State of the U.S. Multifamily Market

Q3 2016 Review and Forecast

Agenda

Macro Overview

Apartment Market Fundamentals

Apartment Rent Trends

Capital Markets

Macro Overview

Real GDP Growth (SAAR)

Sources: BEA; CoStar Portfolio Strategy As of 16Q4

2.9%

(6%)

(4%)

(2%)

0%

2%

4%

6%

11 12 13 14 15 16

GDP Growth

GDP Growth by Sector

Sources: BEA; CoStar Portfolio Strategy As of 16Q4

(6%)

(4%)

(2%)

0%

2%

4%

6%

11 12 13 14 15 16

Contribution to GDP Growth

GDP Growth by Sector: Net Exports

Sources: BEA; CoStar Portfolio Strategy As of 16Q4

(6%)

(4%)

(2%)

0%

2%

4%

6%

11 12 13 14 15 16

Contribution to GDP Growth

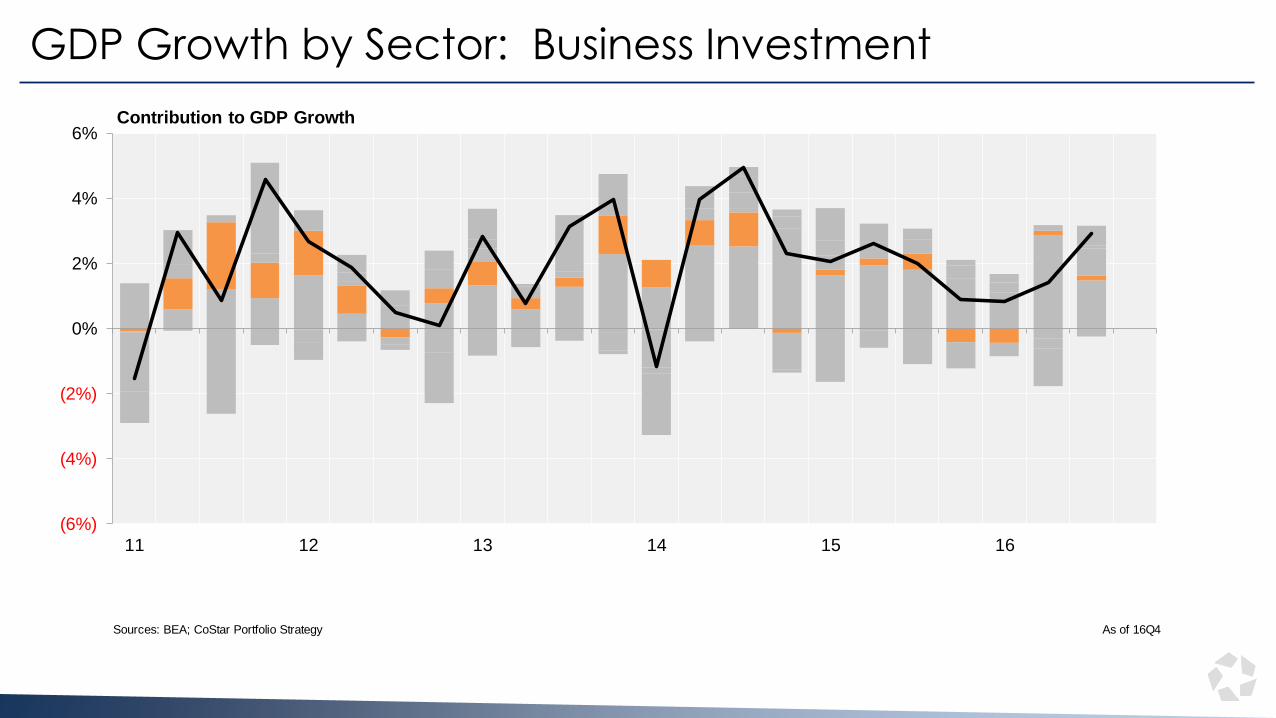

GDP Growth by Sector: Business Investment

Sources: BEA; CoStar Portfolio Strategy As of 16Q4

(6%)

(4%)

(2%)

0%

2%

4%

6%

11 12 13 14 15 16

Contribution to GDP Growth

GDP Growth by Sector: Government

Sources: BEA; CoStar Portfolio Strategy As of 16Q4

(6%)

(4%)

(2%)

0%

2%

4%

6%

11 12 13 14 15 16

Contribution to GDP Growth

GDP Growth by Sector: Residential Investment

Sources: BEA; CoStar Portfolio Strategy As of 16Q4

(6%)

(4%)

(2%)

0%

2%

4%

6%

11 12 13 14 15 16

Contribution to GDP Growth

Too Much Supply? Or Not Enough…

31-Mar-65

30-Jun-65

30-Sep-65

31-Dec-65

31-Mar-66

30-Jun-66

30-Sep-66

31-Dec-66

31-Mar-67

30-Jun-67

30-Sep-67

31-Dec-67

31-Mar-68

30-Jun-68

30-Sep-68

31-Dec-68

31-Mar-69

30-Jun-69

30-Sep-69

31-Dec-69

31-Mar-70

30-Jun-70

30-Sep-70

31-Dec-70

31-Mar-71

30-Jun-71

30-Sep-71

Source: Census Bureau; CoStar. Current totals are annualized based on prior years. As of November 2016

0

500

1,000

1,500

2,000

2,500

1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Multifamily Single Family

Multifamily Average: 399,000 new units per year

Total New Housing Construction (000s of Housing Units)

Average: 1,419,000 new units per year

Too Much Supply? Or Not Enough…

31-Mar-65

30-Jun-65

30-Sep-65

31-Dec-65

31-Mar-66

30-Jun-66

30-Sep-66

31-Dec-66

31-Mar-67

30-Jun-67

30-Sep-67

31-Dec-67

31-Mar-68

30-Jun-68

30-Sep-68

31-Dec-68

31-Mar-69

30-Jun-69

30-Sep-69

31-Dec-69

31-Mar-70

30-Jun-70

30-Sep-70

31-Dec-70

31-Mar-71

30-Jun-71

30-Sep-71

Source: Census Bureau; CoStar. Current totals are annualized based on prior years. As of November 2016

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Multifamily Single Family Change in Households

Total New Housing Construction (000s of Housing Units) and Change in Households

Too Much Supply? Or Not Enough…

31-Mar-65

30-Jun-65

30-Sep-65

31-Dec-65

31-Mar-66

30-Jun-66

30-Sep-66

31-Dec-66

31-Mar-67

30-Jun-67

30-Sep-67

31-Dec-67

31-Mar-68

30-Jun-68

30-Sep-68

31-Dec-68

31-Mar-69

30-Jun-69

30-Sep-69

31-Dec-69

31-Mar-70

30-Jun-70

30-Sep-70

31-Dec-70

31-Mar-71

30-Jun-71

30-Sep-71

Source: Census Bureau; CoStar. As of November 2016

(4,000)

(3,000)

(2,000)

(1,000)

0

1,000

2,000

3,000

4,000

1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Trailing 5-Year Housing Construction less Household Formation

Too much housing relative to household formation over previous 5 years

Not enough housing relative to household formation over previous 5 years

Homeownership Ticked Up In The Third Quarter

60

60

60

60

61

61

61

61

62

62

62

62

63

63

63

63

64

64

64

64

65

65

65

65

66

66

Sources: Moody's Analytics; U.S. Census Bureau (CPS/HVS); CoStar Portfolio Strategy As of 16Q3

30

32

34

36

38

40

42

44

46

60%

61%

62%

63%

64%

65%

66%

67%

68%

69%

70%

94 96 98 00 02 04 06 08 10 12 14 16

Renter Households U.S. HO Rate

Homeownership Rate Renter Occupied Households (Millions)

