“Tuning into the BIG Picture”

For

Eastern Ontario Automotive Summit

Belleville, OntarioOctober 19, 2006

Automotive Parts Manufacturers’ Association

The Voice of the Automotive Original Equipment Suppliers

in Canada

• APMA is Canada’s national association representing OEM producers of parts, equipment, tools, supplies and services for the worldwide automotive industry.

• APMA members and their subsidiaries account for 90% of the over $36 (CDN) billion production of automotive parts in Canada. (2005)

Who are we?

To engage in activities that promote the interests of automotive original equipment suppliers in Canada

that enhance the economic welfare of our members and

be the Voice of the Canadian automotive supply industry

Mission Statement

APMA has an 18 person Board of Directors to provide industry focus and direction and to oversee operations of the association as well as standing committees to allow members to exchange information and deal with issues affecting their sector:

•Marketing and Strategic Initiatives Committee

•Human Resource Development Committee

•Energy, Environment and Health & Safety Committee

•Innovation and Technology Committee

•Other Ad hoc Committees as needed

•APMA has 7 full time staff members to administer the association

How APMA operates:

(top 10 issues condense down to 3 main topics)

1. Making Vehicles Safer

Better electronics/user interfaces, better driver and occupant education, better traffic management systems, stronger and easier to process structural materials.

2. Improving Fuel Economy & Reducing Environmental Impact

Lightweight materials, reducing non-renewable resource usage, hybrid powertrains (need better batteries), better transmissions (CVT’s), reducing emissions (need better catalysts).

3. Re-thinking Old Methods

Improving supplier relationships, making assembly more efficient and safer, controlling cost to improve profitability (lower cost materials & logistics as well as design and test methods improvements).

Source: Automotive News - April 11, 2005

Top Auto Industry Issues

91

8377

6167

64

4348 47

2934 34

17 17 18

3134 33

1418 20

0

20

40

60

80

100

Mo

de

l C

ou

nt

GM Ford DCX Toyota Honda R/N Hyundai

2003-05 2006-08 2009-11

Source: CSM Worldwide

Industry

Model Count

2003-05 3592006-08 3852009-11 371

Automakers and suppliers need flexibility to assembly moremodels and parts for different platforms in the same plant

