The Effectiveness of Countercyclical Fiscal Policy in

Turkey during the Recent Economic Crisis:

Evidence from a Natural Experiment1

Florian Mischa

Atılım Seymenb

March 2012

- preliminary draft -

Abstract

During the recent economic crisis, Turkey was one of the countries experiencing the sharpest

contraction in GDP. Yet, the subsequent recovery was stronger and faster compared to the

OECD average with GDP growth rates of around 10%. Given that Turkey implemented a range of

countercyclical fiscal measures that were fairly large relative to other developing countries and

to previous crises, the question that immediately arises is whether these measures helped to

stabilize the economy. This paper evaluates the effectiveness of a particular measure of the

Turkish fiscal response package to the recent global financial crisis, namely a temporary cut in

the value added tax (VAT) and special consumption tax (SCT) on a range of durable goods which

according to estimates provided a stimulus to the Turkish economy of 0.27% of GDP excluding

any multiplier effects. From a theoretical perspective, contrary to other measures such as a

decrease of income taxes or an increase in public investment, it is much more likely that a cut of

1 We wish to thank Fatih Özatay for extensive comments. This work is supported by the Economic Research Forum

(ERF). The contents and recommendations do not necessarily reflect ERF’s views, and the authors bear the sole

responsibility for all errors.

a Address: Centre for European Economic Research (ZEW), P.O. Box 103443, D-68304 Mannheim, Germany. E-mail:

b Address: Centre for European Economic Research (ZEW), P.O. Box 103443, D-68304 Mannheim, Germany. E-mail:

1

indirect taxes on durable goods helps to stabilize the economy as consumers shift expenditure

to exploit temporarily lower prices.

This paper contributes to the long-standing debate in economics about whether governments

should engage in Keynesian-style countercyclical fiscal policy based on a novel and innovative

approach: from the World Bank Financial Crisis Survey for Turkey, we have firm-level data for

the periods during and after the tax cuts and for firms that benefited from the tax cut and those

which did not or benefited less. This allows us to consider the temporary VAT and SCT cuts as a

natural experiment where the treatment effect is the tax cut and the control group consists of

firms not benefiting or benefiting less from the tax cut according to their product portfolio. The

advantage of this approach is that we avoid well-known caveats of empirical analyses of

countercyclical fiscal policy at the macroeconomic level, in particular the simultaneity between

fiscal aggregates and output, and are able to evaluate a specific fiscal measure that was recently

implemented which could not have been done using macroeconomic data.

We show that once the effects of the tax cuts are properly identified temporary VAT and SCT

cuts appear to have a strong effect on the change of firm sales. In particular, depending on the

specification, the tax cuts appear to increase the change of firm sales by around 30 percentage

points. While we are aware that notably the definitions of treatment and control groups are

subject to a number of problems, we try to address these issues in a number of ways using

various alternative specifications. The treatment effect remains significant and robust across all

specifications when controlling for unobserved shocks at the region and industry level; our

results are consistent with theoretical predictions. While from our evidence it is difficult to

derive the magnitude of the fiscal multiplier of these tax cuts, we conjecture that it was above

one and therefore contributed to stabilizing output by stimulating domestic demand.

JEL codes: E32, E62, H20

Keywords: Countercyclical fiscal policy, consumption tax cuts, firm-level data

2

1 Introduction

There is a long-standing debate in economics about whether governments should engage in

Keynesian-style countercyclical fiscal policy. During the recent global financial crisis, this debate

has gained new momentum as many countries implemented fiscal stimulus packages. A prime

reason for this was the fact that conventional monetary policy as an instrument for stabilization

was no longer part of the feasible policy set as interest rates hit historically low levels in many

countries. Given that the crisis was preceded by years of strong growth which increased fiscal

space, even developing countries which traditionally rather pursue pro-cyclical policies were

able to implement fiscal response packages. The objective of this paper is to re-visit the

effectiveness of such stabilization policies, in particular of a reduction of indirect taxes,

exploiting a natural experiment in with Turkish data from the recent crisis that comes from a

unique firm-level dataset.

Countercyclical fiscal policy can in general comprise a variety of measures including spending on

infrastructure and on goods and services, income transfers and tax cuts, which were

implemented in over a quarter of the countries within a group of 22 advanced and developing

economies surveyed by ILO (2009) in response to the global financial crisis. There is a large

empirical macroeconomic literature that addresses the question of whether fiscal shocks, in

particular a debt-financed increase of public spending or debt-financed tax cuts, can have a

positive impact on output over the short run. In general, this literature mostly applies vector

autoregressions (VARs) comprising quarterly series of output, fiscal variables and various other

inputs to private sector production. Most papers and empirical specifications find positive

output effects as a result of tax cuts (see Hebous, 2011, and Kneller and Misch, 2011, for

surveys of the literature).

Because of the simultaneity thought to exist between output and fiscal aggregates, the

identification strategy in the VAR framework is however critical. Recent papers including Romer

and Romer (2010) and Mertens and Ravn (2009) use narrative evidence such as speeches by

politicians to single out those tax changes that were implemented for reasons not related to

output or the state of the economy and only estimate the effects of those based on the U.S.

data. While this type of identification provides credible evidence on the effects of tax shocks, it

may be difficult to collect similar evidence for other countries. In addition, whether the results

of studies using the narrative approach also apply to the effects of fiscal anti-crisis measures

which these studies essentially omit from their analysis is unclear. More generally, even other

identification strategies cannot be used to evaluate the effectiveness of the specific measures

taken during the recent economic crisis: the crisis is likely to represent a structural break in the

series implying that there are not sufficient post-crisis observations of macroeconomic variables

available yet. From a policy perspective, another disadvantage of this literature relates to the

3

fact that – apart from few exceptions – it estimates the effects of broader fiscal shocks, but not

the specific effects that result from the change in a particular tax. This makes it difficult to ‘use’

these results for fiscal policy design in practice. Macro evidence also remains silent with respect

to the specific transmission channels, e.g., in case it stabilizes output, through what aspect of

the firm behavior this is achieved. More detailed knowledge about this aspect is, however,

crucial for the design of countercyclical fiscal policy packages.