H.O. Rate in 2004 Peak : 69.2%2016 Q3 H.O. Rate : 63.5%

Increase in Renter HH's : 10.3MIncrease due to HH Formation: 3.5M

Increase due to Change in H.O. Rate: 6.8M

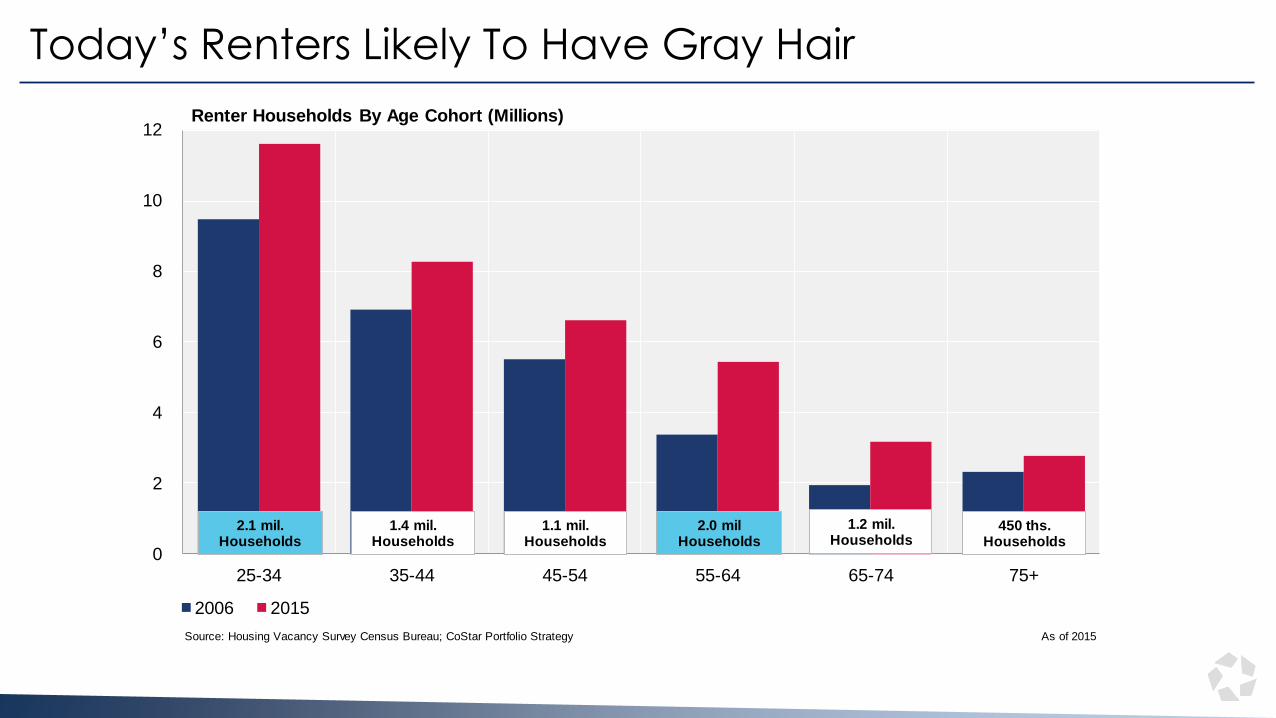

Today’s Renters Likely To Have Gray Hair

25-34

35-44

45-54

55-64

65-74

75+

Source: Housing Vacancy Survey Census Bureau; CoStar Portfolio Strategy As of 2015

0

2

4

6

8

10

12

25-34 35-44 45-54 55-64 65-74 75+

2006 2015

1.2 mil.Households

Renter Households By Age Cohort (Millions)

2.1 mil.Households

1.4 mil.Households

1.1 mil.Households

2.0 milHouseholds

450 ths.Households

Potential Upside Demand For Institutional Landlords?

Renter-occupied housing units:

41423632

114271804

Renter HouseholdsSingle Family or Non-CRE

2185843055.1%

Sources: U.S. Census ACS Survey; CoStar Portfolio Strategy As of 2015

55.1%

44.9%

20%

30%

40%

50%

60%

70%

0

5

10

15

20

25

Single Family or Non-CRE 5+ Units

Renter Occupied Households (Millions) % Of Renter Occupied

# Of Renter Households By Unit Type % Of All Renter Households By Unit Type

Petula Clark Was Right: “Downtown”….

CBD

Urban

Suburban

Sources: Neustar; CoStar Portfolio Strategy As of 16Q4

**Analysis limited to National Index (54 major metros)

CBDSecondary Core

Urban

Prime Suburban

Suburban

(1.0%)

(0.8%)

(0.6%)

(0.4%)

(0.2%)

0.0%

0.2%

0.4%

0.6%

4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15%

Change In Share Of Renter Households (2010-16Q4)

Percentage Growth Of Renter Households (2010-16Q4)

Bu

bb

leS

ize

De

no

tes

# O

f R

en

ter

Ho

us

eh

old

s In

1

6Q

4

The National Market Is Still Quite Healthy

90

90

90

90

91

91

91

91

92

92

92

92

93

93

93

93

94

94

94

94

95

95

95

95

96

96

96

96

Source: CoStar Portfolio Strategy As of 16Q3

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

0

10

20

30

40

50

60

70

80

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Demand Change (Q/Q) Supply Change (Q/Q) Vacancy Historical Avg Vacancy (2001-2016)

Demand & Supply (000s Units) Vacancy

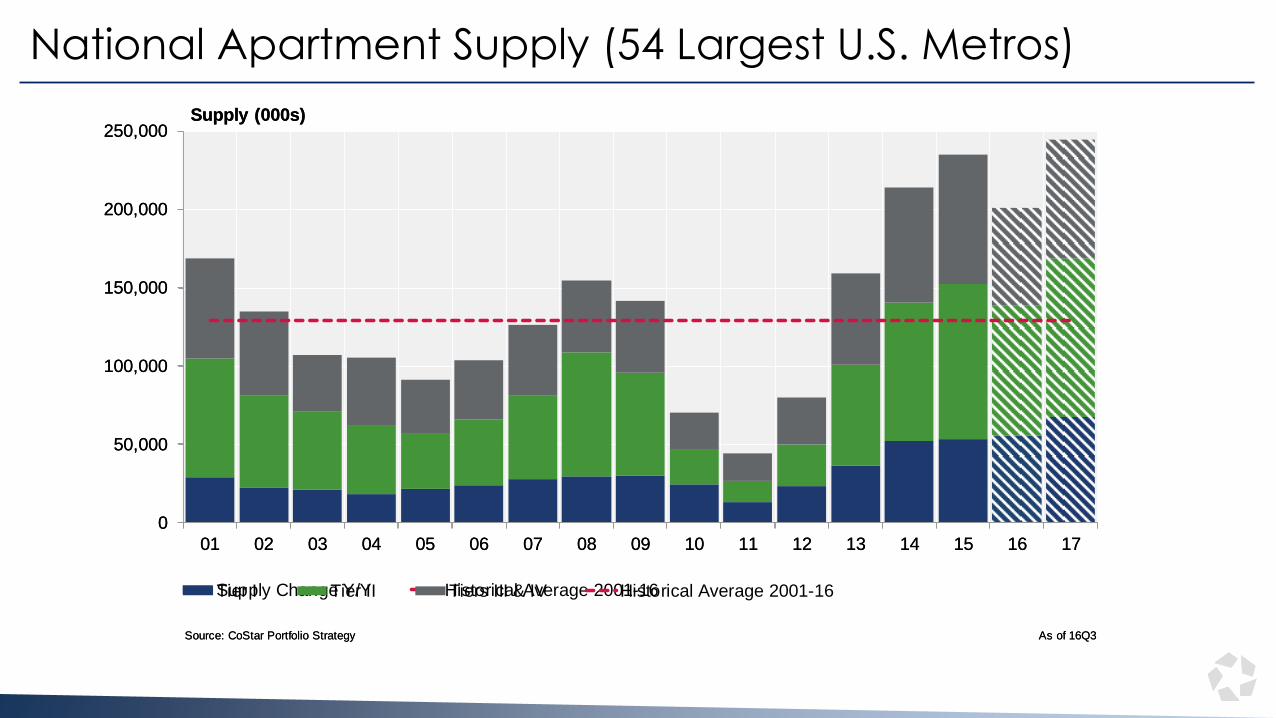

National Apartment Supply (54 Largest U.S. Metros)

