deposits 100

Total funds applied 1,100

Ending Cash $ 550 14

ALL OF THESE STATEMENTS ARE

GENERATED BY:

An Accounting System!

The question is HOW?

15

There are Two Types of

Accounting Systems:

Cash Basis & Accrual Basis

Cash Basis Accounting is like your checkbook:

No transaction is recorded unless

cash is involved – Very Simple

. . . No sale is recorded until cash is

received

. . . No expense is recorded until the

credit card is paid or a check is issued

16

There are Two Types of

Accounting Systems:

Cash Basis & Accrual Basis

Accrual Basis Accounting records each transaction

as it occurs -

. . . Sales are recorded when the goods or

services are delivered to the customer

. . . Expenses are recorded when they are

incurred and a liability is created

17

ADVANTAGE:

Accrual Accounting

No surprises! Everything is accounted for

when it happens!

Example: Have you ever been surprised (and

dismayed) when you received your credit card

billing?

The credit card charges are liabilities which, in

accrual accounting, would have already been

recorded when the card was used.

18

How does accrual basis accounting

take us to this Balance Sheet?

ASSETS LIABILITIES

Cash $550 Accounts Payable $400

Accounts Receivable 300 Payable to Credit Card Co. 50

Inventory 450

Office Equipment 250

Less – Depreciation (50) 200

Utility Deposits 100 Total Liabilities $400

OWNER'S EQUITY

Owner's Investment 1,000

Retained Earnings --

Current Year's Earnings 150

Total Owner's Equity 1,150

Total Assets $1,600 Total Liabilities & Equity $1,600 19

USING YOUR

FINANCIAL STATEMENTS

Understanding How Financial Statements

are developed is just the beginning:

You must learn to use them to successfully to . . .

MANAGE YOUR BUSINESS!

20

Tools for Analysis

21

The following items make analysis

possible:

• Annual Budgets

• Historical Comparisons

• Ratios and Percentages

COMPARE RESULTS WITH BUDGET

Use financial statements to compare

actual results with planned (budgeted) results:

• Prepare a good Budget with projected financial results

• Use Financial Statements that compare the actual with

budgeted results

• Determine the cause of any deviations from Budget

• Take Action to correct any problem areas and to

promote positive results (or . . . If the budget is

wrong, fix it!)

