Download - The Maharaja Dilemma Presented by Sanjay Pamnani Heidi Pellerano Dhanusha Sivajee Vidhi Tambiah

The Maharaja Dilemma

Presented by

Sanjay PamnaniHeidi Pellerano

Dhanusha SivajeeVidhi Tambiah

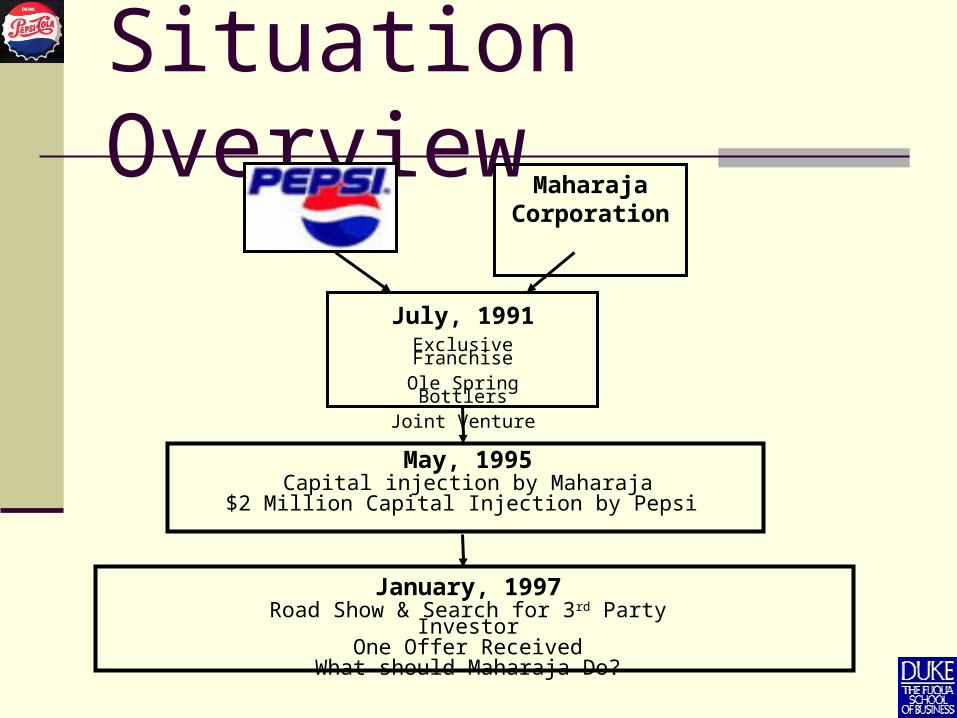

Situation OverviewMaharaja

Corporation

July, 1991Exclusive FranchiseOle Spring Bottlers

Joint Venture

January, 1997Road Show & Search for 3rd Party Investor

One Offer ReceivedWhat should Maharaja Do?

May, 1995 Capital injection by Maharaja

$2 Million Capital Injection by Pepsi

Sri Lanka Population: 18 million Ethnic Make Up:

- Singhalese (Buddhist majority)

- Tamils (Hindu minority)

GDP: 13.6 bn ($US) Main Industries

Agriculture Manufacturing Mining

Raging Ethnic Conflict 11.5 % Inflation Rate Inverted Term Structure Exchange Rate: 56 Rupees to $US

The Players The Maharaja Corporation

Largest Privately-owned conglomerate in Sri Lanka International JV Experience Highly Diversified Business Units

PepsiCo International Lagging behind Coca Cola in International Markets Sri Lankan is a Natural Extension of the Indian Market

Olé Joint Venture Exclusive Bottler & Marketer of the Pepsi, Miranda and 7-Up

Brands Bottling Plant in the Outskirts of Capital City, Colombo Extensive Distributor Network

Ole’s Performance to Date

Capital Structure 1992

Capital Structure 1996

Equity Debt1992 61,147,206 15,286,8011996 208,934,371 112,824,561

80%

20%65%

35%

Cumulative Losses of SL Rs. $268,979,408 (US $ 4.7 million) Marginal Free Cash Flows High Debt Burden – Debt Coverage of close to 2x EBITDA

Competition

Profit (+)

CarbonatedNon-Carbonated

EH

Coke

Pepsi

Profit (-)

Competition

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950,s 1960 to 1978 1978 to 1985 1985 to 1987 1987 to 1991 1992-1995 1995-1997