An obvious remedy for the simultaneity bias thought to exist between fiscal aggregates and GDP

including its main components and other issues relating to macroeconomic evidence is the use

of micro data. Dating back to Shapiro and Slemrod (1995), there are several papers that

examine the effects of mostly income tax rebates or cuts on household expenditure using

mostly U.S. data coming from several different sources of household data. The micro-level

results imply a (modest) rise in aggregate consumption as a result of such tax changes, although

to varying degrees. Auerbach and Gale (2009) and Jappelli and Pistaferri (2010) survey this

literature in detail, and we provide a short summary of various papers in the next section.2

In contrast to the existing empirical literature, this paper takes a novel approach and estimates

the effects of one particular measure of countercyclical fiscal policy, namely a temporary cut of

indirect taxes, on firm sales using firm-level data. So far, firm-level data has rarely if ever been

used in this context.3 While temporary cuts in indirect taxes can be quickly implemented and

are therefore a fairly popular measure aimed at stimulating demand, theoretically, the effects

are ambiguous.4 One the one hand, a temporary value added tax (VAT) cut on durable and/or

luxury goods induces intertemporal substitution effects which policy makers wish to exploit,

namely that unconstrained households change the timing of their purchasing pattern to take

advantage of temporarily lower prices. This becomes possible because the expenditure on

luxury/durable goods does not have to coincide with the timing of their consumption making

them highly responsive to intertemporal price differences induced by temporary VAT cuts

(Crossley et al., 2010). By contrast, temporary tax cuts are unlikely to affect the timing of

consumption of necessity and perishable goods because the timing of purchasing and

consumption often have to coincide (Browning and Crossley, 2000).

2 There is also a branch of the literature that examines the effects of tax changes on firm-level investment which is

reviewed in detail by Auerbach and Gale (2009) and Hassett and Hubbard (2002). However, as Auerbach and Gale

(2009) argue, the results of this literature are not relevant in the context of evaluating the effects of tax changes to

stimulate the private investment over the short run.

3 As Heady (2011) points out, a VAT cut instead of a cut of income taxes, is however inconsistent with the desire to

promote long-run growth.

4 See Crossley et al. (2009), Barrell and Weale (2009) and Blundell (2009) for details.

4

On the other hand, a temporary VAT cut induces a temporary income effect. As a result

forward-looking consumers that are not credit-constrained will save the additional income as

parts of efforts to smooth incomes intertemporally. The reason is that Ricardian equivalence

dictates that future tax increases will be necessary to offset the cuts. As a further complication,

it is unclear whether the substitution and income effects will arise at all because VAT tax cuts do

not necessarily change consumer prices. The reason is that the degree of the pass-through, i.e.

the extent to which producers pass on the reduction to consumers, matters, which depends on

market structure and menu costs. A low pass-through leaves prices and therefore consumption

expenditure by consumers almost unchanged. Whether the pass-through is sufficiently high so

that VAT cuts induce significant price changes and whether the intertemporal substitution effect

exceeds the income effect are ultimately empirical issues. Theoretically, it may be expected that

the pass-through significantly differs from zero, and that the changes induced by the

substitution effect exceed the ones of the income effect.5 This makes it more likely that

temporary indirect tax cuts stimulate demand compared to other potential countercyclical fiscal

measures such as cuts of direct taxes which do not entail intertemporal substitution effects and

public investment programs which are often subject to implementation lags and sometimes

lead to outright waste of public resources.

For the purpose of empirical research, it is therefore most interesting to evaluate the effects of

temporary indirect tax changes where substitution effects can be expected. This is the case

when temporary consumption tax changes occur for durable and luxury goods rather than for

necessity and non-durable goods. At the same time, to be able to construct a control group as a

counterfactual, it is desirable that the VAT cut is not universal but covers some goods only.

Turkey is one of the few countries that have recently implemented such a change as part of

their fiscal response package to the global economic crisis, namely a cut of VAT and the special

consumption tax (SCT) at the peak of the financial crisis in 2009, making it an ideal case for our

investigation.6 The measures introduced by the Turkish government covered exclusively some

but not all durable goods.

In this paper, we use this policy change as a natural experiment to estimate the effects of these

tax changes: our firm level data includes company sales shortly prior to, during and after the tax

change, allowing us to implement a difference-in-difference approach where those firms

primarily relying on goods covered by the tax cuts are the treatment group and firms which

primarily sell goods not covered by the tax cuts are represent the control group. Contrary to the

existing literature and in the absence of detailed and higher frequency household data, we use 5 Blundell (2009) argues that at least for developed countries and most sectors, the pass-through is between 50%

and 100% with the distribution tilting towards the upper limit.

6 In the context of this paper, SCT and VAT cuts can expected to have identical effects and are therefore not

discussed separately.

5

the change in firm sales as an endogenous variable which, in aggregate, are likely to be closely

correlated with the change of aggregate private demand.

The comparability of the treatment and the control group is a crucial aspect in our specification

because firms are likely to have been affected differently by the financial crisis. Some non-

treated firms (i.e. firms that did not directly benefit from the fiscal stimulus) might have

performed better than treated firms (firms that were targeted by the fiscal stimulus measures)

simply because the former were less affected by the financial crisis. The control-group does

therefore not offer a perfect counterfactual because firms in different sectors may have been

subject to different time-specific shocks. In order to control for differences in exposure to

shocks induced by the global financial crisis across the treatment and control groups, we include

time-variant industry effects. Given that few (but not all) of the sectors are entirely part of the

control group, as a robustness check, we also exploit differences in the effects of the tax cuts

within the treatment group based on the export ratio of firms. Here, the underlying rationale is

that the more firms export, the less they are affected by domestic consumption taxes. The use

of this type of methodology and of firm-level data to evaluate countercyclical fiscal policy is the

first contribution of our paper.

The second contribution of the paper is to provide much needed firm-level evidence on the

effects of countercyclical fiscal policies in Turkey, an important emerging market economy, from

the recent crisis. By contrast, most of the existing literature focuses on the U.S. or other

advanced countries and uses macro methods. Given that during the global financial crisis,

Turkey was among those countries that experienced the sharpest contractions in GDP, anti-

crisis measures, and their evaluation, are arguably more relevant compared to advanced market

economies. This holds especially in the light of increased fiscal space that enabled emerging

market economies to implement countercyclical fiscal measures for the first time in many cases.