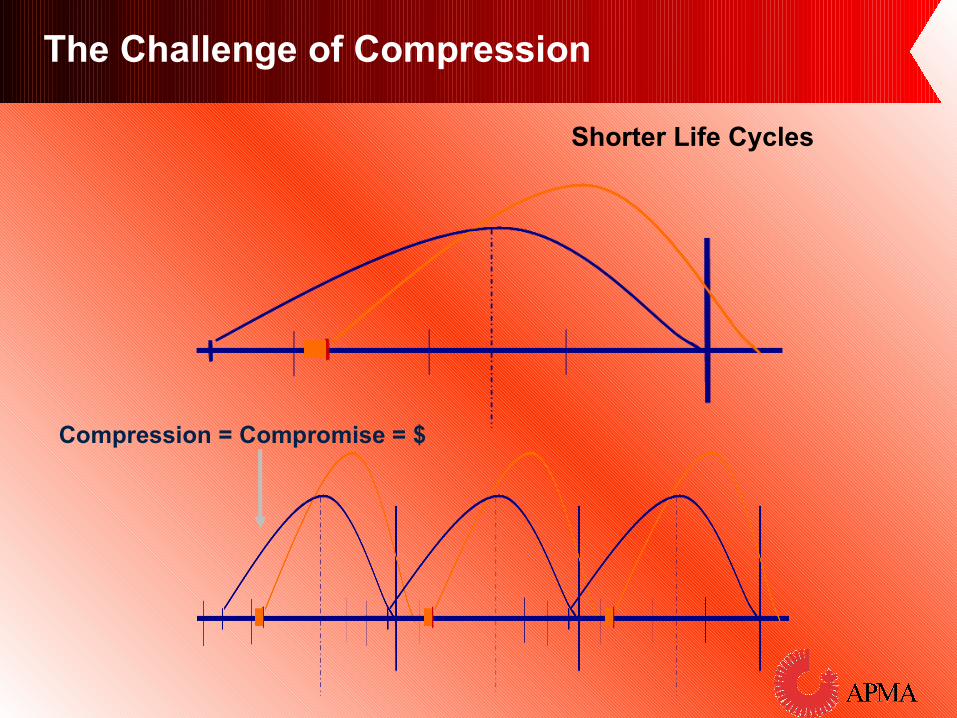

Explosion of New Products

Compression = Compromise = $

Shorter Life Cycles

The Challenge of Compression

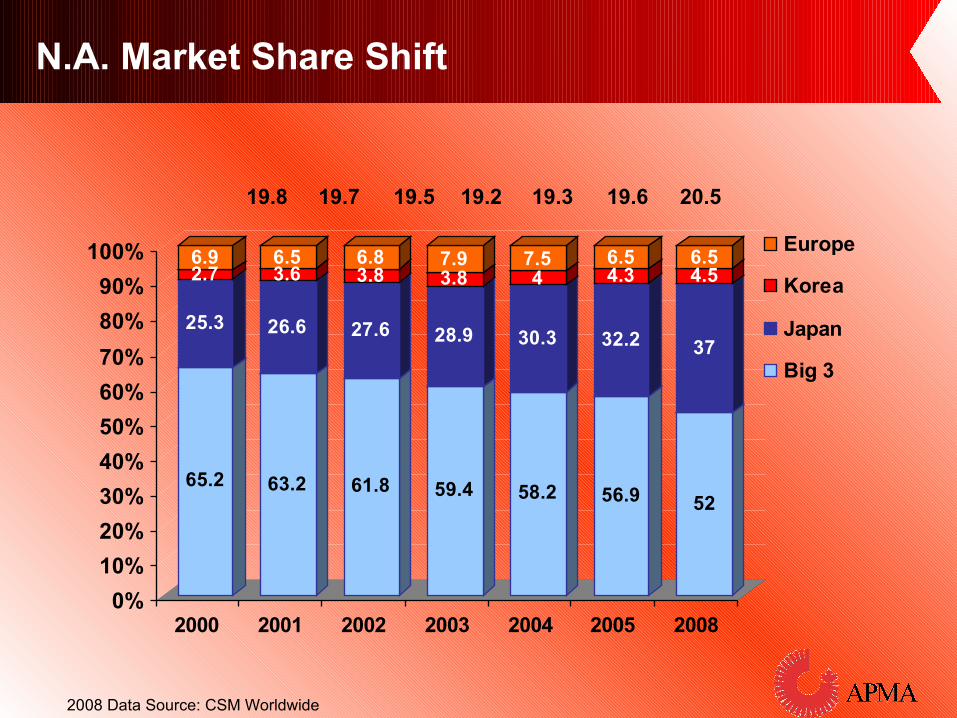

North America

2008 Data Source: CSM Worldwide

65.2

25.3

2.76.9

63.2

26.6

3.66.5

61.8

27.6

3.86.8

59.4

28.9

3.87.9

58.2

30.3

47.5

56.9

32.2

4.36.5

52

37

4.56.5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2008

Europe

Korea

Japan

Big 3

19.7 19.5 19.2 20.519.319.8 19.6

N.A. Market Share Shift

Number of Automotive Suppliers

Based on OESA Projections

Consolidation of Supply Base

Canada

• World’s 8th largest producer of motor vehicles (> 2.6 million units). Ontario produces more vehicles than anywhere else in North America.

• Six OEM’s: 12 active assembly plants (+1 more in 2007) + a number of engine and drivetrain part plants and support facilities. Over $7 billion has been committed to Canada in past two years.

• 3 OEM engineering R&D centres including DaimlerChrysler Canada, General Motors Canada & International Truck & Engine-Navistar.

• Hundreds of suppliers of parts at all tier levels including Magna, Siemens-VDO, Dofasco, Alcan, Dupont, Wescast Ind., Woodbridge, Solectron-Invotronics, NEMAK Aluminum, Ballard Power Systems, General Hydrogen, Stuart Energy Systems, Hydrogenics, Schukra, QSS, Ventra Group, AutoLIV Canada, Ventra, Delphi, Lear Canada.

• Over 500,000 Canadians work in the auto industry - 1/7 jobs and 1/6 in Ontario. Workers here are highly skilled!

• The auto sector generates 12-13% of Canada’s manufacturing gross domestic product and is the largest source of foreign exchange.

Canada’s Automotive Sector

10

12

14

16

18

20

22

24

26

28

30

32

34

36

38

40

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

$ billion

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Canadian Vehicle Production VS. Canadian Automotive Parts Shipments

Canadian Vehicle Production (units)

Canadian Automotive Parts Shipments (CDN $)

Motor Vehicle Assembly Manufacturing vs. Motor Vehicles Parts Manufacturing

0

20000

40000

60000

80000

100000

120000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

AssemblyManufacturing

PartsManufacturing

Statistics Canada

Total Employment

Oshawa

OakvilleBrampton

Alliston

Cambridge

Windsor St. ThomasIngersoll

Canadian Assembly Plant Locations

Woodstock (opening 2008)

Vehicles Key to the North American Market

Canadian Assembly Plants

ASSEMBLER PRODUCTS

CAMI Chevrolet Equinox *Pontiac Torrent

DAIMLER CHRYSLER Chrysler 300 *Dodge Magnum *Dodge Grand Caravan/Chrysler Towne & CountryDodge Charger * **