CCS (Elephant House) Pure Beverages (Coke) The Maharaja (Pepsi)

Decision AlternativesStatus Quo

Terminate JV

Inject New Internal Capital

Bring in New 3rd Party Investor

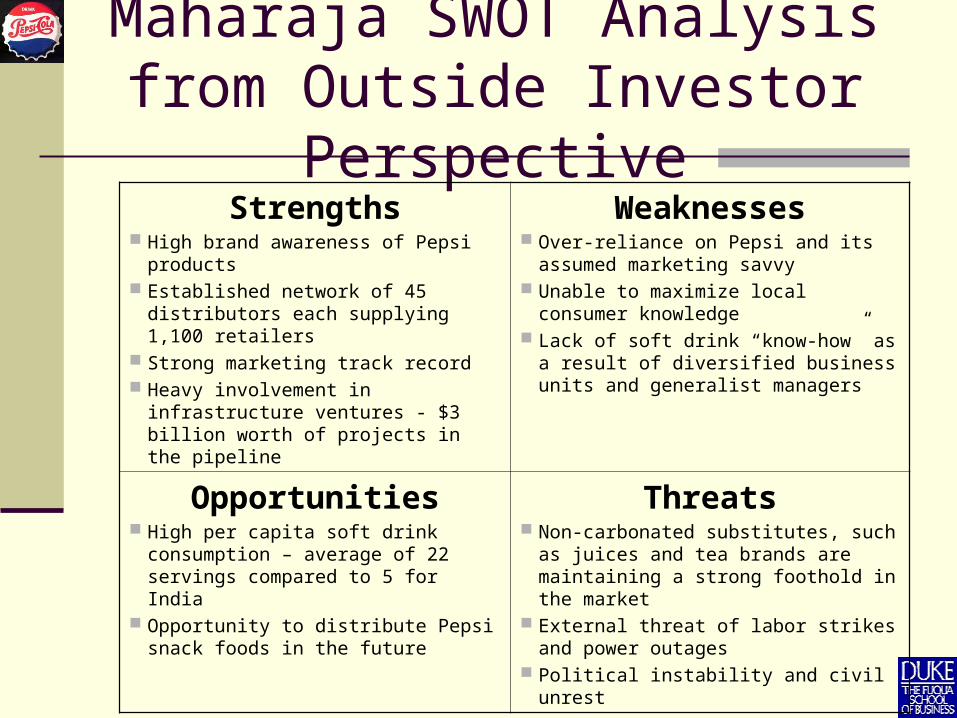

Maharaja SWOT Analysisfrom Outside Investor Perspective

Strengths High brand awareness of Pepsi products Established network of 45 distributors

each supplying 1,100 retailers Strong marketing track record Heavy involvement in infrastructure

ventures - $3 billion worth of projects in the pipeline

Weaknesses Over-reliance on Pepsi and its assumed

marketing savvy Unable to maximize local consumer

knowledge Lack of soft drink “know-how” as a result of

diversified business units and generalist managers

Opportunities High per capita soft drink consumption –

average of 22 servings compared to 5 for India

Opportunity to distribute Pepsi snack foods in the future

Threats Non-carbonated substitutes, such as juices

and tea brands are maintaining a strong foothold in the market

External threat of labor strikes and power outages

Political instability and civil unrest

Risk Analysis from Outside Investor Perspective

High Risk Description Mitigation

Currency Risk

Currency depreciation and high inflation could lead to an increase in input prices for Pepsi Concentrate.

Revenues in Rupees and main in put in dollars

Demand investment and returns in dollar returns

Political Risk

Risk of political unrest in the form regime change and labor strikes.

Bottling plant may be the target of a Tamil separatist attack

Fairly difficult to do as a result of force majeure

Creeping Expropriation

High risk of the government targeting and collecting cash flows in the form of higher taxes from privately-held companies

Employ Maharaja’s political weight to lobby government

Management RiskMaharaja’s immense business diversification leads to uncertainty about management’s competency.

Bring in industry experts as part of

management team.