However, given that time series of developing countries are often too short and that other

econometric problems are likely to arise, our type of micro evidence is a more promising

approach to evaluate the effects of such policies in Turkey and other emerging market

economies. Our results indicate that the VAT and SCT cuts indeed boosted firm sales suggesting

that this measure helped to stabilize the Turkish economy by stimulating private demand. While

the data we use has limitations, our results appear nevertheless to be robust when we address a

number of possible concerns about their reliability. We conjecture that such temporary cuts of

indirect taxes are a suitable measure of countercyclical policy if stabilization is the prime policy

objective.

The paper is organized as follows. Section 2 provides a review of microeconomic evidence on

the effects of tax cuts at the household level and Section 3 some background information on the

crisis and countercyclical policies implemented during the crisis in Turkey. Section 4 presents

6

the data and provides descriptive statistics. Section 5 develops the specification to be tested

and presents the results. Section 6 concludes and discusses possible policy implications.

2 Literature

This section reviews the empirical literature on the effects of income tax cuts that were often

implemented as part of fiscal response packages at the household level which is probably the

closest related strand of literature. Shapiro and Slemrod (1995, 2003, 2009) investigate the

issue extensively. In particular, Shapiro and Slemrod (2003, 2009) conduct a household survey

and find that only a fifth of the households increased spending as a result of the 2001 and 2008

tax rebates. In other studies, the results are somewhat more nuanced. Broda and Parker (2008)

use weekly expenditures of a large number of households and estimate that the average

household increased spending on non-durables by 3.5% as a result of the 2008 tax rebate which

they argue had significant effects on non-durable consumption expenditure. Johnson et al.

(2006) use data from the consumer expenditure survey to examine the 2001 tax rebate and find

that households spent 20 to 40 percent of their rebates on non-durables which would imply

significant aggregate consumption effects. Finally, Agarwal et al. (2007) use credit card account

data to estimate the household response to the 2001 rebate. They find that while initially some

of the rebate was saved, spending increased subsequently. Watanabe et al. (2001) seems to be

one of the few papers that examine similar issues for other countries. They estimate the effects

of various changes to income and consumption taxes that were mostly meant to stimulate the

economy between 1975 and 1998. They find that the effects of temporary and permanent, as

well as anticipated and unanticipated, tax changes on consumer expenditure significantly differ.

Hori and Shimizutani (2007) likewise use Japanese micro data to estimate the effects of the

1995 and 1997 income tax cuts on household consumption. They also find differences between

both tax shocks.

3 Crisis and Countercyclical Cyclical Policy in Turkey

3.1 Macroeconomic Background The 2008-2009 recession was preceded by an average and fairly constant annual GDP growth

rate of 6.8% over the period 2002-2007 in Turkey, exceeding the ones of many other developing

economies (see Uygur, 2010). Yet, Turkey experienced one of the largest declines in GDP growth

during the crisis period in 2008-2009, and its performance was characterized by significant

volatility. Figure 1 compares the year-on-year growth of GDP and industrial production in Turkey

with the average of the OECD countries. At the deepest point of the crisis, the first quarter of

2009, the y-o-y GDP decline was registered 13% in Turkey, while it amounted to only 5.47% in

the OECD as a whole. However, Turkish GDP recovered from this deep point more strongly than

7

many other economies starting in the last quarter of 2009. The growth rates of both the GDP

and the industrial production in Turkey were much higher than in many other economies

following that period.

Figure 1: Macroeconomic indicators of Turkey and the OECD in comparison

The foregoing strong performance in the aftermath of the crisis was also reflected in the

unemployment rate numbers. As Figure 1 shows, the y-o-y percent change in the

unemployment rate was slightly higher than the OECD average during the worst periods of the

crisis, but the change in the unemployment rate turned negative earlier and stronger in Turkey

than in many other economies. In line with the hitherto picture, the consumption growth of

Turkey has been above the OECD average following the crisis.

3.2 Background on the Fiscal and Monetary Response The period of strong GDP growth between 2002 and 2007 witnessed at the same time declining

levels of public net debt stock: as percent of GDP, it gradually declined from 61.5% in 2002 to

28.2% in 2008 according to the Turkish Treasury. Strong GDP growth coupled with debt

reductions prior to the crisis and fairly low budget deficits of 0.6 to 1.8% of GDP between 2005

8

and 2008 provided fiscal space for relatively large fiscal response packages to counteract the

crisis. According to the estimates of SPO (2009), the total costs of the direct fiscal measures

taken in response to the global crisis amounted to (and were expected to amount to) 0.83%,

2.25% and 2.22% of the GDP in 2008, 2009 and 2010, respectively.

In addition, there were strong anti-crisis measures taken by the Turkish Central Bank (CBRT).

After the beginning of the recession, the overnight lending rate of CBRT had reached a peak of

20.25% in June 2008 and decline thereafter gradually to 8.75% in November 2010. As the first

wave of the consumption tax measures were announced in mid-March 2009, the rate was 13%,

and it had gradually declined to 9.75% by the time the second wave of the measures were

reaching an end in September 2009. Alp and Elekdağ (2011), who focus on the role played by

monetary policy in Turkey during the global financial crisis, argue that the recession would have

been much more severe without the interest rate cuts of CBRT. While in this paper, we do not

focus on the effects of monetary policy, the time effects that we include in the regressions

should pick up most of the impact of interest rate cuts.

The natural question that arises in this context is whether and to what extent the anti-crisis

measures contributed to the superior growth and unemployment performance of Turkey

following the lowest point of the crisis. SPO (2009) classifies the direct fiscal measures into two

groups: revenue and expenditure measures. The expenditure measures cover the extraordinary

government consumption and investments, social security contributions as well as transfers to

households and business. Under the revenue measures fall particularly changes in taxes on

individual income as well as business and consumption taxes.

3.3 VAT and SCT Cuts In Turkey, there are two main indirect taxes imposed on sales: the VAT and the SCT. Both taxes

are imposed on the same value. A VAT is applied to all goods and services sold, yet in three

different groups subject to a rate of 1%, 8% or 18%, respectively. The VAT and SCT cuts which

we focus on in this paper and which were an important element of the fiscal response to the

crisis amounted to an estimated GDP share of approximately 0.27% which is significant. Adding

to this number the reduction from 15% to 10% in the Resource Utilization Support Fund

deduction on consumer loans, an estimated 0.36% of GDP was used to boost consumption

directly by the State Planning Organization. Note that these numbers reflect the fiscal costs of

the undertaken measures, while their impact on GDP may have been much larger due to

multiplier effects. A number of VAT and SCT tax rate changes were aimed at the automobile

industry, amounting to about 40% of entire consumption tax measures.