Chrysler Pacifica *

FORD FreestarCrown Victoria / Grand Marquis / Town Car (2008)

GM Buick AllureChevrolet ImpalaChevrolet Monte CarloChevrolet SilveradoGMC Sierra

Pontiac Grand PrixCamaro (2009)

HONDA Acura CSX * /Honda Civic HatchbackAcura MDX *

Honda Pilot *Honda Ridgeline * **

TOYOTA Toyota CorollaToyota Matrix

Lexus RX 350 HinoRAV 4 (2008)

* Solely Ontario Sourced

** New Vehicle Launch

Lincoln MKX (2007)Ford Edge (2007)Fairlane (2008)

Suzuki XL-7

Auto Part Sites by region

01 Bas St-Laurent (1)

02 Saguenay / Lac St-Jean (3)

03 Capitale Nationale (10)

04 Mauricie (4)

05 Estrie (22)

06 Montréal (38)

12 Chaudière-Appalaches (8)

14 Lanaudière (1)

15 Laurentides (10)

16 Montérégie (28)

17 Centre du Québec (4)

( ) number of companies located in each region

Chicoutimi

Québec

Trois-Rivières

DrummondvilleMontréal Sherbrook

e

Hull

Automotive Parts Manufacturers are mainly located in Ontario and Quebec

Quebec

Ontario

Source: Ontario Ministry of Economic Development and Trade

Source: Québec Ministry of Economic Development, Innovation and Export Trade

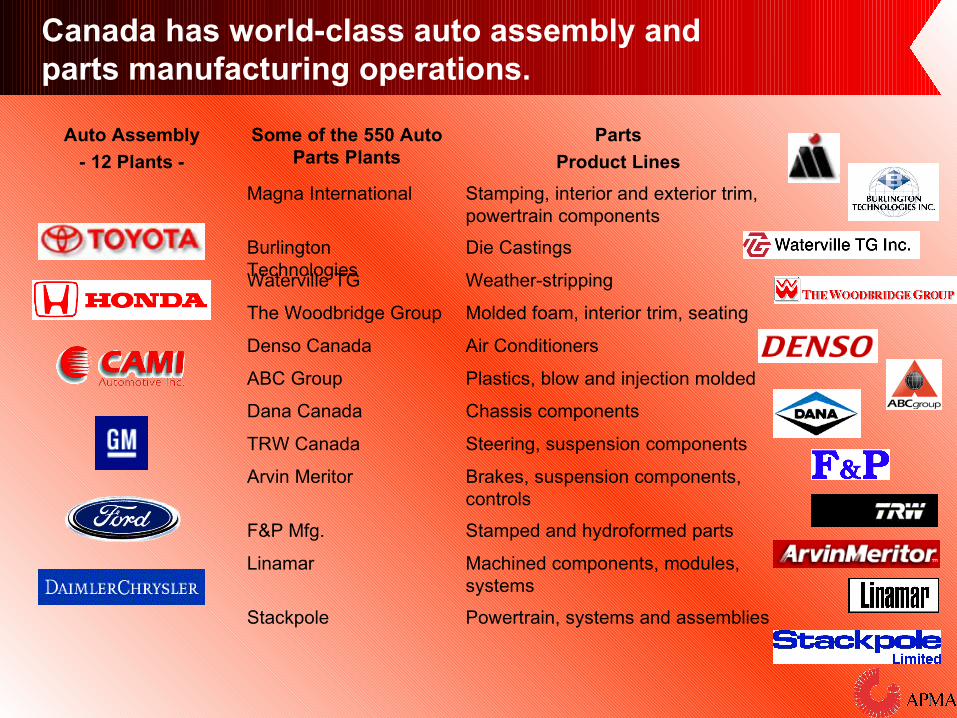

Canada has world-class auto assembly and parts manufacturing operations.

Powertrain, systems and assembliesStackpole

Machined components, modules, systems

Linamar

Stamped and hydroformed partsF&P Mfg.