22

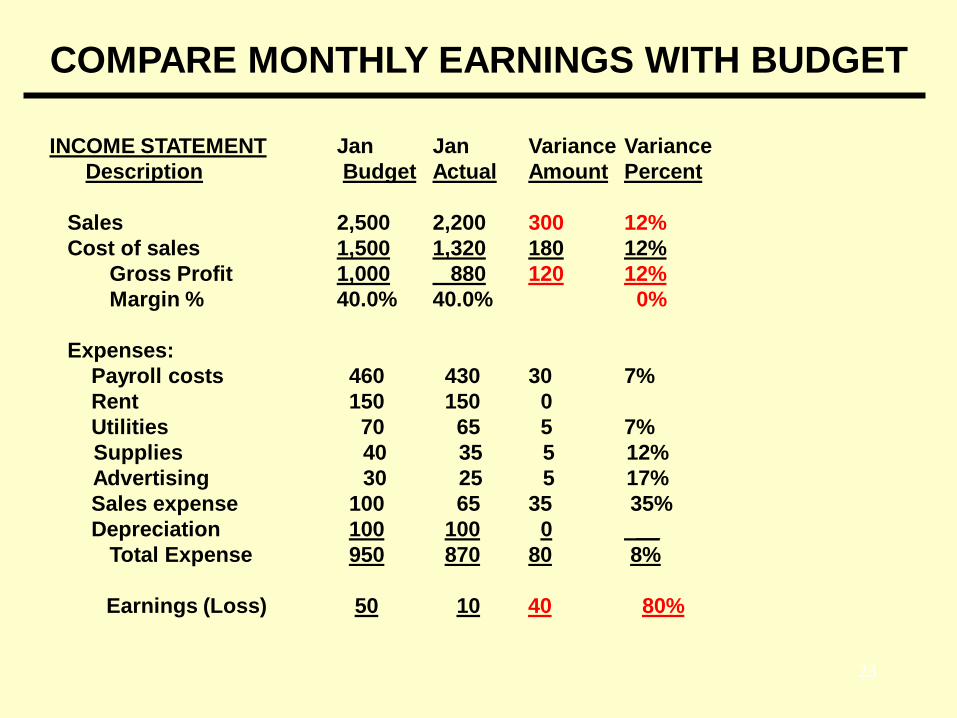

COMPARE MONTHLY EARNINGS WITH BUDGET

INCOME STATEMENT Jan Jan Variance Variance

Description Budget Actual Amount Percent

Sales 2,500 2,200 300 12%

Cost of sales 1,500 1,320 180 12%

Gross Profit 1,000 880 120 12%

Margin % 40.0% 40.0% 0%

Expenses:

Payroll costs 460 430 30 7%

Rent 150 150 0

Utilities 70 65 5 7%

Supplies 40 35 5 12%

Advertising 30 25 5 17%

Sales expense 100 65 35 35%

Depreciation 100 100 0 __

Total Expense 950 870 80 8%

Earnings (Loss) 50 10 40 80%

23

DETERMINE THE CAUSE OF VARIANCES

• Are deviations due to uncontrollable external factors and, if

so, what were they?

• Are deviations due to errors in accounting or a bad budget,

and if so, in what respect?

• Are deviations due to poor sales effort, a failure to control

expenses or inefficiency in the production or delivery of

product/service? And if so, what problems occurred and

how can they be avoided in the future?

Note: Some companies prepare a Variance Report

to focus on, and explain, deviations from Plan.

24

MANAGING GROSS MARGIN

Sales $1,000

Cost of sales 600

Gross profit $400 40%

Gross profit is the dollar value of Sales minus Cost of

Sales. Gross margin is the percentage relationship of

Gross Profit to the Sales dollars.

Gross Margin = $400 divided by $1,000 = 40%

25

MANAGING GROSS MARGIN

Because Gross Margin relates to the price of your

product and the cost of supplying that product, to

improve your gross margin, you must:

. . . Increase the sales price of your product or

service, or

. . . Lower the cost of your product or service

. . . Or Both!

Note: Because the operating expenses of most companies

are relatively stable, the ability to increase profitability

lies with improving the company’s gross margin.

26

MANAGING GROSS MARGIN

Price your product or service at the HIGHEST PRICE THE

MARKET WILL BEAR! (check your competitors’ prices), then

examine your costs.

If the gross margin is sufficient to allow a satisfactory gross

margin and “bottom line” profit, it is priced OK.

If not, either reduce the cost to create a satisfactory

margin and resulting profit, or

. . . DROP THE PRODUCT FROM YOUR LINE!

27

COMPARE YOUR MONTHLY BALANCE SHEET TO PLAN

BALANCE SHEET Budget Jan Feb Mar

Assets

Cash 250 250 200 430

Accounts Receivable 550 560 700 675

Inventory 800 700 1000 1100

Equipment & Furniture 1000 1000 1000 1000

Utility Deposits 200 200 200 200

Total Assets 2800 2710 3100 3405

Liabilities

Accounts Payable 400 450 975 1100

Payable to Credit Card Co. 700 700 550 610

Total Liabilities 1100 1150 1525 1710

Owner's Equity

Owner's Investment 1000 1000 1000 1000

Retained Earnings 550 550 550 550

Current Year Earnings* 150 10 25 145

Total Owner's Equity 1700 1560 1575 1695

Total Liabilities & Equity 2800 2710 3100 3405

*Assumes earnings of $50 per month. Plan increases $50 every month. 28

COMPARE YOUR MONTHLY

BALANCE SHEET TO BUDGET

In comparing the Balance Sheet accounts to Plan, the principal

deviations were:

• Increase in Receivables: Was this due to increased sales

or failure to follow up on collections?