The Turkish government decreased either the VAT or the SCT for some product groups in the

period between March and September 2009. These anti-crisis measures were implemented

using four different government decrees, see Table 1. The first three decrees numbered 14802,

14812 and 14881 referred to the period March/April-June, the last decree, numbered 15081, to

9

the period June/July-September 2009. All products that were the subject of the last decree were

included also in one of the previous decrees corresponding to the first period of the measures.

Yet, not all products that were mentioned in the first-period decrees were also subject to

reductions in the second period. The decrees numbered 14802, 14812, 14881 and 15081 were

announced and approved by the government only a short time before they entered into force,

namely on March 13, March 25, April 4 and June 12, respectively. Thus, there was generally a

short time period between announcement and implementation.

Table 1: Indirect tax reductions during the crisis

Types of products covered

Decree Period of tax cut

2nd

quarter

2009

3rd

quarter

2009

2nd

quarter

2009

3rd

quarter

2009

SCT reduction in white goods

and electronic household goods

as well as car industry

2009/14802 2009/15081a 17.03-

15.06

16.06-

30.09

VAT reduction furniture,

information, communication,

industrial and office equipment

2009/14812 2009/15081b 30.03-

30.06

01.07-

30.09

The list of products covered by

2009/14812 further extended 2009/14881 2009/15081b

15.04-

30.06

01.07-

30.09

An important characteristic of the foregoing cabinet decrees is that they reduce the VAT or the

SCT for different product groups at different rates. Therefore, there is a large heterogeneity in

this respect. The decree 14802 covers, among others, an SCT reduction from 6.7% to 0% for

various white and electronic goods and different levels of SCT reductions on different types of

products the car industry. The reduction in less-than-1600 cc passenger cars is, for example

from 37% to 18%, whereas it is from 1% to 0% for buses. Thus, when the VAT is also taken into

account, the total consumption tax declines from 55% to 37% for small passenger cars and from

19% to 18% for buses. The decrees 14812 and 14881 cover VAT reductions in new offices,

furniture, and some information, communication and bureau equipment. One part of the

decree 15081, that contains the measures for the second period, is called 15081a in Table 1 and

refers to a sub-group of goods in the decree 14802. The rest of the same decree, called 15081b

in the table is related to the decrees 14812 and 14881.

10

4 Data

Our firm level data comes primarily from the Financial Crisis Surveys (FCS) provided by the

World Bank, a specialized firm-level dataset to study firm behavior and performance during the

global economic crisis. Firms were surveyed during three periods: during June and July 2009

(wave 1), during February and March 2010 (wave 2), and during June and July 2010 (wave 3).

The resulting panel is unbalanced with 802 different firms surveyed and 1484 observations; the

average number of observations per firm is 1.83. All firms surveyed as part of the FCS are also

included in the 2008 round of the Enterprise Survey of Turkey (ES) carried out at the onset of

the crisis. This allows us to use additional variables on firm characteristics not included in the

FCS that can be considered as quasi time-invariant over the short run.

4.1 Assignment of Treatment and Control Groups We assign all firms in the data to either the treatment group (i.e., firms most affected by the tax

cut) and the control group (i.e., firms less or not at all affected by the tax cut). To do this, we use

firm-level information on the sector included in the FSC and on the main product which is the

product that represented the largest share of firm sales in 2008 from the ES. We then match

this information with detailed information on which product types were covered in the

government decrees implementing the tax cuts.

We recognize that this way of assigning firms to control and treatment groups may be subject to

different types of concerns which we address in several ways. First, and most obviously, even if

the main product is not subject to tax cuts, the firm may still have benefited from tax cuts if

secondary products that it sells but which we do not observe are subject to tax cuts. The

(unobserved) secondary products are likely to include close substitutes as in many cases as firms

specialize in certain areas. The tax cuts are designed such that they typically include most

substitutes. However, we cannot completely rule out that secondary goods of firms in the

control group may have been affected by tax cuts, but we argue that they are affected relatively

less compared to the treatment group.

Second, given that the product-level information comes from 2008, it is possible that firms

discontinued a particular product line, or that changes in demand led to changes in the product

mix so that firms started a new product line possibly changing their main product and thereby

the classification in treatment / control groups. In turn, demand changes may have been the

result of tax changes. For instance, firms that did previously not produce or sold a particular

product may have deliberately changed their strategy and increased the share of goods subject

to tax cuts in their overall sales through increased production for instance. To take these

problems into account, in some specifications, we exclude firms where sector information in the

11

FCS is contradictory and does not coincide with the 2008 information.7 While this may simply

indicate data problems or simply mistakes in the coding of the sector as part of the ES, it may

also possibly indicate a change in the product line. We find that the coefficient estimates are

only robust once we exclude these firms from the treatment group suggesting that this problem

is indeed important.

However, given that the decrees which led to the tax cuts were announced only few days prior

to implementation and that the duration of the tax cuts was only relatively short, it is unlikely

that, with adjustment costs, firms deliberately changed their product mix in response to the tax

cuts themselves. Adjustment costs make it also unlikely that firms which were subject to tax

cuts according to their main product in 2008 changed their product mix to the extent that their

classification as either firms of the treatment or control group changes. Even if they

discontinued the main product of 2008, it still seems likely that the remaining products are

substitutes and are affected by the tax cuts in the same way.

Third, sales of firms of which products are not covered by the tax cuts may still increase if their

products are complements with the products covered by the tax cut. This is typically the case for

intermediate inputs. For instance, sales for automobile parts used in the production of

automobiles may increase as well if taxes for automobiles are lowered thereby triggering an

increase in demand. As a robustness check, we therefore also include those firms in the

treatment group that produce goods which we believe are complementary with those goods

subject to tax cuts. In particular, in this specification, we include firms in the treatment group

that produce parts exclusively used by car producers.

Fourth, sales of firms that are exporting a large share of their output are not affected by tax cuts

as VAT and SCT are only levied on domestic sales, but not on exports. However, many firms

export only some share of their output thereby simply benefiting to a lesser extent from the tax

cut. As a robustness check, we only include non-exporters which we define as firms where

exports amounted to no more than 30% of total sales prior to the crisis. Given that demand in

export markets contracted as a result of the crisis, it is unlikely that firms were able to increase

their exports share to compensate for a decline in demand in the domestic market. In turn, this

implies that the share is likely to have remained constant or may have declined, rather than

increased, during the financial crisis.