Brakes, suspension components, controls

Arvin Meritor

Steering, suspension componentsTRW Canada

Chassis componentsDana Canada

Plastics, blow and injection moldedABC Group

Air ConditionersDenso Canada

Molded foam, interior trim, seatingThe Woodbridge Group

Weather-strippingWaterville TG

Die CastingsBurlington Technologies

Stamping, interior and exterior trim, powertrain components

Magna International

Parts

Product Lines

Some of the 550 Auto Parts Plants

Auto Assembly

- 12 Plants -

The Nature of the North American Automotive Industry Trade Flow

• $60.0 B cars and trucks

• $20.3 B parts, engines

Total: $80.3 B

• $23.1 B cars and trucks

• $33.2 B parts, engines

Total: $56.3 B

Source: Statistics Canada

Issues Facing the Automotive Original Equipment Supply Industry in Canada

1. Developing a diversified customer base

2. Securing a fair share of automotive investment in Canada

3. Globalization

4. Seamless passage at the Canada – United States borders

5. Maintaining competitiveness through innovation

1. Developing a diversified customer base

• Market shares continue to change. Suppliers, must aim to have their customer make up mirror that of the new vehicle market shares and be able to quickly respond to:

•Rapid model/vehicle changes

•Lower volumes per platform but more platforms to supply

•Rapid market demand changes – vehicle segment fluctuations

•Global competitive variables-F/X, input costs (raw material, labour, etc.), foreign competition for your business

How does APMA help? Events from 2004 to dateTrade Missions:•Toyota Engineering Centre (Michigan)•Honda, Toyota, Nissan, Tokyo Motor Show (Japan)•Shanghai GM, Volkswagen, Tier I companies (China)•Nissan Technical Centre (Michigan)•Audi, Volkswagen, Hyundai/Kia (Central Europe)•Honda Of America (Ohio)•BMW North America (South Carolina) (3 times)•China (Shanghai, Beijing, Hong Kong)•One-on-One Mission & Tokyo Motor Show (Japan)•Many incoming missions

APMA Events and Publications•APMA’s Annual Conference & Exhibition) for education and networking•Publications to help you stay current

• Investments by foreign governments helped other jurisdictions. We had no new Assembly plants in Canada for last 19 out of 20.

• Our governments’ investments re-leveled the playing field and we have since had good “hits” with virtually all vehicle manufacturers in Canada.

2. Securing a fair share of Automotive Investment in Canada

Results:

•Ford flexible manufacturing - $1 Billion

•GM’s Beacon project - $ 2.5 Billion-Camaro $740 million

•International Truck plant

•Toyota plant 7 – Woodstock for RAV4 - $800 million

•DaimlerChrysler expansions

•Hino (Toyota subsidiary) new truck plant in Woodstock

Over $7 Billion committed resulting from Government’s $1 Billion investment

3. Globalization

1. Not a new concept – for our sector, the AutoPact of 1965 was the start.

2. FTA (late 80s)

3. NAFTA (mid 90s) – big change. High labour content (i.e. wiring harnesses, windshield wiper assemblies) went to Mexico. Benefits of NAFTA are not yet fully realized by the auto industry (non-tariff barriers, harmonization of regulations, border crossing logistics, etc.)

4. Need to find what our core competencies are and develop from there

3. Globalization

1. Asian manufacturing costs are lower – pressure for Asian

pricing in North America

2. More goods will come from Asia and Central Europe-Mexico

may be most at risk!

To be economic and travel 10,000 kilometers, auto parts:

• Cannot be on JIT process

• Must travel well (ie. Difficult to damage)

• Must stack well (high value per container) No value in

shipping air

3. China is hot now for goods, but India will be close behind.

4. Look to China, India, and Central Europe countries for more

competition

4. Seamless passage at the border

• Under NAFTA, goods are to flow freely between countries, but at the border; we know this isn’t always the case.

• Implement Intelligent Technology Systems (ITS) to help control border congestion

• Encourage use of advanced paperless customs and security systems for the pre-clearance for low risk goods

• Can we learn from the European Union, which provides uninterrupted travel (commercial) between 25 countries?

5. Maintaining competitiveness through innovation, research and commercialization

• AUTO21 – Federal Centres of Excellence across the country

* 39 Universities participate

• NRC – Aluminum Technology Centre in Chicoutimi

• Centre for Automotive Research and Education and Automotive Engineering Program at the University of Windsor

• Centre for Automotive Parts Expertise at Georgian College (CAPE)

• University of Windsor/International Truck Diesel Emissions and Manufacturing Process Improvement

Highly qualified skilled trades are essential to a successful auto industry. Advanced research and commercialization of its outputs is equally important. These are our Competitive Advantages!

In summary, the future includes:

• Manufacturers rebalancing and diversifying their customer base – ideal is customer base should mirror customer market share

• Rapid response: Changes/demands will come in many forms

• Low cost country components will be part of the supply chain – use it to your advantage

• Canada must continue to improve trade infrastructure with US – our biggest customer for the foreseeable future

• Canada must continue to remain globally competitive through enhanced R & D, fostering innovation and attracting new investment

• Embracing globalization-not running from it. It provides great opportunities for those willing to reach for it!

and

• Investments in human resources aka “The Human Element”

Gerry Fedchun

(416) 620-4220 Fax (416) 620-9730

The Voice of the Automotive Original Equipment Suppliers

in Canada