00010203040506070809101112131415161718192021

Source: CoStar Portfolio Strategy As of 16Q3

0

50,000

100,000

150,000

200,000

250,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Supply Change Y/Y Historical Average 2001-16

Supply (000s)

00010203040506070809101112131415161718192021

Source: CoStar Portfolio Strategy As of 16Q3

0

50,000

100,000

150,000

200,000

250,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Tier I Tier II Tiers III & IV Historical Average 2001-16

Supply (000s)

Supply Growth Snapshot (16Q3-17Q4)

Rank1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 16Q3

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Ne

w Y

ork

Da

llas

Ho

usto

n

Los A

ngele

s

Washin

gto

n, D

C

Sea

ttle

Atlan

ta

De

nve

r

Bosto

n

Ch

icago

Austin

Ch

arlotte

Na

sh

vill

e

Mia

mi

San

An

tonio

Ora

ng

e C

ounty

Tam

pa

Pho

enix

Kan

sa

s C

ity

Port

land,

OR

San

Jo

se

Fort

Laud

erd

ale

San

Fra

ncis

co

Orlando

Co

lum

bus

Completions As A % Of InventorySouth East Midwest West

New Supply (As % of Inventory)New Supply (Units)

Does Los Angeles Need More Supply?

1

2

3

4

5

6

7

8

9

10

xx

Source: CoStar Portfolio Strategy As of 16Q3

0%

2%

4%

6%

8%

10%

12%

2012 2013 2014 2015 2016 2017

Cumulative Supply Growth

Memphis

Sacramento

National Index

Inland EmpireLos Angeles

Las Vegas

Detroit

East BayCleveland

Lease Up Takes Time

3/31/20006/30/20009/30/2000

12/31/20003/31/20016/30/20019/30/2001

12/31/20013/31/20026/30/20029/30/2002

12/31/20023/31/20036/30/20039/30/2003

12/31/20033/31/20046/30/20049/30/2004

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/2006

Source: CoStar Portfolio Strategy As of 16Q3

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

08 09 10 11 12 13 14 15 16

Overall Vacancy 4 & 5 Star 3 Star 1 & 2 Star

Vacancy

Market Scorecard: Year-Over-Year Vacancy Change

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

Source: CoStar Portfolio Strategy As of 16Q3

*Historical Average Since 2001

(150)

(100)

(50)

0

50

100

150

200

Salt L

ake C

ity

San

An

tonio

Ha

rtfo

rdS

an

Die

go

Long I

sla

nd

Min

nea

polis

Orlando

Sea

ttle

Bosto

nIn

dia

na

polis

San

Jose

De

nve

rD

alla

s -

FW

No

rthern

NJ

Sacra

mento

Ho

nolu

luR

ichm

ond

Austin

Tam

pa

Co

lum

bus O

HK

an

sa

s C

ity

Pho

enix

De

troit

Ra

leig

hN

ew

York

Ne

w O

rlean

sC

leve

land

Mia

mi

Cin

cin

nati

Jacksonvill

eS

tam

ford

Las V

egas

Inla

nd E

mpire

Atlan

taW

ashin

gto

n, D

CE

ast

Bay

No

rfolk

Ora

ng

e C

ounty

Los A

ngele

sC

harlotte

Sain

t Louis

Milw

aukee

Phila

delp

hia

Mem

phis

Ch

icago

San

Fra

ncis

co

Na

shvill

eB

altim

ore

Pitts

burg

hP

ort

land O

RF

ort

Laud

erd

ale

Palm

Be

ach

Okla

hom

a C

ity

Ho

usto

n

Below Historical Avg. Above Historical Avg.

One Year Vacancy Change (BPS)

High Supply Growth* Submarkets Have More Coming

30

29

28

27

26

25

24

23

22

21

20

19

18

17

16

15

14

13

12

11

10

9

8

7

6

5

4

Source: CoStar Portfolio Strategy As of 16Q3

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000

NEWY - Jersey City Waterfront

DALL - Plano

AUST - South

KANS - Johnson County KS

HOUS - Cinco Ranch

DALL - East Dallas

RALE - Central Raleigh

NEWY - Midtown West

HOUS - Northwest Houston

DALL - Farmers Branch/Addison

HOUS - Briar Forest/West Memorial

LOSA - Downtown Los Angeles

SANA - Northwest Side

NASH - West End/CBD

ATLA - Downtown/Midtown

DALL - Uptown/Park Cities

DENV - Downtown/Cherry Creek

ATLA - Buckhead-Brookhaven

HOUS - Neartown/River Oaks

CHIC - Downtown Chicago

Units Delivered Units Under Construction

Units Delivered And Under Construction

*Units Delivered 14Q4-16Q3, Under Construction As of 16Q3

Largest Vacancy Changes By Submarket (Y/O/Y)

25

24

23

22

21

20

19

18

17

16

15

14

13

12

11

10

9

8

7

6

5

4

3

2

1

Source: CoStar Portfolio Strategy As of 16Q3

*Includes submarkets with at least 5,000 units.

3.1%

3.2%

3.3%

3.3%

3.4%

3.4%

3.4%

3.4%

3.6%

3.7%

4.0%

4.1%

4.2%

4.5%

5.2%

5.7%

6.5%

6.9%

10.1%

10.1%

0% 5% 10% 15%

BALT - Harford County

PITT - Central Pittsburgh

WASH - Reston-Herndon Corridor

HOUS - Pearland

BOST - Quincy/Milton/Randolph

SEAT - Lake Union

AUST - Southeast

HOUS - Westchase/Woodlake

NEWY - Staten Island

HOUS - Alief

PALM - Boca Raton

CHIC - Downtown Chicago

OKLA - Central Oklahoma City

BALT - North Baltimore City

HOUS - Greenspoint/IAH Airport

CHAR - Southpark/Myers Park

SANF - South Of Market

NASH - West End/CBD

PHIL - Art Museum

WASH - Southwest/Navy Yard

(3.3%)

(3.3%)

(3.4%)

(3.5%)

(3.5%)

(3.7%)

(3.7%)

(3.8%)

(4.0%)

(4.1%)

(4.2%)

(4.6%)

(4.6%)

(4.7%)

(4.8%)

(5.2%)

(6.5%)

(7.9%)

(8.0%)

(9.1%)