• Increase in Inventory: Was this due to poor inventory

management, a bad plan or was it needed to support

future expected sales?

Note: The answers to these questions must be studied and

appropriate action taken to avoid further deviations that

could be detrimental to profitability.

29

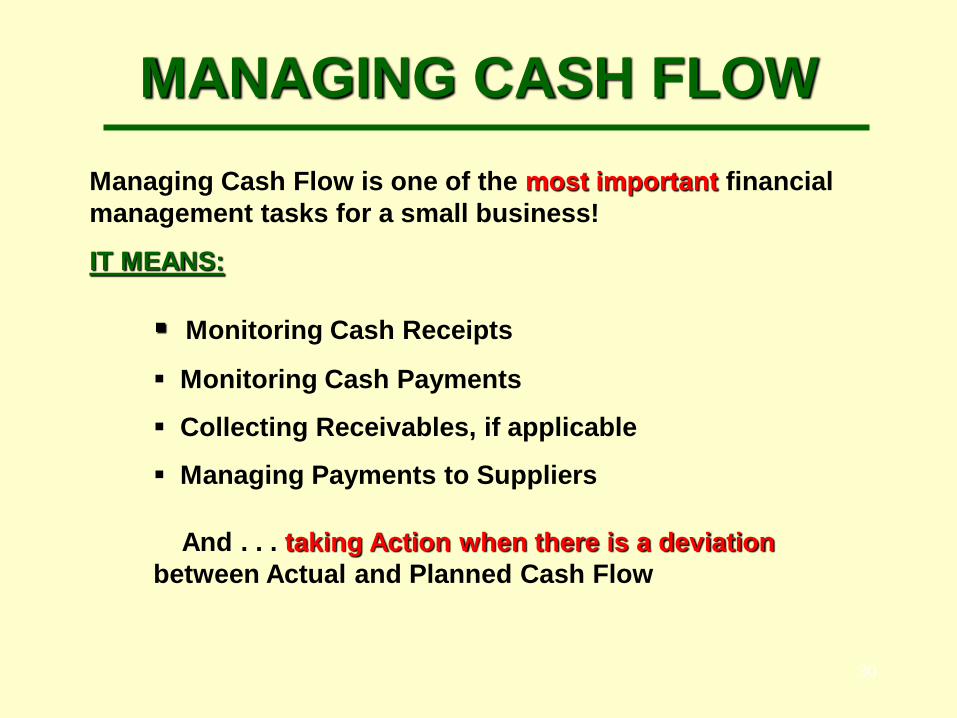

MANAGING CASH FLOW

Managing Cash Flow is one of the most important financial

management tasks for a small business!

IT MEANS:

Monitoring Cash Receipts

Monitoring Cash Payments

Collecting Receivables, if applicable

Managing Payments to Suppliers

And . . . taking Action when there is a deviation

between Actual and Planned Cash Flow

30

FORECAST YOUR CASH NEEDS

1. Estimate your Cash Sales by week for the next four weeks

2. Review you Accounts Receivable Aging and list the

amounts that you expect to collect by week, for the next

four weeks.

3. List any other sources of Cash that you expect to receive,

by week, for the next four weeks. (Bank loan, refunds, etc.)

FORECAST CASH RECEIPTS:

FORECAST CASH DISBURSEMENTS:

1. Review your Accounts Payable detail aging and total the

amounts you must pay, by week, for the next four weeks.