Cost of Capital Calculation Time varying Harvey ICCRG (May 97) Crisis Factor

Skew

Result - 23%- 26%

Spikes up to 36% - 40%

DCF Valuation DCF

APV approach as leverage changes Cash Flows Forecast 10 years out 1997-2006 PPP used to convert Cash Flows to USD Cost of Capital arrived at using ICCRG

Riskiness addressed in the Cost of Capital Historical Cost of Debt Growth Rate close to Historic Inflation Value per share in SLR And USD terms

DCF Valuation

Par Value

Par Value Rs. 10

X Rate 56.82

US $ Par V $0.176

Sensitivity Analysis

5.0% 0.169

5.5% 0.170

6.0% 0.172

6.5% 0.174

7.0% 0.176

7.5% 0.178

8.0% 0.180

8.5% 0.182

9.0% 0.185

9.5% 0.187

10.0% 0.190

10.5% 0.193

11.0% 0.197

11.5% 0.200

12.0% 0.204

Growth Rates

Share Value

Equity Value SL Rs. US $

Total Firm Value 990,169 $10,818

Less Debt (112,825) ($1,986)

Less Preference Share Capital (944) ($17)

Total Equity Value 876,400 $8,816

# of Equity Shares 47,697 47,697

Value per Equity Share 18.37 $0.185

Firm Value SL Rs. US $ % of value

APV Firm Value 504,792 $6,340 50.98%

Terminal Value 376,151 $3,176 37.99%

Tax Shield Value 109,226 $1,303 11.03%

Total Firm Value 990,169 $10,818 100.00%

Comparables Valuation Comparables

Performance Metric: P/E (Two Year Leading) Two comparables from the beverage industry chosen

2-year leadingMarket Cap/Earnings

Market Capitalization(US$ mn)

Ceylon Cold Stores 5.26

Maskeliya Plantations 2.52

Ole Springs Bottlers

Ceylon Cold Stores (60%) $ 2.379

Maskeliya Plantations (40%) $ 1.140

Enterprise Value for Ole $ 1.884

Proposed Deal Structure New Investor Demands

Guaranteed $ Investment Returns Convertible Preference Shares Put Option that essentially a convertible bond 10% return if option exercised Optional 3 year or 4 year exercise period

Recourse: Pepsi & Maharaja guarantors Should they accept the deal? What risks have they ignored?

Our Recommended Analysis

Value of the Put Option Monte Carlo DCF including skew Real Option

Value of Option

Combination valued at $387k

Payoff on the three year option exercise

Payoff on the four year option exercise

0.249

0.22.7

Asset Price

0.227 0.249

Call Option

0

Bonds

Monte Carlo DCF with Skew

Compare with cost of Par value of Rs10. - Looks good

BUT – When consider the dollar value of the share, - below the par value of $17.6

Our ConclusionValue to Maharaja Org. Value to DLJ.

DCF Value

Option Value $387k-$387k

-$104k

$283k-$387kNet

N/A

BUT REAL OPTIONS ?

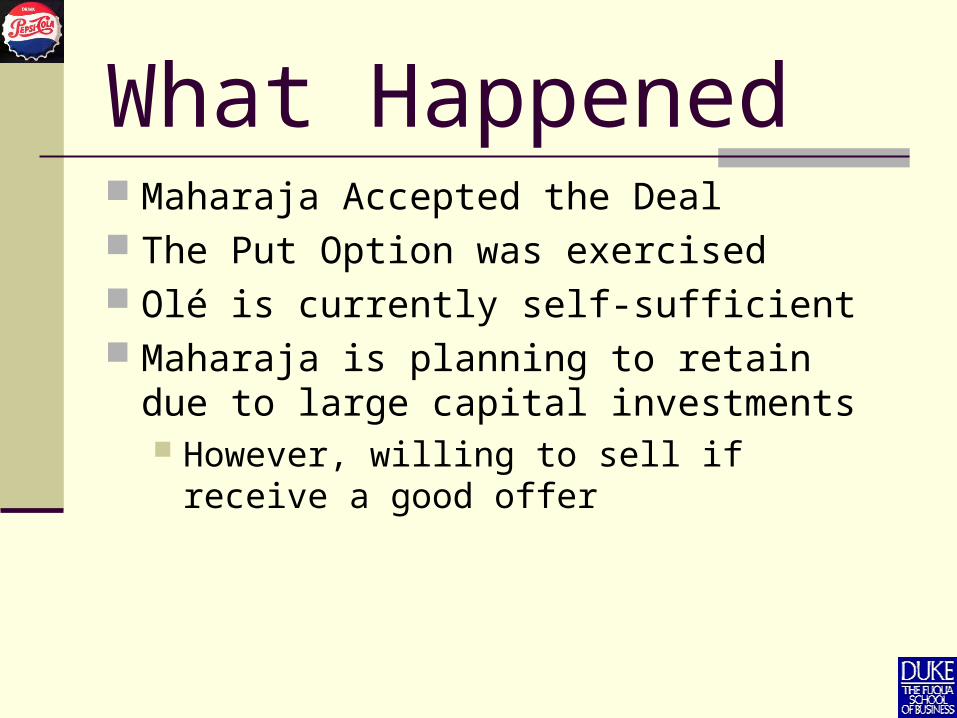

What Happened Maharaja Accepted the Deal The Put Option was exercised Olé is currently self-sufficient Maharaja is planning to retain due to large