(15%) (10%) (5%) 0%

DALL - Allen/McKinney

MIAM - Coral Gables

DENV - Highlands/Lone Tree

COLU - Downtown

AUST - Downtown/University

WASH - Ashburn/Sterling

BOST- Harvard/Cambridge

WASH - Falls Church/Vienna

SEAT - Kirkland

BOST - Everett/Malden

ORLA - Osceola County

NEWO - St Tammany Parish

WASH - H Street/NoMa

ATLA - Buckhead-Brookhaven

DENV - DTC/Southeast Corridor

ATLA - Cherokee County

HOUS - Cinco Ranch

SAND - Downtown

OKLA - Moore

SANJ - North San Jose

Largest Vacancy Increase Largest Vacancy Decrease

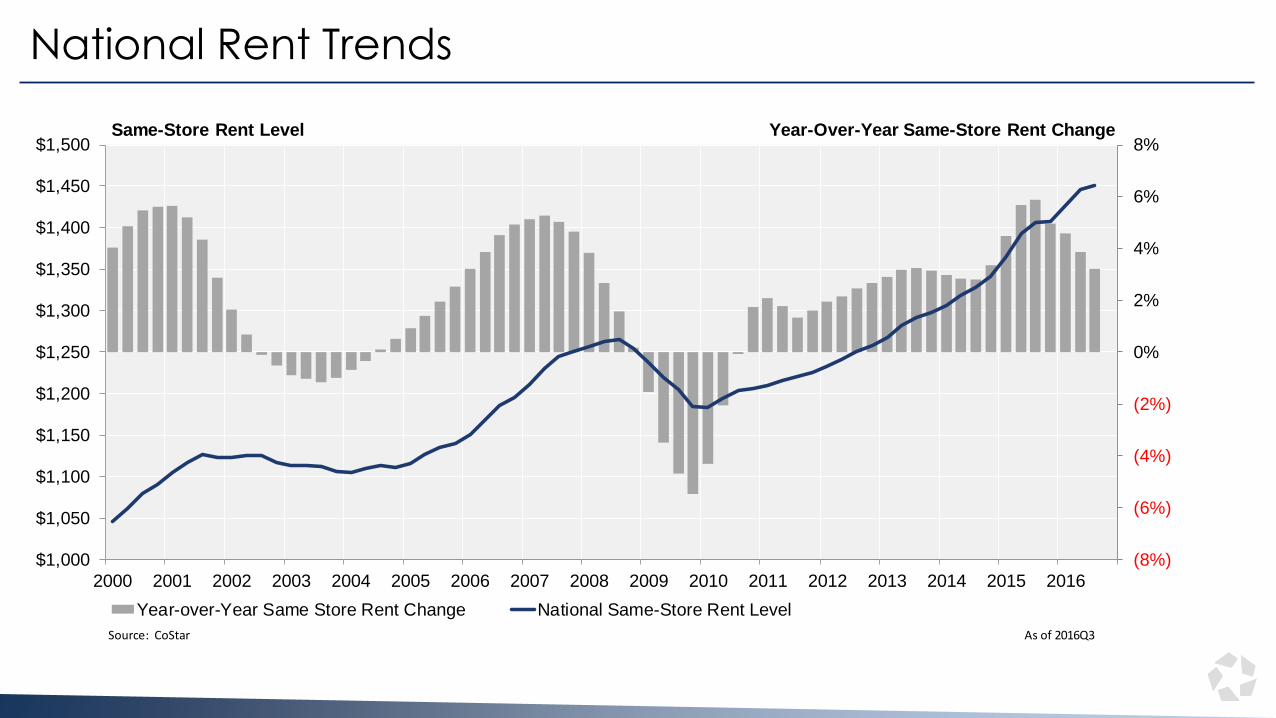

Rents

National Rent Trends

ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54ZPPR54

Source: CoStar As of 2016Q3

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

$1,000

$1,050

$1,100

$1,150

$1,200

$1,250

$1,300

$1,350

$1,400

$1,450

$1,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Year-over-Year Same Store Rent Change National Same-Store Rent Level

Same-Store Rent Level Year-Over-Year Same-Store Rent Change

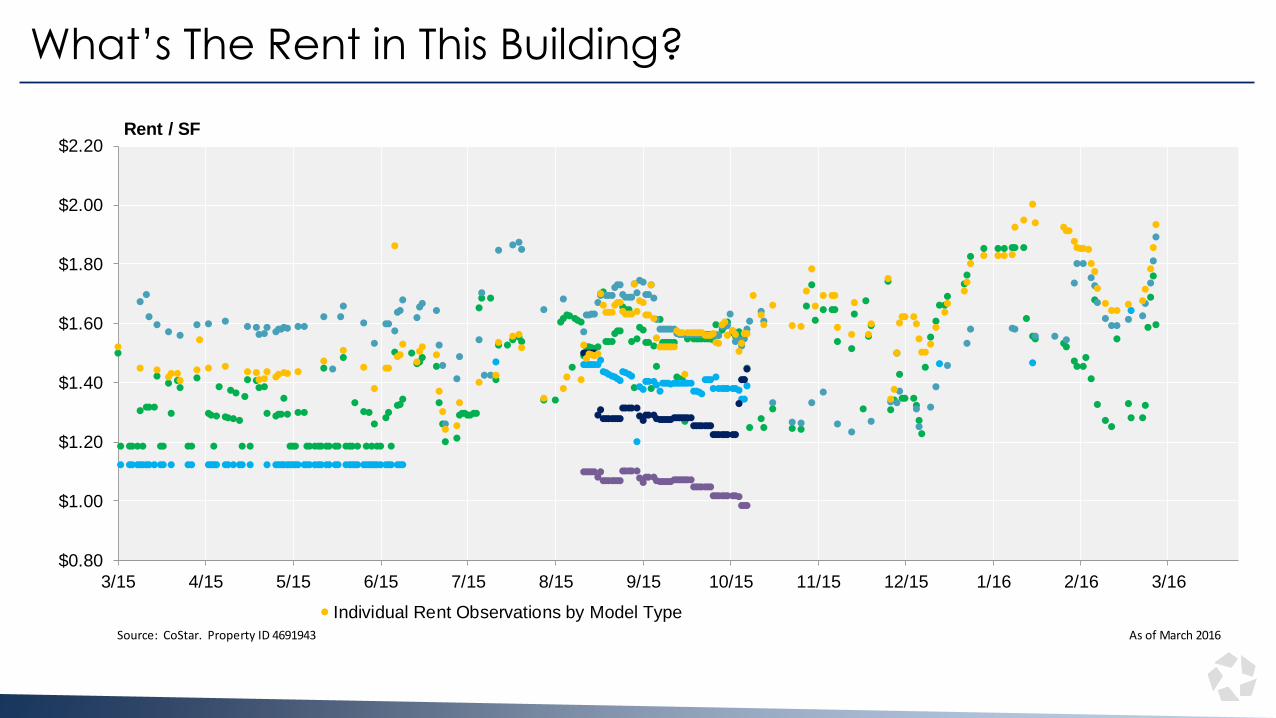

What’s The Rent in This Building?

1111111111111111111111111111111

Source: CoStar. Property ID 4691943 As of March 2016

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

3/15 4/15 5/15 6/15 7/15 8/15 9/15 10/15 11/15 12/15 1/16 2/16 3/16

Individual Rent Observations by Model Type

Rent / SF

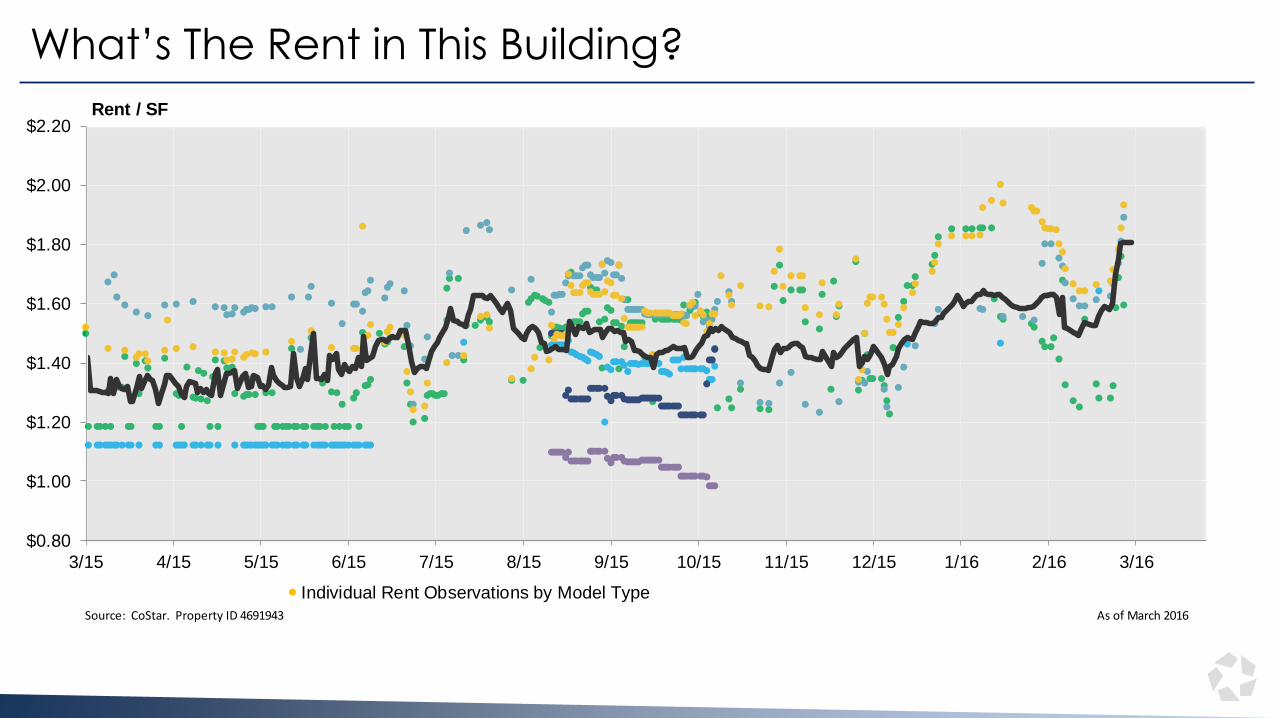

What’s The Rent In This Building?