Fifth, while the decrees to implement the tax cuts contain detailed product descriptions, the

product descriptions in our firm data are sometimes imprecise in the sense that there may still

7 As an exception, we do not exclude firms reported to operate in the retail or wholesale sectors in the ES or in the

FCS from our sample in most cases as these sectors do not have any implications for the types of goods sold. In

other words, sector switches involving these sectors do not necessarily imply changes in the product mix and may

rather have occurred due to mistakes made in the survey.

12

be uncertainty as to whether a particular product is covered by the decrees or not. In particular,

the terms used for the same product in the decrees and the firm dataset may be different. In a

robustness check, we therefore include all those firms in the treatment group for which this

type of uncertainty arises, but where we assume that the product was covered by the tax cut.

In essence, depending on which of these factors we take into account, we are able to construct

several distinct treatment groups that only partially overlap in terms of the firms they cover (see

Table 2). The treatment groups differ by whether we include firms in the treatment group with

recorded sector changes, firms that export over 30% of their output, firms that produce

intermediate inputs for the production of goods covered by the tax cuts and firms where we

assume that their main product was subject to the tax cut but where ultimately we cannot be

sure as the firm-level product description is not fully clear. We combine these dimensions to

construct seven treatment groups that only partially overlap and differ in terms of the number

of observations included. We use all of these treatment groups as a robustness check.

Table 2: Number observations by treatment group

Treatment

group

Only non-

exporters

Reliable

industry

classification

Intermediate

goods

included

Unclear

product

classification

Number

of obs. in

wave 1

Number

of obs.

across all

waves

1 no no no no 14 61

2 yes no no no

3 no yes no no 8 36

4 yes yes no no

5 no yes yes no 15 57

6 yes yes yes no 13 53

7 no yes yes yes

Finally, the products covered by the tax cuts are likely to not have been randomly selected. In

particular, the government may have selected those products with projected significant falls in

demand. If this leads to systematic differences in demand between the products included in the

treatment and control groups, this would result in underestimating the effects of the tax cuts

because the demand for goods in the treatment group declined more sharply compared to the

demand for goods in the control group. This would imply that the magnitude of the estimated

coefficients is rather at the lower bound. However, while we cannot control for unobserved

13

time- and product-specific effects with our data, we are able to control for time-varying sector-

specific effects as there are no sectors exclusively in the treatment group.

4.2 Dependent Variable As dependent variable in our baseline specification, we use the change of sales compared to the

same month in the previous year, which we label as SALES_CHANGE. The corresponding

question asked in the interview of the first round of the FCS (wave 1) was “If you compare this

establishment’s sales for the last completed month in 2009 with the same month in 2008, how

did they change?”. For the subsequent rounds carried out in 2010, the question was identical

but referred to 2009. We refer to the same month in the previous year as the ‘reference’ period,

and ‘last month’ as the ‘comparator’ period; for wave 1 SALES_CHANGE is the difference in sales

between May / June 2009 (comparator period) and May / June 2008 (base period), for wave 2

SALES_CHANGE is the difference between January / February 2010 (comparator period) and

January / February 2009 (base period) and for wave 3 SALES_CHANGE denotes the difference

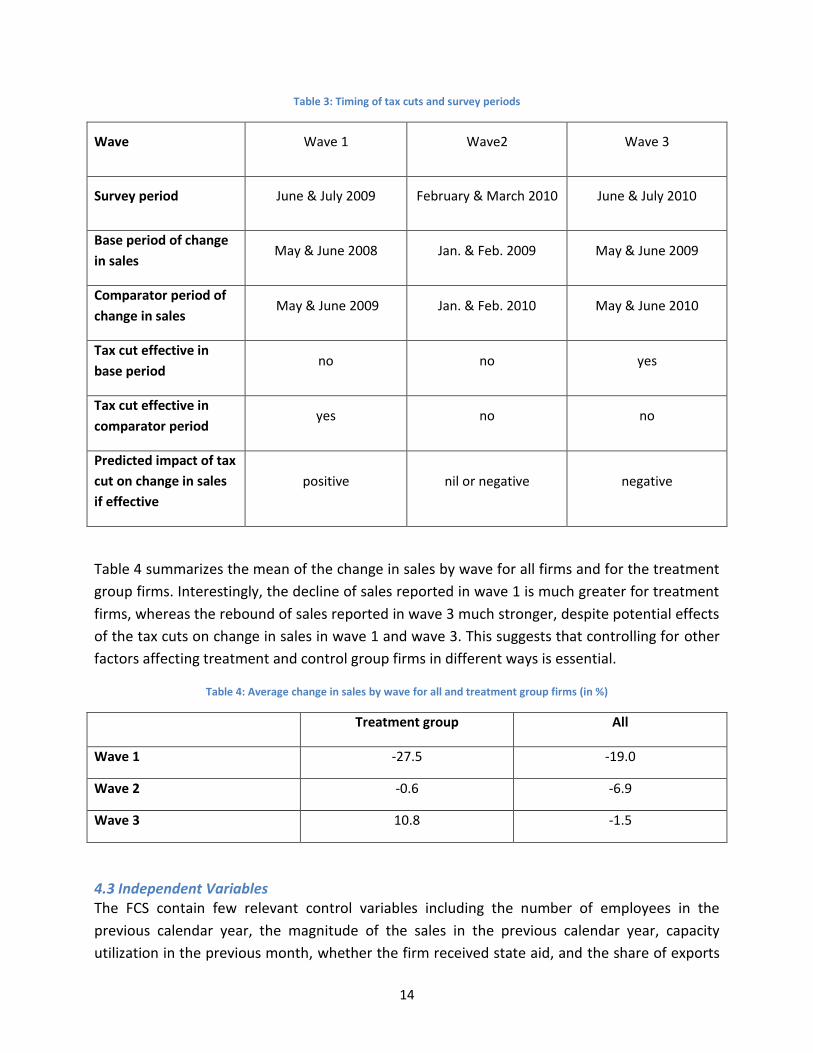

between May / June 2010 (comparator period) and May / June 2009 (base period). Table 3

summarizes this information.