2. List any other payments you must make, by week, for the

next four weeks. (Payroll, loan payments, taxes, rent,

insurance, and other costs) 31

PREPARE A CASH FORECAST

CASH FORECAST: WEEK 1 WEEK 2 WEEK 3 WEEK 4

Cash Receipts –

Cash sales 300 250 450 250

Receivables paid 220 150 300 270

Other receipts 0 20 100 0

Totals 520 420 850 520

Cash Disbursements –

Pay payables 350 400 750 500

Tax payments 160 0 0 0

Loan payments 0 0 150 0

Totals 510 400 900 500

Cash Over (Short) - 10 20 (50) 20

32

ADDRESS PROBLEM AREAS

1. Increase receipts – higher cash sales, more collections

of accounts receivable or money from some other

source.

2. Decrease disbursements – contact a vendor and ask for

a one week delay in payment or visit with your bank and

ask for a few days leeway in making the loan payment.

In short – you must deal with the problem but . . .

By using the Cash Forecast properly you have the

time needed to resolve the issue!

WEEK 3 IS A PROBLEM AREA! YOU MUST:

33

IMPROVE COLLECTIONS

1. If the account becomes 10 days past due, call the

customer to determine if there is a problem with quality,

service or billing . . . and resolve the problem!

REMEMBER - TIME IS CRITICAL

DO NOT DELAY!

3. If the customer simply cannot pay, you can either -

• Work with the customer on a payment plan

• Turn account over to a collection agency

• Consider Small Claims Court for small amounts

2. Get a payment commitment from the customer and

then follow up to assure he meets the commitment.

34

MONITORING PAYABLES

If it is clear that you will not be able to meet a

payment when due, call the vendor and ask for

his patience. Give him a date of payment that

you are SURE you can meet . . . then MEET IT!

Weekly Payables Reports to help you monitor

payables are available in QuickBooks® and in

Peachtree Accounting®.

35

MANAGING TAX LIABILITIES

Some of the most critical liabilities are

taxes due to local, state and Federal taxing

authorities. You must pay these obligations on

time and in the proper amount.

The penalties for failure are significant!

Some tax liabilities are payable in future months.

Be sure to maintain sufficient funds to make the

future payments.

36

Importance of the

Banking Relationship

The importance of a good banking relationship is

illustrated by your Cash Flow Forecast. If there is a

shortfall in cash flow that cannot be avoided, it can be

covered by using a Bank Loan or a “Revolving Line of

Credit” which allows the amount of the loan due the

Bank to fluctuate.

Absent this Banking relationship, adjustments

would have to be made in the payments to Vendors.

The important point here is:

Don’t be surprised. Anticipate the needs!

37

MANAGING FOR SUCCESS!

Your business should provide:

Reasonable compensation for your work

A return on your owner investment

Additional profit used for growth

- - - - - - - - - - - - - - - -

You may be willing to forego some of these provisions

in the short run, but these

should be your long-term objectives!

38

MANAGING FOR SUCCESS!

REASONABLE COMPENSATION:

Your business should enable you to earn the

same amount (or more) that you would pay

someone else for doing the same job (reasonable

compensation)

. . . and generate an -

39

MANAGING FOR SUCCESS!

Adequate Return on Owner Investment:

Whatever you can earn as a reasonable return on

an investment in say, mutual funds . . .

You should expect your business to generate at

least that amount on the investment you have made in

your own business . . . in addition to the payment of a

reasonable wage for the work you are doing!

40

MANAGING FOR SUCCESS!

Profit For Growth:

In addition to a reasonable wage and return

on investment, your business should return an

additional profit to enable its continued growth.

The amount is subjective but relates to the

need to replace aging equipment, provide

additional facilities and conduct research to

provide for continued growth.

41

Concluding Thoughts

1. Price your product or service properly

2. Monitor your costs to achieve desired gross margin

3. Measure results against your Business Plan

4. Maintain high product (or service) quality … it sells!

5. Listen to your customers and respond to their needs

6. Know your competition and why you are better

7. Treasure your people . . . They make the difference!

8. Innovate . . . For better quality and better service!

EIGHT KEYS TO BUSINESS SUCCESS:

42