capital investments However, willing to sell if receive a good offer

Key Lessons Exchange rate and skew are key Uncertainty involves time varying risks Option value underpins deal structure

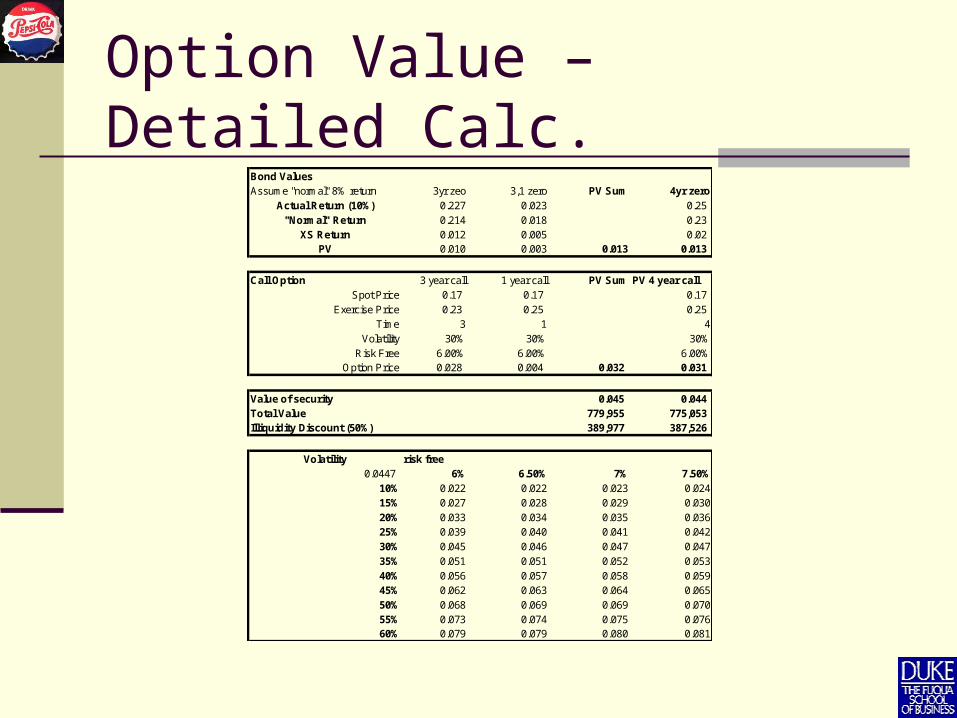

Option Value – Detailed Calc.Bond ValuesAssume "normal" 8% return 3yr zeo 3,1 zero PV Sum 4yr zero

Actual Return (10%) 0.227 0.023 0.25 "Normal" Return 0.214 0.018 0.23

XS Return 0.012 0.005 0.02 PV 0.010 0.003 0.013 0.013

Call Option 3 year call 1 year call PV Sum PV 4 year callSpot Price 0.17 0.17 0.17

Exercise Price 0.23 0.25 0.25 Time 3 1 4

Volatility 30% 30% 30%Risk Free 6.00% 6.00% 6.00%

Option Price 0.028 0.004 0.032 0.031

Value of security 0.045 0.044 Total Value 779,955 775,053 Illiquidity Discount (50%) 389,977 387,526

Volatility risk free0.0447 6% 6.50% 7% 7.50%

10% 0.022 0.022 0.023 0.02415% 0.027 0.028 0.029 0.03020% 0.033 0.034 0.035 0.03625% 0.039 0.040 0.041 0.04230% 0.045 0.046 0.047 0.04735% 0.051 0.051 0.052 0.05340% 0.056 0.057 0.058 0.05945% 0.062 0.063 0.064 0.06550% 0.068 0.069 0.069 0.07055% 0.073 0.074 0.075 0.07660% 0.079 0.079 0.080 0.081