The timing of the interviews together with the framing of the question in the survey are crucial

for our estimation strategy. Supposing that the tax cuts have measurable effects, we would

expect them to affect the change in sales if they were effective either in the base period or in

the comparator period. In the first (second) case, holding all other factors constant, they raise

the levels of sales in the comparator (base) period leaving sales in the base (comparator) period

unaffected and thereby increasing (decreasing) the change in sales. By contrast, if both base and

comparator periods are affected by the tax cut or unaffected by the tax cut, we do not expect to

observe any effects of the tax cuts on the change in sales.

With respect to wave 1, the tax cut was in effect in the comparator period but not in the base

period suggesting that we would observe a positive effect of tax cuts on the change in sales of

those firms selling relevant goods if tax cuts indeed boost firm sales. With respect to wave 2, the

tax cut was in effect neither in the comparator period nor in the base period suggesting that we

do not observe any direct treatment effects. However, it is possible that if intertemporal

substitution effects were present, demand for products under the tax cut were reduced in the

period following the tax cut, i.e., in the months following the expiry of the tax cuts in September

2009. As a result, it may be possible to observe either nil or indirect negative treatment effects

in wave 2, i.e., the firms in the treatment group may have a experienced a greater fall in sales in

comparison to the control group holding other factors constant. Finally, with respect to wave 3,

the tax cut was in effect in the base period but not in the comparator period which would imply

negative treatment effects on the change of sales if tax cuts indeed helped stabilize private

consumption. Table 3 summarizes this information.

14

Table 3: Timing of tax cuts and survey periods

Wave Wave 1 Wave2 Wave 3

Survey period June & July 2009 February & March 2010 June & July 2010

Base period of change

in sales May & June 2008 Jan. & Feb. 2009 May & June 2009

Comparator period of

change in sales May & June 2009 Jan. & Feb. 2010 May & June 2010

Tax cut effective in

base period no no yes

Tax cut effective in

comparator period yes no no

Predicted impact of tax

cut on change in sales

if effective

positive nil or negative negative

Table 4 summarizes the mean of the change in sales by wave for all firms and for the treatment

group firms. Interestingly, the decline of sales reported in wave 1 is much greater for treatment

firms, whereas the rebound of sales reported in wave 3 much stronger, despite potential effects

of the tax cuts on change in sales in wave 1 and wave 3. This suggests that controlling for other

factors affecting treatment and control group firms in different ways is essential.

Table 4: Average change in sales by wave for all and treatment group firms (in %)

Treatment group All

Wave 1 -27.5 -19.0

Wave 2 -0.6 -6.9

Wave 3 10.8 -1.5

4.3 Independent Variables The FCS contain few relevant control variables including the number of employees in the

previous calendar year, the magnitude of the sales in the previous calendar year, capacity

utilization in the previous month, whether the firm received state aid, and the share of exports

15

prior to the crisis from the 2008 Enterprise Survey. Both whether the firm received state aid and

the magnitude of sales contains many missing observations reducing our sample so that we

decided not to use these variables. However, as a robustness check, we re-ran all of our

specifications with the magnitude of sales as an explanatory variable and find that the results

hardly change and remain robust qualitatively. While capacity utilization is certainly driven by

the level of sales, the link to the change of sales which is our dependent variable is less direct.

Again, as a robustness check, we re-run all specifications with capacity utilization omitted and

the results remain robust and do not change qualitatively. Table 5 provides descriptive statistics

of all variables used.

Table 5: Descriptive statistics

variable min p25 p50 mean p75 max sd

sales_change -100 -30 0 -9.714483 10 100 34.23311

labour 1 13 35 132.5868 103 3590 326.0394

capacity 0 20 60 50.77314 75 100 31.50077

non_exporter 0 1 1 0.8140162 1 1 0.3892248

5 Empirical Specification and Results

5.1 Identification We start out by estimating a simple difference-in-difference estimation with the treatment

group 1 which corresponds to specification 1 in Table 2:

SALES_CHANGE = const. + treat.group + wave1 + wave2 + treat.group x wave1 + controls

Treat.group is a dummy for the treatment group 1, wave1 and wave2 are time dummies for the

respective waves and the interaction term treat.group x wave1 measures the treatment effect.

We also include three control variables including the number of employees last year

(represented by labour), capacity utilization, and a dummy with indicates whether the firm is a

an exporter (i.e., according to our definition whether it exports more than 30% of its sales).

With respect to the control variables, the signs of the coefficients are generally plausible: size as

measured by the number of employees has a positive and significant effect on the change of

firm sales; this may suggest that larger firms are more diversified so that their sales declined less

during the crisis. The sign of capacity utilization is likewise positive mirroring probably the

correlation with the level of sales. Firms with higher levels of capacity utilization, which hence

showed a higher efficiency in production, experienced thereby a less steep decline of sales or

conversely a stronger increase, but we acknowledged above that there may also be a problem

of reverse causality; however, our results remain robust to the exclusion of this variable. Finally,

firms that relied less heavily on foreign markets at the onset of the crisis as measured by the

16

time-invariant non_exporter variable taken from the ES from 2008 also experienced less steep

declines of sales or conversely stronger sales increases. Given that the origin of the crisis was

abroad, this may be somewhat intuitive. In this specification, we also include unobserved time

effects and a dummy indicating whether the firm is part of the treatment group. The interaction

term of the dummy indicating whether the firm is part of the treatment group with the time

dummy for wave 1 is the treatment effect and therefore the variable of interest. Here the

coefficient is negative and not significant. This would indicate that the tax cut had no effects on

firm sales, or alternatively, that the effects of the tax cuts are poorly identified, especially given

that there may be additional unobserved effects that we do not control for in specification (1).

In the remaining specifications of Table 5, we successively control for additional unobserved

effects to examine whether identification is indeed an important issue. In specification (2), we

add unobserved region and industry effects. In specification (3), we instead add firm fixed

effects which are likely to capture most of the unobserved region and industry effects given that

most firms do not move between regions and do not switch industries. In the first two cases,

the coefficient of the treatment effects remains negative, but changes sign in the third case.

Given that the treatment group dummy and the non-exporter dummy are time-invariant, we

omit these variables from all specifications with firm fixed effects.