1/1/20151/2/20151/3/20151/4/20151/5/20151/6/20151/7/20151/8/20151/9/2015

1/10/20151/11/20151/12/20151/13/20151/14/20151/15/20151/16/20151/17/20151/18/20151/19/20151/20/20151/21/20151/22/20151/23/20151/24/20151/25/20151/26/20151/27/20151/28/20151/29/20151/30/20151/31/2015

Source: CoStar. Property ID 4691943 As of March 2016

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

3/15 4/15 5/15 6/15 7/15 8/15 9/15 10/15 11/15 12/15 1/16 2/16 3/16

Individual Rent Observations by Model Type

Rent / SF

How To Make A Same-Store Rent Series

— Interpolate between data points

— Assume rents followed building—or market—trend before first datapoint and after last datapoint

— Estimate rents in models that don’t have ANY data

Estimating Rent Levels: CoStar Relative Rent Matrix

National

Source: CoStar As of 2015Q4

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.10

/1

1/1

1/2

2/1

2/2

2/3

3/1

3/2

3/3

4/2

4/3

National: 3 Star National: 4 & 5 Star

Relationship of Rents at Unit Type to Each Other

55 potential coefficients to estimate(1 bed 1 bath to 1 bed 2 bath, etc.)

Studio1 Bed1 Bath

1 Bed2+ Bath

2 Bed1 Bath

2 Bed2 Bath

2 Bed3+ Bath

3 Bed1 Bath

3 Bed2 Bath

3 Bed3+ Bath

4 Bed2 Bath

4 Bed3+ Bath

Possible Coefficients between all unit types

Model Another Number and Estimate Based on That

11 potential coefficients to estimate

Studio1 Bed1 Bath

1 Bed2+ Bath

2 Bed1 Bath

2 Bed2 Bath

2 Bed3+ Bath

3 Bed1 Bath

3 Bed2 Bath

3 Bed3+ Bath

4 Bed2 Bath

4 Bed3+ Bath

µ

Example: Estimating a Unit Type Which Has No Data

The unit types that we observe are used to predict µ, based on theirobserved coefficients

1 Bed1 Bath

1 Bed2+ Bath

2 Bed1 Bath

2 Bed2 Bath

2 Bed3+ Bath

µ

µ is used to predict the remaining unit type, based on its predicted coefficient, from the submarket-slice

Equations for µ, the Coefficients, and the Estimates

1111111111111111111111111111111

Source: CoStar. Property ID 4691943 As of March 2016

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

3/15 4/15 5/15 6/15 7/15 8/15 9/15 10/15 11/15 12/15 1/16 2/16 3/16

Individual Rent Observations by Model Type

Rent / SF 1111111111111111111111111111111

What’s The Rent in This Building?

Top 20 Rent Growth Markets

SACRSEATINLASALTDURHLASVATLAORANPHOENASHTAMPPORTDALLSANDLOSAORLARALELONGMEMPDETRCHARMINNCOLUCINCKANSINDIFORTJACKRICHEASTNORT

Source: CoStar As of November 2016

9.7%

7.5%7.0%

6.5% 6.3%5.9% 5.8% 5.7% 5.7% 5.5% 5.3% 5.2% 5.2% 5.1% 5.0%

4.7% 4.7% 4.4% 4.3% 4.1%

0%

2%

4%

6%

8%

10%

12%S

acra

mento

Sea

ttle

Inla

nd E

mpire

Salt L

ake C

ity

Du

rham

Las V

egas

Atlan

ta

Ora

ng

e C

ounty

Pho

enix

Na

shvill

e

Tam

pa

Port

land O

R

Da

llas -

Fort

Wort

h

San

Die

go

Los A

ngele

s

Orlando

Ra

leig

h

Long I

sla

nd

Mem

phis

De

troit

Year-Over-Year Same-Store Rent Change, 2015Q3 - 2016Q3

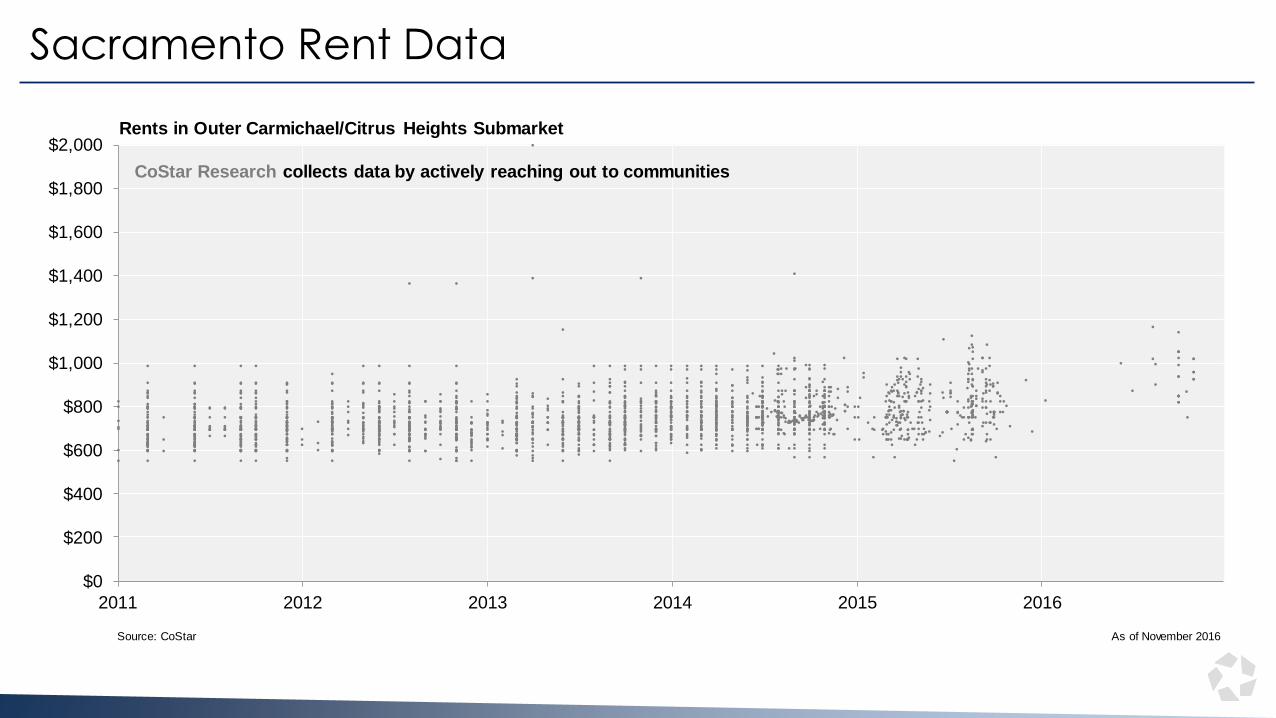

Sacramento Rent Data

AR Data

PropertyID

841302

1593865

4062347

4115560

7761475

4411690

7761475

7761475

4411690

4062003

7762534

4106521

4115560

4683162

7761475

7762534

5897524

5897524

4341184

850078

850078

7768831

7761670

7762467

742121

5881201

4494520

1593865

Source: CoStar As of November 2016

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2011 2012 2013 2014 2015 2016

Rents in Outer Carmichael/Citrus Heights Submarket

CoStar Research collects data by actively reaching out to communities

Sacramento Rent Data

AR Data

PropertyID

841302

1593865

4062347

4115560

7761475

4411690

7761475

7761475

4411690

4062003

7762534

4106521

4115560

4683162

7761475

7762534

5897524

5897524

4341184

850078

850078

7768831

7761670

7762467

742121

5881201

4494520

1593865

Source: CoStar As of November 2016

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2011 2012 2013 2014 2015 2016

Rents in Outer Carmichael/Citrus Heights Submarket

Community Callers collect rent information as potential renters

Sacramento Rent Data

AR Data

PropertyID

841302

1593865

4062347

4115560

7761475

4411690

7761475

7761475

4411690

4062003

7762534

4106521

4115560

4683162

7761475

7762534

5897524

5897524

4341184

850078

850078

7768831

7761670

7762467

742121

5881201

4494520

1593865

Source: CoStar As of November 2016

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2011 2012 2013 2014 2015 2016

Rents in Outer Carmichael/Citrus Heights Submarket

Automated Data Collection uses web scraping technology to collect high-frequency rent observations

Sacramento Rent Data

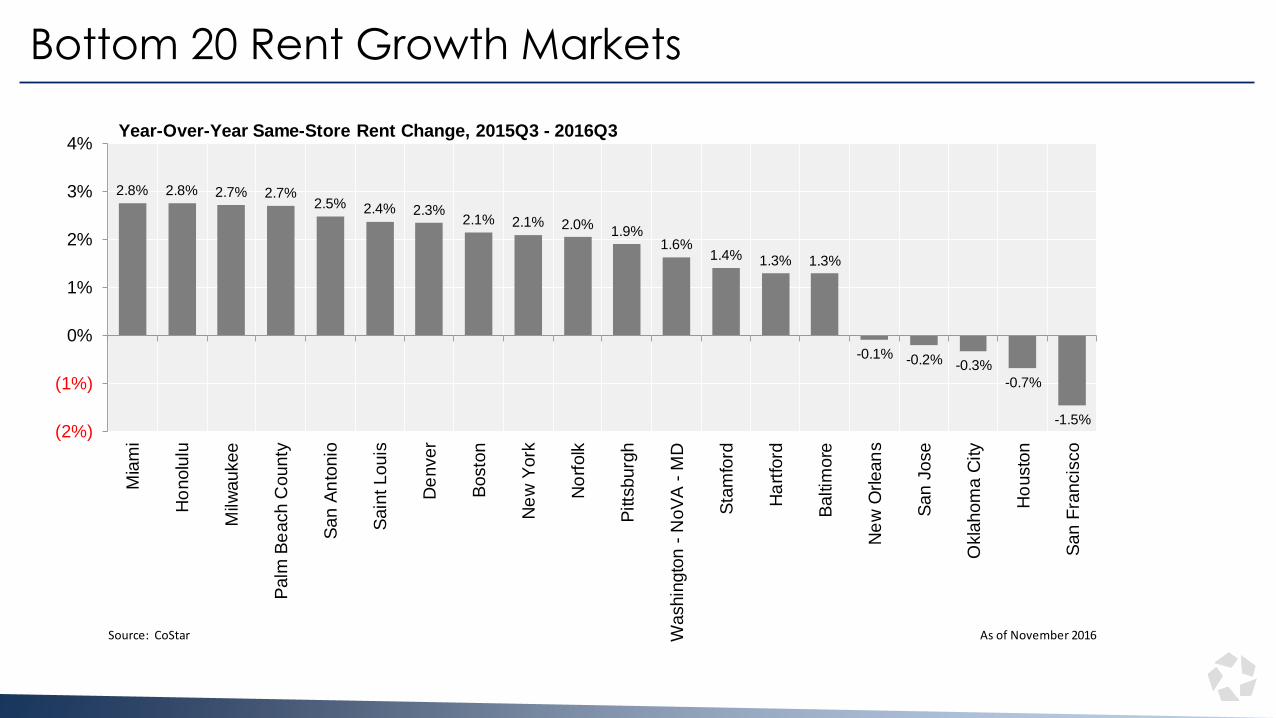

Bottom 20 Rent Growth Markets

MIAMHONOMILWPALMSANASTLODENVBOSTNEWYNORFPITTWASHSTAMHARTBALTNEWOSANJOKLAHOUSSANF

CHICCLEVAUSTPHILNORTEASTRICHJACKFORTINDI

Source: CoStar As of November 2016

2.8% 2.8% 2.7% 2.7%2.5% 2.4% 2.3%

2.1% 2.1% 2.0%1.9%

1.6%1.4% 1.3% 1.3%

-0.1% -0.2% -0.3%

-0.7%

-1.5%(2%)

(1%)

0%

1%

2%

3%

4%M

iam

i

Ho

nolu

lu

Milw

aukee

Palm

Be

ach C

ounty

San

An

tonio

Sain

t Louis

De

nver

Bosto

n

Ne

w Y

ork

No

rfolk

Pitts

burg

h

Washin

gto

n -

NoV

A -

MD

Sta

mfo

rd

Ha

rtfo

rd

Baltim

ore

Ne

w O

rlean

s

San

Jose

Okla

hom

a C

ity

Ho

usto

n

San

Fra

ncis

co

Year-Over-Year Same-Store Rent Change, 2015Q3 - 2016Q3

San Francisco Rent Data

Houston Rent Data

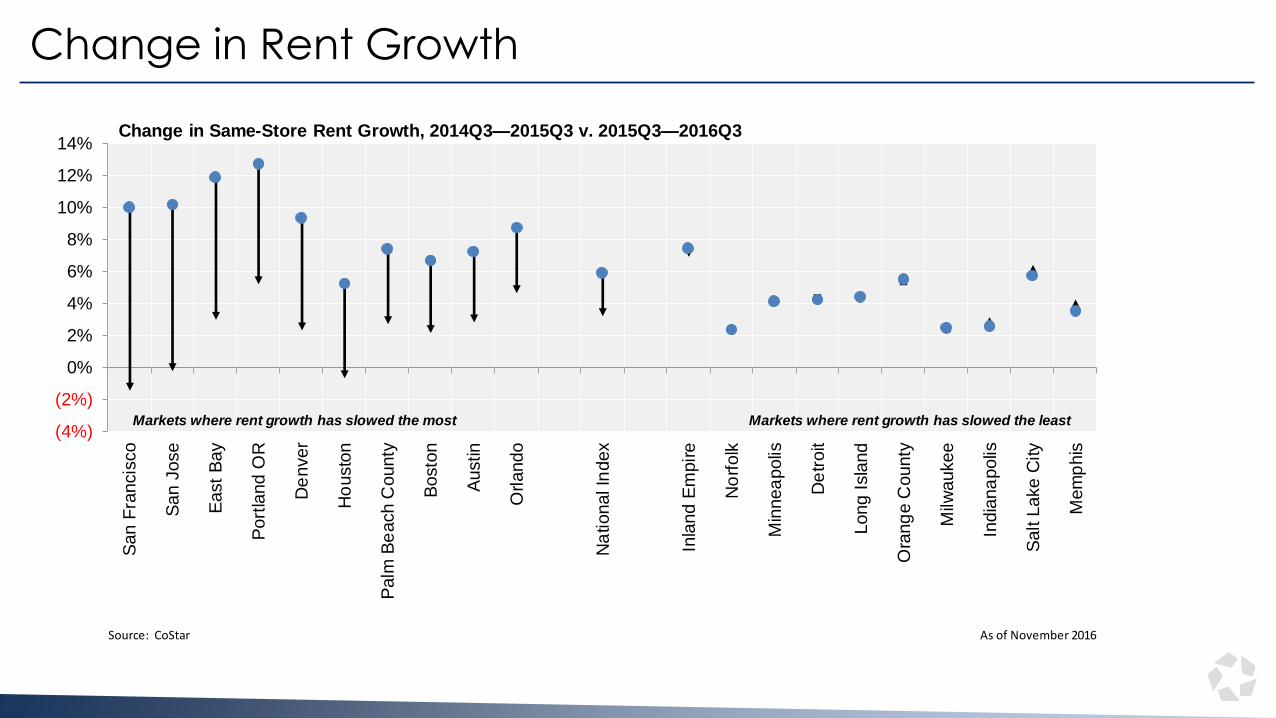

Change in Rent Growth

SANFSANJEASTPORTDENVHOUSPALMBOSTAUSTORLA

ZPPR54

INLANORFMINNDETRLONGORANMILWINDISALTMEMP

Source: CoStar As of November 2016

(4%)