In specifications (4) and (5), we control for unobserved and time-variant industry effects. This

appears to be critical: the coefficient of the treatment group increases in size and becomes

significant. Time-industry effects are especially important to explain the change in firm sales

during an economic crisis as different industries are likely to be subject to different shocks, for

instance due to a decrease in demand for durables relative to the demand of necessity goods. It

is these type of effects that industry-time effects account for in the regression. In specification

(5), we only include non-exporters in treatment group (i.e., we use treatment group 2) and add

also unobserved time-variant region-specific effects. The coefficient estimates indicates that

treatment effect (i.e., the tax cut) increases the change in sales by between 16 and 18

percentage points.

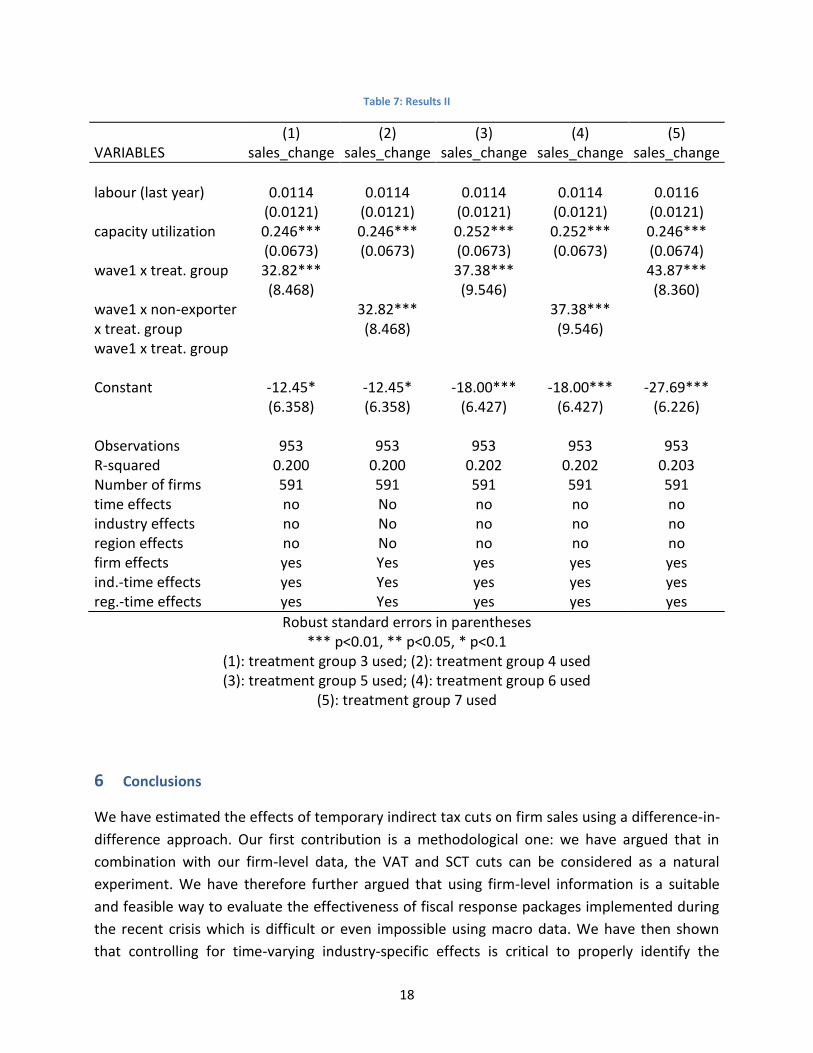

5.2 Alternative Treatment Groups Following our discussion above, we now test the robustness of our results using the remaining

treatment groups as defined in Table 2. All of the specifications are based only on those firms

for which no sector change is recorded which reduces the number of observations and notably

those in the treatment group. However, in specifications (3) to (5), we enlarge the treatment

group by including firms producing intermediate goods and in specification (5) by also including

firms where we believe that they benefited from the tax cut but where we cannot be fully sure

due to a poor description of the main product. In all specifications, we control for unobserved

industry-time and region-time effects.

17

Table 6: Results I

(1) (2) (3) (4) (5)

VARIABLES sales_change sales_change sales_change sales_change sales_change

labour (last year) 0.00952*** 0.0108*** 0.0161 0.0174 0.0172 (0.00286) (0.00299) (0.0116) (0.0115) (0.0113) capacity utilization 0.259*** 0.275*** 0.207*** 0.219*** 0.224*** (0.0312) (0.0325) (0.0528) (0.0534) (0.0529) non_exporter 5.536** 3.956 (2.344) (2.534) treat. group 13.80** 12.24* (6.109) (6.528) wave1 x treat. group -7.163 -8.794 1.292 16.82* (11.39) (11.59) (12.83) (10.09) wave1 x non-exporter x treat. group

17.99*

(10.81) Constant -37.95*** -38.84*** -29.95*** -27.46*** -27.02*** (3.080) (4.355) (3.517) (7.358) (7.461) Observations 1,379 1,379 1,379 1,379 1,379 R-squared (within) 0.087 0.195 0.201 Number of firms 774 774 774 774 774 time effects yes yes yes No no industry effects no yes no No no region effects no yes no No no firm effects no no yes yes yes ind.-time effects no no no yes yes reg.-time effects No no no No yes

In all specifications, the coefficient of the treatment group is highly significant and increases in

size compared to the one in Table 7 but does not change sign. Our results therefore appear to

be robust when we attempt to address the issues related to the classification of the firms in

treatment and control groups described in Section 4.1.

18

Table 7: Results II

(1) (2) (3) (4) (5) VARIABLES sales_change sales_change sales_change sales_change sales_change

labour (last year) 0.0114 0.0114 0.0114 0.0114 0.0116 (0.0121) (0.0121) (0.0121) (0.0121) (0.0121) capacity utilization 0.246*** 0.246*** 0.252*** 0.252*** 0.246*** (0.0673) (0.0673) (0.0673) (0.0673) (0.0674) wave1 x treat. group 32.82*** 37.38*** 43.87*** (8.468) (9.546) (8.360) wave1 x non-exporter x treat. group

32.82*** (8.468)

37.38*** (9.546)

wave1 x treat. group Constant -12.45* -12.45* -18.00*** -18.00*** -27.69*** (6.358) (6.358) (6.427) (6.427) (6.226) Observations 953 953 953 953 953 R-squared 0.200 0.200 0.202 0.202 0.203 Number of firms 591 591 591 591 591 time effects no No no no no industry effects no No no no no region effects no No no no no firm effects yes Yes yes yes yes ind.-time effects yes Yes yes yes yes reg.-time effects yes Yes yes yes yes

Robust standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1

(1): treatment group 3 used; (2): treatment group 4 used (3): treatment group 5 used; (4): treatment group 6 used

(5): treatment group 7 used

6 Conclusions

We have estimated the effects of temporary indirect tax cuts on firm sales using a difference-in-

difference approach. Our first contribution is a methodological one: we have argued that in

combination with our firm-level data, the VAT and SCT cuts can be considered as a natural

experiment. We have therefore further argued that using firm-level information is a suitable

and feasible way to evaluate the effectiveness of fiscal response packages implemented during

the recent crisis which is difficult or even impossible using macro data. We have then shown

that controlling for time-varying industry-specific effects is critical to properly identify the

19

effects of the tax cuts. This is critical in times of the recent economic crisis where different

sectors and regions in Turkey were likely to be subject to a range of different shocks affecting

firm sales.