(2%)

0%

2%

4%

6%

8%

10%

12%

14%S

an

Fra

ncis

co

San

Jose

East

Bay

Port

land O

R

De

nver

Ho

usto

n

Palm

Be

ach C

ounty

Bosto

n

Austin

Orlando

Na

tional In

dex

Inla

nd E

mpire

No

rfolk

Min

nea

polis

De

troit

Long I

sla

nd

Ora

ng

e C

ounty

Milw

aukee

India

na

polis

Salt L

ake C

ity

Mem

phis

Change in Same-Store Rent Growth, 2014Q3—2015Q3 v. 2015Q3—2016Q3

Markets where rent growth has slowed the most Markets where rent growth has slowed the least

Capital Markets

Sales Volume Last Four Quarters Remains Strong

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

previous

Y/Y Change

Source: CoStar Group As of 16Q3

(15%)

(10%)

(5%)

0%

5%

10%

15%

20%

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

Hospitality Industrial Office Multi-Family Retail

Sales Volume (Billions)

Sales Volume Y/Y Change

Y/Y Change In Sales Volume

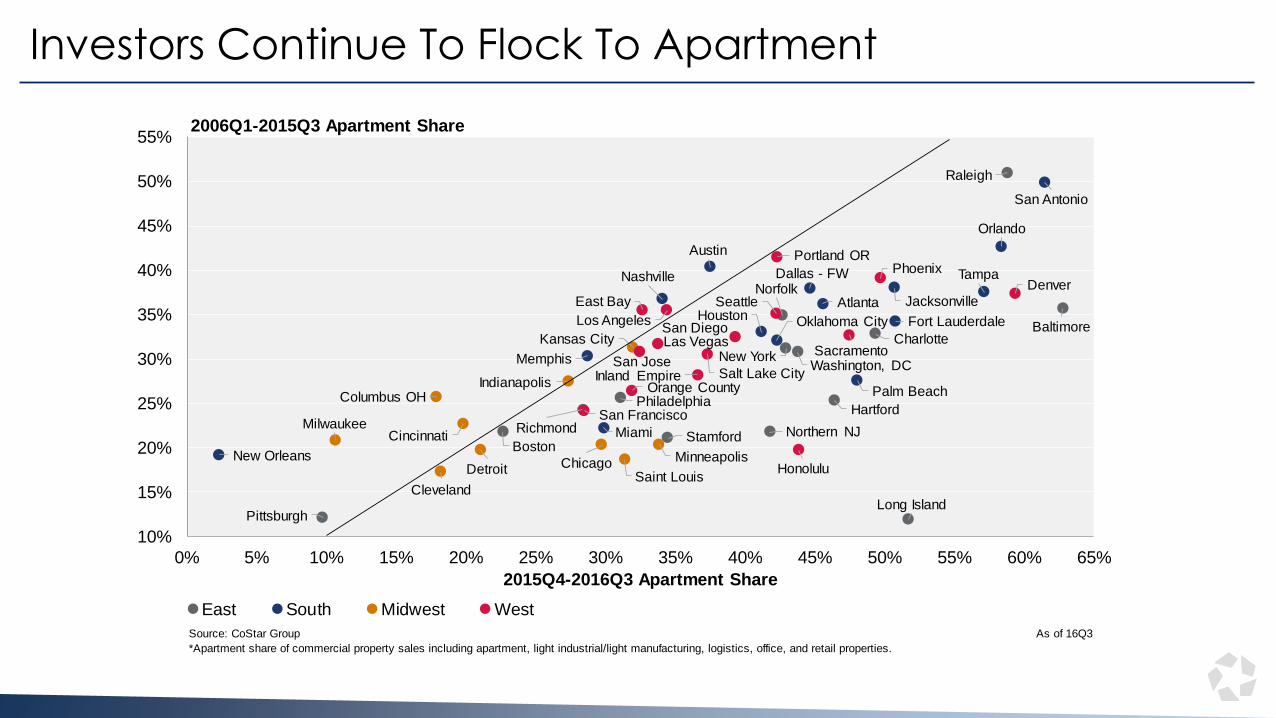

Investors Continue To Flock To Apartment

Atlanta

Austin

Baltimore

Boston

Charlotte

Chicago

Cincinnati

Cleveland

Columbus OH

Dallas - FW

Denver

Detroit

East Bay

Hartford

Honolulu

Houston

Indianapolis

Inland Empire

Jacksonville

Kansas City

Las Vegas

Long Island

Los Angeles

Memphis

Miami

Milwaukee

Minneapolis

Nashville

Source: CoStar Group As of 16Q3

*Apartment share of commercial property sales including apartment, light industrial/light manufacturing, logistics, office, and retail properties.

Baltimore

Boston

Charlotte

Hartford

Long Island

New York

Norfolk

Northern NJ

Philadelphia

Pittsburgh

Raleigh

RichmondStamford

Washington, DC

Atlanta

Austin

Dallas - FW

Fort LauderdaleHoustonJacksonville

Memphis

Miami

Nashville

New Orleans

Oklahoma City

Orlando

Palm Beach

San Antonio

Tampa

Chicago

Cincinnati

Cleveland

Columbus OH

Detroit

Indianapolis

Kansas City

Milwaukee

Minneapolis

Saint Louis

Denver

East Bay

Honolulu

Inland Empire

Las Vegas

Los Angeles

Orange County

PhoenixPortland OR

Sacramento

Salt Lake City

San Diego

San Francisco

San Jose

Seattle

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65%

East South Midwest West

2015Q4-2016Q3 Apartment Share

2006Q1-2015Q3 Apartment Share

Are Apartment Capital Markets Peaking?

67

66

65

64

63

62

61

60

59

58

57

56

55

54

53

52

51

50

49

48

47

46

45

44

43

42

41

40

Source: CoStar Group As of 16Q3

0

1

2

3

4

5

6

7

8

9

$0

$10

$20

$30

$40

$50

$60

05 06 07 08 09 10 11 12 13 14 15 16

Sales Volume (Billions)

Quarterly Sales Volume Number Of Buildings Sold

Number Of Buildings Sold (000s)

Sustained Price Growth Across All Regions

07

07

07

07

08

08

08

08

09

09

09

09

10

10

10

10

11

11

11

11

12

12

12

Source: CoStar Portfolio Strategy As of 16Q3

$0

$50,000

$100,000

$150,000

$200,000

$250,000

07 08 09 10 11 12 13 14 15 16

Price Per Unit (Four-Quarter Rolling Average)

East South Midwest West National Index

Recent Price Appreciation Strongest In West Coast Metros

Cleveland

Long Island

Miami

Palm Beach

Hartford

Denver

Honolulu

Las Vegas

Phoenix

San Jose

East Bay

Richmond

Jacksonville

Raleigh

Austin

Baltimore

San Diego

Charlotte

Portland OR

Columbus OH

Nashville

Northern NJ

Minneapolis

Source: CoStar Portfolio Strategy As of 16Q3

(40%)

(20%)

0%

20%

40%

60%

80%

Cle

vela

nd

Long I

sla

nd

Mia

mi

Palm

Be

ach

Ha

rtfo

rdD

enver

Ho

nolu

luLas V

egas

Pho

enix

San

Jose

East

Bay

Ric

hm

ond

Ora

ng

e C

ounty

Fort

Laud

erd

ale

Jacksonvill

eO

kla

hom

a C

ity

Ra

leig

hA

ustin

Baltim

ore

Washin

gto

n, D

CS

an

Die

go

Ch

arlotte

Port

land O

RC

olu

mbus O

HN

ashvill

eN

ort

hern

NJ

Min

nea

polis

Ne

w Y

ork

Inla

nd E

mpire

Ch

icago

Salt L

ake C

ity

Kan

sas C

ity

De

troit

Los A

ngele

sN

orf

olk

Atlan

taT

am

pa

Cin

cin

nati

India

na

polis

Sea

ttle

Sacra

mento

Da

llas -

FW

Orlando

Milw

aukee

Phila

delp

hia

Bosto

nH

ousto

nS

an

An

tonio

Mem

phis

Sta

mfo

rdS

an

Fra

ncis

co

Pitts

burg

hS

ain

t Louis

Ne

w O

rlean

s

Y/Y Price Growth

South East Midwest West

DecreaseIncrease

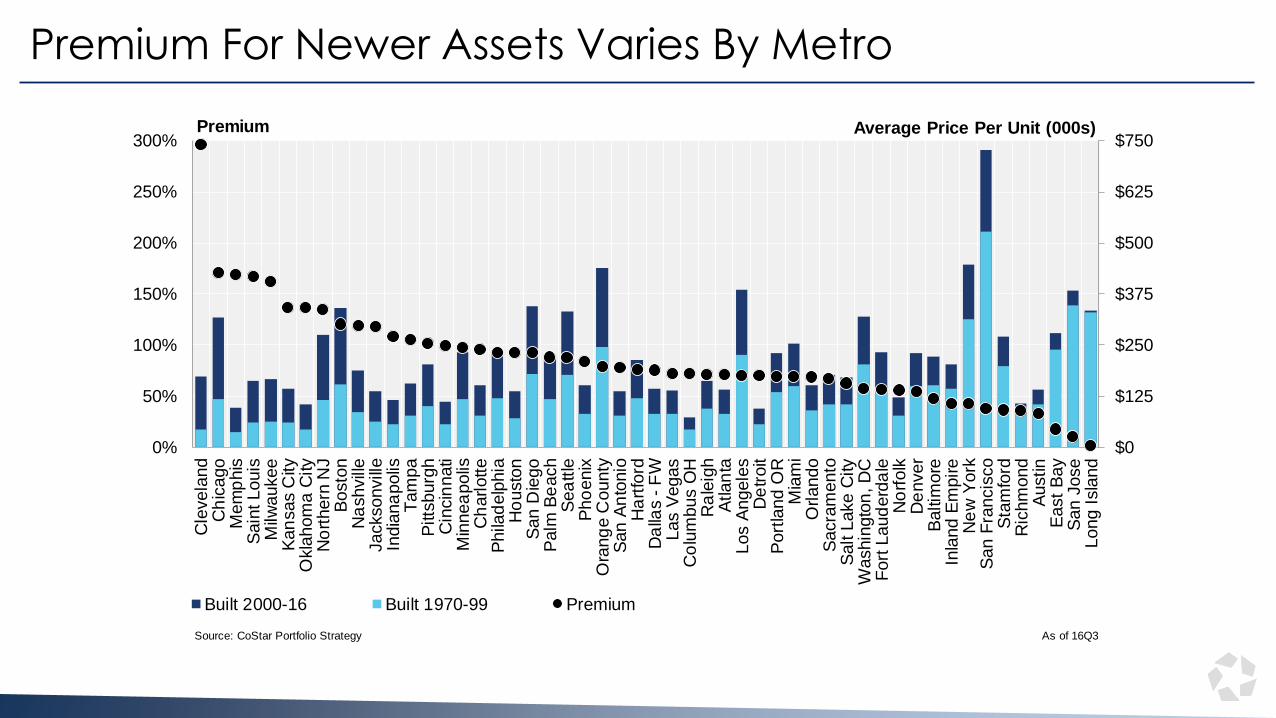

Premium For Newer Assets Varies By Metro

Cleveland

Chicago

Memphis

Saint Louis

Milwaukee

Kansas City

Northern NJ

Boston

Nashville

Jacksonville

Indianapolis

Tampa

Pittsburgh

Cincinnati

Minneapolis

Charlotte

Philadelphia

Houston

San Diego

Palm Beach

Seattle

Phoenix

San Antonio

Hartford

Dallas - FW

Source: CoStar Portfolio Strategy As of 16Q3

$0

$125

$250

$375

$500

$625

$750

0%

50%

100%

150%

200%

250%

300%

Cle

vela

nd

Ch

icago

Mem

phis

Sain

t Louis

Milw

aukee

Kan

sas C

ity

Okla

hom

a C

ity

No

rthern

NJ

Bosto

nN

ashvill

eJackso

nvill

eIn

dia

na

polis

Tam

pa

Pitts

burg

hC

incin

nati

Min

nea

polis

Ch

arlotte

Phila

delp

hia

Ho

usto

nS

an

Die

go

Palm

Be

ach

Sea

ttle

Pho

enix

Ora

ng

e C

ounty

San

An

tonio

Ha

rtfo

rdD

alla

s -

FW

Las V

egas

Co

lum

bus O

HR

ale

igh

Atlan

taLos A

ngele

sD

etr

oit

Port

land O

RM

iam

iO

rlando

Sacra

mento

Salt L

ake C

ity

Washin

gto

n, D

CF

ort

Laud

erd

ale

No

rfolk

De

nver

Baltim

ore

Inla

nd E

mpire

Ne

w Y

ork

San

Fra

ncis

co

Sta

mfo

rdR

ichm

ond

Austin

East

Bay

San

Jose

Long I

sla

nd

Premium

Built 2000-16 Built 1970-99 Premium

Average Price Per Unit (000s)

Select Top Multifamily Deals – 3Q 2016

Savoy Park

New York, NY

A joint venture comprised of L&M

Development Partners and Savanna sold

the 1,790-unit apartment community to

Fairstead Capital for $315 Million or

$176K/unit.

LIV Apartments

Bellevue, WA

Goodman Real Estate, Inc. sold the 451-

unit apartment community to Kennedy-

Wilson Properties, Ltd. for $172 Million or

$381K/unit.

Cap Rate: 4.7%

Axion Tustin

Tustin, CA

AvalonBay Communities, Inc. sold

the 628- unit community to Raintree

Partners for $163.55 Million or

$260K/unit.

Cap Rate: 4.94%

The Residence Buckhead Atlanta

Atlanta, GA

Oliver McMillan sold the 370-unit

community to Simpson Housing for

$136.5 Million or $369K/unit.

Pro-Forma Cap Rate: 5.6%

Century Summerfield @ Morgan Metro

Landover, MD

Camden Property Trust sold the 478-unit

community to Centennial Holding

Company, LLC for $110 Million or

$230K/unit.

Cap Rate: 6%

One East Delaware

Chicago, IL

Waterton Associates, LLC sold the 306-

unit community to a joint venture

comprised of Golub & Company and

Alcion Ventures for $146 Million or

$477K/unit.

Cap Rate: 4.75%

© Copyright 2016 CoStar Group, Inc. All Rights Reserved. Although CoStar makes efforts to ensure the accuracy and reliability of the information contained herein, the following information includes projections that are based on various assumptions by CoStar concerning future events and circumstances, as well as historical and current data maintained in CoStar’s database. Actual results may vary from the projections presented. The information in this presentation is provided ‘as is’ and CoStar expressly disclaims any guarantees, representations or warranties of any kind, including those of merchantability and fitness for a particular purpose. Features shown in this presentation may require additional subscriptions.