The second contribution is to shed more light on the long-standing debate about the

effectiveness of countercyclical fiscal policy and to provide evidence that the tax cuts in Turkey

appeared to have boosted firm sales. We recognize that the data we use have limitations which

we addressed to the extent possible in a number of robustness checks. The coefficients of

interest are remarkably stable. So far, the literature has predominantly been limited to

advanced economies, and it is questionable if those results apply to developing countries as

well. We worked with data from Turkey, an important emerging market economy, where the

recovery from the crisis was fairly quick. Our results indicate that the contribution of a specific

aspect of the fiscal response package played a role in this context.

However, from a policy perspective, the implications to be drawn are limited. Using micro data,

it is difficult to calculate the fiscal multiplier, although from the size of the coefficients, we

would expect the fiscal multiplier is likely to exceed one. From this perspective, temporary VAT

cuts seem to be a suitable measure to stabilize the economy, and our results shed novel type of

evidence on the long-standing debate between advocates and adversaries of Keynesian-style

fiscal policy. Yet, while according to our evidence temporary VAT cuts may attain the objective

of output stabilization, they may conflict with other objectives of policy makers in developing

countries including the protection of the most vulnerable groups in times of recession that by

definition consume less than other parts of the population. Other measures that simultaneously

protect the poor, such as targeted transfers, may be more suitable if this is an important

concern for policy makers. In addition, from a long-run growth perspective, increases of

productive spending financed by indirect taxes or income tax cuts financed by increases of

indirect taxes are growth-enhancing as shown by various papers. VAT and SCT cuts are

therefore not compatible with this.

7 References

Aghion, P., Hemous, D. and Kharroubi, E., 2009. Financial Constraints, Cyclical Macroeconomic Policy and Industry Growth. ZEW Lecture on December, 18., 2010

Aghion, P., Hemous, D. and Kharroubi, E., 2009. Credit constraints, cyclical fiscal policy and industry growth, NBER Working Paper No. 15119

20

Agarwal, S., Liu, C. and Souleles, N. 2007. The Reaction of Consumer Spending and Debt to Tax Rebates—Evidence from Consumer Credit Data. Journal of Political Economy, 115(6), pp. 986-1019.

Auerbach, A. J. and William G. Gale, 2009. Activist Fiscal Policy to Stabilize Economic Activity. Unpublished Conference Paper,

Auerbach, A. J., William G. Gale, and Benjamin H. Harris. 2010. Activist Fiscal

Barrell, R. and Weale, M., 2009. The Economics of a Reduction in VAT. Fiscal Studies, 30(1), pp.17-30.

Blundell, R., 2009. Assessing the Temporary VAT Cut Policy in the UK. Fiscal Studies, 30(1), pp.31-38.

Broda, C. & Parker, J., 2008. The Impact of the 2008 Tax Rebates on Consumer Spending: Preliminary Evidence 1. Unpublished Paper.

Chari, A., 2011. Identifying the aggregate productivity effects of entry and size restrictions: An empirical analysis of license reform in India. American Economic Journal: Economic, 3(May), pp.66-96.

Crossley, T. F., Low, H. & Wakefield, M., 2009. The Economics of a Temporary VAT Cut. Fiscal Studies, 30(1), pp.3-16.

El-Ganainy, A., 2006. Essays on Value-Added Taxation. Economic Dissertation at GSU

Heady, C., 2011. Tax Policy to Aid Recovery And Growth. Article on VOX

Hori, M., and Shimizutani, S., 2007. Are Tax Cuts Effective Even in Anticipation of a Future Tax Increase? Evidence from Japan`s Unique Episodes in the 1990s. The Singapore Economic Review, 52 (2), pp. 167-177.

Hebous, S., 2011. The effects of discretionary fiscal policy on macroeconomic aggregates: A reappraisal. Journal of Economic Surveys, 25 (4), 674 - 707.

Kneller, R. and Misch, F., 2011. What Does Ex-post Evidence Tell us About the Output Effects of Future Tax Reforms? ZEW Discussion Paper No. 11-029.

Jappelli, T., and Pistaferri, L., 2010. The Consumption Response to Income Changes. Working Paper 15739, NBER

Johnson, D.S., Parker, J. a & Souleles, N.S., 2006. Household Expenditure and the Income Tax Rebates of 2001. American Economic Review, 96(5), pp.1589-1610.

21

Rajan, R. G., and Zingales, L., 1998. Financial Dependence and Growth. The American Economic Review, 88 (3), pp. 559-586.

Shapiro, M.D. and Slemrod, J., 1995. Consumer response to the timing of income: Evidence from a change in tax withholding. Change, 85(1), pp.274-283.

Shapiro, M.D. and Slemrod, J., 2003. Consumer Response to Tax Rebates. American Economic Review, 93(1), pp.381-396.

Shapiro, M.D. and Slemrod, J., 2009. Did the 2008 Tax Rebates Stimulate Spending? American Economic Review, 99(2), pp.374-379.

Souleles, N., 2002. Consumer response to the Reagan tax cuts. Journal of Public Economics, 85(1), pp.99-120.

SPO (State Planning Organization of Turkey), 2009, Pre-Accession Economic Programme.

Uygur, E., 2010, The Global Crisis and the Turkish Economy, TWN Global Economy Series Working Paper, No. 2010/3.

Watanabe, K., Watanabe, Takayuki & Watanabe, Tsutomu, 2001. Tax policy and consumer spending: evidence from Japanese fiscal experiments. Journal of International Economics, 53(2), pp.261-281.